Sample Category Title

USD/JPY Holds Steady As Crypto Market Rallies

Key Highlights

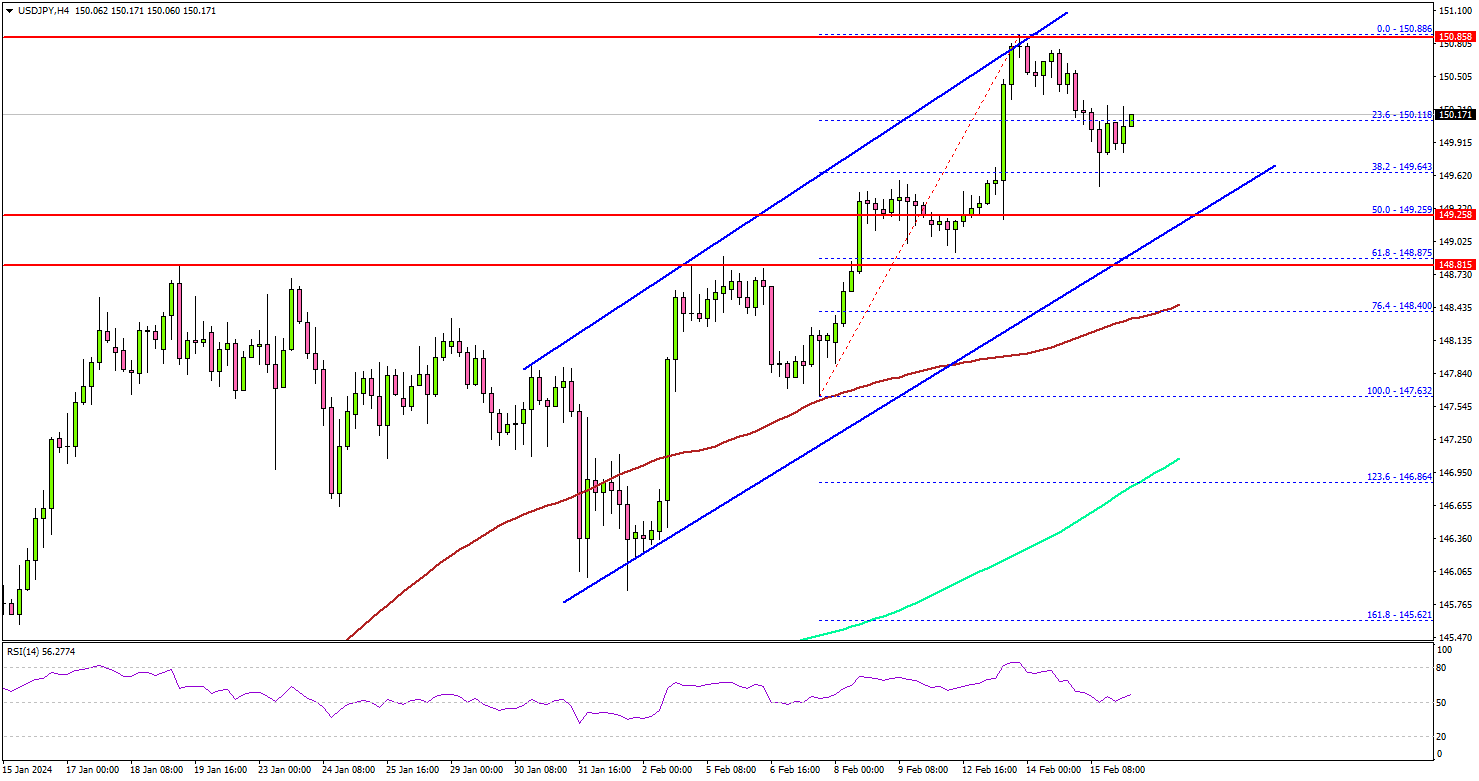

- USD/JPY started a downside correction from the 150.80 resistance.

- A major rising channel is forming with support at 149.25 on the 4-hour chart.

- Gold price dived below $2,000 before it started a recovery wave.

- Bitcoin price extended its rally above the $52,200 resistance.

USD/JPY Technical Analysis

The US Dollar remained in a positive zone above 148.00 against the Japanese Yen. USD/JPY accelerated higher and even broke the 150.00 level before the bears appeared.

Looking at the 4-hour chart, the pair traded as high as 150.88 before there was a pullback. The pair declined below the 150.20 level. There was a spike toward the 38.2% Fib retracement level of the upward move from the 147.63 swing low to the 150.88 high.

Immediate support is near the 149.65 level. The first major support sits near the 149.25 level. There is also a major rising channel forming with support at 149.25 on the same chart. The channel is close to the 50% Fib retracement level of the upward move from the 147.63 swing low to the 150.88 high.

