Sample Category Title

Swiss KOF falls to 101.6 in Feb, rather positive economic signals intact

Swiss KOF Economic Barometer fell from 102.5 to 101.6 in February, below expectation of 102.0. Despite this marginal cooling, KOF maintains an optimistic stance regarding the Swiss economy, asserting that "the rather positive economic signals in Switzerland remain intact."

This assertion is particularly relevant to manufacturing and construction sectors, which have seen an improvement in their outlooks. Contrastingly, projections for financial and insurance services, hospitality, other services, and foreign demand have experienced a downturn. Meanwhile, forecast for private consumption within Switzerland remains stable.

Swiss GDP grows 0.3% qoq in Q4, abv exp 0.1% qoq

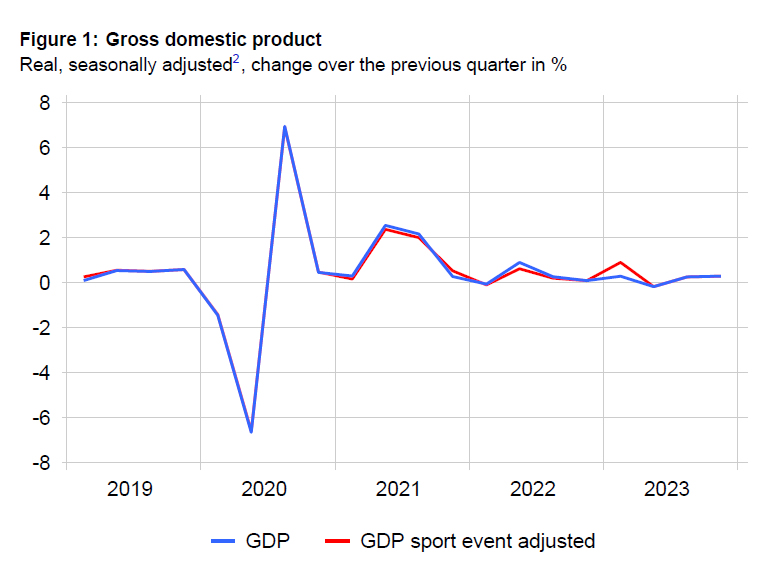

Switzerland's GDP grew by 0.3% qoq in Q4, slightly surpassing expectation of 0.1% qoq growth.

Despite this modest uptick, the nation faced slight decline in domestic final demand, which fell by -0.3%. This downturn was primarily driven by a significant, broad-based decrease in investments in equipment, plummeting by -2.5%. Construction investment also fell by by -0.3%, which in turn, led to -0.2% decrease in the construction industry.

Meanwhile, private consumption saw a marginal increase of 0.3%, buoyed by spending in housing, health, mobility, and foreign travel sectors. However, spending on food and other retail goods witnessed a decline. The retail and trade sectors also reported contraction, with retail dropping by -0.3% and trade by -1.0% . Additionally, imports of goods and services showed weak performance, registering 0.7% increase after adjusting for sporting events.

AUDJPY Correction Has Reached Short Term Support Area

The short-term Elliott Wave View in the AUDJPY suggests that the cycle from 01 February 2024 low unfolded in an impulse sequence and shows a bullish sequence supporting more upside. Whereas the rally to 96.92 high ended wave (i), a pullback to 96.18 low ended wave (ii). A rally to 97.67 high ended wave (iii) then a pullback to 97.04 low ended wave (iv). Above from there, a rally to 99.05 high ended wave (v) thus ended wave ((i)) in a 5 wave structure.

Down from there, the pair is doing a short-term pullback in wave ((ii)) to correct the cycle from the 2/01/2024 low. The pullback from the peak is unfolding as Elliott wave double three correction where wave (w) ended at 98.18 low in 3 swings. While a bounce to wave (x) ended at 98.62 high and started the (y) leg lower. Towards 97.47- 97.20 100%- 161.8% Fibonacci extension area of (w)-(x) blue box area. Near-term, as long as it remains above the 97.20 low the pair is expected to find buyers from the blue box area for the next leg higher or should produce a 3 wave reaction higher at least.

