Sample Category Title

Week Ahead – Markets Quiet Down After Central Bank Frenzy

- Dollar recovers after Fed selloff, turns to PCE inflation

- Yen falls despite rate increase, testing three-decade lows

- Quarter-end flows could disturb the waters in a quiet week

Dollar stages recovery after Fed

It was an action-packed week for FX traders, with five central bank meetings injecting volatility into the market. In a surprising move, the Federal Reserve continued to signal three rate cuts for this year, even though its new economic forecasts pointed to slightly hotter inflation and faster growth.

The overarching message was that the Fed will probably start cutting rates this summer, despite recent signs that inflation might be more persistent. In other words, the Fed seems willing to let inflation run hot for a while longer, to minimize the risk of a recession.

Investors reacted by selling the dollar, but the greenback managed to recover those losses to close the week higher overall, as other major currencies encountered their own problems and fell even harder. The euro was hammered by disappointing business surveys, while the pound slumped after the Bank of England softly opened the door for a summer rate cut.

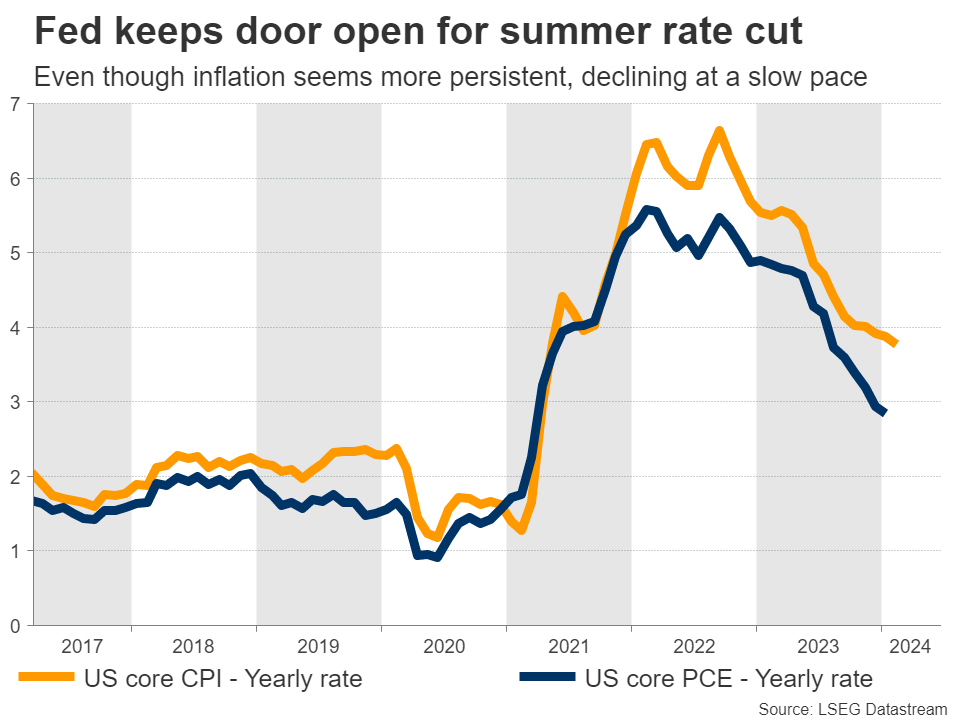

Next week, the ball will get rolling with US durable goods orders and consumer confidence on Tuesday. Of course, the main event will come on Friday, when the core PCE price index is released. Forecasts suggest the core PCE rate held steady at 2.8% in February, which would reaffirm that progress on the inflation front has stalled.

