Sample Category Title

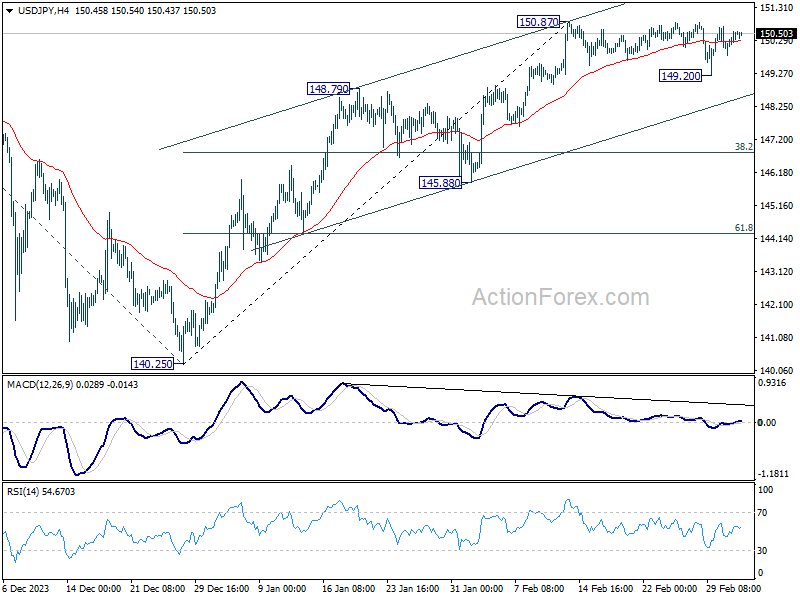

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.05; (P) 150.31; (R1) 150.78; More...

No change in USD/JPY's outlook as consolidation from 150.87 is extending. Intraday bias stays neutral for the moment. On the upside, break of 150.87 will resume the rise from 140.25 to 151.89/93 key resistance zone. On the other hand, considering bearish divergence condition in 4H MACD, firm break of 149.20 will confirm short term topping at 150.87. Deeper fall would be seen to channel support (now at 148.60) and possibly below, even as a corrective move.

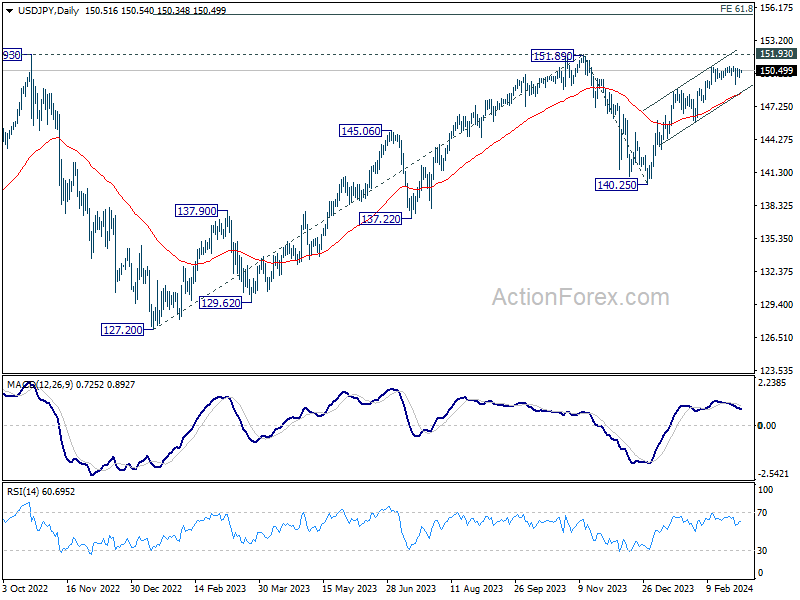

In the bigger picture, rise from 140.25 is seen as resuming the trend from 127.20 (2023 low). Decisive break of 151.89/.93 resistance zone will confirm this bullish case and target 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. However, break of 148.79 resistance turned support will delay this bullish case, and extend the corrective pattern from 151.89 with another falling leg.

