Sample Category Title

Ethereum Price Exceeds $2,800

The last time the ETH/USD price was at this level was in May 2022, which was the start of a massive drop of more than 65% in 1.5 months.

However, now the ETH/USD market is dominated by bullish sentiment, for the following reasons:

→ deployment of the Dencun update on the Ethereum network this month, which will open up new opportunities for users and developers;

→ expectations that this year, following the approval of Bitcoin ETFs, applications for the launch of ETFs on Ethereum will be approved;

→ waiting for a traditional bull market after halving in the Bitcoin network.

So far, the ETH/USD chart shows that the price of Ethereum is moving within an ascending channel that begins in 2023. Moreover, the price is in its upper half — an indication of the strength of demand. If the trend continues, the price of Ethereum could reach $3,000 within a month.

At the same time, the price of Ethereum is approaching the upper border of the channel, which may provide resistance. It is possible that the indicators will indicate that the market is overbought, creating the preconditions for the formation of a correction.

Probable support levels can help the bulls in a scenario where a correction develops:

→ 2,400: this level influenced the price of ETH starting in December 2023;

→ 2,700: former 2024 high, which was broken on a wide bullish candle (a sign of strong demand);

→ median line and lower boundary of the current channel.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*At FXOpen UK and FXOpen AU, Cryptocurrency CFDs are only available for trading by those clients categorised as Professional clients under FCA Rules and Professional clients under ASIC Rules respectively. They are not available for trading by Retail clients.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

European Commission forecasts slower Eurozone growth, but quicker inflation slowdown

According to European Commission's Winter 2024 Economic Forecast, Eurozone's GDP growth for 2024 was revised notably downwards to 0.8% from Autumn's estimate of 1.2%, reflecting a more subdued outlook than previously anticipated. For 2025, GDP growth forecast as slightly downgraded to 1.5% from 1.6%.

Inflation is expected to decelerate more rapidly in 2024, with HICP forecasted at 2.7%, down from prior 3.2%. Meanwhile, inflation forecast for 2025 remains unchanged at 2.2%.

Vice-President Valdis Dombrovskis highlighted that despite the challenges faced in 2023, "rebound should speed up gradually this year and into 2025". Inflation will continue its "broad-based decline" and bolstered consumer demand through real wage growth and a robust labour market.

Commissioner for Economy Paolo Gentiloni acknowledged the "more modest" economic rebound this year. But growth is set to "firm" and inflation to decline to close to ECB's 2% target in 2025.

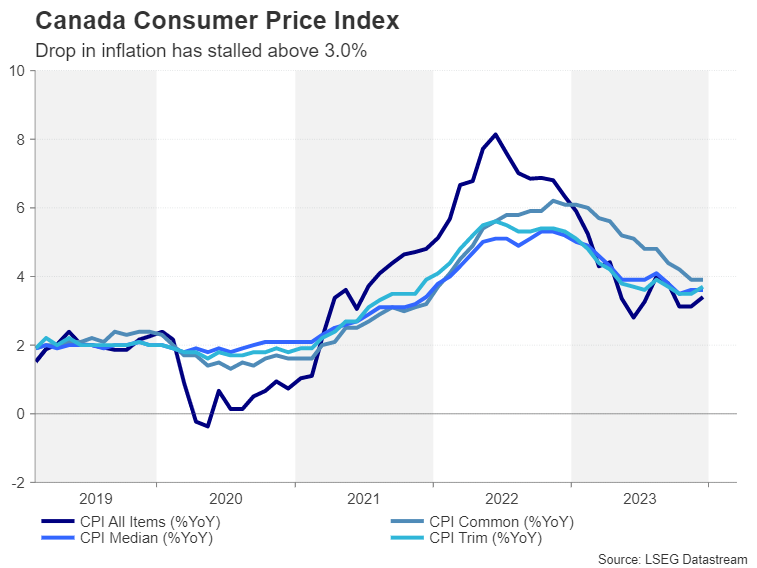

Will Canadian CPI Data Offer Loonie Any Support?

- Inflation in Canada has been stuck above 3.0% since the summer

- The Bank of Canada is keeping rate hike option on the table

- Yet, the loonie has been on the backfoot versus the dollar this year

- Will Tuesday’s CPI data (13:30 GMT) put BoC’s inflation fight back on track?

The long fight to get inflation to target

The Bank of Canada has made great strides in its bid to get inflation back to its 1-3% target band, but as is the case in the United States and other major economies, the progress has stalled lately. The downward trend in both the headline and underlying price metrics in Canada appear to be bottoming out in the 3-4% range.