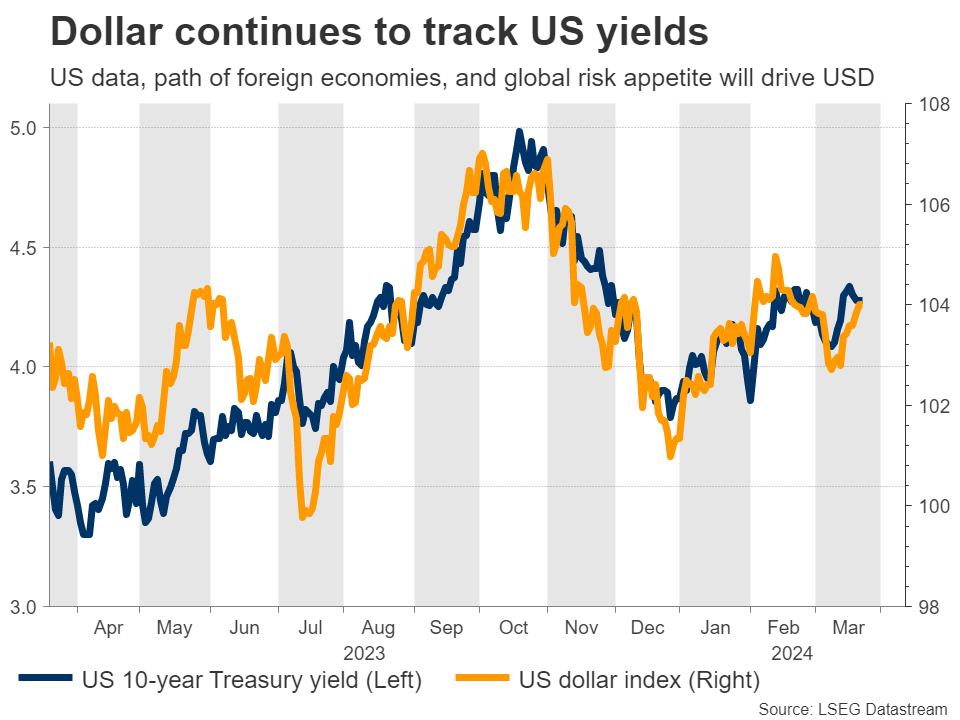

Beyond economic data, the performance of other major currencies and the evolution of global risk sentiment will also be crucial for the safe-haven dollar. In this sense, a persistent rally in the greenback might require a pullback in stock markets that fuels demand for haven assets, alongside more signs of weakness in foreign economies.

Note that Friday will be a public holiday in most major economies, so stock and bond markets will remain shut. The FX market will be open for business, but liquidity will probably be in thin supply, especially since it will also be the end of the quarter. In such an environment, sharp FX moves can happen without much news behind them.

Note that Friday will be a public holiday in most major economies, so stock and bond markets will remain shut. The FX market will be open for business, but liquidity will probably be in thin supply, especially since it will also be the end of the quarter. In such an environment, sharp FX moves can happen without much news behind them.

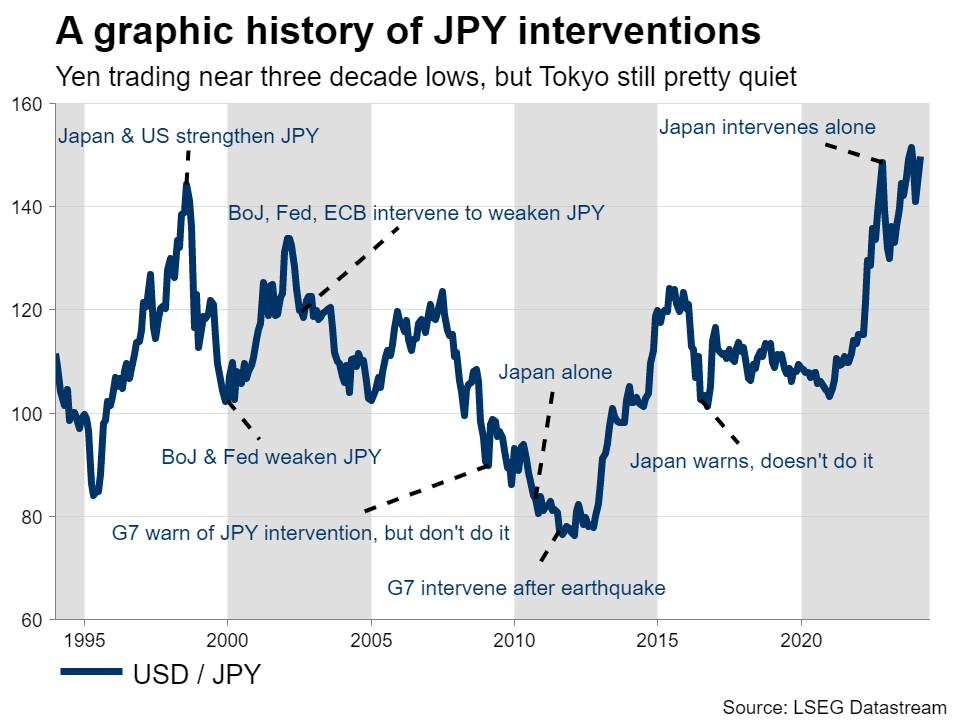

Yen gets smashed despite BoJ hike

Over in Japan, the yen collapsed towards its lowest levels in three decades, even after the Bank of Japan raised interest rates out of negative territory.

It seems the market was disappointed because the BoJ did not provide any clear signals about future rate increases. Investors are concerned this might have been a one-and-done move, especially since most other central banks are preparing to cut rates.

The summary of opinions from that meeting will be released on Thursday and will provide more color around the decision to raise rates, while on Friday, the latest CPI data from Tokyo will reveal what’s next for inflation nationwide.

As for the yen, it is trading very close to the 151.90 region against the dollar, which is a 34-year low. This area has been tested multiple times over the last two years, and Japanese authorities even intervened in the FX market to defend it, so it holds tremendous importance.

How the market behaves around this region will be telling. If it holds strong once again, that would leave some scope for a yen recovery in the spring, whereas a break would signal a resumption of the longer term downtrend. That said, a break would probably draw more FX intervention warnings from Tokyo, which could slow the pace of any selloff.

Australian inflation and Canadian growth

Crossing into Australia, inflation data for February will hit the markets on Wednesday and will provide clues on how soon the Reserve Bank might cut rates, which the markets are currently pricing for September.

Meanwhile in Canada, monthly GDP stats for January are due on Thursday. With the quarter almost over, this release is a little outdated, but could still attract some market attention. That said, the path of oil prices might be even more important for the oil-exporting Canadian dollar.

