Sample Category Title

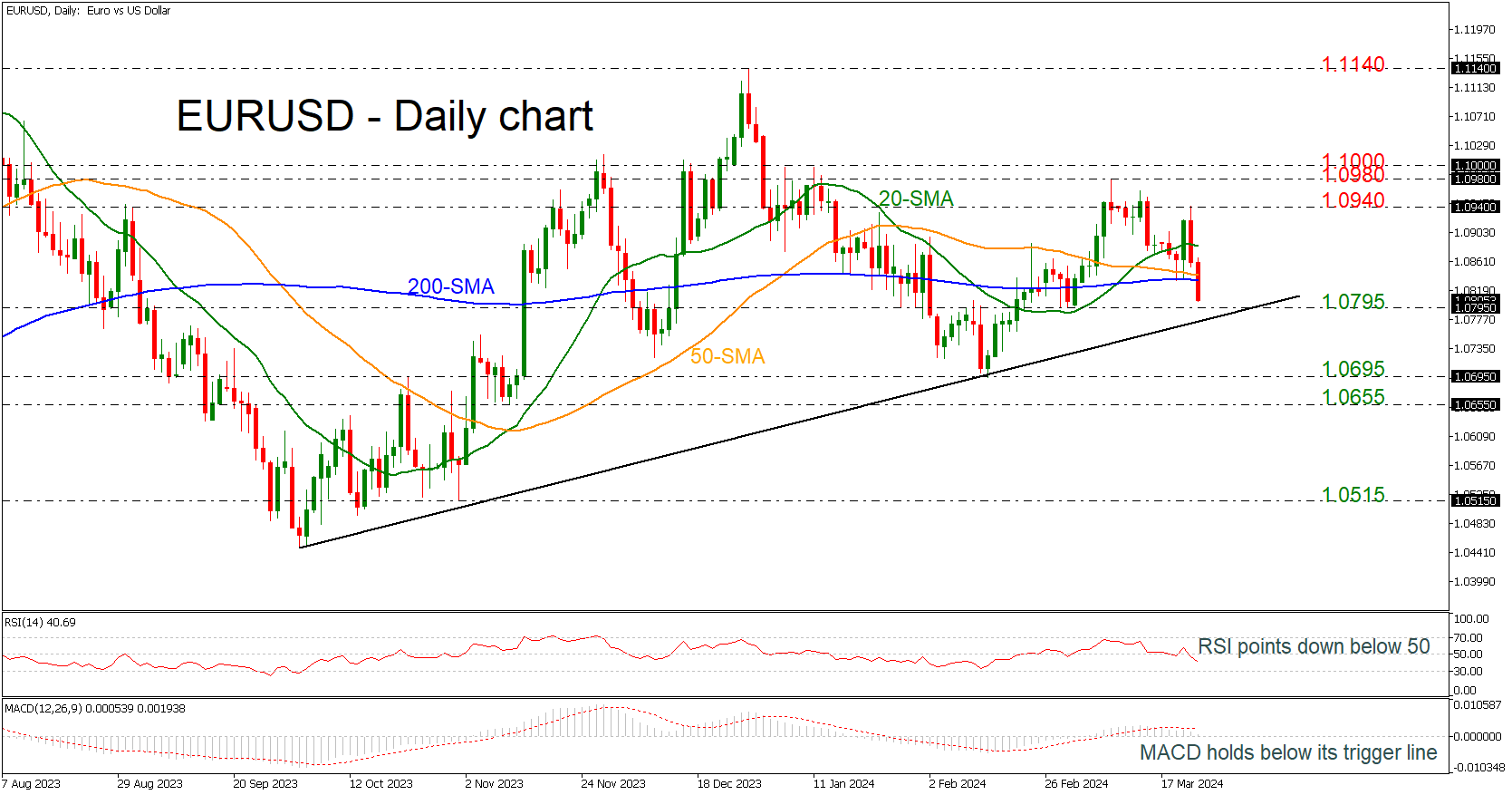

EURUSD Dives Towards 1.0800

- EURUSD breaks SMAs to the downside

- Immediate support at rising trend line

- MACD and RSI suggest more negative movements

EURUSD is showing some strong selling interest over the last couple of days, following the pullback from the 1.0940 resistance level. The price is also falling beneath the 50- and the 200-day simple moving averages (SMAs) with the next support coming from the 1.0795 bar and the medium-term ascending trend line which may act as a turning point.

Looking at the technical oscillators, the RSI is pointing south, crossing the 50 level to the downside, while the MACD is losing momentum beneath its trigger line and near the zero level.

In case of a rebound near the ascending trend line, the pair may meet again the next resistance of 1.0940 ahead of the 1.0980-1.1000 restrictive region.

On the other hand, a successful drop beneath the diagonal line may change the broader outlook to a more neutral one, hitting the 1.0695 support level. Below that, the market may find some pushback near the 1.0655 hurdle before heading lower again.

Summarizing, EURUSD is looking bullish in the medium-term window, despite the latest bearish correction in the very short-term view.

Chinese and Japanese Officials Started Offensive to Prevent Further Currency Losses

Markets

The path of least resistance on yields markets on Friday still was south. Investors after Wednesday’s Fed meeting/press conference clearly saw the glass half empty, rather than half full. The dots suggested otherwise with both growth and inflation forecasts upwardly revised. However, markets drew ‘dovish comfort’ from the fact that the median dot for the 2024 rate path (narrowly) kept the ‘guidance for 75 bps cumulative rate cuts. At the same time, Powell didn’t show worry about the ongoing easing of financial conditions even as (dis)inflation was on a more bumpy path. He also suggested that the Fed’s dual mandate could bring it in a position where it, if labour market data were to deteriorate, can start cutting rates even before a full return to the 2% target has been achieved. Markets again fully consider the option of a first Fed rate cut in June (currently +/- 85%). US yields drifted further away from recent YTD top levels, losing 4.7 bps (2-y) to 7 bps (5 & 10-y). Question remains whether Powell’s ‘selective’ assessment of recent data (and of the dots) will be confirmed by the data and whether his soft view has the backing of a majority within the MPC. Looking at the distribution of the interest rate dots, we’re not convinced. Atlanta Fed president Bostic on Friday indicated that he only sees room for one rate cut this year as he is becoming less confident on inflation. European and UK yields declined in lockstep. German yields ceded between 4.8 bps (2-y) and 8.4 bps (30-y). UK yields eased between 5.6 bps (2-y) and 6.7 bps (10-y) as the focus within the BoE now fully turned to the timing of a rate cuts. We also take notice that the decline in yields this time didn’t really help equities (S&P 500 -0.14%, a tentative sign of fatigue?). On FX markets, the dollar remained in the driver’s seat. DXY returned north of 104 (104.43 close). EUR/USD came within reach of the 1.08 big figure (close 1.0808). USD/JPY lost a few ticks as markets were on alert for (verbal) interventions as the yen again neared multi-year lows (close 151.41).

