Sample Category Title

Crypto Has Retreated from Lows, But No Rush for Growth

Market picture

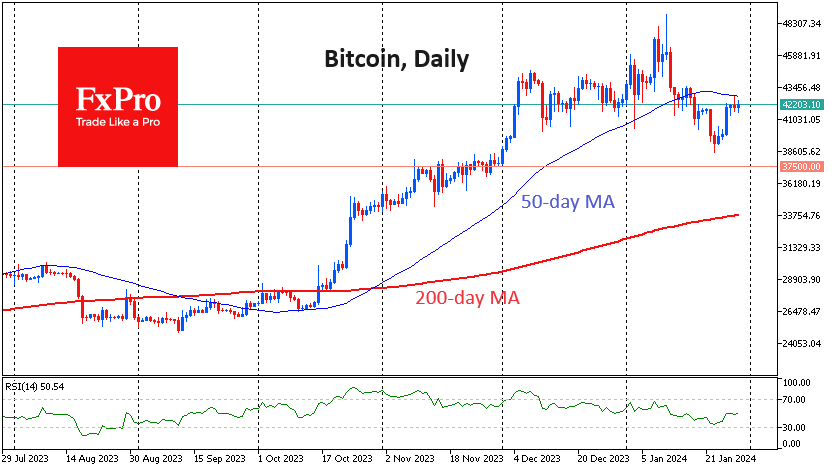

Crypto market capitalisation at around $1.62 trillion is less than 1% higher than it was seven days ago, thanks to a growth spurt on Friday. Bitcoin has added 3% in the same period and continues to be the driving force behind crypto volatility. The sentiment is gradually returning to greed territory, taking the corresponding index to 55 after lows of 48 in the middle of last week.

Bitcoin has stabilised near $42K over the past three days. The 50-day moving average at $42.8K has acted as local resistance for short-term gains. This curve changed direction from rising to falling last week, which looks to be an additional short-term negative factor.

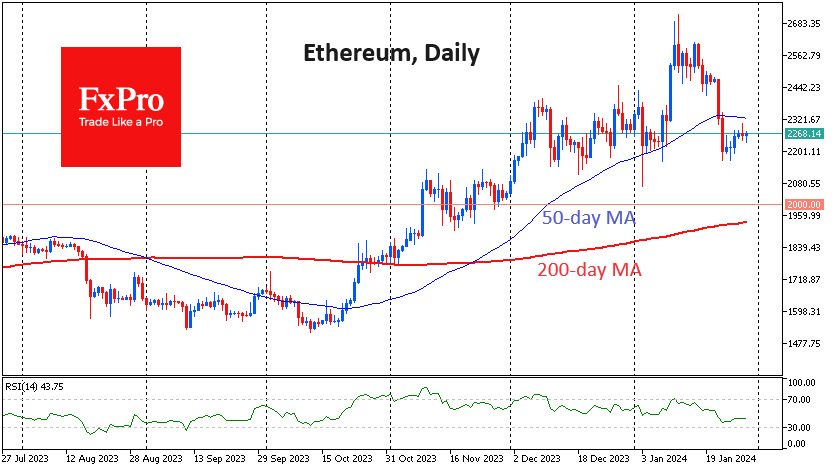

Ethereum, as the flagship cryptocurrency, has pulled back from local lows but is in no hurry to gain altitude, trading near $2270.

The two major cryptocurrencies have started stabilising and rebounding higher than we expected. But we assume that the current calm is a local trap for bulls, and the decline will continue after some pause. The trigger for the decline may be volatility in equities ahead of the reports of giant corporations, the results of the Fed meeting and the employment report.

News background

The US Department of Justice has filed a notice to sell another batch of crypto assets confiscated from the criminal trading platform Silk Road. A total of 2,934 BTC worth $115 million is to be sold.

The US Securities and Exchange Commission (SEC) is likely to approve an ETF based on the spot price of Ethereum in the summer of 2024, Grayscale expects.

According to cryptocurrency payment operator BitPay, XRP has become one of the most used crypto asset for making payments, with the number of payment transactions up 42%. Bitcoin topped the top 10, followed by Litecoin and Ethereum.

