Sample Category Title

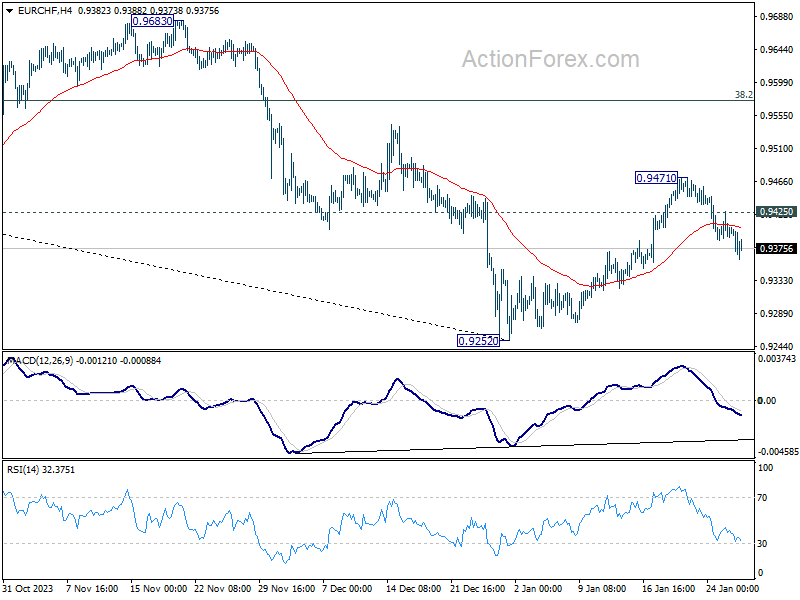

EUR/CHF Weekly Outlook

EUR/CHF failed to sustain above 55 D EMA (now at 0.9443) last week, and reversed from there. Initial bias stays mildly on the downside this week for deeper pull back. But downside should be contained above 0.9252 low to bring rebound. On the upside, above 0.9425 minor resistance will turn bias back to the upside. Further break of 0.9471 will resume the rebound to 38.2% retracement of 1.0095 to 0.9252 at 0.9574.

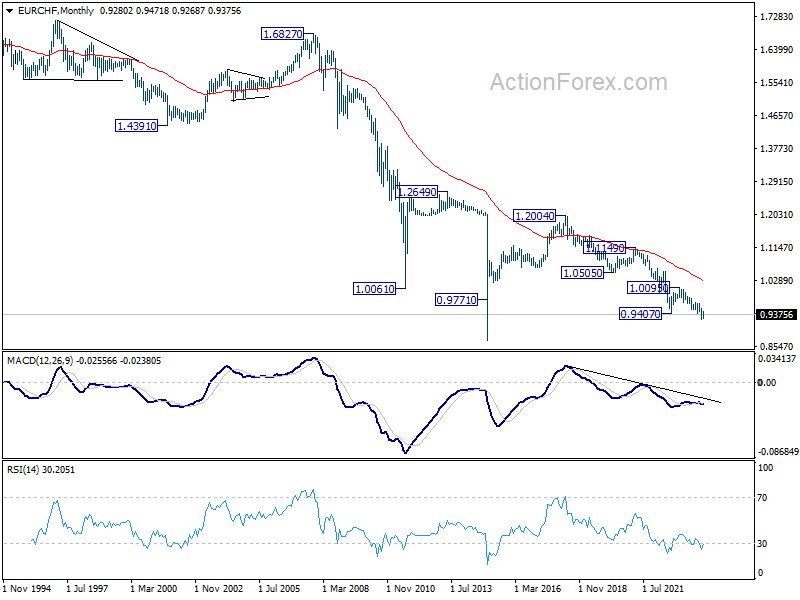

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Another decline is in favor after rebound from 0.9252 completes. However, firm break of 0.9683, and sustained trading above 55 W EMA (now at 0.9659) will argue that EUR/CHF is already in a medium term rally, even as a corrective move.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0265). Larger down trend from 1.2004 (2018 high) is in progress.

Summary 1/29 – 2/2

Monday, Jan 29, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Dec | -975M | -1234M |

| 23:30 | JPY | Unemployment Rate Dec | 2.50% | 2.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Dec | |

| Forecast: -975M | Previous: -1234M | ||

| 23:30 | JPY | Unemployment Rate Dec | |

| Forecast: 2.50% | Previous: 2.50% | ||

Tuesday, Jan 30, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Dec | -1.90% | 2.00% |

| 06:30 | EUR | France Consumer Spending M/M Dec | 0.00% | 0.70% |

| 06:30 | EUR | France GDP Q/Q Q4 P | 0.00% | -0.10% |

| 07:00 | CHF | Trade Balance (CHF) Dec | 2.55B | 3.71B |

| 08:00 | CHF | KOF Leading Indicator Jan | 98.2 | 97.8 |

| 09:00 | EUR | Italy GDP Q/Q Q4 P | 0.00% | 0.10% |

| 09:00 | EUR | Germany GDP Q/Q Q4 P | -0.30% | -0.10% |

| 09:30 | GBP | M4 Money Supply M/M Dec | 0.20% | -0.10% |

| 09:30 | GBP | Mortgage Approvals Dec | 53K | 50K |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | -0.10% | -0.10% |

| 10:00 | EUR | Eurozone Economic Sentiment Jan | 96.2 | 96.4 |

| 10:00 | EUR | Eurozone Industrial Confidence Jan | -9 | -9.2 |

| 10:00 | EUR | Eurozone Services Sentiment Jan | 8 | 8.4 |

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Nov | 4.80% | 4.90% |

| 14:00 | USD | Housing Price Index M/M Nov | 0.20% | 0.30% |

| 15:00 | USD | Consumer Confidence Jan | 113.2 | 110.7 |

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 23:50 | JPY | Industrial Production M/M Dec P | 2.40% | -0.90% |

| 23:50 | JPY | Retail Trade Y/Y Dec | 5.00% | 5.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Dec | |

| Forecast: -1.90% | Previous: 2.00% | ||

| 06:30 | EUR | France Consumer Spending M/M Dec | |

| Forecast: 0.00% | Previous: 0.70% | ||

| 06:30 | EUR | France GDP Q/Q Q4 P | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 07:00 | CHF | Trade Balance (CHF) Dec | |

| Forecast: 2.55B | Previous: 3.71B | ||

| 08:00 | CHF | KOF Leading Indicator Jan | |

| Forecast: 98.2 | Previous: 97.8 | ||

| 09:00 | EUR | Italy GDP Q/Q Q4 P | |

| Forecast: 0.00% | Previous: 0.10% | ||

| 09:00 | EUR | Germany GDP Q/Q Q4 P | |

| Forecast: -0.30% | Previous: -0.10% | ||

| 09:30 | GBP | M4 Money Supply M/M Dec | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 09:30 | GBP | Mortgage Approvals Dec | |

| Forecast: 53K | Previous: 50K | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Jan | |

| Forecast: 96.2 | Previous: 96.4 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Jan | |

| Forecast: -9 | Previous: -9.2 | ||

| 10:00 | EUR | Eurozone Services Sentiment Jan | |

| Forecast: 8 | Previous: 8.4 | ||

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Nov | |

| Forecast: 4.80% | Previous: 4.90% | ||

| 14:00 | USD | Housing Price Index M/M Nov | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 15:00 | USD | Consumer Confidence Jan | |

| Forecast: 113.2 | Previous: 110.7 | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Industrial Production M/M Dec P | |

| Forecast: 2.40% | Previous: -0.90% | ||

| 23:50 | JPY | Retail Trade Y/Y Dec | |

| Forecast: 5.00% | Previous: 5.30% | ||

Wednesday, Jan 31, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Jan | 33.2 | |

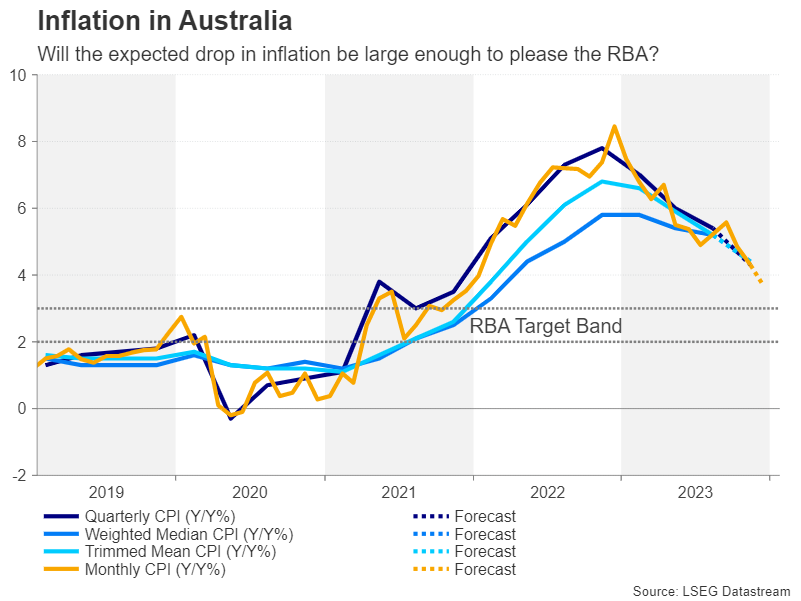

| 00:30 | AUD | CPI Q/Q Q4 | 0.80% | 1.20% |

| 00:30 | AUD | CPI Y/Y Q4 | 4.30% | 5.40% |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q4 | 0.90% | 1.20% |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q4 | 4.40% | 5.20% |

