Sample Category Title

Australian Dollar Slides After CPI Stays Steady

The Australian dollar took a hit after Australian inflation was lower than expected. In the North American session, AUD/USD is trading at 0.6493, down 0.78%.

CPI holds steady at 3.4%

Australia’s inflation rate remained steady in January at 3.4% y/y, unchanged from December and below the market estimate of 3.6%. This matched the lowest rate of annual inflation since November 2021. The Reserve Bank of Australia’s preferred core indicator, the trimmed mean, dropped to 3.8%, its lowest level since March 2022.

The soft inflation data is an encouraging sign for the Reserve Bank of Australia that its aggressive rate-tightening cycle is keeping inflation in check and the upper level of the 1%-3% target range is not too far off. More importantly, it reduces the likelihood that the RBA will hike rates and raises expectations of two or three rate cuts late in the year. This explains the sharp decline in the Australian dollar today, as lower interest rates would make the Australian dollar less attractive to investors.

The RBA has raised rates only once since June 2023 and hasn’t ruled out rate hikes, although the markets believe that this is posturing by the central bank and the tightening cycle is over. Still, the RBA is unlikely to jump on the rate-cut bandwagon until it is convinced that inflation will continue to fall or the strong labour market shows signs of cooling. The next meeting is on March 18th and the RBA is widely expected to maintain rates and continue its “higher for longer” stance.

AUD/USD Technical

- AUD/USD has pushed below support at 0.6584 earlier and is putting pressure on support at 0.6453

- 0.6526 and 0.6560 are the next resistance lines

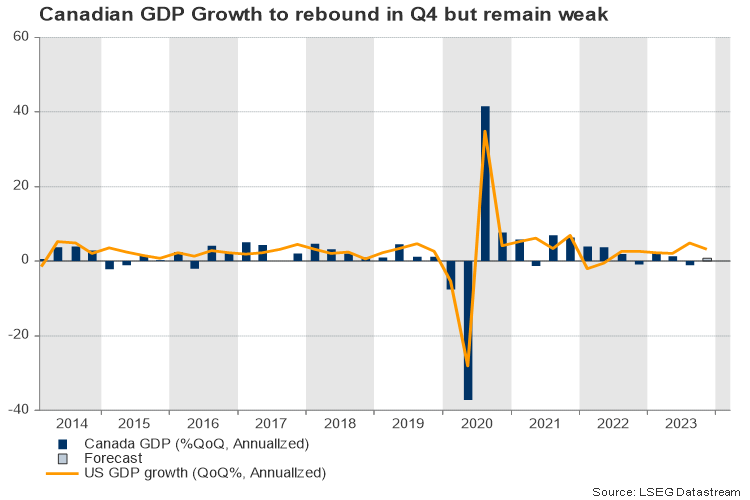

Canada’s GDP to Rebound But Not the Loonie

- Canadian economy set to return to growth but remain sluggish

- Will the Loonie be able to capitalize on any good news?

Canadian economy to avoid recession once again

The Canadian dollar has barely made any serious progress against other major currencies this year besides the battered Japanese yen. Canadian Q4 GDP data may not come to the rescue on Thursday to give the much-needed boost, but investors will still look for any signs rate cuts will be necessary sooner than later.

The Canadian economy experienced a mild quarterly contraction of 0.3% in the three months to September and shrank by 1.1% in annualized terms on the back of falling exports and muted household spending. While a technical recession would have been the case, an upward revision in the second quarter data did not meet the rule of “two consecutive negative quarters”.

Analysts believe that the economy escaped a recession in the last quarter too, finishing the year 0.8% stronger in annualized terms. Such news would bring some relief to analysts, but perhaps only temporarily, as the overall economic picture would still remain fragile.

Canada vs US

Compared to its US cousin, Canada has been facing choppier growth, probably because of the relatively tighter fiscal spending, which Biden’s administration enhanced significantly to boost production incentives, especially in the semiconductor industry through its CHIPS act. Perhaps Trudeau’s administration might also seek more fiscal engagement when the 2025 election season starts to heat up.

