Sample Category Title

EUR/JPY Weekly Outlook

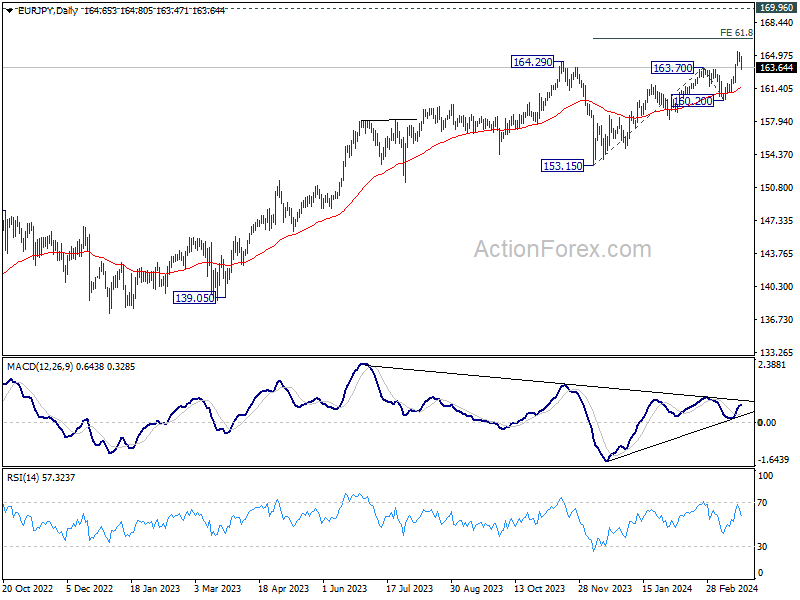

EUR/JPY's up trend resumed last week and surged to 165.33. But as a temporary top was formed with subsequent retreat, initial bias stays neutral this week for more consolidations. Downside should be contained by 55 4H EMA (now at 163.23) to bring rebound. On the upside, break of 165.33 will resume larger up trend to 61.8% projection of 153.15 to 163.70 from 160.20 at 166.71.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

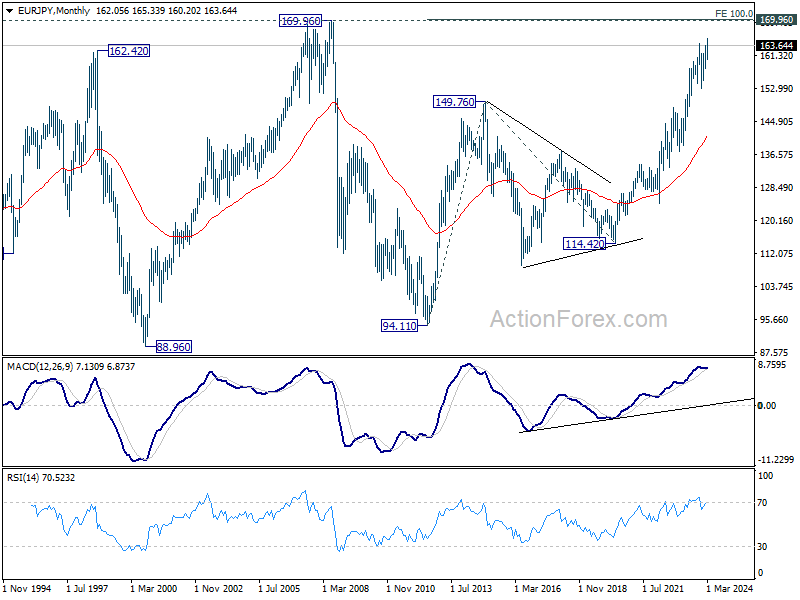

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 153.15 support holds.

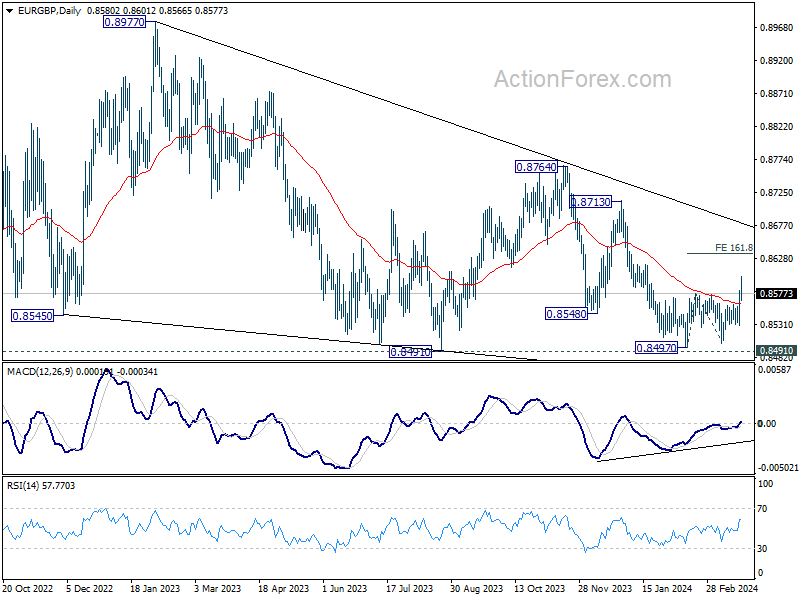

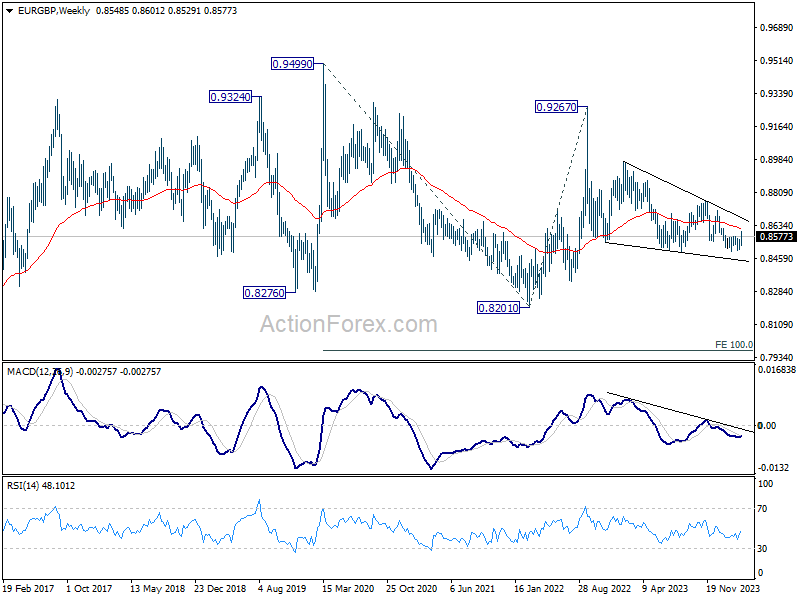

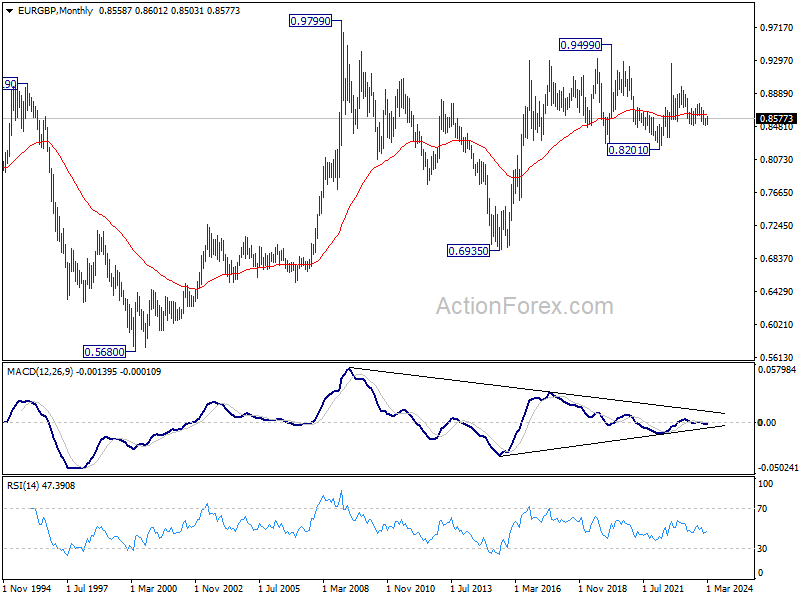

EUR/GBP Weekly Outlook

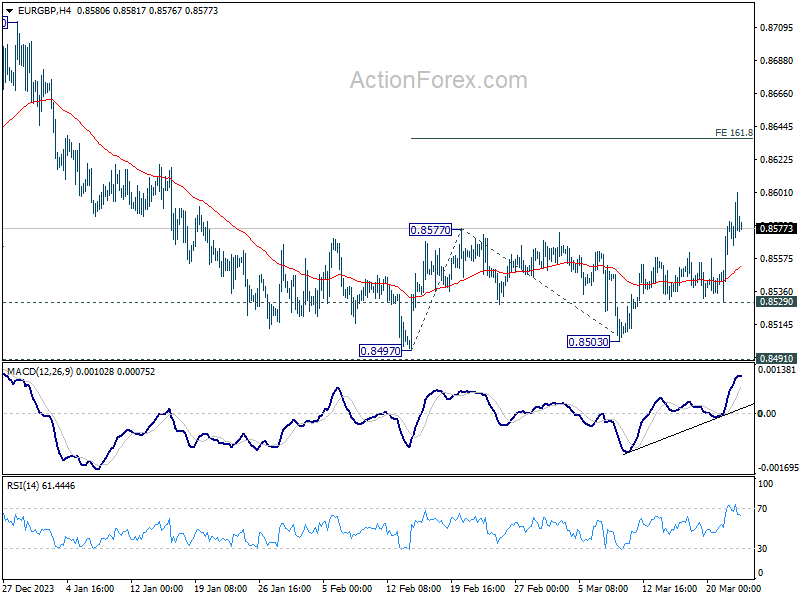

EUR/GBP's break of 0.8577 resistance and 55 D EMA (now at 0.8562) last week suggest that rebound from 0.8497 is at least correcting the fall from 0.8764. Initial bias is now on the upside this week for 161.8% projection of 0.8497 to 0.8577 from 0.8503 at 0.8632. For, further rise will remain in favor as long as 0.8529 minor support holds, in case of retreat.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8713 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Fall from 0.9267 is the third leg of the pattern from 0.9499. Break of 0.8201 (2022 low) will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969.

