Sample Category Title

New Zealand’s trade deficit widens, exports falls -7.1% yoy and imports down -20% yoy

New Zealand's trade activity in January showed notable downturn, with goods exports dropping by -7.1% yoy to NZD 4.9B and goods imports declining by a substantial -20.0% yoy to NZD 5.9B. This resulted in trade deficit of NZD -976m, significantly larger than the anticipated NZD -200m.

A closer examination of the data reveals Australia as the leading contributor to the monthly fall in New Zealand's exports, with a -17% decrease amounting to NZD -112m. Not far behind, Japan saw a dramatic -34% reduction in its exports from New Zealand, translating to NZD -105m. Conversely, EU was a rare bright spot, where New Zealand's exports actually increased by 5.8%, or NZD 15m. Other major trading partners like China and the USA also experienced declines in exports from New Zealand, by -2.8% (NZD -42m) and -5.6% (NZD -31m), respectively.

On the import side, EU recorded the most significant monthly drop, with imports falling by -33% to NZD -386m. South Korea followed closely with a -34% decrease, equating to NZD -286m. Other notable decreases in imports came from China (NZD -84m, -5.4%), Australia (NZD -57m, -9.2%), and the USA (NZD -30m, -5.6%).

FOMC minutes: A majority hesitant on swift monetary easing

The latest FOMC minutes reveal a predominant caution against premature easing of monetary policy. The document underscores a consensus among "most participants" over the potential risks of reducing interest rates too hastily, expressing a preference for delaying cuts rather than risking the need to reverse course.

During the FOMC meeting held on January 30-31, the discussion emphasized that participants did not anticipate it being appropriate to lower the federal funds rate target range without "greater confidence" that inflation was on a sustainable path back to 2% target. The determination of the future policy rate path was tied closely to "incoming data, the evolving outlook, and the balance of risks." .

Although the balance of risks towards employment and inflation goals was seen as "moving into better balance", participants remained "highly attentive to inflation risks". While upside risks to inflation have "diminished", inflation remains above target. This vigilance is framed within a broader context of concern that "progress toward price stability could stall", particularly in scenarios where demand strengthens unexpectedly or supply-side improvements falter.

The predominant narrative within the FOMC leans towards a cautious approach to policy easing, with "most participants" underscoring the perils of "moving too quickly" and the importance of a meticulous evaluation of incoming data to ascertain whether inflation trends align with the target sustainably. In contrast, only "a couple of participants" raised concerns about the economic downsides of an "overly restrictive stance" persisting for an extended period.

(FED) Minutes of the Federal Open Market Committee

January 30–31, 2024

A joint meeting of the Federal Open Market Committee and the Board of Governors of the Federal Reserve System was held in the offices of the Board of Governors on Tuesday, January 30, 2024, at 10:00 a.m. and continued on Wednesday, January 31, 2024, at 9:00 a.m.1

Attendance

Jerome H. Powell, Chair

John C. Williams, Vice Chair

Thomas I. Barkin

Michael S. Barr

Raphael W. Bostic

Michelle W. Bowman

Lisa D. Cook

Mary C. Daly

Philip N. Jefferson

Adriana D. Kugler

Loretta J. Mester

Christopher J. Waller

Susan M. Collins, Austan D. Goolsbee, Kathleen O'Neill, Jeffrey R. Schmid, and Sushmita Shukla, Alternate Members of the Committee

Patrick Harker, Neel Kashkari, and Lorie K. Logan, Presidents of the Federal Reserve Banks of Philadelphia, Minneapolis, and Dallas, respectively

Joshua Gallin, Secretary

Matthew M. Luecke, Deputy Secretary

Brian J. Bonis, Assistant Secretary

Michelle A. Smith, Assistant Secretary

Mark E. Van Der Weide, General Counsel

Richard Ostrander, Deputy General Counsel

Trevor A. Reeve, Economist

Stacey Tevlin, Economist

Beth Anne Wilson, Economist

Shaghil Ahmed, James A. Clouse, Edward S. Knotek II, David E. Lebow, Sylvain Leduc, Paula Tkac, and William Wascher, Associate Economists

Roberto Perli, Manager, System Open Market Account

Julie Ann Remache, Deputy Manager, System Open Market Account

Stephanie R. Aaronson, Senior Associate Director, Division of Research and Statistics, Board

Jose Acosta, Senior System Administrator II, Division of Information Technology, Board

Isaiah C. Ahn, Information Management Analyst, Division of Monetary Affairs, Board

Roc Armenter, Executive Vice President, Federal Reserve Bank of Philadelphia

Alyssa Arute, Manager, Division of Reserve Bank Operations and Payment Systems, Board

Penelope A. Beattie,2 Section Chief, Office of the Secretary, Board

David Bowman, Senior Associate Director, Division of Monetary Affairs, Board

Celso Brunetti,3 Assistant Director, Division of Research and Statistics, Board

Juan C. Climent, Special Adviser to the Board, Division of Board Members, Board

Daniel M. Covitz, Deputy Director, Division of Research and Statistics, Board

Jennifer S. Crystal, Senior Adviser, Division of International Finance, Board

Stephanie E. Curcuru, Deputy Director, Division of International Finance, Board

Ryan Decker, Special Adviser to the Board, Division of Board Members, Board

Sarah Devany, First Vice President, Federal Reserve Bank of San Francisco

Rochelle M. Edge, Deputy Director, Division of Monetary Affairs, Board

Eric C. Engstrom, Associate Director, Division of Research and Statistics, Board

Jon Faust, Senior Special Adviser to the Chair, Division of Board Members, Board

Jenn Gallagher, Assistant to the Board, Division of Board Members, Board

Carlos Garriga, Senior Vice President, Federal Reserve Bank of St. Louis

Michael S. Gibson, Director, Division of Supervision and Regulation, Board

Joseph W. Gruber, Executive Vice President, Federal Reserve Bank of Kansas City

Luca Guerrieri, Associate Director, Division of International Finance, Board

Christopher J. Gust, Associate Director, Division of Monetary Affairs, Board

Andrew Haughwout, Acting Director of Research, Federal Reserve Bank of New York

Valerie S. Hinojosa, Section Chief, Division of Monetary Affairs, Board

Jane E. Ihrig, Special Adviser to the Board, Division of Board Members, Board

Michael T. Kiley, Deputy Director, Division of Financial Stability, Board

Kyungmin Kim, Principal Economist, Division of Monetary Affairs, Board

Elizabeth K. Kiser, Senior Associate Director, Division of Research and Statistics, Board

Andreas Lehnert, Director, Division of Financial Stability, Board

Kurt F. Lewis, Special Adviser to the Chair, Division of Board Members, Board

Dan Li,4 Assistant Director, Division of Monetary Affairs, Board

Laura Lipscomb, Special Adviser to the Board, Division of Board Members, Board

Ann E. Misback, Secretary, Office of the Secretary, Board

Phillip Monin, Senior Economist, Division of Monetary Affairs, Board

Michelle M. Neal, Head of Markets, Federal Reserve Bank of New York

Christopher J. Nekarda, Principal Economist, Division of Research and Statistics, Board

Anna Paulson, Executive Vice President, Federal Reserve Bank of Chicago

Eugenio P. Pinto, Special Adviser to the Board, Division of Board Members, Board

Andrea Raffo, Senior Vice President, Federal Reserve Bank of Minneapolis

Andres Schneider, Principal Economist, Division of Monetary Affairs, Board

Samuel Schulhofer-Wohl, Senior Vice President, Federal Reserve Bank of Dallas

Felipe F. Schwartzman, Senior Economist, Federal Reserve Bank of Richmond

Chiara Scotti,3 Senior Vice President, Federal Reserve Bank of Dallas

Zeynep Senyuz, Deputy Associate Director, Division of Monetary Affairs, Board

Arsenios Skaperdas, Senior Economist, Division of Monetary Affairs, Board

Balint Szoke, Senior Economist, Division of Monetary Affairs, Board

Clara Vega, Special Adviser to the Board, Division of Board Members, Board

Annette Vissing-Jørgensen, Senior Adviser, Division of Monetary Affairs, Board

Jeffrey D. Walker, Associate Director, Division of Reserve Bank Operations and Payment Systems, Board

Fabian Winkler, Principal Economist, Division of Monetary Affairs, Board

Paul R. Wood, Special Adviser to the Board, Division of Board Members, Board

Egon Zakrajsek, Executive Vice President, Federal Reserve Bank of Boston

Rebecca Zarutskie, Special Adviser to the Board, Division of Board Members, Board

Annual Organizational Matters5

The agenda for this meeting reported that advices of the election of the following members and alternate members of the Federal Open Market Committee for a term beginning January 30, 2024, were received and that these individuals executed their oaths of office.