| 00:30 | AUD | Private Sector Credit M/M Dec | 0.40% | 0.40% |

| 01:00 | CNY | NBS Non-Manufacturing PMI Jan | 50.4 | |

| 01:00 | CNY | NBS Manufacturing PMI Jan | 49.3 | 49 |

| 05:00 | JPY | Housing Starts Y/Y Dec | -6.20% | -8.50% |

| 05:00 | JPY | Consumer Confidence Jan | 37.6 | 37.2 |

| 07:00 | EUR | Germany Import Price Index M/M Dec | -0.50% | -0.10% |

| 07:00 | EUR | Germany Retail Sales M/M Dec | 0.60% | -2.50% |

| 07:30 | CHF | Real Retail Sales Y/Y Dec | 0.90% | 0.70% |

| 08:55 | EUR | Germany Unemployment Change Jan | 10K | 5K |

| 08:55 | EUR | Germany Unemployment Rate Jan | 5.90% | 5.90% |

| 09:00 | CHF | Credit Suisse Economic Expectations Jan | -23.7 | |

| 09:00 | EUR | Italy Unemployment Dec | 7.50% | 7.50% |

| 13:00 | EUR | Germany CPI M/M Jan P | 0.20% | 0.10% |

| 13:00 | EUR | Germany CPI Y/Y Jan P | 3.40% | 3.70% |

| 13:15 | USD | ADP Employment Change Jan | 143K | 164K |

| 13:30 | CAD | GDP M/M Nov | 0.10% | 0.00% |

| 13:30 | USD | Employment Cost Index Q4 | 1.00% | 1.10% |

| 14:45 | USD | Chicago PMI Jan | 48.2 | 46.9 |

| 15:30 | USD | Crude Oil Inventories | -9.2M | |

| 19:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% |

| 19:30 | USD | FOMC Press Conference |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Jan | |

| Forecast: | Previous: 33.2 | ||

| 00:30 | AUD | CPI Q/Q Q4 | |

| Forecast: 0.80% | Previous: 1.20% | ||

| 00:30 | AUD | CPI Y/Y Q4 | |

| Forecast: 4.30% | Previous: 5.40% | ||

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q4 | |

| Forecast: 0.90% | Previous: 1.20% | ||

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q4 | |

| Forecast: 4.40% | Previous: 5.20% | ||

| 00:30 | AUD | Private Sector Credit M/M Dec | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 01:00 | CNY | NBS Non-Manufacturing PMI Jan | |

| Forecast: | Previous: 50.4 | ||

| 01:00 | CNY | NBS Manufacturing PMI Jan | |

| Forecast: 49.3 | Previous: 49 | ||

| 05:00 | JPY | Housing Starts Y/Y Dec | |

| Forecast: -6.20% | Previous: -8.50% | ||

| 05:00 | JPY | Consumer Confidence Jan | |

| Forecast: 37.6 | Previous: 37.2 | ||

| 07:00 | EUR | Germany Import Price Index M/M Dec | |

| Forecast: -0.50% | Previous: -0.10% | ||

| 07:00 | EUR | Germany Retail Sales M/M Dec | |

| Forecast: 0.60% | Previous: -2.50% | ||

| 07:30 | CHF | Real Retail Sales Y/Y Dec | |

| Forecast: 0.90% | Previous: 0.70% | ||

| 08:55 | EUR | Germany Unemployment Change Jan | |

| Forecast: 10K | Previous: 5K | ||

| 08:55 | EUR | Germany Unemployment Rate Jan | |

| Forecast: 5.90% | Previous: 5.90% | ||

| 09:00 | CHF | Credit Suisse Economic Expectations Jan | |

| Forecast: | Previous: -23.7 | ||

| 09:00 | EUR | Italy Unemployment Dec | |

| Forecast: 7.50% | Previous: 7.50% | ||

| 13:00 | EUR | Germany CPI M/M Jan P | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 13:00 | EUR | Germany CPI Y/Y Jan P | |

| Forecast: 3.40% | Previous: 3.70% | ||

| 13:15 | USD | ADP Employment Change Jan | |

| Forecast: 143K | Previous: 164K | ||

| 13:30 | CAD | GDP M/M Nov | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 13:30 | USD | Employment Cost Index Q4 | |

| Forecast: 1.00% | Previous: 1.10% | ||

| 14:45 | USD | Chicago PMI Jan | |

| Forecast: 48.2 | Previous: 46.9 | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -9.2M | ||

| 19:00 | USD | Fed Interest Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 19:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

Thursday, Feb 1, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q4 | -1 | |

| 00:30 | AUD | Building Permits M/M Dec | 0.10% | 1.60% |

| 00:30 | AUD | Import Price Index Q/Q Q4 | 0.60% | 0.80% |

| 00:30 | JPY | Manufacturing PMI Jan F | 48.0 | 48.0 |

| 01:45 | CNY | Caixin Manufacturing PMI Jan | 50.9 | 50.8 |

| 08:30 | CHF | Manufacturing PMI Jan | 44.5 | 43.0 |

| 08:45 | EUR | Italy Manufacturing PMI Jan | 47.3 | 45.3 |

| 08:50 | EUR | France Manufacturing PMI Jan F | 43.2 | 43.2 |

| 08:55 | EUR | Germany Manufacturing PMI Jan F | 45.4 | 45.4 |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | 46.6 | 46.6 |

| 09:30 | GBP | Manufacturing PMI Jan F | 46.9 | 47.3 |

| 10:00 | EUR | Eurozone Unemployment Rate Dec | 6.40% | 6.40% |

| 10:00 | EUR | Eurozone CPI Y/Y P | 2.70% | 2.90% |

| 10:00 | EUR | Eurozone CPI Core Y/Y P | 3.20% | 3.40% |

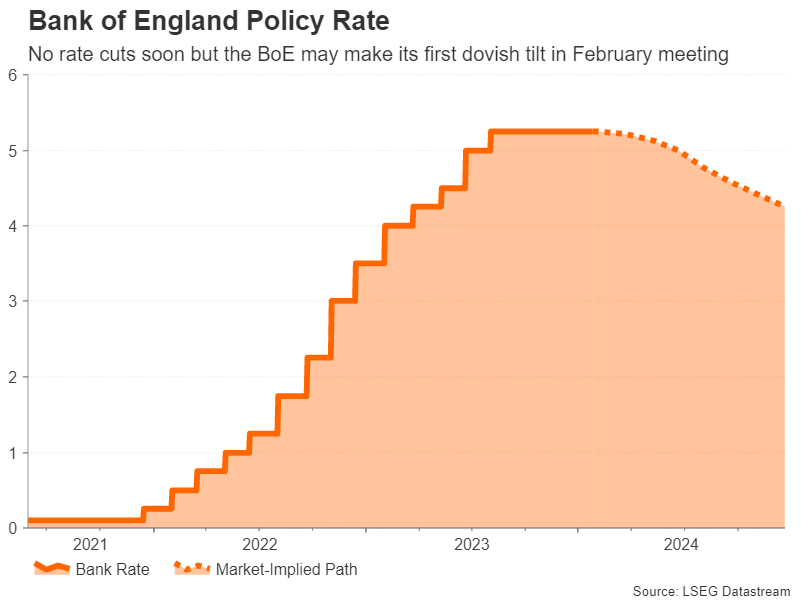

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% |

| 12:00 | GBP | MPC Official Bank Rate Votes | 2--0--7 | 3--0--6 |

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | -20.20% | |

| 13:30 | USD | Initial Jobless Claims (Jan 26) | 211K | 214K |

| 13:30 | USD | Nonfarm Productivity Q4 P | 2.40% | 5.20% |

| 13:30 | USD | Unit Labor Costs Q4 P | 2.10% | -1.20% |

| 14:30 | CAD | Manufacturing PMI Jan | 45.4 | |

| 14:45 | USD | Manufacturing PMI Jan F | 50.3 | 50.3 |

| 15:00 | USD | ISM Manufacturing PMI Jan | 47.7 | 47.4 |

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | 45.6 | 45.2 |

| 15:00 | USD | ISM Manufacturing Employment Index Jan | 48.1 | |

| 15:00 | USD | Construction Spending M/M Dec | 0.50% | 0.40% |

| 15:30 | USD | Natural Gas Storage | -326B | |

| 21:45 | NZD | Building Permits M/M Dec | -10.60% | |

| 23:50 | JPY | Monetary Base Y/Y Jan | 7.50% | 7.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q4 | |