Moreover, Canadian mortgage holders can enjoy fixed interest rates for a period of no more than five years, which makes them more vulnerable to rate changes. On the other hand, their US counterparts are allowed to pay steady borrowing costs for the entire term of the mortgage, which can last up to thirty years.

Last but not least, the Canadian economy is smaller and more exposed to international trade, with exports and imports accounting for more than 60% of its GDP compared to the US’s 25%. Hence, businesses might be more conservative with their future investment plans as their second-best trade partner, China, might have a bumpy road ahead and the European Union might keep struggling with a changing geopolitical landscape.

Hence, with the headline CPI inflation having slipped below 3% and back into the BoC’s range target of 1-3%, investors might think that lower interest rates will arrive earlier in Canada than in other major economies, especially if economic growth remains stagnant.

Inflation falls into the BoC range target, but confirmation needed

Yet, the decision of rate cuts may not be straightforward for the central bank. January’s CPI data showed that underlying inflation was still above 3.0% y/y, while shelter prices continued to grow by more than 6% y/y. Therefore, given the pickup in wage growth, premature rate cuts could cause an inflation resurgence. Note that futures markets are currently eyeing 69bps of rate cuts throughout 2024. The odds are relatively higher in the second half of the year but show no confidence for any meeting.

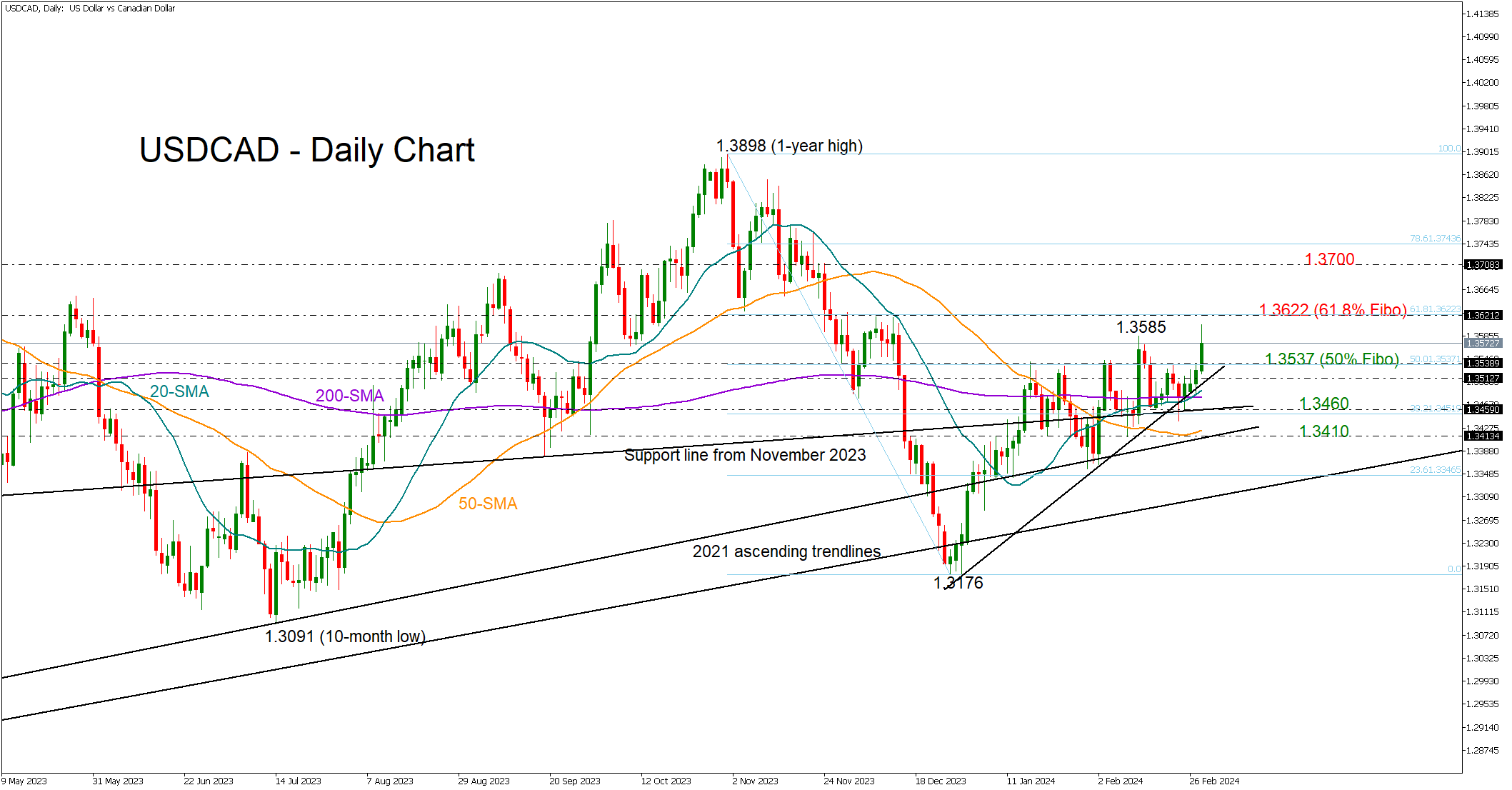

USDCAD levels to watch

Meanwhile in FX markets, the loonie has already given up half of its November-December gains against the greenback, falling to a new two-month low of 1.3600 per US dollar earlier today. Stronger-than-expected GDP prints might provide a helping hand to the loonie, though any potential gains might be short-lived as inflation is still the only game in town.

Technically, USDCAD could extend its uptrend towards the 1.3622 resistance area, a break of which might trigger an aggressive rally towards the 1.3700 round level. Otherwise, the pair could flip backwards to test the 1.3537-13515 support region ahead of its 20- and 200-day simple moving averages (SMAs). The 1.3410-1.3460 restrictive zone could be the next destination on the downside.

Sunset Market Commentary

Markets:

