Sample Category Title

A Week Packed with Data and Decisions

You wouldn’t know, by looking at the S&P 500’s performance on Friday, that a US regional bank was having a rough time. Almost a year into last year’s regional bank crisis and about a month after a first post-earnings free-fall, the New York Community Bancorp – a commercial real estate lender in New York - fell more than 25% on Friday after saying that it discovered ‘material weaknesses’ in the way it tracks loan risks. The bank wrote down the value of the companies it bought years ago and changed its leadership to deal with the problems. Interestingly, the NY Community Bancorp’s free-fall didn’t really impacted sentiment elsewhere, the KBW’s bank ETF closed the session near flat, the S&P500 rose to a fresh record, its 15th fresh record since the year began, Nasdaq 100 advanced to a fresh record as well, even the small cap index closed the week at an almost 2-year high. While the US regional banks which have a large exposure to commercial real estate sector – which, in turn, is in trouble due to the pandemic hit to activity in commercial real estate and higher interest rates – are still seen on a slippery ground, the Federal Reserve’s (Fed) ability to contain last year’s mini-banking crisis, the efficiency of its liquidity tools and credibility it gained are certainly why the New York Community Bancorp’s issues are taken as a separate case by investors and don’t spill over to the rest of the market.

So, besides for the NY Community Bancorp, Friday was a record-breaking day for major US indices. Stocks in Europe also closed the week on a high note, while the Japanese Nikkei hit a fresh record, at 40'000, before giving back advance early Monday. But news from Europe on Friday weren’t fully soothing for the market bulls. Inflation in euro-area fell last month but not as much as expected. Headline inflation eased from 2.8% to 2.6% versus a fall to 2.5% penciled in by analysts, while core inflation eased from 3.3% to 3.1%, and not to 2.9% as expected by a consensus of analyst estimates on a Bloomberg survey. The higher-than-expected inflation read revived the European Central Bank (ECB) hawks. ECB’s Robert Holzmann couldn’t contain himself in the pre-meeting quiet period and slipped a ‘we have to wait, we cannot rush to a decision’ regarding the rate cuts. The ECB is expected to maintain its policy rates unchanged at this week’s meeting; all eyes and all ears will be on any minor changes in the communique and forecasts. While the morose economic outlook in the region calls for an ECB action, inflation could be a drag to any concrete hint. The ECB has a single mandate – and that’s price stability. Therefore, the ECB won’t cut rates before making sure that inflation is headed toward its 2% target. June looks like the earliest mark for a concrete action.

The EURUSD bounced back above the 100 and 200-DMA after having spent some time below these levels last week. If there is one thing, it is that Europe needs rate cuts more than the US does. European economies’ softer growth outlook should limit the euro’s upside potential against the greenback. I think that price rallies are interesting opportunities for top sellers. The next key resistance stands at 1.0870, the 50-DMA, until the ECB meeting. Unless Lagarde violently pushes back on the rate cut expectations, we should not see the EURUSD record a significant rebound.

In the US, the week will be packed with jobs data and Fed Chair Powell’s congressional testimony. The US economy is expected to have added around 190K new nonfarm jobs, the unemployment rate is seen steady near 3.7% but the wages growth may have slowed in February. Higher job additions and higher pay are inflationary, and should push the Fed cut expectations to an ulterior date, while slower job additions and softer pay rise could pull them forward. The week starts with the expectation that the first Fed cut could come in June with more than a 70% chance assessed to it.

Anyway, if you are willing some stimulus news, you might turn your attention to China’s National People’s Congress. They will likely announce more measures to reach their 5% growth target amid a deepening property crisis and entrenched deflation.

In energy, US crude made an attempt above the $80pb mark on Friday, on rumours that OPEC+ would extend its production cuts to the 2nd quarter. The weekend news confirmed the rumours. The barrel of American crude saw a limited enthusiasm however above the $80pb after the announcement – a sign that OPEC cuts alone won’t keep the price of crude above the $80pb level.

Euro Area Inflation Fell Less Than Expected

In focus today

We get the euro zone Sentix Investor Confidence index this morning at 08.30 CET.

In China the annual key policy event the 'Two Sessions' kicks off today. Focus is on the government's work report at the National People's Congress (NPC). The report will among other things include China's 2024 growth target, which is highly expected to be set again at 5%, albeit this seems rather ambitious given less favourable base effects facing the Chinese economy in 2024.

The party leaders in Sweden's government will give a press conference at 11:00 on new fiscal policies.