According to Flipside, the Polygon project has equalled Ethereum in terms of new users. For 2023, Polygon recorded 15.24 million new accounts, compared to 15.4 million for Ethereum.

Matthew Schultz, co-founder of mining firm CleanSpark, believes that unless Bitcoin shows significant growth, 11 major mining companies will be unprofitable after the halving.

Swiss Franc Recovering, But Will SNB Shift Policy?

The Swiss franc has edged higher on Monday. In the European session, USD/CHF is trading at 0.8618, down 0.25%.

SNB concerned about Swiss franc’s surge

The Swiss National Bank isn’t shy about intervening on the currency markets, as it views intervention as an important tool to keep the Swiss franc competitive for export purposes. The central bank purchased Swiss francs during 2023 in order to boost its value and dampen inflation, which rose above the SNB’s 0%-2% target range.

The strategy worked as inflation returned to the target range, but the SNB may have been too successful, as the Swiss franc soared 9.0% against the US dollar in 2023. This made the Swiss franc the highest-gaining currency against the US dollar last year. In December, the Swiss franc hit a 12-year high against the US dollar.

The Swiss franc has recovered somewhat, rising 2.3% in January. Still, the SNB is concerned about the high-flying Swissie. At the Davos Summit earlier this month, SNB President Thomas Jordan warned that the SNB might rethink its current policy due to the Swiss franc’s sharp appreciation.

The SNB has held the benchmark rate at 1.75% since June and meets next on March 21. Jordan may be pivoting toward a rate cut – the markets have priced in a cut in June but Jordan’s comments have raised the odds of an initial cut in March.

In the US, the Fed’s preferred inflation gauge, the PCE Price Index, rose 0.2% m/m in December, compared to 0.1% in November. On an annual basis, the index remained steady at 2.6%. The Core PCE Index eased to 2.9%, down from 3.2% in November. Inflation continues to ease while economic growth remains solid, which is the recipe that the Fed hopes will continue. The Fed is in no rush to raise rates, and the markets have pared the odds of a quarter-point cut in March to 48%, down sharply from 72% a month ago, according to CME’s FedWatch tool.

USD/CHF Technical

- USD/CHF is testing resistance at 0.8647. Above, there is resistance at 0.8678

- 0.8610 and 0.8559 are the next support lines

ECB’s Kazimir: June is the more probable timing for first rate cut

ECB Governing Council member Peter Kazimir indicated in a blog post that June is the "more probable" timing for the first rate cut. But he emphasized that the timing is "secondary" to the decision itself, and he remains open on this issue.

"The next move will be a cut, and it is within our reach," he asserted, adding, "I am confident that the exact timing, whether in April or June, is secondary to the decision's impact."

"The latter seems more probable, but I will not jump to premature conclusions about the timing," he added.

ECB’s Centeno endorses early, gradual interest rate cuts

ECB Governing Council member Mario Centeno advocates to start cutting interest rates "sooner and more gradually", as there are a lot of evidence that inflation is falling sustainably towards 2% target. He also argued that ECB doesn't need to wait for May wage data before acting.

"We can react later and more strongly, or sooner and more gradually. I am completely in favour of gradualism scenarios, because we have to give economic agents time to adapt to our decisions," he said in a Reuters interview.

This perspective underscores his preference for a steady, sustainable reduction in interest rates, proposing 25 basis-point steps as "a good metric".

Centeno's stance also diverges from some ECB policymakers who propose waiting for Q1 wage data in May, to assess the potential second round effects on inflation. He argues that ECB's decisions should not be exclusively hinged on wage data. "Data-dependent is not wage-data dependent...we don't need to wait for May wage data to get an idea about the inflation trajectory," Centeno remarked.

ECB’s de Guindos: No fixed calendar for rate cuts

ECB Vice President Luis de Guindos expressed cautiously optimistic view on the trajectory of inflation in Eurozone. But he also emphasized that the central bank is data-dependent regarding cutting interest rates, rather than time-dependent.