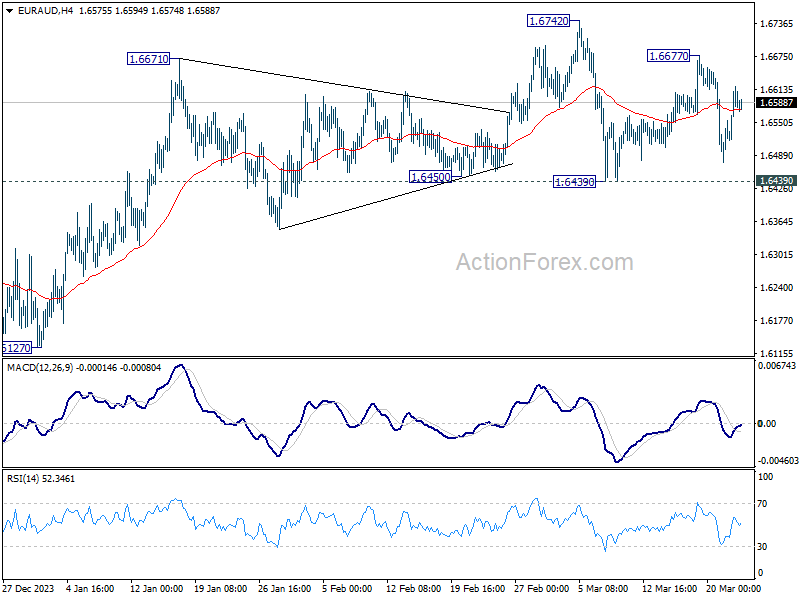

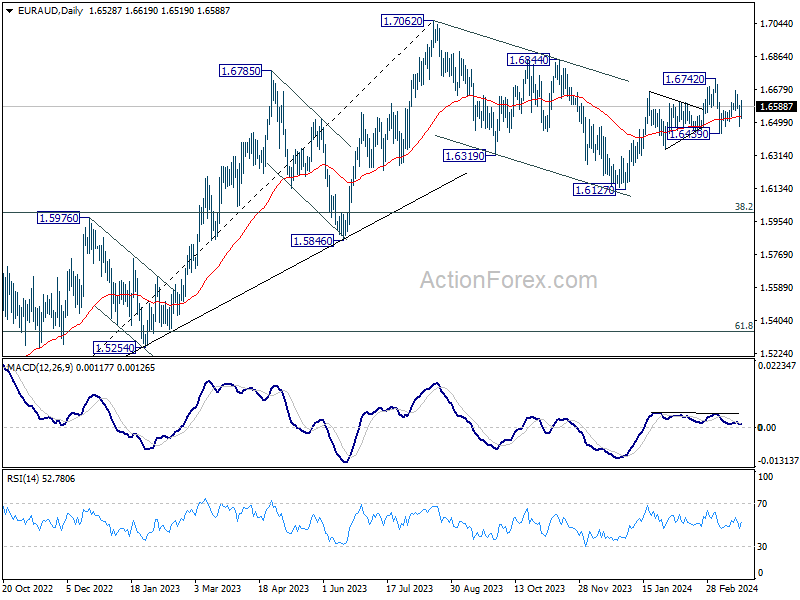

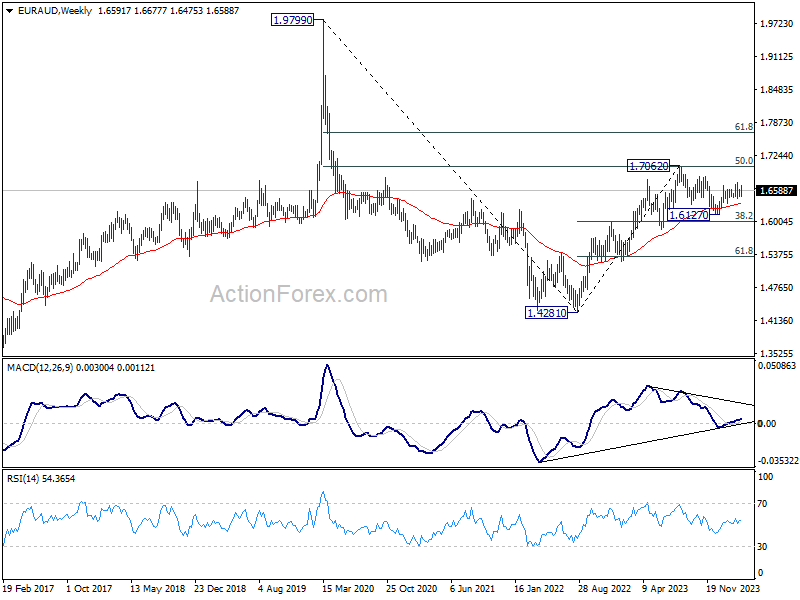

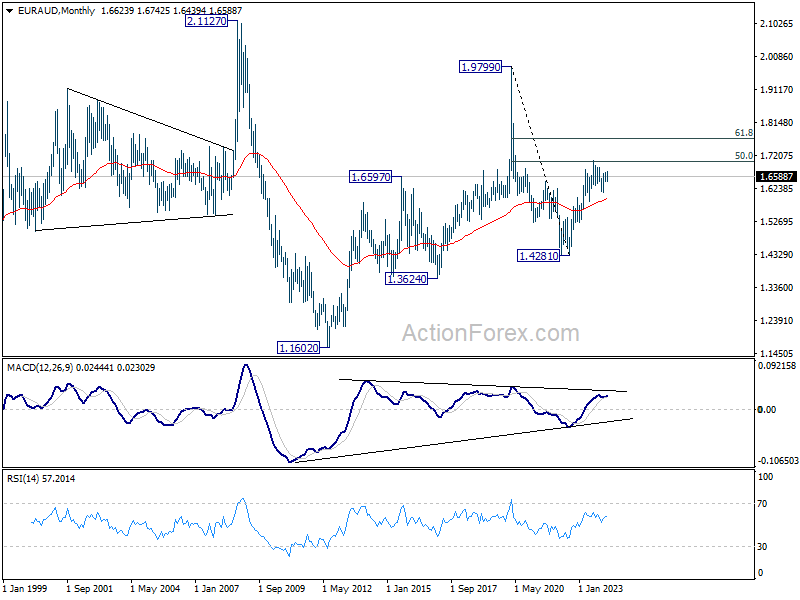

EUR/AUD Weekly Outlook

EUR/AUD stayed in consolidation in range of 1.6439/6742 last week and outlook is unchanged. Initial bias remains neutral this week first. Near term outlook will stay cautiously bullish as long as 1.6439 support holds. On the upside, above 1.6677 will target 1.6742 first. Decisive break there will resume whole rise from 1.6127 and target 1.6844 resistance next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5932) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

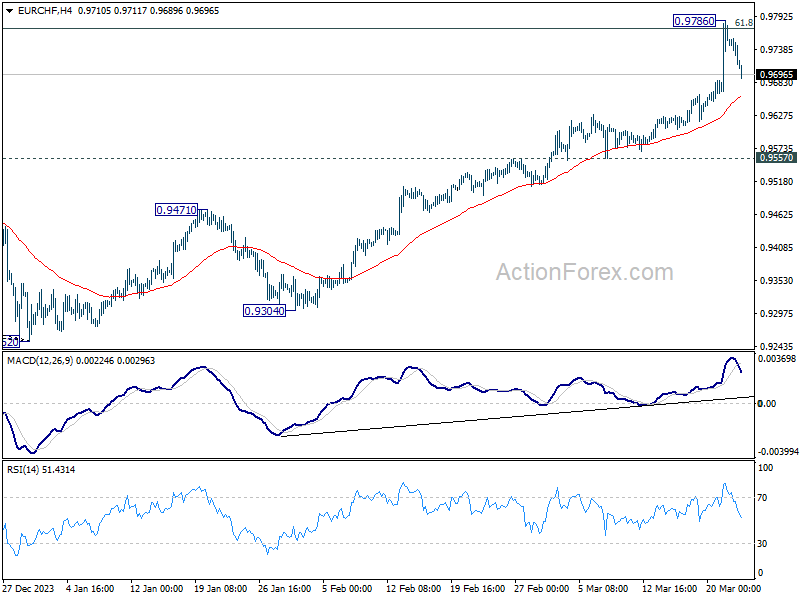

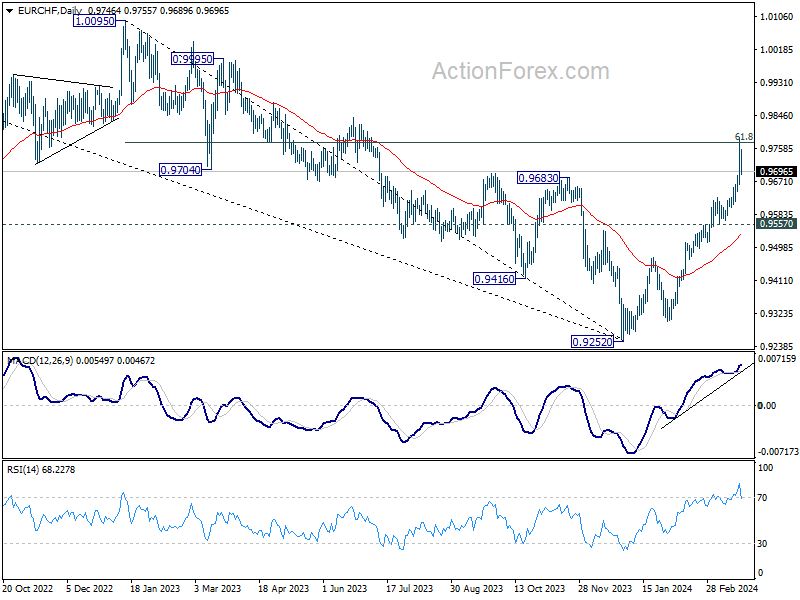

EUR/CHF Weekly Outlook

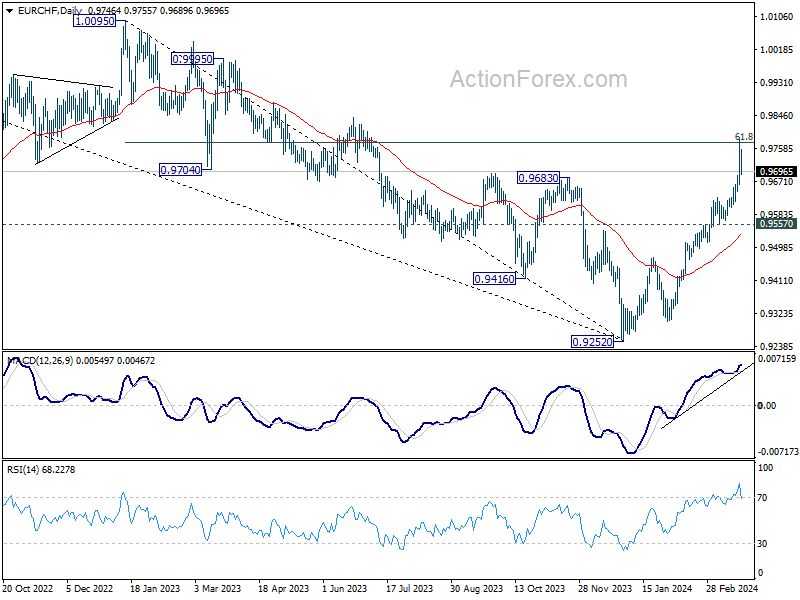

EUR/CHF's rally accelerated to as high as 0.9786 last week. But a temporary top should be formed after hitting 61.8% retracement of 1.0095 to 0.9252 at 0.9773. Initial bias is turned neutral this week for some consolidations. Downside of retreat should be contained by 0.9557 support to bring rebound. On the upside, above 0.9786 will resume the rally towards 1.0095 resistance next.