Fed's Harker speaks at 17.00 CET.

Economic and market news

What happened overnight

The Japanese stock index Nikkei rose past 40,000 for the first time ever during its Monday session. The index has seen a strong performance so far this year, which amongst other things has been fuelled by a loose monetary policy from the Bank of Japan as well as a weak Japanese yen.

What happened over the weekend and on Friday

In the euro area, inflation numbers on Friday came out strong with core inflation standing at 0.30% m/m, and services inflation at 0.39% m/m. The monthly momentum does not align with the ECB's 2% target, and it fuels fears of upside risk to inflation from wages. Headline HICP came out at 2.6% y/y down from 2.8% in January, falling less than expected. Core inflation stood at 3.1% y/y, down from 3.3% the month before, but had equally been expected to have dropped further. On Friday, we published our ECB Preview - Policy normalisation in sight, 1 March, ahead of Thursday's ECB Governing Council meeting. We believe the ECB will deliver its first rate cut in June, in line with recent speeches by Governing Council members.

In the US, former president Donald Trump won the caucuses in Michigan, Missouri, and Idaho bringing him one step closer to securing the republican nomination. This Tuesday, more than a third of all delegates in the republican race will be up for grabs as the so-called Super Tuesday kicks off. The day may prove final to Trump's only left opponent Nikki Haley whose odds have been slimming as Trump has been securing delegates. Haley secured all delegates in the Washington D.C. primary on Sunday, making it her first win in the 2024 primaries ahead of the Super Tuesday.

On Friday US stock indices Nasdaq and the S&P 500 closed at record levels. Whereas the S&P500 beat its record from the day before, Nasdaq beat its previous record from 2021.

In the Middle East, Israel on Sunday boycotted ceasefire talks with Hamas in Cairo after the organisation rejected Israel's demand of handing over a list of all hostages still alive. A US official had otherwise said Israel had nearly accepted the terms of a proposed ceasefire agreement which would see fighting paused for six weeks.

In the commodity space, OPEC+ decided to extend its output cut to the second quarter of this year. The organization said the cuts could be reversed gradually in accordance with demand. OPEC+ sees demand growth this year land at around 2.25 million barrels per day, whereas the International Energy Agency expects more modest growth of 1.22 million bpd.

Equities: Global equities were higher on Friday across regions with relatively large cyclical outperformance. There were several new all-time highs last week, and the S&P 500 has now been higher in 16 out of the large 18 weeks; this has not happened in more than 50 years. It goes without saying that this fit well into our strategy, but we must also admit that some of our reality gaps are starting to look stretched, limiting the short-term potential in equities. In US on Friday, Dow +0.2%, S&P 500 +0.8%, Nasdaq +1.1% and Russell 2000 +1.1%. Asian markets are mixed this morning just like US and European futures.

FI: European rates ended broadly unchanged on Friday after trading in a 5bp low-to-high range, which left 10y Bunds at 2.41% by the end of day. The February inflation print pointed to the European disinflation process continuing with headline inflation coming in at 2.6% and core at 3.1%. Coupled with the recent guidance from ECB Governing Council members, we see the ECB is on route to deliver a June rate cut. This is aligned with market pricing with 4bp priced by April and 21bp cumulated by June. On Friday night, Portugal got upgraded to A- by S&P as expected. In short term, it should have modest price impact given that Portugal already trades like a single A country.

FX: EUR/USD holds the range of 1.0800-1.0850 and starts this week at the upper end. Likewise, USD/CHF continues to be range-bound. EUR/JPY is close to 163 after last week's high at 163.60. Following strong performance through February, EUR/CHF is just below 0.96 and will take direction from today's Swiss inflation data. EUR/NOK saw a sharp drop on Friday and trades at 11.40, whereas EUR/SEK kicks off this week at 11.20.

