Sample Category Title

Bitcoin Will Have to Settle Here

Market picture

The cryptocurrency market hit new highs on Monday, reaching a capitalisation of $2.5 trillion. Profit-taking was evident at the start of the active trading session in Asia on Tuesday. But before this, the market lacked enthusiasm.

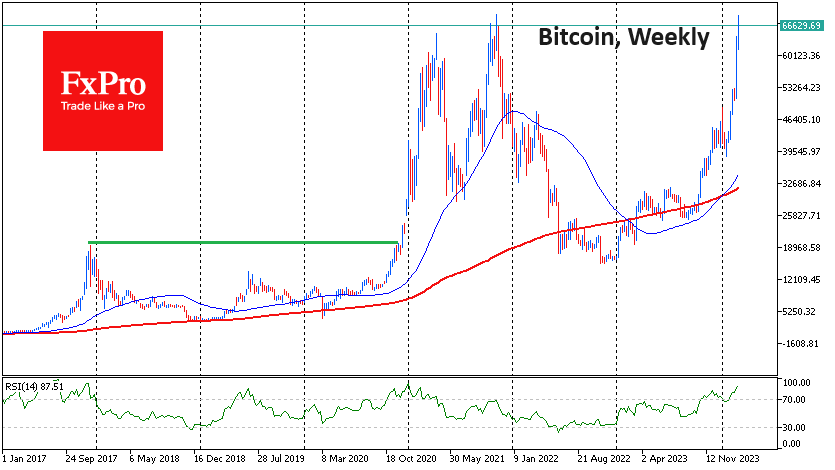

Bitcoin peaked at $68,789, just $122 below its historical high. This is before the halving and before the final capitulation of buyers, typical of the weeks leading up to the halving, when some miners leave the market and sell coins.

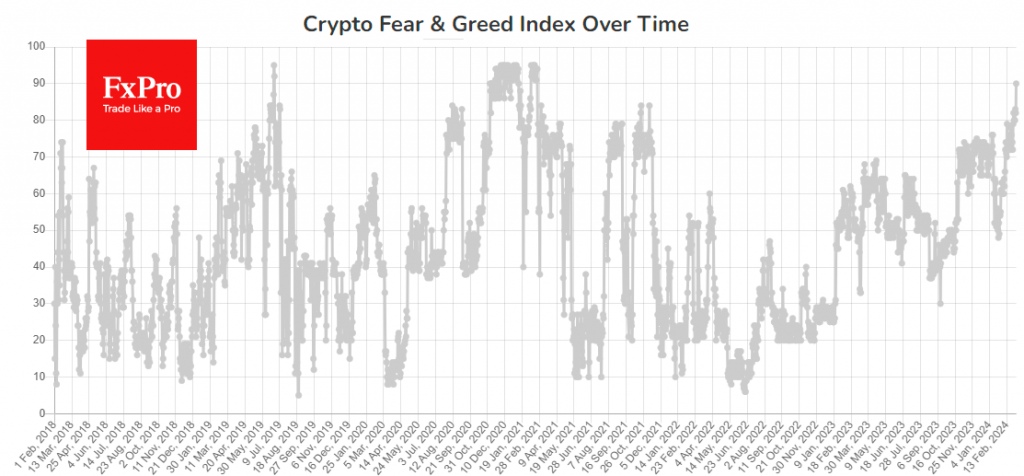

The Fear and Greed Index hit 90, the level last seen at the end of 2020. That’s when we saw a similar test of all-time highs after almost two years. Back then, bitcoin needed about four weeks of fluctuations within 15% to form a base before the next leg up.

News background

According to CoinShares, crypto funds saw their second-largest inflows last week with $1.837 billion, up from $598 million the week before. Bitcoin investments increased by $1.728 billion, Ethereum by $85 million, Polygon by $7.6 million, and Solana decreased by $12 million. Investments in funds that allow shorting bitcoin increased by $22 million.

Trading volumes in investment products reached a record high of over $30bn during the week, with total assets under management (AuM) reaching $82.6bn, very close to the record high of $86bn set in early November 2021.

As a result of the market’s growth, USDT stablecoin capitalisation reached $100 billion (+9% YTD), according to CoinGecko.

Double to triple-digit growth in a week for meme coins such as DOGE, SHIB, BONK, PEPE, and WIF is an early sign of the altcoin season, according to K33 Research. However, demand for ETFs is ten times greater than the number of coins being mined. Inventories on OTC platforms have shrunk many times over, and issuers of ETFs will soon have to buy directly from exchanges, leading to a surge in BTC.

