Sample Category Title

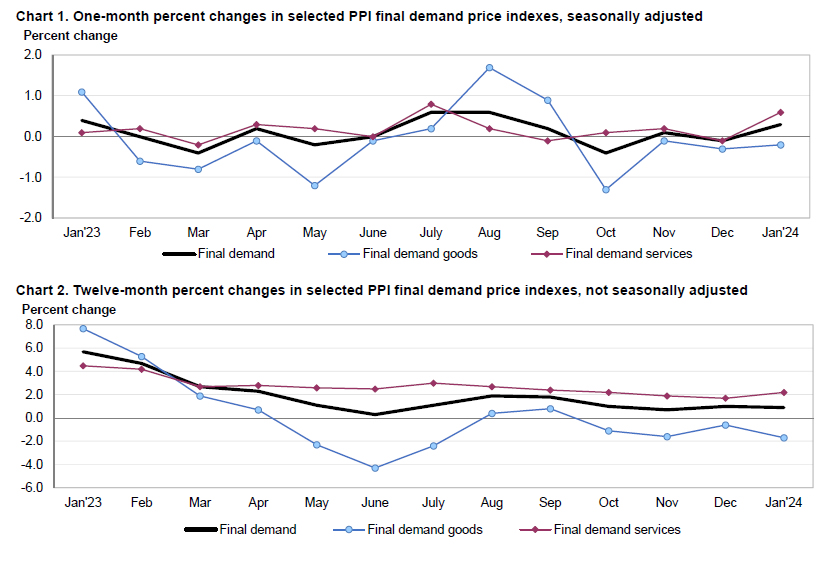

US PPI up 0.3% mom, 0.9% yoy in Jan

US PPI rose 0.3% mom in January above expectation of 0.1% mom. PPI goods declined -0.2% mom while PPI services rose 0.6% mom. PPI less foods, energy, and trade services rose 0.6% mom, the largest advance since January 2023.

For the 12-month period, PPI slowed from 1.0% yoy to 0.9% yoy, above expectation of 0.7% yoy. PPI less foods, energy, and trade services was unchanged at 2.6% yoy.

ECB’s Schnabel warns of premature policy ease amid wage-driven inflation pressures

In a speech today, ECB Executive Board member Isabel Schnabel noted the role of "persistently low, and recently even negative, productivity growth" in exacerbating the inflationary pressures from the current strong growth in nominal wages.

She pointed out that this scenario increases the likelihood of firms passing higher wage costs onto consumers, thus "delaying inflation returning to our 2% target."

With the backdrop of a prolonged period of high inflation, Schnabel argued for the necessity of maintaining restrictive monetary policy stance until there is clear confidence that inflation will sustainably return to ECB's medium-term objective.

She warned against premature policy adjustments, suggesting that to avoid a "stop-and-go policy" reminiscent of the 1970s, a cautious approach is essential.

"We must be cautious not to adjust our policy stance prematurely," she said.

GBP/USD Yawns as UK Retail Sales Soar

The British pound has edged lower on Friday. In the European session, GBP/USD is trading at 1.2578, down 0.17%.

UK retail sales rebound with 3.4% gain

UK retail sales were more than impressive, surging 3.4% m/m in January. This crushed the market estimate of 1.5% and followed a 3.3% decline in December. The reading was the largest monthly gain since April 2021. The sharp gain was driven by increased sales of food and fuel. On an annualized basis, retail sales rebounded with a 0.7% gain, compared to a 2.4% decline in December and well above the market estimate of -1.4%.

Will the real UK economy please stand up?

Traders can be forgiven for scratching their head after the latest retail sales report, which points to consumers spending with gusto. Just a day earlier, the markets were digesting the news that the UK economy had entered a recession late in 2024, after recording back-to-back quarters of negative growth. GDP fell 0.3% in the fourth quarter and 0.1% in the third quarter. What gives?

The answer could well be that the UK economy, although hurting, may be turning a corner. The sharp rise in interest rates has cooled down the economy and lowered inflation dramatically, but this effect appears to be fading fast. The “R” word (recession) may be making headlines but it is a shallow recession and the economy could quickly return to growth mode with some decent economic data.

The Bank of England meets on March 21th and will try to make sense of where the UK economy is headed. The BoE has kept rates unchanged since August and there is pressure on the central bank to provide some relief to households and businesses and lower rates. At the same time, inflation remains sticky and the BoE is determined to stamp out high inflation and bring it closer to the 2% target before it lowers rates.

