Sample Category Title

WTI Oil Technical: Approaching a Key Medium-term Resistance, At Risk of Mean Reversion Decline

- WTI crude oil has started to evolve into a short-term uptrend phase reinforced by the recent liquidity infusion by China’s central bank, PBoC upcoming 50 bps cut on the RRR.

- The current 5-day rally of WTI crude oil has reached a key medium-term resistance zone of US$79.00/79.40 with a short-term overbought condition.

- At the risk of a minor mean reversion decline with intermediate supports at US$75.30 and US$74.80.

Benchmark oil prices have bottomed and traded higher since the start of this week as the West Texas Oil (a proxy of WTI crude oil futures) had rallied by +4.9% week-to-date at this time of the writing, its best weekly gain since the 9 October 2023.

On top of the rising geopolitical risk premium that is supporting firmer oil prices from the ongoing tensions in the Middle East region and Red Sea shipping route, the additional liquidity infusion from China’s central bank (PBoC) with an upcoming 50 bps cut on commercial banks’ reserve requirement ratio has also triggered an indirect “demand-pull” catalyst on oil prices.

CTA funds may have contributed to the current bullish momentum frenzy

All in all, these factors have created short-term reflexive positive feedback into the oil market reinforced by possible speculative CTA funds that run on momentum-driven models that piled into oil futures with a bullish bias.

The price actions of the benchmark Brent and WTI crude oil have pierced above their respective 50-day moving averages on Monday, 22 January and have capped their prices previously since late October 2023; positive momentum begets positive momentum.

At the risk of a minor mean reversion decline below US$78.40

Fig 1: West Texas Oil medium-term trend as of 26 Jan 2024 (Source: TradingView, click to enlarge chart)

Fig 2: West Texas Oil minor short-term trend as of 26 Jan 2024 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the recent push-up of West Texas Oil since the start of this week has led its hourly RSI momentum indicator to hover close to an extremely overbought level of around 74 in place since 12 January 2024.

This current overbought condition has also taken form as its price action is now coming close to a key medium-term resistance zone of US$78.00/78.40 (upper boundary of the minor ascending channel from 17 January 2024 low & close to the key 200-day moving average).

Therefore, the odds have increased for a potential minor mean reversion decline to retrace a portion of the ongoing short-term uptrend phase with the next intermediate supports coming in at US$75.75/75.30 and US$74.80.

On the flip side, clearance above the US$78.40 pivotal resistance invalidates the mean reversion decline scenario for a continuation of the bullish trend towards the next intermediate resistance at US$79.75 in the first step.

ECB’s Kazaks cautions against hasty rate cuts

ECB Governing Council member Martins Kazaks emphasized a cautious approach to reducing interest rates in an interview with BloombergTV. He acknowledged that while a downward adjustment in rates is anticipated, the ECB should not hasten this process, cautioning against premature actions that could potentially rekindle inflation.

Kazaks drew parallels to historical instances, particularly from the 1970s and 80s, to underline the risks associated with relaxing monetary policy too soon. "There's the risk that inflation starts to come back and then one would need to raise rates much more," he added.

Regarding, the timing and magnitude of easing cycles, he indicated that ECB could opt for either smaller steps initiated earlier or larger steps taken at a later stage. But Kazaks emphasized that would be "all data dependent".

Money Markets Added to ECB Easing Bets

Markets

ECB president Lagarde’s “I stand by the comments made in Davos” did little to impress markets. They even interpreted it the other way around as if the ECB chair went slightly off-script at the World Economic Forum (“summer seems to be right time to start cutting policy rates”). Comments about downside economic risks, a downward trend in underlying inflation and declining wage growth only added to the feeling that the central bank wants to keep all options open. That is obviously after the April policy meeting as they rather forcibly committed to wanting to see the outcome of Q1 wage negotiations first. Money markets added to policy easing bets, fully discounting an April rate cut (not our preferred scenario) and discounting a cumulative 50 bps rate cuts by June and almost 150 bps by the end of the year. That’s more or less equal to a 25 bps rate cut at each and every meeting starting in April. German Bunds outperformed US Treasuries. Daily changes on the German yield curve ranged between -9.3 bps (2-yr) and -2.4 bps (30-yr). US yields followed the move south with daily changes varying between -3.8 bps (30-yr) and -8.8 bps (3-yr) despite another strong quarterly GDP figure. Q4 growth beat consensus at an annualized 3.3% (vs 2% forecast) with another strong contribution of personal consumption (2.8%). We believe that US Treasuries followed Bunds higher because yesterday’s display by ECB Lagarde will likely see a repeat in Powell’s testimony next week given that the Fed Chair wasn’t even fighting market expectations back in December. US money markets attach a 50% probability to a March rate cut. In FX space, the single currency lost out after Lagarde’s unconvincing performance. EUR/USD closed at 1.0846 after testing the YTD low at 1.0822. Our bias remains for a weaker EUR/USD with 1.0724/12 the important reference (Dec 2023 low and 62% retracement on Q4 rally). EUR/GBP closed before the December low of 0.8549, with the downside of long-standing sideways range at EUR/GBP 0.8493 coming ever closer in the run-up to next week’s Bank of England policy meeting. Stock markets added another victory lap with key European and US benchmarks closing up to 0.5% higher. Today’s eco calendar is empty apart from December US PCE deflators. Those shouldn’t come as a surprise though as they can be derived from yesterday’s GDP data. The countdown to next week’s Fed gathering starts and we don’t expect an immediate reversal of the post-ECB market moves.

