Sample Category Title

Will FOMC Minutes Give Clues on the Timing of Rate Cuts?

In focus today

Today, we receive euro area consumer confidence figures for February. Consumer confidence is still at a low level which is likely the reason for the sluggish consumption ratio. Consumer confidence rebounded strongly during the first half of 2023 but has since stagnated. An increase in consumer confidence could be the trigger for higher private consumption in 2024 as real incomes improve.

Tonight, minutes from the FOMC's January meeting will be released. Markets will keep a close eye on any clues regarding the timing of the first rate cut, which we now expect to come in May. In addition, the Fed's Bostic and Bowman will be on the wires ahead of the release.

Overnight, Japanese PMI figures kick off the slew of PMI data that is due tomorrow.

Economic and market news

What happened overnight

Japanese export volumes declined 4.6% in January indicating a slow start to the year following the technical recession in 2023H2. That said, January PMIs were more uplifting but have not been a good GDP indicator recently.

What happened yesterday

Yesterday we got Q4 GDP figures for Denmark, which showed an impressive rebound with a growth rate of 2.0% q/q. Furthermore, Q3 growth was revised up to 0.4% from -0.7%. The development was largely driven by pharmaceuticals, where manufacturing GVA increased almost 8% q/q in Q4, which also drove exports higher. Consumption also ticked up with quarterly growth of 1.7%, indicating somewhat less cautious consumers. All in all, this means the economy grew 1.8% for the year 2023, which is substantially more than the Eurozone. However, when excluding pharmaceuticals, the numbers show a decline of 0.1%.

Euro Area negotiated wage growth declined to 4.46% in Q4 from 4.7% y/y in Q3. This was in line with other trackers from the ECB and suggests that wage growth peaked in Q3. The ECB has repeatedly told markets that they await more data on wage growth, so this should provide some comfort, though they will likely still be cautious as we have yet to get the full overview of wage growth in Q4, which we will get with the "compensation per employee" print, due for release on 8 March. The market reaction was muted, with pricing still suggesting the first rate cut in June.

Finally, we got somewhat dovish comments from Bank of England governor Andrew Bailey who said that it was "not necessary" to wait for inflation to come back to target before cutting rates, adding also that the Bank was particularly focused on whether services inflation and wage growth were on a sustained path towards headline inflation. The market reaction was muted.

Equities: Global equities were lower yesterday with DM underperforming EM. DM is driven by macro and inflation data while EM is driven by China and the next step of policy support for the property sector. Defensive value outperforming globally on the higher for longer narrative but also boosted by earnings reports and earnings expectations yesterday. Investors embracing the earnings from retailers while taking some chips of the table in tech space ahead of tonight's reporting from Nvidia. Yesterday in the US Dow -0.2%), S&P 500 -0.6%, Nasdaq -0.9% and Russell 2000 -1.4%. Asian markets are mixed as the tech sector is dragging down most indices. Chinese indices are mostly higher as property developers are rising on the back of the last batch of policy support. Futures in US and Europe are mixed this morning with the tech-heavy indices trailing the rest.

FI: There was a modest decline in global bond yields yesterday, where 10Y US Treasury yields declined 3-4bp relative to the opening level on Tuesday morning. 10Y German govt yield also declined 4-5bp. There was also a bullish steepener between 2Y and 10Y for both the US and European government bond yield curves.

FX: SEK gained for the second straight day versus the rest of the G10 closely followed by the EUR, NZD and AUD. CAD and USD lost some ground yesterday, with EUR/USD rising to a two-week high just below 1.0840.

Nvidia Hasn’t Said Anything Yet, and Market Already Making Big Swings

Nvidia hasn’t said anything yet, and the market is already making big swings – to give you an idea on the potential of a positive or a negative move when the results finally arrive. Yesterday, Nvidia tumbled nearly 6% out of the blue, and closed the session more than 4% down, as some investors – who were obviously long Nvidia - preferred to take their profits in their pockets and move to the sidelines to avoid taking the risk of a major move that could spoil their profits – if the move happens toward the wrong direction.