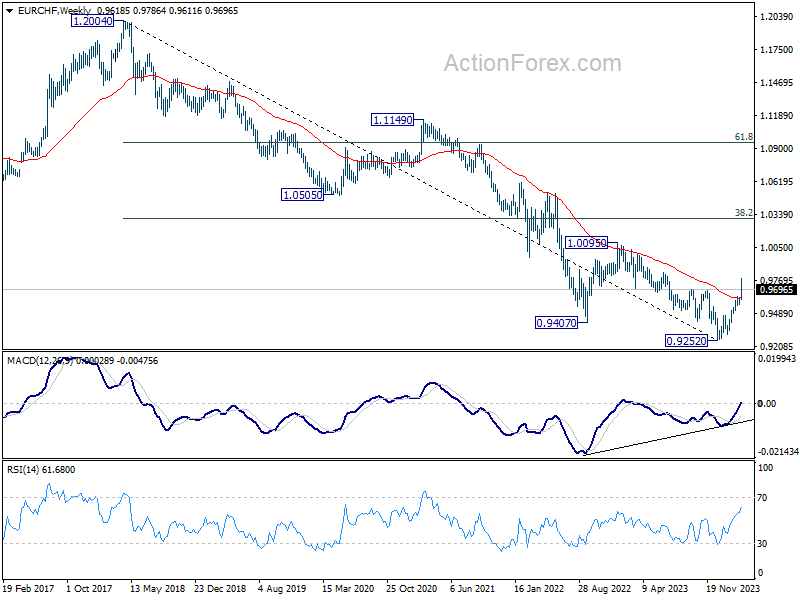

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9535) holds.

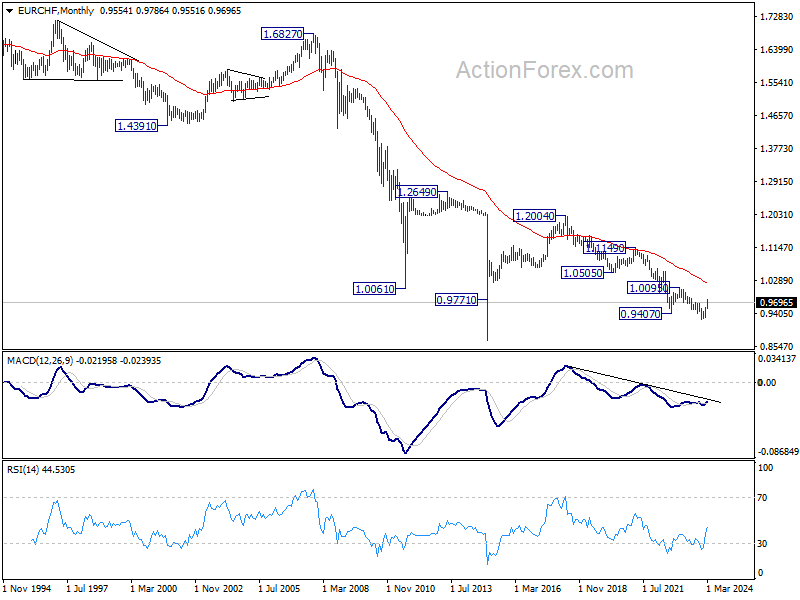

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

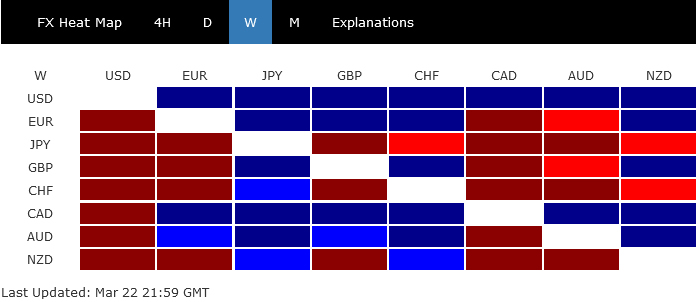

Dollar Triumphs Following a Turbulent Week of Central Bank Shocks

The past week in the currency markets was a dramatic whirlwind, marked by pivotal moves from major central banks across the globe. From BoJ's unexpected hike to SNB's surprise cut, from Fed's hawkish leaning projections to BoE's dovish voting, they collectively orchestrated a much volatile than usual trading environment.

Amidst this chaos, Dollar emerged victorious as the best performer. The technical picture in Dollar index suggests that more upside is likely in the greenback for the near term. Conversely, Swiss Franc and Japanese Yen bore the brunt of these developments, ending the week as the two worst performers by a mile. However, their late recovery indicate short-term stabilization, offering a reprieve from their downward spirals.

As the dust settles, attention shifts towards identifying the next currency at risk of an intensified downturn. British Pound is a candidate following BoE's dovish pivot, which has ignited speculation about rate cut as soon as June. At least, it's probably now already in a near term bearish reversal against Euro.

Furthermore, while New Zealand Dollar has already been under pressure due to concerns over the nation's economic outlook, as voiced by New Zealand's Finance Minister, Australian Dollar might be next in line. The steep plunge in Chinese Yuan last week, if sustained, could precipitate a broader sell-off in the stock markets of China and Hong Kong, adversely affecting Aussie in the process.

Dollar Dominates After Fed's Hawkish Tilt

Following a turbulent week, Dollar eventually asserted its dominance and ended as the stronger performer. The new dot plot accompanying Fed's rate decision to keep rate steady at 5.25-5.50% might have initially perceived as dovish. Fed maintained the projection of three rate cuts this year, tentatively placing the first reduction in June.

Upon a more detailed review, however, it became apparent that Fed's stance had subtly shifted towards a more hawkish orientation instead. This shift is illustrated by a nearly even split among FOMC members, with nine anticipating two rate cuts and ten forecasting three within the year—a notable change from December's 8-11 split. Furthermore, Fed's projections suggest a more gradual path to easing, with the federal funds rate expected to decrease to 3.875% by the end of 2025 (vs prior 3.625%) and 3.125% by the end of 2026 (vs prior 2.875%). This revised outlook, including a slight increase in the long-term federal funds rate estimate from 2.5% to 2.6%, indicates that the projections are clearly not dovish at all.

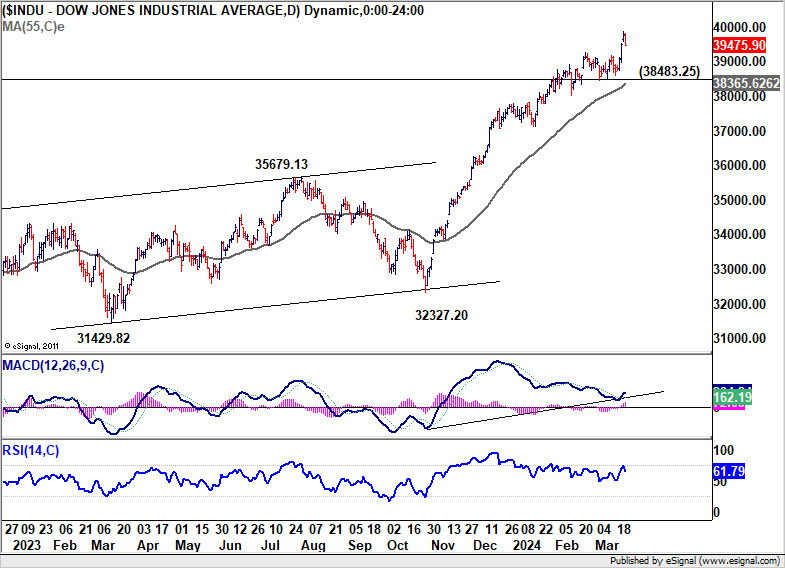

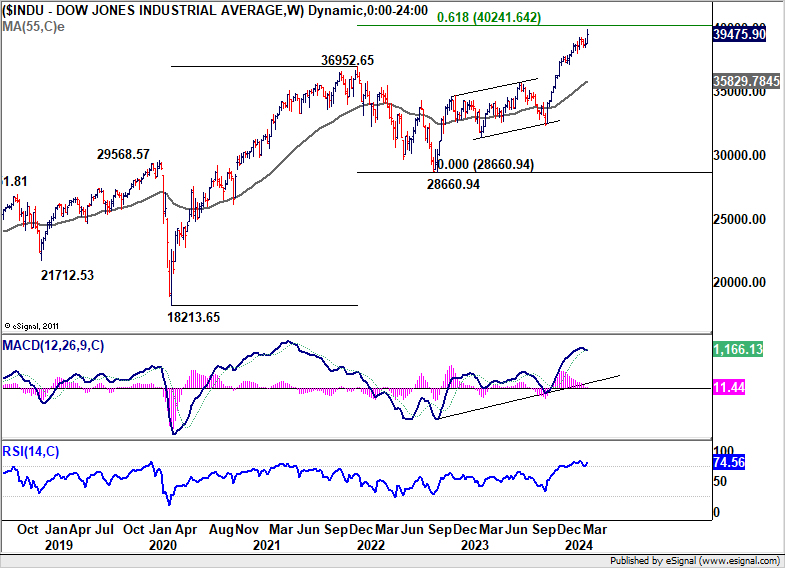

Regarding market reactions, DOW surged to new record high at 39889.05 last week. While DOW ended -305 pts lower on Friday, it still notched the best week since December. Next term outlook will stay bullish as long as 38483.25 support holds. The question is whether DOW has enough momentum to rise through 40k handle sustainably, considering that 61.8% projection of 18213.65 to 36952.65 from 28550.94 at 40251.64 is around.

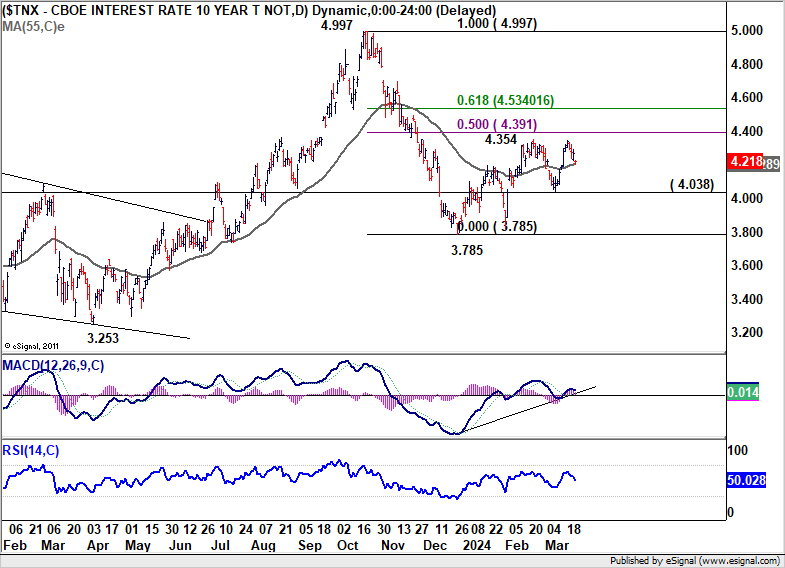

10-year yield failed to break through 4.354 resistance and restreated to close at 4.218. For now, it looks like the range is set for some sideway trading for the near term, between 4.038 and 50% retracement of 4.997 to 3.785 at 4.391. Or in short, the range is set between 4.0-4.4. Break of 4.000 is unlikely until there is firm indication that Fed' easing has started.