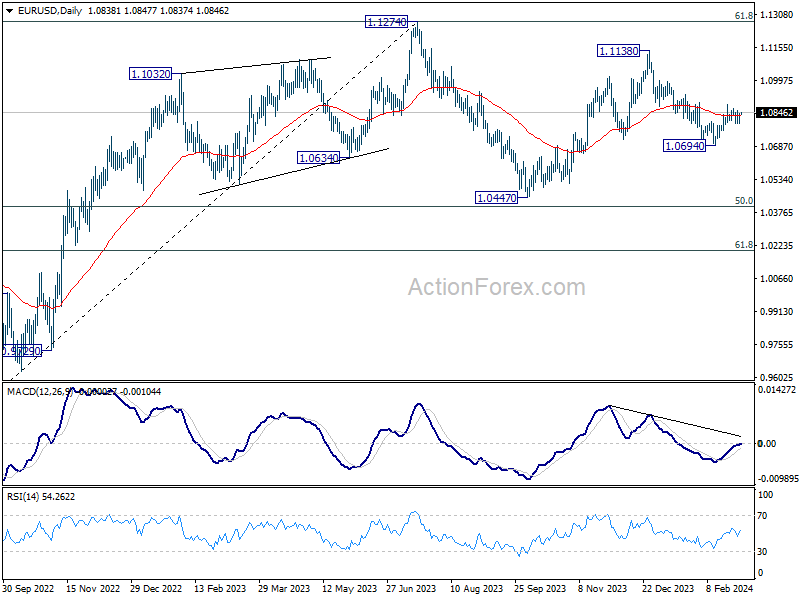

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0808; (P) 1.0825; (R1) 1.0857; More...

Intraday bias in EUR/USD remains neutral as range trading continues below 1.0887. On the upside, break of 1.0887 and sustained trading above 55 D EMA (now at 1.0831) will affirm the case that fall from 1.1138 has completed. Stronger rally would then be seen back to 1.1138. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

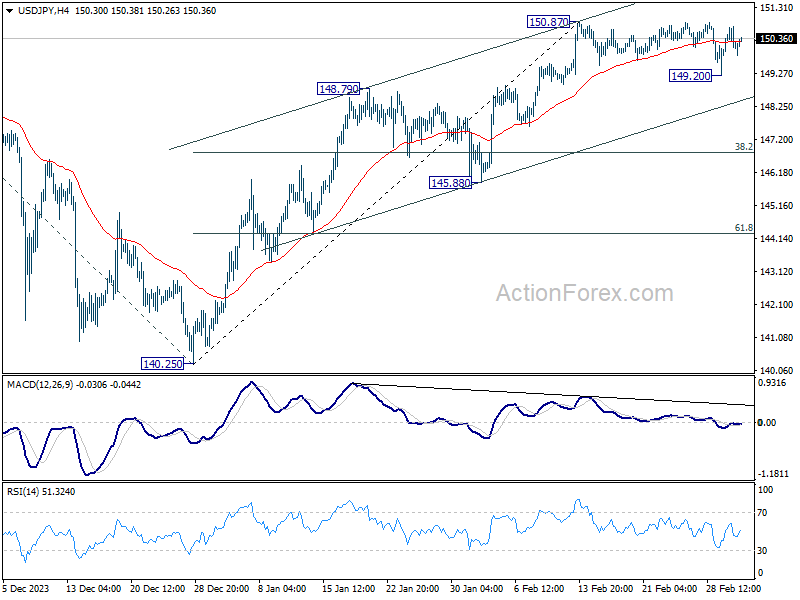

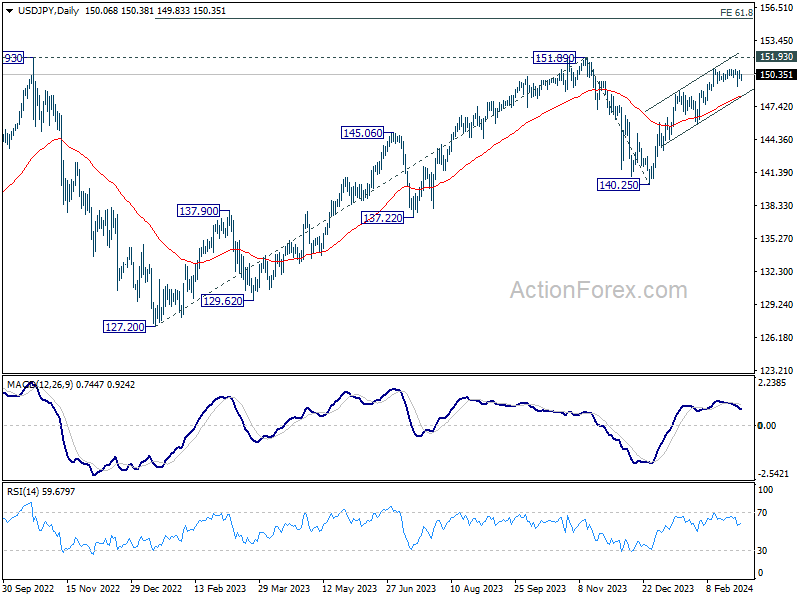

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.79; (P) 150.26; (R1) 150.56; More...