GBP/USD Technical

- GBP/USD is testing support at 1.2597. Below, there is support at 1.2550

- There is resistance at 1.2676 and 1.2723

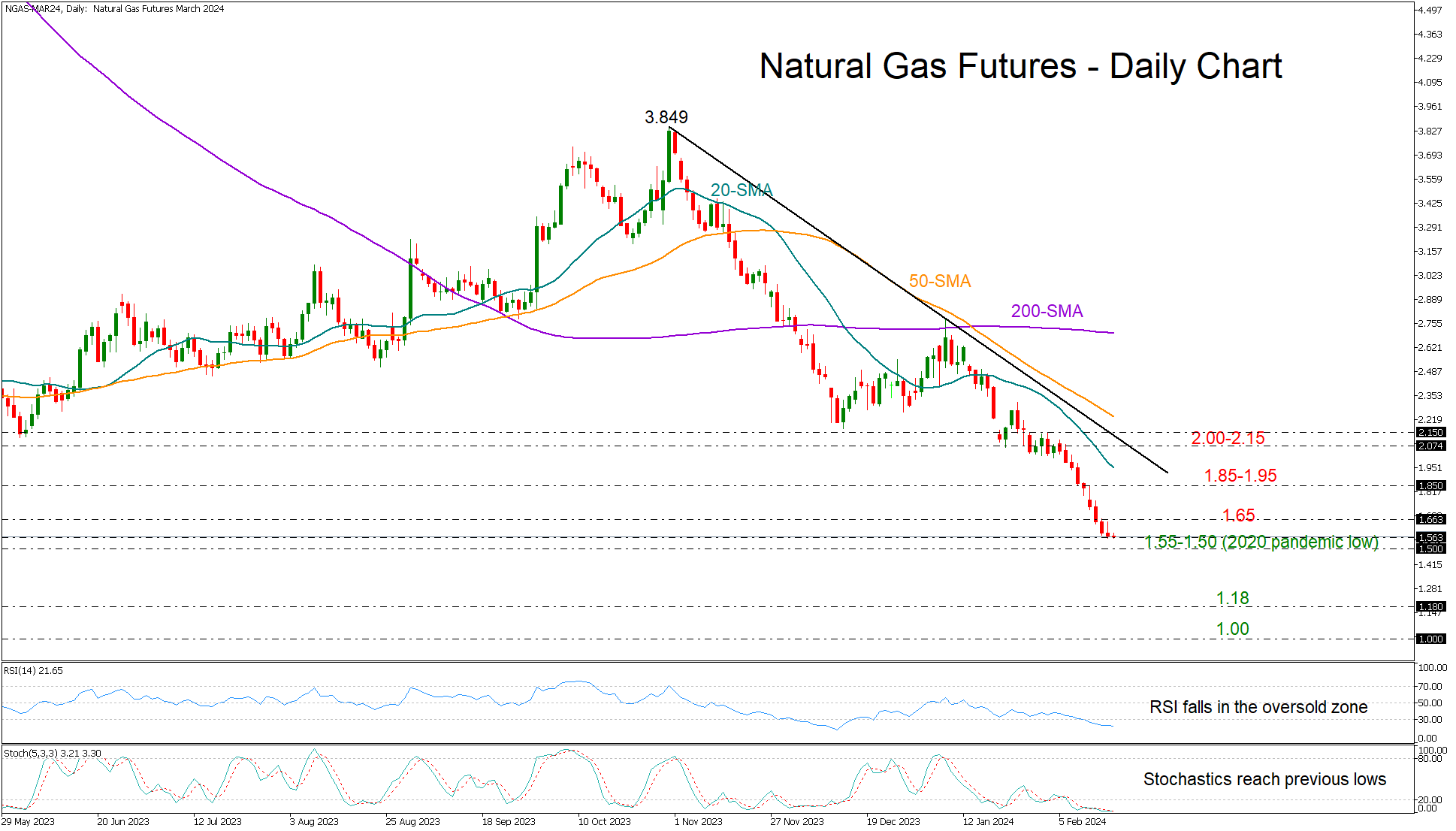

Natural Gas Dives to Pandemic Lows; Near-Term Oversold

- Natural gas futures reach pandemic lows

- Oversold signals present; confirmation above 1.65

Natural gas futures (March delivery) experienced another painful week, plummeting towards the pandemic floor of 1.50, which halted the 2014-2016 downtrend too.

The RSI and the stochastics have detected oversold conditions, while Thursday’s candlestick, which seems to have the shape of an inverse hammer, is adding to the optimism that the price could soon change direction to the upside.

Yet, a clear extension below the 1.50 threshold could cancel this bullish scenario, activating a new bearish wave towards the 1.18 level, which coincides with the 261.8% Fibonacci extension of the December-January upleg. Failure to pivot there could bring the case of parity under the spotlight.

Should selling forces fade out, the price may reverse up to test the nearby resistance zone of 1.65. A break higher would validate the bullish hammer candlestick pattern, bolstering buying appetite towards the 1.85 territory. A steeper increase above the 20-day simple moving average (SMA) and the 2.00 round level might provide direct access to the tentative resistance trendline from November’s high at 2.07. However, buyers may not gain confidence unless the recovery continues sustainably above the 2023 constraining region, around 2.16.

In short, natural gas futures have been sold aggressively, reaching attractive levels for a bullish reversal. For that to happen, though, the price will have to set a strong foothold within the 1.50 area.