Yesterday’s US data (shipments, durable goods orders, house prices, consumer confidence) was mixed and failed to given guidance for (bond) trading. (US) markets over the previous two months reverted to a more neutral positioning, putting themselves in line with the December Fed dots ‘guiding’ 75 bps of cumulative rate cuts by the end of the year. To really move away from this equilibrium, markets need hard news, but this wasn’t available today. US Q4 GDP was marginally downwardly revised (3.2% Q/Qa), but the core PCE price index printed slightly higher (2.1%). Still, this remains old news. Tomorrow’s US January PCE deflators and maybe even more the ISM’s (manufacturing on Friday, services on Tuesday) should provide more forward looking insights. US yields are changing less than 2 bps across the curve. A similar set-up for European interest rate markets: investors are counting down to tomorrow’s flash EMU CPI estimate. Favourable base effects compared to last year should result in a renewed decline (headline expected 0.6% M/M but the Y/Y measure easing from 2.9% to 2.5%, core expected at 2.9% Y/Y from 3.3%). Base effects for EMU CPI will remain favorable in March and April. However, the ECB will keep a close eye at the underlying (monthly) dynamics and at the potential impact of wage negotiations on inflation going forward. Soft EC confidence data (economic confidence down from 96.1 to 95.4) published today at least suggest that sentiment doesn’t call for wage exuberance. In technical trading, German yields soften less than 1 bp. Markets still pinpoint the first ECB rate cut at the June meeting. Equities ease marginally but stay near recent peak levels (EuroStoxx -0.15%, S&P -0.35%). Oil is drifting higher (Brent $84/b) as markets are pondering headlines that OPEC+ will (have to) extend voluntary production. On FX, the dollar gains modestly without changing the (neutral) technical set-up. DXY regains the 104 barrier (open 103.81). USD/JPY (150.7) gains marginally, with the February top (150.89) and the cycle multi-year peak levels (151.91/95) again within reach. The euro underperformed, especially this morning, as EUR/USD quickly dropped to test bids just below 1.08. We didn’t see an unequivocal trigger. Were negative comments from Russian officials on French President Macron’s idea to potentially deploy NATO troops in Ukraine in play? Whatever the driver, EUR/USD gradually recouped part of the initial loss to currently trade near 1.0825. Sterling still underperforms a soft euro, with EUR/GBP changing hands near 0.856.

