Sample Category Title

AUD/USD and NZD/USD Signal More Losses

AUD/USD declined below the 0.6575 and 0.6550 support levels. NZD/USD is also moving lower and might trade below the 0.6000 zone.

Important Takeaways for AUD/USD and NZD/USD Analysis Today

- The Aussie Dollar started a fresh decline from well above the 0.6600 level against the US Dollar.

- There was a break below a connecting bullish trend line with support at 0.6570 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD declined steadily from the 0.6105 resistance zone.

- There was a break below a key bullish trend line with support at 0.6040 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair struggled to clear the 0.6635 zone. The Aussie Dollar started a fresh decline below the 0.6600 support against the US Dollar.

The pair even settled below 0.6575 and the 50-hour simple moving average. There was a clear move below the 50% Fib retracement level of the upward move from the 0.6504 swing low to the 0.6634 high. Moreover, there was a break below a connecting bullish trend line with support at 0.6570.

The pair is now trading below the 76.4% Fib retracement level of the upward move from the 0.6504 swing low to the 0.6634 high. On the downside, initial support is near the 0.6520 zone.

The next support sits at 0.6505. If there is a downside break below 0.6505, the pair could extend its decline. The next support could be 0.6455. Any more losses might send the pair toward the 0.6420 support.

On the upside, an immediate resistance is near the 0.6550 level. The next major resistance is near 0.6575, above which the price could rise toward 0.6635. Any more gains might send the pair toward 0.6700.

A close above the 0.6700 level could start another steady increase in the near term. The next major resistance on the AUD/USD chart could be 0.6780.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair also followed a similar pattern and declined from the 0.6105 zone. The New Zealand Dollar gained bearish momentum and traded below 0.6055 against the US Dollar.

The pair dived below the 61.8% Fib retracement level of the upward move from the 0.6024 swing low to the 0.6106 high. Besides, there was a break below a key bullish trend line with support at 0.6040. The pair settled below the 0.6025 level and the 50-hour simple moving average.

On the downside, immediate support on the NZD/USD chart is near the 0.6005 level. It is close to the 1.236 Fib extension level of the upward move from the 0.6024 swing low to the 0.6106 high.

The next major support is near the 0.5980 zone. If there is a downside break below 0.5980, the pair could extend its decline toward the 0.5950 level. The next key support is near 0.5920.

Immediate resistance on the upside is near 0.6025. The next resistance is at 0.6055 and the 50-hour simple moving average. If there is a move above 0.6055, the pair could rise toward 0.6090. Any more gains might open the doors for a move toward the 0.6150 resistance zone in the coming days.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Sudden Weakening of Chinese Yuan Stands Out in Asian Dealings

Markets

German Bunds outperformed US Treasuries yesterday. The front end lost up to 5 bps with longer maturities easing between 1.1 and 2.7 bps. Aside from catching up with post-Fed US markets, it also followed yesterday’s PMI readings. While slightly better on the account of services (51.1), easing price pressures (be it from elevated levels) in the sector combined with the ongoing manufacturing slump sets up the stage for a June ECB rate cut. US yields recovered from initial follow-up losses on solid and/or stronger-than-expected economic data. These included weekly jobless claims, the Philly Fed business outlook, US PMIs and existing home sales. Net daily changes ranged between -1.8 bps (30-y) and +3.4 bps (2-y). EUR/USD two-staged drop was inspired by euro weakness followed by dollar strength. The pair retreated from 1.094 to pre-Fed levels of 1.086. Sterling was hit by a shift in the voting behavior of members Mann and Haskel at yesterday’s Bank of England meeting. They dropped their longstanding calls for additional hikes. The internal debate is now squarely focused at the timing of a first cut. Markets frontloaded bets to June (80%) from August. EUR/GBP rose from an intraday low around 0.853 to 0.858.

The sudden weakening of the Chinese yuan stands out in Asian dealings this morning. USD/CNY 7.20 has been a red line since mid-January as Chinese authorities seek to balance easy monetary policy without triggering a capital flight. They defended this threshold through daily fixings and state banks being ordered to sell dollars when needed. They appear to have softened their stance today by lowering the daily reference rate by the most since early February. USD/CNY shot up to 7.226 in a first response, the highest since mid-November. And the pair staying there suggests state banks are sidelined. Japanese February inflation numbers came in close to expectations. The BoJ’s favourite gauge quickened from 2% to 2.8%. The Japanese yen trades with minor gains. Earlier JPY losses, though, pushed USD/JPY to the brink of a new multi-decade high, which stands at 151.95 (2022).