News & Views

In an interview with radio broadcaster Inforadio, Hungarian Finance Minister Mihaly Varga said that Hungary won’t be able to reduce the budget deficit to 3% this year. This will probably only be possible by 2025. Varga specified the government needs to balance the budget without hindering economic growth. In this respect, reducing the budget deficit from 6% to 3% in one year would make growth that just has started to recover very difficult. Trying to reach the target would require a HUF 2700bn (€7bn) adjustment. Varga clarified that this assessment is his personal opinion, not an official viewpoint of the government.

Tokyo price inflation, which is seen as a precursor for the national data, eased substantially this month. CPI ex fresh food dropped back below the BoJ’s 2% target, declining from 2.1% in December to 1.6% January (vs 1.9% forecast). This was the lowest reading since March 2022. The decline was mainly driven by energy prices. Still, the core measure ex-fresh food and energy also slow to 3.1% from 3.5%. However, the picture on Japanese price trends is not unequivocal. National services PPI grew by 2.4% Y/Y in December, holding at the highest level since 2015. In the meantime, the Minutes of the BoJ December policy meeting revealed that policymakers considered it important for the MPC to deepen discussions on the timing of the exit from current monetary policy and on the appropriate pace of raising policy interest rates thereafter. However, there are still quite different views within the MPC on the path for monetary policy going forward. Some members indicated that the BoJ can maintain substantial monetary easing even after ending the negative policy rate and yield curve control. After jumping higher earlier this week, the 10y Japanese bond yield today eases slightly (0.72%). The yen is unchanged at USD/JPY 147.8.

Markets Price Higher Probability of ECB Rate Cut in April

In focus today

US December Private Consumption Expenditures (PCE) data will be released today. Strong holiday spending and modest inflation suggest that real consumption volume continued to grow at a solid pace. On the inflation side, consensus sees Core PCE inflation at +0.2% m/m SA (from +0.1%).

We will get the December release of Norwegian retail sales. Retail sales picked up in November partly due to some 'Black week'-effects. Still, it seems as Christmas shopping held up in December as well, so we expect retail sales rose 0.2 % m/m.

We will also get retail sales from Denmark.

A triplet of December data is out from Sweden this morning including the labour force survey, foreign trade balance and household lending. The first two will give important input to the development of Q4 GDP, the latter should add colour about lending growth but we doubt there will be any signs of acceleration yet.

We wish you a happy Friday and a good weekend!

Economic and market news

What happened overnight

From Japan, we got Tokyo CPI Ex-Fresh Foods for January. The figure fell from 2.1% in December to 1.6% in January, which was lower than market expectations at 1.9%. It is the first time in 20 months that the number is below 2%. Earlier this week the Bank of Japan (BOJ) governor Ueda signalled that monetary policy would be tightened this year. However, if inflation continues easing it would give BOJ incentive to move more cautiously.

What happened yesterday

ECB kept policy rates unchanged at yesterday's policy meeting in line with both ours and the market expectations. President Lagarde said that it was still too early to discuss rate cuts. On the other hand, she also sounded soft on inflation and wage pressures. Markets reacted by adding to rate cut expectations for the April meeting (23bp priced vs 16bp prior to the meeting). We stick to our call of the first rate cut in June, albeit highlighting our long-held risk bias for an April meeting cut, for more details see ECB review - Didn't rock the boat, but sailing towards a rate cut, 25 January

Norges Bank kept policy rates unchanged as expected on Thursday's policy meeting, which was fully in line with expectations. Norges Bank signalled that policy rates will likely be kept at that level for some time ahead. As expected, Norges Bank kept the door open to further hikes as the economic outlook is broadly unchanged relative to the last meeting in December. We expect NB to keep policy rates unchanged in March and deliver five rate cuts this year starting with the monetary policy meeting in June.

