Sample Category Title

Renminbi (USDCNH) Bullish Corrective Sequence Still Incomplete

In the last years, the renminbi made a pause in his attempt to get stronger against USD dollar. In February 2014, renminbi found support at 6.0153 as wave ((III)) and from there it made a perfect zig – zag correction structure to equal legs at 7.1964 in June 2020. After these 3 swings, USDCNH should have continued with the downtrend. However, the pair turning up again breaking 7.1964 high suggesting that market is developing a double correction structure.

USDCNH November 2023 Weekly Chart

In the chart above, looks like the first leg of the wave “c” ended as wave ((1)). Up from 6.6883 wave “b” low, we can see 5 swings higher creating an impulse. First wave ended at 6.9967. Wave (2) pullback at 6.8107 low. Then USDCNH rally finishing wave (3) at 7.2855. Wave (4) correction completed at 7.1162 low. Last push to 7.3679 ended wave (5) and wave ((1)). Currently, we are expecting a correction as wave ((2)) of “c”. This movement should drop to 7.12 – 6.95 area correlating with USDX weakness that we are looking for. After finishing wave ((2)), pair should rally in 3 swings to build an impulse as wave “c” to 7.4866 – 7.7646 area. This also will finish the double correction wave (y), and the wave ((IV)) before renminbi continues with the downtrend.

USDCNH March 2024 Weekly Chart

After 4 months, We can see a pullback as we expected. The drop in wave ((2)) ended at 7.08 in the 7.12 – 6.95 area and it has bounced higher. The reaction is not what we expected and pair looks like is lagging. Therefore, we are calling the possibility that structure ended at 7.08 could be wave (A) of ((2)), the bounce the wave (B) of ((2)) and we should see one more low to end wave ((2)) before resuming the rally to 7.4866 – 7.7646 area to complete wave ((IV)) correction.

USDCNH March 2024 Alternative Weekly Chart

As alternative view, we cannot rule out that wave ((2)) is completed at 7.08 and the pair should continue to the upside to end the double correction as wave ((IV)).

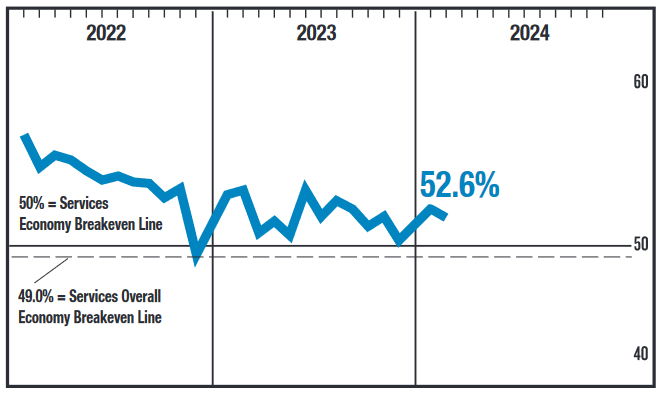

ISM Shows Services Sector Expansion Continued in February

The ISM Services index slipped to 52.6 in February from 53.4 in January, just shy of the 53.0 consensus expectation. However, growth did become more widespread, with 14 of 18 industries reporting growth for the month – up from ten in January.

The business activity sub-index rose to 57.2, while the new orders index ticked up to 56.1 from 55.0 in January.

The prices paid component tumbled 5.4 percentage points (pp) to 58.6 – giving up much of January's gain. The supplier deliveries sub-index fell to 48.9, indicating shorter delivery times compared to January.

The employment sub-component flipped back to signaling contraction, falling 2.5 pp to 48.0.

Key Implications

Another month of expansion in the service sector – albeit at a slightly slower rate than the consensus was expecting. However, there were some mixed signals under the hood, with employment falling short of expectations but new order growth firming in the month.

Despite the slight miss, the details of the report (new orders and business activity) continue to show solid, and broader, growth in the services sector. For Fed watchers, the interesting tidbits are in the employment, supply deliveries and prices indexes. Employment growth continues to trend lower (posting a second contractionary reading in three months), while improving supplier delivery times and a deceleration in prices paid growth suggest improving supply side conditions. Improvements on the supply side, and a loosening in the labor market, suggest inflationary pressure could ease in the coming months.