| Forecast: | Previous: -1 | ||

| 00:30 | AUD | Building Permits M/M Dec | |

| Forecast: 0.10% | Previous: 1.60% | ||

| 00:30 | AUD | Import Price Index Q/Q Q4 | |

| Forecast: 0.60% | Previous: 0.80% | ||

| 00:30 | JPY | Manufacturing PMI Jan F | |

| Forecast: 48.0 | Previous: 48.0 | ||

| 01:45 | CNY | Caixin Manufacturing PMI Jan | |

| Forecast: 50.9 | Previous: 50.8 | ||

| 08:30 | CHF | Manufacturing PMI Jan | |

| Forecast: 44.5 | Previous: 43.0 | ||

| 08:45 | EUR | Italy Manufacturing PMI Jan | |

| Forecast: 47.3 | Previous: 45.3 | ||

| 08:50 | EUR | France Manufacturing PMI Jan F | |

| Forecast: 43.2 | Previous: 43.2 | ||

| 08:55 | EUR | Germany Manufacturing PMI Jan F | |

| Forecast: 45.4 | Previous: 45.4 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | |

| Forecast: 46.6 | Previous: 46.6 | ||

| 09:30 | GBP | Manufacturing PMI Jan F | |

| Forecast: 46.9 | Previous: 47.3 | ||

| 10:00 | EUR | Eurozone Unemployment Rate Dec | |

| Forecast: 6.40% | Previous: 6.40% | ||

| 10:00 | EUR | Eurozone CPI Y/Y P | |

| Forecast: 2.70% | Previous: 2.90% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y P | |

| Forecast: 3.20% | Previous: 3.40% | ||

| 12:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 5.25% | Previous: 5.25% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 2--0--7 | Previous: 3--0--6 | ||

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | |

| Forecast: | Previous: -20.20% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 26) | |

| Forecast: 211K | Previous: 214K | ||

| 13:30 | USD | Nonfarm Productivity Q4 P | |

| Forecast: 2.40% | Previous: 5.20% | ||

| 13:30 | USD | Unit Labor Costs Q4 P | |

| Forecast: 2.10% | Previous: -1.20% | ||

| 14:30 | CAD | Manufacturing PMI Jan | |

| Forecast: | Previous: 45.4 | ||

| 14:45 | USD | Manufacturing PMI Jan F | |

| Forecast: 50.3 | Previous: 50.3 | ||

| 15:00 | USD | ISM Manufacturing PMI Jan | |

| Forecast: 47.7 | Previous: 47.4 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | |

| Forecast: 45.6 | Previous: 45.2 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Jan | |

| Forecast: | Previous: 48.1 | ||

| 15:00 | USD | Construction Spending M/M Dec | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -326B | ||

| 21:45 | NZD | Building Permits M/M Dec | |

| Forecast: | Previous: -10.60% | ||

| 23:50 | JPY | Monetary Base Y/Y Jan | |

| Forecast: 7.50% | Previous: 7.80% | ||

Friday, Feb 2, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | PPI Q/Q Q4 | 1.90% | 1.80% |

| 00:30 | AUD | PPI Y/Y Q4 | 3.80% | |

| 07:45 | EUR | France Industrial Output M/M Dec | 0.20% | 0.50% |

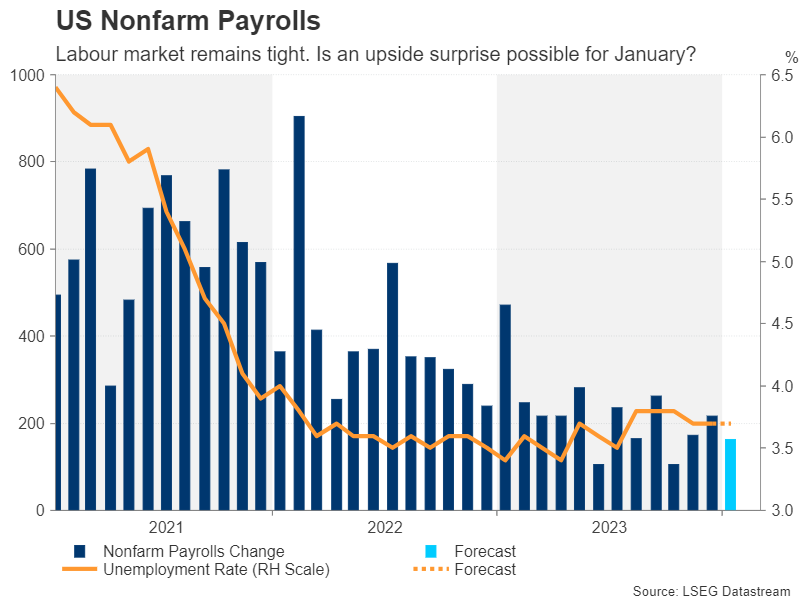

| 13:30 | USD | Nonfarm Payrolls Jan | 178K | 216K |

| 13:30 | USD | Unemployment Rate Jan | 3.80% | 3.70% |

| 13:30 | USD | Average Hourly Earnings M/M Jan | 0.30% | 0.40% |

| 15:00 | USD | Factory Orders M/M Dec | 0.50% | 2.60% |

| 15:00 | USD | Michigan Consumer Sentiment Index Jan F | 78.8 | 78.8 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | PPI Q/Q Q4 | |

| Forecast: 1.90% | Previous: 1.80% | ||

| 00:30 | AUD | PPI Y/Y Q4 | |

| Forecast: | Previous: 3.80% | ||

| 07:45 | EUR | France Industrial Output M/M Dec | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 13:30 | USD | Nonfarm Payrolls Jan | |

| Forecast: 178K | Previous: 216K | ||

| 13:30 | USD | Unemployment Rate Jan | |

| Forecast: 3.80% | Previous: 3.70% | ||

| 13:30 | USD | Average Hourly Earnings M/M Jan | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 15:00 | USD | Factory Orders M/M Dec | |

| Forecast: 0.50% | Previous: 2.60% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Jan F | |

| Forecast: 78.8 | Previous: 78.8 | ||

The Weekly Bottom Line: Feds, BoC Steal This Show This Week

U.S. Highlights

- The U.S. economy ended 2023 on a solid note, with GDP rising 3.3% quarter-over-quarter (annualized) – smashing expectations for a more moderate gain of 2%.

- The consumer remained a key factor underpinning last quarter’s strength, with spending accelerating sharply through the holiday shopping season.

- Inflation continued to drift lower in December, with the 12-month change on core PCE – the Fed’s preferred inflation measure – slipping below 3%.

Canadian Highlights

- The Bank of Canada held their policy rate at 5% this week, while making minor tweaks to their forecasts. Messaging accompanying the decision pointed to no change in rates for the time being.

- Markets have priced in a rate cut in June. Our own call sees rates beginning to move lower in the second quarter.

- The federal government announced a cap on international student visas this week. This will weigh on consumption and offer some relief to Canada’s rental market.

U.S. – The Final Approach

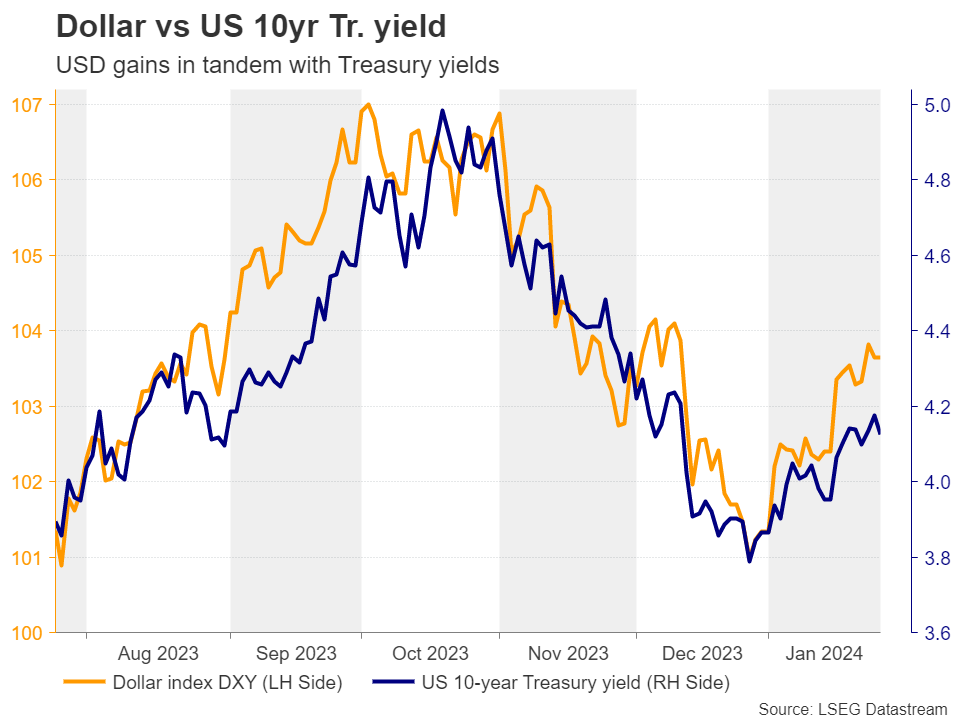

The latest data has shown the U.S. economy had all the markings of a soft landing as 2023 drew to a close. Economic growth held up better than expected, the labor market is coming back into better balance, and price pressures are quickly abating. Market pricing on the timing of the first Fed rate cut has seesawed between March and May in recent months, with March currently priced as a coin-toss. But with progress on the inflation front showing no signs of stalling, market sentiment remained in risk-on mode this week, with the S&P 500 edging up 1% for the week, reaching yet another all-time high. Shorter-term yields drifted a bit lower, leading to a further flattening in the yield curve. At the time of writing, the inversion of the 10Y-2Y spread had narrowed to just -20bps – well off the peak inversion of -110bps seen back in July.