Nikkei’s Resilience Contrasts With Hong Kong’s Setback, US ISM Services watched

Market sentiment was clearly mixed in Asian session today, highlighted by Nikkei's remarkable resilience and Hong Kong's stocks' downturn. The day commenced with Nikkei momentarily succumbing to profit taking pressure, dropping below 40k mark after Tokyo's CPI was reported to have risen to 2.5%. This initial dip, however, was short-lived as the index swiftly recaptured its losses, soaring back above 40k psychological by the afternoon. This swift recovery not only showcases the robust confidence permeating among investors but also suggests that speculations of an imminent market correction might be premature. It appears that the bullish momentum engulfing the index is likely to sustain at least until BoJ clarifies its stance on interest rate hikes at the meeting later this month.

On the other hand, Hong Kong's equity market faced significant setbacks, as reaction to Chinese Premier Li Qiang's economic outlook announcements. The setting of a somewhat conservative GDP growth target at around 5% for the year, coupled with consumer price inflation goal of about 3%, has been interpreted by some economists as a tacit acknowledgment of the prevailing economic challenges. Additionally, the central government's decision to cap deficit at 3% of GDP indicates a reluctance to deploy substantial fiscal stimulus, further tempering expectations of aggressive economic interventions.

In the currency markets, Australian and New Zealand Dollars are languishing as the day's underperformers sofar, trailed by Canadian. Conversely, Dollar and Yen carved out modest gains, with Euro not far behind in performance. Sterling and Swiss Franc found themselves mixed in a middle path. Attention in the forex markets now turns towards upcoming US ISM Services data, with particular emphasis on price and employment components, in addition to the headline figure.

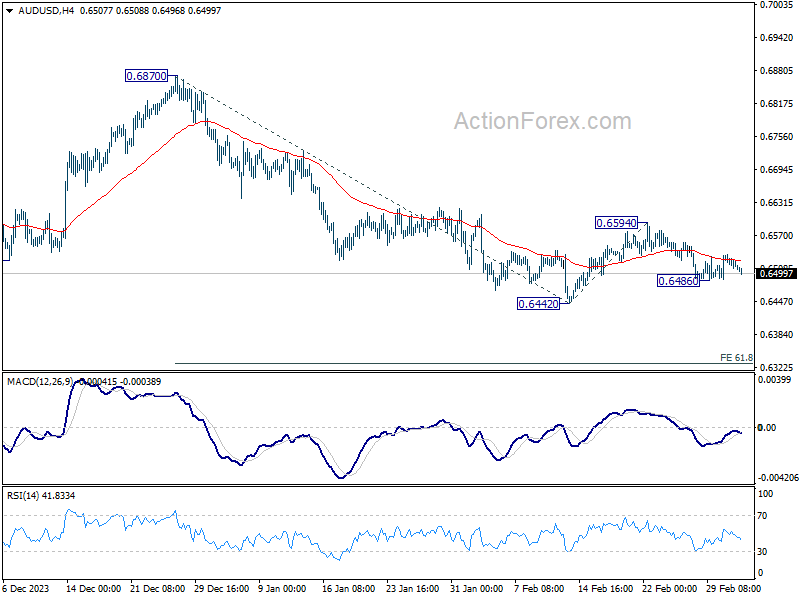

Technically, focus in AUD/USD is back on 0.6486 temporary low after rejection by 55 4H EMA. Break there will resume the fall from 0.6594 to retest 0.6442 low first. Firm break there will resume whole decline from 0.6870 for 61.8% projection of 0.6870 to 0.6442 from 0.6594 at 0.6329 next.

In Asia, at the time of writing, Nikkei is up 0.21%. Hong Kong HSI is down -1.95%. China Shanghai SSE is up 0.26%. Singapore Strait Times is down -0.39%. Japan 10-year JGB yield is down -0.004 at 0.712. Overnight, DOW fell -0.25%. S&P 500 fell -0.12%. NASDAQ fell -0.41%. 10-year yield rose 0.039 to 4.219.

Fed's Bostic: No sequential rate cuts and highlights risks of pent-up exuberance

Atlanta Fed President Raphael Bostic emphasized the necessity of seeing "more progress" on inflation reduction before considering any rate cuts. He said overnight that the prosperity in the labor market and the economy, granting the FOMC the "luxury of making policy without the pressure of urgency."

In terms of the pace of policy loosening once initiated, Bostic envisages a measured approach rather than "back to back" adjustments. The reaction of market participants, business leaders, and households to policy changes will critically influence the pace of rate cuts.