Altcoins Temporarily Benefit from Bitcoin’s Pause

Market picture

The cryptocurrency market is up 1.7% from 24 hours ago, with Bitcoin stuck between $51.5K and $52.5K. Buying interest has focused on the major altcoins such as BNB (+3.6%), XRP (+3.5%) and Cardano (+4%), which were lagging the day before, but they are just trying to keep up with Bitcoin’s rise. In our opinion, altcoins’ time will come when the first cryptocurrency has reached its historic highs and looks too expensive. But it could be another year before that happens.

Moreover, history suggests the market will pick new altcoins with each new growth cycle. The stars of the past era don’t always manage to rewrite their all-time highs, so there’s no rush to pick altcoins at this stage of the cycle.

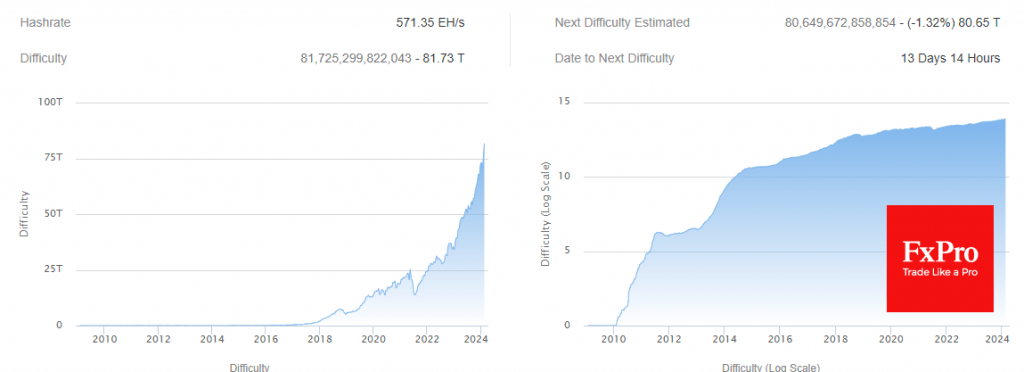

As a result of another recalculation, the difficulty of mining the first cryptocurrency increased by 8.24%. The indicator updated the historical maximum at 81.7 T. The average hashrate for the period since the previous change in value was 583.92 EH/s.

News background

According to data compiled by Bloomberg, outflows from gold ETFs since the beginning of 2024 have reached $2.39 billion, while inflows into spot bitcoin ETFs have reached $3.89 billion.

According to CoinGecko data, the US has captured 83% of the global spot bitcoin ETF market, worth over $41.7 billion, with Europe in second place with an 8.8% share. Canada, which approved spot bitcoin ETFs back in 2021, remains a major player in the segment with a 7.4% share.

In total, there are 33 such Bitcoin ETFs in the world. The first appeared in Europe in 2020. The largest by assets is the Grayscale Bitcoin Trust ETF (GBTC), which has been operating as a trust since 2014. The fund’s AUM is $22.8 billion (54.7% of the total).

Tron Foundation founder Justin Sun announced plans to develop a Tron-based L2 network to scale Bitcoin. The roadmap includes the integration of a cross-chain solution to link the tokens of the two ecosystems.

GameFi project WormFare partnered with Polygon Game Studio to improve game performance and security.

China will revise provisions of its outdated anti-money laundering law to prevent the use of crypto assets to launder criminal proceeds.

JPY Under Pressure. Technical Analysis of USDJPY, EURJPY, and AUDJPY

Fundamental Scenario of the Yen

The Japanese yen was the worst-performing currency this week, falling by 0.6% and trading near a three-month low.

Recent preliminary GDP data for the fourth quarter of Japan show a warning of a fall into a technical recession, something that will be confirmed after next month's final release, preventing the Bank of Japan from starting the expected cycle of monetary tightening, or interest rate hikes this year. This scenario has prompted yen sales against its counterparts.

However, the Japanese currency's major losses were limited by anticipation of possible government intervention in the foreign exchange markets, as weakness above the $150 level has prompted government intervention in the past.

Next, we will present the technical analysis and suggested levels for various yen crosses.

USDJPY

Sell Zone: 150.575 // Buy Zone: 149.26

Situation and general trend:

The pair maintains a bullish macro and intraday trend with the last resistance at 150.88 and the last relevant support coinciding with the weekly open at 149.20. This implies that as long as this support is not broken, further upside movement is expected with the breakout of the indicated resistance.

Bearish Scenario:

After the bullish opening of the day, the price is expected to extend the ascent towards Wednesday's uncovered POC* at 150.575, with an expected bearish reaction towards 150.00, the support at 149.57, and the next buying zone around the weekly open at 149.20, from where buying is expected to resume, considering that the bulls will defend their previous positions.

The RSI in negative territory and the descending vertical volume on price rises reflect a more bearish intraday momentum.

Bullish Scenario:

The decisive breakout (with candle bodies) of Wednesday's POC at 150.57 will extend intraday purchases towards the bullish average range at 150.91, implying further upside potential for the next week with attention to the following resistances and uncovered POCs between 151.27 and 151.69.

*Uncovered POC: POC = Point of Control: It is the level or zone where the highest volume concentration occurred. If a bearish movement occurs from it, it is considered a selling zone. If a bullish impulse occurs, it is considered a buying zone.