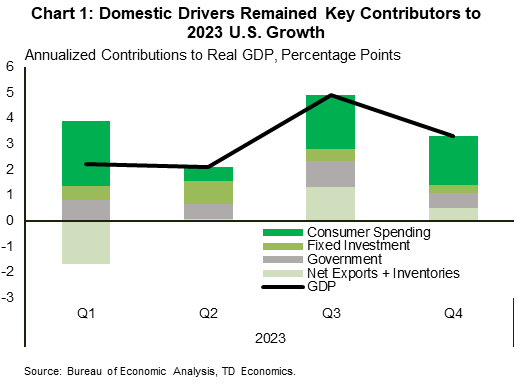

The Bureau of Economic Analysis’ advance estimate of fourth quarter real GDP came in at 3.3%, a downshift from Q3’s blistering 4.9%, but well above the consensus forecast calling for a more moderate gain of 2%. Economic resilience remained on full display, with the consumer, private investment, and government spending accounting for the lion’s share of last quarter’s gain (Chart 1). While the rearview mirror isn’t always the best guide to the road ahead, the solid end to last year provides a more favorable starting point heading into 2024.

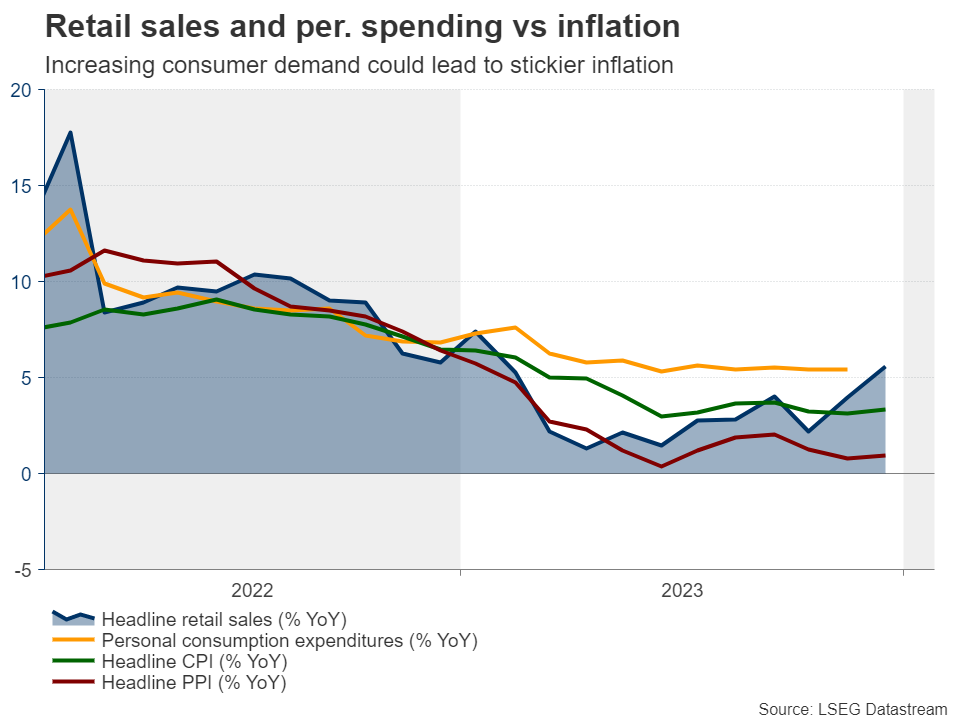

This is especially true for the consumer. The monthly income and spend figures for December – released a day after the GDP report – showed consumer spending accelerated sharply through the holiday shopping season. This was happening even though the tailwinds from excess savings had slowed from the gale force gust felt at the beginning of the tightening cycle to just a gentle breeze by the end of last year. At the same time, 27 million student loan borrowers were faced with the harsh reality of having to restart regular loan repayments in October following the expiration of the three-year student loan moratorium. But neither of these factors appear to have phased the consumer, as a still sturdy labor market has continued to support meaningful gains in real income and help to sustain a healthy pace of consumer spending.

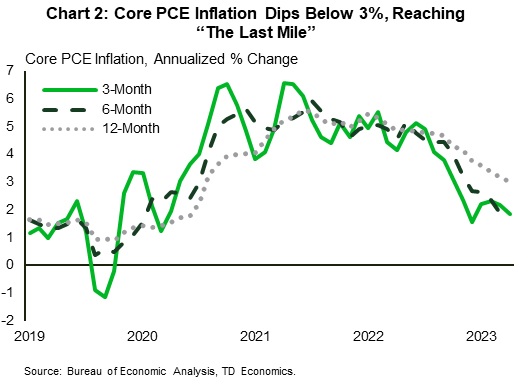

The puzzle has been on the inflation front. Despite the economy continuing to run well above its long-run potential through H2’2023, inflation has still made incredible progress. As of December, the 12-month rate of change on core PCE fell to 2.9%, while the annualized 3-and-6-month rates slipped to 1.5% and 1.9%, respectively (Chart 2). Falling goods prices and some cooling in non-housing services have both been the key contributors to the recent downward pressure on inflation.

From the Fed’s perspective, time (and the economic data) remain on their side. With the economy showing no signs of keeling over, and the labor market still relatively tight, policymakers can afford to be patient. Fed officials will want to see at least a few more ‘soft’ readings on inflation and a bit more easing in the labor market before pulling the trigger on rate cuts.

Canada – Feds, BoC Steal This Show This Week

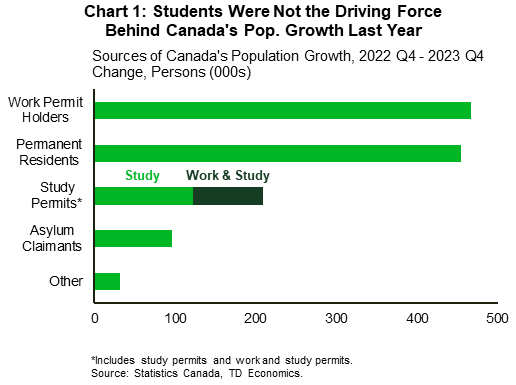

Multigenerational highs in Canada's population growth have strained the country's social systems and inflamed the country's housing crisis. In view of these challenges (and others), the federal government announced a cap on international students. The idea is that in the fall of this year, the number of student visas will be rolled back to 2022 levels, and some estimates suggest that this could lower the student intake by at least 200k spots over time. To put this figure in perspective, it would amount to roughly 20% of Canada's massive population inflow in 2023.

This will undoubtedly sap some steam from Canada's frothy population growth. This weaker growth will then weigh on consumption and housing. On the latter, the policy should slow down rent growth relative to its prior trajectory. However, it's tough to envision a large-scale cool down in rents this year. Note that even if this policy begins to weigh on population growth this year, it was newcomers with work permits (not students) who were largely responsible for Canada's population surge last year (Chart 1). What's more, immigration levels (untouched by the policy) remain robust.

The even bigger news this week for financial markets was the Bank of Canada's interest rate decision. There are a handful of important takeaways. First, the Bank of Canada left their policy rate on hold, as expected. Second, their inflation and economic growth forecasts were little changed from the prior report. Notably, the Bank still sees headline inflation falling to 2.4% by the end of this year and 2.1% by the final quarter of 2025. These projections match our own. However, we see the economy posting weaker growth in 2024 and 2025, with rising debt service costs keeping the pressure on Canada's highly indebted households. Third, the statement accompanying the decision was a touch more dovish than October, and Governor Macklem's opening remarks after the decision noted that no further tightening will be required if their forecast evolves as expected. Fourth, the Bank took great pains to acknowledge that shelter costs will be a "material headwind" against the return of inflation to its target. These costs do complicate the Bank's inflation fight, as they are partly due to factors beyond the Bank's control, and policymakers will seemingly not "look through" them when setting policy. Fifth, Governor Macklem acknowledged the broad range of inflation indicators that the Bank is looking at to get a sense of underlying inflation, even if the preferred measures are CPI-trim and CPI-median. This could offer the Bank some degree of optionality on how they frame the trend in inflation moving forward.

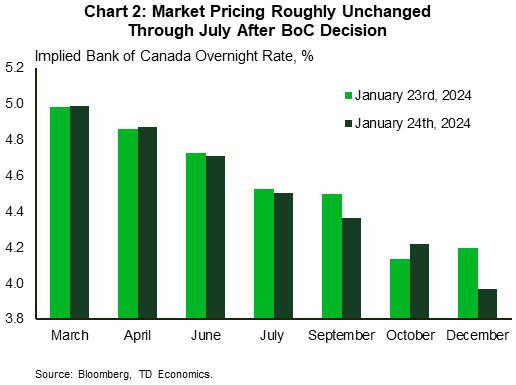

The Bank's interest rate decision didn't meaningfully sway the markets' rate expectations, at least over the next few meetings (Chart 2). June remains the likeliest month for the first rate cut, in the mind of markets. Our own expectation is that policymakers will be in position to cut their policy rate sometime in the second quarter of this year.