Highlighting ongoing inflation concerns, Bostic pointed out the continued price increases in a significant portion of goods and services at rates exceeding 5% annually. Moreover, a Dallas Fed measure indicated that underlying inflation remains slightly above Fed's target at 2.6%, further complicating the path towards rate normalization.

Bostic also reflected on the feedback from business executives, noting a widespread strategy of holding back investments and hiring until more favorable conditions emerge. He warned of the "pent-up exuberance" that could result from a large-scale unleashing of this dormant capacity, introducing a new variable of upside risk to the economy.

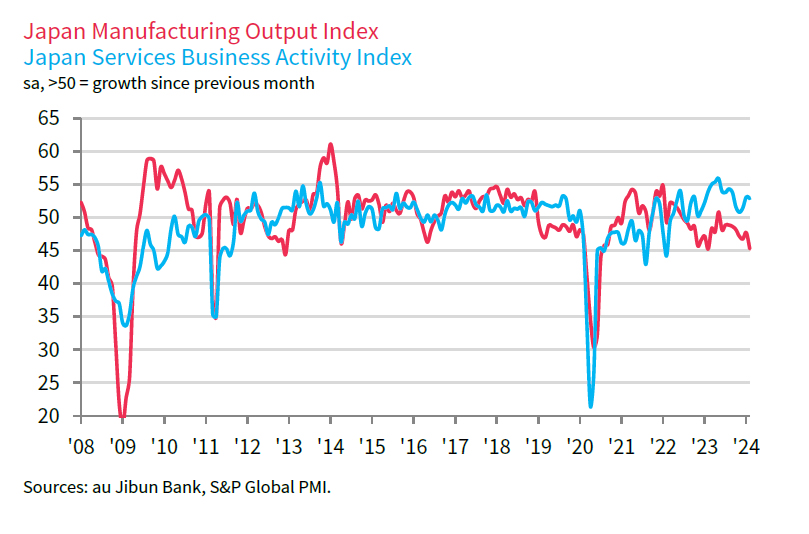

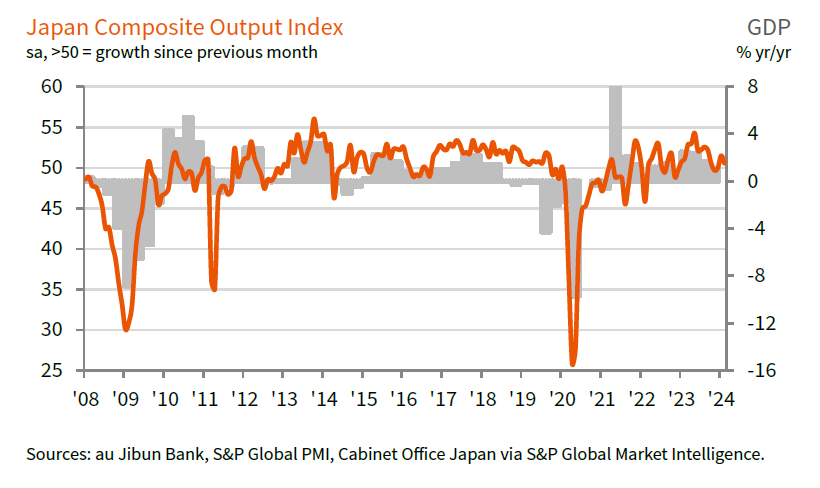

Japan's Tokyo CPI core rises to 2.5% yoy, PMI services finalized at 52.9

Japan's Tokyo CPI core (ex-fresh food) rose from upwardly 1.8% yoy to 2.5% yoy in February, matched expectations. CPI core-core (ex-food and energy) slowed from 3.3% yoy to 3.1% yoy. Headline CPI in the capital city rose from 1.8% yoy to 2.6% yoy.

Also released, PMI Services was finalized at 52.9 in February, down from January's 53.1, but stays in expansion for the 18th month in a row. PMI Composite was finalized at 50.6, down from prior month's 51.5.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence,services business activity growth was sustained into February while the rate of growth in new business accelerated to a six-month high. However, steeper reduction in manufacturing output levels contributed to a slowdown in overall private sector activity growth.