Nvidia will release the most expected earnings of the quarter today, after the bell. Nvidia is expected to announce a sales revenue of around $20bn in the Q4 and earnings per share of $4.60. The numbers are huge if you think that sales were worth around $6 billion, and EPS was just 88 cents a year ago. We are talking about a more than 200% sales growth – which, no matter if the company meets expectations or not – is HUGE. But of course, the price action was big too. Nvidia is up by more than 400% since the beginning of 2023. This is why any correction could be massive. According to options positioning we could see a 10% move to the upside or to the downside – which is totally acceptable for a tech giant, mind you. Meta rallied 20% after reporting its own earnings this season. Still, the capital shake is expected to be impressive. Nvidia results could trigger a quake of a magnitude of $200bn, and a tsunami of tens and potentially hundreds of billion dollars across the market. Mixed earnings and – God Forbid – an earnings miss has potential to send Nvidia’s stock price tumbling, while an earnings beat could fail to gather enough positive momentum – if the beat is not enough strong. This is HOW STRONG the expectations are.

Zooming out, Nvidia’s 4% drop yesterday sent an early warning to the market. The S&P500 retreated 0.6% and settled below the 5000 at the close, while Nasdaq fell nearly 0.80%. It almost feels like Nvidia earnings could be a decisive moment in the AI rally as many expect the AI bubble to burst at some point. But it’s worth noting that, whatever happens today, the AI revolution is happening. Massive investments are being made in the sector and money will continue to follow. The question won’t be whether demand for AI businesses will be enough, it is whether the companies have enough capacity to satisfy the exploding demand.

Did someone say a ‘hike’?

Besides Nvidia, the Federal Reserve (Fed) will release its latest meeting minutes in the middle of confused expectations. The year started with the expectation that the Fed would start cutting the rates as soon as March. These expectations got quickly scaled back on the back of very strong jobs data, otherwise strong economic data and an uptick in latest inflation updates. And now we can feel the winds changing direction as not only that the first Fed cut expectation has been pushed back to June – with some 80% chance attached to it – but some start saying that the next move from the Fed could even be a rate hike!

That’s clearly now what currency traders think right now. The US dollar index is giving back strength, and the EURUSD is back above the 1.08 level before the surprised eyes of the euro bears - who were expecting the morose European growth outlook to at least keep the EURUSD within the ytd bearish trend. The dollar appetite will determine whether the pair deserves to extend gains above the 200-DMA or not.

And one more thing about the rate HIKE discussion. The Reserve Bank of Australia (RBA) and the Reserve Bank of New Zealand (RBNZ) have both left the door open to the possibility of further policy tightening. At this stage, it is just an idea and not a maturing decision, but desolation would be massive if the RBNZ decided to hike on February 28.