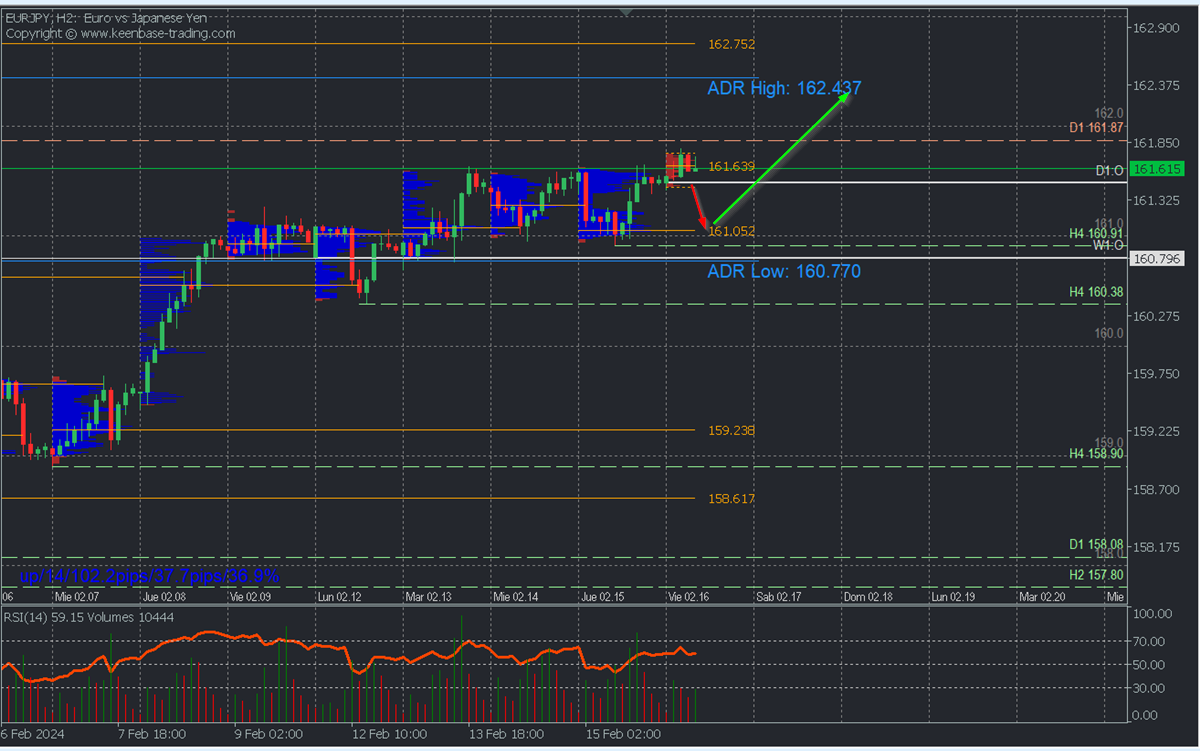

EURJPY

Sell Zone: 162.75 and 161.63 // Buy Zone: 161.05

Situation and general trend:

It seems to have regained bullish strength after the December decline. It faces the January resistance at 161.86, a decisive breakout of which will extend purchases towards 163.00, as long as quotes remain above 161.00, very close to yesterday's uncovered POC at 161.05.

Corrective Bearish Scenario:

Sales below 161.63 with a target in the intraday buying zone of 161.00 with an expected rebound as a reaction.

Bullish Scenario:

Buying above 161.00 (wait for a pullback to this zone) with a target at the resistance breakout of 161.87 and the daily bullish average range at 162.43, with an expected extension towards the selling zone at 162.75.

*Uncovered POC: POC = Point of Control: It is the level or zone where the highest volume concentration occurred. If a bearish movement occurs from it, it is considered a selling zone. If a bullish impulse occurs, it is considered a buying zone.

AUDJPY

AUDJPY

Sell Zone: 98.13 // Buy Zone: 97.78 and 97.47

Situation and general trend:

Bullish and surpassing the resistances of January and December, so further upside extension is expected to decisively surpass the September 2022 and November 2023 resistances, especially after the intraday correction. A scenario that will remain valid as long as the last relevant support at 97.31 is not decisively broken.

Corrective Bearish Scenario:

Sales below 98.13 with a target at 97.78 and 97.47 on extension, from where consider purchases.

Bullish Scenario:

Buying above 97.47 (wait for a pullback to this zone) with targets at the bullish average range at 98.33 and the surpassing of the September 2022 and November 2023 resistances at 98.56.

*Uncovered POC: POC = Point of Control: It is the level or zone where the highest volume concentration occurred. If a bearish movement occurs from it, it is considered a selling zone. If a bullish impulse occurs, it is considered a buying zone.