Weekly Focus – Historical Central Bank Week: A Hike and A Cut in G10

The past week will go down in history as the Bank of Japan (BoJ) hiked the policy rate for the first time in 17 years while the Swiss National Bank (SNB) cut its rate, becoming the first G10 central bank to do so in the current cycle. The BoJ decided to set the overnight call rate as its new policy rate and guided it in a range of 0.0-0.10% which finally marks the end of the era with negative policy rates. At the same time, it officially terminated yield curve control, although it promised to continue its bond purchases at broadly the same pace. The SNB cut the policy rate by 25bp to 1.50% in line with our call but clearly against consensus and market expectations. The cut came on the back of reduced inflationary pressures as well as the appreciation of the Swiss franc in real terms.

Both the Federal Reserve (Fed), Bank of England (BoE), and Norges Bank (NB) left policy rates unchanged, as expected. The Fed suggested that rate cuts are on the way, and the rate projections still showed three 25bp rate cuts for 2024 in line with our expectations. However, 2025, 2026 and longer-term 'dots' we revised slightly higher. The BoE maintained the Bank Rate at 5.25% as widely expected. Both the vote split in the committee, the statement, and comments from Governor Bailey were more dovish than previously, which sent EUR/GBP higher. Norges Bank unanimously decided to leave policy rates unchanged including the sight deposit rate at 4.50% as expected. Importantly, Norges Bank maintained the guidance for the first rate cut to come in September, which makes us postpone our call for the first 25bp rate cut from June to September.

On the data front, we got PMIs for the euro area, US, and UK. In the euro area, the composite PMI rose to 49.9 in March, indicating stagnation in the economy. Within the euro area, the service sector expanded with the PMI index at 51.1, while the manufacturing sector lagged at 45.7, particularly impacted by Germany. In the UK, composite PMI stood at 52.9, indicating economic growth, albeit with ongoing concerns regarding price pressures. In the US, PMI readings met expectations, with manufacturing rising to 52.5 and services remaining stable at 51.7.

We also got data from Asia where Chinese housing sales were slightly better than at the end of last year and industrial production had a decent start to the year. In Japan, February inflation came in 2.8% y/y as expected and "core-core" inflation at 3.2% y/y.

Due to Easter we will not publish weekly focus next week. However, there are plenty of important data releases during Easter and the week after. On Good Friday, we receive US February PCE inflation, and on Easter Monday we receive March ISM manufacturing. On Friday 5 March, we receive the US Job Report where we expect non-farm payrolls growth to slow to 180k and see average hourly earnings growth at 0.2% m/m SA. In the euro area, we focus on March inflation on 3 April. We expect both headline and core inflation remained unchanged at 2.6% y/y and 3.1% y/y, respectively. The sticky core inflation is due to strong service momentum and a base effect due to Easter. In China, focus is on manufacturing PMIs, and in Japan we look out for Tokyo inflation, wage growth figures, and the Tankan business survey.

Sunset Market Commentary

Markets

Wednesday’s Fed dots & Powell’s press conference brought a diffuse message, hampering an unequivocal market reaction. Higher/above neutral growth, a material uplift in especially this year’s inflation forecast and the unemployment rate holding below NAIRU contrasted with the interest rate dots confirming the scenario of 75 bps rate cuts this year. Powell at the same time stayed confident that inflation is on a gradual (admittedly bumpy) path to the 2% target. Interest rate markets and equities apparently are inclined to trade the second part. In a session deprived of data, US yields are falling between 4-5 bps across the curve, further extending the post-Fed decline going into the weekend. In the same vein, (US) equities are holding near all-time top levels. Powell apparently (unintentionally?) ‘convinced’ investors that financial conditions can stay…’easy for longer’. German yields follow the downdrift easing between 4.5 bps (2-y) and 7 bps (10 & 30-y). German Ifo business confidence printed better than expected (87.8 from 85.7), with both current assessment and expectations contributing to the improvement. Still, this doesn’t change markets’ view that the ECB will scale back tightening in June if (inflation and wage) data allow to do so. Even ECB’s Nagel again subscribed this scenario. UK gilts stay well bid too with yields easing 5-7 bps even as UK data this morning printed constructive. Retail sales avoided a setback (0.0% M/M) after a jump higher in January (3.6%). UK GFK consumer confidence also gave some comfort for spending going forward (-21 unchanged, but better prospects for personal finance). However, interest rate markets are driven by yesterday’s BoE policy pivot. The debate on a final rate cut is formally closed. BoE governor Bailey in an interview with the FT this morning even ‘approved’ market pricing with respect to (multiple) rate cuts later this year. Money markets are ever more embracing the option of a first BoE rate cut in June (> 80%) rather than August.

On FX markets, the dollar shows a mixed picture. EUR/USD traders apparently give some more weight to the higher-for-longer bias of the Fed dots. Combined with the ECB potentially frontrunning/outpacing Fed easing, makes EUR/USD vulnerable. The pair dropped to the 1.081 area intraday (currently 1.082). A break below 1.0796 would open the door for a return to the 1.0695 YTD low. In USD/JPY, technical considerations are at work. Today’s decline in US yields prevented a real attack/break of the multi-year top (151.95), trigger a modest setback (currently 151.25). However, Japanese officials probably stay on red alert as a break contains the risk of more unwarranted/disorderly yen losses. EUR/GBP briefly touched the 0.86 big future after leaving its 0.8850 peg post the BoE. However, momentum dwindled going into the weekend. Still, at EUR/GBP 0.858 the key 0.8500/0.8493 key support looks much better protected compared to a week ago.