Weekly Economic & Financial Commentary: Almost Everything Coming Up Roses

Summary

United States: Almost Everything Coming Up Roses

- Data released this week garnered further optimism that the economy can power through the Federal Reserve's efforts to corral inflation—an endeavor the Fed could increasingly be construed as achieving. Economic activity ended the year on better footing than expected, and inflation continued its deceleration.

- Next week: Construction Spending (Thu.), ISM Manufacturing (Thu.), Employment (Fri.)

International: Foreign Central Banks at the Forefront

- It was a busy week for foreign central banks. The Bank of Japan appears to be on course for an April rate hike, while a dovish Bank of Canada announcement suggested the risks are tilted toward an earlier initial rate cut than our June base case. We still forecast an initial rate cut from the European Central Bank in April, though we acknowledge that risks for a later June move do exist.

- Next week: China PMIs (Wed.), Bank of England Policy Rate (Thu.), Eurozone CPI (Thu.)

Interest Rate Watch: In a Holding Pattern

- As discussed in our Fed Flashlight report released this week, we share the near-universally held view that the FOMC will leave the fed funds rate and pace of quantitative tightening (QT) unchanged at its upcoming meeting on January 31.

Credit Market Insights: Increased Borrowing in the Beige Book

- In the most recent Beige Book released by the Fed, a majority of the 12 Federal Reserve Districts reported little or no change in economic activity, reflecting the continuing resilience of the economy. However, closer examination of this month’s Beige Book reveals the cracks that are beginning to emerge in the economy, particularly for household borrowing.

Topic of the Week: Sea of Red

- The recent Houthi militant attacks in the Red Sea have thrown a wrench in global supply chains. Container ship spot rates have jumped as capacity is stretched and popular trade routes are diverted around the southern tip of Africa. For the U.S., the impact may be more muted as businesses look to be in far better shape to weather any potential supply disruption today.

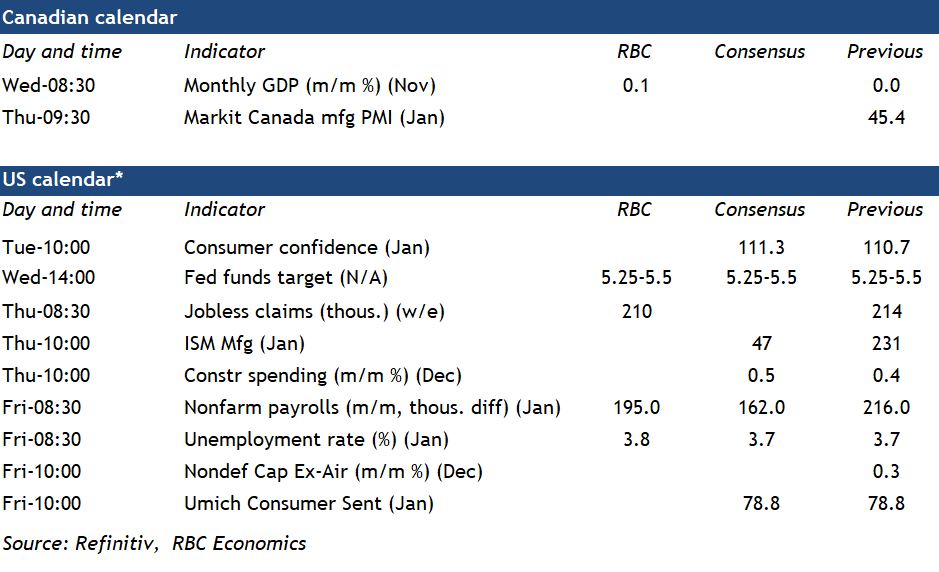

Canada’s November GDP to Edge Higher for First Time Since May But Economy Still Looks Weak

The November Canadian gross domestic product (GDP) estimate released on Wednesday will probably tick higher for the first time in six months, but the economic backdrop to end 2023 still looks soft.

We expect a 0.1% increase in GDP from October, which would be in line with Statistics Canada’s early estimate a month ago. These advance estimates have been prone to revisions. Still, data released since for November has largely been consistent with a tick higher in output. Retail sale volumes edged lower in November, but manufacturing and wholesale sale volumes rose (by 1.6% and 0.6% month-over-month, respectively) and oil production in Alberta increased.

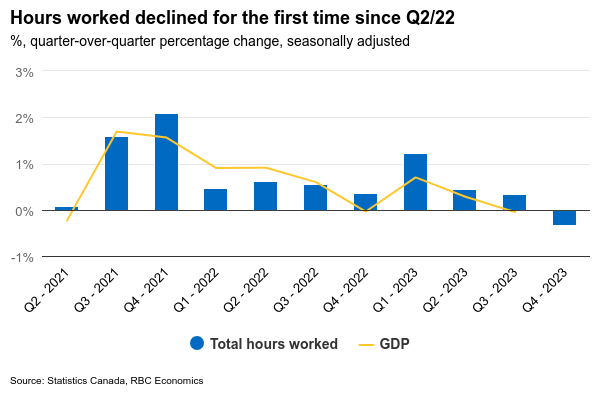

Still, other indicators have been softer. Employment continued to rise through the end of last year, but actual hours worked declined for the first time in Q4 since the early days of the pandemic (Q2/2020). The early estimate of December manufacturing sales was down 0.6%.

The economic growth data looks substantially weaker on a per-capita basis after controlling for still rapid population growth. We continue to expect a small decline in Q4 GDP once all the numbers have been counted, but even a small increase would leave output per person down for a sixth consecutive quarter.

The labour market also still looks substantially softer with the unemployment rate up 0.8 percentage points since spring 2023. The Bank of Canada has referenced the softer economic backdrop as the reason additional interest rate hikes this year are unlikely and we continue to expect a pivot to gradual cuts by mid-year.

Week ahead data watch

The U.S. Federal Reserve is widely expected to hold the fed funds target range unchanged for a fourth consecutive meeting on Wednesday. Attention will be focused on any hints on the potential timing of a pivot to cuts. Another round of strong GDP data in Q4 showed that the economy is still weathering higher interest rates better than expected. But slowing price growth is leaving the Fed with flexibility to hold the line on interest rates for now – and to respond with lower rates later this year (we expect before mid-year) once the economy starts to soften more significantly.

Next Friday, we will get the first U.S. jobs report for 2024. Payroll employment is likely up by 195K in January, slightly below the 216K in December. The unemployment rate should continue to edge up to 3.8% from 3.7% in December, reflecting some easing conditions in the labour market.

Bank of England Preview – Topside Risk to EUR/GBP as BoE Removes Tightening Bias

- We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 1 February, which is in line with consensus and current market pricing.

- Overall, we expect the MPC to deliver a dovish tilt to its guidance coupled with a downward revision to its inflation forecast.

- We expect EUR/GBP to move modestly higher upon announcement.

We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 1 February, which is in line with consensus and current market pricing. We expect the vote split to be 9-0, although we stress that risks are two sided for a three-way split. Note, this meeting will include updated projections and a press conference following the release of the statement.

Overall, we expect the MPC to deliver a dovish tilt to its guidance coupled with a downward revision to its inflation forecast and more explicitly to remove its tightening bias in the form of "further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures." However, we think the BoE will be cautious in being too optimistic on the inflation outlook to prevent premature easing of financial conditions.

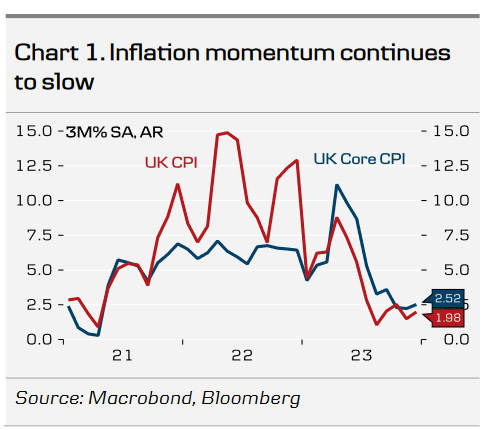

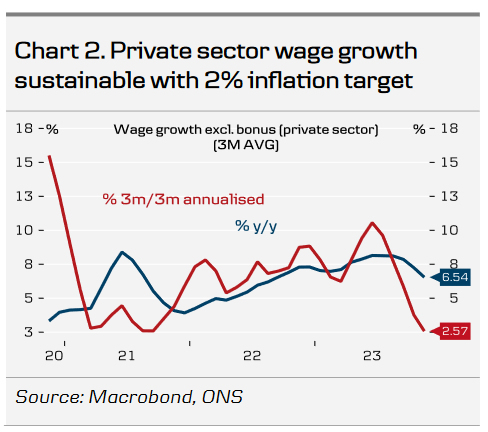

Since the last monetary policy decision in December, data releases have overall pointed to more muted price pressures. November delivered a sharp broad-based downside surprise and while December brought an uptick, primarily due to volatile components such as air fares, it highlights that the road back to 2% will be bumpy. Importantly, the Q4 2023 headline print now stands at 4.2% y/y, which is below the BoE's forecast from the November MPR at 4.6% y/y. Large base effects from energy prices last spring are set to bring headline inflation back to 2% during the first half of the year. As previously flagged, we do not see inflation developing materially different in the UK compared to elsewhere. Wage growth continues to edge lower with the pace of wage growth in the private sector now sustainable with a 2% inflation target (assuming 1% productivity growth), see chart 2. The growth backdrop remains a challenge for the MPC, with both composite and service PMIs remaining in expansionary territory pointing to the UK avoiding a recession in 2024.