Intraday bias in USD/JPY remains neutral at this point. On the upside, break of 150.87 will resume the rise from 140.25 to 151.89/93 key resistance zone. On the other hand, considering bearish divergence condition in 4H MACD, firm break of 149.20 will confirm short term topping at 150.87. Deeper fall would be seen to channel support (now at 148.47), even as a corrective move.

In the bigger picture, rise from 140.25 is seen as resuming the trend from 127.20 (2023 low). Decisive break of 151.89/.93 resistance zone will confirm this bullish case and target 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. However, break of 148.79 resistance turned support will delay this bullish case, and extend the corrective pattern from 151.89 with another falling leg.

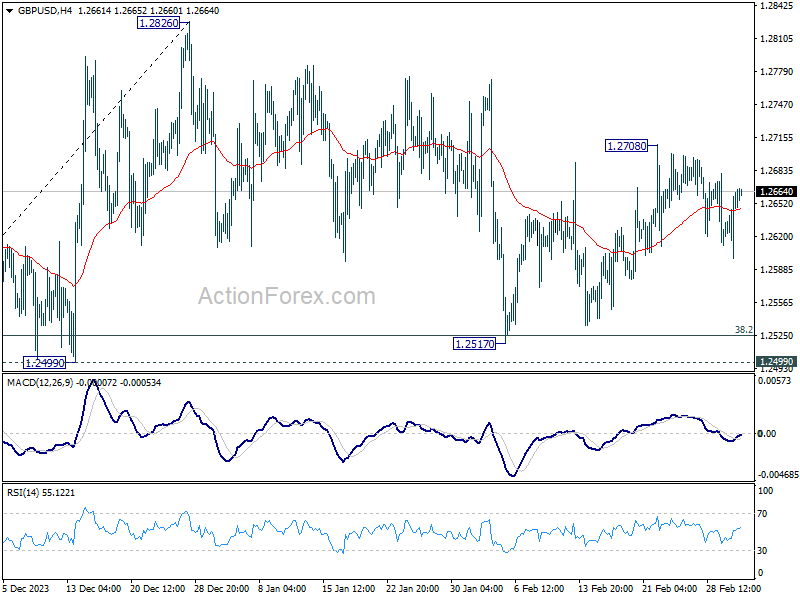

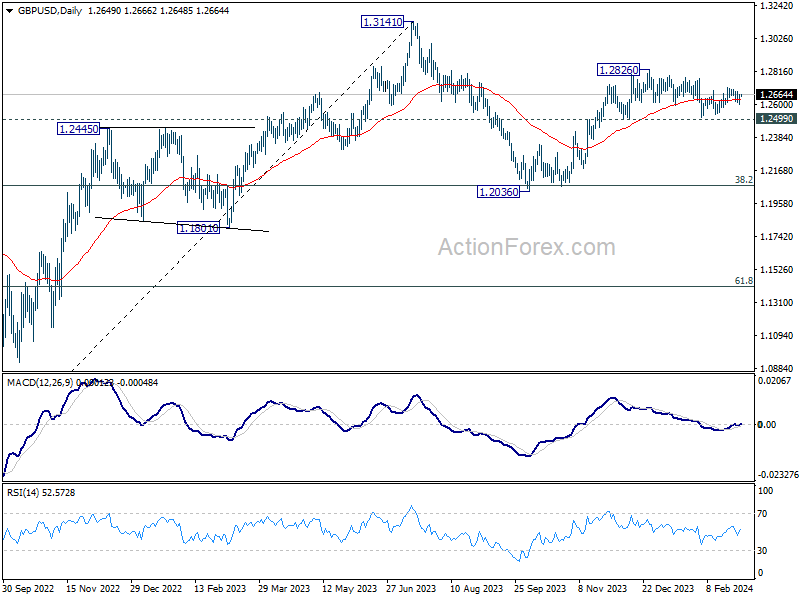

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2615; (P) 1.2640; (R1) 1.2679; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