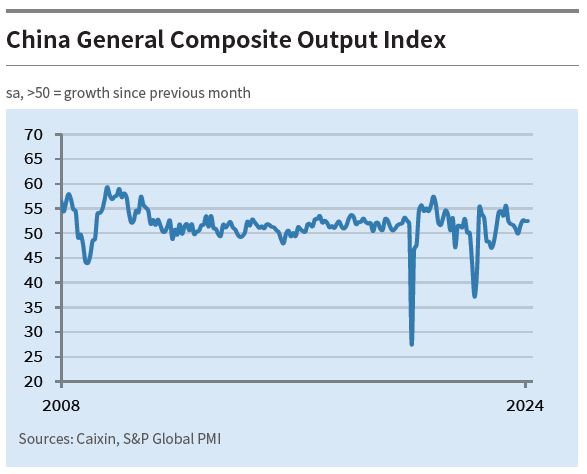

China's Caixin PMI services falls to 52.5, composite unchanged at 52.5

China's Caixin PMI Services fell from 52.7 to 52.5 in February, below expectation of 52.9. PMI Composite was unchanged at 52.5.

Wang Zhe, Senior Economist at Caixin Insight Group, noted that both manufacturing and services sectors recorded steady growth. However, he noted supply was "still running ahead" of improved demand. Employment across both sectors saw contraction. On the pricing front, pressures of low prices becoming more pronounced within the manufacturing sector.

Overall, "market sentiment remained optimistic", Wang noted.

Looking ahead

Eurozone PMI services final and PPI will be released in European session. UK will also publish PMI services final. Later in the day, US ISM services will take center stage while factory orders will also be featured.

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.05; (P) 150.31; (R1) 150.78; More...

No change in USD/JPY's outlook as consolidation from 150.87 is extending. Intraday bias stays neutral for the moment. On the upside, break of 150.87 will resume the rise from 140.25 to 151.89/93 key resistance zone. On the other hand, considering bearish divergence condition in 4H MACD, firm break of 149.20 will confirm short term topping at 150.87. Deeper fall would be seen to channel support (now at 148.60) and possibly below, even as a corrective move.

In the bigger picture, rise from 140.25 is seen as resuming the trend from 127.20 (2023 low). Decisive break of 151.89/.93 resistance zone will confirm this bullish case and target 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. However, break of 148.79 resistance turned support will delay this bullish case, and extend the corrective pattern from 151.89 with another falling leg.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Feb | 2.60% | 1.60% | 1.80% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Feb | 2.50% | 2.50% | 1.60% | 1.80% |

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Feb | 3.10% | 3.10% | 3.30% | |

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Feb | 1.00% | 1.40% | ||

| 00:30 | AUD | Current Account Balance (AUD) Q4 | 11.8B | 5.0B | -0.2B | 1.3B |

| 01:45 | CNY | Caixin Services PMI Feb | 52.5 | 52.9 | 52.7 | |

| 07:45 | EUR | France Industrial Output M/M Jan | -0.10% | 1.10% | ||

| 08:45 | EUR | Italy Services PMI Feb | 52.3 | 51.2 | ||

| 08:50 | EUR | France Services PMI Feb F | 48 | 48 | ||

| 08:55 | EUR | Germany Services PMI Feb F | 48.2 | 48.2 | ||

| 09:00 | EUR | Eurozone Services PMI Feb F | 50 | 50 | ||

| 09:30 | GBP | Services PMI Feb F | 54.3 | 54.3 | ||

| 10:00 | EUR | Eurozone PPI M/M Jan | -0.10% | -0.80% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Jan | -8.10% | -10.60% | ||

| 14:45 | USD | Services PMI Feb F | 51.3 | 51.3 | ||

| 15:00 | USD | ISM Services PMI Feb | 0.30% | 53.4 | ||

| 15:00 | USD | Factory Orders M/M Jan | -2.80% | 0.20% |

Bitcoin (BTCUSD) Next Bullish Leg In Progress

Short Term Elliott Wave View in Bitcoin (BTCUSD) suggests that cycle from 2.1.2024 low is in progress as an impulse. Up from 2.1.2024 low, wave ((i)) ended at 52998 and dips in wave ((ii)) ended at 50639.8. The crypto currency extended higher in wave ((iii)) towards 64105.7. Internal subdivision of wave ((iii)) unfolded as a 5 waves impulse in lesser degree. Up from wave ((ii)), wave (i) ended at 51958.1 and pullback in wave (ii) ended at 50909.5. The crypto currency extended higher in wave (iii) towards 57456.9 and pullback in wave (iv) ended at 56267.9.