US flash GDP growth came in at 3.3% Q/Q (annualized) in Q4, markedly above consensus expectations at 2.0%. This marks another clear upside surprise on the US macro data front. Recent data releases (GDP, Retail Sales, PMIs) all suggest that the US economy remains in a solid state. US yields edged lower over the afternoon, likely reflecting other factors such as the dovish ECB signals and the uptick in weekly jobless claims (For more details see Research US - Fed preview: Patience & gradualism, 26 January.

The Central Bank of Turkey hiked its policy rate by 250bp to 45% as expected. The committee now assesses that the monetary tightness required to establish the disinflation course is achieved and that this level will be maintained as long as needed. Hence, we do not expect further rate hikes but rates will most likely remain high for some time.

German Ifo was weaker than expected in January like the PMIs yesterday. Current assessment fell to 87.0 (cons: 88.5, prior: 88.5) and expectations fell to 83.5 (cons: 84.8, prior: 84.2). The price expectations rose across services, manufacturing and namely retail.

Equities: Global equities were higher yesterday, with several indices in both Europe and the US closing near session highs. There was a lot of macro, monetary policy, and earnings information to digest, but the combination of a strong US GDP report and the absence of push-back to market pricing from Lagarde ended up setting the tone for equities. The negative standout was consumer cyclicals, which was dragged down by Tesla after disappointing earnings the day before. As a softer tone on the central reemerged and yields came lower, it boosted the appetite for small caps after a couple of weeks with large caps outperforming. In the US yesterday, Dow +0.6%, S&P 500 +0.5%, Nasdaq +0.2%, and Russell 2000 +0.7%. Asian markets are mostly lower this morning, with South Korea going against the trend. European futures are higher, while US ones are lower.

FI: European rates rallied from the front end, with 10y Bunds ending the day 7bp lower on the back of the ECB press conference. 10y Bunds reached 2.36% intraday before reacting to the ECB decisions and ended the day at 2.29%. Markets added 8bp of rate cuts to the end-2024 pricing, now pointing to 140bp this year.

FX: A dovish reading of the ECB decision and press conference pulled the EUR lower across the board including EUR/USD below 1.0850, EUR/JPY toward 160 and sent EUR/NOK and EUR/SEK closer to 11.30. Our long NOK/SEK trade from FX Top Trades 2024 breached parity and is 4.1% in the money. Meanwhile, EUR/DKK fell to 7.4550.

Germany’s Gfk consumer sentiment plummets to -29.7, hopes of recovery dashed

Consumer sentiment in Germany has taken a substantial downturn, reaching its lowest level since March 2023. The Gfk Consumer Sentiment Indicator for February sharply declined from -25.4 to -29.7, faring worse than the anticipated -24.3. This significant drop signals a reversal of the temporary improvement observed last month, which now appears to have been a fleeting pre-Christmas optimism.

Economic expectations in January plummeted to their lowest since December 2022, dropping from -0.4 to -6.6. Income expectations suffered a marked decline from -6.9 to -20.0, the weakest since March 2023. Concurrently, willingness to buy among consumers decreased from -8.8 to -14.8. Willingness to save has shown an increase, rising from 7.3 to 14.0, the highest level since August 2008. This suggests a shift in consumer behavior towards saving rather than spending.

Rolf Bürkl, consumer expert at NIM, remarked that the brief improvement in consumer sentiment witnessed last month was merely a transient spike. The decline in income expectations and willingness to buy, coupled with a growing propensity to save, have contributed to a significant setback in the Consumer Climate at the start of the year.

A Dream Comes True

The EURUSD traded south yesterday, as the European Central Bank (ECB) Chief Christine Lagarde reckoned that growth and inflation are slowing, while insisting that the rate cut decision will be data dependent. The pair cleared the 200-DMA support, fell to 1.0820, it’s a little higher this morning, but we are now below the 200-DMA and the ECB rate cut bets on falling inflation and slowing European economies remain the major driver of the euro weakness, with many investors now thinking that June could be a good time to start cutting the rates. Three more rates could follow this year.

