Sample Category Title

Canada: Inflation Sees Some Welcomed Cooling in January

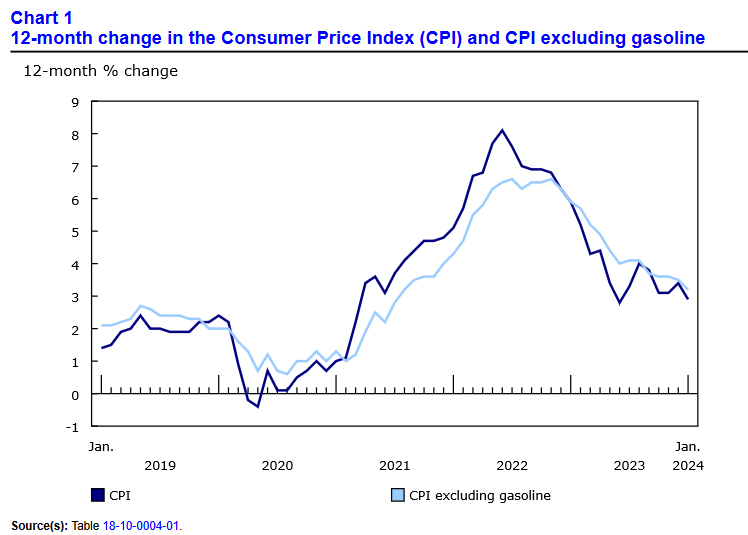

Headline CPI inflation cooled more than expected in January, stepping down half a point to 2.9% year-on-year (y/y).

Energy prices, and more specifically gasoline prices, were a key part of lower inflation, with gasoline prices down 4% versus a year ago. But even ex-gasoline headline CPI inflation slowed from 3.5% y/y in December to 3.2% y/y in January.

Grocery inflation also cooled in January, with prices up 3.4% y/y compared to 4.7% in December. Other good news for consumers came from airfares (-14.3% y/y) and travel tours.

However, consumer's biggest ticket item, shelter, saw steeper price increases in January, up 6.2% y/y from 6.0% in December. Rent inflation ticked up to 7.8% y/y in January, up from 7.5% in December. Owned accommodation inflation remained steady at 6.7%. This kept overall services inflation elevated at 4.2% y/y.

In contrast, goods inflation showed signs of cooling. Core goods prices were up only 1.5% y/y in January, down from 2.2% in December. Clothing and footwear prices were down 1.3% y/y in January, helping to reduce core goods inflation.

The Bank of Canada's preferred "core" inflation measures also cooled a bit in January with CPI trim up 3.4% y/y and CPI median up 3.3% y/y, versus 3.7% and 3.5% in December.

Key Implications

Canadians got a bit better news on the inflation front in January, with headline inflation dipping a toe below 3%, and the Bank of Canada's (BoC) preferred core measures also making progress. With various discretionary items showing signs of larger-than normal seasonal discounting, the weak consumer demand that has prevailed in Canada for some time may finally be starting to show up in prices. Shelter inflation remains a thorn in the BoC's side. As discussed in a report out soon, shelter inflation has become the biggest hurdle preventing the Bank from cutting interest rates.

The BoC is likely to be pleased with the progress on inflation to start the year, but inflation remains too far above target to start cutting rates. We expect that price pressures will continue to come off the boil in the coming months, and that the Bank will be ready to cut rates come the spring.