"There has been good news regarding the evolution of inflation, and that — sooner or later — will end up being reflected in the monetary policy," he told Spain's RNE radio.

However, he was clear about ECB's stance being firmly grounded in data-driven decision-making. Guindos emphasized the absence of a fixed timetable for policy changes, stating, "We are going to be dependent on the data, we don't have any kind of calendar, it will depend on the evolution of inflation."

Could BoE Maintain Its Hawkish Stance?

- The BoE meets on Thursday but low expectations for significant announcements

- Quarterly projections could support market expectations for rate cuts

- Pound would benefit against the US dollar from a hawkish BoE meeting

First rate-setting meeting for 2024

The Bank of England holds its first gathering for 2024 on Thursday at 12:00 GMT, a day after the respective Fed meeting. The same setup in December 2023 proved favourable for the pound as during the December 13-15 sessions it managed to record a quick 2.5% rally against the dollar. The main reason was the divergent rhetoric of the two central banks, with the market getting excited by the comments such as “the decision to hike or to hold was again finely balanced” appearing in the December BoE statement.

What has happened since December 14?

Going into this week’s meeting and data releases have been mixed since December 14, forcing the BoE doves to minimize their rhetoric to a minimum. Inflation remains elevated with the core CPI component proving stubborn and still hovering north of 5%. Retail sales have taken a dive despite the fact that average earnings remain very strong and cause concern in the BoE corridors about future inflation. Interestingly, PMI surveys are edging higher and potentially opening the door to a gradual growth acceleration.

Having said that, the overall rhetoric at this meeting will most likely be a tad more dovish than the December one, but not as dovish as the market might be hoping for. Therefore, in order to justify its 100bps of rate cuts expectations for 2024, the market will most likely pay more attention at three factors: 1/ the number of BoE members voting in favour of a rate hike, 2/ Governor Bailey’s possible effort to add a dovish twist at the press conference, and 3/ the quarterly projections.

How many will vote for another rate hike?

BoE members Greene, Haskel and Mann have been very quiet lately but considering the incoming data, analysed above, it looks unlikely that they would change their stance at this meeting. This is very important for market sentiment as a reduction in the number of the BoE members voting for a rate hike at this meeting would immediately commence the countdown for the much-touted rate cut, currently priced in for June 2024.

On Thursday there is a press conference taking place with Governor Bailey having the chance to further explain the BoE’s thinking process. He has always been a true believer of BoE’s inherit dovishness and, despite the record-breaking inflation in the 2022-2023 period, he managed to keep rate hikes to a minimum. Considering his monetary policy pedigree, there is a risk of him appearing more dovish than circumstances currently demand.

Quarterly projections to play a key role

At the end of the day, the quarterly projections would stir up the discussion. The November Monetary Policy Report had headline inflation dropping to 3.1% and 1.9% by the end of 2024 and 2025 respectively. Any hint of an upgrade in the latter figure could somewhat derail market expectations.

Similarly, the year-end Bank Rate projections for 2024 and 2025 in November 2023 stood at 5.1% and 4.5% respectively. This means that in November, the BoE staff were expecting a single 25bps move lower during 2024. More rate cuts could be added to Thursday projections, but it looks premature for the BoE to fully adopt the market’s current stance of four rate cuts in 2024. Therefore, a figure around 4.8% could please the BoE doves and the market without angering the more hawkish members of the Bank of England.

Pound’s performance to be driven by the Fed and BoE meetings

Pound bulls would clearly enjoy a repeat of the December post-meeting performance in the pound-US dollar pair. For this outcome to take place, the Fed has to be more dovish than currently expected and the BoE more hawkish than foreseen. In this case, pound-dollar could finally overcome the 1.2750 level, which has been acting as a strong resistance point in the past two months, and then have a go at reaching 1.3011.

On the flip side, should the BoE send a strong dovish signal, pound bears could have the chance to push the pound-dollar pair much lower. There are numerous support levels on the way down with the 200-day simple moving average at 1.2552 level being the most plausible target for the pound bears.