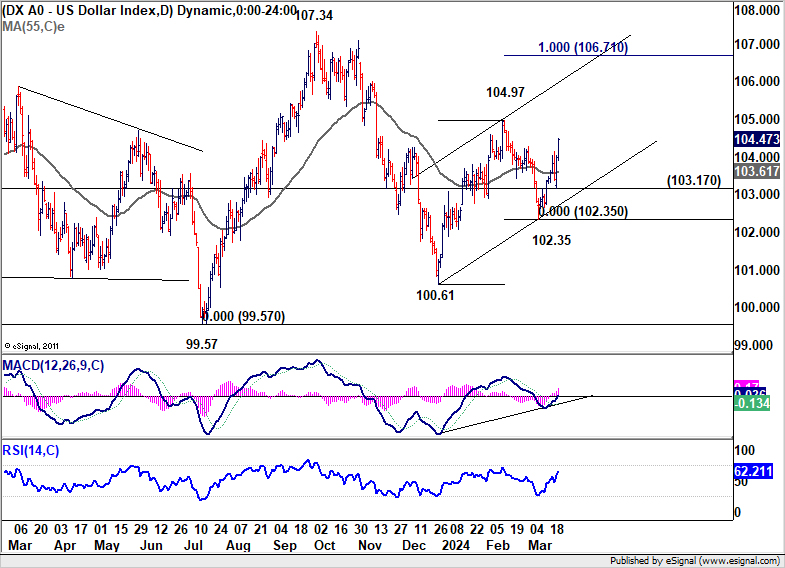

Dollar Index's strong rally suggests that pull back from 104.97 has completed at 102.35 already. Rise from there is likely resuming the rise from 100.61, which is the third leg of the pattern from 99.67 low. Near term outlook will stay cautiously bullish as long as 103.17 support holds. Break of 104.97 should pave the way to 100% projection of 100.61 to 104.97 from 102.35 at 106.71.

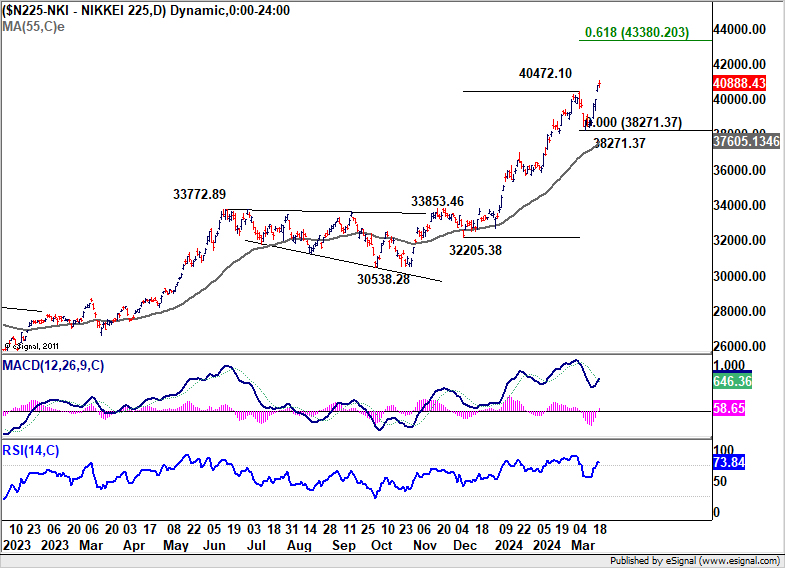

BoJ's Rate Increase Marks a Historic Shift, Yet Steady Tightening Is Not Imminent

Investors responded very positively to BoJ's surprised move to raise its interest rate to 0-0.1% and conclude its long-standing Yield Curve Control policy. This historic adjustment sent shockwaves through the markets, propelling Nikkei to unprecedented heights while concurrently sending Yen into a nosedive.

The reactions reflected market's interpretation of BoJ's actions as a strategic overhaul of the monetary policy framework, rather than the commencement of a sustained tightening cycle. While there are talks around the possibility of another rate hike in the latter half of the year, such discussions remain speculative at this juncture.

Nikkei's up trend resumed last week and hit as high as 41087.75. Near term outlook will stay bullish as long as 38271.37 support holds. Next target is 61.8% projection of 32205.38 to 40472.10 from 38271.37 at 43380.23. There is prospect of topping around this projection level to end the five wave rally from 30538.28, to start a medium term correction phase.

BoE's Dovish Pivot, FTSE Gains Momentum

While BoE left interest rate unchanged at 5.25% last week, the voting and subsequent comment from Governor Andrew Bailey were seen as a dovish pivot, setting the stage for the start of interest rate reduction later in the year. Firstly hawks Jonathan Haskel and Catherine Mann dropped their votes for hike this round, while Swati Dhingra advocating for a reduction again, making it an 8-1 split to stand pat.

Bailey's remarks reinforced this perspective, acknowledging the market's expectations for three rate reductions within the year as "reasonable." This commentary has led to increased speculation in financial markets, June is now seen as a possibility for the first cut, with bets now fully pricing in by August. Further, markets are anticipating a total of three reductions by the year's end, which would lower rates to 4.5% by December.

FTSE, the laggard index comparing to DOW, DAX and CAC, appeared to be finally catching up. The strong rally last week suggests that triangle consolidation from 8047.06 has completed, larger up trend could be ready to resume. Near term outlook will now stay bullish as long as 7785.73 resistance turned support holds. 61.8% projection of 6707.62 to 8047.06 from 7404.08 at 8231.85 would be the key level to determine FTSE's underlying medium term momentum.

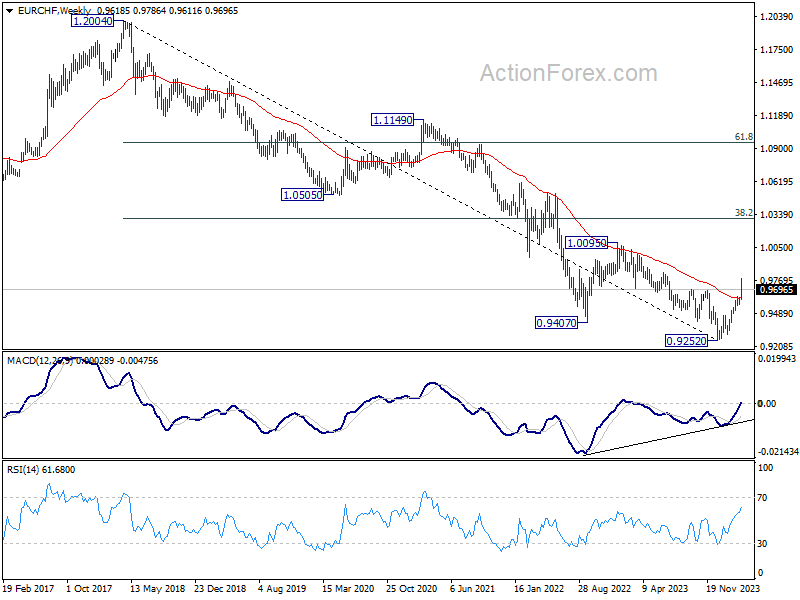

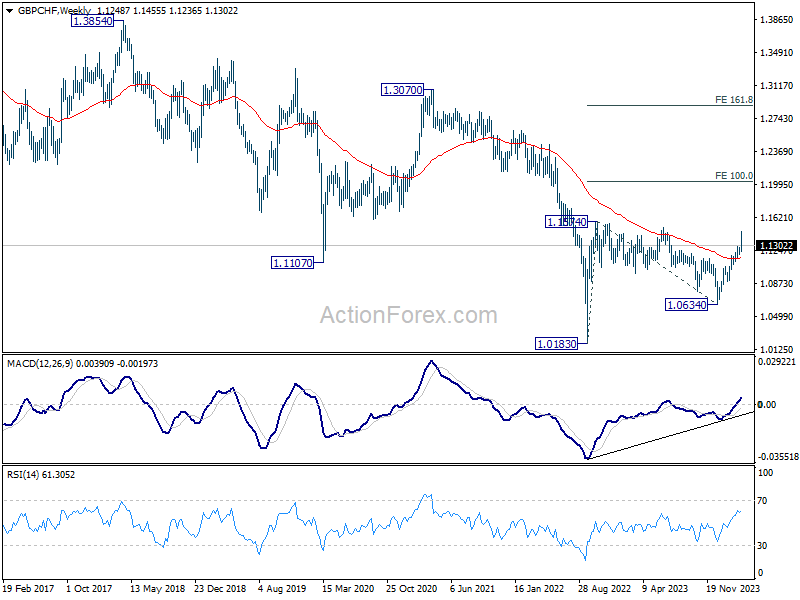

Swiss Franc's Bearish Turn after SNB's Rate Cut

Swiss Franc was sold off deeply after SNB's surprised rate cut, and ended as the worst performer. Franc's late recovery may hint that the initial selling frenzy might have peaked. However, that could only offer a momentary respite for the France as the bearish trend has likely been established already.

EUR/CHF rose to as high as 0.9786 but retreated after hitting 61.8% retracement of 1.0095 to 0.9252 at 0.9773. Some consolidations would be seen below this level in the near term. But downside of retreat should be contained above 0.9557 support to bring rebound.

The strong break of 55 W EMA argues that a medium term bottom was formed at 0.8252 on bullish convergence condition in W MACD. Rise from there should now target 1.0095 resistance or further to 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a corrective bounce in the long term down trend.