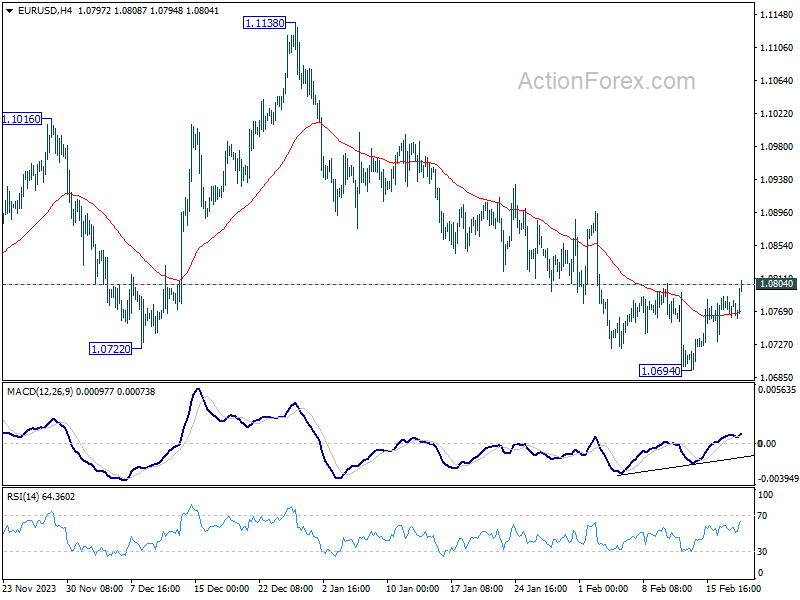

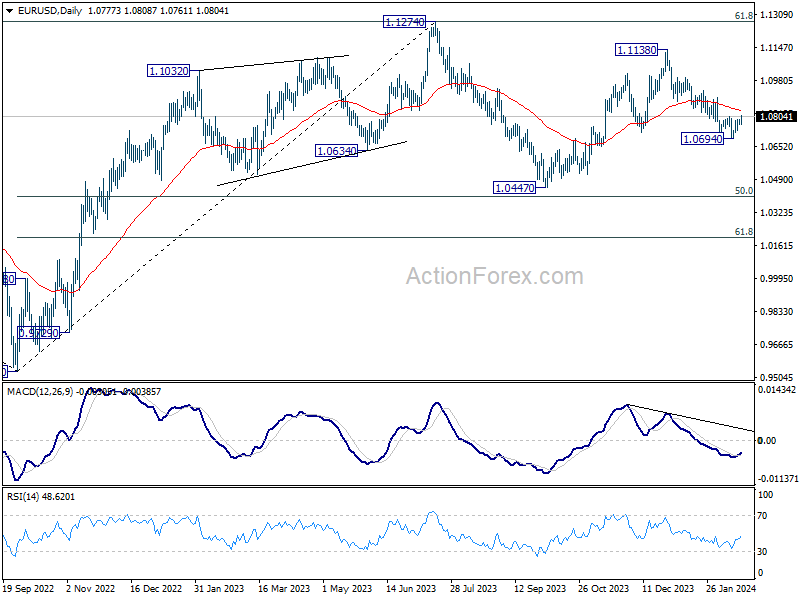

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0765; (P) 1.0777; (R1) 1.0792; More...

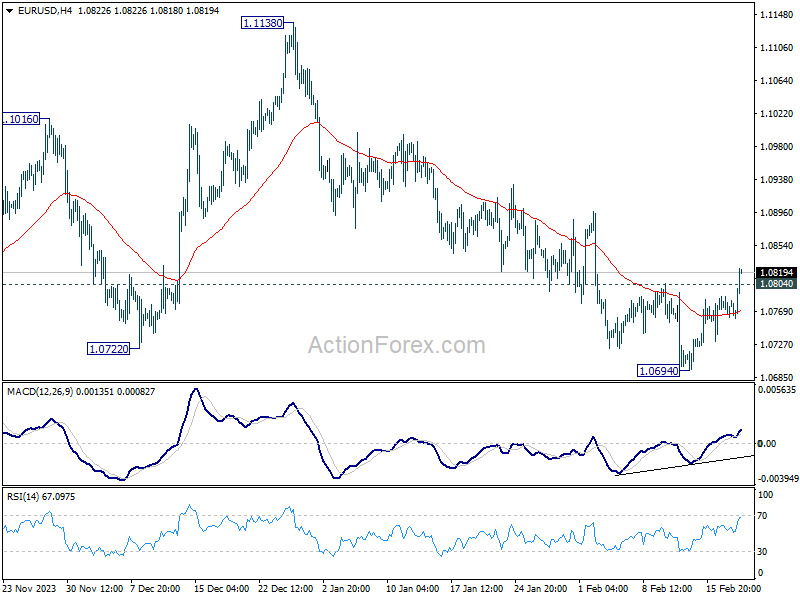

EUR/USD's break of 1.0804 resistance suggests short term bottoming at 1.0694, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for stronger rebound. Sustained above 55 D EMA (now at 1.0833) will argue that fall from 1.1138 has completed and target this resistance. Meanwhile, rejection by 55 D EMA, followed by break of 1.0694, will resume the fall from 1.1138 to 1.0447 support.

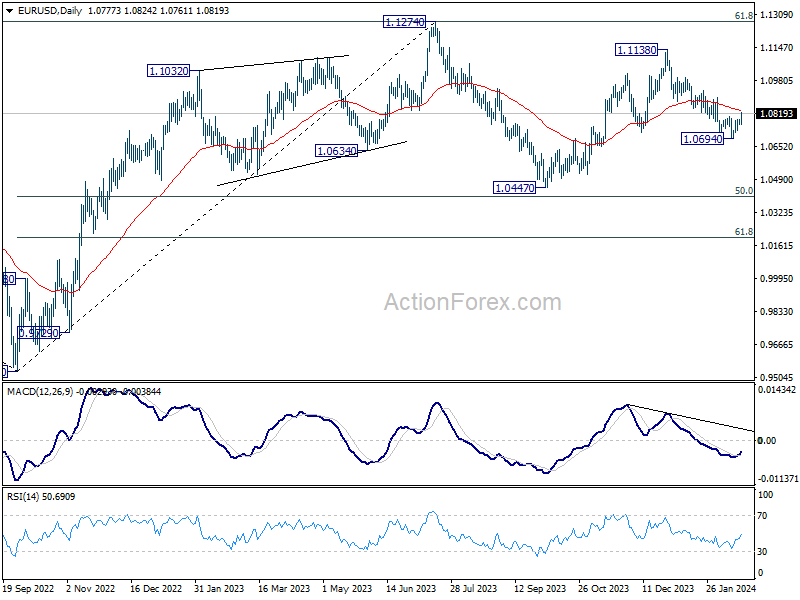

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

Disinflation Progress Spurs Loonie Decline, Euro Climbs on Wage Data

Canadian Dollar weakens broadly in early US session, sparked by data indicating a stronger-than-anticipated progress in disinflation. Headline CPI fell below the 3% mark, accompanied by significant easing in core inflation measures. This development potentially opens the door for BoC to consider an interest rate cut sooner than anticipated, with the second quarter now appearing as a viable window for such a policy adjustment.