Fiscal policy remains a joker for the monetary policy outlook. The chancellor is expected to have a larger than expected headroom at around GBP 20bn in the Spring Budget presented on 6 March. Coupled with an upcoming general election, the budget will likely include tax cuts. However, we expect measures to be largely supply side driven, which would minimise the potential upward pressure on inflation.

BoE call. We expect the BoE to prime markets for an upcoming rate cut at the May meeting while delivering the first cut of 25bp in June and subsequently 25bp cuts in the following quarters, totalling 75bp of cuts for 2024. This is less than current market pricing of 100bp. Importantly, we do not see the BoE deviating from the Fed and ECB by the extent currently priced by markets and expect markets to scale back on expectations from the latter.

FX. In our base case we expect EUR/GBP to move higher on softer guidance and updated projections. Overall, we see relative rates as a negative for GBP and see the recent rebound as attractive levels to sell GBP. We continue to forecast EUR/GBP towards 0.89 and stay short GBP/USD.

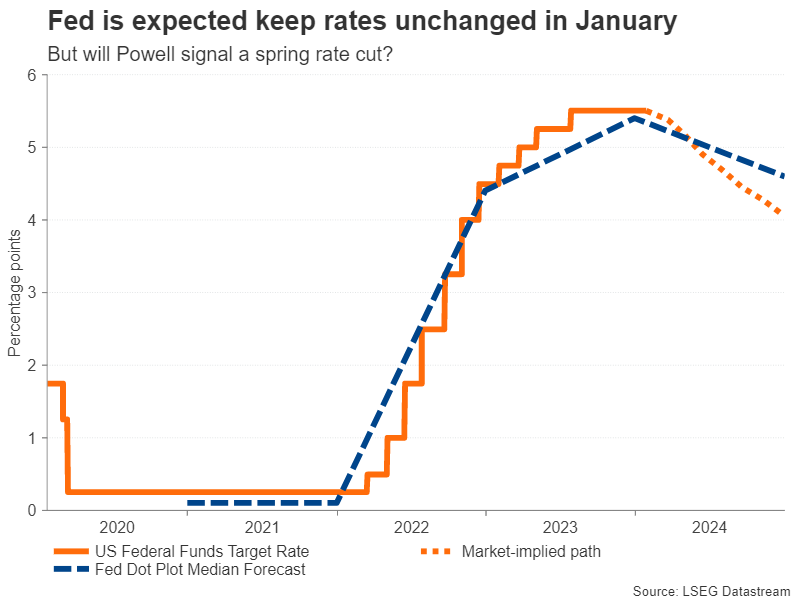

Fed Preview: Patience and Gradualism

- We expect the Fed to maintain its monetary policy unchanged in the January meeting. We expect the first rate cut in March and a total of four cuts in 2024.

- The Fed is in a comfortable position with regards to both sides of its dual mandate. Cooling inflation warrants cutting rates towards neutral, but solid growth and labour markets allow the Fed to move gradually.

- The Fed is also starting to look towards fine-tuning the endgame for QT, which we expect to last at least until the end of the year. Overall, we see risks tilted towards slightly higher yields and lower EUR/USD around the meeting.

The title of this preview quotes SF Fed's Mary Daly, a new FOMC voter for 2024, who was the last participant to comment on monetary policy outlook ahead of the January blackout. Next Wednesday, with no new economic forecasts, all eyes will be on Powell, who we expect to echo Daly and several of their colleagues' recent remarks, emphasizing cautious yet optimistic outlook.

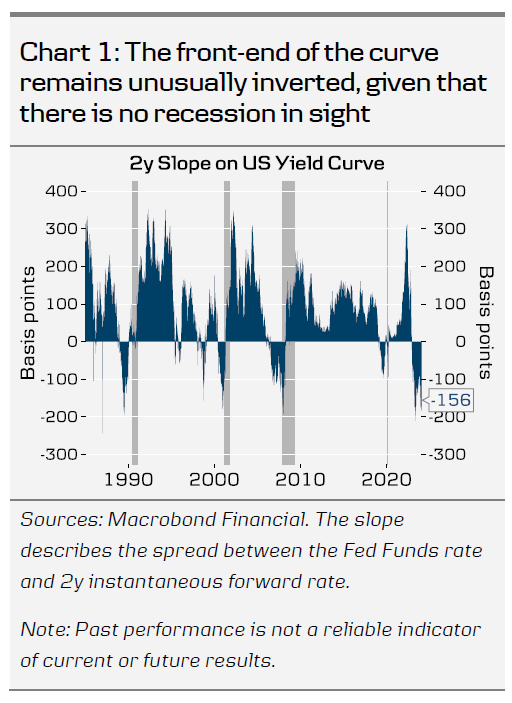

Market prices in around 140bp of cuts for this year. Over the past 40 years, the front-end of the curve has only been as inverted just ahead of recessions, which does not seem like the case today. Recovering real wages, easier financial conditions, rising consumer optimism and supportive fiscal policy all suggest that an imminent slowdown is unlikely.

The December projections showed that real policy rate would remain somewhat above 2% this year, around 1.5% in 2025 and then settle close to neutral in 2026. While the Fed is happy to discuss rate cuts for 2024, monetary policy will not be expansionary anytime soon.

The December minutes suggested that upside risks to inflation have 'diminished', but some risk of persistent inflation still remains, especially in housing and non-housing services. With the recent strong data signals from labour markets, consumer demand and housing market, we think that the near-term inflation outlook supports the gradual approach.

In addition to Daly, also Mester, Barkin and Bostic are rotating in as the new FOMC voters for 2024, while Goolsbee, Harker, Kashkari and Logan are moving out. We do not expect the rotation to have a significant impact on the Fed's decision making, but if anything, the new voters' recent comments have been on the hawkish side of the spectrum. Mester explicitly noted that March is too early for a rate cut in her view, while Bostic outlined Q3 as his base case for the first cut. Barkin has not specified a timeline for cuts but noted that progress on inflation has remained narrow and focused on goods.

The outlook for tapering QT has also been increasingly brought up in the latest Fed speak. Waller noted that the endpoint level of reserves could as low as 10-11% of GDP, and that the ON RRP could well be drained to zero. We looked at the arithmetics of QT in our recent edition of Reading-the-Markets USD (16 January), but the key takeaway is that liquidity conditions will likely allow the Fed to continue QT at least until the end of 2024. Overall, we think Powell could guide modestly against the notion of rapid rate cuts and/or end of QT, which leaves risks tilted towards a hawkish market reaction. That said, the upside potential to yields is likely limited, as we still expect a total of four cuts in 2024.

Markets: Stronger USD & stable UST yields in 2024

UST yields looks somewhat vulnerable to a pushback from Powell, especially if it coincides with the Quarterly Refunding statement (also out Wednesday evening) signalling further increases in long-end issuance. Our base case is for the 10Y UST yield to remain close the current level (4.15%-4.20%) by the end of the year, though risks are tilted to the upside in the short run.

If Powell pushes back on the market notion of rapid rate cuts, as we anticipate, we could see a lower EUR/USD upon announcement. Our forecast for the cross is lower at 1.07/1.05 on a 6/12M horizon.

Will Fed Push Back Against Imminent Rate Cuts?

- Investors scale back bets of a March Fed rate cut

- US economic data since December point to improvement

- Focus turns to Fed meeting for clearer guidance on interest rates

- Decision on Wednesday at 19:00 GMT, press conference at 19:30

To cut in March or not to cut?