News & Views

Hungary’s Economy Ministry yesterday announced it’ll remove a yield cap on bank deposits of some investors from April 1, saying it was no longer needed now that the central bank has halved the policy rate to 9%. The cap was one of a series of measures that sparked central bank outrage, saying they interfered with monetary policy. Just last week, the government also said it would phase out an interest-rate cap on loans of SMEs. With these rate caps the government sought to shield smaller and mid-sized companies from an aggressive central bank tightening campaign against soaring inflation. With the announcements following the decision to delay controversial plans to strengthen central bank supervision some weeks ago, there appears to be a thaw between the cabinet and the central bank. Markets, including the forint, are wary though. The Hungarian currency didn’t profit from the news yesterday and losses enlarge today. EUR/HUF moves beyond 396, turning the forint into the regional underperformer.

Businesses in Belgium gained more confidence in March. The headline indicator rose for a second month to -10.4, the highest since May of last year. The uptick was not across all sectors though. Confidence grew manufacturing with business leaders expressing much more positive demand and employment expectations. They also upgraded their order book assessments but were less positive about inventory levels. Business climate in the building industry improved as well, mainly on demand expectations. Sharply falling expectations for demand and for placing orders with suppliers triggered a retreat in the trade subseries. In business-related services, finally, a recovery in demand expectations was insufficient to compensate for a slump of expected activity levels.

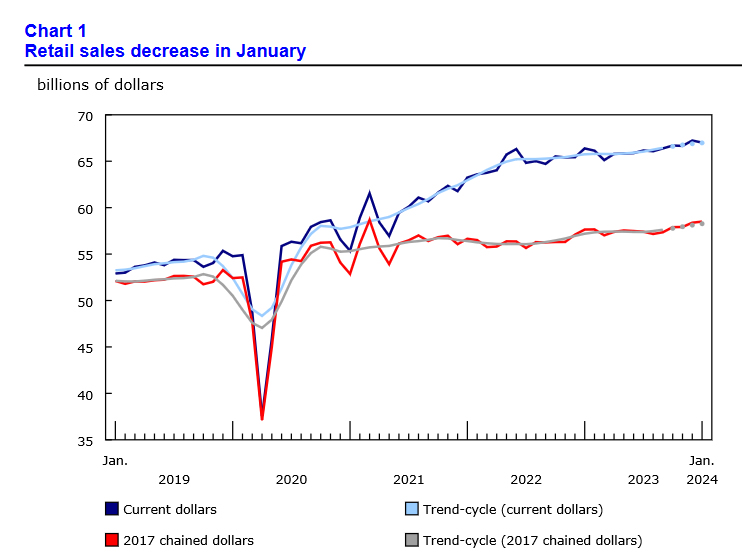

Canadian Dollar Dips as Retail Sales Disappoint

The Canadian dollar has extended its losses on Friday. USD/CAD is trading at 1.3569 in the North American session, up 0.29%.

Canada’s retail sales slip in January

Canada’s retail sales fell 0.3% m/m in January, revised from the earlier estimate of -0.4% and well off the 0.9% gain in December. The decline was driven by a sharp drop in motor vehicles and parts dealers (-2.4%).

The silver lining was that six of nine sub-categories showed an increase, which points to some strength in consumer spending. The estimate for February retail sales stands at 0.1%. Year-to-year, retail sales rose 0.9% in January, shy of the forecast of 2.5% and well off the December gain of 2.9%.

The retail sales data comes on the heels of the inflation report for February, in which inflation fell to 2.8% y/y. This was better than expected and the lowest rate since June 2023.

Core CPI, which excludes energy and food and is considered a better indicator of inflation trends, fell to 2.1% in February, which was lower than expected and the lowest level since March 2021.

With inflation continuing to fall toward the 2% target, pressure is growing on the Bank of Canada to lower rates and provide some relief to households, which are feeling the squeeze from elevated interest rates and the high cost of living.

The Bank of Canada has maintained the cash rate of 5.0% for six straight times and rates have likely peaked, although the BoC hasn’t signaled that it plans to lower rates.

The markets have priced in a rate cut in June at around 70% and other major central banks are moving in the direction of lowering rates. There is a 70% probability that the Fed will lower rates, according to the CME FedWatch tool, and the Swiss National Bank surprised with a rate cut on Thursday, the first major central bank to lower interest rates.

USD/CAD Technical

- USD/CAD tested resistance at 1.3577 earlier. Above, there is resistance at 1.3611