This morning, Chinese and Japanese officials indeed started an offensive to prevent further currency losses. Japan’s vice finance minister of economic affairs this morning warned that current weakening of yen is not in line with fundamentals and is clearly driven by speculation. He concluded that authorities will take appropriate action against excessive fluctuations. USD/JPY eases marginally this morning (151.35). The yuan also rebounded back to the USD/CNY 7.20 area after breaking this key technical barrier last week as the PBOC via a strong fixing suggested its discomfort with a weaker currency. Today, the eco calendar in US and EMU only contains sector tier releases. Later this week, US data include consumer confidence and durable goods orders (Tues), jobless claims and Chicago PMI (Thurs) and the February PCE deflators (Friday). In EMU, members states from Wednesday on will release March CPI data. We look out however the ‘Powell bond rally’ has room to go. The technical picture for the dollar (DXY and EUR/USD) strengthens. A break below EUR/USD 1.0796 would open the way to the YTD low (1.0695).

News & Views

NBP governor Glapinski in an interview with the Financial Times held out an olive branch to prime minister Tusk. Tusk accuses PiS-appointee Glapinski of politically motivated rate cuts ahead of the October elections at a time when inflation was still way too high. His lawmakers have recently also drawn up charges for alleged wrongdoings related to unlawful buying (at the primary market) of government bonds and misleading accounting (projecting a sizeable profit - which turned into a loss eventually - for 2023, allowing the former PiS government to factor in a big dividend in its pre-election budget). The NBP governor denies all charges and said he understands that accusing the (previous) government and central bank of causing inflation was the easiest way to manage the election campaign. But with the ballot now over Glapinski calls for talks in a bid to end a feud that is hurting the country’s international image.

Slovakia’s Korcok pulled off a surprise victory in the first round of the presidential elections over the weekend. The pro-European former diplomat secured 42.5% of the votes vs the 37% for Pellegrini. Pellegrini is the leader of the Hlas party, which has joined a government coalition led by prime minister Fico and his Smer party in the wake of the October 2023 elections. Slovakia’s president can veto legislation and appoint government officials, judges and central bankers. With Pellegrini as head of state, the Fico-led government’s ability to push through an agenda that’s increasingly raising European concerns rises dramatically. The final presidential round will take place April 6.

No Major Data Releases Today – ECB President Lagarde and Fed’s Bostic and Cook Will Speak

In focus today

The week starts out without any major data releases today. ECB president Lagarde and Fed's Bostic and Cook will speak today.

Later this week we look out for local inflation prints from Spain, France, and Italy that will give clues of where we can expect the euro area HICP print on Wednesday next week to come in. The PCE inflation from the US is due on Good Friday. The Central Bank of Hungary will announce its monetary policy rate decision on Tuesday.

Economic and market news

What happened over the weekend

In Russia a terrorist attack took place Friday night near Moscow. More than 130 people are confirmed dead, and more than 180 persons were wounded in the attack. The Islamic militant group Islamic State has claimed responsibility for the attack, however, Kremlin seemed eager to involve Ukraine in at least being partly responsible for the attack. Ukraine as well as American intelligence service have denied that Ukraine had any role in the attack. Russian President Putin claimed Saturday that the attackers were caught trying to escape to the Ukrainian border, not mentioning Islamic State in connection with the attack.

In Poland, a Russian missile violated Polish airspace early Sunday. The violation happened after Russia launched a massive air strike between Saturday and Sunday broadly on Ukraine including Kyiv and the western Lviv region bordering Poland. Polish and allied aircraft were activated early on Sunday as a reaction. The Polish government has demanded an explanation from Russia.

In the US, President Biden signed a USD 1.2 trillion spending bill to keep the US government funded and avoiding a partial government shutdown, which did not come as a surprise. The bill was signed after Congress voted in favour of the bill early Saturday. These bills fund only the government and are separate from, for example, the package including further support to Ukraine.

What happened Friday

In the US, Fed's Bostic (voter) said that he now expects only one 25bp rate cut in 2024, instead of the two cuts he had projected earlier, sounding quite hawkish on inflation, saying that he is less confident than in December that inflation will fall to Fed's 2 percent target. The 2024 dot plot signals three rate cuts, in line with our forecast, with the Fed delivering the first rate cut at the May meeting.

In the euro area, ECB's Centeno said that "We are at the end of this inflationary process." "Inflation is back at levels below 3% - monetary policy has to follow that reality as is evident, and will do it." ECB's Scicluna spoke as well and would not leave out a rate cut already in April. Both have typically leaned dovish. We still consider June close to a done deal for the first rate cut.

In Germany, the March Ifo print rose more than expected to 87.8. Despite the higher than expected number, Ifo is still at a very low level indicating a weak German economy. The assessment of the current situation rose to 88.1 (cons: 86.8, prior: 86.9) and expectations rose to 87.5 (cons: 84.7, prior: 84.1). The rise in expectations and the business situation give some ray of light for the economy but we still expect it to be weak near-term likely with another quarter of negative growth in Q1 2024.

In Japan, the largest union group Rengō says average wage hike was seen at 5.25% after the second tally. This is only slightly lower than the first tally, indicating that wage growth is more broad-based and supporting the BoJ's narrative for exiting NIRP. That said, two tallies more are ahead and smaller businesses are not a part of the data yet.

Equities: Global equities were marginally lower last Friday, dragged down by US markets despite some of the US heavy-weight sectors such as tech outperforming and Nasdaq ending higher. Friday weakness did not change yet another strong week for equities, up 2%, with cyclicals outperforming defensives by 2%, momentum outperforming the market by 2% and min vol underperforming. Small cap was in line with large cap as the two narratives of 'soft landing' and 'high-for-longer' were basically a neck-to-neck last week. In the US on Friday, Dow -0.8%, S&P 500 -0.1%, Nasdaq +0.2% and Russell 2000 -1.3%. Asian markets are mostly lower this morning though India and China are both higher. US and European futures are mostly lower.

FI: The bond markets is becoming more convinced regarding the first rate cut from the global central banks after last week's central bank meeting. The consensus is gathering around June on the back of comments from both ECB and Federal Reserve. This also drove the rally on Friday where European bonds yields decline, Bunds outperformed EU semi-core and periphery as well as Bund ASW-spread which widened after the prolonged tightening.