Except for some central bank speeches from ECB’s Nagel & Lane as well as Fed chair Powell (opening remarks at the Fed listens Event), the eco calendar is not very enticing. We may see some of the typical core bond gains ahead of the weekend, even if current circumstances offer an ideal opportunity for markets to reflect on the discrepancy between Powell’s words on Friday and the Fed’s dot plot. Dollar trading is likely going to be a derivative of equity markets. Current Asian/Chinese weakness gives the dollar an edge. EUR/USD drops to the lowest level since early March 1.0833). Support is located at 1.0793 (50% retracement on the Q4 2023 rally). UK retail sales were better than expected for February and an already strong January was revised upward a bit. EUR/GBP holds steady near yesterday’s closing levels in a first reaction.

News & Views

The Mexican central bank cut its policy rate for the first time since 2021 in a 4-1 split vote, from 11.25% to 11%. Forward guidance was unaltered, stressing data dependence and that monetary policy will remain tight over the 2-yr forecast horizon. In updated forecasts, headline inflation is still foreseen to converge to the target in Q2 2025. Upward risks remain dominant, including persistence of core inflation, FX depreciation, greater cost-related pressures, a greater-than-expected resilience of the economy and climate-related and geopolitical risks. The Mexican peso holds near strongest levels since end 2015 against the dollar at USD/MXN 16.75.

The Turkish central bank (CBRT) yesterday unexpectedly extended its tightening cycle after pausing in February. They did so in fashion, raising the policy rate by 500 bps to 50%. The CBRT also doubled its interest rate corridor from +- 150 bps to +- 300 bps, creating room to maneuver to tighten policy even more via liquidity rules. More rate hikes might be coming if necessary. A deterioration in the inflation outlook, led by sticky services inflation, warrants the rate hike. Apart from bringing down inflation, the CBRT also pursuits a real appreciation in the lira. The Turkish currency hit a new all-time low in the run-up to the meeting (EUR/TRY 35.60), before dipping to 34.85 in the aftermath.

A Week Full of Surprises

The second big surprise of the week came from the Swiss National Bank (SNB). The Swiss cut the interest rate by 25bp to 1.5% yesterday, in a surprise move and became the first major central bank to cut rates. The Swiss 10-year yield fell to 65bp and franc lost against the dollar and the euro. The USDCHF broke above the 2022 to 2024 downtrending channel and the EURCHF spiked above a minor Fibonacci retracement, though it remains well above the prepandemic levels both against the greenback and the single currency. The SNB is expected to lower rates two more times this year and the latter should lead to a gradual depreciation of the Swiss franc, help exporters to see the light at the end of the tunnel and support the stock valuations. UBS observes that a 1% deprecation in the franc leads to around 0.9% rise in the Swiss stocks. The SMI jumped 0.73% yesterday.

Now, if the Swiss could kick off the pivot party, it is because inflation in Switzerland has been easier to fight for the SNB thanks to the traditionally strong franc. The Swiss inflation fell to 1.2% in February. But the fact the Swiss jumped into the water raised the expectation that the others will join ‘soon’.

How soon? If all goes well and inflation remains under control, the Fed and the ECB are also expected to cut in June. In the UK, two Bank of England (BoE) hawks dropped their rate hike vote. As such, no one voted to hike the rates in Britain yesterday, 8 MPC members voted to stay pat and 1 voted to cut. Votes in favour of cut are yet to rise, but the BoE also gives signs of turning its back to policy tightening.

Cable slipped below the 50-DMA and is testing the 100-DMA to the downside this morning, the Japanese yen remained offered despite latest data showing that inflation in Japan rose to a 3-month peak, and the EURUSD sank to the 200-DMA. The selloff was amplified by a surprisingly strong set of economic data released in the US yesterday that got some Fed doves to scratch their heads about the Fed’s determination to cut rates ‘sometime this year’ and boosted the dollar appetite.

Confusion reigns. The Fed – whose underlying economy doesn’t necessarily need a rate cut sounds dovish and the ECB – whose underlying economies need a rate cut – remains relatively hawkish. The data tells one story, the policymakers tell another and the prices move unpredictably.