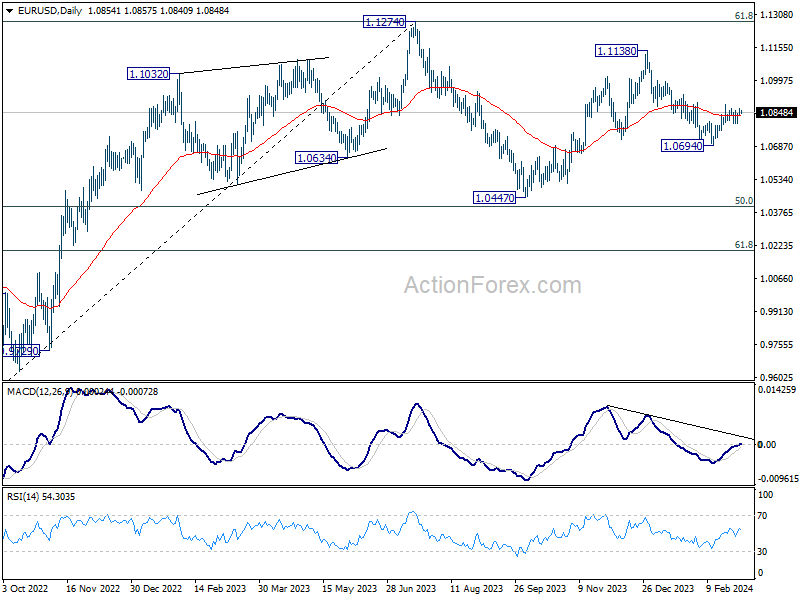

EUR/USD Shows Strength Amid Anticipation of Key Events

The EUR/USD pair is exhibiting resilience, navigating around the 1.0850 mark on Tuesday, following a sequence of rises in the previous two sessions. The current market atmosphere is one of cautious optimism, as participants brace for significant upcoming events, including a speech by Jerome Powell, the head of the US Federal Reserve, and the release of February's employment sector statistics on Friday. Particularly, the focus will be on the wage growth components for February, which are speculated to have nearly tripled, potentially indicating a diminishing impact of pro-inflationary factors.

The consensus among market observers is leaning towards an expectation that the Federal Reserve may initiate the first interest rate cut of this monetary cycle in June, with possibilities of further reductions occurring up to three times by year-end.

EUR/USD Technical Analysis

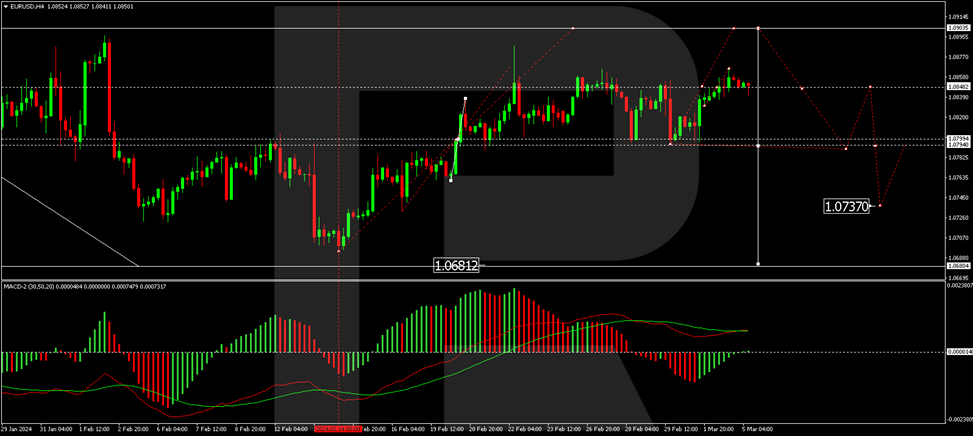

On the H4 chart, the EUR/USD pair is currently carving out a consolidation pattern around the 1.0831 level, with a recent extension up to 1.0866. A downward correction to 1.0831, testing the level from above, could materialize today. An upward break from this consolidation could herald the start of a growth wave towards 1.0900, at which point the current growth phase is anticipated to conclude, potentially giving way to a new downtrend with an initial target at 1.0680. This outlook is supported by the MACD indicator, which shows the signal line above zero and a sharply rising histogram, indicating a continuation of the growth trend.