The elected members and alternate members were as follows:

John C. Williams, President of the Federal Reserve Bank of New York, with Sushmita Shukla, First Vice President of the Federal Reserve Bank of New York, as alternate;

Thomas I. Barkin, President of the Federal Reserve Bank of Richmond, with Susan M. Collins, President of the Federal Reserve Bank of Boston, as alternate;

Loretta J. Mester, President of the Federal Reserve Bank of Cleveland, with Austan D. Goolsbee, President of the Federal Reserve Bank of Chicago, as alternate;

Raphael W. Bostic, President of the Federal Reserve Bank of Atlanta, with Kathleen O'Neill, Interim President of the Federal Reserve Bank of St. Louis, as alternate;

Mary C. Daly, President of the Federal Reserve Bank of San Francisco, with Jeffrey R. Schmid, President of the Federal Reserve Bank of Kansas City, as alternate.

By unanimous vote, the following officers of the Committee were selected to serve until the selection of their successors at the first regularly scheduled meeting of the Committee in 2025:

| Jerome H. Powell | Chair |

| John C. Williams | Vice Chair |

| Joshua Gallin | Secretary |

| Matthew M. Luecke | Deputy Secretary |

| Brian J. Bonis | Assistant Secretary |

| Michelle A. Smith | Assistant Secretary |

| Mark E. Van Der Weide | General Counsel |

| Richard Ostrander | Deputy General Counsel |

| Charles C. Gray | Assistant General Counsel |

| Trevor A. Reeve | Economist |

| Stacey Tevlin | Economist |

| Beth Anne Wilson | Economist |

| Shaghil Ahmed | |

| Kartik B. Athreya6 | |

| James A. Clouse | |

| Brian M. Doyle | |

| Edward S. Knotek II | |

| David E. Lebow | |

| Sylvain Leduc | |

| Paula Tkac | |

| William Wascher | |

| Alexander L. Wolman | Associate Economists |

By unanimous vote, the Committee selected the Federal Reserve Bank of New York to execute transactions for the System Open Market Account (SOMA).

By unanimous vote, the Committee selected Roberto Perli and Julie Ann Remache to serve at the pleasure of the Committee as manager and deputy manager of the SOMA, respectively, on the understanding that these selections were subject to being satisfactory to the Federal Reserve Bank of New York.

Secretary's note: The Federal Reserve Bank of New York subsequently sent advice that the selections indicated previously were satisfactory.

By unanimous vote, the Committee approved the FOMC Authorizations and Continuing Directives for Open Market Operations, with a revision to Section II, Continuing Directive for Domestic Open Market Operations, to add a standing seven-day term option to the existing standing Foreign and International Monetary Authorities Repurchase Agreement Operations.

Ahead of the vote on policies relating to investment and trading, information security, and external communications, the Chair commented on the critical importance of earning and keeping the public's trust in the impartiality of the Committee's decisionmaking. A revised investment and trading policy was proposed which expanded the scope of employees subject to the Committee's investment and trading rules, and introduced new investment restrictions on all employees with access to FOMC information. All participants indicated support for, and agreed to abide by, the FOMC Policy on Investment and Trading for Committee Participants and Federal Reserve System Staff, the Program for Security of FOMC Information, the FOMC Policy on External Communications of Committee Participants, and the FOMC Policy on External Communications of Federal Reserve System Staff. The Committee voted unanimously to approve those four policies.5

Ahead of the vote on the Statement on Longer-Run Goals and Monetary Policy Strategy, the Chair indicated the next five-year review of the statement would begin in the latter half of this year, and the results would be announced about a year later. All participants indicated support for the Statement on Longer-Run Goals and Monetary Policy Strategy, and the Committee voted unanimously to reaffirm it without revision.5

Developments in Financial Markets and Open Market Operations

The manager turned first to a review of developments in financial markets over the intermeeting period. Financial conditions eased modestly but remained about as tight as they were last summer and much tighter than when the hiking cycle began. Over the intermeeting period, declines in nominal Treasury yields were concentrated at the front end of the yield curve. Staff models suggested that the declines in shorter-term yields were mostly attributable to a lower expected policy rate path and were concentrated in expected real rates, while expected inflation was little changed. Pricing of inflation derivatives continued to suggest a near-term path of inflation consistent with a return to 2 percent later this year. Broad equity prices reached new highs over the intermeeting period, but they were driven mostly by the strong gains of large-capitalization technology companies; broader measures of equity valuations were more subdued. Still, equities appeared priced for continued economic resilience.

The manager turned next to expectations for monetary policy. Market participants broadly viewed recent inflation data and the December Summary of Economic Projections (SEP) as increasing the odds that rate cuts might start sooner than previously thought. The modal path of the federal funds rate from the Open Market Desk's Survey of Primary Dealers and Survey of Market Participants was little changed from December but showed an increased likelihood of earlier rate cuts. The modal path implied by options prices declined some over the intermeeting period. Both modal paths were closer to the December median SEP projection than the average path for the policy rate implied by futures prices, which had declined more substantially over the period. The futures-based path likely reflected the effect of investors' perceived probability of more substantial rate cuts rather than their baseline expectations.

Communications over the period heightened market attention around a potential slowing of balance sheet runoff. Most Desk survey respondents expected a slowing of the pace to start by July, although there was considerable uncertainty about the exact start date. The average expected timing for the end of runoff shifted slightly earlier, and the portfolio size at the end of runoff was slightly higher than in the December surveys.

Regarding developments in money markets and Desk operations, the effective federal funds rate was stable over the intermeeting period. While the Secured Overnight Financing Rate experienced temporary and modest upward pressure over the past few month-ends, including the year-end, such a pattern was common before the pandemic. The usage of the overnight reverse repurchase agreement (ON RRP) facility continued to fall over the period, with balances below $600 billion in late January. Since June 2023, when the debt ceiling was suspended, usage of the ON RRP facility had declined at a much faster pace than the Federal Reserve securities portfolio, and reserve balances had increased some.

As part of its ongoing market surveillance, the staff continued to monitor a wide range of money market indicators; those gauges suggested that the supply of reserves remained abundant. The staff also noted that once the ON RRP facility is either depleted or stabilized at a low level, reserves will decline at a pace comparable with the runoff of the Federal Reserve's securities portfolio, all else equal.

By unanimous vote, the Committee ratified the Desk's domestic transactions over the intermeeting period. There were no intervention operations in foreign currencies for the System's account during the intermeeting period.

Staff Review of the Economic Situation

The data available at the time of the January 30–31 meeting indicated that growth in U.S. real gross domestic product (GDP) was solid in the fourth quarter of 2023 but had stepped down from the third quarter's strong pace. Labor market conditions continued to be tight but showed further signs of easing. Consumer price inflation had declined markedly over the course of the year, though it remained above 2 percent.