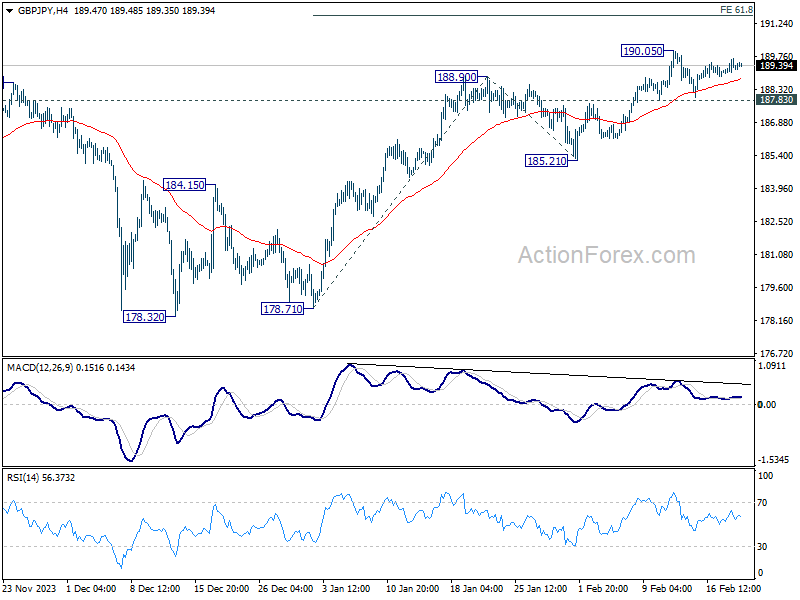

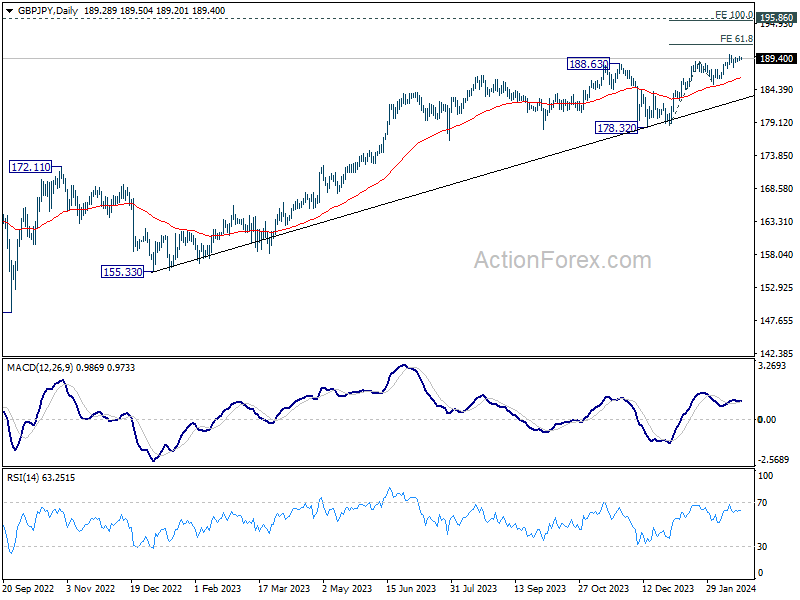

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.99; (P) 189.36; (R1) 189.70; More...

Intraday bias in GBP/JPY remains neutral as consolidations continue below 190.05. Further rally is expected with 187.83 minor support intact. Break of 190.05 will target 61.8% projection of 178.71 to 188.90 from 185.21 at 191.50. However, break of 187.83 will turn bias to the downside for deeper correction back to 185.21 support instead.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