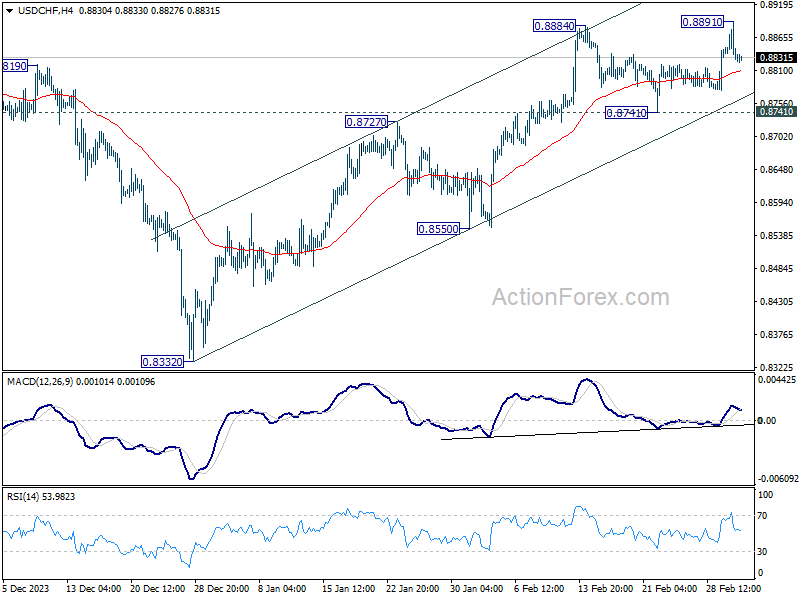

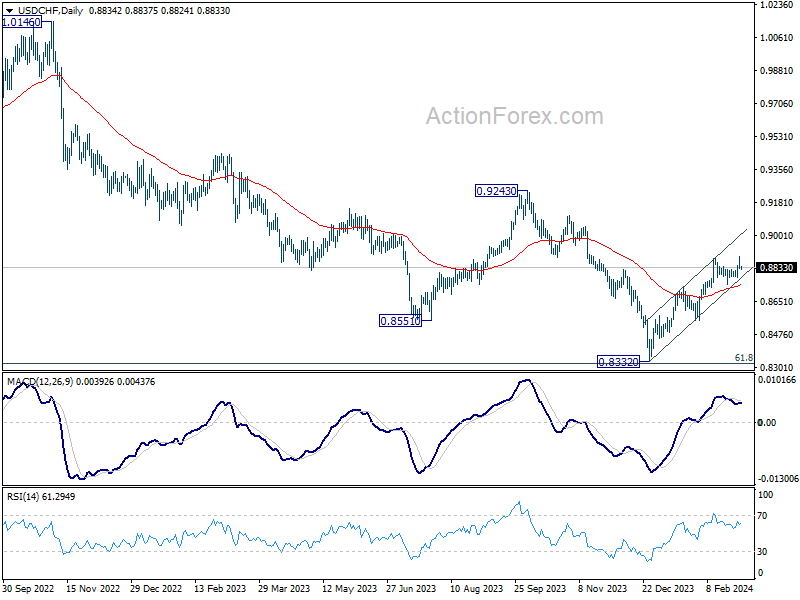

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8811; (P) 0.8852; (R1) 0.8874; More....

Intraday bias in USD/CHF remains neutral for consolidations below 0.8891 temporary top. Further rally is in favor as long as 0.8741 support holds. Break of 0.8891 will resume the whole rebound from 0.8332 towards 0.9243 key resistance. Nevertheless, break of 0.8741 support will turn bias back to the downside for deeper pullback.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