- 1.3518 and 1.3484 are providing support

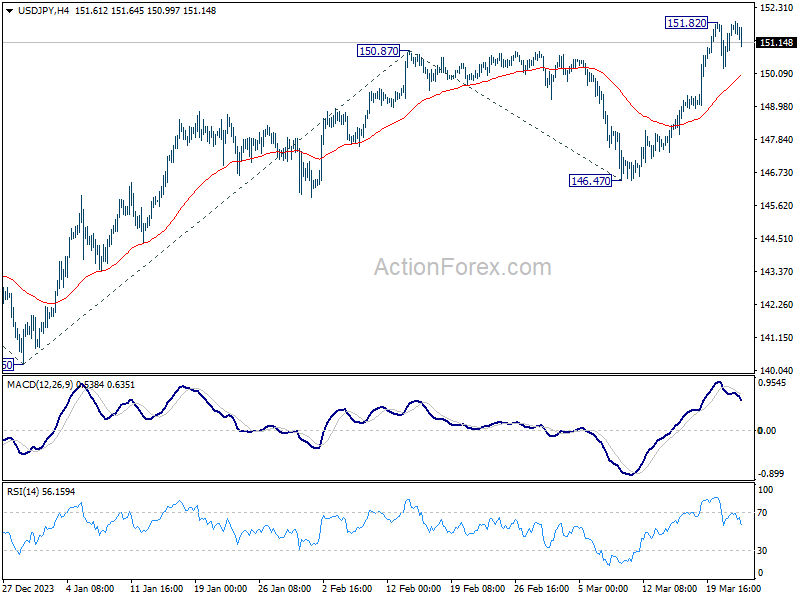

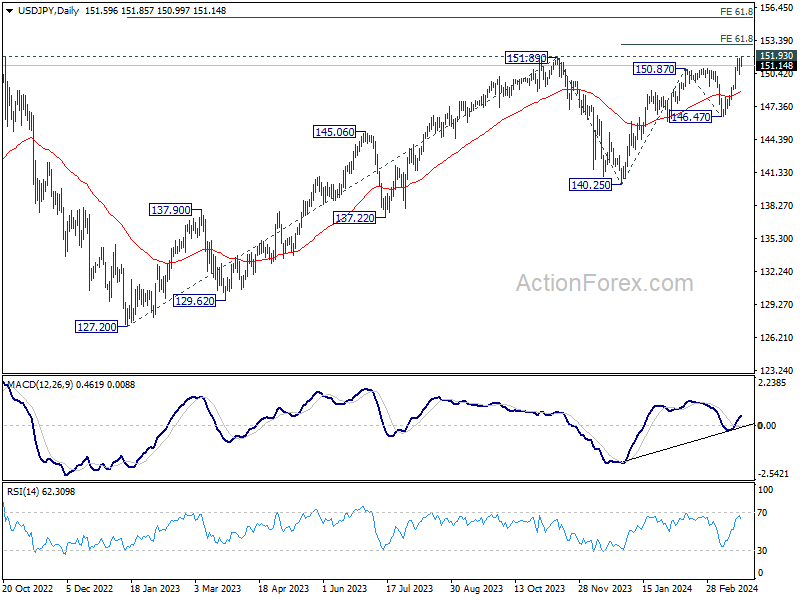

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.69; (P) 151.22; (R1) 152.18; More...

USD/JPY is staying in consolidation from 151.82 and intraday bias remains neutral. Further rally is expected as long as 55 4H EMA (now at 149.97) holds. On the upside, decisive break of 151.93 key resistance will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03. However, sustained trading below 55 4H EMA will bring deeper fall back to 146.47 support instead.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