But not in the stock markets. There, everything is fine. The European stocks traded at a fresh ATM, the S&P500 extended gains to a fresh record as well, this time because the strong data, combined to dovish Fed, fueled optimism about soft landing. Nasdaq 100 also renewed record as Micron Technology jumped 14% yesterday beating Q2 expectations on strong AI demand. Nike gained timidly after beating expectations on surprise China strength and FedEx also rose on earnings beat and $5 billion buyback program. Apple however tanked 4% as regulators on both side of the Atlantic Ocean went after the tech giant and its monopolistic behaviour. The company looks like it’s carrying the misery of the world on its shoulders these days. It missed the AI rally, it’s sued by regulators around the world and China is not playing along. Price-wise, there is now a death cross formation on the daily chart, where the 50-DMA crossed below the 200-DMA, a technical formation that encourages some traders to position short on the stock.

Elsewhere, Reddit made a strong debut on the NYSE, the shares opened 38% higher, rose as much as 60% and settled at +48% at the end of the first day of trading. As I was saying yesterday, the weather conditions for excellent for a first fly, but trading Reddit is suitable for those who love meme stocks.

Last but not least, Bitcoin managed to hold ground near the $60K this week, gold retreated after hitting a fresh ATH posterior to the Fed decision, while US crude failed to extend gains above the $83.70 and is back below the $81pb this morning on weaker US gasoline demand and hope of a ceasefire in Gaza, although the Israeli government said that they will ultimately invade Rafah no matter what the US says. I believe that we will see decent buying into and below the $80pb level both on the back of geopolitical tensions and the dovish central bank expectations. The actual positive trend in US crude could extend to $85pb level.

SNB First G10 Bank to Cut Rates

In focus today

It should be a quiet finish to a very busy week for macro news. Today we will get the second wage tally from the Japanese "spring wage offensive". It will be interesting to see if the solid pay hike in big business has rubbed off more broadly.

Today we also look out for German ifo data for March.

Economic and market news

What happened overnight

Japanese CPI excl. fresh food rose to 2.8% y/y in February (prior: 2.0%), in line with polls, and affected by base effects due to energy subsidies last year. Stripping away energy, the "core-core" CPI, which the BoJ closely monitors, moderated to 3.2%. The BoJ will be closely watching whether they are right that sustained inflation near the 2% target has been reached after hiking earlier this week.

What happened yesterday

The SNB delivered a 25bp rate cut to 1.50%, in line with our expectations, and cited reduced inflationary pressure and a strong CHF, as well as materially lower inflation projections. Consensus was for a hold and markets sent the EUR/CHR higher during the day with the cross up 0.8% as of last night. The SNB is the first of the G10 central banks to lower rates, so this could be the start of a global rate-cutting cycle.

The BoE maintained the Bank Rate at 5.25% in line with consensus, but the committee gave dovish signals as Mann and Haskel (hawks) voted for unchanged rather than their previous hike-stance.

Norges Bank also maintained the policy rate as expected and maintained guidance for a first rate cut in September. We got a slightly hawkish surprise however, with Norges Bank upgrading the medium-term growth outlook and lifting the 25/26-part of the rate path. The NOK gained on release and traded higher during the day.

Euro area PMIs painted a mixed picture, with the service PMI remaining in growth territory, and beating expectations at 51.1 (cons: 50.5), while the manufacturing contraction worsened with the PMI at 45.7 (cons: 47.0). However, the underlying indicators showed an improvement in output, employment, and new orders, so things are not as bad as the headline numbers suggest.

US PMIs were largely in line with expectations, with the manufacturing outlook improving and service activity growth weakening a tad. Yields and the USD edged slightly higher upon release as the data showed an uptick in price indices.

Equities: Global equities were higher yesterday, heading for a very strong week and another set of all-time highs in several indices. Yesterday, a cyclical value driven outperformance with small caps also outperforming large caps. In other words, it could not have matched our strategy better although there were some macro signals which did not fully match our expectation. In US Dow +0.7%, S&P 500 +0.3%, Nasdaq +0.2% and Russell 2000 +1.1%. Asian markets are mostly lower this morning led down by China. Japanese stocks go against the trend as USD/JPY approaches 152. US futures are marginally higher this morning while European futures are mixed.