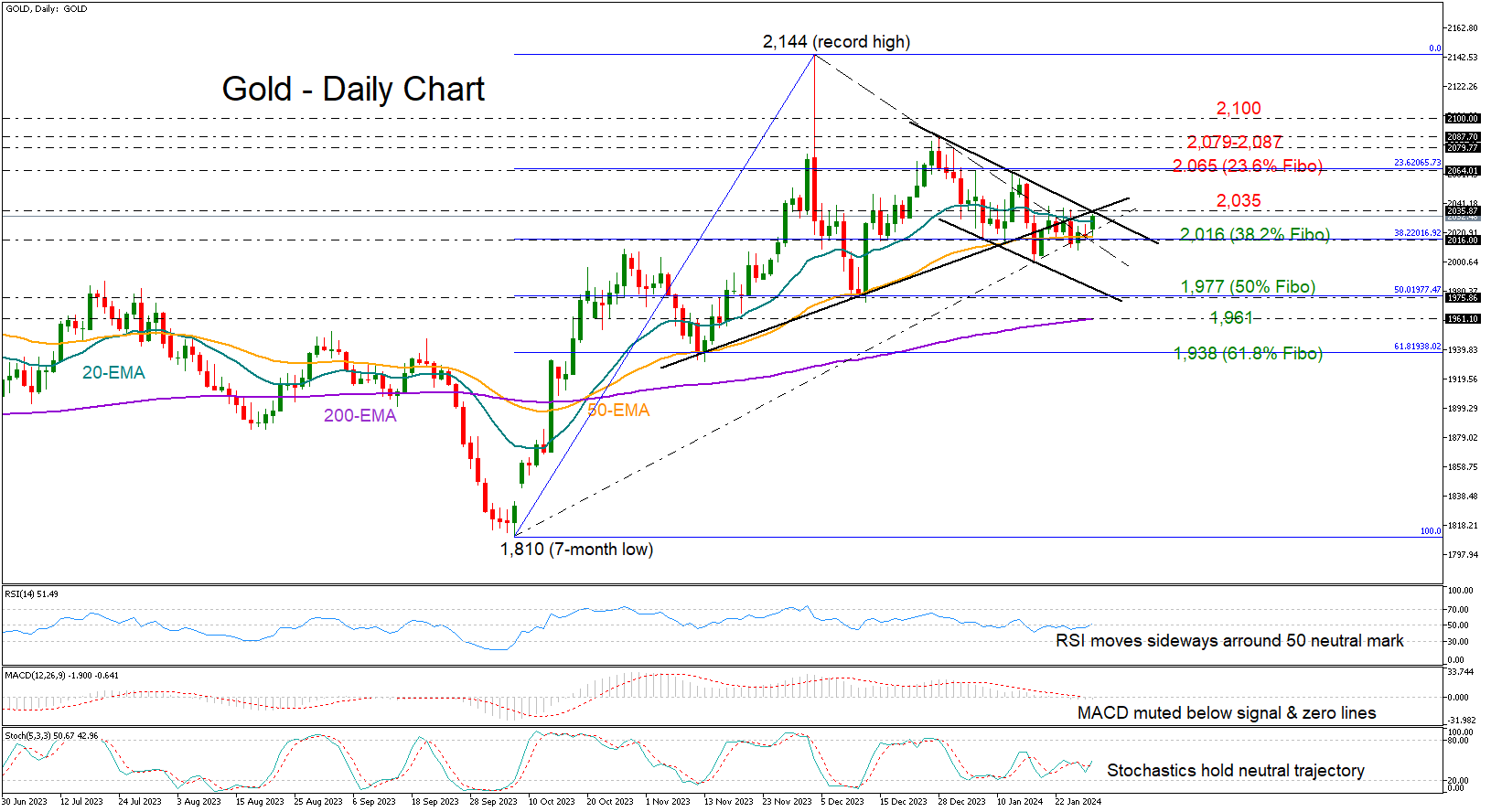

Gold Opens Week Higher But Not Bullish Yet

- Gold rises, but technical signals keep sentiment in balance

- Needs a break above bearish channel at 2,035

Gold started the week on a positive note, aiming to exit last week’s sideways trajectory above its 20-day exponential moving average (EMA) and the 2,035 trendline area after a couple of failed attempts.