Over the next 15 years, the price of bitcoin could increase 64-fold to $10.63 million. Former physics professor Giovanni Santostasi made such a prediction based on his ‘Power Law’ model. According to the professor’s calculations, BTC will peak at $210K in January 2026 and then fall to $60K.

A US court has recognised the trading of some cryptocurrencies as securities transactions. This is not the first time that a court has approved the classification of virtual assets promoted by SEC Chairman Gary Gensler. The head of the agency has repeatedly stated that virtually all cryptocurrencies are securities.

Tether, the issuer of the USDT stablecoin, has unveiled an asset recovery tool. The tool will allow USDT to be transferred between blockchains if one of the supported networks fails.

Meanwhile, Chinese investors were reminded of the Bitcoin ban. China’s state-run newspaper Jingji Ribao warned locals about the risks of investing in the first cryptocurrency.

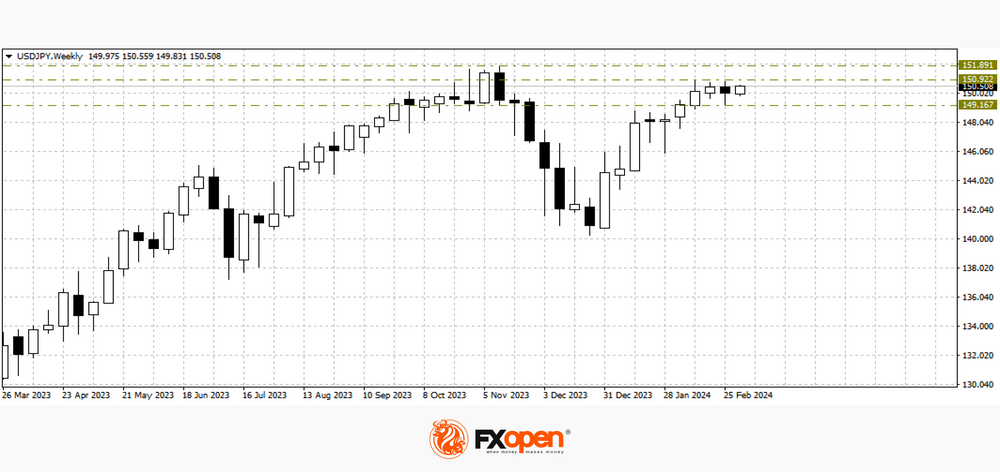

USD/JPY: Bullish Bias Above 150, Key US Data Eyed for Fresh Signals

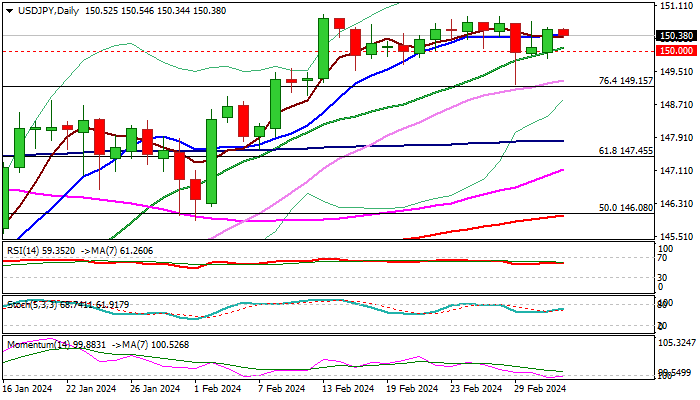

USDJPY edged lower in late Asian / early European trading on Tuesday, following release of Tokyo CPI data which showed inflation jumping in February (2.5% from 1.8% previous month) and adding to expectations that the Bank of Japan may start to tighten its monetary policy soon.

The pair steadies above broken psychological 150 barrier for the third consecutive week and also holds for the fourth week above broken Fibo barrier at 149.15 (76.4% of 151.90/140.25) bias with bulls.

Although near-term action is in a sideways mode, it keeps bullish bias while holding above 150 mark, for renewed attack at 2024 high (150.88, posted on Feb 13), violation of which to signal bullish continuation and expose key barriers at 151.94/90 (peaks of 2022/23.

Technical studies on daily chart remain bullishly aligned and support the action, but caution is required on existing risk of violating 150 pivot, which would weaken near-term structure and expose lower pivot at 149.15.

Key economic events this week (US non-manufacturing PMI / testimony of Fed Chair Powell / series of US labor data) will be closely watched for fresh signals.

Res: 150.72; 150.88; 151.43; 151.90.

Sup: 150.00; 149.15; 148.57; 147.83.