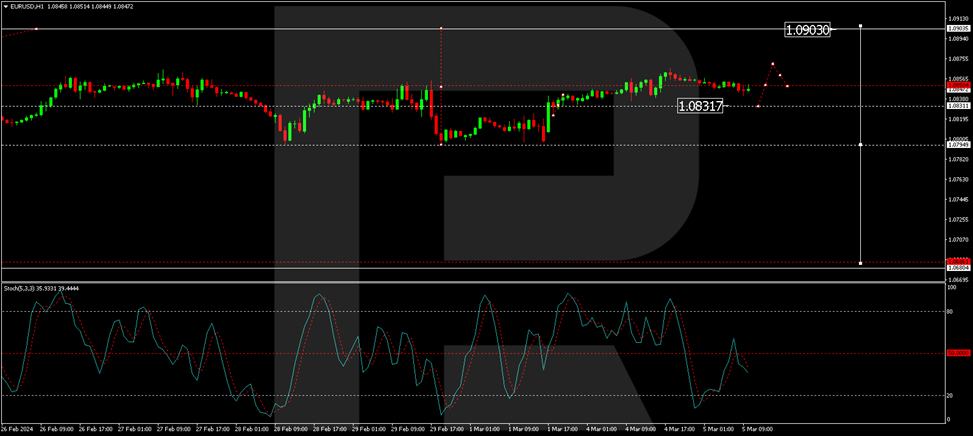

The H1 chart reveals a consolidation phase around the 1.0831 level, with a growth structure targeting 1.0870 currently unfolding. The local target of 1.0866 for this wave has been achieved, with a correction back to 1.0831 anticipated. Following this correction, the focus will shift towards the structure's growth potential to 1.0870. The Stochastic oscillator, currently below the 50 mark and expected to drop to 20, validates this scenario, suggesting a potential for further fluctuations within this bullish trend.

Sunset Market Commentary

Markets

It was a drawn-out stretch towards the publication of the US services ISM today (read about it down below). Core bonds in the meantime gained ground with US Treasuries in particular shaking off yesterday’s Bostic’s comments. The Atlanta Fed president warned for inflation risks from “pent-up exuberance”. That’s how he describes companies being ready to spend and hire when “the time is ripe” (read: when the Fed starts cutting rates). Should the Fed heed Bostic’s advice and pause after it cut rates for a first time in Q3, the December dot plot’s total of 75 bps (three cuts) is even beginning to look overly optimistic. Anyway, US yields drop between 2.9 and 6.2 bps with the long end outperforming. Losses in the 10-y yield for example extended after slipping below intermediate support area between 4.17% (200 daily moving average) and 4.18% (mid-February correction low). German Bunds outclass Treasuries. Yields print 4.8 (2-y) to 8.2 bps (30-y) lower in a similar curve shift. The drop in core bond yields helped gold to temporarily surpass the previous intraday record high of early December. In terms of closing prices, the shiny metal already set a new record yesterday following a curious two-day rally and is on track to hit another today. Stock markets struggle for direction. The EuroStoxx50 wavers some 0.2% from its post-GFC top while Wall Street returns 0.5-1%. Switching to currency markets, we note some JPY outperformance vs global peers – be it without technical implications. USD/JPY holds just north of 150, EUR/JPY eases a few ticks but hovers around recent highs at 162.8. Sterling is doing good despite gilt outperformance pushing yields more then 10 bps (10-y) lower. EUR/GBP inches lower to below 0.855 but with the broader stalemate in the pair not going anywhere.