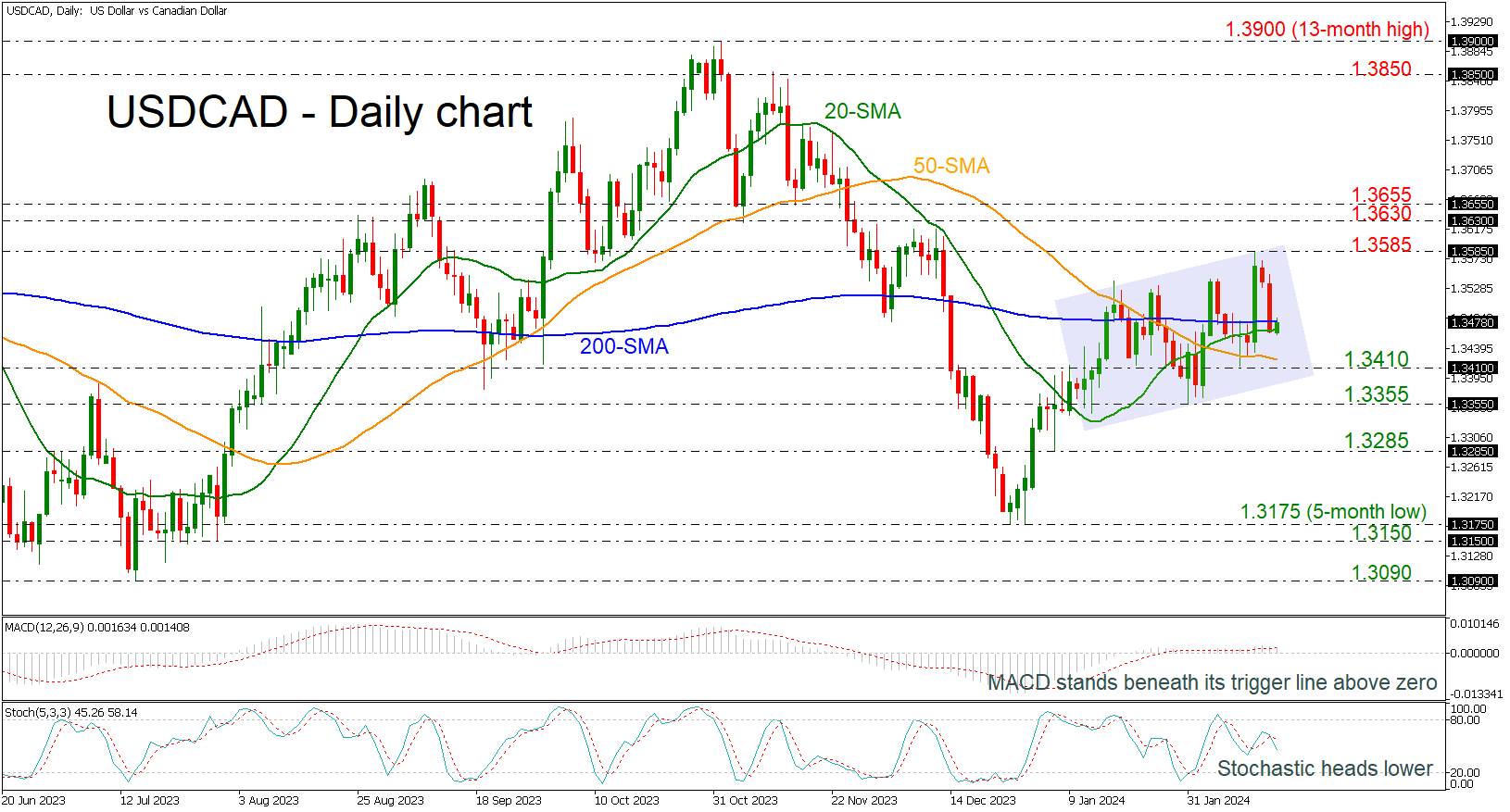

USDCAD Retains Upside Pressure in Ascending Channel

- USDCAD starts a battle with 200-day SMA

- However, MACD and stochastic suggest bearish retracement

USDCAD has been recouping some losses after the strong bearish movement in the preceding two sessions but is currently finding strong resistance near the 200-day simple moving average (SMA) at 1.3480. The pair has been developing within an upward sloping channel over the last month.

Technically, the MACD oscillator is heading beneath its trigger line but is still holding above its zero level. Also, the stochastic are moving lower after the bearish crossover within its %K and %D lines.

If the price could edge higher and break the 200-day SMA to the upside, it could revisit the 1.3585 resistance level. Piercing though that wall, the pair may challenge the 1.3630-1.3655 resistance zone.

On the flipside, should the pair reverse lower, immediate support could be found at the 50-day SMA at 1.3420 ahead of the 1.3410 support. A move below that region could trigger a retreat towards the 1.3355 support. In case of a downside violation, the bears may then attack the 1.3285 barricade, which held strong in the beginning of the year.

In brief, USDCAD retains a bullish tone despite the signs in the technical oscillators. Can the pair extend its advance or are we heading for a reversal?