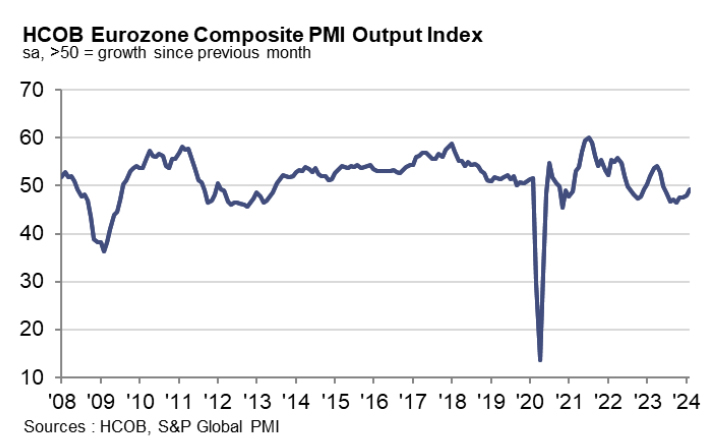

Eurozone PMI services finalized at 50.2, two important insights for ECB

Eurozone PMI Services was finalized at 50.2 in February, up from January's 48.7, a 7-month high. PMI Composite was finalized at 49.2, up from January's 47.9, an 8-month high.

Country-specific data revealed varying degrees of economic activity, with Ireland leading the pack with PMI Composite of 54.4, a 12-month high. Spain and Italy followed closely, posting 9-month highs of 53.9 and 51.1, respectively. However, not all news was positive, as France and Germany trailed behind, with Germany recording a 4-month low of 46.3, and France at 9-month low of 48.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlighted two critical insights from the PMI survey in the context of the upcoming ECB meeting on March 7.

Firstly, output prices in the service sector continue to "surge at an accelerated rate", driven by "escalating wages", underscores inflationary pressures that are yet to abate.

Secondly, the service sector's "unexpectedly robust pricing power", amidst a slow economic recovery and a forecasted growth rate below 1% for 2024, suggests the risk of "a wage-price spiral and stagflation" scenario, exacerbated by structural labor shortages impacting productivity.

"Those advocating late rate cuts may very well find reinforcement in the PMI findings," de la Rubia noted.

Market Focusing on Speech of Federal Reserve Head

Despite the abundance of fundamental data of the past trading week, the main currency pairs continue to trade in rather narrow flat corridors. Thus, the US dollar/yen currency pair is trading above 150.00, from time to time testing the figure 149, buyers of the pound/US dollar pair do not give up trying to go above 1.2700, and the euro/US dollar pair has been trading between 1.0900-1.0800 for about three weeks. Apparently, investors are waiting for more specific signals from leading central banks to open new positions.

USD/JPY

Last week, greenback buyers in the USD/JPY pair once again tried to test important resistance at 151.00. The attempt was unsuccessful and ended with a sharp rollback to 149.10, which allowed the formation of a reversal pattern to begin on the weekly timeframe. If on the USD/JPY chart in the coming trading sessions the level of 151.00 remains in resistance status, the price may test 149.00 again. If buyers manage to gain a foothold above 151.00, growth may resume towards last year's highs at 151.90.

Today at 17:45 GMT+3, we are waiting for the publication of data on the business activity index (PMI) in the services sector for February. A little later, the Purchasing Managers' Index for the US non-manufacturing sector from ISM will be published for the same period.

Tomorrow at 18:00 GMT+3, Fed Chairman Jerome Powell is scheduled to speak.