The next major support sits at 148.40, below which the pair might gain bearish momentum. In the stated case, the pair could even revisit the 146.80 support level.

On the upside, the bulls are facing hurdles near the 150.50 level. The next key resistance is near the 150.80 zone. A close above the 150.80 zone could open the doors for more upsides. The next stop for the bulls might be 151.50. Any more gains might send USD/JPY toward 152.00.

Looking at Bitcoin, the bulls remained in action and pumped the price above $52,200. Ethereum, Solana, and other altcoins also extended gains.

Economic Releases

- US Producer Price Index for Jan 2024 (MoM) – Forecast 0.1%, versus -0.2% previous.

- US Producer Price Index for Jan 2024 (YoY) – Forecast +0.6%, versus +1.0% previous.

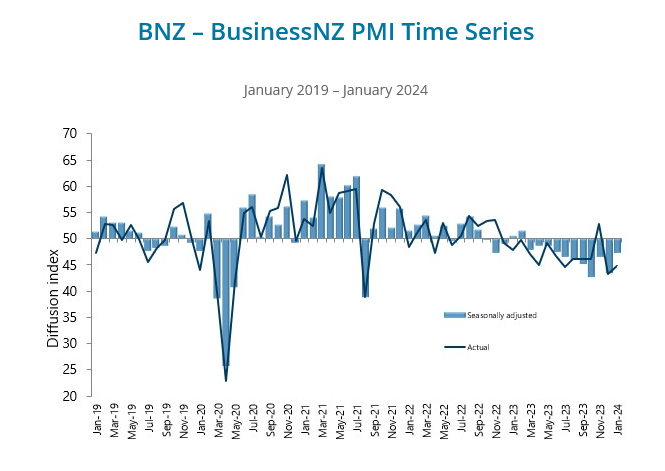

NZ BNZ manufacturing rises to 47.3, still someway off to expansion

New Zealand BusinessNZ Performance of Manufacturing Index rose from 43.4 to 47.3 in January, hitting the highest level since June last year. Despite this uptick, it's important to note that the manufacturing sector remained in contraction for eleven straight months.

BusinessNZ's Director of Advocacy, Catherine Beard noted that while there are signs of improvement, "the sector is still someway off returning to expansion."

Looking at some details, production rose from 40.5 to 42.1. Employment rose from 47.0 to 51.3. New orders rose from 44.0 to 47.7. Finished stocks rose from 45.9 to 47.3. Deliveries rose from 43.7 to 49.3.

However, the persistence of negative sentiment among businesses cannot be overlooked. The proportion of negative comments in January rose to 63.2%, up from 61% in December and 58.7% in November, reflecting concerns over seasonal factors such as holiday disruptions and a sustained lack of demand or orders.

RBNZ’s Orr stresses continued effort needed to anchor inflation expectations

In a forum today, RBNZ Governor Adrian Orr indicated that the central bank's primary challenge lies in firmly anchoring inflation expectations around the 2% target, a goal that remains elusive despite significant progress.

This "tail end" of the inflation fight, as Orr describes, requires meticulous attention to both "capacity pressures" within the economy and the public's "inflation expectation"s.

"We've got more work to do to have inflation expectations truly anchored at that 2% level, he added.

"We observe headline but we are targeting in a large sense core inflation," Orr stated, emphasizing the importance of these metrics in shaping the central bank's policy decisions.

Fed’s Bostic: Robust economy allows for unhurried monetary easing without oppressive urgency

Atlanta Fed President Raphael Bostic noted there has been "substantial and gratifying progress" in reducing inflation's pace, but he warns against premature celebrations.

While inflation is expected to continue to decline, it would be "more slowly than the pace implied by where the markets signal monetary policy should be," Bostic said in a speech overnight.

With a "strong labor market and macroeconomy," Bostic highlighted the opportunity to deliberate policy shifts "without oppressive urgency".

ECB’s Scicluna: March could be it for rate cut

In an interview, ECB Governing Council member Edward Scicluna pointed to March economic projections as a crucial factor that could justify a shift in policy, opening the door for rate cuts. "March could be it," he suggested, "We'll see how many think that there's no need to wait for June."

Acknowledging the "bumpy" path toward achieving ECB's disinflation objectives, Scicluna emphasized the clear trend of declining inflation. "You should see the writing on the wall and admit objectively that the trend is going down," he stated.

Despite the possibility of justifying a hold on rate cuts due to various concerns, including geopolitical tensions, Scicluna argued for a more direct approach: "You have to make a judgment; you don't find these excuses."

"Let's face reality — of course, risks are flying all around us," he said. "But when you get a comprehensive look at things, prices are falling."