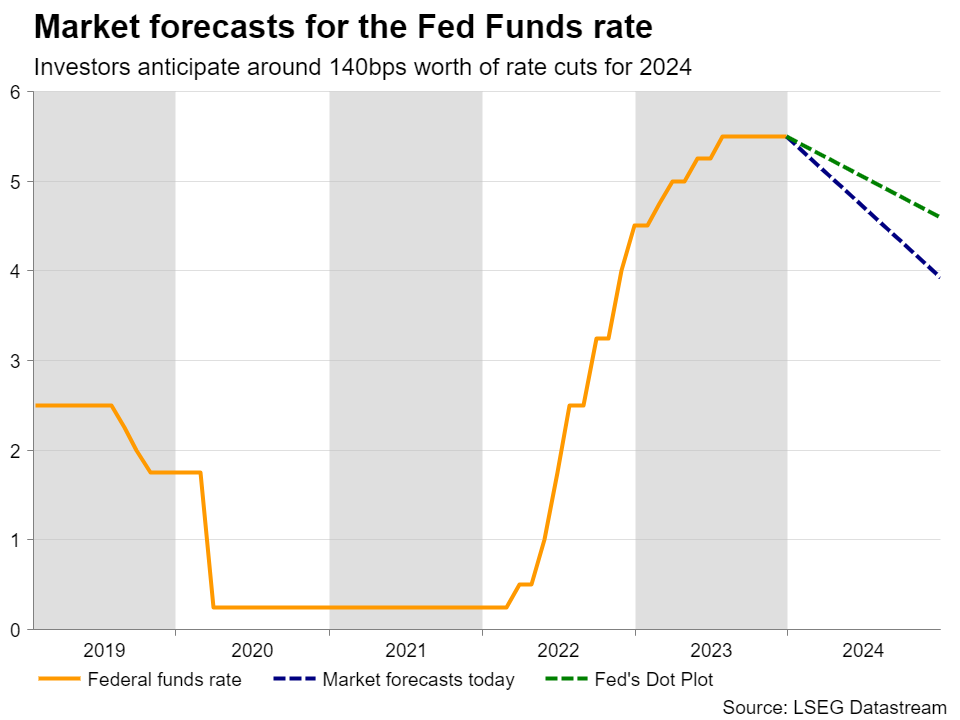

There has been a notable repricing regarding the Fed’s future course of action since the beginning of 2024. From fully pricing in a 25bps cut in March, investors are now assigning around a 50% for such a move, despite former St. Louis Fed President James Bullard recently saying that he expects the Committee to start lowering interest rates as soon as March.

It seems that the reason why investors were not particularly shocked by Bullard’s remarks was that he is not a rate setter anymore. They likely preferred to wait for Wednesday’s FOMC decision, where they could get clearer and more valid information regarding the Fed’s thinking.

Market still more dovish than the Fed

At its December gathering, the Committee revised down its interest rate projections, with the median dot for 2024 being dragged down to 4.6% from 51%. Yet, despite lifting their own implied path lately, market participants still expect borrowing costs to end the year lower, at around 3.93%. Perhaps their view was affected by Powell raising the question of when it may be appropriate to start lowering rates at the presser following the last meeting.

What encouraged traders to dial back some of their rate cut bets at the turn of the year may have been upside surprises in US economic data, but also remarks by Fed officials who pushed against an imminent rate reduction. Even Waller, who was the first policymaker to officially talk about the possibility of rate reductions, recently said that they should not rush into cutting interest rates until low inflation is sustained.

Data point to improving economic activity

After the December gathering, the CPI report revealed that headline inflation rebounded in December, while the core rate slid by less than expected. Retail sales for the same month came in better than expected, with both the headline and core rates coming in at double their November prints, while the flash PMIs for January pointed to further improvement in business activity, with the composite index rising to 52.3 from 50.9. Adding to the bright picture, the first GDP estimate showed that the US economy grew by much more than anticipated in Q4.

With all that in mind, it seems that there is room for further upside adjustment to the market’s implied path should data and headlines continue to corroborate the view that the world’s largest economy can withstand high interest rates for longer. But will the Fed signal this when it meets on Wednesday?

Fed to stand pat, spotlight to fall on guidance

The Committee is widely expected to keep interest rates untouched and so, the big question is whether they will push back against or leave the door open to imminent rate reductions. Given that no updated economic projections will be released at this gathering, investors may seek answers in the accompanying statement and from Fed Chair Powell at the press conference. It is worth mentioning that in the minutes of the December meeting, it was noted that the future policy path will depend on how the economy evolves and that most policymakers wanted to keep borrowing costs high for “some time.”

With improving economic numbers succeeding one another lately and inflation rebounding somewhat, Fed officials may not opt for rate reductions anytime soon in order not to risk letting inflation spiral out of control again. Thus, they may pour more cold water on rate cut speculation, which could allow Treasury yields to continue their recovery and thereby the US dollar to gain.

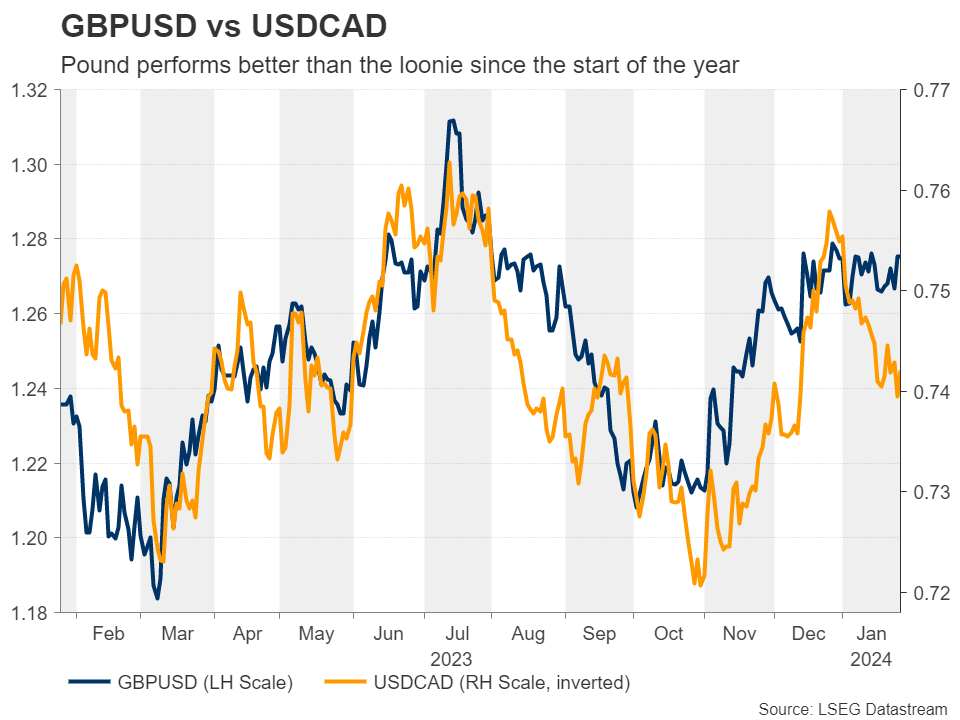

Will dollar/loonie continue trending north?

Having said all that though, with Treasury yields in some other major economies also rising and risk appetite remaining elevated, the dollar may not dominate across the board. For example, any gains against the British pound could stay limited if the BoE continues to refuse talking about rate cuts. Given the BoC’s dovish stance on Wednesday, the greenback may perform better against the loonie.

From a technical standpoint, dollar/loonie rallied after the BoC decision, but pulled back on Thursday, perhaps due to the rising oil prices. However, the pair continues to trade well above a prior downtrend line taken from the high of November 1.

A potential rebound from near the 1.3415 zone could initially aim for the recent peak of 13535, the break of which would confirm a higher high and allow extensions towards the 1.3620 territory, marked by the high of December 7.

Now, in case the Fed stresses that the rebound in inflation was solely due to base effects and that prices will slow again soon, then the market may be tempted to lift back up the probability of a March rate cut, which could result in a larger slide in dollar/loonie, perhaps towards the 1.3340 area.

Week Ahead – Fed and BoE Decisions, NFP Report, Eurozone GDP Incoming

- It’s a packed week ahead with key central bank decisions and big data releases

- Will the Fed (Wednesday) and Bank of England (Thursday) signal rate cuts?

- US jobs report, Eurozone GDP & CPI will also be crucial

- Plus, Aussie inflation and an OPEC meeting

Fed meets: more pushback or a cautious green light?

The Federal Reserve’s January policy meeting will undoubtedly be the highlight of the coming week as investors remain convinced a dovish pivot is drawing closer. Speculation about the timing and scale of rate cuts by the Fed have been the dominant market theme for some time now. The soundbites from Fed officials in the run up to Wednesday’s decision have been on the hawkish side and market pricing has become better aligned with the Fed’s guidance, but nevertheless, there is still a significant gap that needs to be closed.

With no change in policy anticipated and no dot plot to dissect, investors will be watching for any fresh hints on the timing of the first rate reduction by Chair Powell in his press conference. Powell will probably steer away from giving a precise timeline for cutting rates, while attempting to dampen expectations for a policy shift as early as March. However, it’s also unlikely that Powell will want to completely rule out a cut in the first half of the year and this would be supportive of risk assets and possibly negative for the US dollar.

Will Powell and jobs data be on the same page?

But the Fed will not have the final say on the dollar’s direction as the latest nonfarm payrolls report is due on Friday. Despite fears that higher rates would lead to a massive jobs cull, everything for now seems to point to a soft landing in the labour market, which would almost certainly translate to the same for the US economy.

After unexpectedly heating up in December, the jobs market likely cooled in January. Employment is projected to have risen by 162k versus 216k in the prior month. The unemployment rate is forecast to stay unchanged at 3.7%, while average hourly earnings are expected to maintain a moderate pace, growing by 0.3% month-on-month in January.