The February US services ISM missed the headline reading of 53 by coming in at 52.6, a slightly bigger retreat from the 53.4 in January. Details showed employment dipping to 48 as the main culprit for the undershoot. New orders however unexpectedly expanded at a faster clip (56.1 from 55). The latter is coming on top of already strong business activity (rises from 55.8 to 57.2). That combination may well mean the employment setback is only temporary. Prices paid eased to 58.6, erasing part of the January uptick. All in all a good reading considering the underlying series. Yields in the US nevertheless lose a few more extra basis points in a first reaction, dragging German yields along.

News & Views

The German government coalition today proposed plans for supplementary pension scheme that should help to address the challenges to the funding of the pension system in the next decade. The new scheme will be funded both by loans and transfers from the federal budget. Investment in the fund should amount to €200 bln by the middle of next decade. From 2035, the proceeds from the fund should flow back to the pension system and mitigate the burden of the pension costs for employees and the government budget. From the mid-2030’s, €10 bln should annually flow from the fund to the pension system. The government intends to guarantee that pension payments can be kept at least at 48% of the average wage until end of the 2030’s. Additional measures should be taken to guarantee it beyond 2039, according to the government. The government wants the new measures to be approved in Parliament before summer.

Hungary today published details on Q4 GDP growth. Activity in the economy was unchanged both from the previous quarter as well as compared to the same quarter in 2022. The expenditure approach showed that households consumption rose by 0.8% Q/Q while government consumption decreased by 0.7% Q/Q. Gross fixed capital formation increased by 1.0%. With respect to external trade, both volumes of imports and exports decline respectively by 2.0% and 2.3%. In a production approach agriculture (+4.2%) and services contributed positively to Q4 growth. Activity in construction (-1.6% Q/Q) and industry (-1.9%) decreased in Q4. Overall in 2023, activity in the Hungarian economy was 0.7% lower (calendar adjusted) compared to 2022.