FI: European bond yields ended the trading with a modest decline in the long end and very modest curve steepener after the rate cut by the Swiss National Bank (SNB) and a dovish statement from Bank of England. 10Y US Treasury yield also declined yesterday but bounced back in the afternoon. Hence, the overall picture is that global central banks are looking towards a rate cut in June, although Norges Bank was a bit more hawkish than expected and here we are looking towards a rate cut in September.

FX: The SNB surprised markets, but not us, and cut its policy rate yesterday, which triggered a sharp sell-off in CHF. GBP followed CHF lower as the BOE, while keeping rates unchanged, struck a more dovish tone. NOK also lost some ground yesterday even though Norges Bank was a little less dovish than expected.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.35; (P) 192.43; (R1) 193.02; More.....

Intraday bias in GBP/JPY is turned neutral with current retreat and some consolidations would be seen. Nevertheless, outlook will stay bullish as long as 187.94 support holds. On the upside, break of 193.51 will resume larger up trend to 61.8% projection of 178.32 to 191.29 from 187.94 at 195.95, which is close to 195.86 long term resistance.

In the bigger picture, current rally is part of the uptrend from 123.94 (2020 low), and is in progress for long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

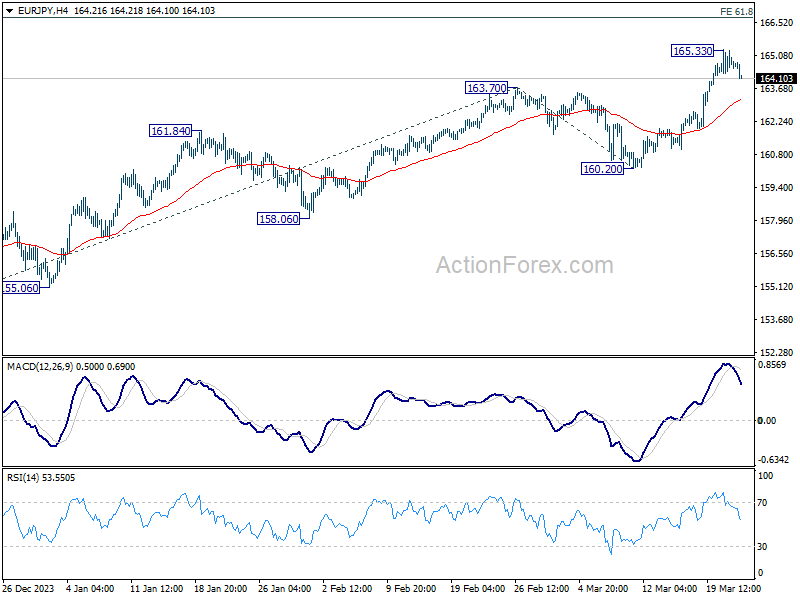

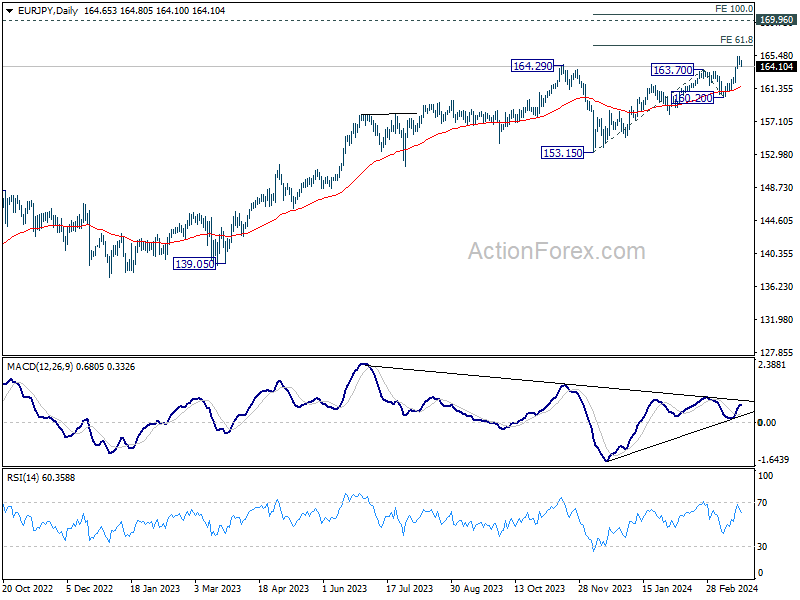

EUR/JPY Daily Outlook

Daily Pivots: (S1) 164.23; (P) 164.79; (R1) 165.22; More...