Final leg wave (v) ended at 64105.7 which completed wave ((iii)). Pullback in wave ((iv)) ended at 58498.9. Bitcoin then extends higher again in wave ((v)). Up from wave ((iv)), wave (i) ended at 63676.4 and dips in wave (ii) ended at 60357.6. The crypto extended again in wave i towards 63260.7 and pullback in wave ii ended at 61437.3. Expect wave iii to end soon and the crypto to pullback in wave iv before turning higher again. Near term, as far as pivot at 58498.9 low stays intact, expect pullback to find support in 3, 7, 11 swing for further upside.

Bitcoin (BTCUSD) 60 Minutes Elliott Wave Chart

Bitcoin (BTCUSD) Elliott Wave Video

https://www.youtube.com/watch?v=0UU3hBz2uYk

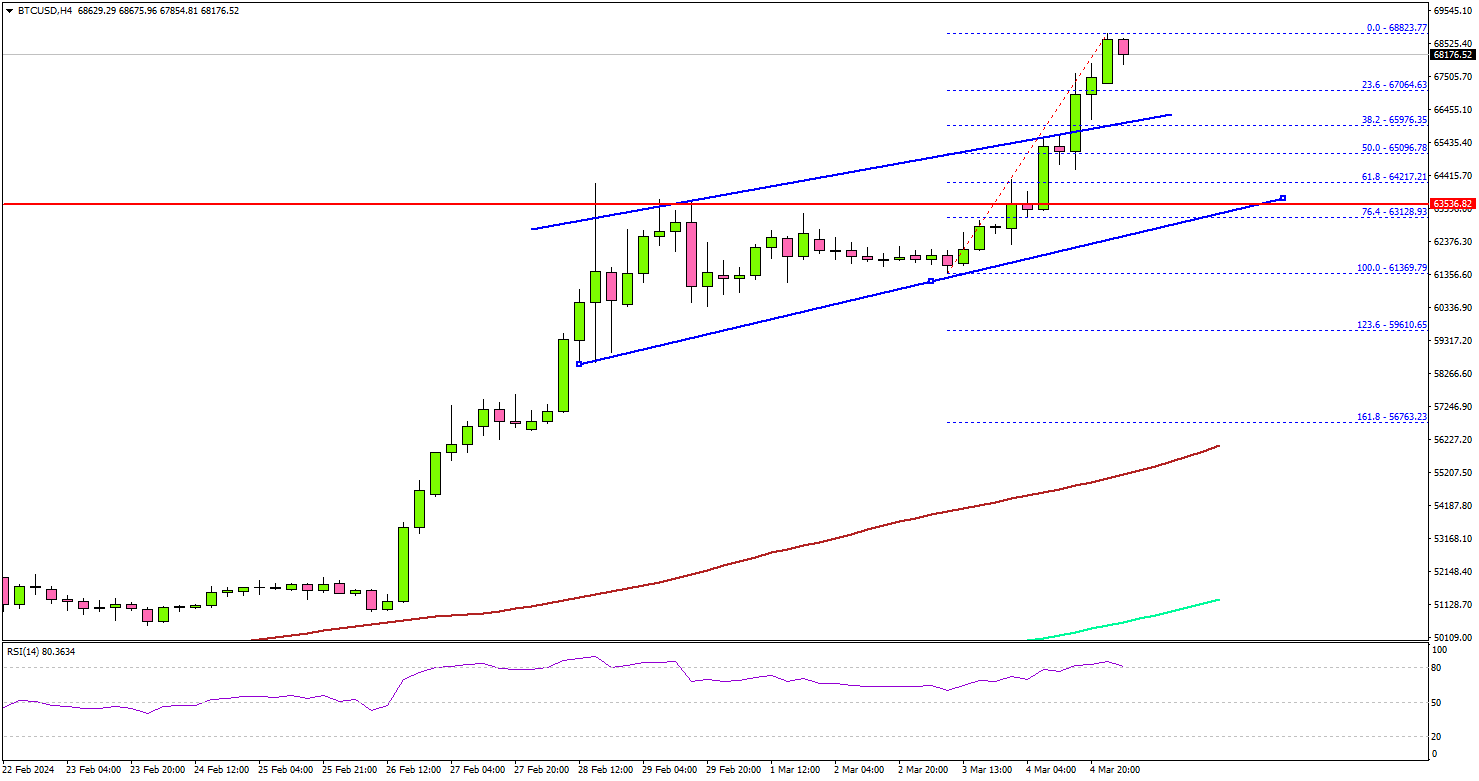

Bitcoin Price Breaks $68K and Eyes New ATH, Why Dips Are Attractive

Key Highlights

- Bitcoin price extended its rally above $65,000 and $68,000.

- BTC cleared a rising channel with resistance at $65,750 on the 4-hour chart.

- Ethereum also rallied above the $3,450 and $3,500 resistance levels.

- Gold prices are accelerating higher toward the $2,120 resistance.

Bitcoin Price Technical Analysis

Bitcoin price remained in a strong uptrend above the $58,000 level. BTC extended its rally above the $65,000 and $68,000 resistance levels.

Looking at the 4-hour chart, the price settled above the $63,500 pivot level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

BTC cleared a rising channel with resistance at $65,750 on the same chart. The bulls were able to pump the price above the $68,000 level. A new multi-month high was formed at $68,823 and the price is now consolidating gains.

The first major support is near the $67,000 level. It is close to the 23.6% Fib retracement level of the upward move from the $61,369 swing low to the $68,823 high. The next major support is $66,000. Any more losses might send the price toward the $65,000 support zone.

Immediate resistance is near the $68,750 level. The next resistance is near $69,500 or the last all-time high. A successful close above the $69,500 level might start another steady increase. In the stated case, the price may perhaps rise toward the $72,000 level.

Economic Releases

- Euro Zone Services PMI for Feb 2024 – Forecast 50.0, versus 50.0 previous.

- UK Services PMI for Feb 2024 – Forecast 54.3, versus 54.3 previous.