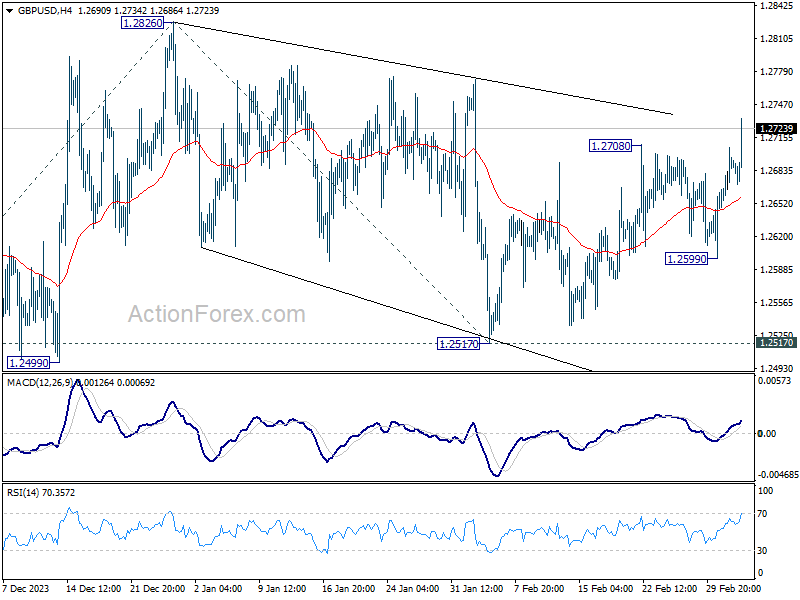

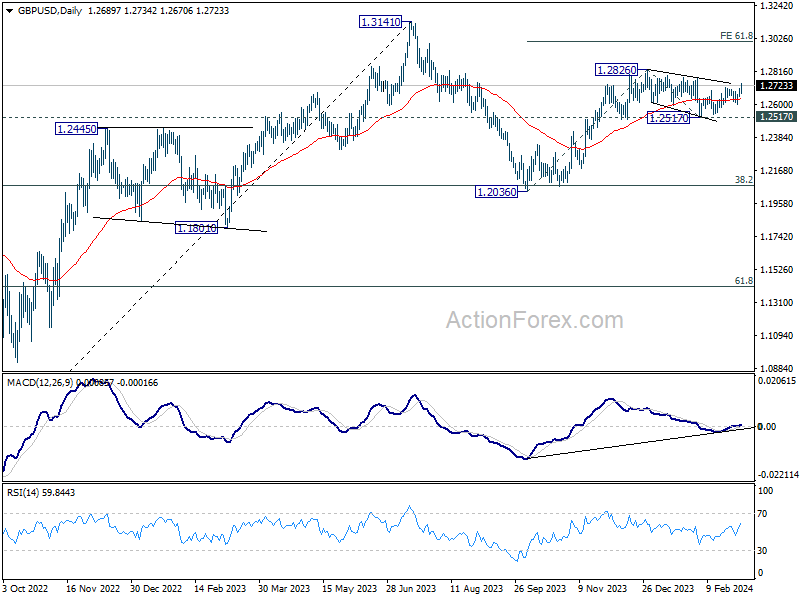

GBP/USD upside breakout after US ISM services miss

Dollar falls broadly after slightly lower than expected ISM Services PMI reading. But more importantly, employment component was back in contraction while price component dipped notably.

GBP/USD's rebound from 1.2517 resumed by breaking through 1.2708 resistance. The development argues that corrective from 1.2826 has completed at 1.2517 already. Further rise is now in favor to retest 1.2826 resistance first. Decisive break there will resume whole rally from 1.2517 to 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005 next.

US ISM services falls to 56.2, employment back in contraction

US ISM Services PMI fell from 53.4 to 52.6 in February, worse than expectation of 53.0. Looking at some details, business activity/production rose from 55.8 to 57.2. New orders rose from 55.0 to 56.1. Employment fell from 50.5 to 48.0, back in contraction. Prices fell from 64.0 to 58.6.

Anthony Nieves, Chair of ISM Services Business Survey Committee, said, "The slight decrease in the rate of growth in February is a result of faster supplier deliveries and the contraction in the Employment Index. The majority of respondents are mostly positive about business conditions. Respondents remain concerned about inflation, employment and ongoing geopolitical conflicts."

"The past relationship between the Services PMI and the overall economy indicates that the Services PMI for February (52.6 percent) corresponds to a 1.2-percent increase in real gross domestic product (GDP) on an annualized basis."

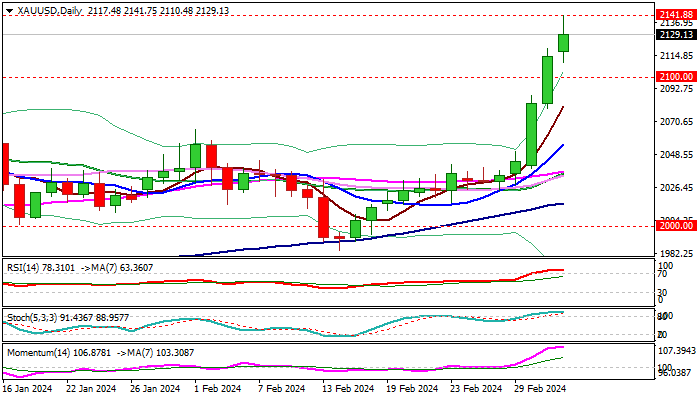

XAU/USD: Gold Retests Record High, Bulls Likely to Take a Breather Before Resuming

Steep rally extends into the fifth straight day on Tuesday, after the metal closed above $2100 level for the first time in history on Monday.

Strong demand for safe haven bullion was sparked by further drop in the activity in US manufacturing sector and persistently weak consumer sentiment.

Bulls retested key barrier at $2141 (gold’s record high, posted on Dec 4), break of which to spark fresh acceleration higher and open way for 2200+ gains.

Meanwhile, increased headwinds at this zone should be anticipated, due to significance of resistance and strong rejection seen after last rally to this level (Dec 4 bearish daily candle with very long upper shadow), as well as strongly overbought daily studies.