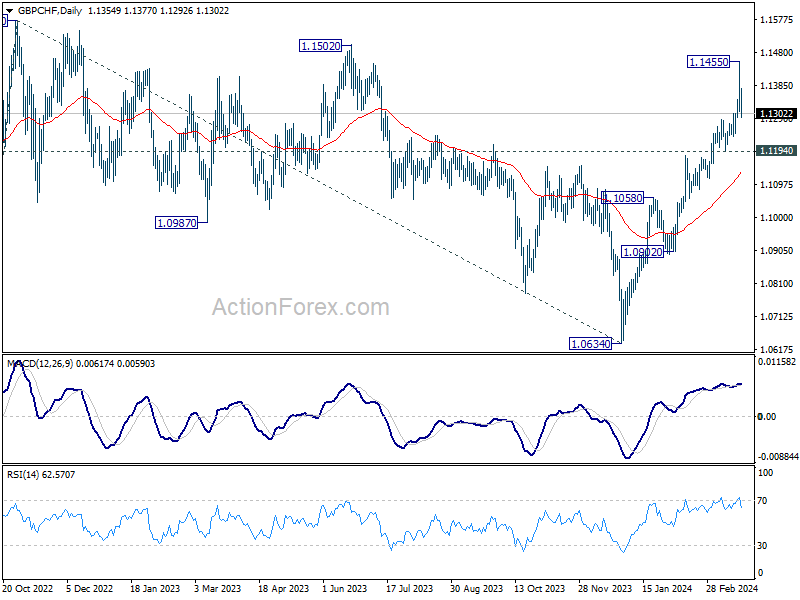

GBP/CHF also retreated after rising to 1.1455. Some consolidations is likely in the near term, but downside of retreat should be contained above 1.1194 support to bring rebound.

Current development affirms the case that rise from 1.0634 is resuming whole rally from 1.0183. Break of 1.1574 resistance will confirm and target 100% projection of 1.0183 to 1.1574 from 1.0634 at 1.2025 in the medium term.

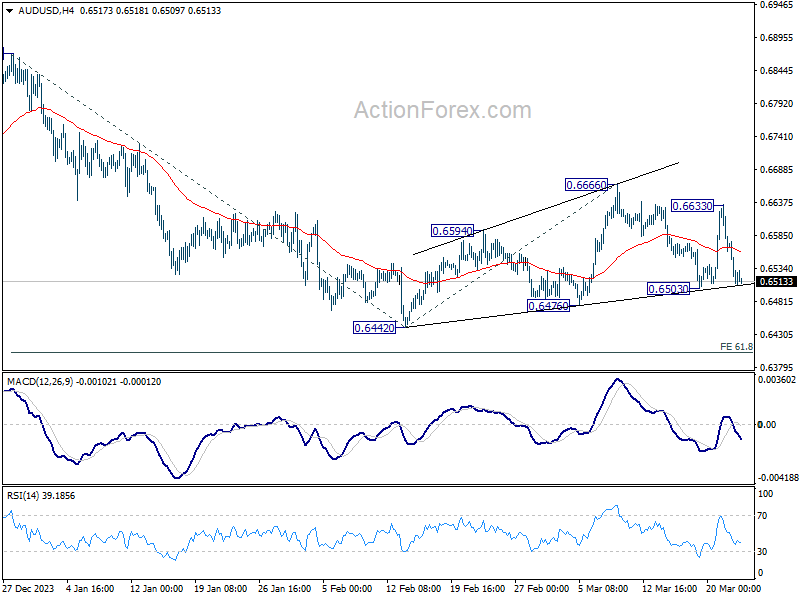

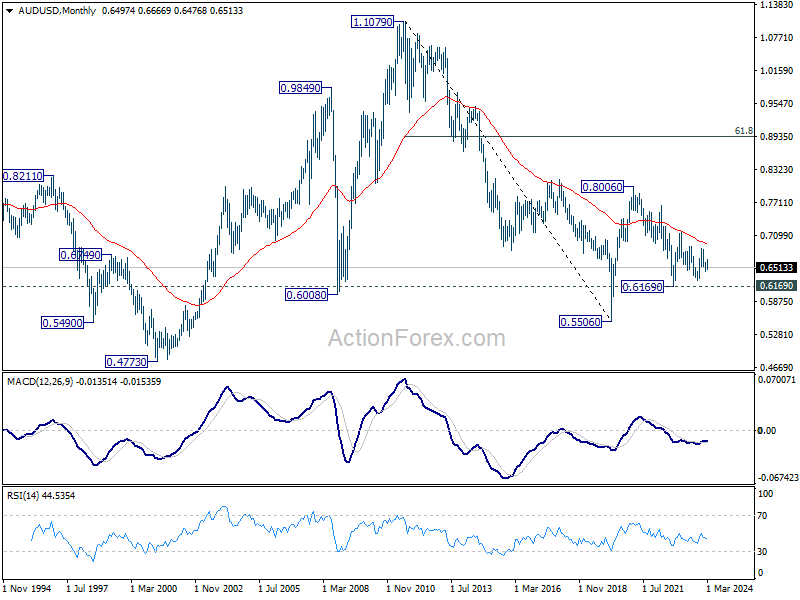

AUD/USD Weekly Report

AUD/USD's strong was rebound last week was capped below 0.6666 resistance, and followed by equally steep decline. Initial bias remains neutral this week first, with focus on 0.6503 support. Decisive break there will indicate that larger fall from 0.6870 is ready to resume, and turn bias to the downside for 0.6442 low. For now, risk will stay on the downside as long as 0.6633 resistance holds, in case of recovery.

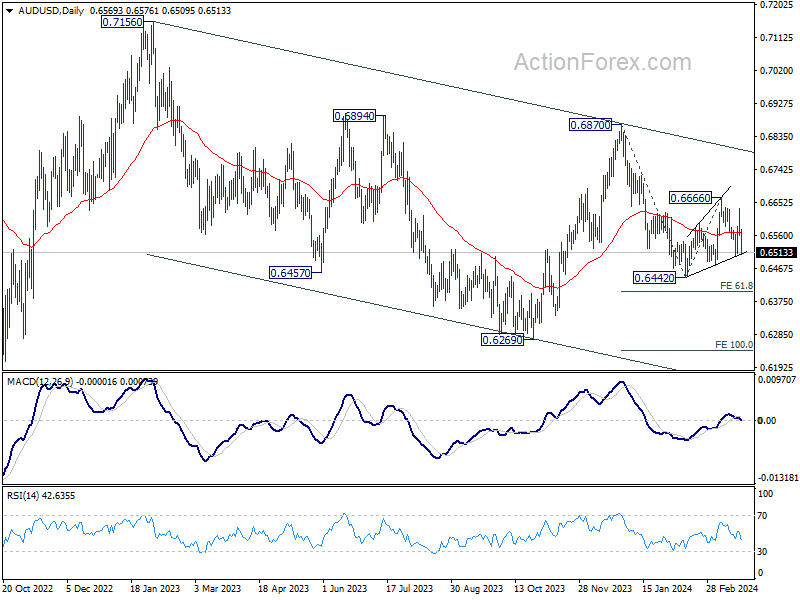

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

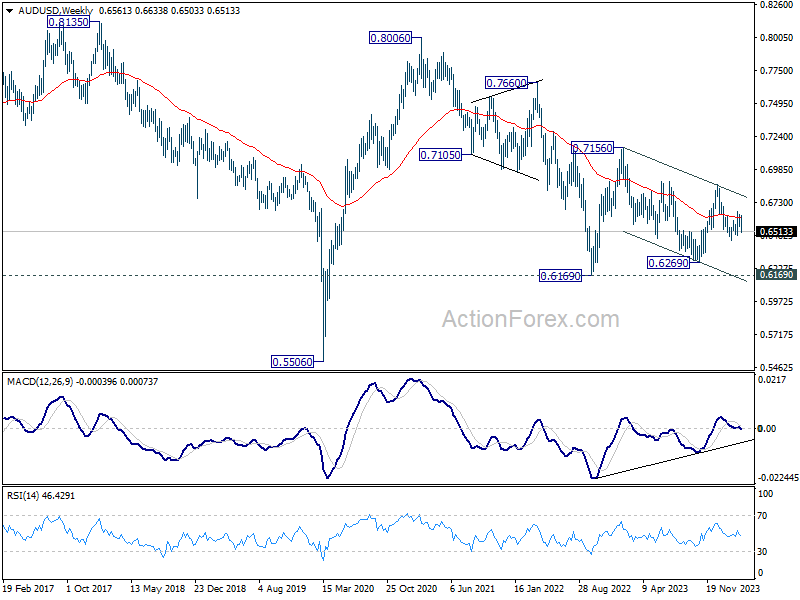

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen the second leg of the pattern. Hence, in case of deeper decline, strong support should emerge above 0.5506 to bring reversal.

Summary 3/25 – 3/29

Monday, Mar 25, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||

| 14:00 | USD | New Home Sales Feb | 675K | 661K |

| 23:30 | AUD | Westpac Consumer Confidence Mar | 6.20% | |

| 23:50 | JPY | Corporate Service Price Index Y/Y Feb | 2.00% | 2.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | |

| Forecast: | Previous: | ||

| 14:00 | USD | New Home Sales Feb | |

| Forecast: 675K | Previous: 661K | ||

| 23:30 | AUD | Westpac Consumer Confidence Mar | |

| Forecast: | Previous: 6.20% | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Feb | |

| Forecast: 2.00% | Previous: 2.10% | ||

Tuesday, Mar 26, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | EUR | Germany Gfk Consumer Confidence Apr | -27.8 | -29 |

| 12:30 | USD | Durable Goods Orders Feb | 1.30% | -6.20% |

| 12:30 | USD | Durable Goods Orders ex-Trans Feb | 0.40% | -0.40% |

| 12:30 | USD | Durable Goods Orders ex Defense Feb | 1.30% | -7.40% |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jan | 6.20% | 6.10% |

| 13:00 | USD | Housing Price Index M/M Jan | 0.20% | 0.10% |

| 14:00 | USD | Consumer Confidence Mar | 107.2 | 106.7 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | EUR | Germany Gfk Consumer Confidence Apr | |

| Forecast: -27.8 | Previous: -29 | ||

| 12:30 | USD | Durable Goods Orders Feb | |

| Forecast: 1.30% | Previous: -6.20% | ||

| 12:30 | USD | Durable Goods Orders ex-Trans Feb | |

| Forecast: 0.40% | Previous: -0.40% | ||

| 12:30 | USD | Durable Goods Orders ex Defense Feb | |

| Forecast: 1.30% | Previous: -7.40% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jan | |

| Forecast: 6.20% | Previous: 6.10% | ||

| 13:00 | USD | Housing Price Index M/M Jan | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 14:00 | USD | Consumer Confidence Mar | |

| Forecast: 107.2 | Previous: 106.7 | ||

Wednesday, Mar 27, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Feb | -0.10% | |

| 00:30 | AUD | Monthly CPI Y/Y Feb | 3.50% | 3.40% |

| 09:00 | CHF | Credit Suisse Economic Expectations Mar | 10.2 | |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Mar | 96.1 | 95.4 |

| 10:00 | EUR | Eurozone Industrial Confidence Mar | -9 | -9.5 |

| 10:00 | EUR | Eurozone Services Confidence Mar | 7.8 | 6 |

| 10:00 | EUR | Eurozone Consumer Confidence Mar F | -14.9 | -14.9 |

| 14:30 | USD | Crude Oil Inventories | -2.0M | |

| 23:50 | JPY | BoJ Summary of Opinions |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Feb | |

| Forecast: | Previous: -0.10% | ||

| 00:30 | AUD | Monthly CPI Y/Y Feb | |

| Forecast: 3.50% | Previous: 3.40% | ||

| 09:00 | CHF | Credit Suisse Economic Expectations Mar | |

| Forecast: | Previous: 10.2 | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Mar | |

| Forecast: 96.1 | Previous: 95.4 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Mar | |

| Forecast: -9 | Previous: -9.5 | ||

| 10:00 | EUR | Eurozone Services Confidence Mar | |

| Forecast: 7.8 | Previous: 6 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Mar F | |

| Forecast: -14.9 | Previous: -14.9 | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -2.0M | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