- US Services PMI for Feb 2024 – Forecast 51.3, versus 51.3 previous.

- US ISM Services Index for Feb 2024 – Forecast 53.0, versus 53.4 previous.

China’s Caixin PMI services falls to 52.5, composite unchanged at 52.5

China's Caixin PMI Services fell from 52.7 to 52.5 in February, below expectation of 52.9. PMI Composite was unchanged at 52.5.

Wang Zhe, Senior Economist at Caixin Insight Group, noted that both manufacturing and services sectors recorded steady growth. However, he noted supply was "still running ahead" of improved demand. Employment across both sectors saw contraction. On the pricing front, pressures of low prices becoming more pronounced within the manufacturing sector.

Overall, "market sentiment remained optimistic", Wang noted.

Japan’s Tokyo CPI core rises to 2.5% yoy, PMI services finalized at 52.9

Japan's Tokyo CPI core (ex-fresh food) rose from upwardly 1.8% yoy to 2.5% yoy in February, matched expectations. CPI core-core (ex-food and energy) slowed from 3.3% yoy to 3.1% yoy. Headline CPI in the capital city rose from 1.8% yoy to 2.6% yoy.

Also released, PMI Services was finalized at 52.9 in February, down from January's 53.1, but stays in expansion for the 18th month in a row. PMI Composite was finalized at 50.6, down from prior month's 51.5.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence,services business activity growth was sustained into February while the rate of growth in new business accelerated to a six-month high. However, steeper reduction in manufacturing output levels contributed to a slowdown in overall private sector activity growth.

Fed’s Bostic: No sequential rate cuts and highlights risks of pent-up exuberance

Atlanta Fed President Raphael Bostic emphasized the necessity of seeing "more progress" on inflation reduction before considering any rate cuts. He said overnight that the prosperity in the labor market and the economy, granting the FOMC the "luxury of making policy without the pressure of urgency."

In terms of the pace of policy loosening once initiated, Bostic envisages a measured approach rather than "back to back" adjustments. The reaction of market participants, business leaders, and households to policy changes will critically influence the pace of rate cuts.