Dips should be limited (ideally to find ground at $2100/$2080 zone) to keep bulls intact and offer better levels to re-enter bullish market.

Res: 2141; 2181; 2206; 2226.

Sup: 2110; 2100; 2088; 2080.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0840; (P) 1.0853; (R1) 1.0870; More...

Range trading continues in EUR/USD and intraday bias remains neutral. On the upside, break of 1.0887 and sustained trading above 55 D EMA (now at 1.0831) will affirm the case that fall from 1.1138 has completed. Stronger rally would then be seen back to 1.1138. However, break of 1.0795 minor support will turn bias back to the downside for retesting 1.0694 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

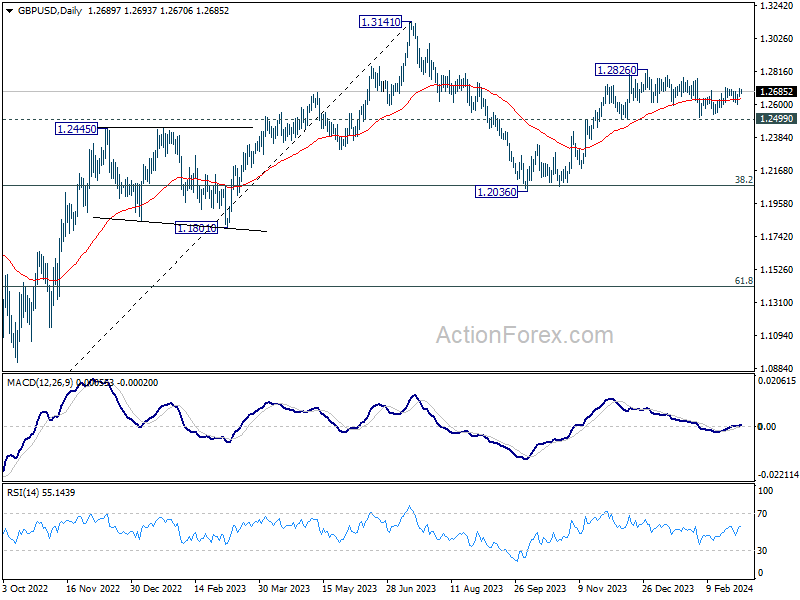

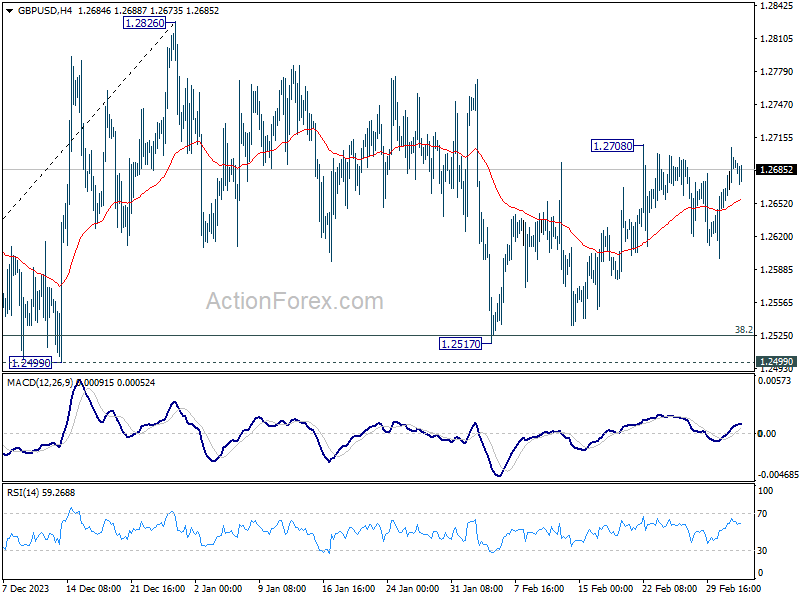

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2659; (P) 1.2683; (R1) 1.2716; More...

Intraday bias in GBP/USD stays neutral as it's staying in range below 1.2708. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.