AUDJPY 1-Hour Elliott Wave Chart

AUDJPY Elliott Wave Video

https://www.youtube.com/watch?v=MDDSKErwBGY

USD/JPY Tanks About a Full Yen

Markets

Barring an outdated US Q4 GDP and PCE revision there was again not much to inspire markets yesterday. Speeches from Fed’s Williams, Collins and Bostic yielded the known mantra of data dependency and caution against premature cuts. That resulted in muted trading. Core bonds gained with US Treasuries outperforming, specifically into the final hours of US trading. Net daily changes varied between -2.2 (30-y) and -5.6 bps (2-y). German yields eased less than 2 bps Equities meandered around the highs. Wall Street recorded some minor losses. Investors favoured the largest currencies over the likes of NOK, SEK and especially AUD (weaker than expected January CPI) and NZD (central bank softened its rate hike threat). EUR/USD closed almost unchanged but experienced a sharp intraday U-turn. The pair tested the 1.08 big figure in early European dealings. Some flagged French president Macron’s apparent openness towards (NATO) boots on the Ukrainian ground and the Kremlin’s staunch warning against it as a reason for euro weakness. The common currency recovered in the hours after. The trade-weighted dollar eked out a small gain to just south of 104. Sterling and the Japanese yen completed the top four of the scoreboard. The latter is jumping straight to the first place this morning, though. Bank of Japan Takata gave a strong signal towards the end of the central bank’s ultra-easy monetary policy. He said the 2% price target is finally coming into sight and put Japan “at a juncture for a shift in the entrenched belief that wages and inflation won’t rise.” His speech comes at a time when dwindling growth momentum and decelerating (but still above-target) inflation is closing the BoJ’s window of opportunity. Takata’s “It’s fine to shift the gear one notch lower” now rekindles speculation even if he said it wouldn’t be one rate hike after another. USD/JPY tanks about a full yen to below 150. Japanese yields rise between 0.9 and 2.6 bps with the 2-y setting a new 13-year high. US Treasury yields are broadly stable and currencies ex JPY trade mostly flat. Today’s economic calendar finally gets a bit interesting. The US publishes PCE deflators for January. These lag the regular CPI’s but being the Fed’s preferred inflation gauge they are worth following. Other US data include weekly jobless claims and personal income & spending. The European eco calendar focuses at national inflation readings from France & Germany over Spain to Portugal. Risks, if any, are slightly tilted to the downside. Markets have come a long way in finally adjusting to central bank talk. For this reason both US PCE and European CPI would have to deviate strongly in one way or another to unlock the rates – and by extension the FX stalemate.

News & Views

News agency Bloomberg refers to an email sent out by the US Bureau of Labour Statistics, commenting on the unexpected surge in January CPI inflation and more specifically rental inflation. The BLS indicates that the weights for single family detached homes increased materially from December 2023 to January 2024. The relative weighting compared to multifamily units changed. Both contribute to the owner equivalent rent (OER) component which is by far the largest individual component of the CPI basket. Giving more importance to the single-family detached homes suggests that OER can remain sticky at high levels for longer given restraint supply in this specific part of the housing market.

Reuters provides more off the record insight on the ECB’s future liquidity management for the banking sector. The framework needs changing following the end of the negative/zero interest rate policy and as the ECB started draining excess liquidity by winding down its APP/PEPP bond portfolios. Sources suggest that the central could as soon as March 13 announce a “demand-driven” floor system, similar to the Bank of England’s approach. The ECB will thus still effectively set the lowest rate at which banks can lend to each other. Under the system, the ECB would also lower the main refinancing rate (4.5%) closer to the deposit rate (4%), reducing the penalty and stigma for financial institutions short in cash (narrow corridor). In the future, the ECB will no longer single-handedly decide how much liquidity it provides to the banking system via its regular refinancing operations, but consult commercial banks on determining the amount. Other decisions would include allowing some fluctuation in ESTR around the ECB’s own deposit rate and keeping minimum reserve requirements at 1% of customer deposits.

Bitcoin FOMO is Back

Economic data from the US kept investors in a cautious mode yesterday as the latest wave of data showed that the US economic growth was indeed strong at 3.2% for the Q4, but that was slightly lower than the 3.3% penciled in by analysts; consumer spending remained strong while the price indicators were higher than expected. That’s exactly the opposite of what the bulls wanted to see. The S&P500, Nasdaq and Russell 2000 fell and the US dollar index failed to extend gains above the 100-DMA.

Good news from yesterday was that US congressional leaders reached a last minute deal to avert a government shutdown. The discussion will come back in September.