Highlighting ongoing inflation concerns, Bostic pointed out the continued price increases in a significant portion of goods and services at rates exceeding 5% annually. Moreover, a Dallas Fed measure indicated that underlying inflation remains slightly above Fed's target at 2.6%, further complicating the path towards rate normalization.

Bostic also reflected on the feedback from business executives, noting a widespread strategy of holding back investments and hiring until more favorable conditions emerge. He warned of the "pent-up exuberance" that could result from a large-scale unleashing of this dormant capacity, introducing a new variable of upside risk to the economy.

Sunset Market Commentary

Markets

US yields softened going into the weekend as a poor manufacturing ISM triggered a short squeeze. Today, the calendar was almost empty. However, with several key events/data scheduled later this week, markets didn’t draw any firm conclusions from Friday’s repositioning. In technical trade, US yields even reverse a big part of Friday’s setback, adding about 5 bps across the curve. German yields, which hardly followed the decline in de US on Friday, change less than 1 bp across the curve. Both US and EMU money markets currently see about 90% chance of both the ECB and the Fed starting with a first 25 bps rate cut in June, with a reality check to follow later this week.

Regarding the data part of this reality check, the US will take center stage. Tomorrow, the services ISM is expected to hold well above the 50 mark (53). After Friday’s disappointing manufacturing measure, markets might become a bit more sensitive to a softer than expected release. The same is true in case of weaker US labour market data (JOLTS job openings and ADP on Wednesday, payrolls on Friday). However, given the upward January inflation surprise, one shouldn’t expect the Fed to feel forced to change ‘guidance’ after just one set of less buoyant activity data. At his hearing before Congress on Wednesday/Thursday, Fed’s Powell can easily hold the message that recent data perfectly justify MPC’s December dots for a gradual approach of 75 bps of cumulative easing this year. ECB’s Lagarde at the press conference on Thursday probably will face more questions as to what extent ongoing sluggish growth will affect the start of its easing cycle. Headline inflation probably will be downwardly revised in the new ECB staff forecasts, but we see little reason for the ECB to change its assessment on core inflation until it is ‘sure’ that wage negotiations are in line with (core/services) inflation returning to 2% in a sustainable way. Due to softer activity data, Lagarde’s wait-and-see narrative might be slightly less convincing that Powell’s, but she has also as every reason not to complicate future policy steps by giving the market a pretext to ease monetary conditions prematurely.

Briefly returning to FX, volatility remains extremely low with no clear directional bias for the US dollar. DXY is going nowhere in the middle of the ST consolidation range between 103 and 105 (currently 103.9). EUR/USD gains marginally (1.085), but first resistance in the 1.09 area stays out of reach. Sterling gains marginally with EUR/GBP easing to 0.856 as investors ponder the chances of some fiscal support as UK Chancellor of the Exchequer Jeremy Hunt will present the government’s ‘final’ (spring) budget going into the parliamentary elections expected in autumn.

News & Views

Swiss inflation picked up in February, with the monthly pace accelerating from 0.2% to 0.6% vs 0.5% expected. Favourable base effects still allowed for the Y/Y figure to ease from 1.3% to 1.2% - be it slightly less than anticipated. Core inflation (ex. fresh and seasonal products, energy and fuel) rose a solid 0.7% as well, to be up 1.1% y/y. The Swiss franc’s attempt to rise on the release was very short-lived. The Swiss National Bank meets on March 21 and today’s CPI numbers have barely changed market’s 50-50 assessment whether or not the SNB will kick off with a first rate cut. If any, they pared bets somewhat as the sharp monthly CPI bump indeed warrants a cautious approach towards monetary easing. EUR/CHF is testing the 0.96 big figure, the highest level since end-November and more than 300 points higher than the all-time low (closing levels) seen around the turn of the year.

Turkish inflation rose 4.53% m/m, pushing up the yearly figure from 64.86% to 67.07%. All subcomponents printed higher with hotels, cafes and restaurants (+5.43% m/m), food (+8.25%) and education (+12.76%) composing the top three. Underlying inflation gauges (ex. energy, food and non-alcoholic & alcoholic beverages, tobacco and gold) rose a monthly 3.57% to a new record of 72.89%. It begs the question whether the central bank has raised policy rates high enough. After having hiked to 45% in January, the CBRT signaled a pause in the cycle. It retained the option of further hikes of needed but that doesn’t change the fact real rates are and will stay extremely negative for some time to come. That keeps the Turkish currency vulnerable on international markets, despite an improving external position. EUR/TRY today moves further north of 34, a new record TRY-low. USD/TRY is similarly hitting new highs around 31.53.