FX: After an eventful central bank week last week that included both a historical rate hike (BoJ) and a rate cut (SNB) within the G10 sphere the most notable development was still the strengthening of the USD and the sell-off in the CNY. The 'greenback' ended the week as the clear winner in Major's space and EUR/USD is back to the 1.0800 level after having almost reached 1.0950 after the FOMC meeting. CNY fell sharply towards the end of last week amid speculations of the authorities allowing for a weaker CNY but this morning USD/CNY has fallen back towards 7.20 amid a lower-than-expected fixing. Both SEK and NOK had a poor week with EUR/SEK and EUR/NOK trading above 11.40 and 11.65, respectively.

Threat is the Only Way to Stop Yen Bleeding

The Bank of Japan’s (BoJ) decided to hike the interest rates for the first time after 17 years but the yen has been weakening since then, on fear that this would be a ‘one and done’ cut. As a result, not only that the yen bulls are nowhere to be found but some traders revised their USDJPY forecasts to 155 for the next 3 months, to 150 for the next 6 months and 145 for the next 12 months post the BoJ meeting. Last week’s BoJ meeting and the market reaction to the meeting was a complete disappointment for the yen bulls who thought that the long yen would be the trade of the year. Finally, authorities had to step in this Monday and warn against speculative moves. The yen is stronger this morning, the Nikkei is down by nearly 1%. The FX warnings could limit the seller’s appetite, but will unlikely bring the yen bulls back.

Up, up and away

The Federal Reserve (Fed) policymakers didn’t sound much concerned about the latest blip in inflation at their last week meeting. The latter sent the US 2-year yield lower, and the dollar weakened in the immediate aftermath of the meeting, but the dollar index rebounded to close the week at the highest levels since February as the strong US economic data brought the Fed doves to doubt the Fed’s ability to cut the rates as soon as in June.

This week, the US will reveal its latest GDP update for the Q4 and the US economy is expected to have grown more than 3% in the final quarter of last year. That’s down from near 5% growth the quarter before, but the number is well above average growth for an economy which is preparing to see its monetary policy loosen.

The US equity markets remain on a euphoric mode on the back of soft Fed and robust data. The S&P500 had a slow session on Friday, but the index had its best week of the year – and it hasn’t been a bad year so far! The index is up by 12% since the year started and nearly 30% since last October – on track for its biggest-ever advance since 1970 ahead of a likely policy easing cycle according to Bloomberg. You bet it is, look at the Fed’s balance sheet, worth more than $7.5 trillion as of today.

And the stats are in favour of a further rise for the S&P500. Over the past 12 rate-cut cycles, the S&P500 climbed 15% on average – again according to Bloomberg. The positive trend is also true for sovereign and corporate bonds. Two major themes emerge into Q2: rate cuts and the AI adoption – both are favourable for stock valuations.

In Europe, the stocks had a record-breaking week, as well. Despite mounting headaches regarding the European luxury stocks and European Central Bank (ECB) Chief Lagarde’s warning that they can’t commit to more rate cuts beyond a June cut – which now sounds like an evidence – the Stoxx 600 advanced and closed the week above 500. In Switzerland, the SNB cut rates in a surprise move. The franc weakened and the SMI also extended gains last week. In contrast to the American and the European stocks, the Swiss equities are well below their post-pandemic peak. But given that around 90% of the SMI revenues are made abroad, a softer franc should clearly help the Swiss stocks healing from an extended period of strong franc. As per franc, there is room for depreciation. The dollar-franc tests the 0.90 psychological resistance to the upside. This is also the major 38.2% Fibonacci retracement on 2022 to end of 2023 drop. The pair will step into a medium term bullish consolidation zone above this level, but the franc’s weakness will be limited by the dovish outlook of its major peers. Against the euro, the parity is the most plausible target but again, franc depreciation will likely be slow and gradual.

This week, some Eurozone countries will reveal their latest inflation figures this week, but the aggregate number is not due before next Wednesday. The EURUSD has been having a rough time despite a more dovish Fed decision and a more hawkish ECB vibes. But I still think that the dollar’s strength will be limited by the dovish Fed talk and that the EURUSD will see support near 1.08 and rebound.

On the corporate calendar, Reddit and Galderma were the biggest IPOs of last week. Both went relatively well as conditions were ideal for a first day. And this week, Trump’s Truth Social will become a publicly traded company by as early as this week according to the latest news. The shareholders of DWAC approved the merger last week. TMGT – Trump Media and Technology Group – will replace DWAC. Note that DWAC has been subject speculation and high volatility since Trump is back on the political scene. Those who like risk and speculation will be well served.

Analytical RBA Interest Rate Predictions in 2024 and Beyond

In an era of economic recalibration, the Reserve Bank of Australia's (RBA) interest rate decisions are in the spotlight. This FXOpen article delves into analytical predictions for RBA interest rates through 2024 and beyond, offering insights into the factors shaping Australia's monetary policy. The insights and forecasts that follow are aimed at helping traders, investors, and the public seeking to grasp the future of Australia’s economic landscape.

Current Australian Interest Rate Environment

At the time of writing, on the 19th of March, interest rates in 2024 in Australia stood at 4.35%, a decision orchestrated by the Reserve Bank of Australia. This rate, also known as the cash rate, is pivotal, influencing borrowing costs, the Australian dollar's value, and overall economic momentum.

This rate reflects a significant shift from the era of historically low rates seen between 2013 and mid-2022. The 2010s were a period of relative economic stability in Australia, with interest rates falling from 3% in 2013 to 0.75% at the end of 2019. As the COVID-19 pandemic set in, the RBA slashed rates further to support economic growth. By the end of 2021, rates fell to a record low of 0.1%.

As the pandemic's impact waned and Australia's economy embarked on a recovery path, the RBA initiated a series of rate increases to normalise economic conditions. This shift was evident as the cash rate climbed from 0.1% in May 2022 to 3.1% by the close of 2022, signalling a move to temper inflationary pressures without derailing economic recovery.

Inflation, indeed, has been a central concern for the RBA. Annual inflation rose sharply from 1.1% in Q1 of 2021 to a multi-decade high of 7.8% in Q4 2022. With the goal to steer inflation back to its target range of 2–3%, the central bank's strategy has been to manage inflationary pressures through rate adjustments. This strategy is taken through the lens of the RBA's commitment to economic stability, with a keen eye on both global economic trends and domestic demand and labour market conditions.

As of early 2024, the RBA's monetary policy stance remains cautious yet responsive. Despite easing cost pressures in Australia, inflation continues to hover above desired levels—at 4.1% per Q4 2023’s reading—prompting the RBA to maintain the cash rate at 4.35% at its most recent meeting in March 2024.

Interested in seeing how these dynamics affect Australian markets, like AUD/USD and the ASX 200? Head over to FXOpen’s free TickTrader platform to access real-time data and interactive charts.