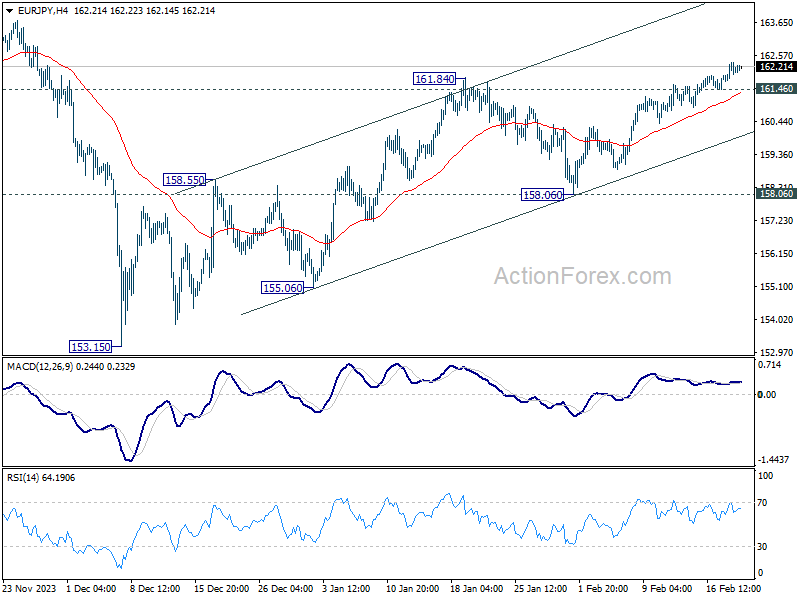

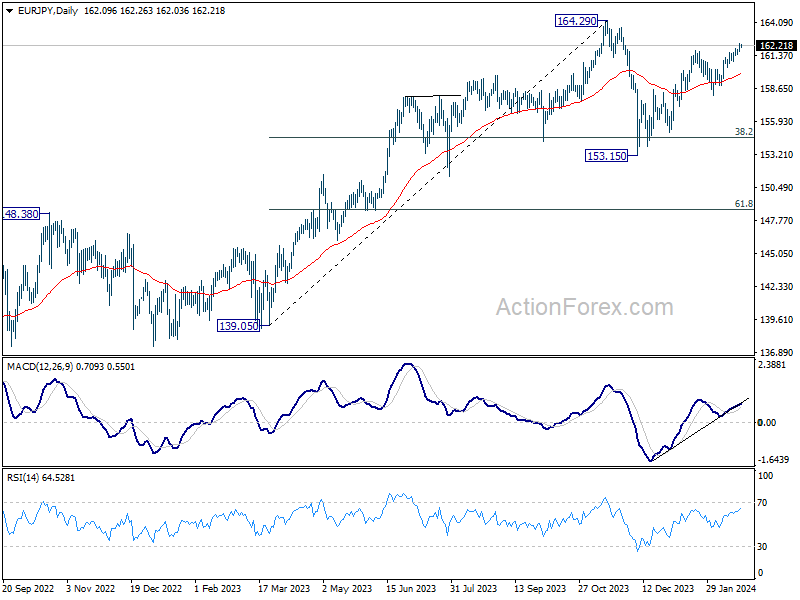

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.78; (P) 162.07; (R1) 162.41; More...

Intraday bias in EUR/JPY remains on the upside at this point. Current rally from 153.15 is in progress for retesting 164.29 high. On the downside, however, below 161.46 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