Although the horizontal move in the RSI and the stochastic oscillators are balancing hopes for a bullish breakout, upside pressures could stay in play if the 2,016 floor stays intact.

A clear close above the 2,035 border and the short-term bearish channel could cheer buyers, lifting the price straight up to the key 2,065 region, which overlaps with the 23.6% Fibonacci retracement of the October-December upleg. Another success there could see a retest of December’s tough resistance region of 2,079-2,087 before the 2,100 psychological mark comes on the radar.

Otherwise, a slide beneath the 2,016 base, where the 50-day EMA is currently flattening, may cause a sharp decline towards the 50% Fibonacci of 1,977. The 200-day EMA is also in the neighborhood at 1,961. If the bears overpower that barricade, the door will open for the 61.8% Fibonacci level of 1,938 and November’s low of 1,931.

All in all, the precious metal keeps fluctuating within a well-defined area despite starting the week with positive momentum. An extension above 2,035 could confirm a new bullish wave, whereas a slide below 2,016 could activate fresh selling orders.

Brent Oil Price Faces Key Resistance Zone Amid Geopolitical Tensions

The reasons for the rise in Brent oil prices are a drone attack on an American military base in Jordan, as well as an attack on an oil tanker in the Red Sea. These events cause concerns about the safety of oil transportation through the Red Sea and the potential escalation of the conflict in the Middle East. Bloomberg writes that President Biden is under pressure, and the response can be decisive.

The Brent crude oil chart today shows that:

→ The price strengthened higher than the zone of consolidation (shown by narrowing black lines), having completed its bullish break at the psychological level of 80 US dollars per barrel.

→ The price forms an ascending channel (shown in blue).

→ The price rose to the USD 83.00-85.00 zone, which previously served as a support area, but changed its role in November.

→ The market is overbought, judging by the readings of the RSI indicator.

If the geopolitical tension increases, then the bulls can try to raise the price of Brent oil through the specified zone - it is possible that it will reach the upper border of the channel.

On the other hand, if the fundamental background indicates a decrease in the degree of threats in the Middle East, the price can form a pullback from the resistance zone so that the RSI drops closer to values around 50.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

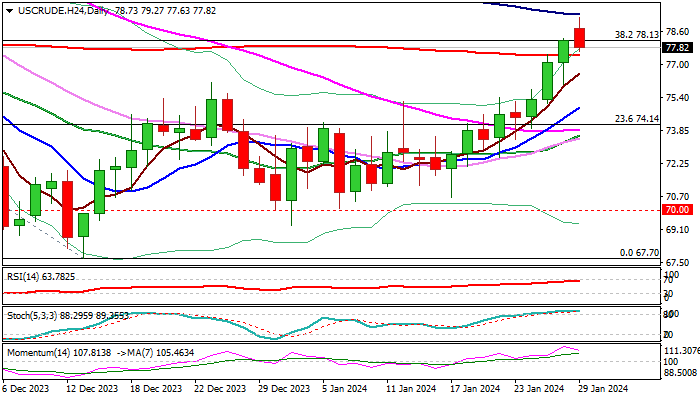

WTI Oil: Enters Corrective Phase But Remains Supported by Growing Supply Disruption Concerns

WTI oil eases in early Monday trading after opening with a gap higher and price rose new two-month high ($79.27).

Growing tensions in the Middle East and fall in Russian refined products export, continue to fuel fears of supply disruption and lift oil prices.

Last week’s 6.3% rally (the biggest weekly gain since the last week of November) registered a marginal close above pivotal Fibo barrier at $78.13 (38.2% retracement of $95.00/$67.70 downtrend).

Monday’s rise probed briefly above the top of thick daily Ichimoku cloud ($78.75) but gains were capped by falling 100DMA ($79.73).

Strongly overbought daily studies and fading bullish momentum contributed to current pullback, which accelerated during European session on Monday.

Broken 200DMA offers initial support at $77.43, followed by $76.91 (Fibo 23.6% of $69.27/$79.27 upleg) and $76.16 (former recovery top of Dec 26).