Economic Analysis and Australian Interest Rate Forecasts from Leading Analysts for 2024

Analysts forecast the economic trajectory of Australia in 2024 to be a nuanced blend of initial restraint followed by a gradual relaxation of monetary policy. The first half of the year is expected to remain under the influence of the RBA’s existing monetary stance, with the cash rate held steady at 4.35%. This approach is indicative of the RBA's intent to carefully navigate between controlling inflation—which has been a persistent challenge—and not stifling economic growth.

Inflationary pressures, especially from the services sector, continue to be a significant concern for the RBA despite a faster-than-anticipated decrease in goods price inflation. The RBA forecast for trimmed mean inflation has been adjusted to 2.8% for the calendar year 2025, hinting at cautious optimism about achieving the inflation target. However, the services sector's resistance to price reductions underscores the complexities in the path to disinflation.

Domestically, several factors contribute to a restrained economic outlook for the early part of 2024. Consumer spending is forecasted to face challenges exacerbated by a fall in real household disposable income and a significant reduction in the household savings ratio to 1.1%. The sensitivity of the Australian economy to interest rate changes due to the prevalence of variable-rate mortgages amplifies the impact of the current monetary policy stance.

Moreover, the anticipated slowdown in population growth due to a decline in net overseas migration after a surge in 2023 is seen as likely to moderate one of the key growth drivers from the previous year. However, this does not alleviate the pressures on the housing market, characterised by low stock and high rental costs, which are expected to persist as significant economic constraints.

On the global front, Australia's economic outlook is further clouded by uncertainties, including potential geopolitical tensions and their impact on trade routes and energy prices. Specifically, any escalation in the Red Sea region could have broad implications for global trade and, by extension, the Australian economy. Additionally, the economic situation in China, particularly concerning its property sector and debt levels, poses indirect risks to Australia's economic stability.

Despite these challenges, the latter half of 2024 holds the potential for a more positive economic shift. The RBA's stance, as of February 2024, remains open to adjustments based on evolving economic data and risks. This flexibility suggests that monetary policy could lean towards easing should inflationary pressures subside as forecasted and economic conditions warrant. Tax cuts, real wage growth improvement, and an overall uplift in sentiment are expected to contribute to a recovery phase, enhancing domestic demand and potentially easing some pressures on household finances.

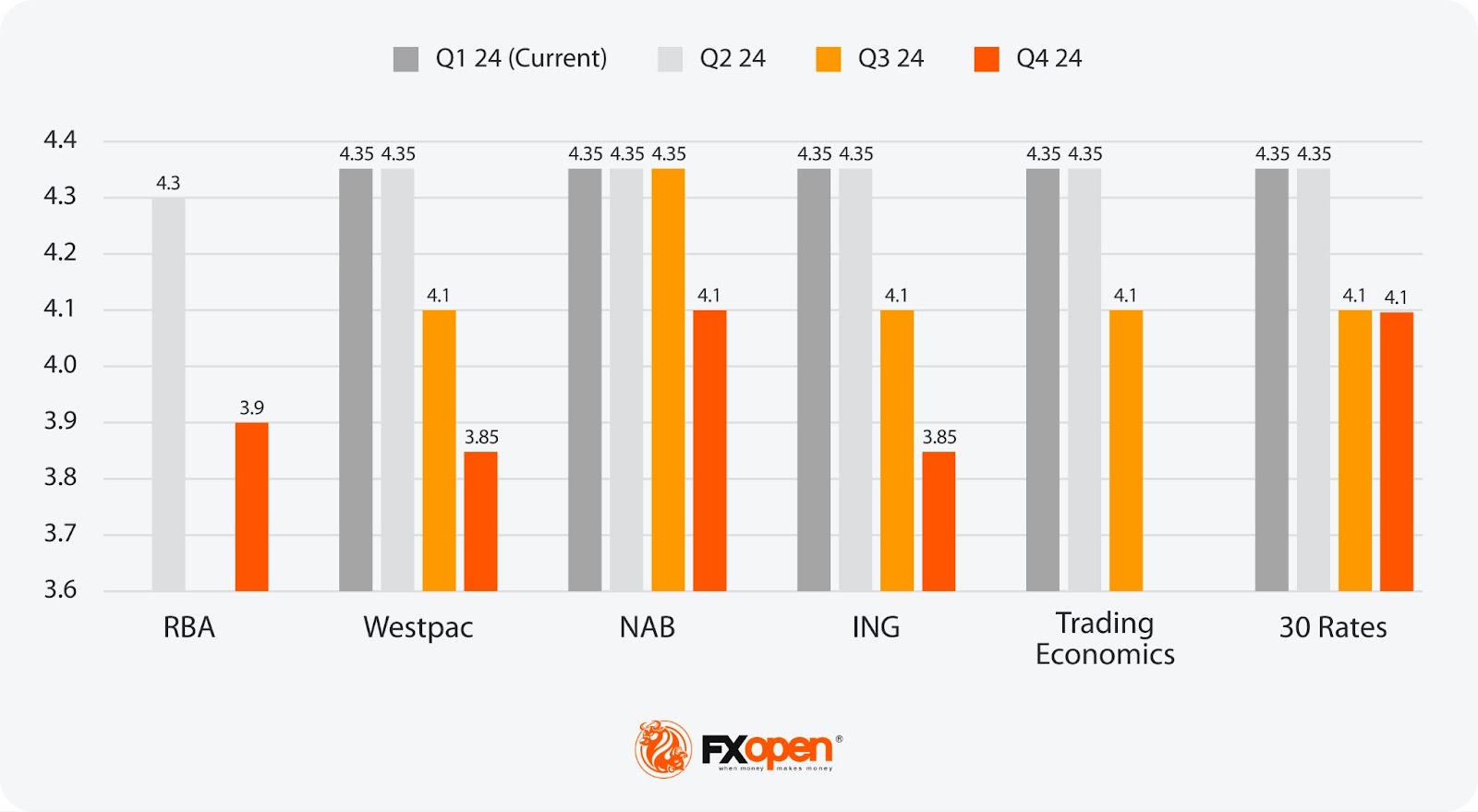

2024 Australian Interest Rate Predictions from Analysts

- Highest/Lowest Projection for Q2 2024: Consensus lies at 4.35%.

- Highest Projection for Q4 2024: NAB and 30 Rates both put Q4 Australian interest rates at 4.1%.

- Lowest Projection for Q4 2024: RBA, Westpac, and ING see rates declining to 3.85%.

Note: RBA projections are rounded to one decimal place.

Australian Interest Rate Forecasts in the Next 5 Years from Analysts

As we look towards interest rate predictions in the next 5 years in Australia, the RBA’s strategic focus on inflation control and economic stabilisation is expected to heavily influence their trajectory.