Conversely, Euro surges earlier today, buoyed by data from ECB's wage tracker that reported only a marginal decrease in wage growth. Although this slight dip may be viewed as a positive sign, it does not sufficiently alleviate pressures to prompt an immediate rate cut in March. With wage pressures remaining on the higher side, a rate cut by ECB is more feasibly expected around June rather than April.

Despite Euro's jump, it currently finds itself outperformed by both Australian and New Zealand Dollars in terms of currency strength. Dollar trails behind Canadian as the second weakest, followed by Japanese Yen, while Swiss Franc and Sterling are mixed.

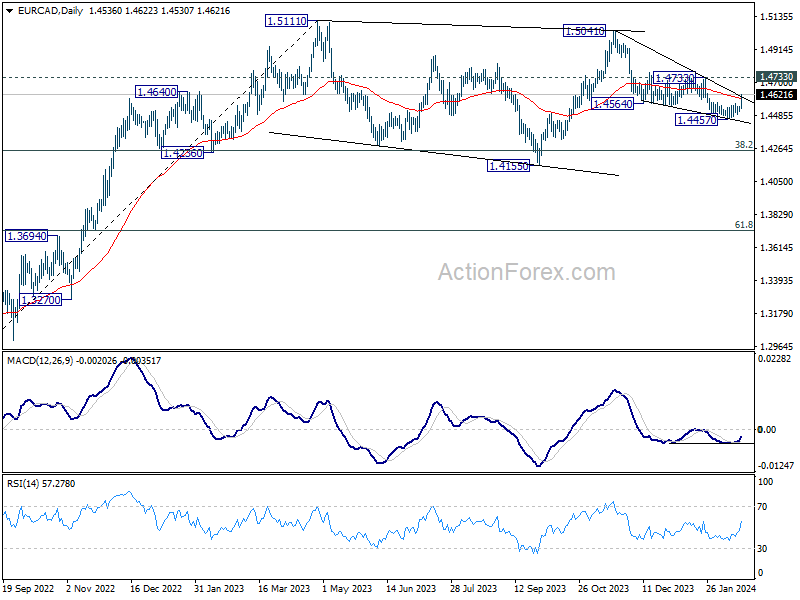

Technically, EUR/CAD breaks through 55 D EMA with today's strong rise. Focus is now back on 1.4733 resistance in the near term. Firm break there will argue that fall from 1.5041 has completed as a correction, with three waves down to 1.4457. That would revive the case that medium term consolidation from 1.5111 has completed at 1,.4155. In other words, if this bullish development realizes, EUR/CAD could then be ready to break through 1.5111 to resume the larger up trend.

In Europe, at the time of writing, FTSE is up 0.13%. DAX is don -0.13%. CAC is up 0.24%. UK 10-year yield is down -0.0376 at 4.072. Germany 10-year yield is down -0.017 at 2.397. Earlier in Asia, Nikkei fell -0.28%. Hong Kong HSI rose 0.57%. China Shanghai SSE rose 0.42%. Singapore Strait Times rose 0.56%. Japan 10-year JGB yield rose 0.0030 at 0.733.

Canada's CPI slows to 2.9% yoy in Jan, ex-gasoline down to 3.2%

Canada's CPI slowed from 3.4% yoy to 2.9% yoy in January, much lower than expectation of 3.3% yoy. The largest contributor to headline deceleration was lower year-over-year prices for gasoline (-4.0%). Excluding gasoline, CPI also fell from 3.5% yoy to 3.2% yoy. Food prices growth also fell from 4.7% yoy to 3.4% yoy. On a monthly basis, the CPI was unchanged, following a -0.3% mom decline in December.

Looking at the core measures, CPI median fell from 3.5% yoy to 3.3% yoy, below expectation of 3.6% yoy. CPI trimmed fell from 3.7% yoy to 3.4% yoy, below expectation of 3.6% yoy. CPI common fell from 3.9% yoy to 3.4% yoy, below expectation of 3.8% yoy.

BoE Bailey: Market's rate cut outlook not unreasonable, yet unendorsed

In a session with the Treasury Select Committee today, BoE Governor Andrew Bailey acknowledged that It's "not unreasonable" for the market to think about reductions in interest rates this year

However, he was quick to qualify this by stating that MPC "do not endorse the market curve" forecasting such cuts, adding that "we are not making a prediction of when or by how much" BoE cuts interest rates.

Bailey pointed to "encouraging signs" in key economic indicators, but stressed the importance of "sustained progress" in tackling inflation.

Addressing recent data indicating the UK's entry into a technical recession in the latter half of the previous year, Bailey downplayed its impact, describing the downturn as "very weak" and pointing to "distinct signs of an upturn."