Intraday bias in EUR/JPY is turned neutral first with current retreat. Some consolidations could be seen but downside should be contained by 55 4H EMA (now at 163.19) to bring another rally. On the upside, break of 165.33 will resume larger up trend to 61.8% projection of 153.15 to 163.70 from 160.20 at 166.71.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

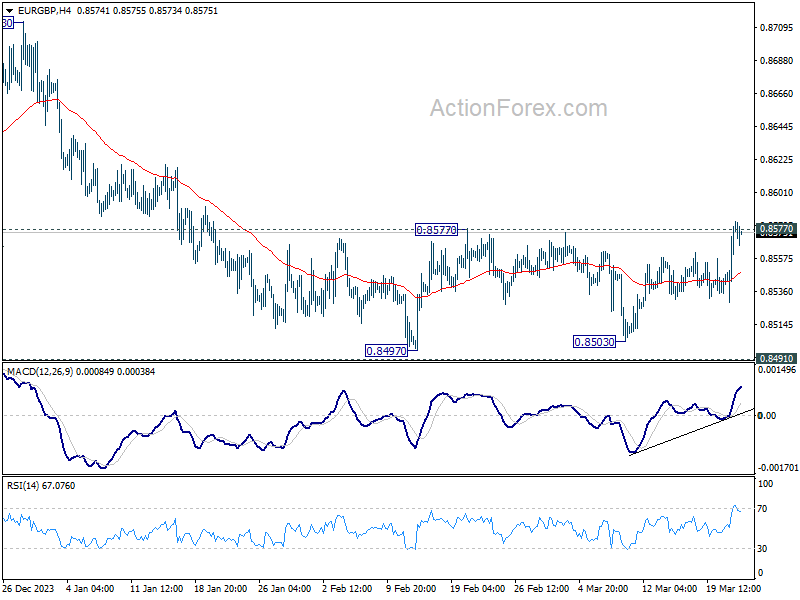

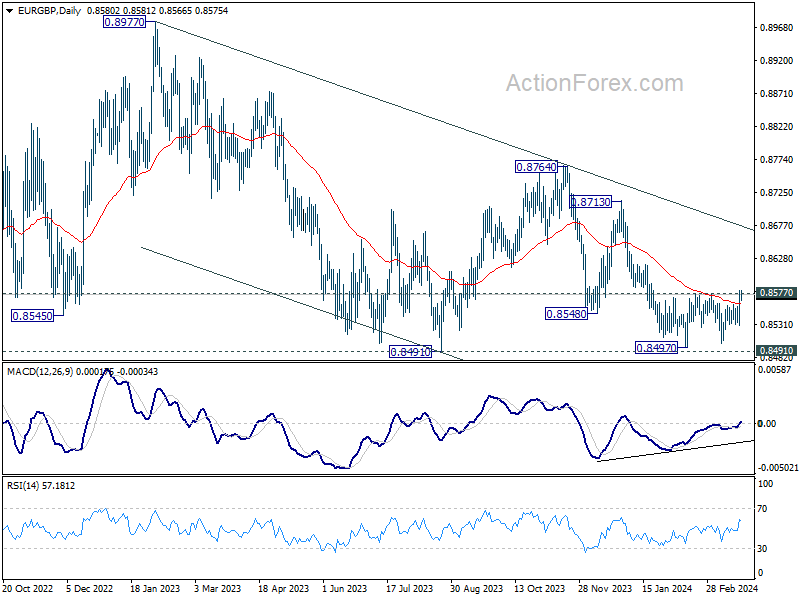

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8546; (P) 0.8564; (R1) 0.8599; More...

Immediate focus is now on 0.8577 resistance in EUR/GBP with current rebound. Decisive break there will argue that fall from 0.8764 has completed and turn bias back to the upside for stronger rebound. On the downside, decisive break of 0.8491/7 support zone will resume larger down trend from 0.9267 instead.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