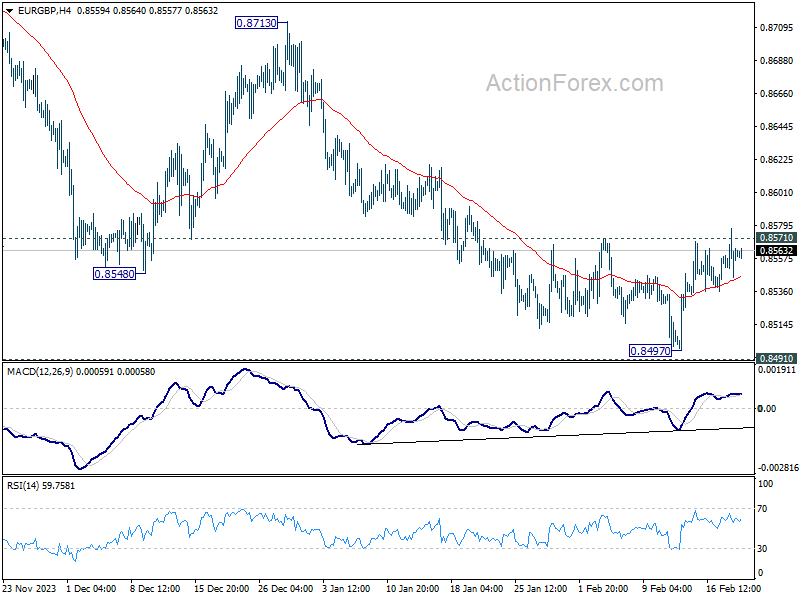

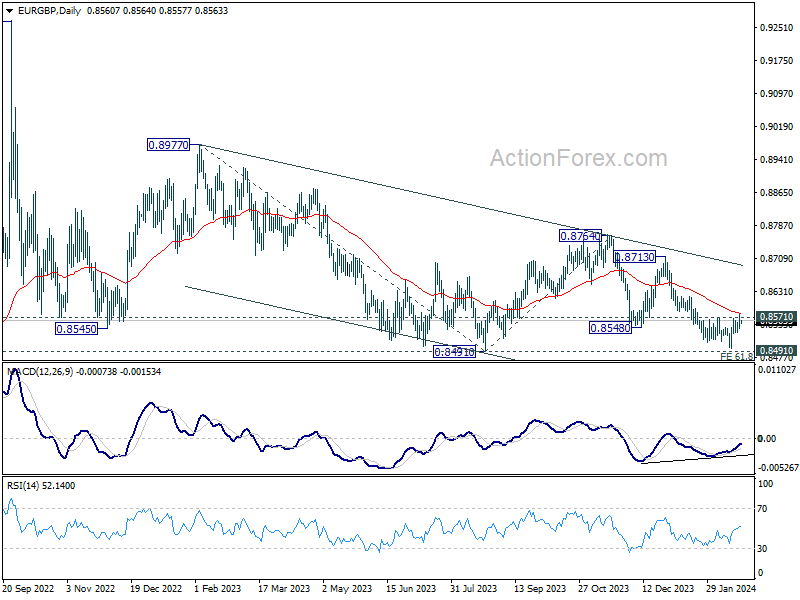

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8546; (P) 0.8562; (R1) 0.8578; More...

Intraday bias in EUR/GBP remains neutral for the moment and outlook is unchanged. On the downside, break of 0.8497 will resume recent fall to 0.8464 projection level. However, considering bullish convergence condition in 4H MACD, sustained break of 0.8571 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

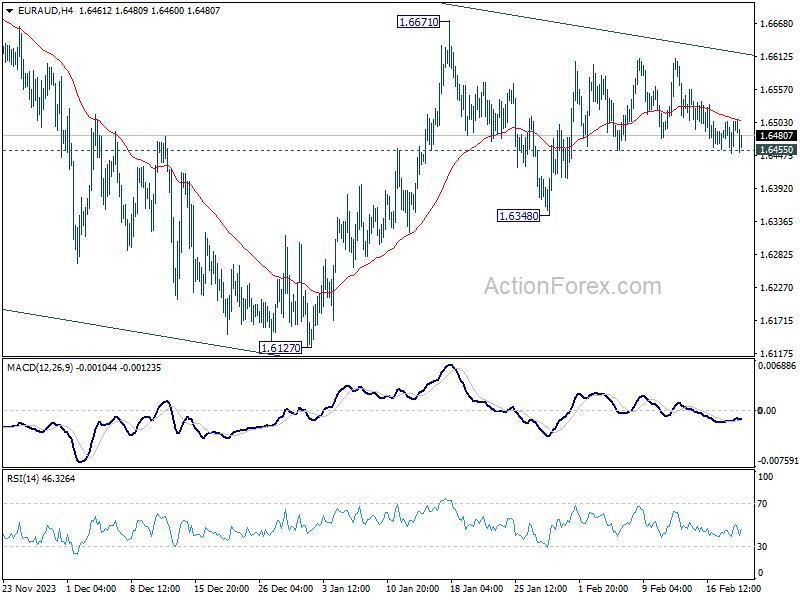

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6469; (P) 1.6487; (R1) 1.6523; More...

Intraday bias in EUR/AUD stays neutral at this point. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, below 1.6455 minor support will turn bias to the downside for 1.6348 and possibly below.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