Labor demand and supply continued to gradually move into better alignment. The average monthly pace of nonfarm payroll employment gains in the fourth quarter was slower than in the third quarter. The unemployment rate remained at 3.7 percent in December, the same as its third-quarter average. However, the labor force participation rate moved down, as did the employment-to-population ratio. The African American unemployment rate declined, and the rate for Hispanics rose; both rates were higher than those for Asians and for whites. The private-sector job openings rate was little changed in November and December, and the quits rate edged down; both rates were below their levels at the start of 2023. Easing labor market imbalances were also apparent in the wage data, with the December 12-month changes in the employment cost index and in average hourly earnings for all employees each below their year-earlier levels.

Consumer price inflation continued to slow. The price index for total personal consumption expenditures (PCE) increased 2.6 percent over the 12 months ending in December, while core PCE price inflation—which excludes changes in energy prices and many consumer food prices—was 2.9 percent over the same period. Both total and core PCE price inflation were well below their year-earlier levels. The trimmed mean measure of 12-month PCE price inflation constructed by the Federal Reserve Bank of Dallas was 3.3 percent in December, also lower than its level a year earlier. Survey measures of consumers' short-run inflation expectations moved lower in December, while survey measures of medium- to longer-term inflation expectations were broadly in line with the levels seen in the decade before the pandemic.

According to the advance estimate, real GDP rose at a solid pace in the fourth quarter. Private domestic final purchases—which comprises PCE and private fixed investment and which often provides a better signal than GDP of underlying economic momentum—also rose solidly, though at a slower rate.

Real exports grew robustly in the fourth quarter of 2023, driven in part by a jump in exports of industrial supplies, which had declined markedly earlier last year. By contrast, real imports grew at a tepid pace, as gains in imports of capital goods and services were partially offset by declines in imports of consumer goods and autos. All told, net exports contributed about 1/2 percentage point to U.S. GDP growth in the fourth quarter after making roughly neutral contributions in the preceding two quarters.

Foreign economic growth remained subdued in the fourth quarter. In the advanced foreign economies (AFEs), a significant tightening of monetary policy over the past two years, the erosion of real household incomes from high inflation rates, and the repercussions of last year's energy shock in Europe continued to weigh on economic activity. In China, a property-sector slump and depressed consumer confidence continued to weigh on domestic demand, with the government rolling out a series of policy measures to support growth. Economic activity in Asia excluding China firmed, supported in part by rebounding global demand for high-tech products.

Foreign headline inflation continued to fall. However, the pace of decline had varied across countries as well as sectors, with a moderation in goods prices generally having outpaced that in services prices. Most major foreign central banks kept their policy rates unchanged over the intermeeting period and emphasized the need to maintain a stance of policy that is sufficiently restrictive to ensure that inflation falls back to their targets.

Staff Review of the Financial Situation

Over the intermeeting period, nominal Treasury yields declined, and the expected market-implied path for the federal funds rate through 2024 shifted downward, as market participants viewed monetary policy communications, on balance, as pointing to notably less restrictive policy than expected. Indicators of broad financial conditions eased over the period, but the staff's Financial Conditions Impulse on Growth index remained restrictive. Similarly, financing conditions for households and businesses continued to be moderately restrictive, as borrowing costs remained elevated.

The market-implied path for the federal funds rate through 2024 decreased over the intermeeting period. A straight read of federal funds futures rates suggested that market participants were placing higher odds on significant policy easing in 2024 than they did just before the December FOMC meeting. Beyond 2024, the policy rate path implied by overnight index swap quotes declined. Consistent with the decline in the implied policy path, short- and intermediate-term Treasury yields also declined notably. Real yields declined more than nominal yields, implying somewhat higher measures of inflation compensation. Market-based measures of interest rate uncertainty remained highly elevated by historical standards.

Broad stock price indexes increased, and spreads on investment- and speculative-grade bonds narrowed modestly over the intermeeting period. The one-month option-implied volatility on the S&P 500 increased somewhat over the period but remained low by historical standards.

Movements in foreign markets over the intermeeting period were modest, on net, with most foreign asset prices and the exchange value of the dollar little changed. Market participants generally considered current levels of most AFE policy rates to be at the peaks of their respective tightening cycles. Declines in market-based measures of U.S. policy expectations contributed to a moderate step-down in short-term yields in most AFEs, while longer-term foreign yields were little changed. Major AFE equity indexes increased slightly.

Conditions in short-term funding markets remained stable over the intermeeting period, with typical dynamics observed surrounding year-end. Usage of the ON RRP facility continued to decline over the period, primarily reflecting money market funds reallocating their assets to Treasury bills and private-market repurchase agreements, which offered slightly more attractive market rates relative to the ON RRP rate. Banks' total deposit levels were roughly unchanged in the fourth quarter of last year, as outflows of core deposits were about offset by inflows of large time deposits.

In domestic credit markets, borrowing costs for most businesses, households, and municipalities decreased moderately over the intermeeting period but remained elevated. Rates on loans to households declined over the intermeeting period but remained relatively high, while interest rates on existing credit card accounts were little changed. Interest rates on commercial and industrial (C&I) loans and small business loans increased over the intermeeting period. Yields declined on a broad array of fixed-income securities, including investment- and speculative-grade corporate bonds, residential and commercial mortgage-backed securities (CMBS), and municipal bonds. The declines were largely driven by decreases in Treasury yields and, to some extent, by narrower spreads.

Credit continued to be generally available to businesses, households, and municipalities. However, credit availability for smaller firms continued to tighten. Total core loans at banks increased slightly in the fourth quarter. Financing in capital markets continued to be available, although issuance in most markets remained at moderate levels.

In the January Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS), banks reported tightening standards and terms on C&I loans to firms of all sizes over the fourth quarter. Regarding commercial real estate (CRE), banks reported tightening standards across all loan categories in the fourth quarter. Banks reported that they expected to keep lending standards unchanged for C&I loans and to tighten standards for CRE loans during 2024.

Credit in the residential mortgage market remained easily available for high-credit-score borrowers who met standard conforming loan criteria, and consumer credit remained available for most borrowers. Growth in credit card balances was strong in November, though SLOOS respondents indicated that standards for credit cards tightened in the fourth quarter and were expected to tighten further over 2024. Auto loan balances grew modestly in November. A modest share of banks reported in the SLOOS that they tightened standards on auto loans in the fourth quarter and expected to tighten them further over 2024.

The credit quality of businesses and households deteriorated slightly but remained broadly solid, as delinquency rates in most sectors were relatively low. Delinquency rates on conventional mortgages remained low, while delinquency rates on credit cards and auto loans rose in the third quarter to levels notably above those just before the pandemic. The credit quality of nonfinancial firms borrowing in the corporate bond and leveraged loan markets remained sound overall. Aggregate delinquency rates on CMBS backed by office properties continued to be elevated in November. In the January SLOOS, banks reported that credit quality was expected to deteriorate somewhat across loan categories over 2024.

The staff provided an update on its assessment of the stability of the U.S. financial system and, on balance, characterized the system's financial vulnerabilities as notable. The staff judged that asset valuation pressures remained notable, as valuations across a range of markets appeared high relative to fundamentals. House prices increased to the upper end of their historical range, relative to rents and Treasury yields, though underwriting standards remained restrictive. CRE prices continued to decline, especially in the multifamily and office sectors, and low levels of transactions in the office sector likely indicated that prices had not yet fully reflected the sector's weaker fundamentals. Vulnerabilities associated with business and household debt were characterized as moderate. Nonfinancial business debt growth declined, and the ability of firms to service their debt remained high relative to history.

Leverage in the financial sector was characterized as notable. In the banking sector, regulatory risk-based capital ratios continued to increase and indicated ample loss-bearing capacity in the banking system. The fair value of banks' longer-term fixed-rate assets, including loans, increased in the fourth quarter as longer-term interest rates decreased, though banks remained vulnerable to significant increases in longer-term interest rates. Insurers had been increasing their investments in risky corporate debt. Funding risks were also characterized as notable. Uninsured deposits declined in the aggregate but remained high for some banks. Assets in prime money market mutual funds and other cash management vehicles continued to increase.