Nevertheless, the Bank of Canada sees inflationary pressures receding further over the coming months and decided to drop its tightening bias at its January meeting. Although policymakers did not completely rule out the possibility of more hikes either, the shift to a more neutral stance has opened the door to a rate cut later in the year.

Will inflation ease back in January?

The key question now for both the BoC and the markets is the timing. Investors have almost fully priced in a 25-basis-point reduction in July, which represents somewhat of a dialling back from earlier bets that the first cut would come in June. For the timing to be brought forward again, there would have to be a significant change in the inflation outlook. However, it’s unlikely that the January CPI report would alter the picture much.

The annual rate of CPI is expected to have moderated to 3.2% y/y in January after ticking up to 3.4% y/y in December. This probably would not be enough to prompt policymakers to make another dovish turn imminently. Still, if CPI resumes its descent and some or all the core measures also decline, this could encourage investors to up their bets of a rate cut sooner rather than later.

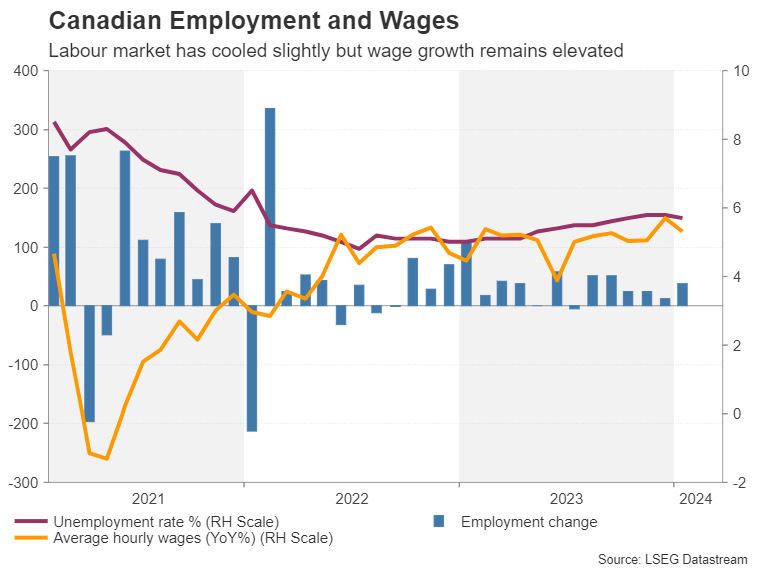

The problem with a strong labour market

In reality, however, the Bank of Canada is in much the same predicament as other central banks like the Federal Reserve and Bank of England where a strong labour market is preventing them from taking a less cautious stance.

Although there’s been a notable cooldown in Canada’s hot jobs market – the unemployment rate has edged up from 4.8% in July 2022 to 5.7% currently – wage growth remains elevated. Average hourly wages were up 5.3% y/y in January, down from 5.7% in December but well above the pre-pandemic average.

Housing market turnaround might not be welcome

However, with economic growth coming to a standstill in the second half of 2023, the risks to the price outlook are tilted to the downside. The one worry is that the housing market emerges out of the doldrums, boosting shelter costs, amid some signs that a turnaround is underway.

Shelter costs are the biggest contributor to keeping inflation above target according to the BoC so policymakers are watching the property sector closely.

Can the loonie stage a rebound?

For the Canadian dollar, which has been battling a resurgence in its US counterpart, weaker-than-expected CPI readings on Tuesday could deliver a further blow.

Dollar/loonie hit a two-month peak of 1.3586 earlier this week, as rate cut expectations for the Fed were further pushed back. Fresh gains for the greenback combined with a selloff in the loonie could push the pair to the November 2023 peak of 1.3899.

However, if Canadian inflation surprises to the upside, dollar/loonie could initially seek support at the 50-day moving average just above the 1.3400 level before heading for the December low of 1.3174.

Beyond all the speculation about rate cuts, the loonie has been unable to reap the benefits of the recent recovery in oil prices, suggesting that US dollar dynamics remain in the driving seat. It also implies that in the event the data points to a more aggressive rate cut path for the BoC, oil prices are likely to offer limited support to the loonie.

JP 225 Index in Sight of Historic Peak

- JP 225 index approaches its 1989 record high

- Bulls might be exhausted as overbought signals detected

Japan’s 225 stock index (cash) marked another green day on Thursday despite GDP figures pointing to a recessionary economy, extending its weekly bull run closer to the 1989 record high of 38,915.