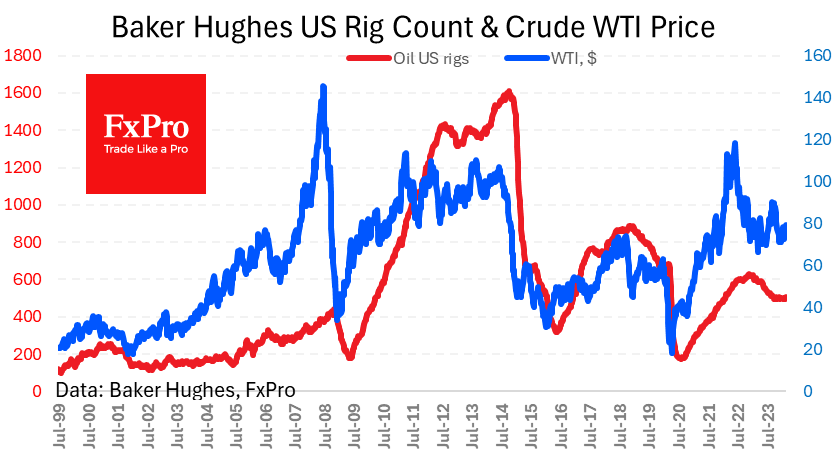

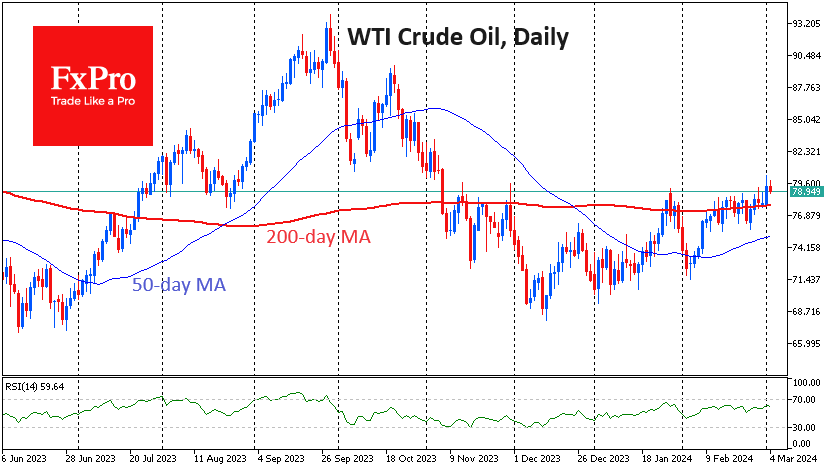

Did Oil Find Its Way Up?

Oil is correcting 0.2% on Monday after closing almost 2% higher on Friday and peaking at 3.4%. WTI’s high of $80.3, last seen in November 2023, and a consolidation above $79 would indicate a break of long-term horizontal resistance, something the bulls have failed to do over the past four months.

Friday’s rally allowed a widening gap to the 200-day moving average, which should also be seen as a demonstration of bullish strength. Technically, there is no significant obstacle to oil rallying to the $89-92 area.

Of course, this bullish outlook is only valid if the coming days confirm oil’s ability to grow from current levels, which has not been the case since November.

OPEC+ is openly playing on the Bulls’ side by extending and strengthening (Russian) oil production and export quotas. The production recovery is postponed indefinitely “depending on market conditions”.

This could be a golden opportunity for the US to regain oil market share, but it is in no hurry to do so. Friday’s data showed that the number of oil drillers rose to 506. That’s the highest since September, but only adding 9 units from the low of 497, which is more stagnation than growth. Just over a year ago – in January 2023 – there were 623 oil and 152 gas-producing wells in operation, compared to 123 now.

Perhaps the price rise will encourage oil producers who are still wary of the green agenda and new sudden price falls. Simply put, America has so far been highly sluggish in playing on the Bears’ side.