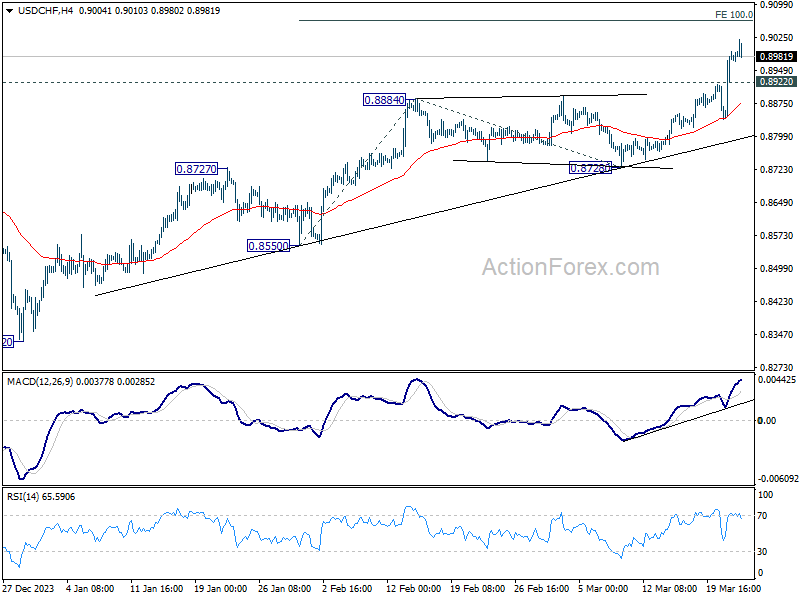

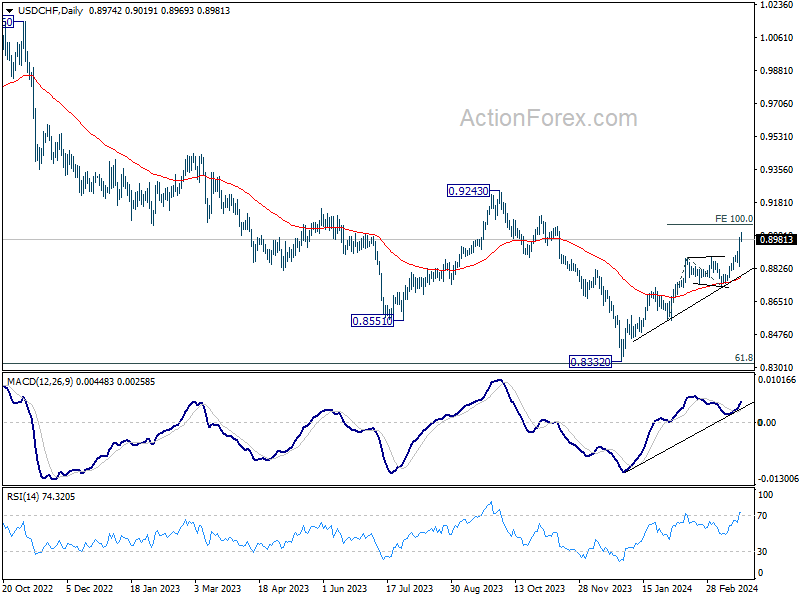

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8878; (P) 0.8936; (R1) 0.9033; More....

Intraday bias in USD/CHF remains on the upside for the moment. Current rally from 0.8332 is in progress for 100% projection projection of 0.8550 to 0.8884 from 0.8728 at 0.9062. On the downside, below 0.8922 minor support will turn intraday bias neutral again. But, outlook will remain bullish as long as 0.8728 support holds.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

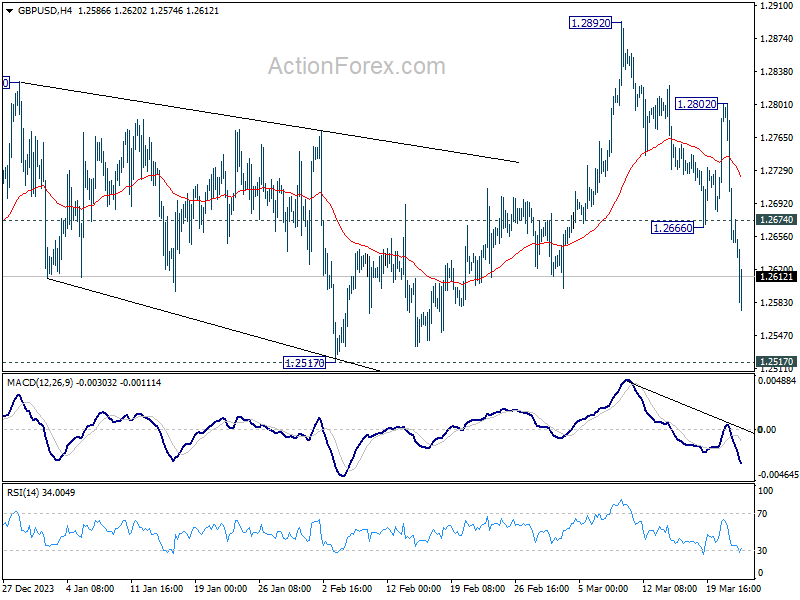

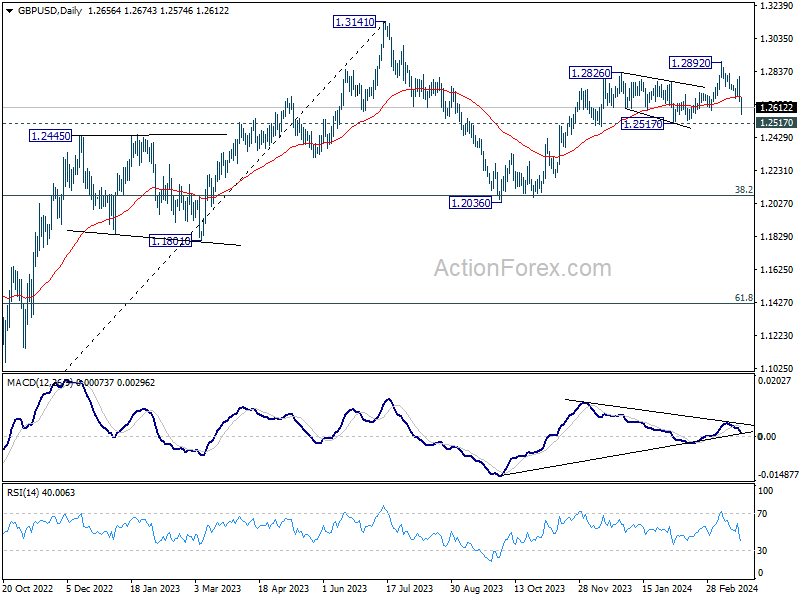

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2605; (P) 1.2704; (R1) 1.2757; More...