While the upward pattern has shown no cracks so far, the market might be at risk of a downside correction. Specifically, the price could not strengthen its positive momentum above the resistance trendline, which connects the highs from November 2023 and January 2024 at 38,200. The overbought signals coming from the RSI and the stochastic oscillator are adding to the negative risks.

In the event of a pullback, the index could initially retest the 37,770 region ahead of the 37,000 round level. An extension lower could challenge the 20-day simple moving average (SMA) near the tentative support trendline at 36,700. A break lower would dampen market sentiment, likely causing a sharper decline towards the 35,678 floor.

If the bulls stay in charge, the price may attempt to pierce through the critical 38,915-39,000 wall. A successful penetration higher would open a new chapter for the market, bringing the 40,000 number on the radar.

All in all, Japan’s 225 index is in a bullish mode, though whether the bulls have more fuel to extend the ongoing uptrend in the coming days remains to be seen as the price is currently hanging near an important resistance.

GBP/USD – UK in Recession But That’s Unlikely to Sway BoE Yet

- UK GDP -0.3% in Q4 and -0.1% in December

- BoE not concerned about recession

- GBPUSD momentum fading near February lows?

The UK fell into recession in the second half of last year after GDP figures for the fourth quarter showed a steeper contraction than expected.

While a recession was expected ahead of the release, the fourth quarter number was slightly worse despite December performing better than anticipated.

The UK has been flirting with recession for some time but despite the inevitable headlines, today's data doesn't change much. The economy isn't growing, nor has it for the bulk of the last couple of years. It's just on this occasion it's tipped slightly the other way and recorded two small negative quarters of growth.

Not that flat growth is anything to celebrate, of course, but many feared it would be much worse when rates started rising and increased to the level they have. The economy, like those in many other countries, has shown significant resilience and is expected to bounce back this year.

The Bank of England obviously won't be swayed by the technical recession, as Governor Bailey alluded to earlier this week, but weaker household spending may suggest demand isn't as strong as they anticipated. We'll get another update on that tomorrow from the January retail sales figures.

With inflation expected to fall to target in the second quarter, maybe even further after this week's readings, the debate around rate cuts could intensify earlier than they would have otherwise thought. Slower wage growth would obviously help that along greatly.

Losing momentum already?

The pound has been drifting lower against the dollar this week on the back of the data but it's yet to surpass the low from earlier this month.

GBPUSD Daily

Source – OANDA

That's not to say it won't and as we can see on the 4-hour chart below, the correction led to a rebound off the 61.8% Fibonacci retracement level following the topping formation breakout earlier in the month, looks to have been another bearish signal.

GBPUSD 4-Hour

What will be interesting is the momentum indicators as we approach those lows though as they already appear to be softening which could be a red flag.

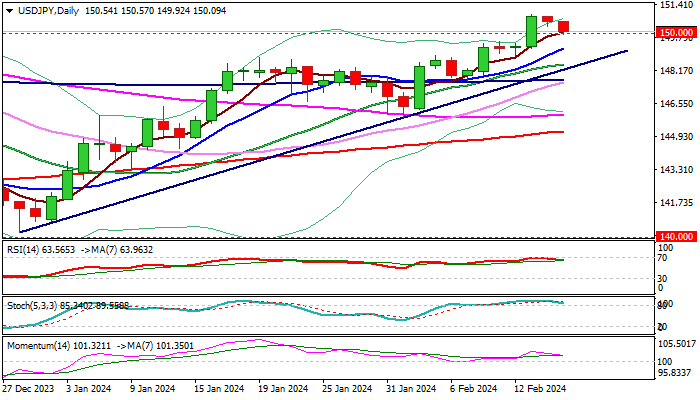

USD/JPY: Correction Likely to be Limited

USDJPY extends pullback from the three-month high (150.88) into second straight day, as traders booked profits after Tuesday’s rally of nearly 1%.

Overbought daily studies contributed to fresh selling, which is expected to push the price lower and offer better levels for new entries into broader bullish market.

Correction is likely to be limited as larger bulls remain fully in play, with initial support at 150 being cracked and guarding rising 10DMA (149.24) and extended dips to find ground above the bull-trendline (148.43) to mark a healthy correction and keep bulls in play for push towards key barrier at 151.90 (2023 high, posted on Nov 13).

Weekly close above psychological 150 level, will be the first one since early November and expected to boost existing bullish outlook.

Res: 150.88; 151.00; 151.43; 151.90.