News & Views:

Belgian inflation accelerated to 0.71% M/M in February with Y/Y-inflation increasing from 1.75% to 3.20%, the highest level since August of last year. Energy inflation is negative since February 2023 but now stands at -5.34% Y/Y from -22.30% Y/Y in January. Food inflation (including alcoholic beverages) has decreased for the 11th month in a row and now stands at 4.65% from 6.58%. Core inflation, which does not take into account price evolutions of energy products and unprocessed food, has decreased for the 9th month in a row and now stands at 4.25% from 4.70% in January. Services inflation decreased to 4.92% from 5.15% and rent inflation to 5.72% from 5.91%. The first inflation estimate according to the European harmonised index of consumer prices (HICP flash estimate) for Belgium amounts to 3.6% for February 2024. In a separate release, the NBB downwardly revised the Q4 growth figure from 0.4% Q/Q to 0.3% with the Y/Y growth at 1.5% instead of 1.6%. Household consumption rose by 0.5% Q/Q, mainly driven by purchases of durable goods. Imports of goods and services fell sharply (-1.2% Q/Q) while export remained stable, resulting in a positive contribution of net exports. Business investments contracted sharply (-8.5% Q/Q) in a general slowdown that was compounded by a number of specific transactions relating to the foreign sales of ships. Government spending and public investment rose by 2% and 0.5% respectively.

Polish state-run economic think-thank PIE estimates that the EU recovery funds just assessed by the Polish government will boost the country’s GDP by 0.2% this year, 1.2% in 2025 and 0.6% after that. They calculated the impact using access to about €60bn of EU’s post-pandemic recovery funds earmarked for Poland (compared to total amount of unblocked payments of €137bn).

Kiwi Dollar Flies Down

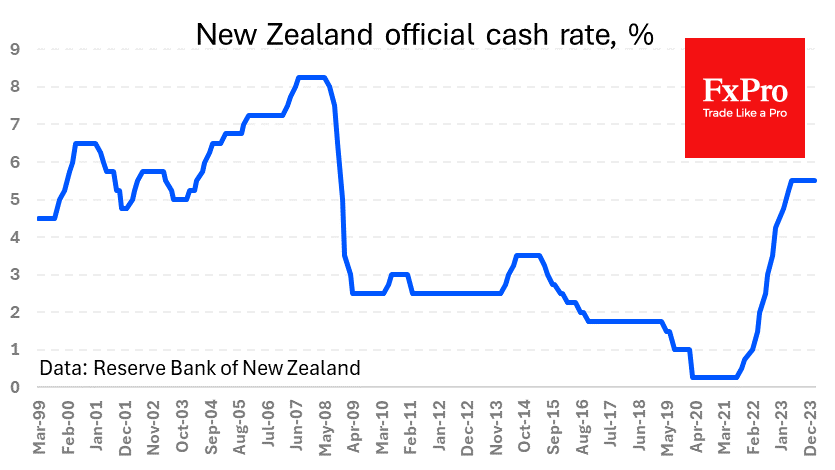

The New Zealand Dollar is down 1.2% since the start of the day on Wednesday due to disappointment with the RBNZ’s actions and comments. The country’s central bank left its key interest rate unchanged at 5.5% and signalled its willingness to keep it at current levels. This is much softer than expected, as markets had been pricing in some chance of a hike at this meeting. To meet such expectations, the RBNZ would have had to at least warn that it was ready to do so in the near future.

In the accompanying commentary, however, the central bank merely indicated that it was prepared to keep interest rates at current restrictive levels for longer than the bond markets expect. One can understand the RBNZ’s reluctance to tighten at a time when the central banks of the major developed countries are discussing the start of rate cuts.

It is also worth remembering that New Zealand has raised rates by 525 basis points this cycle, which is comparable to the Fed’s tightening, while most other central banks have not tightened as much.

The RBNZ’s current decision has implications beyond small New Zealand, but it shows a definite change in tone from the central bank despite inflation running above the target. This RBNZ dovishness is, in our view, a key driver of the USD’s strength against its peers on Wednesday afternoon.