Intraday bias in GBP/USD remains on the downside for 1.2517 support Decisive break there will suggest that rise from 1.2036 has completed at 1.2892 already, and turn near term outlook bearish On the upside, above 1.2674 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

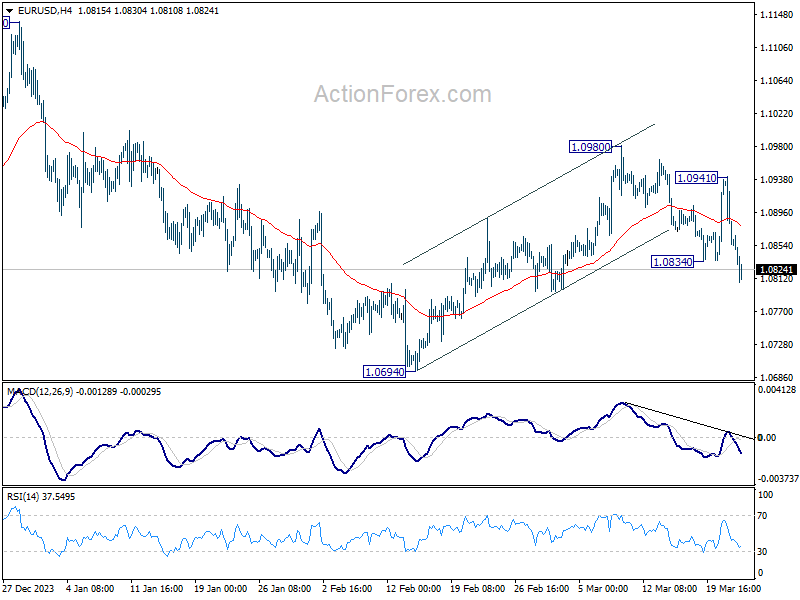

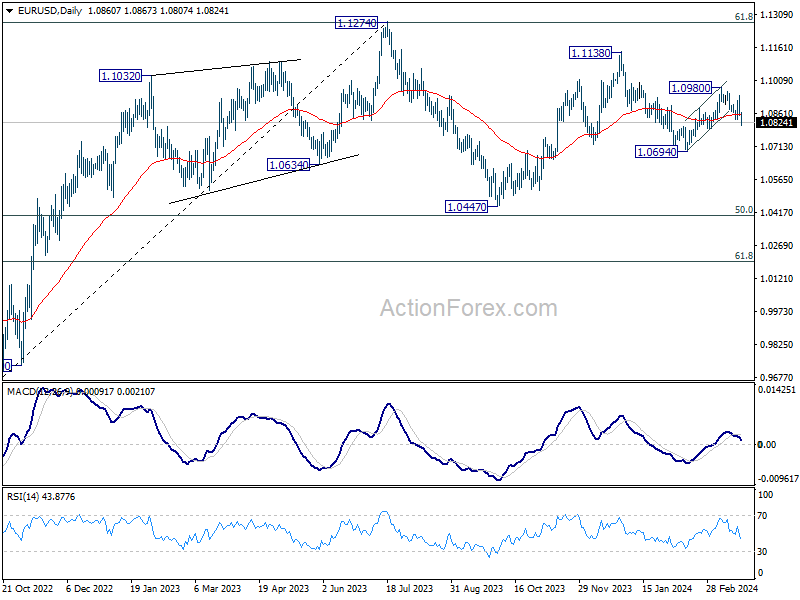

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0830; (P) 1.0886; (R1) 1.0917; More...

Intraday bias in EUR/USD remains on the downside at this point. Current development argues that corrective recovery from 1.0694 has completed at 1.0980 already. Deeper fall is expected to retest 1.0694 next. For now, risk will stay on the downside as long as 1.0941 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Yen Rebounds Amid Short-Covering, Dollar Rally Eases

Japanese Yen rebounds broadly today, likely driven by traders taking profits on short positions after a significant week of sell-off following BoJ's rate hike. This stabilization comes amidst speculations stirred by Japan's latest inflation data, raising the prospect of a second hike by BoJ in the second half of the year. Nevertheless, such predictions seem premature at this juncture. Additionally, the decline in benchmark yields from Germany and the UK has provided some support to Yen.

Meanwhile, Dollar is trading as the second strongest currency for the day, albeit with signs of losing momentum as the week draws to a close. This slight pullback could be attributed to profit-taking activities as well. In contrast, Australian Dollar and New Zealand Dollar are facing downward pressure, trading up as the day's underperformers. Both currencies face additional pressure due to the sharp decline in Chinese Yuan, which hit a four-month low. European majors present a mixed picture, with Sterling notably underperforming compared to its counterparts.

In Europe, at the time of writing, FTSE is up 0.46%. DAX is up 0.07%. CAC is down -044%. UK 10-year yield is down -0.075 at 4.039. Germany 10-year yield is down -0.067 at 2.344. Earlier in Asia, Nikkei rose 0.18%> Hong Kong HSI fell -2.16%. China Shanghai SSE rose 0.26%. Singapore Strait Times fell -0.07%. Japan 10-year JGB yield rose 0.0037 to 0.744.

Canada's retail sales falls -0.3% mom in Jan, led by motor vehicle and parts dealers

Canada's retail value fell -0.3% mom to CAD 67.0B in January, smaller than expectation of -0.4% mom decline. Sales were down in three of nine subsectors and were led by decreases at motor vehicle and parts dealers (-2.4% mom)

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were up 0.4% mom.

In volume terms, retail sales increased 0.2% mom.

Advance estimate suggests that sales increased 0.1% mom in February.

ECB's Nagel: June cut increasingly likely, but no automatism afterwards

In a webcast today, ECB Governing Council member Joachim Nagel indicated that the chance is increasing for a first rate cut "before the summer break" in August. However, he cautioned that afterwards, ECB will maintain a data-dependent approach and policy loosening wouldn't be on autopilot. "I do not see that there is a kind of automatism," he remarked. "It is data dependent and it is not a done deal that everything is going smoothly for the rest of the year or maybe for next year. So we have to be vigilant, we have to be cautious."