Sup: 150.00; 149.24; 148.80; 148.43.

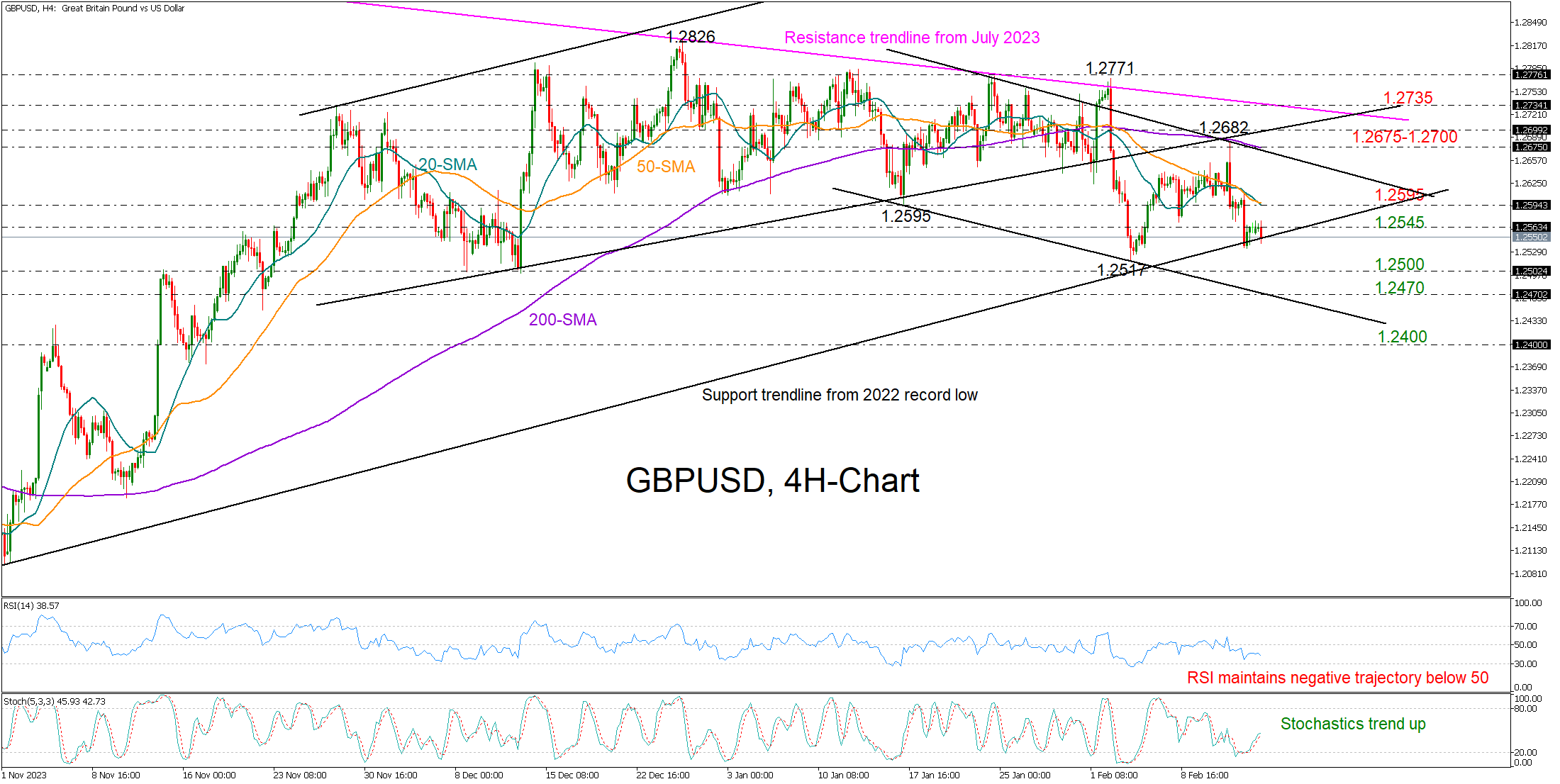

GBPUSD Edges Down as UK Slips into Mild Recession

- GBPUSD holds above key support trendline despite disappointing UK GDP data

- Short-term trend deteriorates, but confirmation needed below 1.2500

GBPUSD remained squeezed between the 1.2563 resistance and the key support trendline from the 2022 record low in the four-hour chart despite the UK economy falling into a mild technical recession in Q4 2023.