"At a time when demand is falling, I believe you can let off the pedal a bit," Scicluna said.

BoE’s Mann focuses on forward-looking indicators after last year’s soft patch

BoE MPC Catherine Mann commented overnight on the -0.3% quarterly contraction in GDP for Q4 2023. She characterized this period as a "soft patch," adding that the downturn was anticipated and aligned with her expectations.

Rather than dwelling on past performance, Mann is directing her attention to forward-looking indicators, such as business surveys and PMIs, along with BoE's Decision Maker Panel. "Those are all looking good," she said.

However, Mann voiced ongoing concerns regarding the persistence of services price inflation in the UK, which she believes is more tenacious than in other advanced economies.

She added that decline in goods price inflation alone would not suffice to sustainably anchor consumer price inflation to the Bank's 2% target.

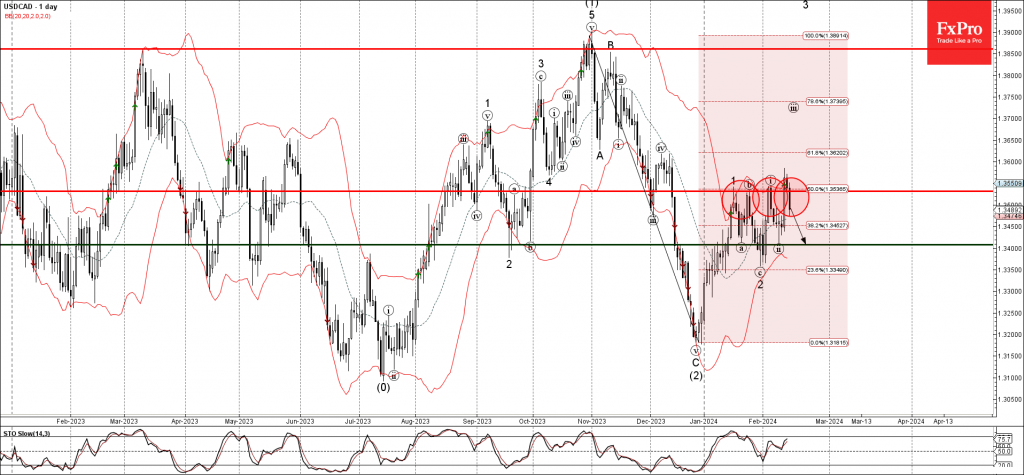

USDCAD Wave Analysis

- USDCAD reversed from resistance level 1.3530

- Likely to fall to support level 1.3400

USDCAD currency pair recently reversed down from the key resistance level 1.3530 (which has been reversing the price from the middle of January), intersecting with the upper daily Bollinger Band and the 50% Fibonacci correction of the downward ABC correction (2) from the start of November.

The downward reversal from the resistance level 1.3530 stopped the previous impulse waves 3 and (3).

Given the strength of the resistance level 1.3530, USDCAD currency pair can be expected to fall further to the next support level 1.3400.

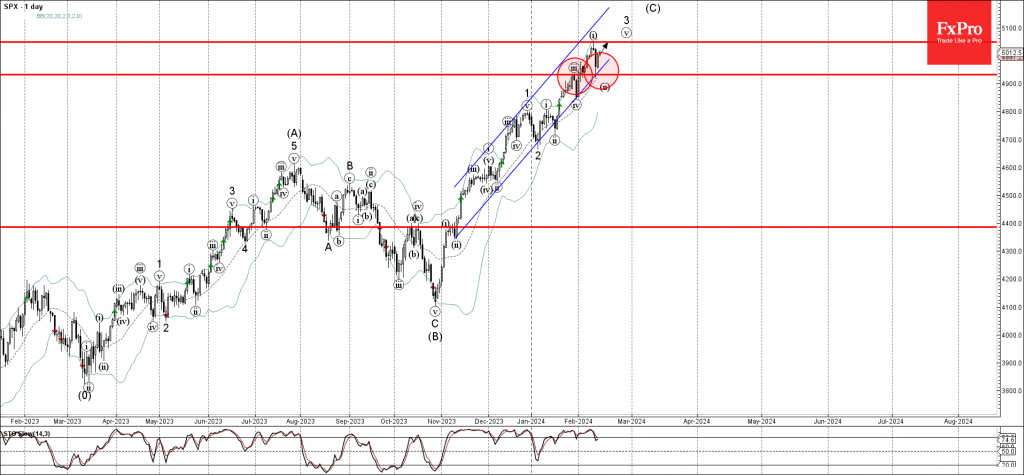

S&P 500 Wave Analysis

- S&P 500 reversed from support level 4930.00

- Likely to rise to resistance level 5050.00

S&P 500 index recently reversed up from the support level 4930.00 (former support from the end of January), intersecting with the 20-day moving average and the support trendline of the daily up channel from November.