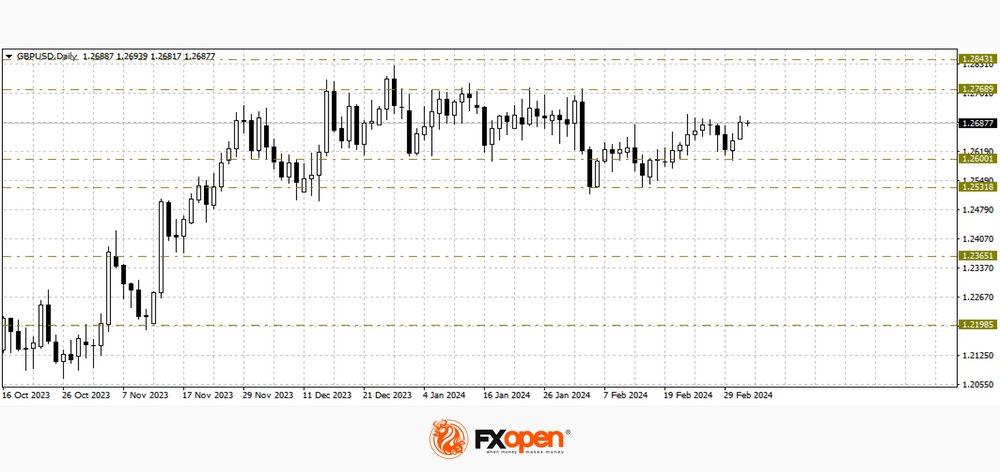

GBP/USD

The decline of the pound/US dollar pair last week slowed down at 1.2600. Buyers of the pair managed not only to find support, but also to return to the February highs at 1.2700. The coming trading sessions will be very important for the further pricing of the pair. If buyers manage to develop an upward trend, the price on the GBP/USD chart may strengthen towards 1.3000. A break of recently tested support levels at 1.2600-1.2500 could contribute to the resumption of the downtrend in the direction of 1.2300-1.2200.

Today at 12:30 GMT+3, it is worth paying attention to the publication of data on the UK composite business activity index (PMI) for February.

EUR/USD

The single European currency, after declining to 1.0700 in early February, managed to find support and test 1.0900. Buyers of the pair failed to go above this level, and at the moment the price is trading at 1.0850. Technical analysis of EUR/USD shows that if the upper limit of the specified range becomes a support status, the price may rise to the psychological level of 1.1000.

From the point of view of fundamental analysis, today at 12:00 GMT+3, it is worth paying attention to the publication of data on the composite business activity index (PMI) from S&P Global in the eurozone for February. A little later, the eurozone producer price index for January will be released.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Euro Area and Nordic Countries to Gradually Move Out of Their Current Stagnation

In focus today

This morning we published our Nordic Outlook with updated economic forecasts. We expect the euro area and the Nordic countries to gradually move out of their current stagnation or mild recession (in Denmark's case, stagnation outside pharmaceuticals). The US economy is stronger than expected, while China continues to muddle through. Interest rates can be gradually cut during 2024 and 2025, with central banks likely to move cautiously. Read more Nordic Outlook - Return to Nordic growth, 5 March.

In the US, Super Tuesday kicks off today when 15 states and one US territory are voting on their preferred candidate for the US presidential election in November. Focus will be on the Republican primaries where former president Trump is up against his former UN ambassador Nikki Haley. Trump is expected to win the most delegates, placing him on the doorstep of formally securing the Republican nomination.

Later today we get the ISM non-manufacturing PMI in the US.

In Sweden we get February service PMI numbers. We expect the numbers to show a third consecutive month above the 50-threshold, as well as come out above last month's reading of 51.8. Deputy governor Bunge from the Riksbank is also due to speak.

Economic and market news

What happened overnight

In China, the growth target for 2024 together with a bunch of other goals were revealed in the Government's Work Report released at the opening of the annual National People's Congress. The growth target was set at 5% as widely expected, the same as in 2023. It is a more ambitious target this year, though, as the base effects are less favourable this year. The inflation target was unchanged at 3%, but in practice means little as inflation is currently far below the target at -0.8% y/y. A market focus in the report was the signal on stimulus and here it disappointed a bit as the budget deficit target was unchanged from 2023 at 3%, and the off-balance special bond issuance did not pose any upward surprises. Overall, the report did not provide much new information compared to previous statements from the government whereas the markets had been hoping for more. Offshore stocks are down around 2% this morning while the CNY is broadly unchanged.

The Chinese service sector disappointed and displayed slightly slower growth signals as the Caixin services PMI came in at 52.5 compared to 52.7 last month and a consensus of 52.9. The official non-manufacturing PMI by the National Bureau of Statistics stood at 51.4 in February.

In Japan, Tokyo CPI numbers for February were released. The numbers show that seasonally adjusted CPI excluding fresh food and energy stands at 0.09% m/m down from last month's 0.19% m/m. We still look out for the first indications from the wage spring negotiations due later this month as these will be key for the Bank of Japan's monetary policy going forward.

What happened yesterday

In the US, the Supreme Court awarded former president Donald Trump a victory by deciding states cannot bar him from running for federal office citing insurrection regarding the 6 January 2021 attack on the US Capitol. With the unanimous decision Trump will once again be able to appear on the Colorado ballot, where he had otherwise been barred from appearing back in December.

In the euro area, the Sentix Indicator measuring investor confidence rose to -10.5 from -12.9 in line with expectations. The reading marks an 11-month high for the indicator, albeit it remains well below its long-term average.

Equities: Global equities were marginally lower yesterday in an uneventful session. Defensive value outperformed not least due to communication services and consumer discretionary was lower. We would not be surprised to see a couple of wait-and-see days ahead of the ECB meeting on Thursday and Non-Farm Payrolls on Friday. In the US yesterday, Dow -0.3%, S&P 500 -0.1%, Nasdaq -0.4% and Russell 2000 -0.1%. Asian markets are lower this morning with China leading the declines following the speech from Xi Jinping at the annual people's congress. Futures are lower in both Europe and US this morning.