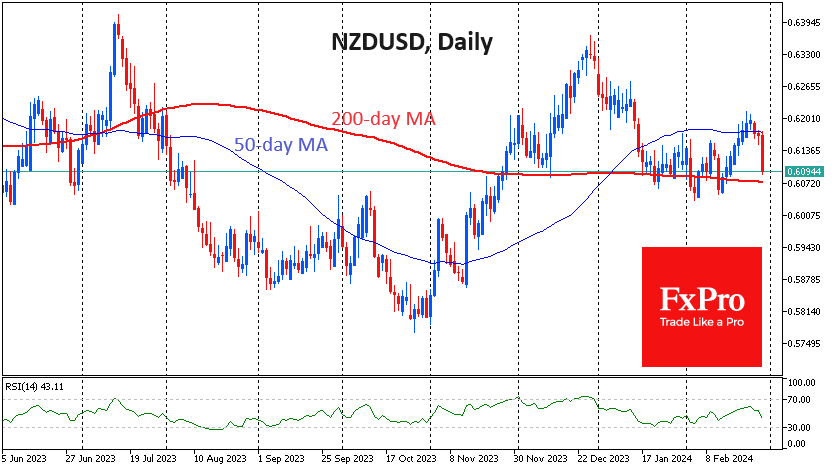

Separately, it is worth considering the implications of the Kiwi’s current failure for the technical picture. The NZDUSD reversed to the downside at the end of last week, failing to break above the 50-day moving average. Today, the bulls finally capitulated, creating a solid move. Such momentum is often the start of a longer trend.

However, the bears’ willingness to keep pushing the market lower is about to face a significant test in the form of the 200-day moving average. It passes 0.6070 against the current price of 0.6090 and 0.6170 earlier in the day. The pair has crossed from the bottom to the top of this curve since the second half of January and has found buying support on dips below it. A revised view on monetary policy seems to be reason enough to break below a vital trendline, but we will have to wait for a break of the 200-day moving average from top to bottom first.