Staff Economic Outlook

The economic forecast prepared by the staff for the January meeting was slightly stronger than the December projection, as the upward revision to 2023 GDP growth implied by incoming data boosted the level of output throughout the projection period. The lagged effects of earlier monetary policy actions, through their continued contribution to tight financial and credit conditions, were still expected to push output growth in 2024 and 2025 below the staff's estimate of potential growth; in 2026, output was expected to rise in line with potential. The projected path for the unemployment rate was revised down slightly, reflecting the upward revision to the level of output.

Total and core PCE price inflation were both projected to step down in 2024 as demand and supply in product and labor markets moved into better alignment. By 2026, total and core PCE price inflation were expected to be close to 2 percent.

The staff continued to view the uncertainty around the baseline projection as elevated but noted that this uncertainty had diminished substantially over the past year. Risks around the inflation forecast were seen as tilted slightly to the upside; although inflation had come in close to expectations throughout most of 2023, the staff placed some weight on the possibility that further progress in reducing inflation could take longer than expected. The risks around the forecast for real activity were viewed as skewed to the downside, as any substantial setback in reducing inflation might lead to a tightening of financial conditions that would slow the pace of real activity by more than the staff anticipated in their baseline forecast. In addition, the possibility of a larger-than-expected erosion of households' financial positions was seen as a downside risk to the projection for real activity.

Participants' Views on Current Conditions and the Economic Outlook

In their discussion of current economic conditions, participants noted that recent indicators suggested that economic activity had been expanding at a solid pace. Real GDP growth in the fourth quarter of last year came in above 3 percent at an annual rate, below the strong growth posted in the third quarter but still above most forecasters' expectations. Participants observed that the unexpected strength in real GDP growth in the fourth quarter reflected stronger-than-expected net exports and inventory investment, which tend to be volatile and may carry little signal for future growth. Still, consumption continued to grow at a solid pace. In addition to strong demand, many participants attributed the recent expansion in economic activity to favorable supply developments. Participants noted that the pace of job gains had moderated since early last year but remained strong and that the unemployment rate had remained low. Inflation had eased over the past year but remained elevated.

Regarding the economic outlook, participants judged that the current stance of monetary policy was restrictive and would continue to put downward pressure on economic activity and inflation. Accordingly, they expected that supply and demand in product and labor markets would continue to move into better balance. In light of the policy restraint in place, along with more favorable inflation data amid ongoing improvements in supply conditions, participants viewed the risks to achieving the Committee's employment and inflation goals as moving into better balance. However, participants noted that the economic outlook was uncertain and that they remained highly attentive to inflation risks.

In their discussion of inflation, participants observed that inflation had eased over the past year but remained above the Committee's 2 percent inflation objective. They remained concerned that elevated inflation continued to harm households, especially those with limited means to absorb higher prices. While the inflation data had indicated significant disinflation in the second half of last year, participants observed that they would be carefully assessing incoming data in judging whether inflation was moving down sustainably toward 2 percent.

Participants noted improvements in both headline and core inflation and discussed the underlying components of these series. Although total PCE inflation in December remained above the Committee's 2 percent objective on a 12-month basis, on a 6-month basis, total PCE inflation was near 2 percent at an annual rate, and core PCE inflation was just below 2 percent. Participants judged that some of the recent improvement in inflation reflected idiosyncratic movements in a few series. Nevertheless, they viewed that there had been significant progress recently on inflation returning to the Committee's longer-run goal. Many participants indicated that they expected core nonhousing services inflation to gradually decline further as the labor market continued to move into better balance and wage growth moderated further. Various participants noted that housing services inflation was likely to fall further as the deceleration in rents on new leases continued to pass through to measures of such inflation. While many participants pointed to disinflationary pressures associated with improvements in aggregate supply—such as increases in the labor force or better productivity growth—a couple of participants judged that the downward pressure on core goods prices from the normalization of supply chains was likely to moderate.

Participants observed that longer-term inflation expectations had remained well anchored at a level consistent with the Committee's 2 percent inflation objective. Measures of near-term inflation expectations had also declined recently, in some cases to within their ranges in the years before the pandemic. Some participants pointed to reports from contacts that firms could not as easily pass on price increases to consumers or were making less frequent price adjustments than they had in recent years.

In their discussion of the household sector, participants observed that consumer spending had been stronger than expected, supported by low unemployment and solid income growth. A number of participants judged that consumption growth was likely to moderate this year, as growth in labor income was expected to slow and pandemic-related excess savings were expected to diminish. In addition, some participants noted signs that the finances of some households—especially those in the low- and moderate-income categories—were increasingly coming under pressure, which these participants saw as a downside risk to the outlook for consumption. In particular, they pointed to increased usage of credit card revolving balances and buy-now-pay-later services, as well as increased delinquency rates for some types of consumer loans.

The reports of business contacts cited by participants varied across industries and Districts. In a few Districts, contacts reported that the pace of economic activity was steady or solid, while in several others, contacts expressed increased optimism about the economic outlook and prospects for investment. District reports from manufacturers were mixed, as some contacts saw increased activity, whereas others saw subdued or weakening activity. A couple of participants noted that although soft commodity prices and elevated borrowing costs had contributed to a decline in farm incomes recently, agricultural land values remained resilient, and delinquencies on farm loans continued to be low. A few participants remarked that financing and credit conditions were particularly challenging for small businesses.

Participants noted that the labor market remained tight, but demand and supply in that market had continued to come into better balance. Payroll growth had remained strong in the last few months of 2023 but had slowed from its pace seen a year ago, while the unemployment rate remained low. Participants also observed that the ratio of job openings to unemployed workers had declined over the past year but still remained somewhat above its pre-pandemic level. Consistent with a reduction in labor market tightness, business contacts in several Districts reported an easing in wage pressures or an increased ability to hire and retain workers. Participants mentioned several developments that had boosted labor supply last year, including higher labor force participation, immigration, and an improved job-matching process; however, a few participants judged that further increases in labor supply may be limited, pointing, for instance, to the decline in labor force participation in December. While labor market conditions were generally seen as strong, several participants noted that recent job gains were concentrated in a few sectors, which, in their view, pointed to downside risks to the outlook for employment.

Participants discussed the uncertainty surrounding the economic outlook. As an upside risk to both inflation and economic activity, participants noted that momentum in aggregate demand may be stronger than currently assessed, especially in light of surprisingly resilient consumer spending last year. Furthermore, several participants mentioned the risk that financial conditions were or could become less restrictive than appropriate, which could add undue momentum to aggregate demand and cause progress on inflation to stall. Participants also noted some other sources of upside risks to inflation, including possible disruptions to supply chains from geopolitical developments, a potential rebound in core goods prices as the effects of supply-side improvements dissipate, or the possibility that wage growth remains elevated. Downside risks to inflation and economic activity noted by participants included geopolitical risks that could result in a material pullback in demand, possible negative spillovers from lower growth in some foreign economies, the risk that financial conditions could remain restrictive for too long, or the possibility that a weakening of household balance sheets could contribute to a greater-than-expected deceleration in consumption. A few participants mentioned the possibility that economic activity could surprise to the upside and inflation to the downside because of more-favorable-than-expected supply-side developments.