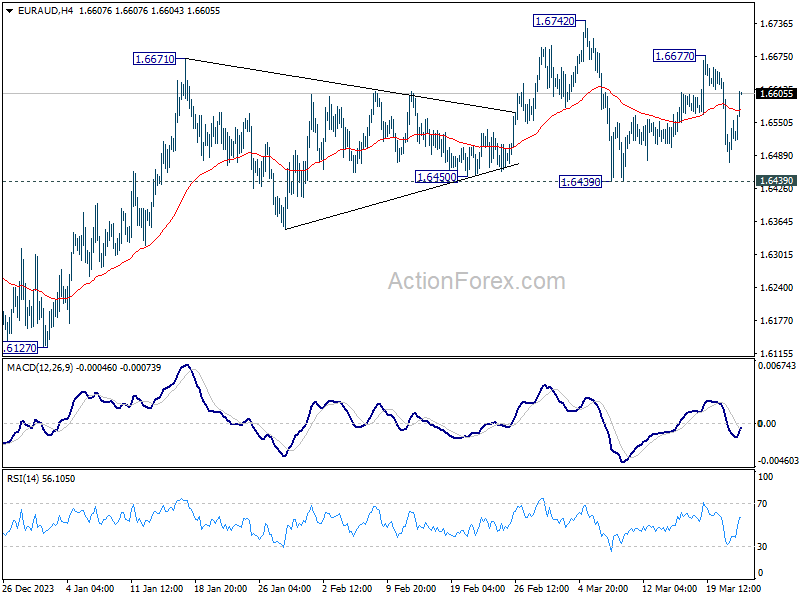

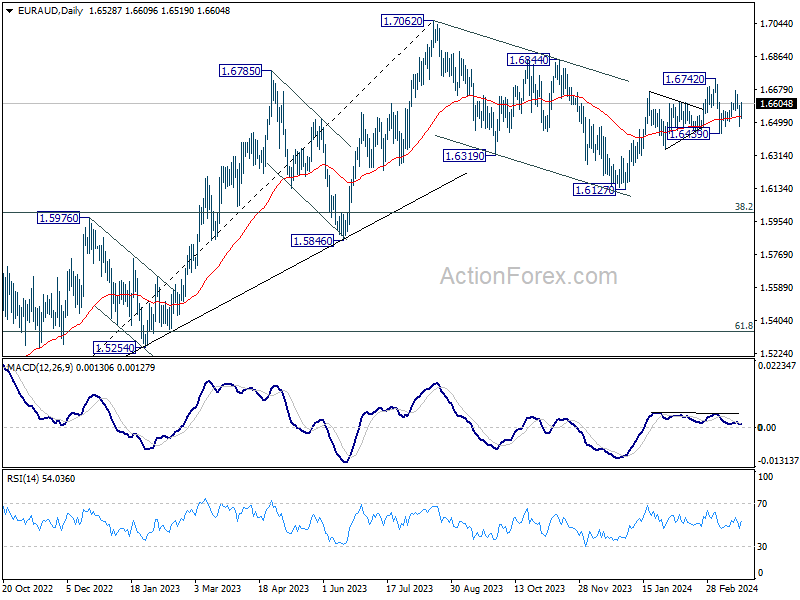

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6468; (P) 1.6539; (R1) 1.6599; More...

Intraday bias in EUR/AUD remains neutral as range trading continues. Near term outlook will stay cautiously bullish as long as 1.6439 support holds. On the upside, above 1.6677 will target 1.6742 first. Decisive break there will resume whole rise from 1.6127 and target 1.6844 resistance next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