Aside from the NFP report, there’s a raft of other releases to keep an eye on. The home price index by S&P CoreLogic Case-Shiller will kick things off on Tuesday and the latest consumer confidence gauge is also due the same day as well as the JOLTS job openings for December. The Chicago PMI and the ADP private employment survey will follow on Wednesday. On Thursday, the closely watched ISM manufacturing PMI is expected to hold steady at 47.4 in January, and finally on Friday, factory orders for December will wrap up the week.

Another upside surprise in the headline payrolls print would not bode well for those betting on an early rate cut and the dollar could spike up in a knee-jerk reaction in such a case. However, unless there’s a very large beat, a solid number would probably not sway rate cut expectations dramatically if the other data aren’t as equally strong and more importantly, if Powell strikes a balanced tone.

Bank of England to take a dovish turn

The Bank of England meets on Thursday to set policy for the first time in 2024. Like the Fed and ECB before it, the BoE is widely expected to keep interest rates on hold as inflation in the UK, whilst falling, remains far above the BoE’s 2% target. Nevertheless, the February meeting could mark a turning point for the central bank’s fight against inflation as the BoE may drop its tightening bias and the three MPC members that had continued to vote for a hike even after the pause in September may end their dissent.

Such a move would signal the first step towards an eventual rate cut and comes after the tumble in headline CPI in October and November. The pound could weaken in the immediate aftermath, but a neutral stance would not alter much the view that the BoE won’t be as aggressive as the Fed and ECB in slashing rates this year.

Yet, despite Governor Andrew Bailey being somewhat firmer than his counterparts lately in reinforcing the message that rates would have to stay higher for longer, there is a small possibility of a dovish surprise. Should the Bank’s updated economic forecasts point to inflation falling towards 2% quicker than earlier anticipated, policymakers may remove the emphasis on keeping policy restrictive “for an extended period of time”.

Moreover, if Bailey opens the door to a rate cut in his press briefing, sterling could come under more substantial pressure.

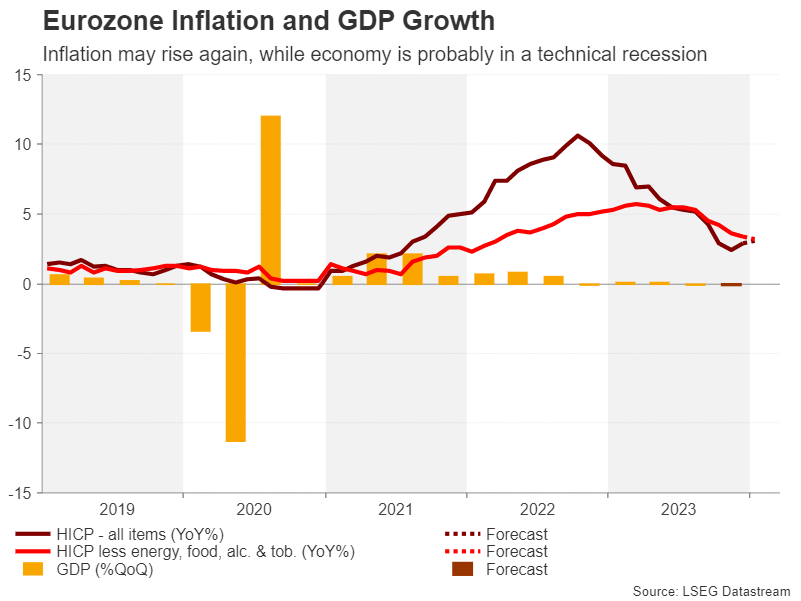

Eurozone economy probably in recession

The flash estimate of fourth quarter GDP growth in the euro area is out on Tuesday and may confirm what many suspect already. The Eurozone economy is expected to have contracted by 0.1% in the final three months of 2023, having shrunk by a similar proportion in the third quarter. This would put it in a technical recession, though the overall picture is one of stagnation rather than a full-blown downturn.

A worse-than-expected reading would likely hurt the euro and would place the currency on a negative footing whichever way rate cut expectations evolve after that. This is because a hawkish ECB would rekindle overtightening concerns against a weaker economic backdrop, while a dovish shift would only fuel all the rate cut speculation.

Just as critical for the euro will be Thursday’s flash CPI numbers. Headline inflation in the bloc edged up from 2.4% to 2.9% y/y in December as the effect of lower energy prices dropped out of the calculations. A further increase is forecast for January, with CPI predicted to climb to 3.1% y/y.

However, this might not necessarily prompt investors to reassess their bets of ECB policy easing as the uptick is expected to be temporary, hence, any boost for the euro could be limited.

Aussie eyes CPI data and Chinese PMIs

Moving to the Asia-Pacific region, the Australian dollar will be keeping tabs on some domestic and Chinese indicators. There’s been some good news for China-sensitive currencies like the aussie in the past week as Beijing has stepped up efforts to support the economy via more lending as well as boost the local stock market.

Chinese releases in the coming week will mainly comprise the manufacturing surveys for January due on Wednesday (official PMI) and Thursday (Caixin PMI). But for aussie traders, the quarterly CPI figures out of Australia on Wednesday will be a bigger priority.

The RBA meets on February 6 so the CPI data could provide vital clues as to whether or not Governor Michele Bullock will tone down her hawkish rhetoric. Australia’s inflation rate stood at 5.4% y/y in the third quarter and analysts are looking for a decline to 4.3% in Q4. A larger-than-forecast fall would be negative for the aussie.

Will BoJ Summary reveal anything new?

In Japan, the latest stats on unemployment (Tuesday), industrial production and retail sales (Wednesday) are on the agenda. But for the yen, the focus will be on the Bank of Japan’s Summary of Opinions of the January meeting, which is published on Wednesday.

Governor Ueda sounded more upbeat about the prospect for higher wages and hitting the 2% inflation goal after the meeting. Any further hints in the summary about policymakers edging closer to exiting negative interest rates could bolster the yen.

OPEC+ to stay the course

Lastly, OPEC and non-OPEC countries are scheduled to hold an online meeting on Thursday to discuss production quotas. It will be the cartel’s first gathering after Angola’s departure in December. OPEC+ members are unlikely to announce any changes to output in February as the production cuts of 900,000 barrels a day agreed last November only came into effect in January.

But any signs of disagreements or difficulty by some countries in meeting the quotas could raise further doubts about additional cuts later in the year, weighing on oil prices.

Weekly Focus – No New Signals from Central Banks

As expected, the ECB kept rates unchanged and did not provide new guidance. At the press conference, President Lagarde said that she stands by her earlier comments that rate cuts could come in the summer. We continue to expect the first cut in June, followed by two more 25bp cuts later this year, but acknowledge that risks are tilted towards earlier cuts, see ECB Review - Didn't rock the boat, but sailing towards a rate cut, 25 January. The ECB Bank Lending Survey published on Tuesday confirmed further tightening of credit standards and a decline in loan demand, while EA January flash PMIs were mixed with manufacturing activity topping expectations and momentum in services disappointing.

Earlier this week, Bank of Japan (BOJ) kept its quantitative and qualitative easing with yield curve control policy unchanged as expected. We expect the BOJ to start normalising policies at the April meeting when they are more certain that wage growth will pick up. Also, Norges Bank (NB) unanimously decided to leave policy rates unchanged, fully in line with consensus expectations and market pricing. We expect NB to keep policy rates unchanged in March and deliver five rate cuts this year starting in June, see RtM Norway: Norges Bank Review - Unchanged - we still expect the first cut in June, 25 January.

In China, the PBOC pre-announced a cut in the reserve requirement ratio (RRR) for banks of 0.5 percentage points effective from 5 February. The PBoC also signalled more easing was on the way by stating that the RRR rate is still relatively high and that the policy pivot by the Fed would expand their policy space. The rising US-China policy rate spread has been a concern for PBOC as it could destabilise the CNY.

Turkey's CBRT finalised its hiking cycle by raising its policy rate to 45% as expected. We do not expect further hikes, but rates will most likely remain high for some time, as the monthly momentum for inflation has declined but headline inflation remains above 60%.

In geopolitics, Sweden took an important step towards becoming a NATO member country after the Turkish parliament finally approved Sweden's accession bid. Hungary's Prime Minister Viktor Orbán was quick to announce that his government would also support the ratification of Sweden's accession. However, Hungary's parliament is on a winter break until 26 February. Read more about the latest developments in our monthly Geopolitical Radar - Political status quo in Taiwan, truce hopes rise in Gaza, 25 January.

Next week, all eyes will be on the FOMC meeting on Wednesday. We think the Fed is in a comfortable position with regards to both sides of its dual mandate, read more in Research US: Fed preview - Patience and Gradualism, 26 January. The US economy remains on a strong footing as confirmed by Q4 GDP data as the US economy grew by 3.3% AR. This week, the Fed decided to raise the lending rate on new loans in its emergency lending program and announced that the program would end in March.

The key data release next week will be EA inflation on Thursday. We will also pay attention to country-specific releases starting on Tuesday. In China, official PMIs are due on Wednesday, and the Caixin manufacturing survey on Thursday. In the US, the Michigan survey on Friday will shed light on consumer sentiment and inflation expectations.