The ECB official flagged several "open issues" that warrant cautions, including the volatility in energy prices and the ongoing uncertainties surrounding wage growth and profit margins. "This meeting-to-meeting approach is the best way to address the current situation," he added.

German Ifo business climate rises to 87.8, glimpses light on the horizon

Germany's Ifo Business Climate Index rose to 87.8 in March, from the previous 85.7, surpassing anticipated 86.2. This uplift is mirrored in both Current Assessment Index, which advanced from 86.9 to 88.1 against expectations of 86.8. Expectations Index, which climbed from 84.1 to 87.5, outstripping the forecasted 84.7.

A closer look at sector-specific changes reveals significant variances: Manufacturing sector saw a substantial leap from -17.1 to -10.0. Services sector marked a positive turn, moving from -4.0 to 0.3. Meanwhile, the trade sector saw an improvement as its index rose from -30.8 to -22.9. However, the construction sector observed a slight decrease from -35.4 to -33.5,.

Ifo President Clemens Fuest encapsulated the sentiment by stating, "The German economy glimpses light on the horizon," highlighting a renewed sense of optimism among businesses.

UK retail sales volumes flat in Feb, sales value down -0.1% mom

In February 2024, UK's retail sales volumes remained unchanged month-over-month, a performance that's better than expectation of -0.3% mom decline. Meanwhile, sales value slightly dipped by a -0.1% mom.

A broader examination reveals -0.4% decline in sales volumes over the three months leading up to February, compared to the preceding three-month period. Additionally, a year-over-year comparison with the three months to February 2023 shows -1.0% decrease.

Japan CPI core rises to 2.8% in Feb, above BoJ's target for 23rd month

Japan's CPI core (ex-fresh food) rises from 2.0% yoy to 2.8% yoy in February, matched expectations. This increase marks the first acceleration in four months and maintains the index above BoJ's 2% target for the 23rd consecutive month.

The uptick in the core CPI was primarily due to a less pronounced decline in energy prices, reflecting diminishing impact of government subsidies introduced to mitigate energy costs. Specifically, energy prices saw a decrease of -1.7% yoy, a significant moderation from -12.1% yoy drop recorded in January.

The overall headline CPI also showed an uptick, accelerating from 2.2% yoy to 2.8%yoy. However, when examining CPI core-core, which excludes both food and energy, there was a slight slowdown from 3.5% yoy to 3.2% yoy.

New Zealand's goods exports rises 16% yoy in Feb, imports up 3.3% yoy

In February, New Zealand's goods exports leaped by 16% yoy to NZD 5.9B. This surge contrasts with a more modest 3.3% yoy increase in goods imports, totaling NZD 6.1B. Consequently, monthly trade deficit narrowed significantly to NZD -218m, far exceeding market expectations of a shortfall of NZD -825m.

Exports to China, New Zealand's largest trading partner, increased by 10% yoy, contributing an additional NZD 154m. US saw a remarkable 52% yoy jump in exports, adding NZD 305m, while EU and Australia also recorded increases in New Zealand exports by 7.9% yoy and 5.9% yoy, respectively. However, trade with Japan contracted, with exports declining by -10% yoy.

On the import front, China and South Korea marked significant increases of 7.1% yoy and 42% yoy, respectively, indicating robust demand for goods from these economies. Conversely, imports from US and EU saw downturns, declining by 20% yoy and 7% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0830; (P) 1.0886; (R1) 1.0917; More...

Intraday bias in EUR/USD remains on the downside at this point. Current development argues that corrective recovery from 1.0694 has completed at 1.0980 already. Deeper fall is expected to retest 1.0694 next. For now, risk will stay on the downside as long as 1.0941 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (MZD) Feb | -218M | -825M | -976M | -1089M |

| 23:30 | JPY | National CPI Y/Y Feb | 2.80% | 2.20% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Feb | 2.80% | 2.80% | 2.00% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Feb | 3.20% | 3.50% | ||

| 00:01 | GBP | GfK Consumer Confidence Mar | -21 | -20 | -21 | |

| 07:00 | GBP | Retail Sales M/M Feb | 0.00% | -0.30% | 3.40% | 3.60% |

| 09:00 | EUR | Germany IFO Business Climate Mar | 87.8 | 86.2 | 85.5 | 85.7 |

| 09:00 | EUR | Germany IFO Current Assessment Mar | 88.1 | 86.8 | 86.9 | |

| 09:00 | EUR | Germany IFO Expectations Mar | 87.5 | 84.7 | 84.1 | |

| 12:30 | CAD | Retail Sales M/M Jan | -0.30% | -0.40% | 0.90% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Jan | 0.50% | -0.50% | 0.60% |

Canada’s retail sales falls -0.3% mom in Jan, led by motor vehicle and parts dealers

Canada's retail value fell -0.3% mom to CAD 67.0B in January, smaller than expectation of -0.4% mom decline. Sales were down in three of nine subsectors and were led by decreases at motor vehicle and parts dealers (-2.4% mom)

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were up 0.4% mom.

In volume terms, retail sales increased 0.2% mom.

Advance estimate suggests that sales increased 0.1% mom in February.