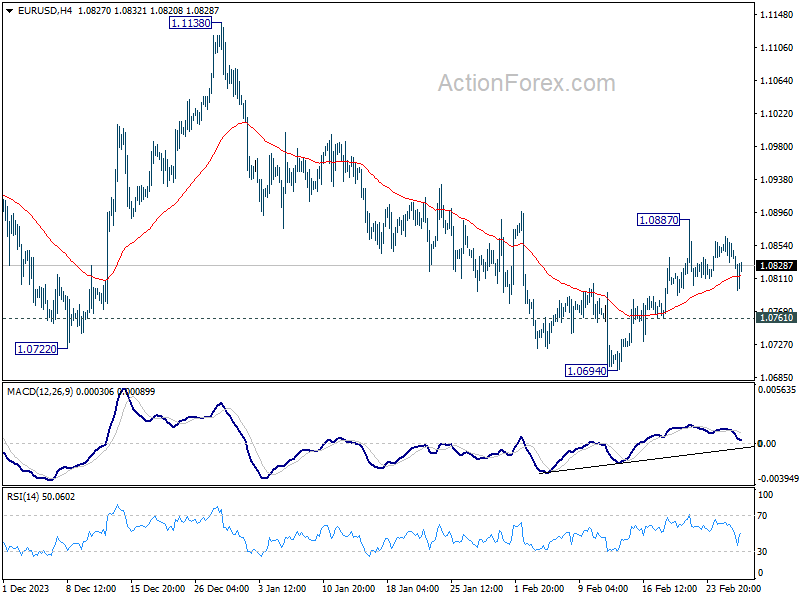

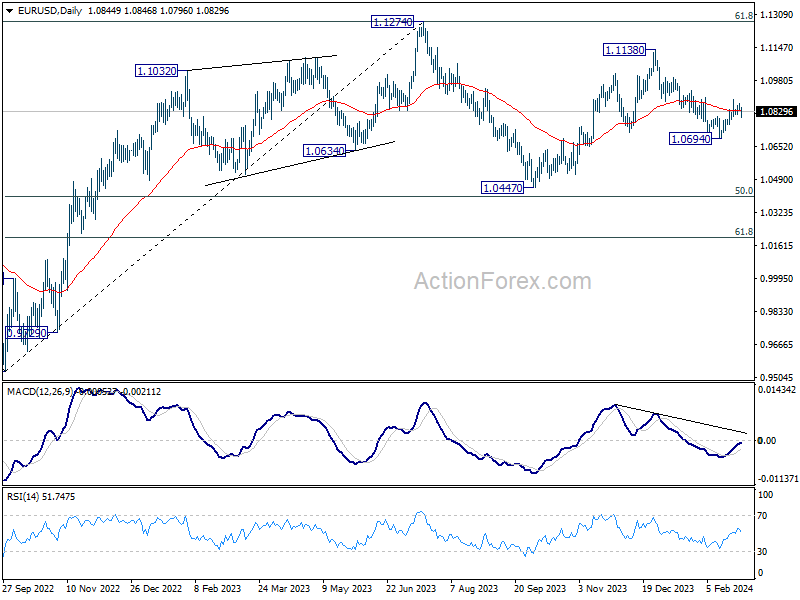

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0830; (P) 1.0848; (R1) 1.0863; More...

EUR/USD dips notably today but stays above 1.0761 minor support. Intraday bias stays neutral for the moment. On the upside, break of 1.0887 and sustained trading above 55 D EMA (now at 1.0832) will affirm the case that fall from 1.1138 has completed. Stronger rally would then be seen back to 1.1138. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

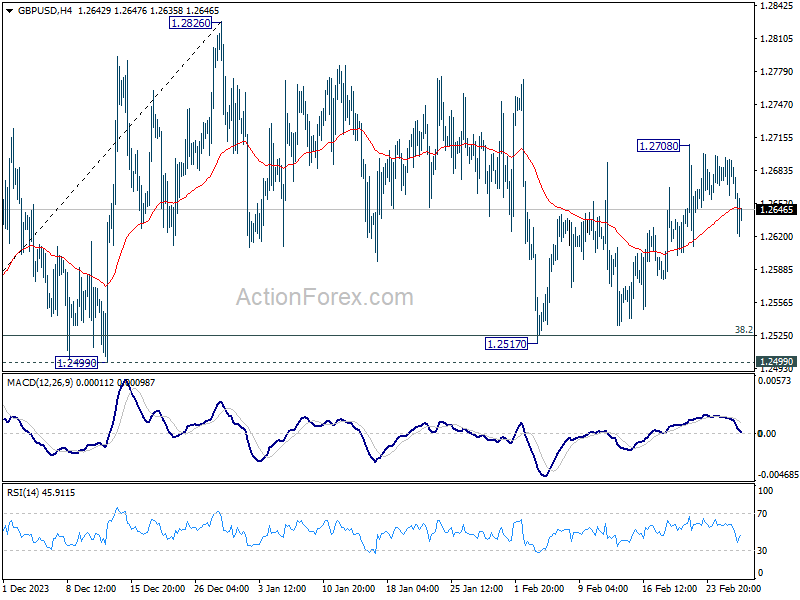

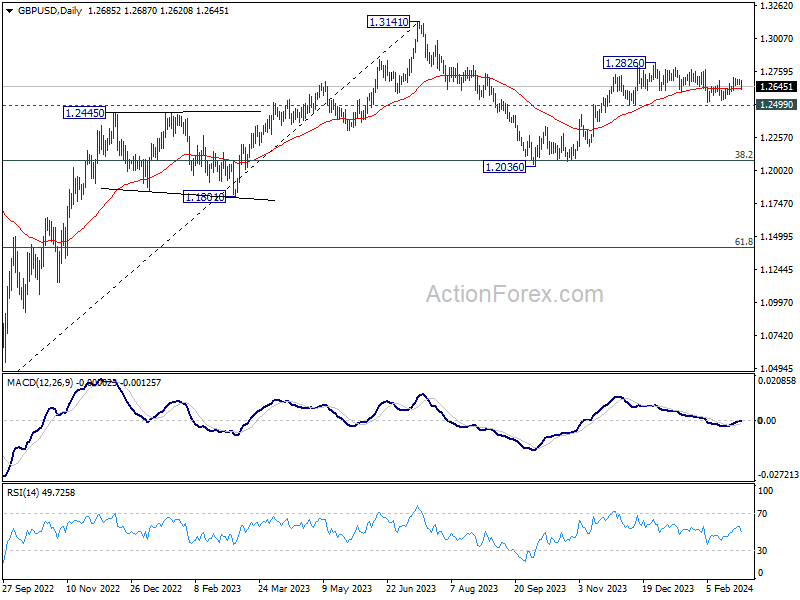

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2665; (P) 1.2681; (R1) 1.2702; More...