All eyes are on the PCE prints today. The Federal Reserve’s (Fed) favourite gauge of inflation, the core PCE, is expected to print the biggest jump in a year, both 3 and 6-year figures are expected to rise back above 2% after having eased below this level by the end of last year. That would back the uptick that the CPI figures also printed at the beginning of this month and further spoil the dovish Fed expectations. The Fed will probably cut the rates this year, yet a cut before summer won’t be on the agenda if inflation doesn’t continue to ease. Three Fed members repeated yesterday that the timing and the pace of policy easing will depend on data. Activity on Fed funds futures gives around 64% chance for a June cut before the data. Bets could go either way. A figure in line or ideally softer than expected should keep the FEd doves betting for the first rate cut to happen in June, whereas a stronger-than-expected figure could strengthen the hawks’ hand and push the expectation of the first cut to… July.

Elsewhere, the Bank of Japan’s (BoJ) core PCE index came in stronger-than-expected. The USJDPY fell below the 150 psychological mark, as the data revived the idea that the BoJ will exit the negative rate territory sooner rather than later (I can’t tell you what ‘soon’ in sooner means though). One board member at the BoJ said that the case for exiting the negative rates is gaining momentum. If that idea gains traction among traders, we will quickly see the USDJPY snap back to 140.

Here in Europe, the Euro area countries will also release their own inflation numbers throughout the day. Softer than expected inflation data from the European countries should keep the idea that the European Central Bank (ECB) would cut its rates into summer. Yearly figures are seen easing, but monthly figures are seen higher – higher energy prices and rising shipping costs could be to blame. The EURUSD bears are waiting in ambush to send the pair below the 100 and 200-DMA in case of a stronger than expected US inflation data. Note that a stronger US inflation, if coupled with a broad-based dollar appreciation, should delay the ECB cut expectations no matter what the current euro area inflation numbers say - higher dollar would be inflationary.

One place that doesn’t seem to be affected by news is Bitcoin. The coin’s price is rising exponentially since the week started; a unit of Bitcoin traded at $64’000 per coin yesterday. That’s around $5K shy of the ATH recorded back in 2021, and the strength of the rally makes us think that there is rising FOMO aiming the $100K mark. Of course, I am not saying that Bitcoin will rally straight to that level, but enthusiasm will clearly be back if Bitcoin successfully clears the $69K offers. From a fundamental perspective, the price surge makes sense. Supply is limited, demand is surging, hodlers aren’t willing to sell and the arrival of Bitcoin ETFs made the asset class more investable for big players. And indeed, spot Bitcoin ETFs have amassed $6bn since their inception, and BlackRock’s ETF saw a whopping $520 million inflows in a single day. It was apparently the second biggest inflow into a US ETF, all asset classes included. And the potential is huge. If Bitcoin’s correlation with traditional asset classes decrease, and if the price moves happen on sector fundamentals, it would be an interesting diversification asset for traditional portfolios. But you should keep in mind that price moves in cryptocurrencies are driven by a fair amount of speculation and fluctuations could be big. Some already call for a 20% downside correction after the rally is done.

Elsewhere, US crude made an attempt to the $80pb yesterday on news that OPEC+ is considering to extend its production cuts into the Q2. The latter should throw a floor under any selloff, but I’m not sure whether OPEC alone could send US crude above the $80pb sustainably. From a technical perspective, US crude has stepped into the medium-term bearish consolidation zone, above the major 38.2% Fibonacci retracement on September to December selloff, which should in theory pave the way for further gains. If the $80pb is cleared, gains could extend to $82pb. But supply in non-OPEC countries is surging, and the war premium in the Middle East remains low as production hasn’t been affected by tensions so far, therefore the sustainability of gains above the $80pb mark is to be seen.

Focus Turns to Inflation

In focus today

In the US, January Personal Consumption Expenditures (PCE) data is due for release this afternoon. Consensus foresees Core PCE, which is the Fed's preferred measure for underlying inflation, at 0.4% m/m SA, in line with a similar increase in the CPI released earlier. We will also keep an eye out for real consumption volumes, which remained on a solid footing towards the end of 2023.