Looking to 2025, inflation is projected to align more precisely with the RBA's target range of 2-3%, with aspirations to reach the midpoint by 2026. This outlook hinges on an anticipated moderation in inflation, particularly noted in the quicker-than-expected decline in goods price inflation, despite services inflation maintaining a steadfast pace.

Given this backdrop, the period extending from 2025 onwards is set to be characterised by a cautious yet optimistic trajectory for interest rates. The RBA's monetary policy stance through the middle of 2024, which expects the cash rate to hover around its current level, serves as a precursor to potential easing as inflationary pressures wane. However, the path towards easing is complex, with several domestic and international variables at play.

Domestically, economic growth is forecasted to pick up from the latter part of 2024, carrying momentum into 2025. This resurgence is attributed to an expected relief in inflationary pressures and an improvement in household incomes, which could rejuvenate household consumption and, subsequently, economic growth.

Nonetheless, the labour market's dynamics, with nominal wage growth expected to stabilise, add layers to the interest rate discourse, emphasising the RBA's careful navigation between stimulating economic growth and maintaining inflation within target.

Internationally, the global economic landscape, particularly the synchronisation of monetary policies among advanced economies and geopolitical uncertainties, could influence Australia's economic prospects and, by extension, interest rate policies. The global economy's softer growth outlook may impact demand for Australian exports, thus affecting domestic economic conditions and the RBA's interest rate decisions.

Beyond 2025, interest rate predictions in Australia are influenced by the interplay between achieving sustainable economic growth and keeping inflation within the target range. The RBA's commitment to adjusting monetary policy in response to evolving economic indicators suggests a readiness to adapt to changing domestic and global economic conditions.

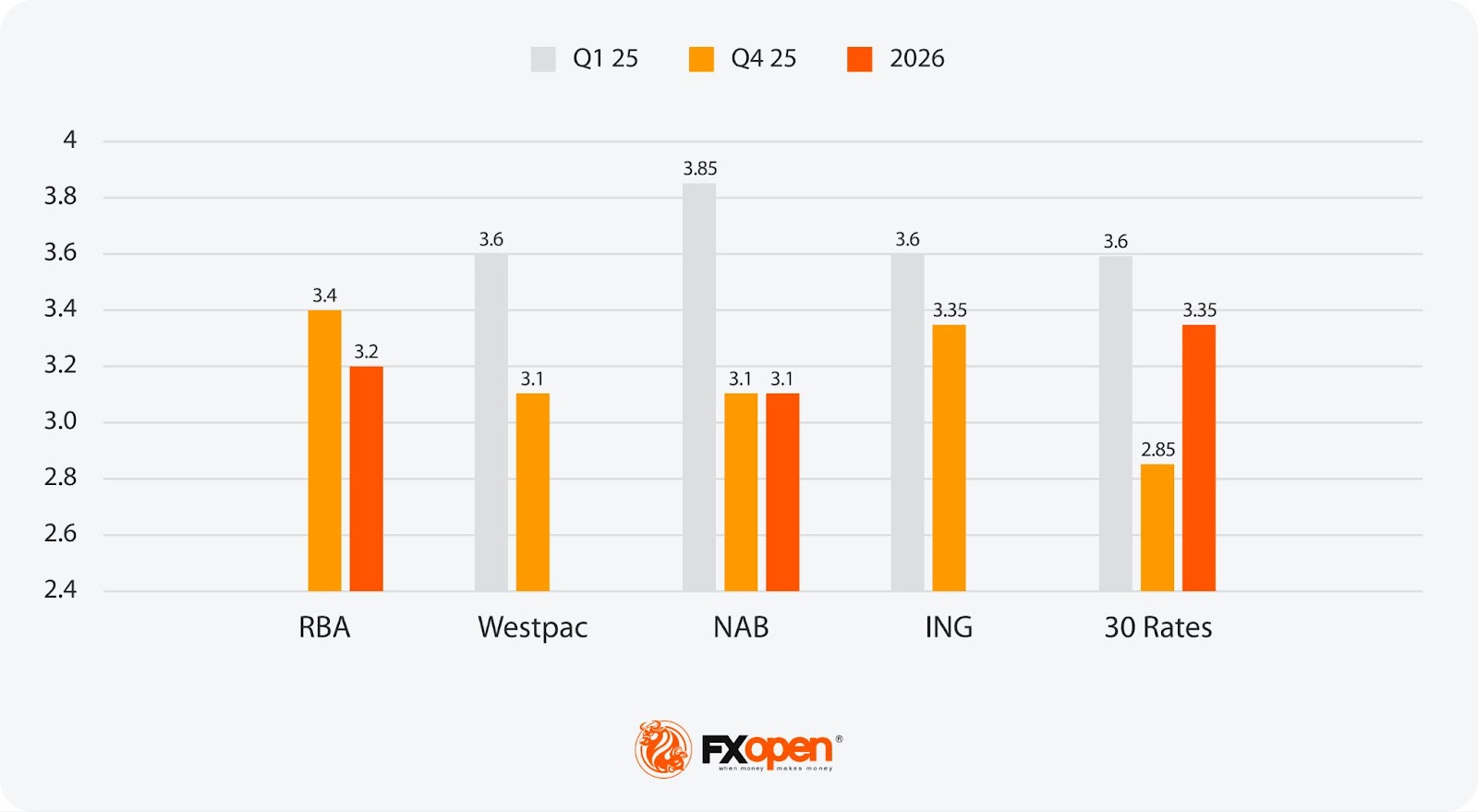

2025/2026 Australian Interest Rate Predictions

- Highest Projection for Q1 2025: NAB pegs Aussie rates at 3.85%.

- Lowest Projection for Q1 2025: Westpac, ING, and 30 Rates see rates falling to 3.60%

- Highest Projection for Q4 2025: RBA projects rates to stay relatively elevated at 3.4%.

- Lowest Projection for Q4 2025: 30 Rates anticipates a steep drop to 2.85%.

- Highest Projection for 2026: 30 Rates projects a rate hike from the end of 2025 to 3.35%.

- Lowest Projection for 2026: NAB puts 2026 Australian interest rates at 3.10%.

Note: RBA projections are rounded to one decimal place.

No predictions are available for 2027 onwards.

Factors Likely to Affect Future Australian Interest Rates

Australian interest rates are anticipated to be influenced by a myriad of factors in the coming years. The RBA will likely adjust its monetary policy in response to both domestic and global economic indicators to achieve its inflation and employment objectives. Key factors expected to impact Australian interest rates in the future include:

- Inflation Dynamics: Inflation is forecasted to move closer to the central bank's target range of 2-3% by 2025. The pace at which services and goods inflation moderates will be crucial in determining interest rate adjustments.