In the discussion of financial stability, participants observed that risks to the banking system had receded notably since last spring, though they noted vulnerabilities at some banks that they assessed warranted monitoring. These participants noted potential risks for some banks associated with increased funding costs, significant reliance on uninsured deposits, unrealized losses on assets resulting from the rise in longer-term interest rates, or high CRE exposures. Participants judged that liquidity in the financial system remained more than ample and discussed the importance of considering liquidity conditions as the Federal Reserve's balance sheet continues to normalize. While participants noted that they were not seeing any signs of liquidity pressures at banks, several participants noted that, as a matter of prudent contingency planning, banks should continue to improve their readiness to use the Federal Reserve's discount window, and that the Federal Reserve should continue to improve the operational efficiency of the window. In addition, some participants commented on the difficulties associated with banks relying on some forms of private wholesale funding during times of stress. A few participants remarked on the importance of measures aimed at increasing the resilience of the Treasury market. A few participants noted cyber risks and the importance of firms being able to recover from cyber events. A few participants also commented on the financial condition of low- and moderate-income households who have exhausted their savings, as well as the importance of monitoring data on rising delinquencies on credit cards and autos.

In their consideration of appropriate monetary policy actions at this meeting, participants noted that recent indicators suggested that economic activity had been expanding at a solid pace. Job gains had moderated since early last year but remained strong, and the unemployment rate had remained low. Inflation had eased over the past year but remained elevated. Participants also noted that the risks to achieving the Committee's employment and inflation goals were moving into better balance and that the Committee remained highly attentive to inflation risks. Participants continued to be resolute in their commitment to bring inflation down to the Committee's 2 percent objective.

In light of current economic conditions and their implications for the outlook for economic activity and inflation, as well as the balance of risks, all participants judged it appropriate to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent at this meeting. All participants also judged it appropriate to continue the process of reducing the Federal Reserve's securities holdings, as described in the previously announced Plans for Reducing the Size of the Federal Reserve's Balance Sheet.

Participants viewed maintaining the current stance of policy as appropriate given the incoming data, which indicated that inflation had continued to move toward the Committee's 2 percent objective and that demand and supply in the labor market had continued to move into better balance. Participants commented that maintaining the target range for the federal funds rate at this meeting would promote further progress toward the Committee's goals and allow participants to gather additional information to evaluate this progress.

In discussing the policy outlook, participants judged that the policy rate was likely at its peak for this tightening cycle. They pointed to the decline in inflation seen during 2023 and to growing signs of demand and supply coming into better balance in product and labor markets as informing that view. Participants generally noted that they did not expect it would be appropriate to reduce the target range for the federal funds rate until they had gained greater confidence that inflation was moving sustainably toward 2 percent. Many participants remarked that the Committee's past policy actions and ongoing improvements in supply conditions were working together to move supply and demand into better balance. Participants noted that the future path of the policy rate would depend on incoming data, the evolving outlook, and the balance of risks. Several participants emphasized the importance of continuing to communicate clearly about the Committee's data-dependent approach.

In discussing risk-management considerations that could bear on the policy outlook, participants remarked that while the risks to achieving the Committee's employment and inflation goals were moving into better balance, they remained highly attentive to inflation risks. In particular, they saw upside risks to inflation as having diminished but noted that inflation was still above the Committee's longer-run goal. Some participants noted the risk that progress toward price stability could stall, particularly if aggregate demand strengthened or supply-side healing slowed more than expected. Participants highlighted the uncertainty associated with how long a restrictive monetary policy stance would need to be maintained. Most participants noted the risks of moving too quickly to ease the stance of policy and emphasized the importance of carefully assessing incoming data in judging whether inflation is moving down sustainably to 2 percent. A couple of participants, however, pointed to downside risks to the economy associated with maintaining an overly restrictive stance for too long.

Participants observed that the continuing process of reducing the size of the Federal Reserve's balance sheet was an important part of the Committee's overall approach to achieving its macroeconomic objectives and that balance sheet runoff had so far proceeded smoothly. In light of ongoing reductions in usage of the ON RRP facility, many participants suggested that it would be appropriate to begin in-depth discussions of balance sheet issues at the Committee's next meeting to guide an eventual decision to slow the pace of runoff. Some participants remarked that, given the uncertainty surrounding estimates of the ample level of reserves, slowing the pace of runoff could help smooth the transition to that level of reserves or could allow the Committee to continue balance sheet runoff for longer. In addition, a few participants noted that the process of balance sheet runoff could continue for some time even after the Committee begins to reduce the target range for the federal funds rate.

Committee Policy Actions

In their discussions of monetary policy for this meeting, members agreed that economic activity had been expanding at a solid pace. Job gains had moderated since early last year but remained strong, and the unemployment rate had remained low. Inflation had eased over the past year but remained elevated. Members judged that the risks to achieving the Committee's employment and inflation goals were moving into better balance. Members viewed the economic outlook to be uncertain and agreed that they remained highly attentive to inflation risks.

In support of the Committee's goals to achieve maximum employment and inflation at the rate of 2 percent over the longer run, members agreed to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. Members concurred that, in considering any adjustments to the target range for the federal funds rate, they would carefully assess incoming data, the evolving outlook, and the balance of risks. Members agreed that they did not expect that it would be appropriate to reduce the target range until they have gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, members agreed to continue to reduce the Federal Reserve's holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. All members affirmed their strong commitment to returning inflation to the Committee's 2 percent objective.

Members agreed that, in assessing the appropriate stance of monetary policy, they would continue to monitor the implications of incoming information for the economic outlook. They would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. Members also agreed that their assessments would take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Given that the stresses that emerged at some banks early last year have subsided, members agreed to remove from the statement the reference to the resilience of the U.S. banking system as well as to tighter financial and credit conditions and their effects on the economic outlook. Members also agreed to note the progress made toward the 2 percent inflation objective and the resilience of economic activity over the past year by stating that the Committee "judges that the risks to achieving its employment and inflation goals are moving into better balance." Regarding considerations relevant for future policy actions, members agreed, given their assessment of the policy rate being likely at its peak for this tightening cycle, to remove the reference to "the extent of any additional policy firming that may be appropriate to return inflation to 2 percent over time," as was included in the December statement. In its place, they agreed to adopt phrasing referencing their "considering any adjustments to the target range for the federal funds rate." Members also agreed that the statement should convey that "the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks" and that it "does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent."

At the conclusion of the discussion, the Committee voted to direct the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the SOMA in accordance with the following domestic policy directive, for release at 2:00 p.m.:

"Effective February 1, 2024, the Federal Open Market Committee directs the Desk to:

- Undertake open market operations as necessary to maintain the federal funds rate in a target range of 5-1/4 to 5-1/2 percent.

- Conduct standing overnight repurchase agreement operations with a minimum bid rate of 5.5 percent and with an aggregate operation limit of $500 billion.

- Conduct standing overnight reverse repurchase agreement operations at an offering rate of 5.3 percent and with a per-counterparty limit of $160 billion per day.

- Roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing in each calendar month that exceeds a cap of $60 billion per month. Redeem Treasury coupon securities up to this monthly cap and Treasury bills to the extent that coupon principal payments are less than the monthly cap.

- Reinvest into agency mortgage-backed securities (MBS) the amount of principal payments from the Federal Reserve's holdings of agency debt and agency MBS received in each calendar month that exceeds a cap of $35 billion per month.

- Allow modest deviations from stated amounts for reinvestments, if needed for operational reasons.

- Engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency MBS transactions."

The vote also encompassed approval of the statement below for release at 2:00 p.m.:

"Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have moderated since early last year but remain strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are moving into better balance. The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments."

Voting for this action: Jerome H. Powell, John C. Williams, Thomas I. Barkin, Michael S. Barr, Raphael W. Bostic, Michelle W. Bowman, Lisa D. Cook, Mary C. Daly, Philip N. Jefferson, Adriana D. Kugler, Loretta J. Mester, and Christopher J. Waller.

Voting against this action: None.

Consistent with the Committee's decision to leave the target range for the federal funds rate unchanged, the Board of Governors of the Federal Reserve System voted unanimously to maintain the interest rate paid on reserve balances at 5.4 percent, effective February 1, 2024. The Board of Governors of the Federal Reserve System voted unanimously to approve the establishment of the primary credit rate at the existing level of 5.5 percent, effective February 1, 2024.