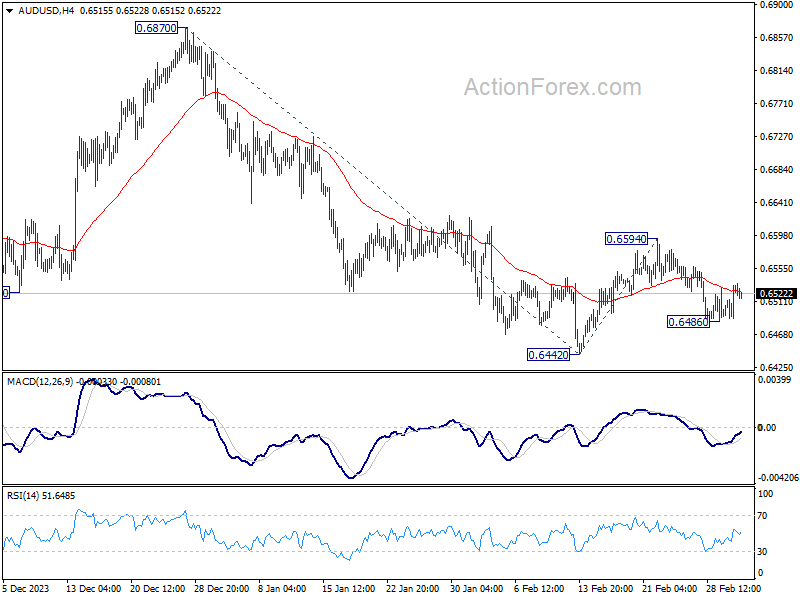

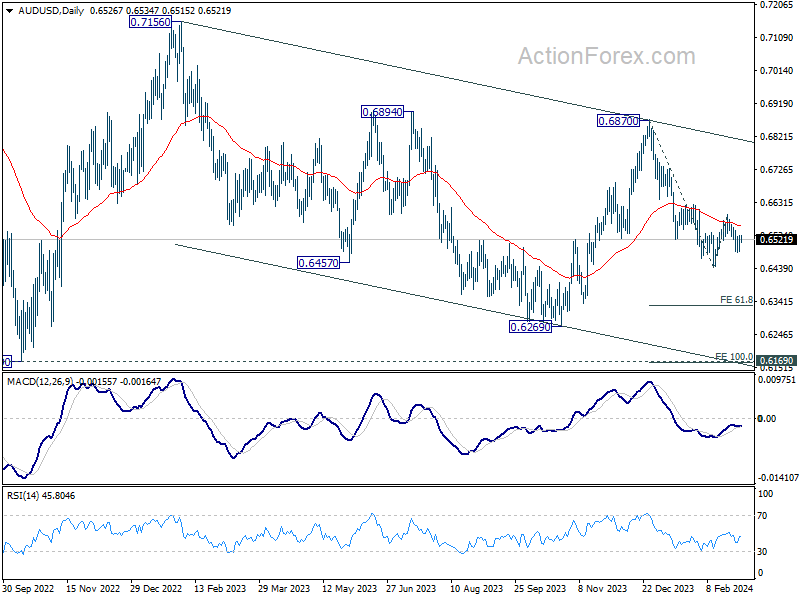

AUD/USD Daily Report

Daily Pivots: (S1) 0.6499; (P) 0.6517; (R1) 0.6543; More...

Intraday bias in AUD/USD remains neutral for consolidations above 0.6486 temporary low. But further decline is expected as long as 0.6594 resistance holds. On the downside, below 0.6486 will target a retest on 0.6442 first. Firm break there will resume whole decline from 0.6870. However, on the upside, break of 0.6594 will resume the rebound from 0.6442 and turn bias back to the upside instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