The market trend is leaning on the downside as the price has already printed a lower low at 1.2517 and a lower high at 1.2682. On the other hand, the technical indicators are sending mixed signals, with the RSI maintaining its negative trajectory below its 50 neutral mark and the stochastic oscillator sloping upwards.

If the price closes below 1.2550 in the coming hours, sellers could next target the 1.2500 round level. A break lower would confirm a negative trend reversal, pressing the price towards the lower boundary of the short-term bearish channel at 1.2470. If the decline continues from there, the door will open for the 1.2400 mark.

On the upside, a step above 1.2563 could immediately halt near the 20- and 50-period simple moving averages (SMAs) at 1.2595. Should the bulls jump that wall, the pair could accelerate towards the 200-period SMA at 1.2675, while an extension above the broken ascending trendline from mid-December could face a test around the critical 2023-2024 resistance trendline at 1.2735.

In summary, GBPUSD is maintaining a cloudy outlook in the short-term picture, with sellers awaiting a clear misstep below 1.2550 to press the price lower.

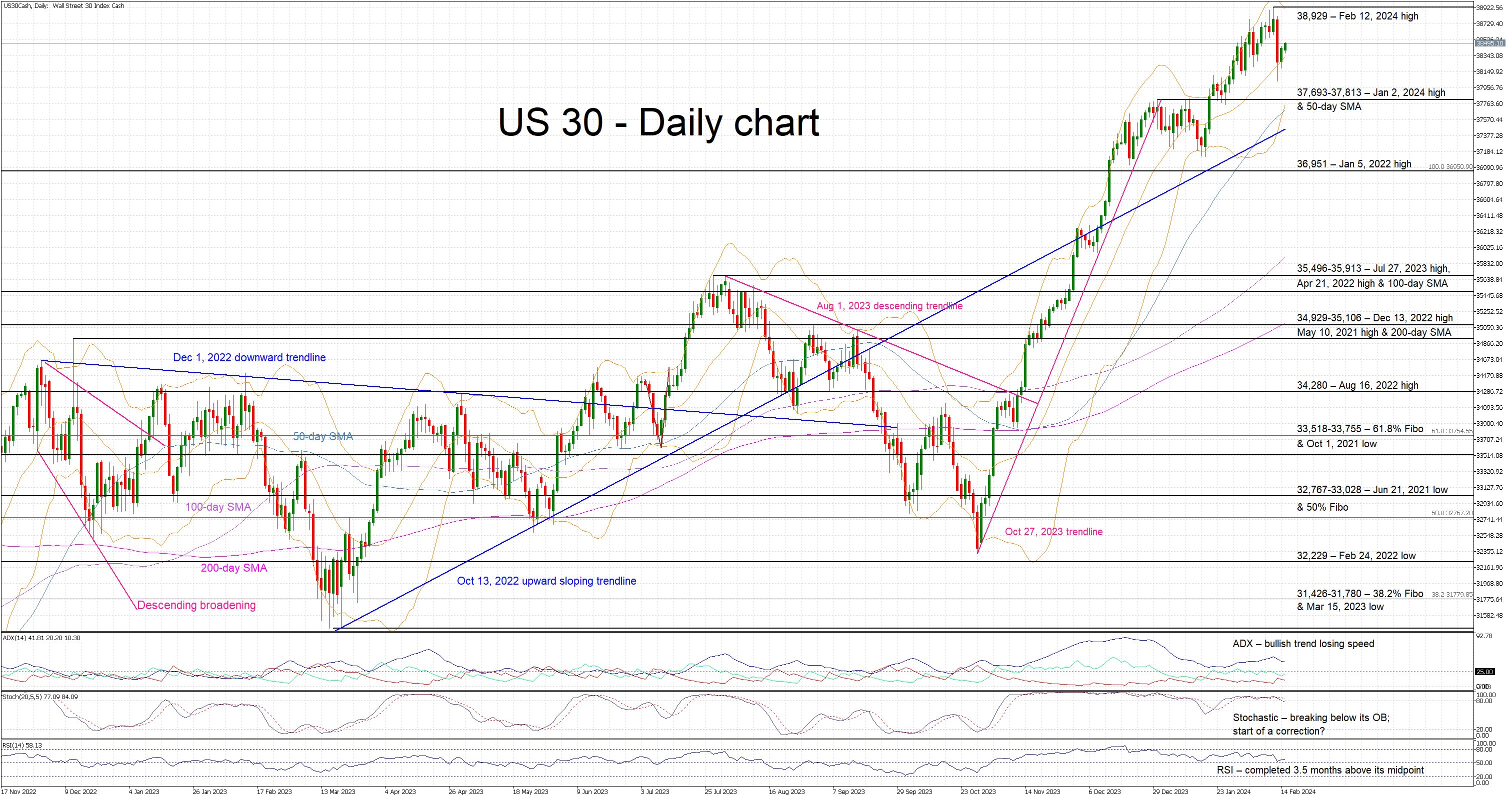

Is a Correction Around the Corner for US 30 Cash Index?