It was agreed that the next meeting of the Committee would be held on Tuesday–Wednesday, March 19–20, 2024. The meeting adjourned at 10:25 a.m. on January 31, 2024.

Notation Vote

By notation vote completed on January 2, 2024, the Committee unanimously approved the minutes of the Committee meeting held on December 12–13, 2023.

_______________________

Joshua Gallin

Secretary

1. The Federal Open Market Committee is referenced as the "FOMC" and the "Committee" in these minutes; the Board of Governors of the Federal Reserve System is referenced as the "Board" in these minutes. Return to text

2. Attended through the discussion of the economic and financial situation. Return to text

3. Attended opening remarks for Tuesday's session only. Return to text

4. Attended Tuesday's session only. Return to text

5. Committee organizational documents are available at www.federalreserve.gov/monetarypolicy/rules_authorizations.htm. Return to text

6. Kartik B. Athreya's selection was effective upon employment at the Federal Reserve Bank of New York. Return to text

Fed Minutes Confirm that FOMC Will Take a Cautious Approach to Rate Cuts

The minutes from the January 30-31, 2024 Federal Open Market Committee (FOMC) highlight that the Fed has not declared victory in its fight against inflation, and that curtailing price pressures remains the current focus for the Fed.

On the current economic backdrop, Committee members noted that "recent indicators suggested that economic activity had been expanding at a solid pace. Real GDP growth in the fourth quarter of last year came in above 3 percent at an annual rate, below the strong growth posted in the third quarter but still above most forecasters’ expectations."

When discussing the appropriate policy actions, "all participants judged it appropriate to maintain the target range for the federal funds rate at 5¼ to 5½ percent at this meeting." This was supported by the progress made on inflation and that the labor market had continued to come into better balance.

On the future path of policy, Committee members viewed " that the policy rate was likely at its peak for this tightening cycle." Additionally, FOMC members stated that it is unlikely to reduce the target rate until they gained "greater confidence" that inflation is on a sustainable path to its target.

When discussing the risks to achieving their dual mandate, FOMC members stated that "the risks to achieving the Committee’s employment and inflation goals were moving into better balance, they remained highly attentive to inflation risks." Additionally, "most" participants noted the risks of moving prematurely, while a "couple" pointed to the risks of leaving rates in a restrictive position for too long.

Key Implications

With rate cuts highly expected in 2024, the timing and pace of cuts has become the focus of financial markets. Today's minutes reiterated that the Fed will take a patient approach to easing policy stating "they did not expect it would be appropriate to reduce the target range for the federal funds rate until they had gained greater confidence that inflation was moving sustainably toward 2 percent". This has been echoed by Chair Powell and several FOMC speakers. The cautious rhetoric can be seen in financial markets with the U.S. 2-year treasury yield adding close to 40 basis points since the beginning of February.

Since the January FOMC meeting, employment and inflation data have both surprised to the upside underscoring the need for the Fed to take a prudent approach to easing policy as the path to price stability will likely be uneven. This has also been reflected in financial markets, which have pared back their expectations for rate cuts in 2024. While economic resilience was the theme for the U.S. economy in 2023, we expect a modest slowdown in economic growth in 2024, setting the stage for the Fed to begin easing policy in the second half of the year.

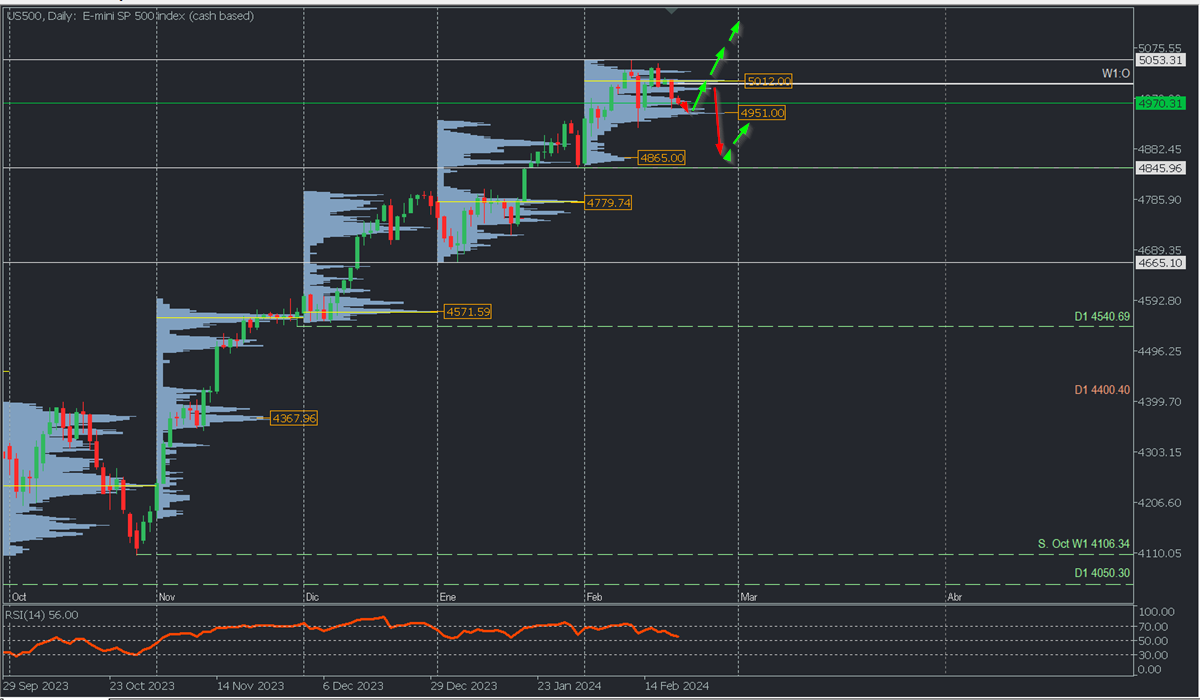

S&P 500 (US500): Consolidates in Buying Zone. Watch for a Surge Towards 5000 Intraday

Bullish Scenario: Buying above 4980 with TP1: 4993, TP2: 5005, and TP3: 5014 (Intraday levels). TP (Swing Trading): 5031.90, 5045.66, and 5054. It is recommended to set a stop loss (S.L.) below 4965 or at least 1% of the account capital**.

Bearish Scenario: Selling below 4960 with TP1: 4935, TP2: 0.6487, and TP3: 4924 (Intraday levels). TP (Swing Trading): 4910 and 4865. It is recommended to place a stop loss above 4975, at least 1% of the account capital**. A trailing stop can be used.

The high valuation of indices has been driven since the last quarter of the year by expectations that the Fed would cut rates early in the first quarter of 2024. Subsequently, with the start of the fourth-quarter earnings season of 2023, the optimism and momentum of technology companies have almost exclusively led the rally to new historic highs. Today, Nvidia, the last of the high-cap technology companies, publishes results with very high expectations that could either renew the indices' momentum to continue the bullish phase or, conversely, extend corrections in the event of results below market expectations. In this analysis, we address possible scenarios from the perspective of liquidity with volume profile and price action.

Analysis from the daily chart. Volume Profile and Structure.

The US500 continues in an uptrend, leaving the last resistance and historical high at 5053.31 on February 12th, trading below a high volume concentration zone or POC* around 5012, which coincides with the week's opening. The high volume node around 4951 represents a support from where bulls could trigger a new price rally seeking to break the macro selling zone around 5012 and thereby possibly breaking the resistance at 5053.31 to extend purchases towards the new psychological level at 5100.

On the other hand, a decisive breakthrough below 4951/50 will pave the way for a more extensive correction towards 4865, the origin buying zone of the February rally. The last support of the uptrend is located at 4844.60.