Thursday, Mar 28, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Mar | 34.7 | |

| 00:00 | AUD | Consumer Inflation Expectations Mar | 4.50% | |

| 00:30 | AUD | Retail Sales M/M Feb | 0.40% | 1.10% |

| 00:30 | AUD | Private Sector Credit M/M Feb | 0.40% | 0.40% |

| 07:00 | EUR | Germany Retail Sales M/M Feb | 0.30% | -0.40% |

| 07:00 | GBP | GDP Q/Q Q4 F | -0.30% | -0.30% |

| 07:00 | GBP | Current Account (GBP) Q4 | -21.5B | -17.2B |

| 08:00 | CHF | KOF Economic Barometer Mar | 102.3 | 101.6 |

| 08:55 | EUR | Germany Unemployment Rate Mar | 5.90% | 5.90% |

| 08:55 | EUR | Germany Unemployment Change Mar | 10K | 11K |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Feb | 0.30% | 0.10% |

| 12:30 | CAD | GDP M/M Jan | 0.40% | 0.00% |

| 12:30 | USD | Initial Jobless Claims (Mar 22) | 211K | 210K |

| 12:30 | USD | GDP Annualized Q4 F | 3.20% | 3.20% |

| 12:30 | USD | GDP Price Index Q4 F | 1.70% | 1.70% |

| 13:45 | USD | ChicagoPMI Mar | 46.4 | 44 |

| 14:00 | USD | Pending Home Sales M/M Feb | -2.00% | -4.90% |

| 14:00 | USD | Michigan Consumer Sentiment Mar F | 76.5 | 76.5 |

| 14:30 | USD | Natural Gas Storage | 7B | |

| 23:30 | JPY | Tokyo CPI Y/Y Mar | 2.60% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Mar | 2.40% | 2.50% |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Mar | 3.10% | |

| 23:30 | JPY | Unemployment Rate Feb | 2.40% | 2.40% |

| 23:50 | JPY | Industrial Production M/M Feb P | 1.40% | -6.70% |

| 23:50 | JPY | Retail Trade Y/Y Feb | 3.00% | 2.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Mar | |

| Forecast: | Previous: 34.7 | ||

| 00:00 | AUD | Consumer Inflation Expectations Mar | |

| Forecast: | Previous: 4.50% | ||

| 00:30 | AUD | Retail Sales M/M Feb | |

| Forecast: 0.40% | Previous: 1.10% | ||

| 00:30 | AUD | Private Sector Credit M/M Feb | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 07:00 | EUR | Germany Retail Sales M/M Feb | |

| Forecast: 0.30% | Previous: -0.40% | ||

| 07:00 | GBP | GDP Q/Q Q4 F | |

| Forecast: -0.30% | Previous: -0.30% | ||

| 07:00 | GBP | Current Account (GBP) Q4 | |

| Forecast: -21.5B | Previous: -17.2B | ||

| 08:00 | CHF | KOF Economic Barometer Mar | |

| Forecast: 102.3 | Previous: 101.6 | ||

| 08:55 | EUR | Germany Unemployment Rate Mar | |

| Forecast: 5.90% | Previous: 5.90% | ||

| 08:55 | EUR | Germany Unemployment Change Mar | |

| Forecast: 10K | Previous: 11K | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Feb | |

| Forecast: 0.30% | Previous: 0.10% | ||

| 12:30 | CAD | GDP M/M Jan | |

| Forecast: 0.40% | Previous: 0.00% | ||

| 12:30 | USD | Initial Jobless Claims (Mar 22) | |

| Forecast: 211K | Previous: 210K | ||

| 12:30 | USD | GDP Annualized Q4 F | |

| Forecast: 3.20% | Previous: 3.20% | ||

| 12:30 | USD | GDP Price Index Q4 F | |

| Forecast: 1.70% | Previous: 1.70% | ||

| 13:45 | USD | ChicagoPMI Mar | |

| Forecast: 46.4 | Previous: 44 | ||

| 14:00 | USD | Pending Home Sales M/M Feb | |

| Forecast: -2.00% | Previous: -4.90% | ||

| 14:00 | USD | Michigan Consumer Sentiment Mar F | |

| Forecast: 76.5 | Previous: 76.5 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 7B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Mar | |

| Forecast: | Previous: 2.60% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Mar | |

| Forecast: 2.40% | Previous: 2.50% | ||

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Mar | |

| Forecast: | Previous: 3.10% | ||

| 23:30 | JPY | Unemployment Rate Feb | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 23:50 | JPY | Industrial Production M/M Feb P | |

| Forecast: 1.40% | Previous: -6.70% | ||

| 23:50 | JPY | Retail Trade Y/Y Feb | |

| Forecast: 3.00% | Previous: 2.10% | ||

Friday, Mar 29, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Housing Starts Y/Y Feb | -5.50% | -7.50% |

| 07:45 | EUR | France Consumer Spending M/M Feb | 0.20% | -0.30% |

| 12:30 | USD | Personal Income M/M Feb | 0.40% | 1.00% |

| 12:30 | USD | Personal Spending Feb | 0.40% | 0.20% |

| 12:30 | USD | PCE Price Index M/M Feb | 0.40% | 0.30% |

| 12:30 | USD | PCE Price Index Y/Y Feb | 2.50% | 2.40% |

| 12:30 | USD | Core PCE Price Index M/M Feb | 0.30% | 0.40% |

| 12:30 | USD | Core PCE Price Index Y/Y Feb | 2.80% | 2.80% |

| 12:30 | USD | Wholesale Inventories Feb P | 0.20% | -0.30% |

| 12:30 | USD | Goods Trade Balance (USD) Feb P | -89.6B | -90.5B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Housing Starts Y/Y Feb | |

| Forecast: -5.50% | Previous: -7.50% | ||

| 07:45 | EUR | France Consumer Spending M/M Feb | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 12:30 | USD | Personal Income M/M Feb | |

| Forecast: 0.40% | Previous: 1.00% | ||

| 12:30 | USD | Personal Spending Feb | |

| Forecast: 0.40% | Previous: 0.20% | ||

| 12:30 | USD | PCE Price Index M/M Feb | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 12:30 | USD | PCE Price Index Y/Y Feb | |

| Forecast: 2.50% | Previous: 2.40% | ||

| 12:30 | USD | Core PCE Price Index M/M Feb | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Feb | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 12:30 | USD | Wholesale Inventories Feb P | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 12:30 | USD | Goods Trade Balance (USD) Feb P | |

| Forecast: -89.6B | Previous: -90.5B | ||

The Weekly Bottom Line: Counting Cuts

U.S. Highlights

- Markets let out a sigh of relief as the Fed’s Summary of Economic Projections reaffirmed expectations for three rate cuts this year.

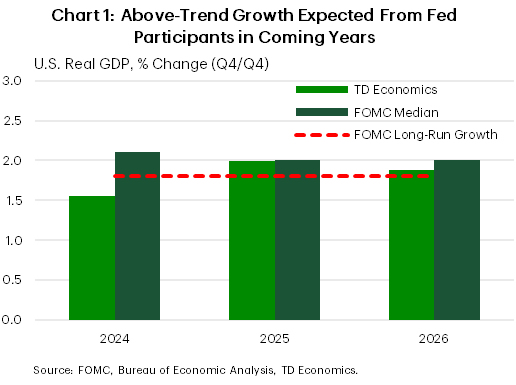

- The Fed’s forecast for the economy is interesting, as it implies above trend growth in each of the next three years – despite interest rates that remain in restrictive territory.

- Forecasts for healthy growth and some renewal in the housing market set the stage for next week’s personal income and expenditures report.

Canadian Highlights

- Canadian inflation showed significant improvement in February, with heavy discounting apparent across the consumer basket.

- The Bank of Canada’s (BoC’s) core inflation measures also decelerated, following other underlying inflation gauges lower.

- The BoC was encouraged by the improvement, but likely wants to see a continuation of recent trends before it decides to cut rates.

U.S. – Counting Cuts

Markets let out a sigh of relief as the Fed’s Summary of Economic Projections reaffirmed expectations for three rate cuts this year – rather than sending a more hawkish message by pulling back to two. In response, longer-term yields have extended their declines, with the 10-year Treasury down about 10 basis points (at the time of writing) since last Friday. Equities rallied on the news of easier policy, up just short of 1% after the projections were released.

While avoiding sending an overtly hawkish signal, officials did upgrade both the economic outlook and expectations for the level of interest rates in 2025 and 2026. The forecast for the economy is interesting, as it implies above-trend growth in each of the next three years – despite interest rates that are in restrictive territory. Conversely, our forecast has the economy slowing in the latter half of 2024 as the cumulative effect of high rates and the drawdown of consumer savings begin to dent both job creation and spending (Chart 1).

Admittedly, the risks remain skewed to the upside for the economy, inflation and interest rates. The U.S. consumer has thus far shrugged off all expectations for a slowdown. Real expenditures grew at roughly three percent through the back half of 2023, and the labor market expanded by an average of 265k jobs (SAAR) in the three months through February. All of this has the first quarter of 2024 looking like it’s going to be another healthy period of expansion.

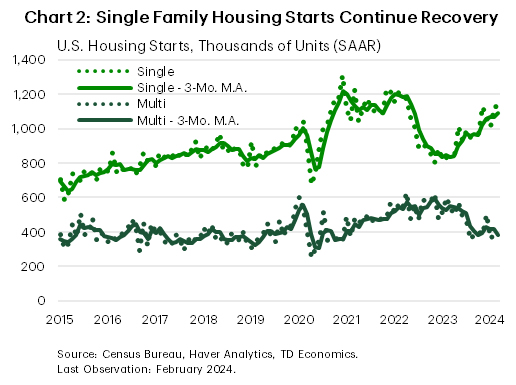

Even the housing sector, which has felt the brunt of a stagging rise in borrowing costs, has shown signs of life lately. Existing home sales and housing starts both left expectations in the rearview mirror. Moreover, the starts data reflect some rebalancing in the marketplace as single-family starts continue to grind higher adding units to a market starved for supply, while the multifamily segment slows down (Chart 2). Looking forward, increasing permitting activity suggests that there is some more room for improvement in housing construction.

Forecasts for healthy growth and some revival in the housing market set the stage for next week’s personal income and expenditures report. Markets will be on the lookout for signs that economic momentum carried through to February. Recall, January saw real spending contract, as weather weighed on economic activity, so a bounce-back is expected in February, with an accompanying uptick in headline inflation.