Focus today is on inflation numbers from Germany, Spain, and France. The prints are important as they tell us where the euro area print tomorrow will likely land. In the euro area we forecast core inflation at 2.8% y/y down from 3.3% in January, in tomorrow's February print. For headline inflation we expect another decline to 2.4% y/y from 2.8%. If we are right about the print tomorrow, this is another print with easing inflationary momentum and a reading significantly lower than the Q1 2024 estimate from the ECB of 2.9%.

Swedish Q4 GDP is released this morning. We expect it to print 0.5 % q/q SA on the back of strong net exports and manufacturing re-stocking. January retail sales are expected to show a positive print month on month.

Norwegian retail sales is released this morning. We expect retail sales dropped again in January. Private consumption is still suffering from a combination of low real wage growth and higher interest rates, which results in negative growth in real disposable income. In addition, the savings ratio is already close to zero.

Overnight, Chinese PMIs for February will be released, which we expect to be a mixed bag. We see some upside for the NBS manufacturing PMI, which has been weaker than the Caixin version. On the other hand, we look for Caixin PMI manufacturing to correct a bit lower from 50.8 to 50.5 (consensus 50.7).

Economic and market news

What happened overnight

In Japan, BoJ's Takata sent a strong signal for ending the negative interest rate policy. JPY strengthened following the remarks. We continue to expect the first rate hike to come at the April meeting.

What happened yesterday

In the US, the Supreme Court agreed that they would decide Donald Trump's claim of immunity after trying to overturn the 2020 election. Earlier this month the U.S. Court of Appeals for the District of Columbia Circuit rejected Trump's immunity claim, which has now been taken by the Supreme Court. The Supreme Court involved in the matter is seen as a boost to Trump as he tries to delay criminal charges while running for president.

Several Fed members spoke about future monetary policy on yesterday. Fed's Collins said officials will likely lower interest rates later this year as the outlook for sustainable 2% inflation strengthens. Williams noted the US central bank still has "a way to go" in its battle over inflation. He reiterated that the Fed will likely cut interest rates "later this year." Fed's Bostic said he is comfortable taking a patient approach to policy.

Democratic and republican leaders in the U.S. Congress reached a deal for advancing 12 annual bills that could avert a partial government shutdown on Saturday.

In the euro area, ECB's Nagel commented on monetary policy saying that ECB needs to stay on the current course until they have more comforting wage data. He said that it would be fatal for ECB to cut rates too early for inflation to rebound, which would hurt the bank's credibility.

In Sweden, export prices fell 0.6% m/m while import prices fell 1.5% m/m in January. The trade balance soared to SEK 13.3bn. Combining these data means that the real goods trade balance seasonally adjusted lands at SEK 8.5bn. Although this is a very strong print it suggests a slight negative impact on GDP growth going intro Q1.

The NIER confidence indicator changed very little in all business sectors except construction which leaped a bit higher. The most important takeaway from the report is that price expectations fell for both retail trade and service. Manufacturing, construction, and retail trade is now close to normal, with service still lagging.

Crypto. Bitcoin hit USD 60,000 on Wednesday for the first time in more than two years. In February, Bitcoin grew 42%, which was the largest monthly gain since December 2020.

Equities: Global equities were marginally lower again yesterday but again with cyclicals outperforming and industrials being the best performing sector. The higher-for-longer in general supported the NII story in banks while challenging the CRE segment and leading to bigger banks outperforming regional in regions with high bank loans to the CRE segment. In US yesterday, Dow -0.1%, S&P 500 -0.2%, Nasdaq -0.6% and Russell 2000 -0.8%. Asian markets are mixed this morning with Chinese mainland markets outperforming. US and European futures are higher this morning.

FI: The US yield curve steepened from the short end on the back of comments from several Federal Reserve members as well as some US economic data including the GDP growth for Q4. The comments suggest that a rate cut would come no earlier than June, and GDP numbers were a bit to the bullish side. Hence, 2Y US government bond yields declined 5-6bp and 10Y US government bond yields declined 4-5bp.

FX: Price action in the FX space remains within tight ranges. In yesterday's session, the USD broadly strengthened in the G10 space, while Scandies alongside AUD and especially NZD weakened, following the dovish unchanged RBNZ rate decision. EUR/USD traded heavily in the first hours of yesterday's session without any major news—likely due to month-end flows—but remains in the mid 1.08-1.09 range.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.40; (P) 190.68; (R1) 191.10; More....