Scenario from the H2 chart:

The bearish correction reached support at 4959.81 with a moderate bullish reaction that could extend if quotes decisively surpass the POC of the first sessions of the day at 4974.68 and of course the day's opening, paving the way for more purchases with the target at yesterday's uncovered POC* at 4993.68, a selling zone that on initial touch may provoke a retreat as previously positioned bears defend it.

However, after a second touch, a decisive breakthrough is likely to occur, taking quotes towards the week's opening at 5005.86 and the daily bullish average range at 5014.23, a scenario that will remain valid as long as quotes do not break the support at 4959.81, in which case we will see the extension of the bearish correction at least towards the bearish average range at 4935.02. The RSI in negative territory could bounce from oversold to the midpoint, confirming not only the bearish momentum but also its temporary exhaustion.

*Uncovered POC: POC = Point of Control: It is the level or zone where the highest volume concentration occurred. If there was a bearish movement from it previously, it is considered a selling zone and forms a resistance zone. On the contrary, if there was a bullish impulse previously, it is considered a buying zone, usually located at lows, forming support zones.

**Consider this risk management suggestion

**It is imperative that risk management is based on capital and traded volume. For this, a maximum risk of 1% of capital is recommended. It is suggested to use risk management indicators such as the Easy Order.

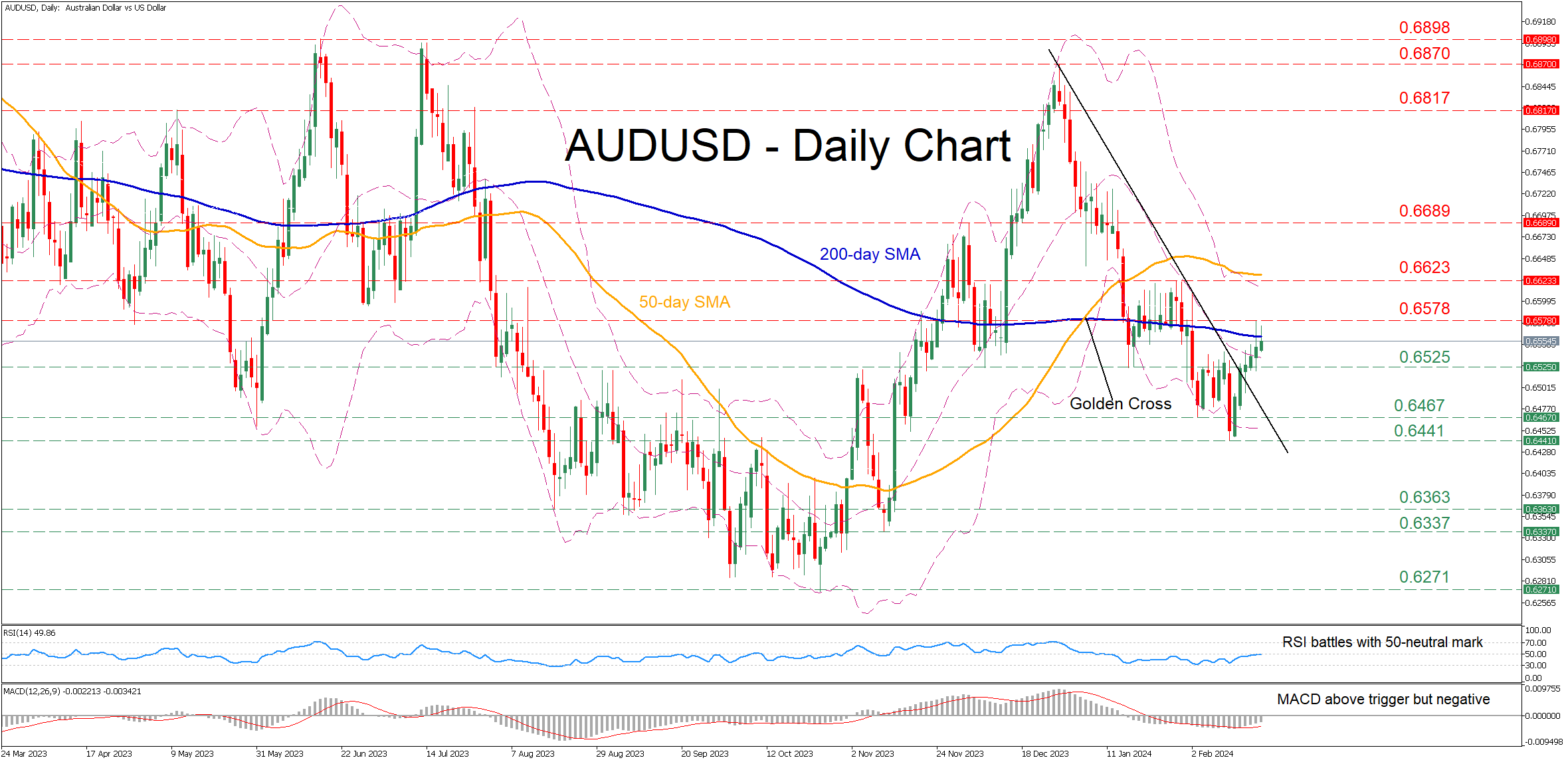

AUDUSD Challenges 200-day SMA

- AUDUSD rebounds from its lowest level since November

- Price jumps above descending trendline to test 200-day SMA

- Momentum indicators improve but remain in negative zones

AUDUSD had been in a constant decline after peaking at 0.6870 in December, breaking below both its 50- and 200-day simple moving averages (SMAs). Nevertheless, the pair managed to find its feet and rotate back above its descending trendline, currently attempting to claim the crucial 200-day SMA.

Should the price break above the 200-day SMA, the recent resistance of 0.6578 could prove to be the first barrier for the bulls to clear. Further advances could then cease at the January resistance of 0.6623 ahead of the 0.6689 hurdle. Surpassing that region, the pair might challenge the May peak of 0.6817.

On the flipside, if the pair reverses back lower, initial support could be found at 0.6525, which held strong both in December and January. A violation of that region could open the door for 0.6467 before the 2024 bottom of 0.6441 comes under examination. Sliding beneath that floor, the pair may descend towards the August low of 0.6363.

Overall, AUDUSD has regained traction following its bounce off the 2024 low of 0.6441. However, a break above the 200-day SMA is needed for the bulls to regain confidence for a full-scale reversal.