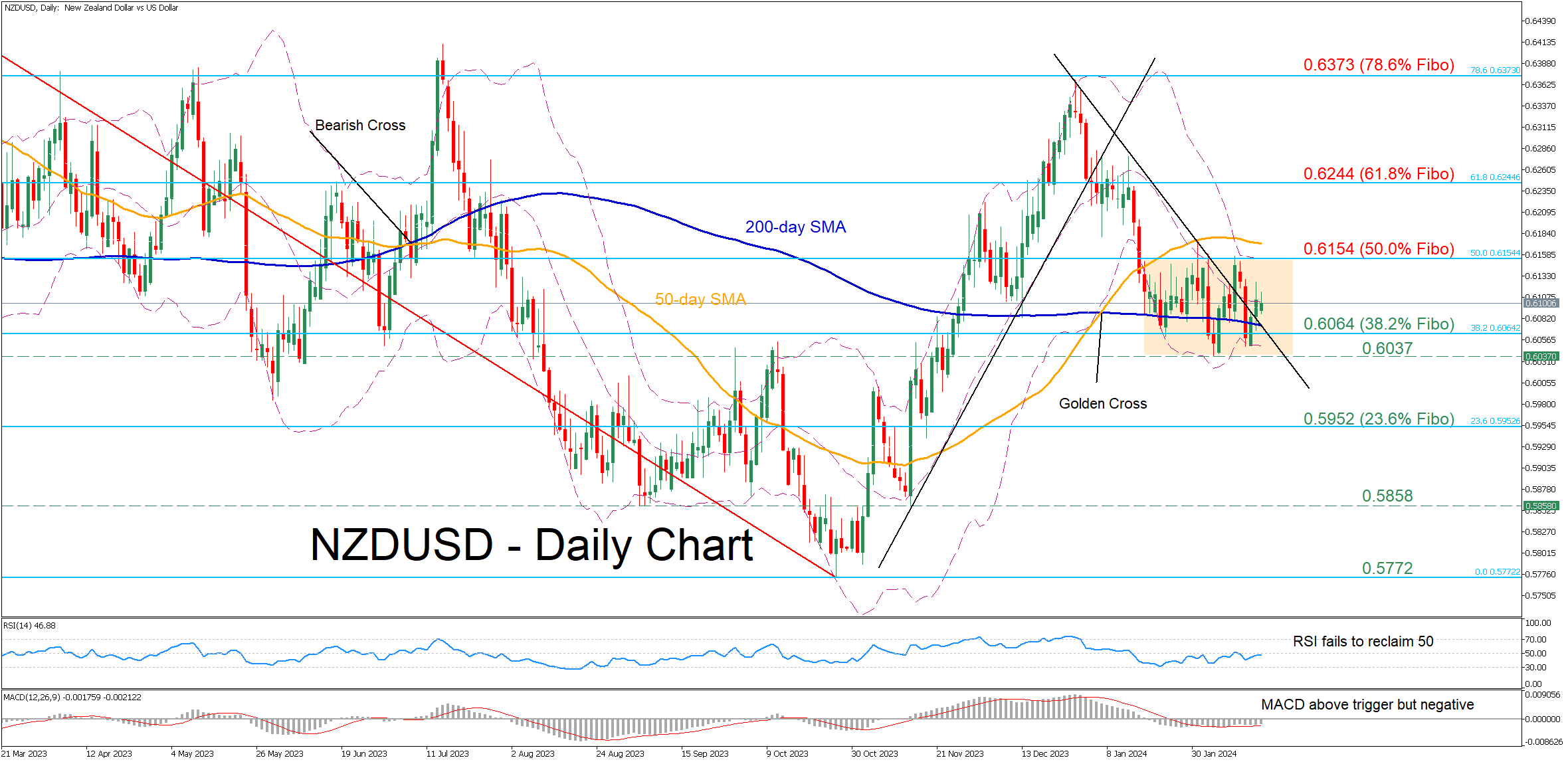

NZDUSD Stuck in a Rectangle Pattern

- NZDUSD claims 200-day SMA and descending trendline

- But the pair fails to rally, extending sideways move

- Oscillators improve but remain in negative territories

NZDUSD entered a downtrend after getting rejected at the 78.6% Fibonacci retracement of the 0.6536-0.5772 downleg in December. However, the pair has adopted a rangebound pattern around the 200-day simple moving average (SMA) since mid-January, while the latest jump above it has failed to trigger a strong advance.

Given that both the RSI and MACD are within their negative zones, the price might drop again below the 200-day SMA and challenge the 38.2% Fibo of 0.6064. Diving beneath that floor, the pair could descend towards the recent two-month bottom of 0.6037. A violation of that region could set the stage for the 23.6% Fibo of 0.5952.

On the flipside, should the recovery resume, immediate resistance could be found at the 50.0% Fibo of 0.6154. Further advances could then cease around the 61.8% Fibo of 0.6244. Piercing through that hurdle, the price might test the 78.6% Fibo of 0.6373, a region that capped the pair's advance in December.

Overall, despite the break above both the 200-day SMA and the downward sloping trendline, NZDUSD continues to hover within its rangebound structure. Hence, in the case that the rebound resumes, the focus will shift on the 50.0% Fibo of 0.6154.