- Global Economic Conditions: Economic performance and monetary policy trends in major economies are projected to influence global demand for Australian exports, potentially affecting domestic interest rates.

- Domestic Economic Performance: Economic growth rates and consumer spending trends within Australia are expected to guide the RBA's policy stance, with efforts to stimulate or cool the economy as needed.

- Labour Market Conditions: Employment levels and wage growth are anticipated to influence domestic inflationary pressures, necessitating careful interest rate management by the RBA to maintain economic stability.

- Housing Market Developments: Given Australia's significant volume of variable-rate mortgages, the health of the housing market and lending practices are likely to have a direct impact on consumer spending and, consequently, interest rate decisions.

- External Shocks and Geopolitical Events: Unforeseen global events, including trade disputes and geopolitical tensions, are expected to pose risks to economic stability, potentially prompting the RBA to adjust interest rates in response.

The Bottom Line

Navigating the Australian economic landscape and interest rate environment from 2024 onwards presents a blend of cautious optimism and complex challenges. With the RBA's strategic focus aimed at inflation control and bolstering economic stability, the period up to 2029 hints at gradual adjustments rooted in evolving economic indicators.

For those keen on exploring opportunities in this dynamic environment, opening an FXOpen account offers a gateway to engaging with Australian financial markets, allowing traders to take advantage of anticipated shifts in Australian monetary policy via numerous assets, including currency pairs and indices, via CFD trading.

FAQs

How High Will Interest Rates Go in Australia?

Interest rates in Australia are expected to have peaked at the current rate of 4.35%. The Reserve Bank of Australia (RBA) has carefully navigated the economic landscape to manage inflation and support growth, with sources suggesting that the likelihood of further increases in the short term is low.

Will Interest Rates Keep Rising in Australia in 2024?

Interest rates are not anticipated to rise further in 2024. With the current rate considered to have reached its peak, the focus shifts towards maintaining economic stability and gradually adjusting policy as inflation aligns with target levels.

What Is the Interest Rate Forecast for the Next 5 Years in Australia?

Forecasts indicate a gradual decrease in interest rates from their current peak over the next two years. As inflationary pressures ease and the economy moves towards a more balanced growth trajectory, rates are expected to fall, reflecting the RBA's long-term monetary policy strategy. Longer-term projections aren’t currently available.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

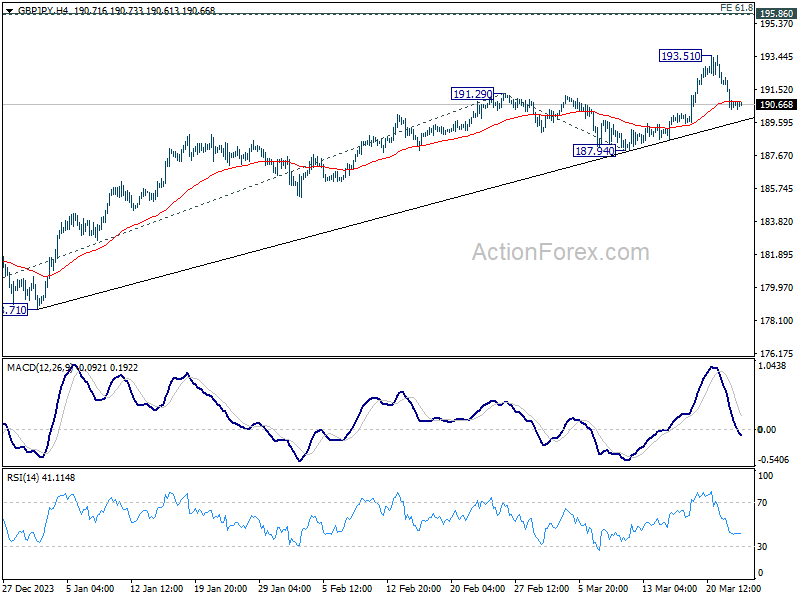

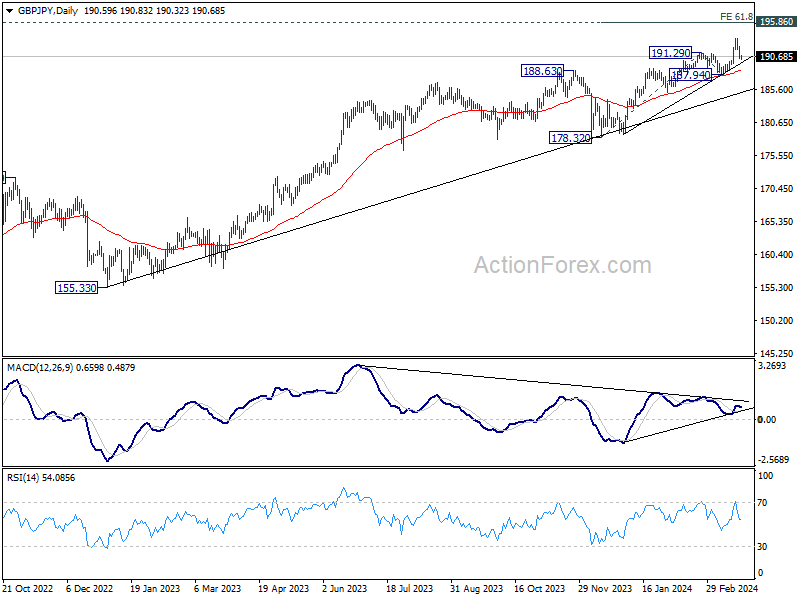

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.07; (P) 191.15; (R1) 191.92; More.....

Intraday bias in GBP/JPY stays neutral at this point and some more consolidations would be seen. Nevertheless, outlook will stay bullish as long as 187.94 support holds. On the upside, break of 193.51 will resume larger up trend to 61.8% projection of 178.32 to 191.29 from 187.94 at 195.95, which is close to 195.86 long term resistance.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