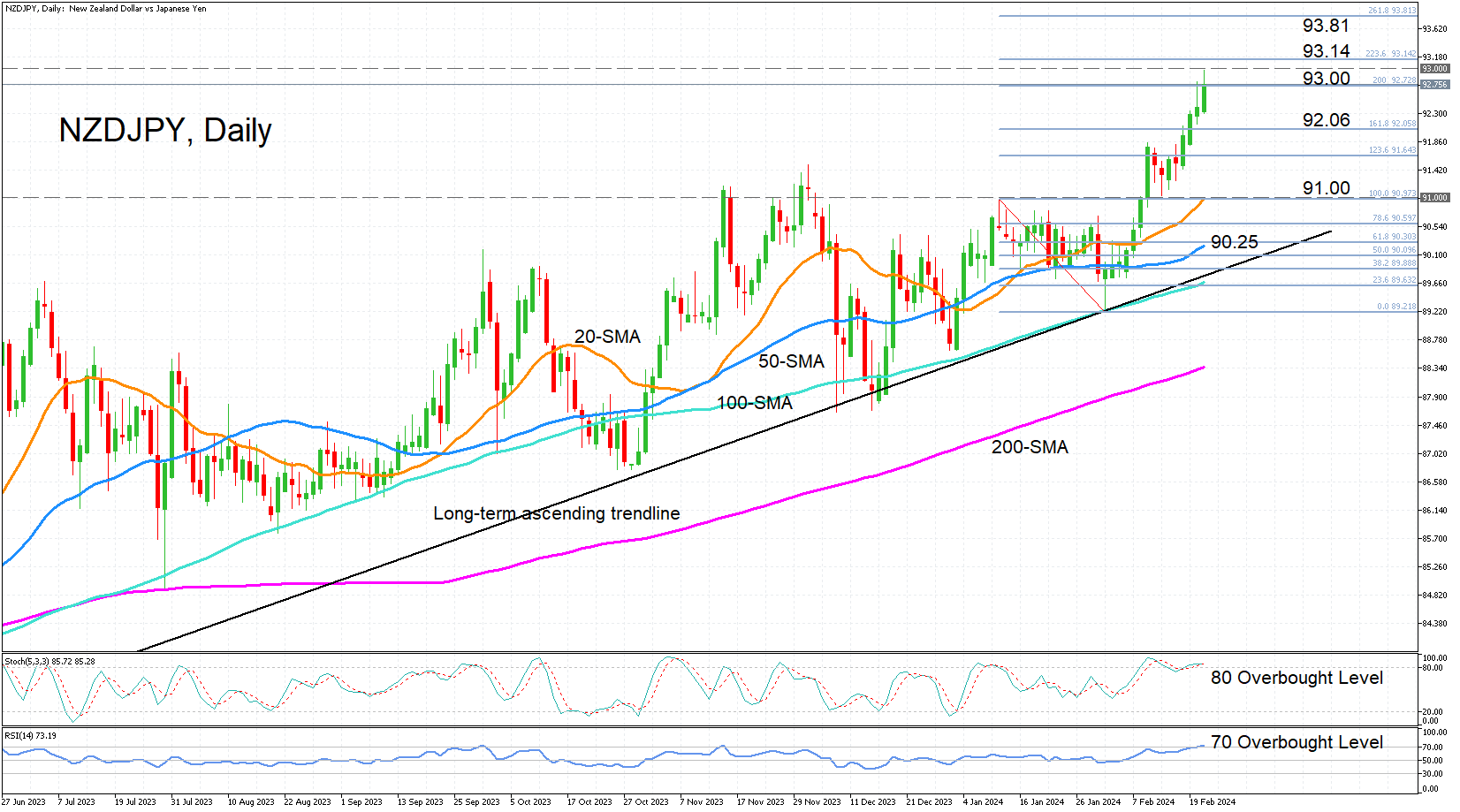

NZDJPY Hits Nine-Year High as Bullish Run Continues

- NZDJPY extends bullish streak above 92.00 level

- Bulls remain firmly in control

- Overbought signals begin to flash red

NZDJPY has been recording fresh highs all week and scaled a nine-year high of 92.98 earlier on Wednesday. The momentum indicators suggest that the bullish bias isn’t likely to fade in the near term. However, both the RSI and the stochastics have entered overbought territory, pointing to increased risk of a downside correction.

If the pair makes a renewed push towards the 93.00 handle, there could be stiff resistance until the 93.14 mark, which is the 223.6% Fibonacci extension of the January downleg. Successfully clearing this area would turn the focus to the 261.8% Fibonacci extension of 93.81.

However, if the rally runs out of steam and the price heads south, there’s likely to be some support around the 161.8% Fibonacci of 92.06. A slip below it could accelerate the decline, dragging the pair towards the 20-day simple moving average (SMA) just below the 91.00 level. Further down, the 50-day SMA might try to stem the losses at 90.25 before the long-term ascending trend line is tested.

In a nutshell, a drop below the 20- and 50-SMAs would shift the short-term picture to negative but as long as the price holds above the uptrend line, the bullish outlook in the long term should stay intact.

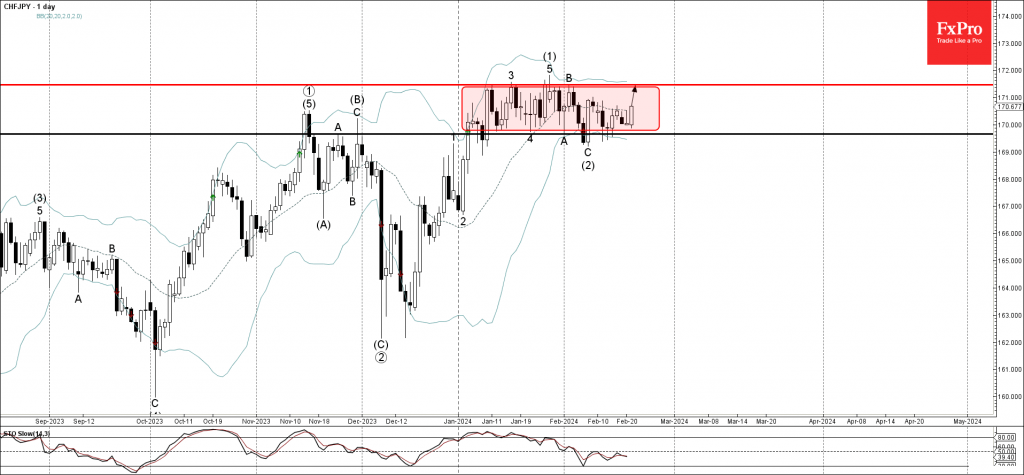

CHFJPY Wave Analysis

- CHFJPY reversed from support level 169.65

- Likely to rise to resistance level 171.45

CHFJPY currency pair recently reversed up from the key support level 169.65 (lower boundary of the narrow sideways price range inside which the pair has been trading from the start of January).

The support level 169.65 was strengthened by the lower daily Bollinger Band.

Given the clear daily uptrend and the continued yen sales, CHFJPY currency pair can be expected to rise further to the next resistance level 171.45, upper border of this price range.

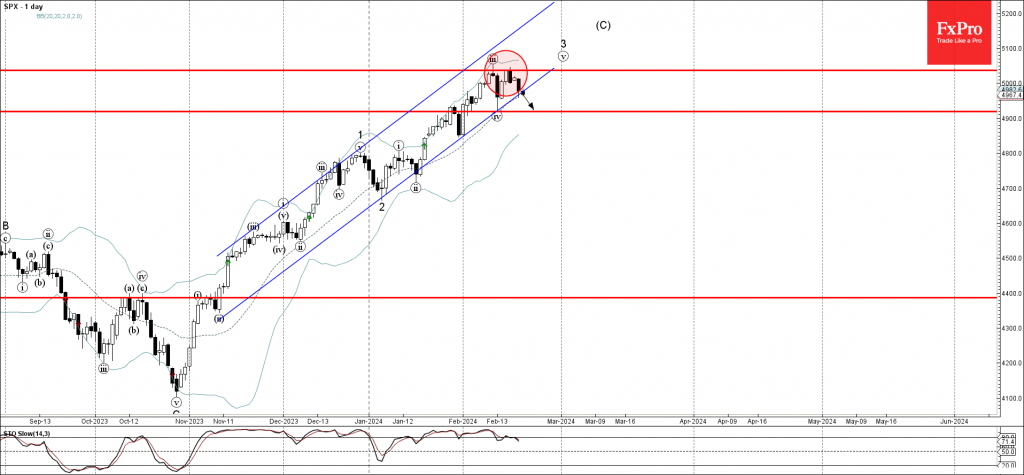

S&P 500 Wave Analysis

- S&P 500 reversed from resistance level 5035.00

- Likely to fall to support level 4920.00

S&P 500 index recently reversed down from the pivotal resistance level 5035.00 (which stopped the previous minor impulse wave iii at the start of this month).

The downward reversal from the resistance level 5035.00 created the daily Japanese candlesticks reversal pattern Bearish Engulfing, which was preceded by the daily Evening Star near this price level.

Having just broken the sharp daily up channel from November, S&P 500 index can be expected to fall further to the next support level 4920.00 (low of the previous wave iv).