FI: The first trading session of the week was a muted one in terms of macro or monetary policy news. Long-end EGB yields extended last week's rally with peripherals such as Italy outperforming the core. Hawkish comments from Atlanta Fed's Bostic provided renewed headwinds to US Treasuries, reversing some of the decline seen on Friday following the weak ISM figures for February. 10Y Bund yields ended down by 2bp, while 10Y UST yields were up 4bp throughout the day.

FX: EUR/USD is starting this week close to the upper end of the 1.0800-1-0850 range. Meanwhile, USD/JPY is comfortably above the 150-mark for now, whereas EUR/JPY at 163.30 still has its eyes on the 26 February 163.70 high. The small kneejerk drop in EUR/CHF immediately after the Swiss inflation data was soon erased and the cross trades above 0.96 for the first time since late November. Both SEK and NOK are on the defensive, with EUR/SEK at 11.26 back into our preferred range of 11.20-11.40 and where EUR/NOK is closing in on 11.50 again.

Beijing Tries to Convey Message of Confidence, Markets Not Impressed

Markets

In a session deprived of data, US yields yesterday easily reversed a big part of Friday’s decline post a weaker than expected US manufacturing ISM. The move started early in US dealings. Comments from Atlanta Fed president Bostic only confirmed recent guidance that the Fed will take a cautious stance on rate cuts as it wants to be sure that inflation is on a sustainable path to its 2% target. Bostic expects the first interest rate cut in the third quarter to be followed by a pause as he wants to asses the impact on the economy. Interestingly, with respect upside risks to inflation and economic activity, in an article on the Atlanta Fed website, he elaborates on ‘expectant optimism’ among businesses. From contacts with businesses, the Atlanta Fed learned they stand ready to deploy assets and hire again if the time is right e.g. when the Fed starts cutting rates. This threat of ‘pent-up exuberance’ holds the ‘potential to unleash a burst of new demand that could reverse the progress toward rebalancing supply and demand’ and would create upward pressure on prices. Interesting framework to assess the Fed’s reaction function not only with respect to inflation but also on (ongoing strong) activity and sentiment indicators. At the end of the day, US yields added between 7 bps (2-y) and 2.5 bps (30-y). Moves in German yields again were more moderate (2-y + 1.3 bps 10-y -2.2 bps). After setting new record levels on Friday, US equities finally showed some hesitancy (S&P -0.12%, Nasdaq -0.41%). Higher (ST) US yields again didn’t help the dollar. DXY closed marginally lower at 103.83. EUR/USD even drifted cautiously higher to close at 1.0856. We also are a bit puzzled by the sharp rally in gold on Friday and yesterday, bring it near record high levels ($ 2116 p/oz). Something to keep an eye on.

This morning Asian (equity) markets are trading mixed as investors are pondering the impact of China maintaining a 5% growth target for this year (cf infra). Mainland Chinese indices gain modestly, but Hong Kong shows a substantial loss (-2.5%). US yields maintain yesterday’s gain. The dollar gains marginally (DXY 103.9, EUR/USD 1.0845). The yen remains in the defensive with USD/JPY (150.5) holding with reach of the 150.89 YTD top. Later today, the US services ISM will take center stage. The headline index is expect to stay comfortably in positive growth territory (53.0). Price pressures are expected to persist (prices paid 62.0). After Friday’s disappointing manufacturing measure, markets might have become a bit more sensitive to a negative surprise. However, we don’t expect the Fed to leave its cautious approach on interest rates by one set of less buoyant sentiment indicators (cf Bostic).

News & Views

China at the annual National People’s Congress set this year’s growth goal at ”around 5%”. The country had set and successfully met the same target last year. But 2024 growth unlike 2023 won’t enjoy the tailwind of favourable base effects, effectively making the 5% a more ambitious target. The other 2023 goalposts haven’t been moved either: a jobless rate of 5.5%, CPI around 3% and a fiscal deficit of 3% of GDP. The latter was raised from 3% to 3.8% late last year though. By sticking to the same targets at a time when the economy is even more clearly in a downturn than what was already the case last year, Beijing tries to convey a message of confidence in the recovery. The report also no longer states that “housing is for living in, not speculation” amid a massive real estate slump. The phrase became common usage since 2016 and was implemented in the official report from 2019 on. Markets are not impressed with targets that are deemed unrealistic without a strong dose of fiscal stimulus. The Chinese yuan stabilizes near recent lows at around USD/CNY 7.20. Equity markets in the region trade mixed.