While GBP/USD dips notably today, downside is held well above 1.2517 support. Intraday bias remains neutral first and outlook is unchanged. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

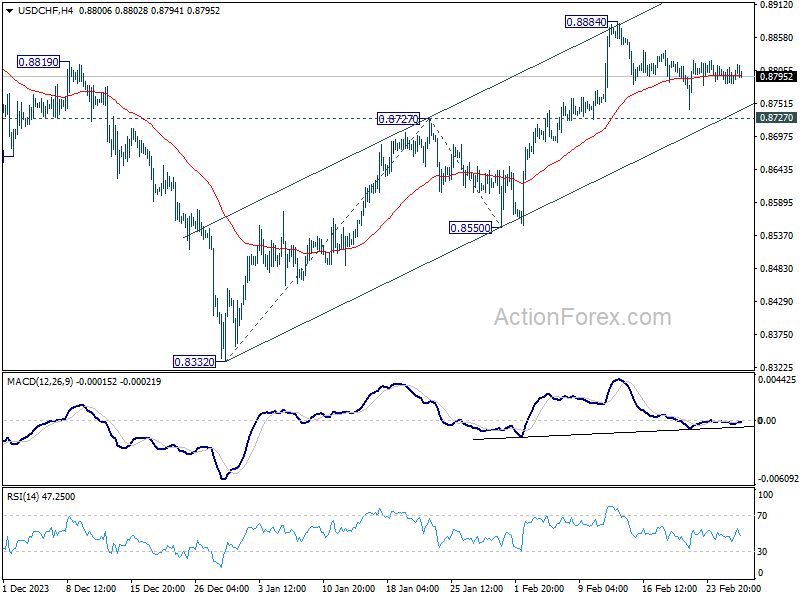

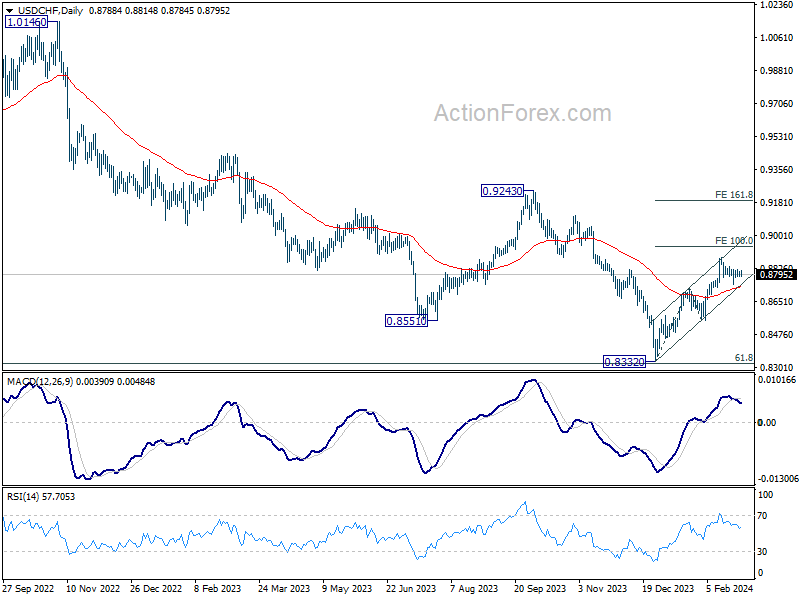

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8776; (P) 0.8794; (R1) 0.8803; More....