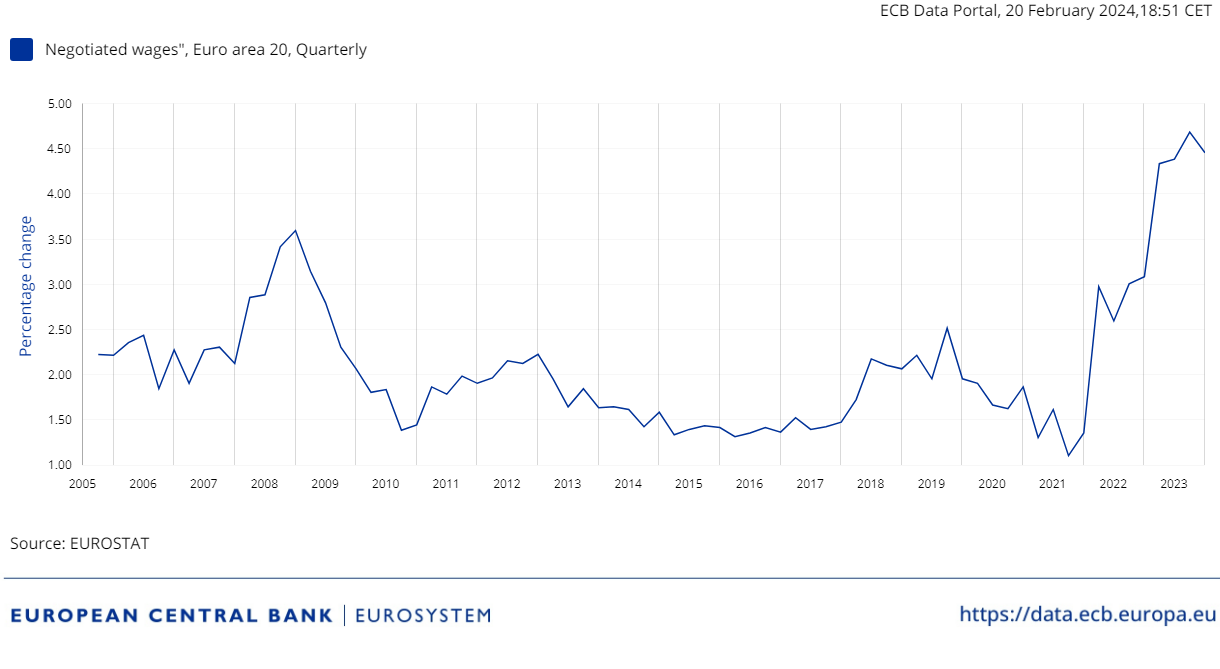

ECB wage growth data: A glimpse of hope but no trigger for immediate rate cuts

ECB released data today indicating a slight decrease in negotiated wage growth to 4.46% in Q4, marking a downturn from the previous quarter's record high of 4.69%. This development, though modest, is likely to be greeted positively by ECB policymakers, signaling a potential onset of wage growth deceleration anticipated throughout the year.

Despite the reduction, the magnitude of the drop is not substantial enough to prompt ECB to consider an immediate rate cut in March. The data presents a cautious optimism rather than a clear-cut rationale for policy easing. If ECB's more hawkish members advocate for further evidence of wage growth deceleration, preferring to wait for the next wage data release in May, the likelihood shifts towards a rate cut in June, rather than April, as the more plausible timeline for monetary policy adjustment.

RBA minutes: High costs of persistent inflation may necessitate additional rate hike

RBA minutes from the February 5-6 meeting revealed that the Board considered both an 25bps rate hike and maintaining the current rate. The choice to hold rates was influenced by a perceived reduction in the risk that inflation would fail to revert to the target range "within a reasonable timeframe." However, the potential repercussions of inflation not normalizing as anticipated were deemed "potentially very high," leaving the door open for future rate increases.

Central to the decision was the observation that moderation in inflation over preceding months had been "slightly larger than previously expected". Global experiences had also provided "additional confidence" on the disinflation trend. Additionally, incoming data suggested "weaker than previously expected" labor market conditions and consumer spending.

The assessment of risks surrounding the economic outlook as "broadly balanced". RBA emphasized the importance of remaining vigilant, opting to monitor evolving risks closely before making further policy adjustments. The acknowledgment of the high "costs" associated with inflation remaining above target for too long underscores the cautious stance, with members unanimously agreeing on the necessity to "not to rule out a further increase" in the cash rate target.

China announces historic reduction in benchmark mortgage rates

In an effort to revitalize its beleaguered property sector and inject vitality into the broader national economy, China has taken larger than expected action by reducing a crucial reference rate for mortgage loans.

PBoC announced a significant cut in five-year loan prime rate to 3.95% from 4.20%. This move surpassed market expectations of a more modest reduction of 5 to 15 basis points. Notably, this adjustment also represents the largest cut in the five-year LPR since its inception in 2019 .

Conversely, one-year LPR, which serves as a barometer for market lending rates, was left unchanged at 3.45%.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0765; (P) 1.0777; (R1) 1.0792; More...