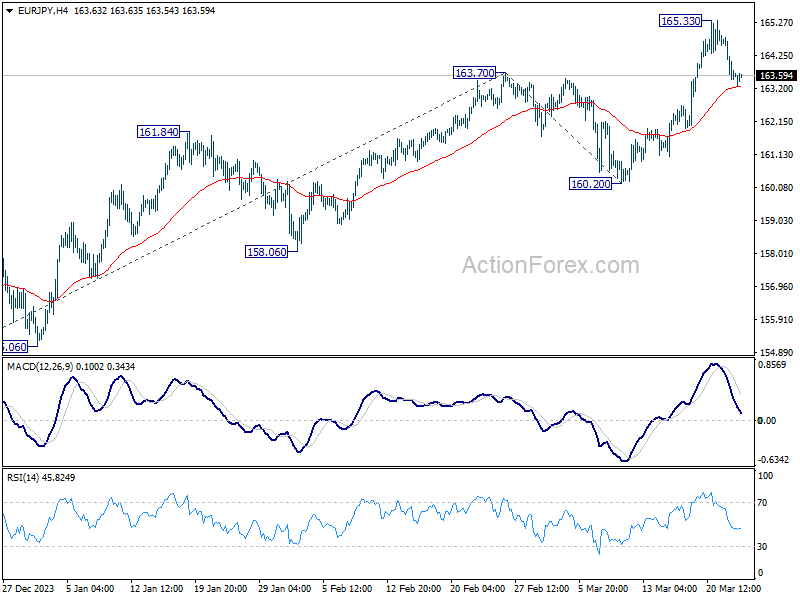

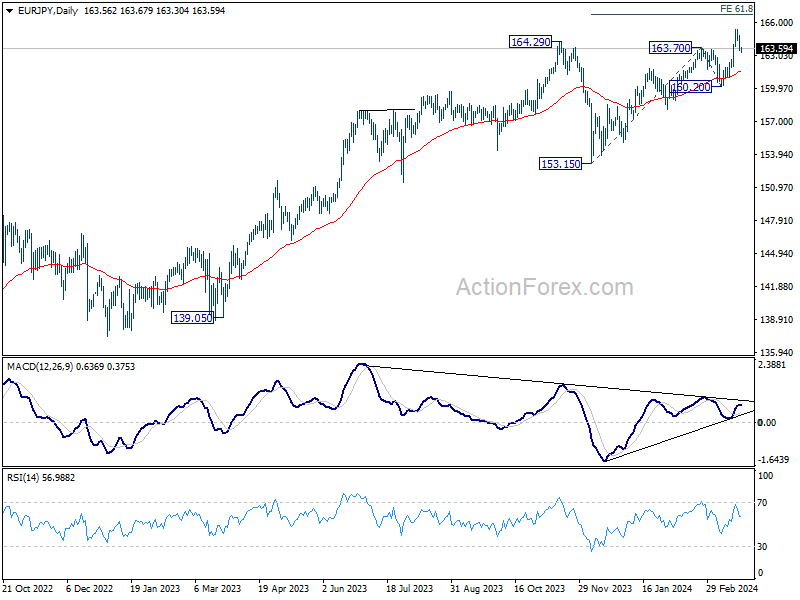

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.15; (P) 163.98; (R1) 164.48; More...

Intraday bias in EUR/JPY remains neutral for the moment. Downside of current retreat should be contained by 55 4H EMA (now at 163.27) to bring rebound. On the upside, break of 165.33 will resume larger up trend to 61.8% projection of 153.15 to 163.70 from 160.20 at 166.71. However, sustained break of 55 4H EMA will turn bias to the downside for deeper fall to 160.20 support instead.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

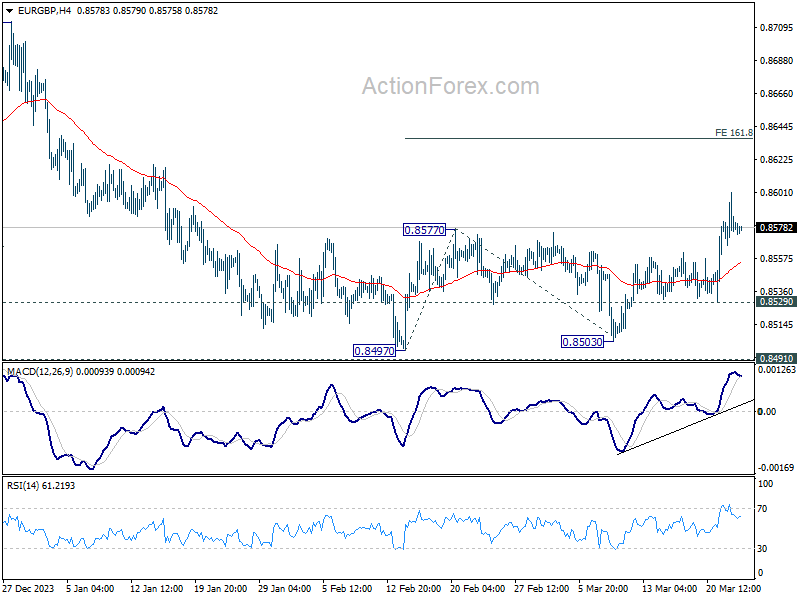

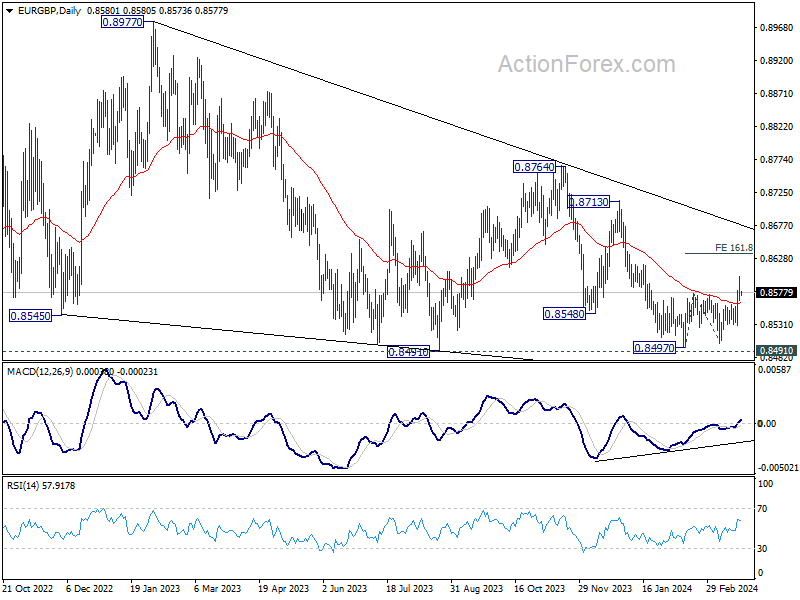

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8563; (P) 0.8583; (R1) 0.8597; More...