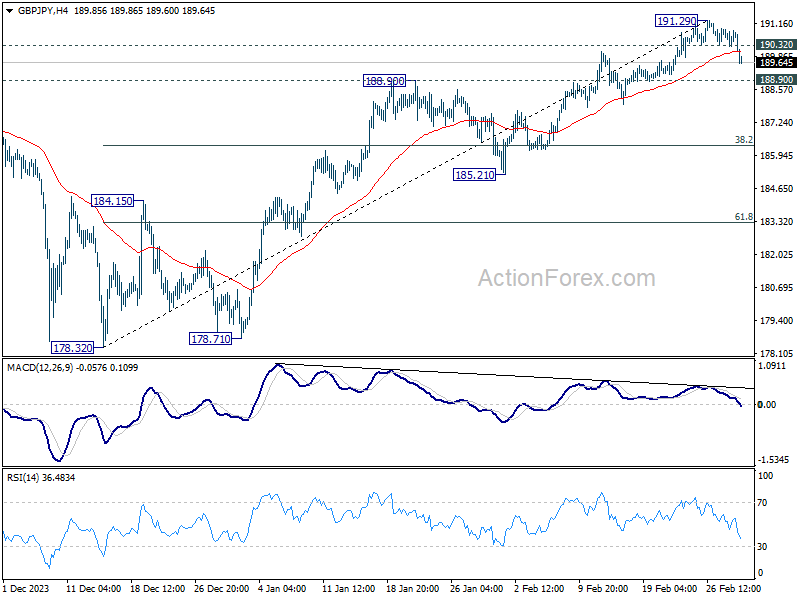

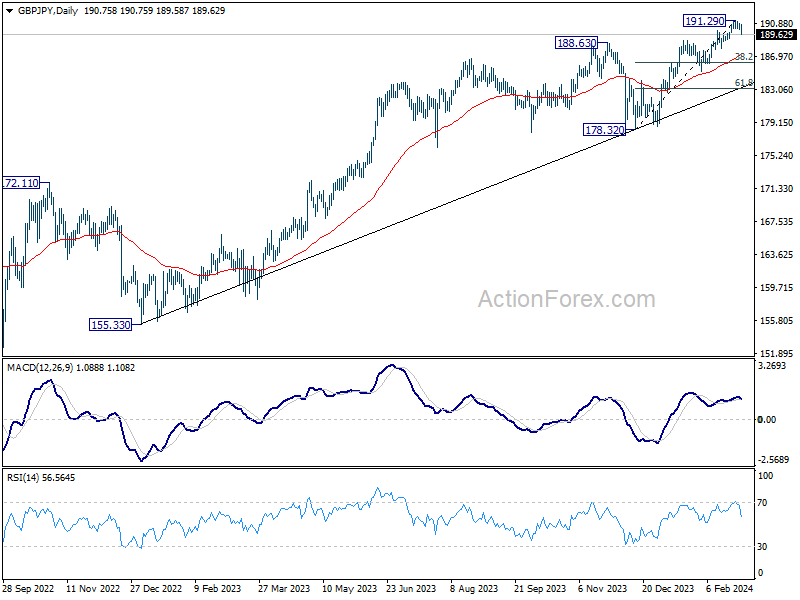

GBP/JPY's break of 190.32 suggests short term topping at 191.29. Considering bearish divergence condition in 4H MACD, it could now be correcting whole rally from 178.32. Intraday bias is back on the downside for 188.90 resistance turned support first. Firm break there will target 38.2% retracement of 178.32 to 191.29 at 186.33. For now, risk will stay on the downside as long as 191.29 resistance holds, in case of recovery.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