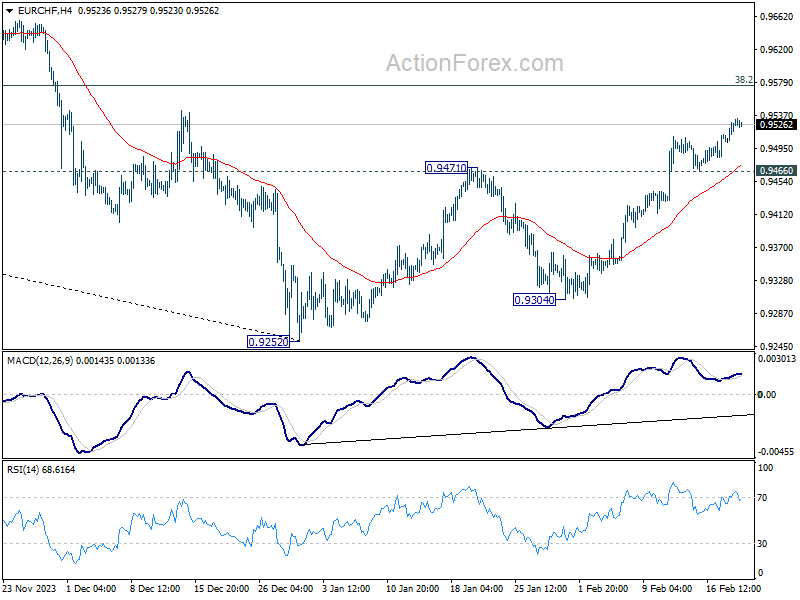

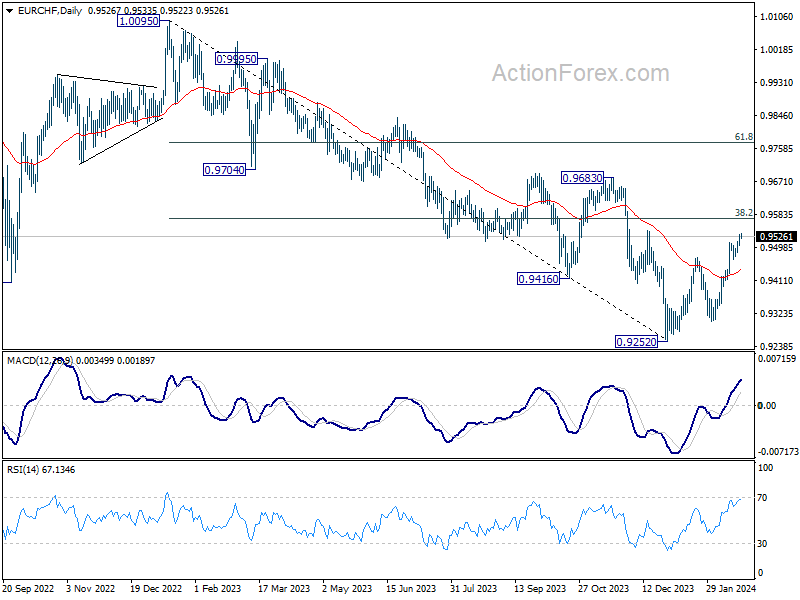

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9514; (P) 0.9523; (R1) 0.9542; More...

Intraday bias in EUR/CHF remains on the upside for the moment. Current rise from 0.9252 should target 0.9574 fibonacci level next. However, considering possible bearish divergence condition in 4H MACD, break of 0.9466 minor support will indicate short term bottoming, and turn bias back to the downside.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574 and possibly above. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