EUR/USD's break of 1.0804 resistance suggests short term bottoming at 1.0694, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for stronger rebound. Sustained above 55 D EMA (now at 1.0833) will argue that fall from 1.1138 has completed and target this resistance. Meanwhile, rejection by 55 D EMA, followed by break of 1.0694, will resume the fall from 1.1138 to 1.0447 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 01:15 | CNY | PBoC 1Y Loan Prime Rate | 3.45% | 3.45% | 3.45% | |

| 01:15 | CNY | PBoC 5Y Loan Prime Rate | 3.95% | 4.10% | 4.20% | |

| 07:00 | CHF | Trade Balance (CHF) Jan | 4.74B | 2.35B | 1.25B | 1.27B |

| 09:00 | EUR | Eurozone Current Account (EUR) Dec | 31.9B | 20.3B | 24.6B | 22.5B |

| 13:30 | CAD | CPI M/M Jan | 0.00% | 0.40% | -0.30% | |

| 13:30 | CAD | CPI Y/Y Jan | 2.90% | 3.30% | 3.40% | |

| 13:30 | CAD | CPI Median Y/Y Jan | 3.30% | 3.60% | 3.60% | |

| 13:30 | CAD | CPI Trimmed Y/Y Jan | 3.40% | 3.60% | 3.70% | |

| 13:30 | CAD | CPI Common Y/Y Jan | 3.40% | 3.80% | 3.90% |

Canada’s CPI slows to 2.9% yoy in Jan, ex-gasoline down to 3.2%

Canada's CPI slowed from 3.4% yoy to 2.9% yoy in January, much lower than expectation of 3.3% yoy. The largest contributor to headline deceleration was lower year-over-year prices for gasoline (-4.0%). Excluding gasoline, CPI also fell from 3.5% yoy to 3.2% yoy. Food prices growth also fell from 4.7% yoy to 3.4% yoy. On a monthly basis, the CPI was unchanged, following a -0.3% mom decline in December.

Looking at the core measures, CPI median fell from 3.5% yoy to 3.3% yoy, below expectation of 3.6% yoy. CPI trimmed fell from 3.7% yoy to 3.4% yoy, below expectation of 3.6% yoy. CPI common fell from 3.9% yoy to 3.4% yoy, below expectation of 3.8% yoy.

BoE Bailey: Market’s rate cut outlook not unreasonable, yet unendorsed

In a session with the Treasury Select Committee today, BoE Governor Andrew Bailey acknowledged that It's "not unreasonable" for the market to think about reductions in interest rates this year

However, he was quick to qualify this by stating that MPC "do not endorse the market curve" forecasting such cuts, adding that "we are not making a prediction of when or by how much" BoE cuts interest rates.

Bailey pointed to "encouraging signs" in key economic indicators, but stressed the importance of "sustained progress" in tackling inflation.

Addressing recent data indicating the UK's entry into a technical recession in the latter half of the previous year, Bailey downplayed its impact, describing the downturn as "very weak" and pointing to "distinct signs of an upturn."

Australian Dollar Shrugs after RBA Minutes, China Rate Cut

The Australian dollar continues to rally and has extended its gains for a fifth successive day. In the European session, AUD/USD is trading at 0.6550, up 0.19%.

Minutes: RBA considered raising rates

The minutes of the RBA’s February meeting were released earlier today. At the meeting, there RBA maintained the cash rate at 4.35%, as expected. The minutes indicated that some members supporting raising interest rates by a quarter-point. This was due to a concern about sticky inflation.

The RBA has raised rates only once since June, which has led to the markets pricing in rate cuts later this year. The RBA has pushed back against these expectations as inflation is running at 4.1%, well above the 1-3% target band. The central bank expects the inflation battle to be a long one, projecting that inflation will only fall back to 3% in mid-2025 and 2% by 2026.

At the February meeting, the RBA warned that it was prepared to raise rates. The minutes noted that the central bank expects the economy to continue to cool and it is prepared to lower rates if economic activity falls more than expected.

The minutes indicated that there is significant uncertainty over the economic outlook and the direction of inflation. Given this backdrop, the RBA has been forced to send mixed messages to the markets, stating that rate cuts and rate hikes both remain on the table. What will likely determine which direction the RBA eventually takes will be dependent on key data, such as the wage price index which will be released on Wednesday.

China cuts 5-year LPR

In a surprise move, the People’s Bank of China cut the five-year loan prime rate by a quarter point to 3.95%, the largest rate cut since 2019. Lower rates should translate into a reduction in mortgage rates for homeowners and support the troubled property sector. Still, the move is not considered a game-changer for the Chinese economy and the Australian dollar isn’t showing much of a response.