Extended pullback should find firm ground at $75.00 zone (near Fibo 38.2% of $69.27/$79.27 / rising 10DMA) to mark a healthy correction ahead of fresh push higher and attack of pivotal barriers at $79.73/$80.00 (100DMA / psychological).

Res: 78.13; 78.75; 79.37; 80.00.

Sup: 77.42; 76.91; 76.16; 75.45.

Oil Prices Spiked to Their Highest Levels Since Early November

Markets

European equities on Friday rallied like there was no tomorrow. The Eurostoxx50 added more than a percent to finish the week at the highest level since the 00s. US indices including the S&P500 rose to a new record high but struggled in the aftermath before closing at virtually unchanged levels. US yields recovered intraday with strong income & spending data outweighing media headlines of an outdated PCE core deflator dropping sub 3% for the first time since 2021. Gains amounted up to 5.5 bps at the front. German yields added about 1.5 bps across the curve. The first ECB speeches since the policy meeting on Thursday from the likes of Simkus, Kazaks and Vujcic sounded more hawkish. Knot and Villeroy over the weekend weighed in as well. Both highlighted the importance of wage growth to adapt to slower inflation before cutting rates. The latter said a pace of 2.5% is needed for sustainable price stability. That compares to the latest figure of 5%. Balanced as ever, he did keep the door open for rate cuts “at any time this year”. EUR/USD whipsawed with stocks dictating the intraday moves. The pair eventually closed a tad higher in the mid 1.08/1.09 region. Sterling ended a strong week on softer footing, allowing a slight uptick in EUR/GBP to 0.854.

This week kicks off quietly with few data scheduled for release. That changes quickly though. European Q4 growth will be published tomorrow. Individual EU member states release January inflation figures tomorrow and Wednesday as an appetizer to the European reading on Thursday (seen at 2.7% from 2.9% headline and at 3.2% from 3.4% for the core gauge). The US gets a whole lot of attention as well. The Fed gathers on Wednesday and will have a most recent update on the Employment Cost Index at its disposal just a few hours before making the decision public. Powell didn’t make much of bond correction (higher) in the run-up to the December policy meeting. Markets since then priced in one more additional rate cut for 2024, bringing the total at 135 bps starting in May. Powell probably won’t alter current market sentiment. The economy is holding up very well but inflation is evolving favourably as well. The Fed chair against that background probably isn’t in the mood for being outright hawkish. We think that anything bar the latter will prolong the dovish tide in markets. Following the Fed meeting, the US manufacturing ISM is due on Thursday with payrolls on Friday ending a busy week. We are also on the lookout for the Bank of England gathering this Thursday. Bailey sounded more hawkish than Powell in December and the recent CPI uptick gave no reason to change that tone.

News & Views

The Financial Times reports that according to a document drawn up by EU officials, Brussels is preparing a strategy to convince Hungary into supporting the use of the EU budget to provide €50bn in financial aid to Ukraine. If Hungarian PM Orban doesn’t back down on its verbal threat to block the support at Thursday’s Summit, other EU leaders should publicly vow to permanently shut off all EU funding to Budapest. The document point out that without this EU money; “financial markets and European and international companies might be less interested to invest in Hungary which could quickly trigger a further increase in the cost of funding of the public deficit and a drop in the currency.” It’s unseen that the EU wants to target and exploit economic vulnerabilities of a member state (“very high public deficit”, “very high inflation”, “highest debt servicing payments as a % of GDP”…) in order to strongarm it into a decision. Hungary’s EU Minister Boka said that his country will continue to participate constructively in the negotiations. The forint is already sliding in illiquid Asian dealings (EUR/HUF 388; weakest HUF since October) with more weakness likely during European trading hours.

Oil prices spiked to their highest levels since early November 2023 this morning on reports that three US service members were killed and at least 34 were injured in an Iran-backed militia’s drone strike on a base in northeast Jordan. It marks another escalation in region apart from the Hamas-Israeli conflict in Gaza and the Houthi-backed attacks in the Red Sea. Brent crude currently trades around $84/b, coming from $79/b only a week ago.