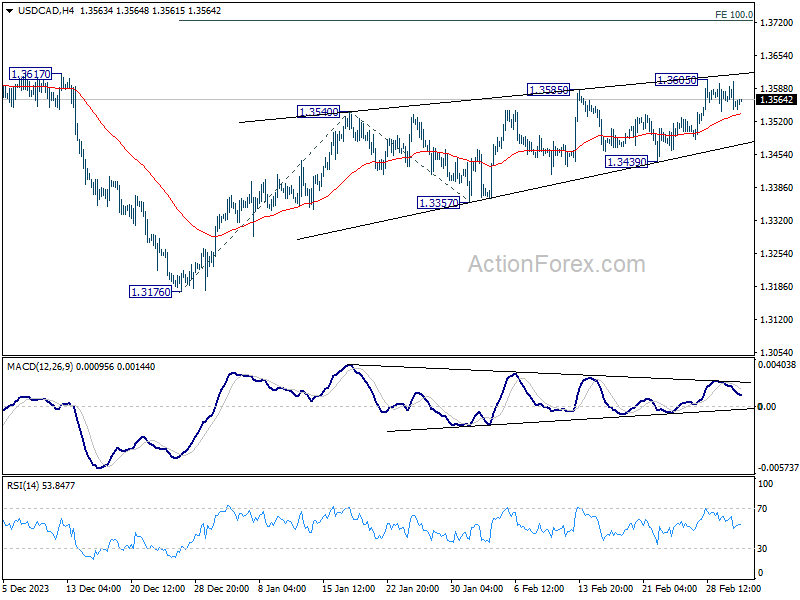

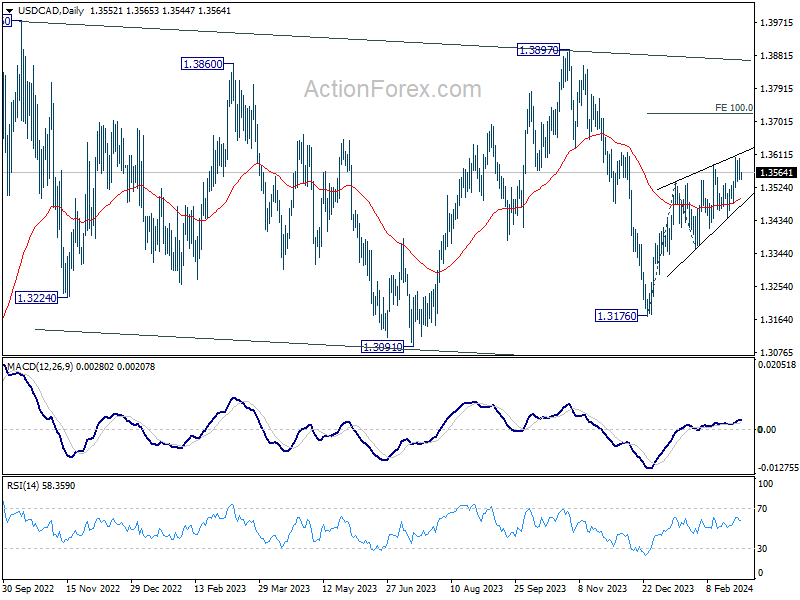

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3536; (P) 1.3569; (R1) 1.3593; More...

Intraday bias in USD/CAD remains neutral as consolidations continue below 1.3605 temporary top. Further rally is expected as long as 1.3439 support holds. Break of 1.3605 will resume the rise from 1.3176 and target 100% projection of 1.3176 to 1.3540 from 1.3357 at 1.3721 next.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

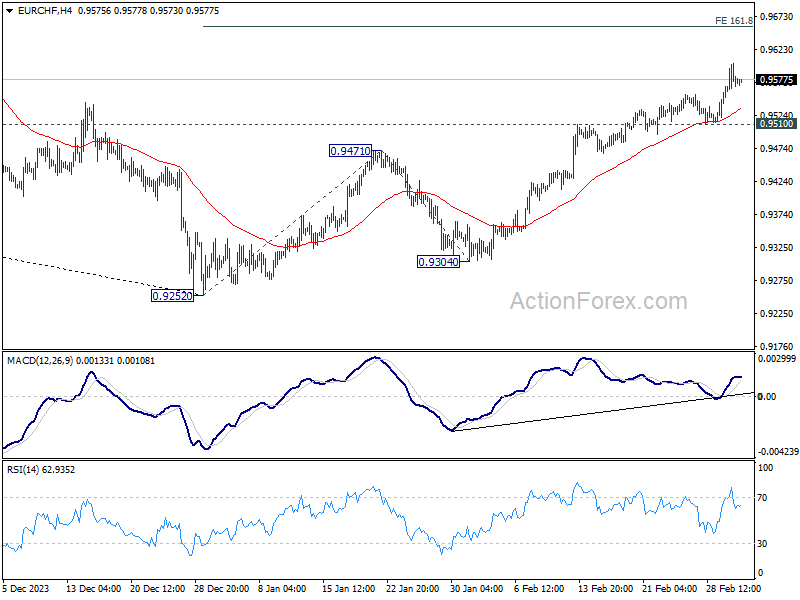

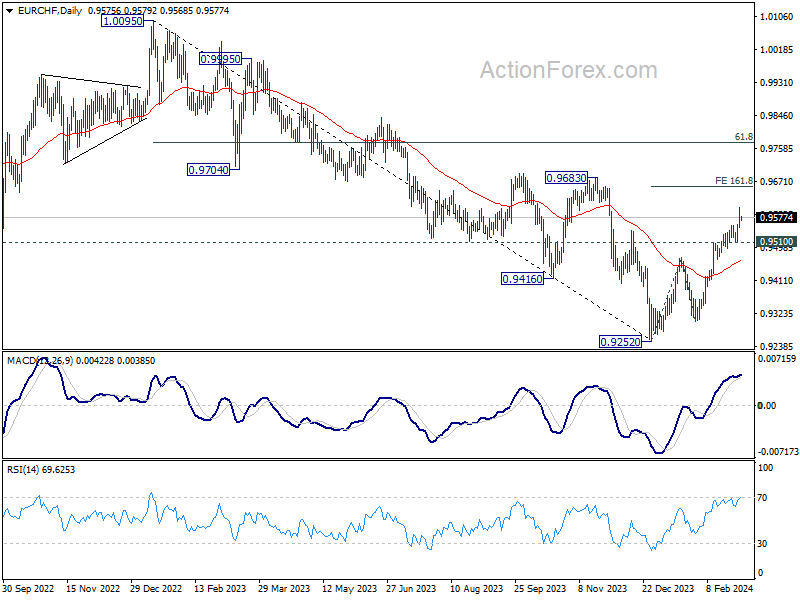

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9550; (P) 0.9578; (R1) 0.9603; More...