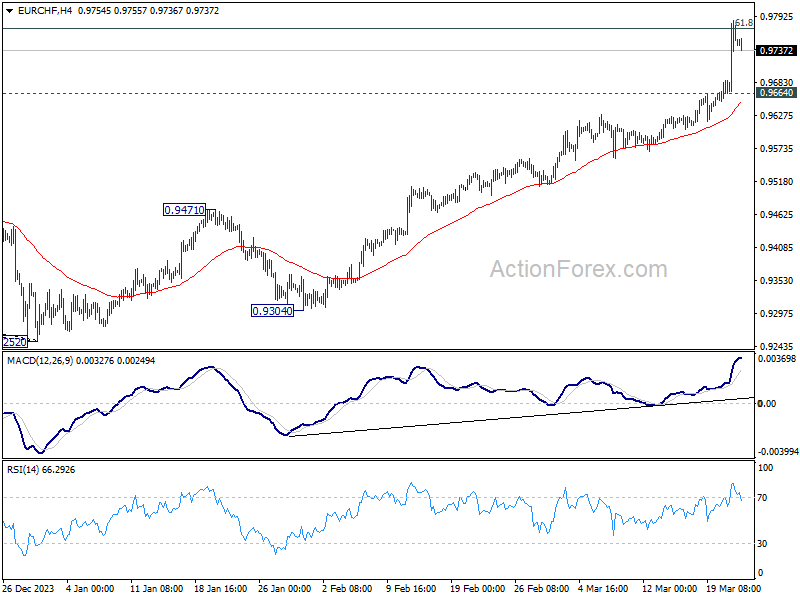

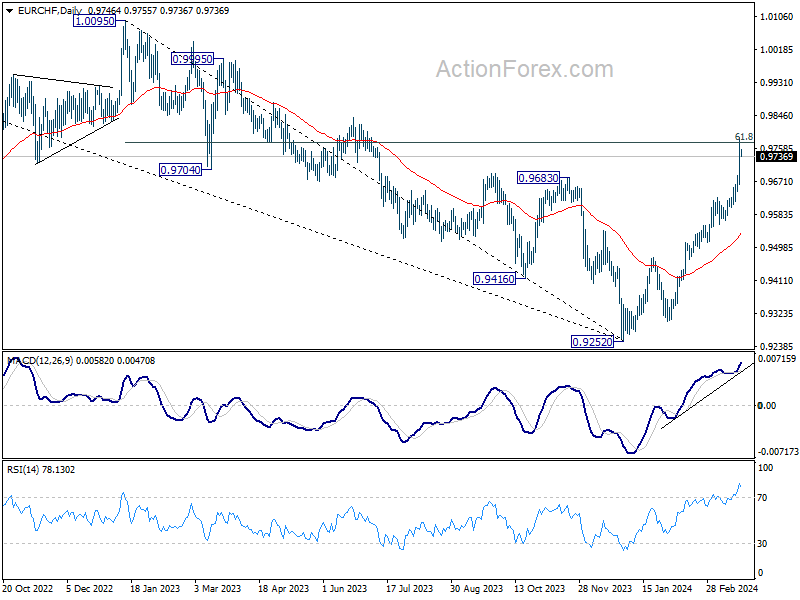

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9678; (P) 0.9733; (R1) 0.9803; More..

Intraday bias in EUR/CHF remains on the upside at this point. Sustained break of 61.8% retracement of 1.0095 to 0.9252 at 0.9773 will extend the rise from 0.9252 to 1.0095 key resistance next. On the downside, below 0.9664 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, the strong break of 0.9683 resistance indicates medium term bottoming at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303. This will remain the favored case as long as 55 D EMA (now at 0.9530) holds.

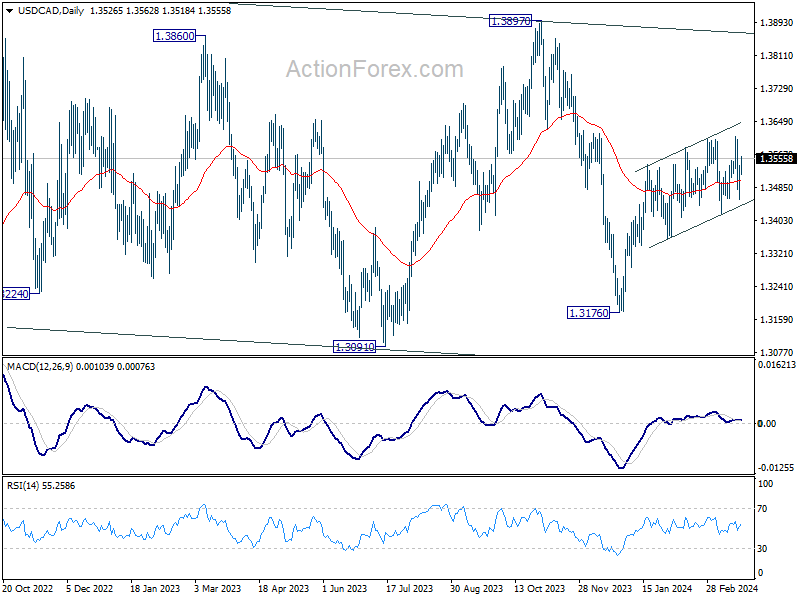

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3477; (P) 1.3510; (R1) 1.3563; More...

Intraday bias in USD/CAD remains neutral as range trading continues inside 1.3419/3612. On the upside, break of 1.3612 will confirm resumption of the rebound from 1.3176. On the downside, firm break of 1.3419 support will argue that rebound from 1.3176 has completed. Near term outlook will be turned bearish for 1.3357 support first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.