AUD/USD Technical

- AUD/USD put pressure on support at 0.6506 earlier. Next, there is support at 0.6468

- 0.6570 and 0.6608 are the next resistance lines

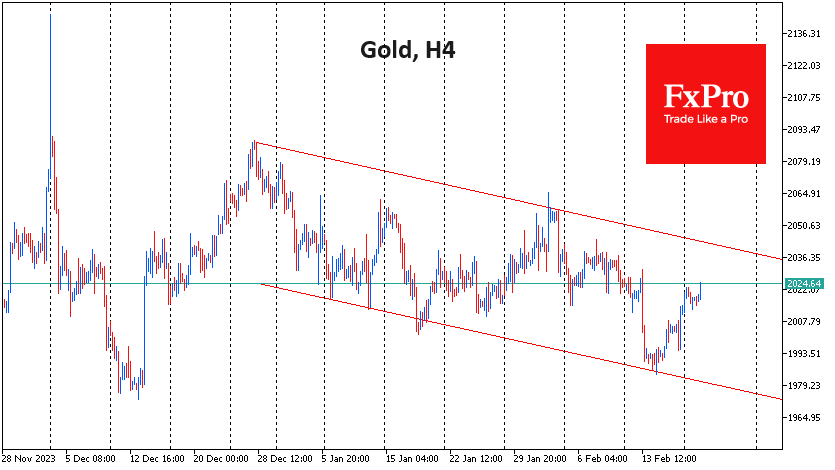

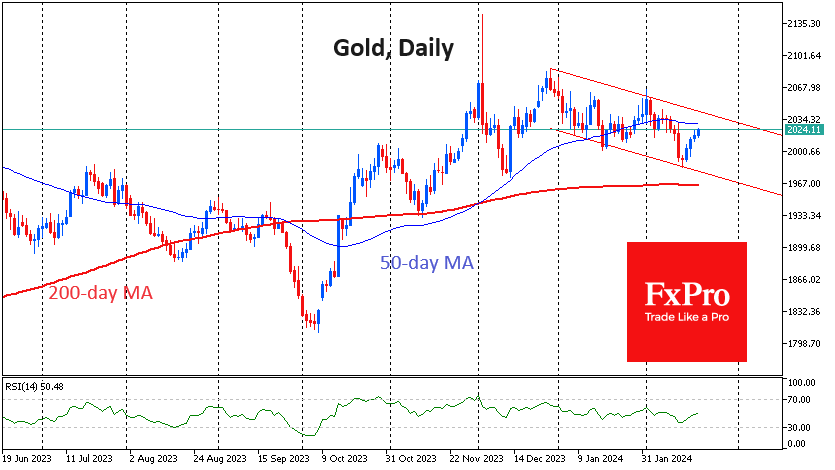

Gold Rises But Within a Downward Channel

Gold rallied for the fourth consecutive session to reach $2023, recovering almost all the losses suffered the week before on the back of the inflation report. Gold’s ability to rally suggests continued domestic demand, as some investors are clearly rushing to buy back any losses.

At the same time, however, we note that since the beginning of the year, gold has been characterised by solid selloffs on the news, forming a smooth downtrend. In the context of this downtrend, a rise to $2040-2045, which is the upper boundary of the bearish range, looks quite acceptable.

The area around $2035 – the highs of two weeks ago – also appears to be a crucial intermediate level. Confident buying from this level would be the first important signal that the recent correction is over and that gold is ready to make a fresh assault on the highs.

Much more important, however, will be the behaviour of gold as it approaches the $2050 level, where the reversal of the decline in late January took place. Consolidation at this level would confirm the breakdown of the downtrend and set the stage for a move towards $2100 and the subsequent renewal of historic highs.

However, as long as gold is trading within the downtrend, there is a greater chance of a breakdown or even an acceleration of the downtrend.

Among the fundamental factors, the potential for growth could be provided by the fall in the dollar if Fed officials show a softening of their position, bringing the start of interest rate cuts closer.

On the bearish side, equities could come under pressure following the optimistic rally in the tech giants and the news of a sharp slowdown in economic activity. We also do not rule out the possibility that the recent support measures for the Chinese stock market and property sector will cool demand for gold as a safe-haven for investors from that part of the world.