Intraday bias in EUR/CHF remains on the upside at this point. Current rise from 0.9252 is in progress for 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. For now, further rally is expected as long as 0.9510 support holds, in case of retreat.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9622) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.9% retracement of 1.0095 to 0.9252 at 0.9773 and above.

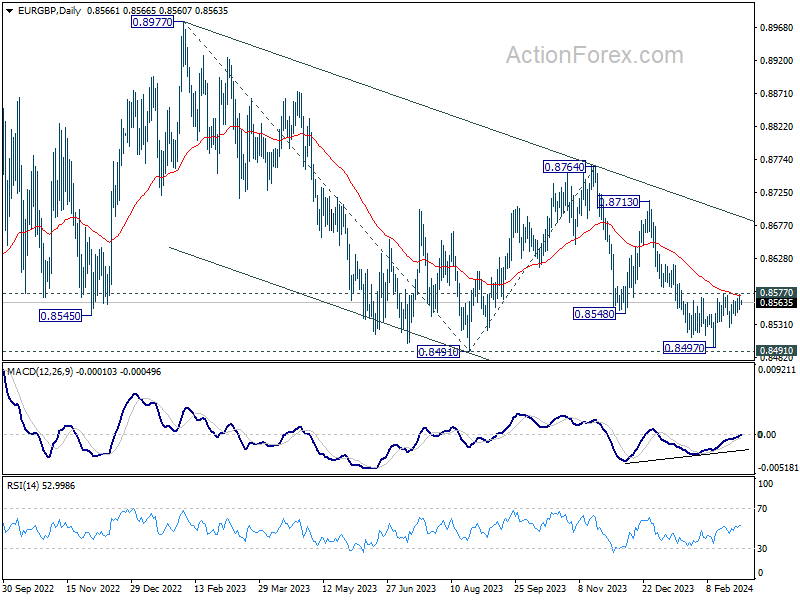

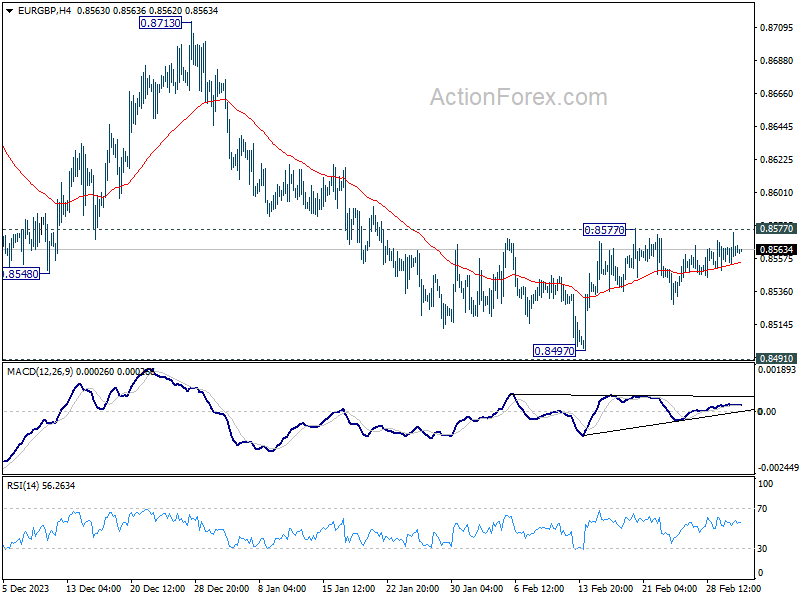

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8555; (P) 0.8565; (R1) 0.8577; More...

Intraday bias in EUR/GBP stays neutral for the moment. Considering bullish convergence condition in D MACD, decisive break of 0.8577 and 55 D EMA (now at 0.8574) will argue that fall from 0.8764 has completed. Intraday bias will be back on the upside for rebound towards 0.8713 resistance. Nevertheless, firm break of 0.8491/7 support zone will confirm larger down trend resumption.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.