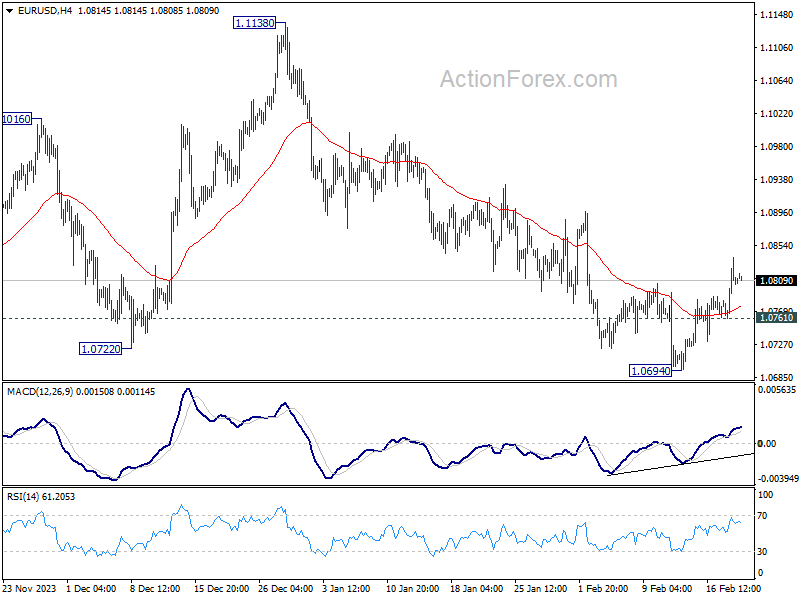

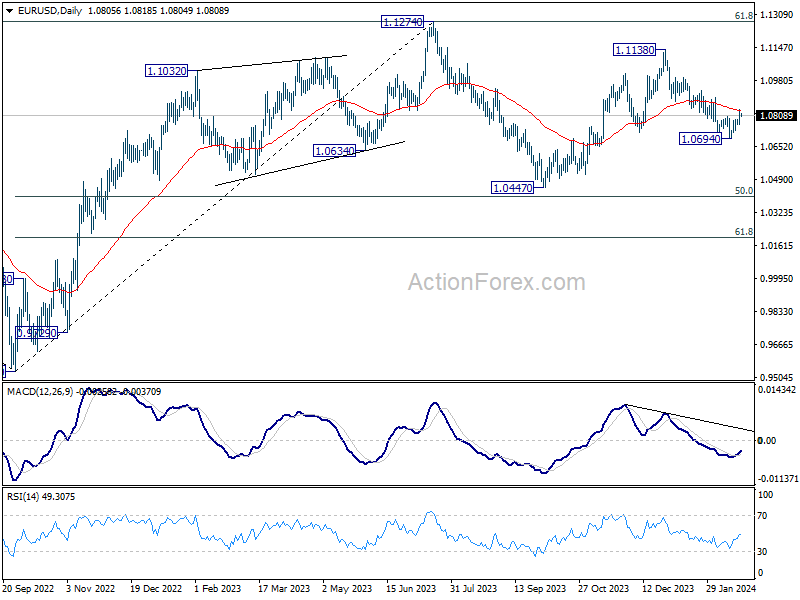

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0767; (P) 1.0803; (R1) 1.0844; More...

Intraday bias in EUR/USD remains mildly on the upside as rebound from 1.0694 short term bottom is in progress. Sustained trading above above 55 D EMA (now at 1.0832) will argue that fall from 1.1138 has completed and target this resistance. Meanwhile, rejection by 55 D EMA, followed by break of 1.0761 minor support will retain near term bearishness, and bring retest of 1.0694 first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