Inflation in Tokyo largely matched expectations. Price growth rebounded from 1.8% in January to 2.6% in February. The core gauge excluding fresh food (looked at by the Bank of Japan) bounced from 1.8% to 2.5% with the figure that omits energy as well holding sticking above 3.0% (3.1% from 3.3%). The M/M jump mostly reflects the fading impact of government subsidies rolled out last year to contain utility costs. It nevertheless reveals how these grants have masked inflation’s true momentum. Tokyo CPI is a good guide for the national reading which will be published on March 22. If confirmed, it will keep those figures comfortably above the 2% BoJ target across all gauges (core and headline), further fueling speculation for an imminent exit from the ultra-easy monetary policy. The BoJ meets March 19. Japanese bond yields erased early kneejerk gains to trade slightly lower on the day.

US Dollar Index Stuck Between 100 and 200-DMA Before Powell’s Speech

China wants to grow 5% this year, create around 12 mio jobs in the urban area and print a 3% inflation. Targets are ambitious – especially the inflation target - given that the base effect will not play in favour of growth this year and deflation is not an easy battle to win – especially in a context of lost confidence, aging – and shrinking - population and a severe property crisis. Of course, the Chinese Premier said that he will need policy support to achieve his goals. He does, indeed, need a lot of support and even then no one guarantees the return of investment and spending. The market reaction is mixed; the CSI 300 extended gains today, while Hang Seng was pulled down by more than 2.5% due to steep losses in mainland stocks. Caixin PMI printed an unexpected slowdown in the expansion of Chinese services in February, while Tesla tumbled 7% yesterday after announcing that its shipments from the Shanghai mega factory slumped to the lowest levels in a year due to a dull activity during the Lunar Year Holiday and renewed price competition in the EV market.

While Tesla was sliding a big 7%, Nvidia was busy traveling through uncharted territories. The company added another 3.50% yesterday and stole the title of the world’s ‘3rd biggest company’ from the Saudi Aramco. Some compare the Nvidia’s rise to Tesla-mania back after 2020, when Tesla was growing 50% a year and we thought nothing could stand on the path of Elon Musk in replacing every single car out there with a Tesla. But today, the sales growth slows, the competition eats into the company’s profit margins, shareholders are not happy – beyond the fact that Elon Musk is cooking unpleasant stuff outside Tesla, and the shares are under a decent selling pressure. It’s certain that Nvidia will experience its own down-moment and face its own challenges. But as Tesla example shows, there is not a price level that will bring investors back to earth.

Elsewhere, Apple fell free yesterday after the EU imposed a $2 billion penalty on accusations that Apple's platform unfairly marginalized competitors in the music-streaming industry, including Spotify. But I believe Apple’s biggest problem today is it’s late arrival in the AI, and the struggling business in China. Price-wise, yesterday’s fall broke the $180pb support. The next crucial support stands at $171 per share, the major 38.2% Fibonacci retracement on the positive trend forming since the beginning of last year, and which should distinguish between the actual positive trend and a medium-term bearish reversal.

Zooming out, the S&P500 timidly advanced to a fresh record but closed the session slightly down. Investors – except for the Nvidia investors – didn’t necessarily wanted to take a clear direction before Federal Reserve (Fed) Chair Jerome Powell’s semiannual testimony before the Congress on Wednesday and Thursday. In this testimony, Powell will likely ask for more patience regarding the timing of the first rate cut, he will probably say that inflation is on the right path but that they don’t want to lower their guard too early. The US 2-year yield settled around the 4.60%, while the 10-year yield is back to 4.20%. Many now say that ‘4.5% is the new 5%’ and that buying the 10-year paper at 4.5% is interesting as the yield will probably not go above this level given the downtrending inflation and the Fed’s plans to cut the rates, even if the first cut can’t come soon enough.

In the FX, the US dollar index is stuck between its 100 and 200-DMA before Powell’s speech and a series of jobs data from the US this week. The EURUSD sees resistance into its 50-DMA, the USDJPY consolidates above 150, while gold is on an impressive rally since last Friday on rising safe haven demand before Powell’s speech. The rising geopolitical tensions are also shown as a potential reason for the recent rally but the geopolitical tensions are here for a while and they are probably not the major driver of the past couple of days’ move. So I stick to the safe haven demand narrative before Powell’s speech. The thing is, a dovish tone from Powell should pressure the US yields lower, decrease the opportunity cost of holding the non-interest-bearing gold and help gold extend gains. But low yields on the other hand will also boost risk appetite and encourage investors to abandon their gold holdings to opt for riskier but better yields assets. Therefore, I think that the upside potential in gold could be limited if the Fed cut bets are what’s driving the gold prices higher these days.