The upward reversal from the support level 1.3530 stopped the previous minor correction (ii).

Given the clear daily uptrend, S&P 500 index can be expected to rise further to the next resistance level 5050.00.

Sunset Market Commentary

Markets

The slew of eco data from the US came in mixed. February regional sentiment indicators including the Empire Manufacturing index and the Philly Fed business outlook were better than expected. Details showed improvement across almost all subseries, including 6-month forward looking gauges. We note the price gauges re-emerging. Weekly jobless claims also joined the consensus-beating side with 212k vs 220k. But US headline retail sales fell 0.8% m/m, more than the -0.2% expected. 9 out of the 13 categories posted decreases, led by building material stores and auto dealers. All core gauges fell short of the +0.2% consensus as well, with the control group (used for private consumption GDP calculations) dropping by 0.4% m/m. While the numbers may have been impacted by harsh winter weather, they dominated the market reaction. Yields were down about 1.5 bps prior to the release. Current changes vary between 4.3 (30-y) and 5.8 (5-y) bps but trade off intraday lows. German yields shrugged off the additional declines caused by US spillovers, limiting daily losses to <2 bps. Appearing before the European Parliament today, ECB’s Lagarde warned against hasty action. She suggested that it could put inflation back on the rise and force the ECB into the brakes again. Lagarde highlighted salaries as “an increasingly important driver of inflation dynamics in the coming quarters.”, adding that services inflation has shown signs of persistence. Her comments came hours before the Commission released updated economic forecasts. It slashed its 2024 GDP growth prognosis from 0.8% to just 0.5% as the economy entered the year on a weaker footing than expected. The forecast for next year was marginally revised down to 1.5%. Inflation is seen easing to 2.7% in 2024 and 2.2% in 2025.

A weaker dollar is the name of the game on FX markets. DXY slips to 104.35. Including yesterday’s move, about two-thirds of Tuesday’s CPI gain is wiped out. EUR/USD extended earlier gains after the releases to change hands in the 1.078 region (1.072 at the open). Sterling joined the Anglo-Saxon trend lower after this morning’s weaker-than-expected Q4 GDP numbers (including weak details). A two-day rally lifts EUR/GBP from the recent lows around 0.85 towards 0.856 currently. UK money markets added to rate cutting bets, even as BoE policymaker Greene said she wanted to see more evidence that inflation is less embedded than previously feared before considering to loosen policy. Greene at the latest meeting called for a stable policy rate after pushing for hikes in the ones before.News & Views

Czech inflation rose less than expected in January, by 1.5% M/M (vs 2% consensus). The usual repricing at the start of the year was thus less stronger than feared. Annual inflation fell from 6.9 Y/Y to 2.3% Y/Y, significantly beating analyst estimates (2.9%) and the Czech National Bank’s assumption (3%). The fade-out of the statistical effect of the energy savings tariff contributed to the sharp slowdown in annual inflation. Administered prices (6% Y/Y instead of 8.4% Y/Y expected by CNB), core inflation (2.9% Y/Y vs 3.8% Y/Y) and monetary policy-relevant inflation (2.2% Y/Y vs 3% Y/Y) all improved much more than hoped for. It prompted an exceptional statement by CNB governor Michl, lauding CNB staff for restoring price stability. He calls it a partial success though as the CNB needs to stay hawkish. The weakening koruna and public finance deficit are upside risks to inflation, arguing for lowering interest rates cautiously and for being able to halt the rate reduction process at any time. Michl also warns that rates will be higher than what has been the case over the last ten years or more as the CNB discusses the option of a need for higher (neutral) rates. The Czech koruna immediately lost ground after the CPI print with EUR/CZK touching 25.50 for the first time since March 2022. The pair reversed course after the Michl statement (CZK-reference unlike after last week’s CNB meeting) towards 25.40. CZK swap yields lose 8 to 15 bps across the curve, the front end outperforming.

Polish inflation accelerated less than feared as well, but the deviation from consensus was much smaller than in the Czech Republic. CPI rose by 0.4% M/M in January (vs 0.5% forecast) with Y/Y-inflation falling from 6.2% to 3.9% (vs 4.1%). Details showed amongst others dwelling prices rising by 0.8% M/M and only transport (-2.8% M/M) and fuel prices (-2.3% M/M) contributing negatively. Polish swap rates lose over 7 bps across the curve, but the biggest part of the move already occurred ahead of the CPI release. Comments by NBP Kotecki might be at play. Unlike NBP governor Glapinski, he thinks that there will be room for a slight Polish rate cut in H2 2024. The Polish zloty stands its ground at EUR/PLN 4.34.