For policymakers, the focus will be on the core personal consumption expenditures (PCE) price deflator. Last month core prices gained 0.4% on the month. Expectations are for a 0.3% monthly advance in February. Remember, monthly price growth of below 0.2% is what is consistent with the 2.0% inflation target, so an upside surprise to prices would suggest a still significant amount of excess demand in the economy – an outcome we should all be used to by now.

Canada – CPIX Marks the Spot

Central bankers took the stage this week, but it was Canadian economic data that stole the show. A significant improvement in inflation for February and a weak reading on retail sales increased expectations for an earlier cut by the Bank of Canada (BoC). Adding to this was the release of the BoC’s March deliberations that confirmed the Bank is preparing to cut rates later this year. While the exact timing of the first rate cut is still uncertain, market pricing has rallied around June/July, matching expectations on timing for other major central banks.

The inflation reading this week showed a meaningful deceleration, with the headline measure remaining within the BoC 1% to 3% target band. But the big surprise was the heavy discounting on items like clothing, cell phone /internet plans, and food. For the latter, that was the first contraction in three years (seasonally adjusted)! As Deputy Governor Toni Gravelle said at a speech later in the week, this was “very encouraging”.

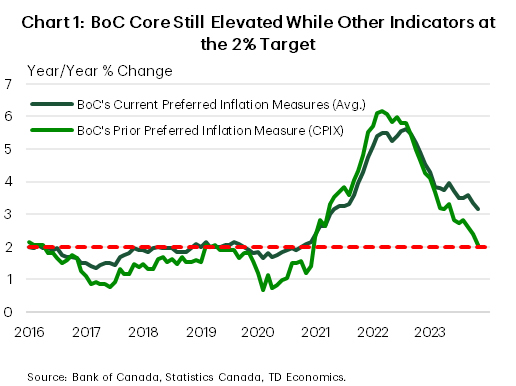

What was even more promising was the progress on the BoC’s preferred inflation metrics. While these have remained stubbornly high over the last few months, they too have started to ease and now sit just above the 3% band. These metrics are starting to follow other measures of inflation lower, including the Bank’s old preferred inflation measure, CPIX (Chart 1). This index excludes the eight most volatile inflation items such as mortgage interest costs. Importantly, this measure has now reached the BoC’s 2% target.

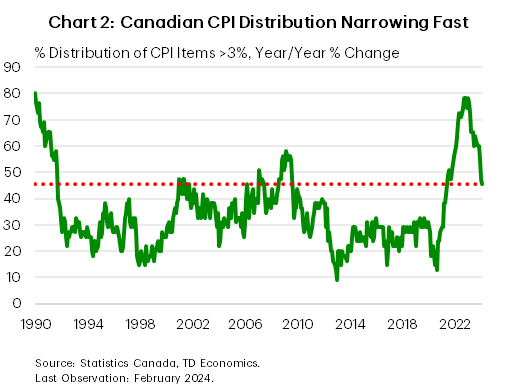

We have been arguing that the BoC should look outside of its preferred indicators of inflation, which are being influenced by structural issues related to shelter inflation. This is something the BoC has started to acknowledge. In recent communications, it has started to list a broad suite of inflation indicators that it will use to determine the state of underlying inflation. CPIX, as mentioned above, is one of them. But another measure that the Bank has started to rely on is the distribution of inflation. Here the BoC has stated that the percent of CPI items growing at 3% or more remains too high (Chart 2). It’s true that the distribution remains above 40%, which is more than the historical average of 35%. But we’d argue that it is getting close to more normal levels. The downward momentum in this index is apparent, and unless there is another supply-side shock to inflation, this measure will keep moving lower, bringing the slow moving BoC measures along with it.

This is why market pricing has become more entrenched around an earlier start to rate cuts. And even though the Deputy Governor showed more optimism than we have seen from other BoC speakers, expect the Bank to keep its cards a little closer to its chest over the coming month. The BoC doesn’t want the market to get any further ahead of itself, as it can’t afford to stoke a spring housing market boom. Rather, the BoC is likely to wait until the spring rush has started to abate before it communicates that it is ready for rate cuts.

Weekly Economic & Financial Commentary: Sitting, Waiting, Wishing

Summary

United States: Residential Tailwind Set to Continue as Monetary Policy Becomes Less Restrictive

- This week's economic data indicate that the U.S. economy is still expanding at a solid pace with the housing sector continuing to provide a tailwind. During February, existing home sales and housing starts both topped expectations and rose at robust rates. Meanwhile, initial jobless claims have remained subdued so far in March.

- Next week: New Home Sales (Mon.), Durable Goods Orders (Tue.), Personal Income & Spending (Fri.)

International: Bank of Japan Exits Negative Interest Rate Policy

- In a historic—albeit well-anticipated—policy shift, the Bank of Japan (BoJ) formally ended its ultra-easy and nonconventional monetary policy stance this week, delivering the first BoJ interest rate hike since 2007. The outcome of Japan's spring wage talks appears to have been a particularly important factor behind the decision.

- Next week: Riksbank Policy Interest Rate (Wed.), Canada Monthly GDP (Thu.), Tokyo CPI (Fri.)

Interest Rate Watch: Sitting, Waiting, Wishing

- The FOMC left the target range on its federal funds rate unchanged and held the pace of balance sheet runoff (QT) constant at the conclusion of its March 20 meeting. Individual forecasts of FOMC participants for rates, growth and inflation this year strike a modestly hawkish tone.

Credit Market Insights: Are American Consumers Learning to Live with Higher Rates?

- This week, the New York Fed released its triannual Credit Access Survey. While the byline of its report, “Credit Application Rate Ticks Up; Rejection Rate Declines,” suggests consumers and bankers are adjusting to the “higher for longer” world, the details reveal that the higher rate environment is dampening demand for current loans and expectations of future credit access.

Topic of the Week: Building the Future

- The high-tech manufacturing sector in the U.S. has been the fastest growing category within nonresidential construction in recent years. In a report published this week, we discuss how the construction boom in high-tech manufacturing may impact the U.S. economy.

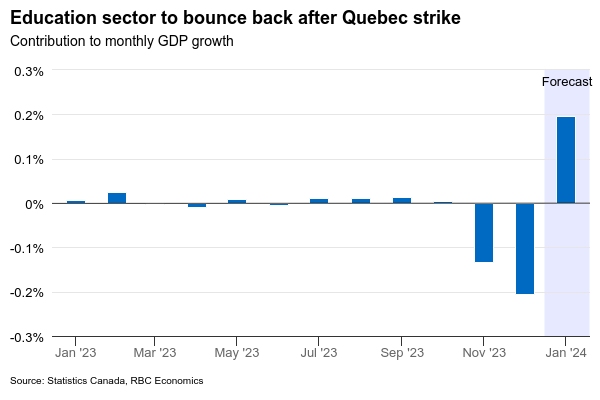

Canada’s January GDP to Edge Higher on Recovery from Quebec Strike

Canadian gross domestic product for January is expected to show modest growth on Thursday, while employment data will highlight whether weakness in job vacancies and wage growth still persists ahead of the Easter long weekend.

We expect the Canadian economy to edge up 0.2% after a flat reading in December—and below the 0.4% increase forecasted by Statistics Canada’s advance estimate a month ago. Public sector strikes in Quebec that weighed on output in the education sector in November and December ended, and these workers returning to their jobs will boost output in January. Output in the manufacturing sector also likely grew by 1%.

But indicators for other sectors have been softer. Wholesale sale volumes were little changed in January and retail sales volumes went up 0.2% in January. Our tracking of card transactions is pointing to a pullback in accommodation and food service spending. Oil production in Alberta also appears to have declined significantly in January. Overall, GDP in the goods-producing side of the economy is expected to be little changed with an increase in service-producing industries largely accounted for by a bounce-back in the Quebec public sector.

The Survey of Employment, Payrolls and Hours (SEPH) for January will be watched closely for a further decline in job vacancies (running about 25% below year-ago levels) and for any sustained underperformance in wage growth. The Bank of Canada referenced “some signs that wage pressures may be easing” in the March policy statement. It was a nod to wage growth in the payroll employment data running about 2 percentage points below the 5% plus growth seen in the separate monthly labour force survey data in Q4 of last year.

Week ahead data watch

U.S. personal income likely edged up 0.3% in February, given that earlier wage growth data from the payroll report was still strong (0.14%). Personal consumption is expected to tick up again (0.5%) during the month on higher retail sales.

Will PCE Data Revive Concerns About Sticky US Inflation?

- Fed continues to see three rate cuts for 2024

- Investors add back to the June cut probability

- Focus shifts to next week’s core PCE index

- The data comes out on Friday at 12:30 GMT

Fed appears more dovish than expected

The Fed appeared more dovish than expected at its highly anticipated March gathering on Wednesday, with the updated dot plot still pointing to three quarter-point rate cuts for 2024.

Despite the upgrades in growth and inflation forecasts, officials just removed only one 25bps cut from their 2025 rate projections, while at the press conference following the decision, Fed Chair Powell said that recent high inflation readings had not changed the narrative of slowly easing price pressures.

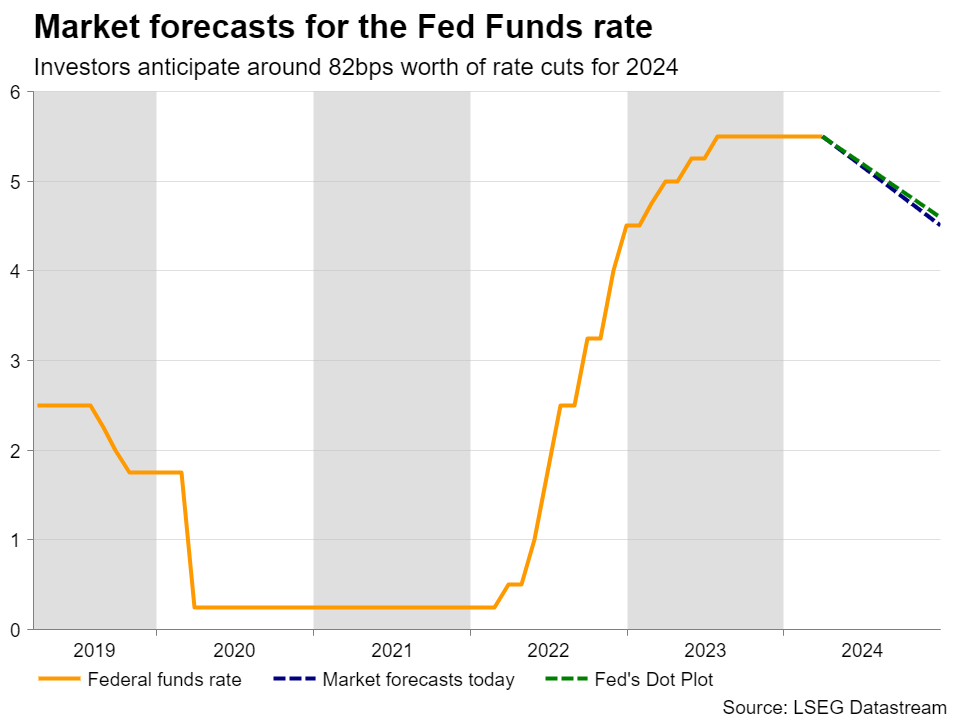

The outcome came as a disappointment to those expecting the Fed to signal two rate reductions by the end of the year, and thus the dollar tumbled in the aftermath of the decision as market participants added back to their rate cut bets. According to Fed funds futures, the probability of a first cut in June has risen to around 80%, with the total number of basis points worth of reductions expected by December increasing to 82.