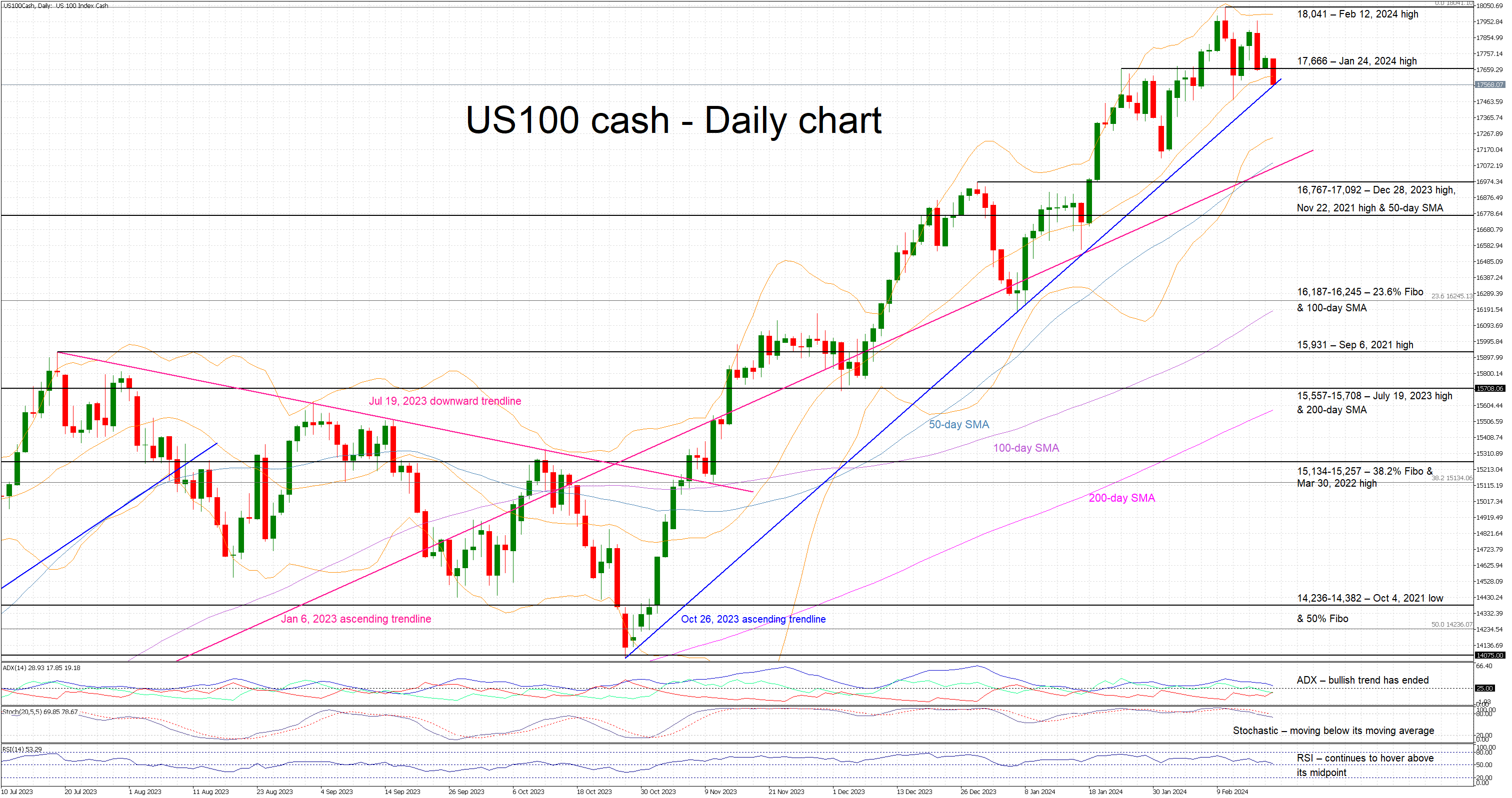

Is the US 100 Cash Index Close to a Correction?

- US 100 index is in red today, testing the support set by a key trendline

- It remains a tad below its all-time high as the market looks for new bullish catalysts

- Stochastic oscillator is trying to send a bearish message

The US 100 cash index is lower today, testing the support set by the October 26, 2023 ascending trendline but remaining very close to its February 12, 2024 high of 18,041. The journey higher has almost been a straight line, raising questions on the soundness of this upleg and potentially opening the door for a sizeable correction if the bears manage to take over control of the US 100 index.

Such a possibility is not really that far-fetched considering the current stance of the momentum indicators. More specifically, the stochastic oscillator has broken below both its moving average and overbought territory. Should this move pick up pace, it could be seen as a strong bearish signal. Additionally, the RSI could be possibly preparing for a decent break below its 50-midpoint for the first time in 2024. Interestingly, the Average Directional Movement Index (ADX) has not yet made up its mind, as it continues its downward move towards its 25-threshold.

Should the bulls remain confident, they could try to protect their gains and gradually lead the US 100 index above the January 24, 2024 high at 17,666. If successful, they could have the chance to test the February 12, 2024 high at 18,041 and then record a new all-time high, with the 18,500 level being their next likely target.

On the flip side, the bears are trying to retake the market reins. They could try to push the US 100 index below the October 26, 2023 trendline and then, provided that they overcome the January 6, 2023 trendline, the bears could stage a correction towards the busy 16,767-17,092 area. This is populated by the December 28, 2023 high, the November 22, 2021 high and the 50-day simple moving average (SMA), and it is expected to prove a strong support area.

To sum up, the US 100 cash index is in the red today as the bears are pinning their hopes on the momentum indicators signalling a much-delayed correction.

ECB wage growth data: A glimpse of hope but no trigger for immediate rate cuts

ECB released data today indicating a slight decrease in negotiated wage growth to 4.46% in Q4, marking a downturn from the previous quarter's record high of 4.69%. This development, though modest, is likely to be greeted positively by ECB policymakers, signaling a potential onset of wage growth deceleration anticipated throughout the year.

Despite the reduction, the magnitude of the drop is not substantial enough to prompt ECB to consider an immediate rate cut in March. The data presents a cautious optimism rather than a clear-cut rationale for policy easing. If ECB's more hawkish members advocate for further evidence of wage growth deceleration, preferring to wait for the next wage data release in May, the likelihood shifts towards a rate cut in June, rather than April, as the more plausible timeline for monetary policy adjustment.

EUR/USD bounces further in European session and the break of 1.0804 resistance argues that a short term bottom was formed at 1.0694, on bullish convergence condition in 4H MACD. Further rebound is now in favor to 55 D EMA (now at 1.0832). Sustained break there will argue that whole fall from 1.1138 has completed and bring stronger rally back to this resistance.