Intraday bias in USD/CHF remains neutral as consolidation from 0.8884 is still extending. With 0.8727 resistance turned support intact, further rally is expected. On the upside, above 0.8884 will resume the rally from 0.8332 to 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

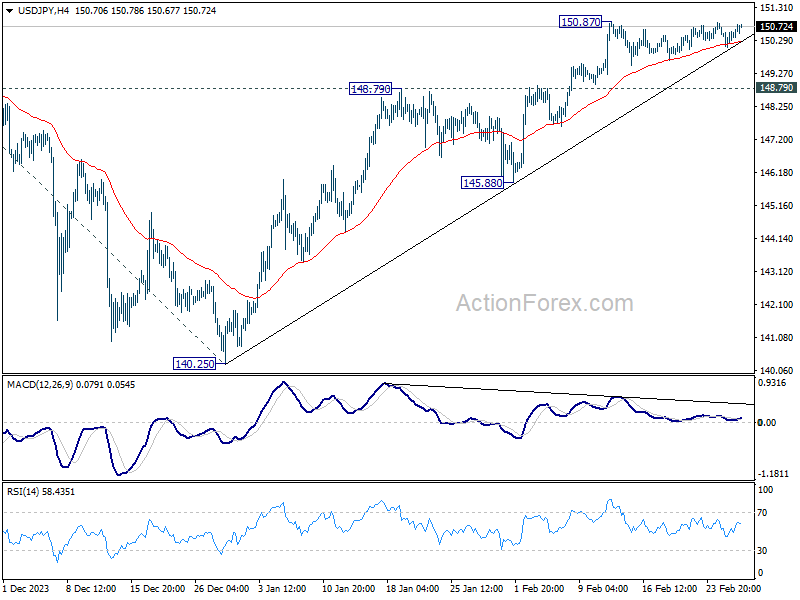

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.17; (P) 150.44; (R1) 150.81; More...

No change in USD/JPY's outlook as range trading is still continuing. Intraday bias stays neutral at this point. In case of deeper retreat, downside should be contained by 148.79 resistance turned support to bring rebound. On the upside, break of 150.87 will resume 140.25 to 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next.

In the bigger picture, rise from 140.25 is seen as resuming the trend from 127.20 (2023 low). Decisive break of 151.89/.93 resistance zone will confirm this bullish case and target 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. However, break of 148.79 resistance turned support will delay this bullish case, and extend the corrective pattern from 151.89 with another falling leg.

US: Economic Resilience Remains on Full Display in Q4 GDP Data, Despite Slight Downward Revision

The second estimate of fourth quarter real GDP was revised down a hair to 3.2% annualized (3.3% prev.), only slightly below consensus expectations for no revision.

Under the hood, downward revisions to inventory investment and federal government spending were partly offset by upward revisions to state and local spending, consumer spending, and housing investment.

Overall government spending saw a decent upgrade to a 4.2% annualized pace (3.3% prev.), thanks to 5.4% growth in state and local government outlays. These outlays have been boosted by generous federal transfers through the pandemic and in infrastructure spending initiatives passed since. Inventory investment flipped from adding a tenth to growth to subtracting 0.3 percentage points in Q4

Consumer spending was upgraded to a 3% pace in the fourth quarter (2.8% prev.) on higher outlays for services. Business invest saw an upward revision to 2.4% (1.9% prev.), thanks to big upgrade to structures investment to 7.5% (3.2% prev.) and a smaller upgrade to intellectual property products +3.3% (+2.1% prev.). However, equipment investment was revised to a contraction (-1.7% vs. +1.0% prev.).

We have to wait until the end of March for Gross Domestic Income and Corporate Profit data, which are delayed one month in the fourth quarter's data. A sizeable gap had opened up between GDP and GDP in the third quarter, with GDP putting economic activity about 2.4% higher than GDI.

Key Implications

If possible, there was mostly good news in the downward revision to GDP growth in the fourth quarter. Final domestic demand was revised up to 3.1% (2.7% prev.). This strength in domestic demand provides a solid base for momentum heading into 2024 . We won't have to wait long to find out how consumers started the year, with personal income and spending for January due tomorrow.

With the economy holding up remarkably well and the labor market still tight by historical standards, policymakers can afford to proceed carefully over the coming months. Economic growth is still running well above its long-run potential, implying the near-term risks to the inflation outlook are skewed to the upside. From the Fed's standpoint, this means any imminent rate cuts are off the table, and policymakers are likely to remain on hold until at least this summer.