Nikkei 225 Technical: Eyeing Potential New All-Time High

- Nikkei 225 has continued its bullish momentum despite a technical recession in the Japanese economy.

- Current price action is just 0.9% away from its 38,957 all-time high printed in December 1989.

- Medium-term momentum is overbought but no clear signs of bullish trend exhaustion.

- Watch the 38,260 key short-term support.

Since our last analysis, the Nikkei 225 has staged a rally of +13% to print a current intraday high of 38,865 at this time of the writing, a whisker away from its all-time high of 38,957 printed around 34 years ago in December 1989.

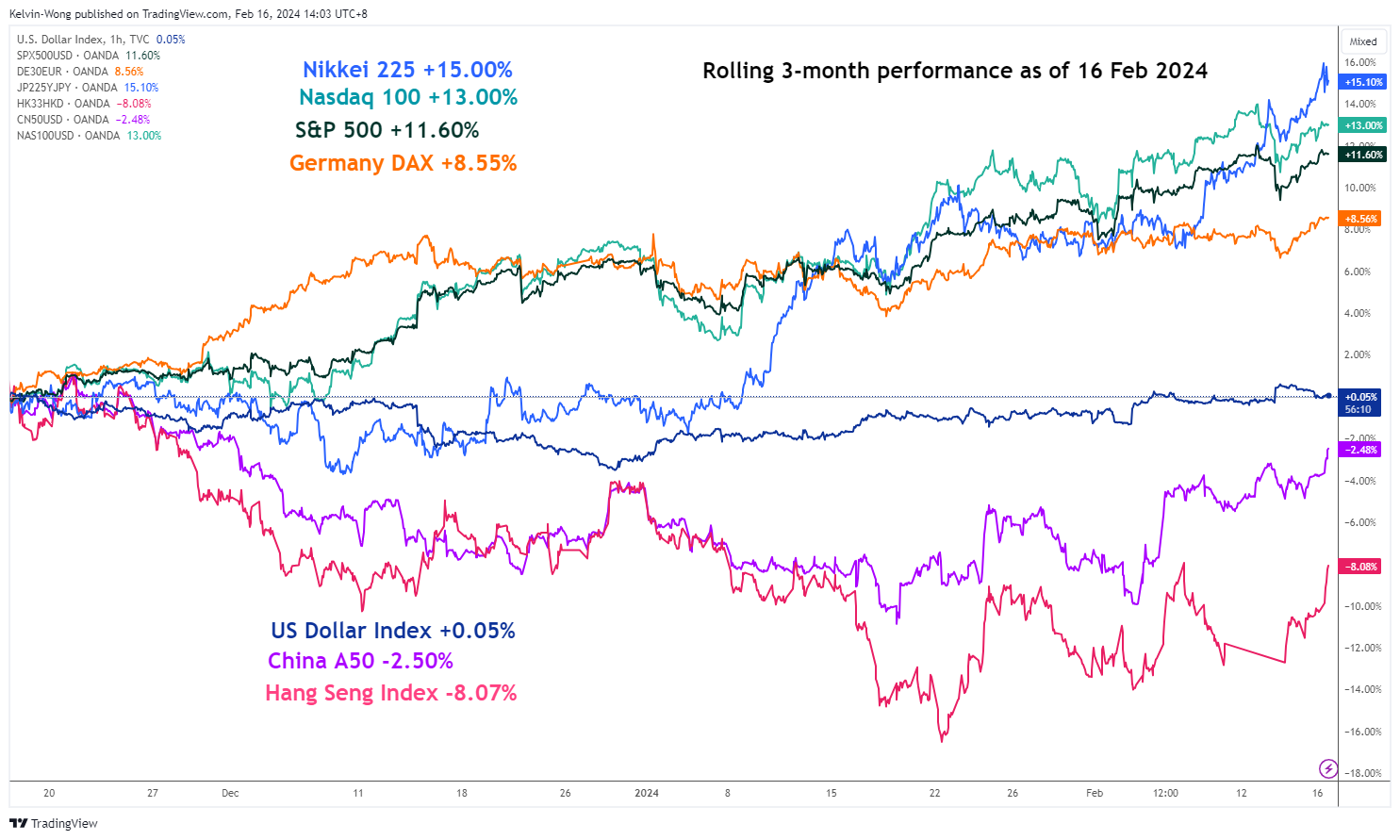

Outperformance of Nikkei 225 over Nasdaq 100

Fig 1: 3-month rolling performance of Nikkei 225 & other major stock indices as of 16 Feb 2024 (Source: TradingView, click to enlarge chart)

Also, on a three-month rolling performance measurement basis as of 16 February 2024, the Nikkei 225 has outperformed the heavily concentrated technology and artificial intelligence-focused Nasdaq 100 marginally (15% vs. 13%) (see Fig 1).

The impulsive upmove sequence remains intact

Fig 2: Nikkei 225 major & medium-term trends as of 16 Feb 2024 (Source: TradingView, click to enlarge chart)

Fig 3: Japan 225 short-term trend as of 16 Feb 2024 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the major uptrend phase of the Nikkei 225 remains intact as its price actions staged a bullish acceleration on this Tuesday, 13 February via the clearance above its former upper boundary of its ascending channel projected from the start of January 2023.