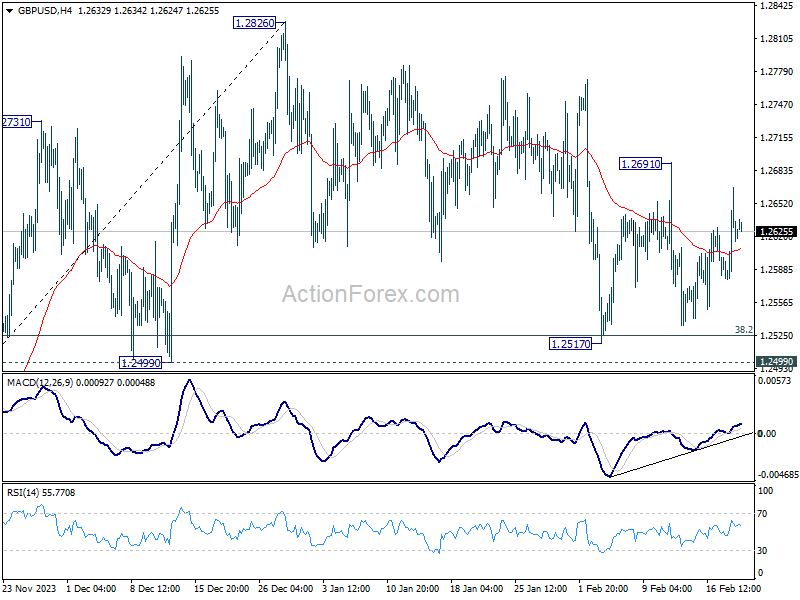

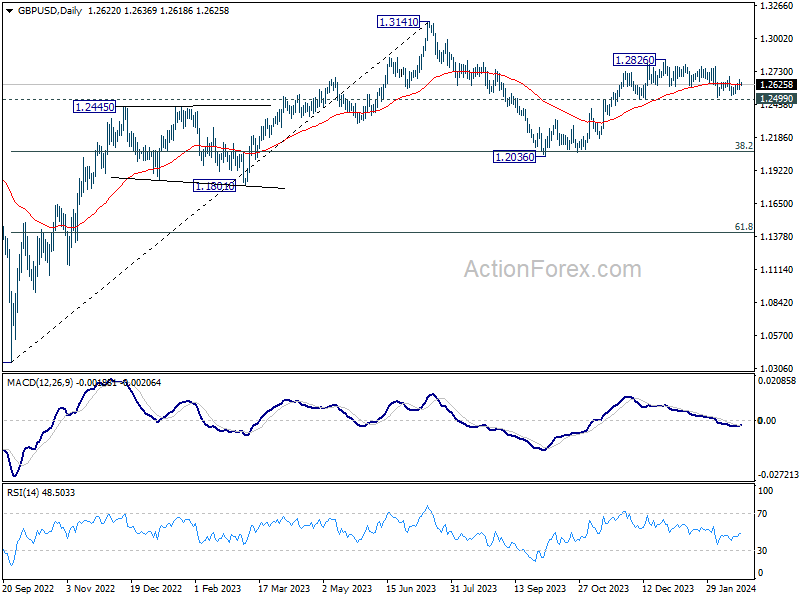

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2578; (P) 1.2623; (R1) 1.2668; More...

GBP/USD is still staying in range of 1.2517/2619 and intraday bias remains neutral at this point. On the upside, break of 1.2691 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

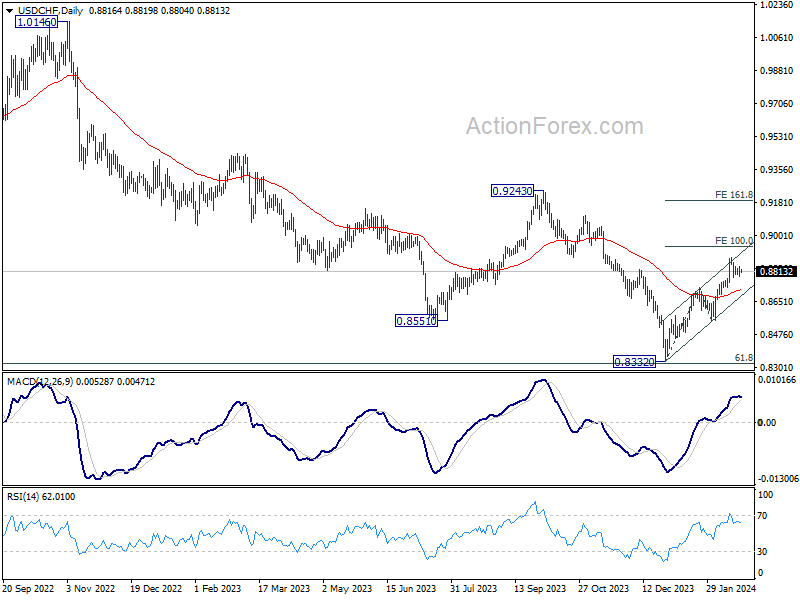

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8791; (P) 0.8814; (R1) 0.8843; More....

Intraday bias in USD/CHF remains neutral as consolidation from 0.8884 is extending. With 0.8727 resistance turned support intact, further rally is still expected. On the upside, break of 0.8885 will resume the rise from 0.8332 and target and 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.