- US 30 index in the green again, after Tuesday’s decent correction

- It remains a tad below its all-time high but bulls might start to worry

- Momentum indicators mixed; all eyes on the stochastic oscillator

The US 30 cash index is in the green again today, reacting to Tuesday’s sizeable red candle that slightly unnerved the bulls. The index remains a tad below its February 13, 2024 high at 38,929 but it is evident that the market is questioning its direction following an almost straight-line rally. The US 30 index is currently 19% higher than the October 27, 2023 trough.

In the meantime, certain momentum indicators could be on the verge of sending bearish signals. More specifically, the Average Directional Movement Index (ADX) is edging lower with the DI+ subcomponent remaining stuck below the 25-midpoint. Similarly, the stochastic oscillator has broken below its overbought (OB) area, and it is trying to widen the gap from its moving average. Should this move pick up speed, it could be seen as a strong bearish signal. On the other hand, the RSI has completed three months above its 50-midpoint and is thus revealing the ongoing bullish pressure.

Should the bulls ignore the mixed signals, they could try to regain market control and lead the US 30 index towards the February 12, 2024 high at 38,929. If they manage to overcome this area, they could then stage a much stronger rally with the 40,000 level possibly being the next key target.

On the flip side, the bears are trying to recapture the market reins and gradually push the US 30 index towards the 37,693-37,813 range, which is populated by the January 2, 2024 high and the 50-day simple moving average (SMA). The bears could then aim for the next support area at 36,951 provided they manage to overcome the long-term October 13, 2022 upward sloping trendline.

To sum up, the US 30 cash index bulls are still enjoying their hard-earned gains but Tuesday’s strong red candle and some early bearish signs from the momentum indicators could gradually turn the table in favour of the bears.

AUD/USD Price Reaction to Labour Market News Provides Important Information for Analysis

Australia's unemployment rate rose to a two-year high of 4.1% in January, while employment was little changed although analysts had expected around 25,000 new jobs, data released this morning showed.

It is believed that weak labour market data should prompt central bank officials to ease monetary policy, which is currently aimed at fighting inflation. According to Trading Economics, the Reserve Bank of Australia is expected to cut interest rates by about 40 basis points this year.

The first reaction to the news was the weakening of the Australian dollar (counting on the easing of the Central Bank's policy), but by the opening of the European session, the price of AUD/USD had recovered a significant part of the decline, which provides important food for thought.

The AUD/USD chart shows that the price is within a downward trend (shown by the red channel), however, there are a number of signs that the bearish pressure has exhausted. The fact that the AUD/USD price is showing some recovery after the initial negative reaction to the unemployment news is one such sign.

It should also be noted that:

→ the median line of the descending channel now acts as support;

→ MACD moved into the green zone;

→ the price was unable to consolidate below the level of 0.647.

This means that if we regard the fundamental background as bearish, then the price shows stability through its action, which can be regarded as a manifestation of the forces of demand. Therefore, it is possible that the bulls will try to break through the upper limit of the current downward channel. If this happens, the price may face resistance at 0.65350.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

ECB’s Lagarde highlights wage growth as increasingly important inflation

In a European Parliament committee hearing, ECB President Christine Lagarde highlighted that the "ongoing disinflation process" is expected to continue "gradually further down over 2024," attributing this trend to the diminishing effects of past upward shocks and the impact of tighter financing conditions on inflation.

Lagarde noted a "gradual decline" in core inflation, which excludes energy and food prices, while also pointing out the "signs of persistence" in services inflation.

Significantly, Lagarde identified wage growth as a crucial factor, stating it is becoming an "increasingly important driver of inflation dynamics." ECB's wage tracker signals sustained wage pressures, although there's "some levelling off" observed in the latest quarter of 2023. The direction of wage pressures in 2024 largely depends on "ongoing or upcoming negotiation rounds" affecting a broad segment of the workforce.

Furthermore, Lagarde observed that the influence of unit profits on domestic price pressures is on the decline, suggesting that wage increments are being partly accommodated through "profit margins."