Dollar bulls stay in the game, await PCE data

That said, dollar bulls did not abandon the game, initiating new long positions after the Swiss National Bank (SNB) surprisingly cut interest rates on Thursday and as the Bank of England appeared more dovish than expected, with Governor Bailey repeating that they are not yet at the point where they can cut interest rates, but adding that with inflation coming down, things are moving in the right direction.

Investors are now assigning the same 80% chance for all three major central banks – the Fed, the ECB, and the BoE – to deliver their first 25bps cut in June. As they try to clear the picture, the data point that may attract investors’ attention next week is the core PCE price index for February, the Fed’s favorite inflation metric, which is accompanied by the personal income and spending figures for the same month.

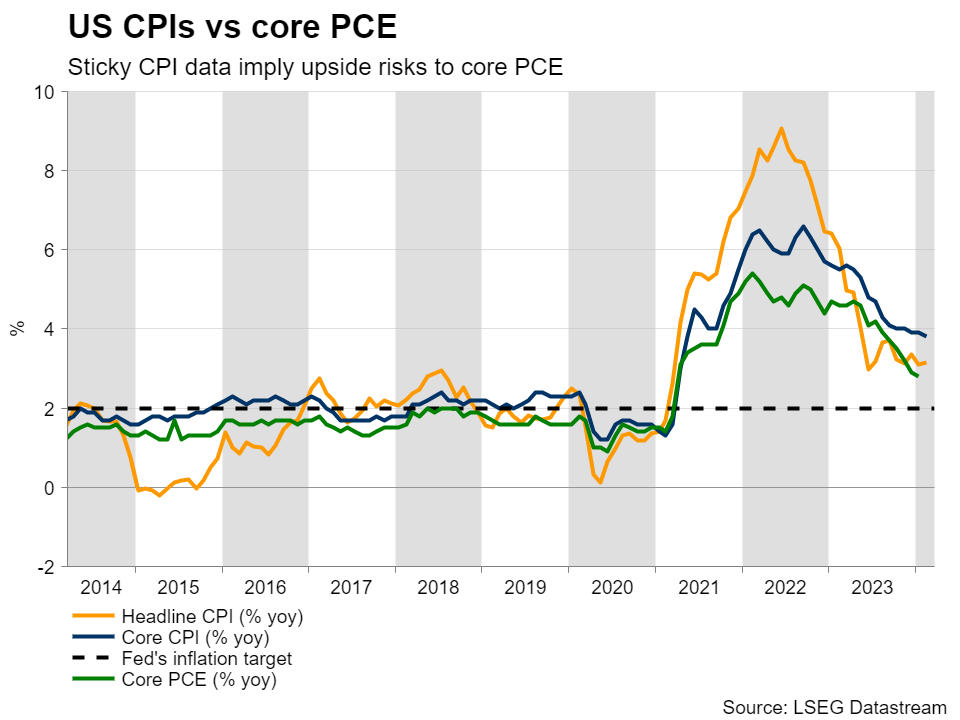

Risks may be tilted to the upside

Core CPI inflation ticked down to 3.8% y/y in February from 3.9%, but that was higher than the 3.7% projection, suggesting that core PCE may also prove to be higher than anticipated. Although Powell has already mentioned that the stickiness in recent inflation data is not a reason for the Fed to alter its plans, a higher-than-expected core PCE rate accompanied by strong income and spending prints could raise fears of accelerating inflation in the months to come.

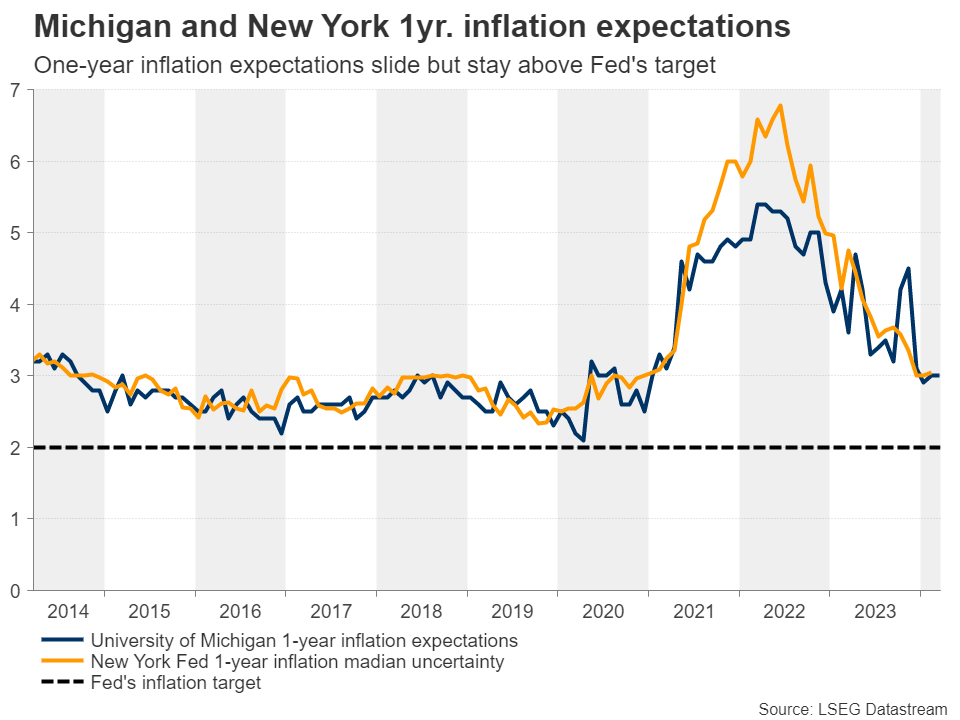

After all, the S&P Global PMIs revealed that selling prices rose at the fastest pace in just under a year, corroborating that notion. On top of that, the Atlanta Fed GDPNow model points to a solid 2.1% seasonally adjusted anneal growth rate for the first quarter of 2024, while both the University of Michigan and New York Fed 1-year inflation expectations remain at 3.0%, suggesting that consumers believe that the Fed’s 2% will not be met even in a year’s time.

Sticky inflation could further boost the dollar

With the US economy continuing to fare better than its major peers, data pointing to sticky inflation may slowly start convincing market participants again that the Fed may not need to rush into cutting interest rates in June. Even if this is not the case, anything pointing to earlier rate reductions elsewhere may allow the dollar to continue recovering ground.

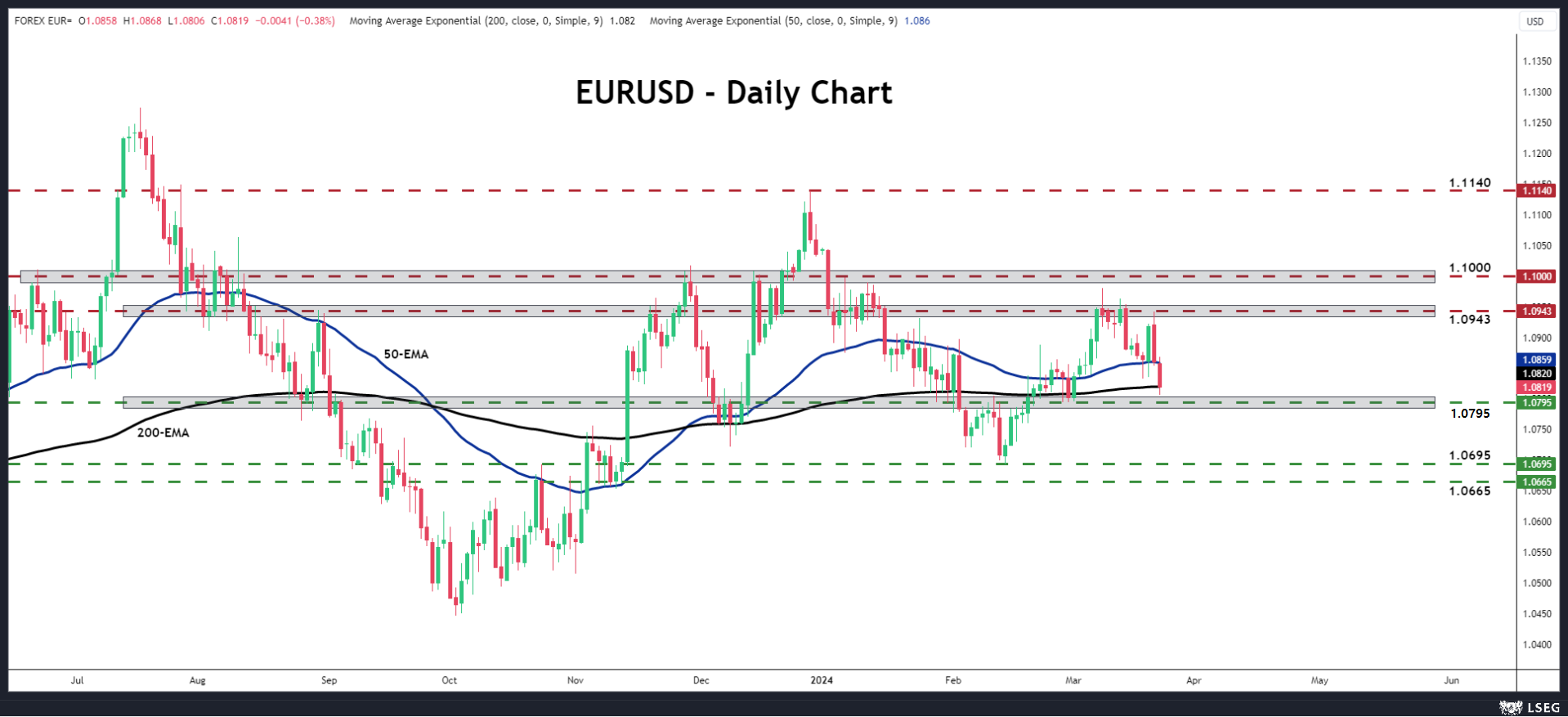

Euro/dollar came under strong selling pressure on Thursday, after it hit resistance at 1.0943. The slide continued on Friday with the pair now hovering near the 200-day exponential moving average (EMA), slightly above the 1.0795 support zone, marked by the lows of February 28 and 29.

A decisive break below that area could encourage the bears to dive all the way down to the 1.0695 barrier, marked by the low of February 14, or even the next key support at around 1.0665. For the near-term outlook of this pair to change, the bulls may need to lift the price above the round figure of 1.1000.