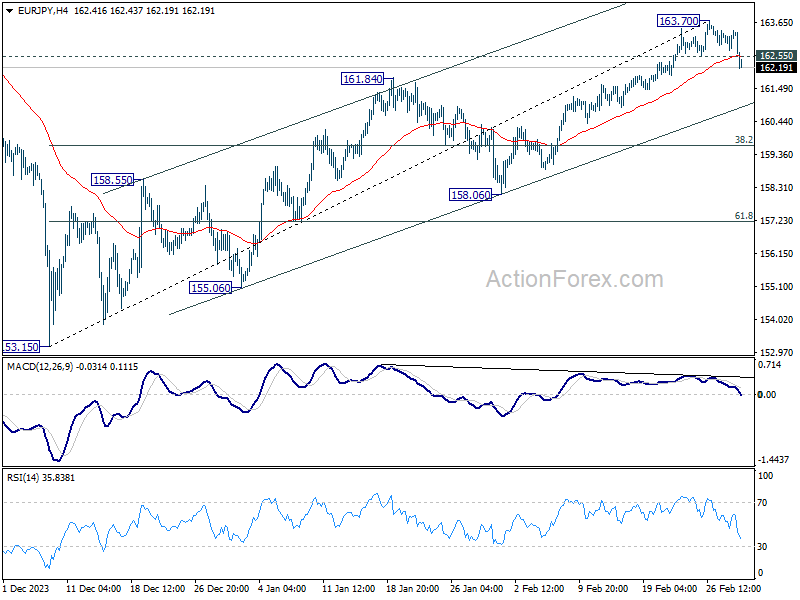

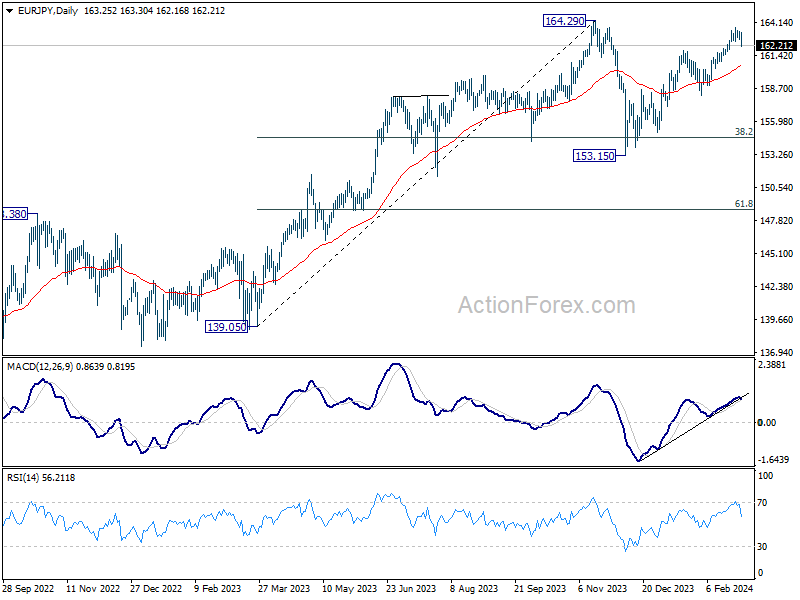

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.94; (P) 163.17; (R1) 163.59; More...

EUR/JPY's break of 162.55 minor support indicates short term topping at 163.70. Considering bearish divergence condition in 4H MACD, it could now be corrective whole rise from 153.15. Intraday bias is back on the downside for channel support (now at 160.93). Firm break there will target 38.2% retracement of 153.15 to 163.70 at 159.66. For now, risk will stay mildly on the downside as long as 163.70 resistance holds, in case of recovery.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

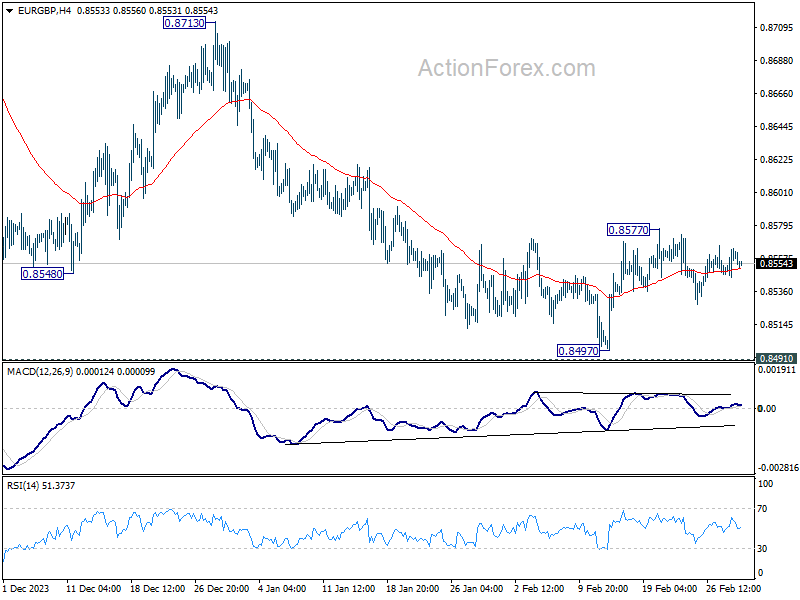

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8549; (P) 0.8558; (R1) 0.8569; More...