A last word for oil, US crude failed to extend gains above $80pb even after the Chinese stimulus bets. As I was saying, OPEC will hardly push the price of a barrel sustainably above that level when non-OPEC countries pump to make up for the supply cuts.

Hang Seng Index Technical: Countertrend Rebound Phase May Have Ended

- Lacklustre movement was seen in China & Hong Kong benchmark stock indices today after the release of China Premier Li Qiang’s economic work report during the second day of the “Two Sessions”.

- Premier Li Qiang has officially announced China’s 2024 GDP growth target of around 5% (within consensus) and stuck to the same rhetoric of targeted stimulus measures to achieve the economic growth target.

- Lack of fresh positive catalysts may reverse the four weeks of the rally seen in China & Hong Kong benchmark stock indices.

- The Hang Seng Index is likely to be undergoing a “bearish flag” with a potential downside trigger level at 16,080.

The weakest major benchmark stock indices of late, China had Hong Kong have roared back to life and became the top-performing stock market for February with monthly gains of +9.35% on the CSI 300, and the Hang Seng Index notched up by +6.63%.

Similar monthly stellar gains can be seen in other related indices; Hang Seng TECH Index (+14.16%) and Hang Seng China Enterprises Index (+9.32%); all of them outperformed the US S&P 500 (+5.17%), and even the Nasdaq 100 (+5.29%) in local currency terms.

The recent bout of outperformance seen in the China/Hong Kong stock markets has been driven by policies that target the trading mechanism of the stock market such as banning or making it difficult for high-frequency firms and hedge funds to enact short positions on Chinese equities.

The deflationary risk spiral remains intact in China’s economy with no fresh positive catalysts from Premier Li’s economic work report

Hence, this is only a short-term fix, and less likely to reverse the long-term secular bearish trend of the CSI 300 and Hang Seng indices in place since February 2021 because top China policymakers see no urgency to address the deflationary risk spiral that is playing out in China economy as consumers and businesses’ face a negative wealth effect from the depressed property market.

In today’s China annual parliamentary session (aka Two Sessions), Premier Li Qiang officially announced China’s 2024 GDP growth target set at around 5%, a similar rate that is within consensus, and the rhetoric of targeted stimulus measures remains intact.

Hence, there are no fresh catalysts on the horizon that may propel the China and Hong Kong benchmark stock indices to kickstart a medium-term uptrend phase.

Forming a potential “bearish flag”

Fig 1: Hong Kong 33 Index medium-term trend as of 5 Mar 2024 (Source: TradingView, click to enlarge chart)

Fig 2: Hong Kong 33 Index short-term trend as of 5 Mar 2024 (Source: TradingView, click to enlarge chart)

Through the lens of technical analysis, the price actions of the Hong Kong 33 Index (a proxy on the Hang Seng Index futures) have indicated that the recent upmove from its 22 January 2024 low is likely to be a countertrend rebound sequence (aka a “bearish flag”) as the daily RSI momentum has just shaped a bearish momentum breakdown below a key parallel ascending trendline support below the 50 level (see Fig 1).

In the short-term, watch the 16,670 key short-term pivotal resistance, and a breakdown below the “bearish flag” support at 16,080 may trigger further weakness to expose the next near-term support at 15,455 in the first step (see Fig 2).

On the other hand, a clearance above 16,670 negates the bearish tone for a squeeze up with the next near-term resistance coming in at 17,010/130 after 16,860 minor swing high area of 23/28 February 2024.

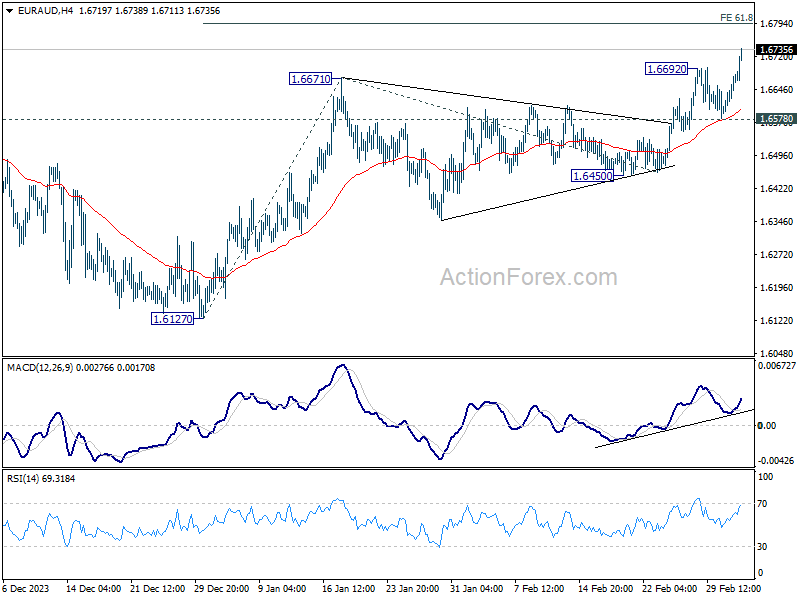

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6623; (P) 1.6652; (R1) 1.6708; More...