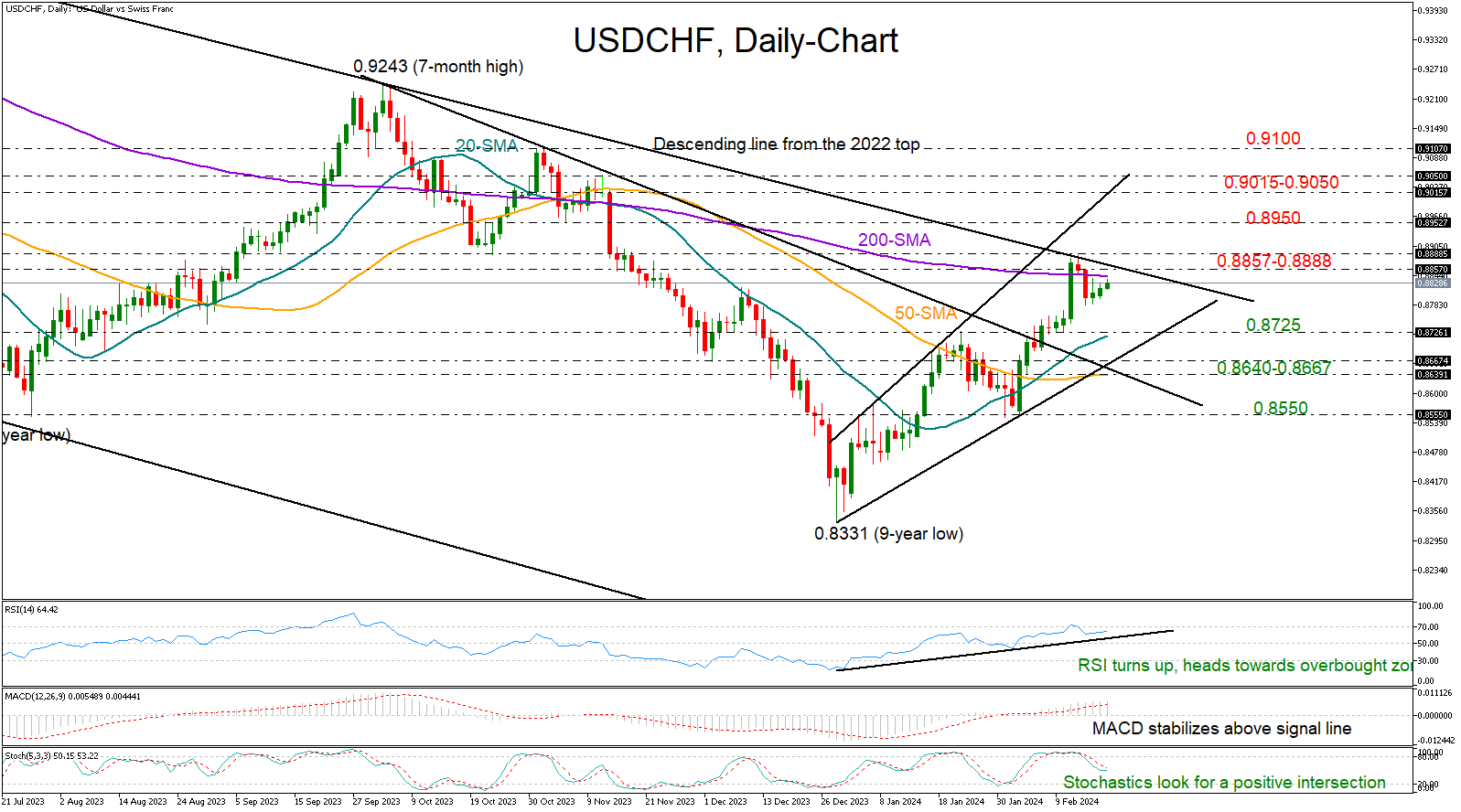

USDCHF Regains Some Power, But Still at Risk

- USDCHF gets rejected near familiar resistance

- Short-term bias remains positive but probably too weak

USDCHF has been in the green almost every week since the plunge to a nine-year low of 0.8331 at the end of December, but the bullish wave was not strong enough to overcome the descending trendline from the 2022 top last week.

The bulls, however, have not totally abandoned the battle. They are currently trying to recoup their latest pullback to stage another fight within the 0.8857-0.8888 area.

From a technical perspective, the short-term bias is still skewed to the upside as the RSI is comfortably above its 50 neutral mark, though the indicator is also a short distance below its 70 overbought level, suggesting that upside pressures might fade soon.

A solid move above the 0.8888 bar could encourage a rally towards the 0.8950 constraining zone. Running higher, the pair may attempt to pierce through the resistance line at 0.9015 and climb the 0.9050 barrier with scope to reach October’s obstacle near the 0.9100 psychological level.

In the event the pair faces another failure near its 200-day simple moving average (SMA) and the 0.8860 region, sellers could enter the market with force, sinking the price towards its 20-day SMA at 0.8725 and January’s high. Slightly lower, the trendline zone of 0.8640-0.8667 may protect the market from a potential slump to 0.8550.

All in all, USDCHF has been on an uptrend so far this year, but its short-term outlook remains fragile as a long-term barrier is still a threat at 0.8888.