The recent upward acceleration has led to a current overbought reading level of 77 in the daily RSI momentum indicator. However, no bearish divergence condition has been flashed out yet and it is still below its prior significant peak of 84 printed on 23 May 2023.

These observations suggest that medium-term upside momentum is likely to be intact. A clearance above the current all-time high level of 38,957 is likely to see the next medium-term resistance coming in at 40,500/41,000 (the upper boundary of a major ascending channel projected from March 2020 low & a Fibonacci extension cluster level).

In a shorter time horizon, as inferred from the hourly chart of the Japan 225 Index (a proxy of the Nikkei 225 futures), the hourly RSI momentum indicator has remained above a key parallel ascending support after a slide from its overbought condition seen in today’s Asian session.

In addition, the hourly RSI has also managed to shape a “higher low” above the 50 level which suggests that the current minor short-term impulsive upmove sequence of the ongoing minor uptrend phase in place since the 7 February 2024 low remains intact.

Watch the 38,260 short-term pivotal support with the next intermediate resistances coming in at 39,120 and 39,510/600 (the upper boundary of the minor ascending channel & a Fibonacci extension cluster level).

However, failure to hold at 38,260 negates the bullish tone for a minor corrective decline to expose the next intermediate support at 37,570 (the pull-back of the former ascending channel resistance projected from the 3 January 2023 low), and below it sees the risk of a further slide towards the next support at 36,880 (also the upward sloping 20-day moving average).

US Data Wraps Up This Week

In focus today

In the US, the University of Michigan's preliminary consumer survey (including inflation expectations) and January producer prices figures (PPI) are due for release in the afternoon. Following the strong CPI earlier this week, markets will be very attentive to any additional signs of inflationary pressures building up.

In Sweden, the LFS survey is released this morning. We focus on employment and hours worked data. Recently, employment has been flat while hours worked recovered by year-end. We expect these positive tendencies to continue rather than deteriorate.

Economic and market news

What happened overnight?

In Japan, BoJ Governor Ueda stated that the central bank will consider adjusting monetary policy when stable achievement of its inflation target comes into sight. Ueda suggested that even without negative rates, monetary policy will remain accommodative.

What happened yesterday?

In the US, retail sales came in significantly lower than expected at -0.8% m/m (cons: -0.2%). However, one-offs such as winter storms distorted the print, making the drop less dramatic. Initial claims continued to surprise on the downside, declining by 8,000, while the NAHB (construction PMI) increased to 48 in February, posting the third consecutive monthly gain. Finally, the regional manufacturing indicators from New York Fed (Empire) and Philadelphia Fed ('Philly-Fed') came in stronger than expected in January, providing further indications that the industrial cycle is now turning towards a recovery phase.

In the UK, GDP edged down in Q4, printing -0.3% q/q (cons: -0.1%). Following the Q3 print of -0.1%, the UK economy is in a technical recession amid two consecutive GDP contractions.

In the euro area, the European Commission revised its economic forecasts, now projecting GDP growth to be 0.8% instead of 1.2% in 2024, while inflation is expected at 2.7% in 2024 (vs. 3.2% earlier) and 2.2% in 2025 (unchanged). This is close to identical to the latest December staff projection by the ECB. ECB President Lagarde repeated in her public remarks yesterday, that the disinflation process is well underway. However, she also stressed the need for more confirmation before cutting rates, emphasizing that wage growth continues to be strong amid tight labour markets and workers' demands for inflation compensation.

Equities: Global equities were higher yesterday although macro data was not overwhelming. We saw broad-based gains, but small caps outperformed together with what we could call the three odd ones; REITs, banks and utilities. Hence, adding this all up the message from investors was that goldilocks continues. Or, put differently, the too hot CPI data from Tuesday and the too weak retail sales data from yesterday should not persist. One thing worth noting is that small caps outperformed substantially yesterday and have outperformed large cap by 1% the last 5 trading days despite the sell-off on Tuesday, higher yields, and the upside surprise in US CPI data. In US yesterday, Dow +0.9%, S&P 500 +0.6%, Nasdaq +0.3%, Russell 2000 +2.5%. The strong market sentiment continues across Asia this morning with Chinese H-shares leading the advances. European futures are higher while US futures are mixed.

FI: Long-end EGBs rose early in yesterday's session, but the rally faded in the second half of the day. 10Y Bund yields ended up by a couple of basis points, while peripheral bonds fared slightly better. German ASW-spreads tightened with credit spreads in line with the tendency over the past week. US yields reacted somewhat mixed on the string of data out yesterday, rising marginally across the curve throughout the day.

FX: In a relatively calm session yesterday the USD lost further ground with only TWD and IDR performing worse in Majors space. Most other currencies were caught in tight ranges with notably both EUR/NOK and EUR/SEK doing very little. EUR/GBP remains close to the 0.855-threshold while USD/JPY has moved marginally below the important 150-level.