EUR/AUD's rally resumed by breaking through 1.6692 temporary top and intraday bias is back on the upside. Rise from 1.6127 should target 61.8% projection of 1.6127 to 1.6671 from 1.6450 at 1.6786. Firm break there will target 100% projection at 1.6994 next. For now, near term outlook will remain cautiously bullish as long as 1.6578 support holds, in case of retreat.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

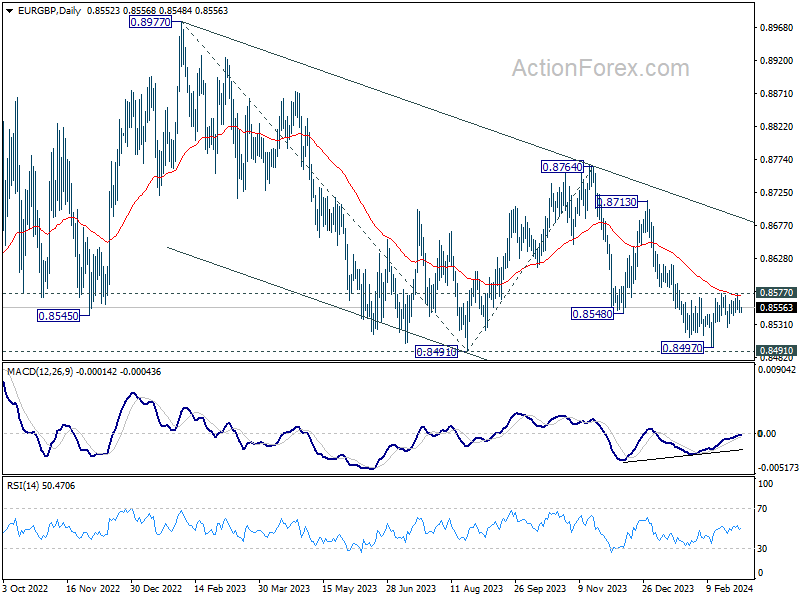

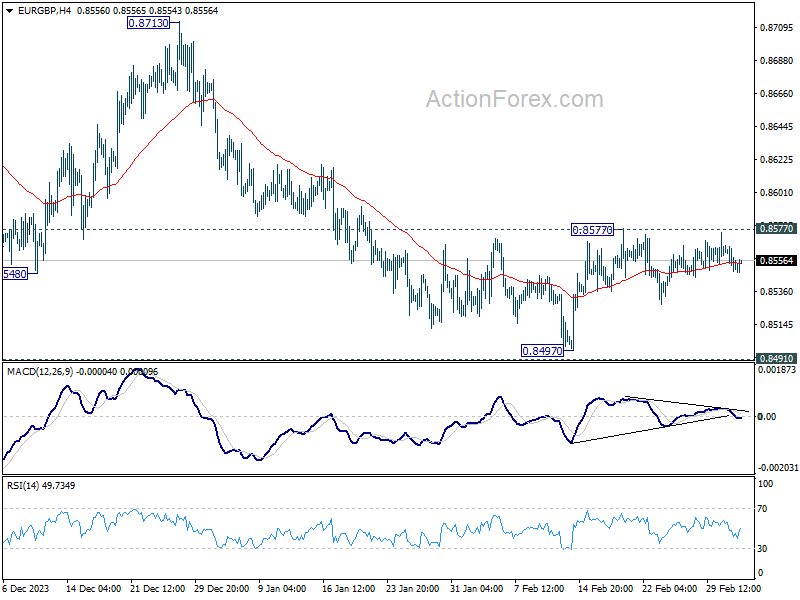

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8548; (P) 0.8557; (R1) 0.8564; More...

Intraday bias in EUR/GBP remains neutral at this point, and outlook is unchanged. Considering bullish convergence condition in D MACD, decisive break of 0.8577 and 55 D EMA (now at 0.8572) will argue that fall from 0.8764 has completed. Intraday bias will be back on the upside for rebound towards 0.8713 resistance. Nevertheless, firm break of 0.8491/7 support zone will confirm larger down trend resumption.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.