Intraday bias in EUR/GBP remains on the upside at this point. Rebound from 0.8497 is seen as at least correcting the fall from 0.8764. Further rally would be seen to 161.8% projection of 0.8497 to 0.8577 from 0.8503 at 0.8632. For now, further rise will remain in favor as long as 0.8529 minor support holds, in case of retreat.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8713 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

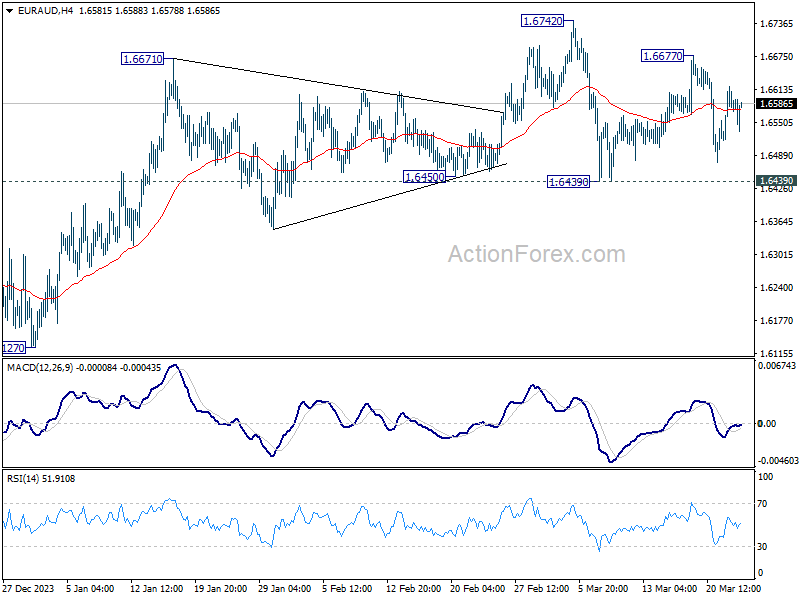

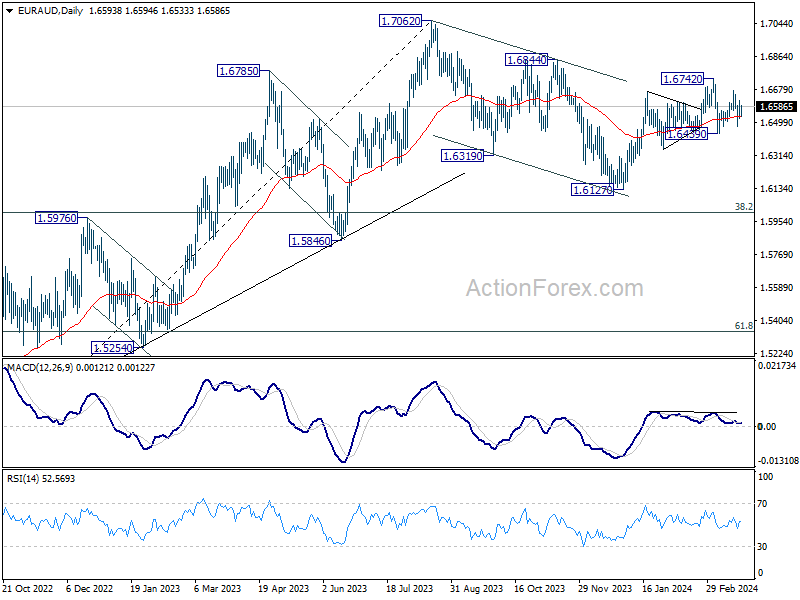

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6524; (P) 1.6572; (R1) 1.6643; More...

Intraday bias in EUR/USD stays neutral as consolidation continues in range of 1.6439/6742. Near term outlook will stay cautiously bullish as long as 1.6439 support holds. On the upside, above 1.6677 will target 1.6742 first. Decisive break there will resume whole rise from 1.6127 and target 1.6844 resistance next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

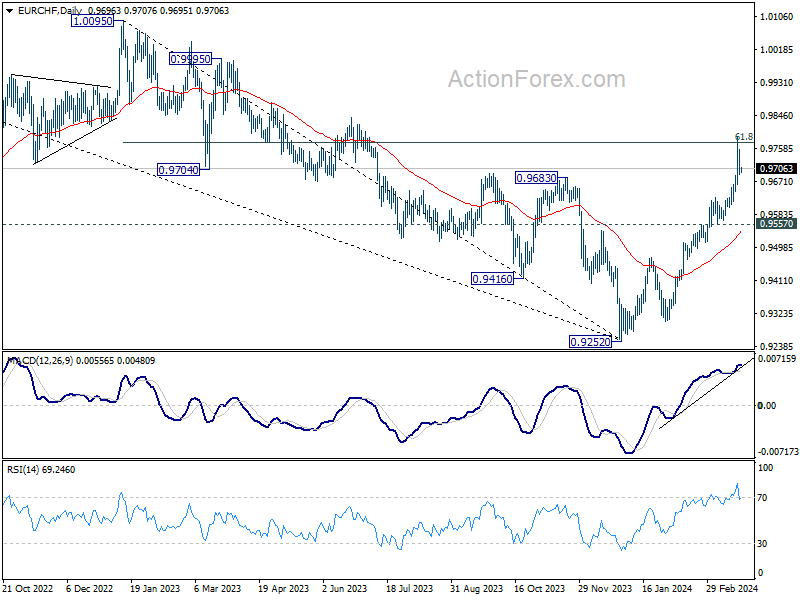

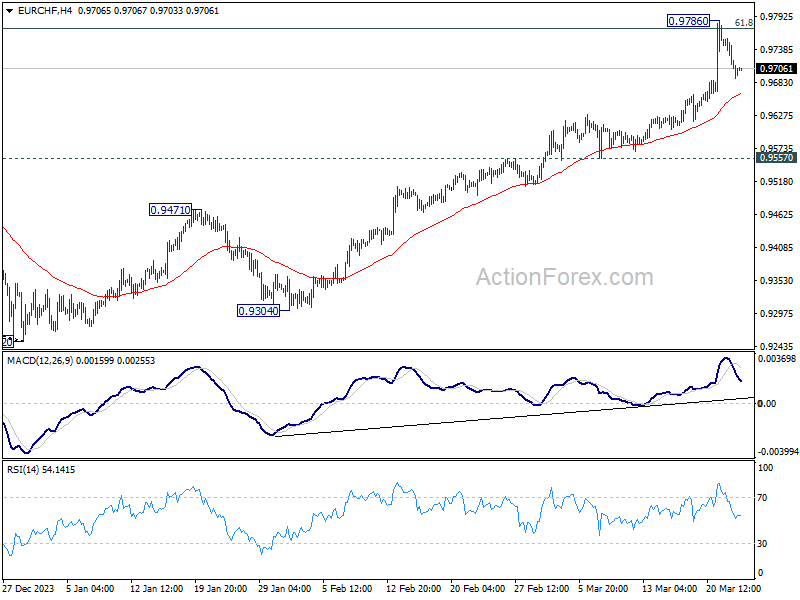

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9675; (P) 0.9716; (R1) 0.9740; More..

Intraday bias in EUR/CHF remains neutral for consolidations below 0.9786. Downside of retreat should be contained by 0.9557 support to bring rebound. On the upside, above 0.9786 will resume the rally from 0.9252 towards 1.0095 resistance next.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9535) holds.