No change in EUR/GBP's outlook and intraday bias remains neutral. Risk stays mildly on the downside with 0.8577 resistance intact. Decisive break of t 0.8491/7 support zone will resume larger down trend. On the upside, however, break of 0.8577 will turn bias to the upside for resuming the rebound from 0.8497.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

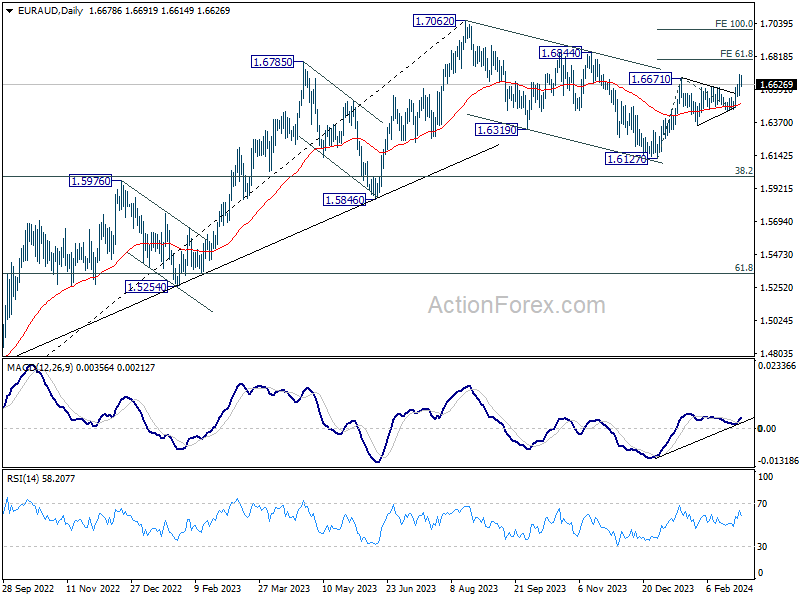

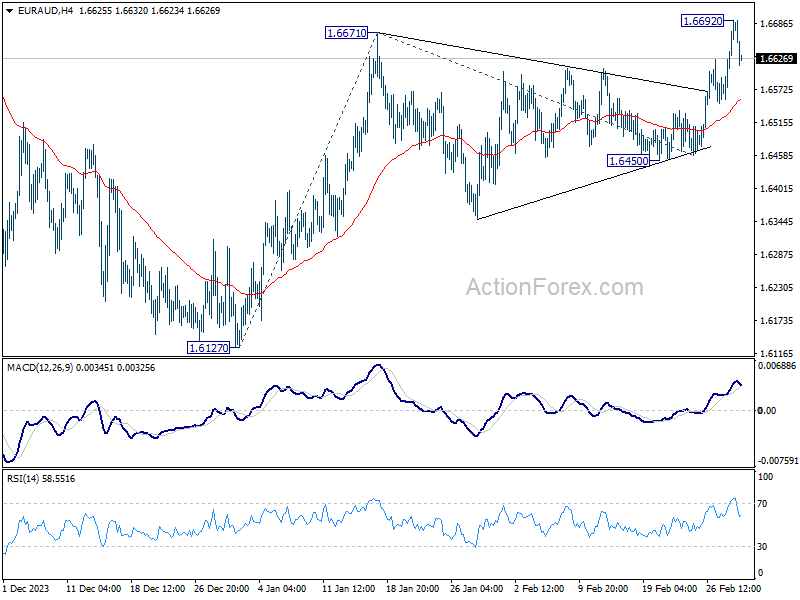

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6598; (P) 1.6646; (R1) 1.6735; More...

EUR/AUD rose to 1.6692 but retreated since then. Intraday bias is neutral for the moment first. The breach of 1.6671 resistance suggests that rebound from 1.6127 is resuming. More importantly, whole correction from 1.7062 should have completed with three waves down to 1.6127. Further rise is now expected as long as 1.6450 support holds. Above 1.6692 will target 61.8% projection of 1.6127 to 1.6671 from 1.6450 at 1.6786 next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.