Across the Atlantic, the US released its latest GDP update and the data was as good as it could possibly get. The US economy grew 3.3% in Q4 versus 2% expected by analysts. It grew 2.5% for all of last year –quite FAR from a recession. The consumer spending growth slowed to 2.8%, but remained strong on healthy jobs market and wages growth, business investment and housing were supportive and… the cherry on top: the GDP price index, a gauge of inflation fell to 1.5%. Plus, data from rent.com showed that the median rent rate declined in December, and that’s good news when considering that rents have been one of the major drivers of inflation lately, and they look like they are cooling down. In summary, yesterday’s US GDP data was the definition of goldilocks in numbers: good growth, slowing inflation. A dream comes true.

As reaction, the US 2-year yield fell below 4.30% and the 10-year yield fell below 4.10%. The strong numbers didn’t necessarily hammer the Federal Reserve (Fed) cut expectations given that inflation slowed! Investors are not sure that March would bring the first rate cut from the Fed – as the probability of a March cut is around 50%, but a May cut is almost fully priced in. Today, all eyes are on the Fed’s favorite gauge of inflation: core PCE – expected to have retreated to 3% in December. A number in line with expectations, or ideally softer than expected could further boost risk appetite.

What could go wrong?

Energy prices could go wrong.

Oil bulls finally got the positive breakout that they were looking for in oil prices. The barrel of American crude cleared the $75pb resistance and extended gains past $77pb on muddy geopolitical picture in the Middle East and on the back of a 9-mio barrel slump in US weekly oil inventories. The American crude tested the 200-DMA, near $77.50pb, to the upside but has so far been unable to take it out.

Moving forward: Positive momentum is building, the ample supply story has been broadly priced in and if Mid East tensions take over the market narrative, there is no reason to keep the oil bulls contained. The next natural target is the 200-DMA. If broken, oil bulls will challenge the $78.60, the major 38.2% Fibonacci retracement on September to December selloff and a breakout above this level will point at a medium term bullish reversal, and could pave the way for a further rise to the $80pb.

Market echoes

The US dollar index ticked higher yesterday, as the euro fell across board during ECB Lagarde’s presser. But any further weakness in today’s PCE numbers could limit the upside move in the dollar index and throw a floor under the EURUSD’s weakness around the 200-DMA.

It would sure be absurd if the Fed started cutting the rates with such a strong underlying US economy before the ECB, which, in opposition, deals with a serious economic slowdown across the euro area. But the Fed doesn’t (need to) decide based on other central banks’ actions. As such, a possible earlier Fed cut could slow down the euro depreciation but should not stop it.

In equities, the good data gave a positive spin to the S&P500 and Nasdaq 100, but Tesla’s 10% slump limited gains. Intel tumbled 10% in the afterhours trading following a disappointing forecast as it has hard time fighting back the all-strong Nvidia and AMD which are catapulted to the moon on the AI craze. The good news is, Nvidia and AMD lovers will barely react to Intel news.

Another Strong Batch of US Data, ECB Giving Little Away

US economic data continues to point to an economy that's doing very well despite the various headwinds including very high interest rates.

GDP data for the fourth quarter easily exceeded expectations, rising 3.3% on an annualized basis, adding to the increasing view that the US could be heading for a fairytale scenario, not just a soft landing.

We've spoken a lot about resilence in the US economy over the last couple of years but that the economy can continue to show such strength and low unemployment with interest rates so high and inflation falling back toward target is unbelievable.

ECB keeps its cards close to its chest

The European Central Bank left interest rates on hold on Thursday and claimed inflation is progressing towards its target, while giving no clear guidance on when interest rates will start falling.

We came into the new year with markets pricing in a March rate cut and that is now looking increasingly difficult. Even with a late pivot - which was always likely the strategy of the central bank - policymakers would have to signal that a rate cut is a live possibility over the next six weeks in appearances made between meetings. That's not impossible but it's arguably not particularly transparent. The data is unlikely to surprise to that degree.

President Christine Lagarde and some colleagues have previously indicated a rate cut in summer may be appropriate but investors are not convinced we'll have to wait that long. Lagarde stuck with that today while suggesting demand was weaker, as is the economy, and inflation is falling.

Perhaps this is her way of leaving the door slightly ajar for March or maybe the usual lack of clear guidance has left everyone desperately looking for something that isn't there. I get the feeling Lagarde and her colleagues wanted to give absolutely nothing away today, instead opting for an array of vague, uninformative statements that buy them six more weeks before they may have to say or do something.

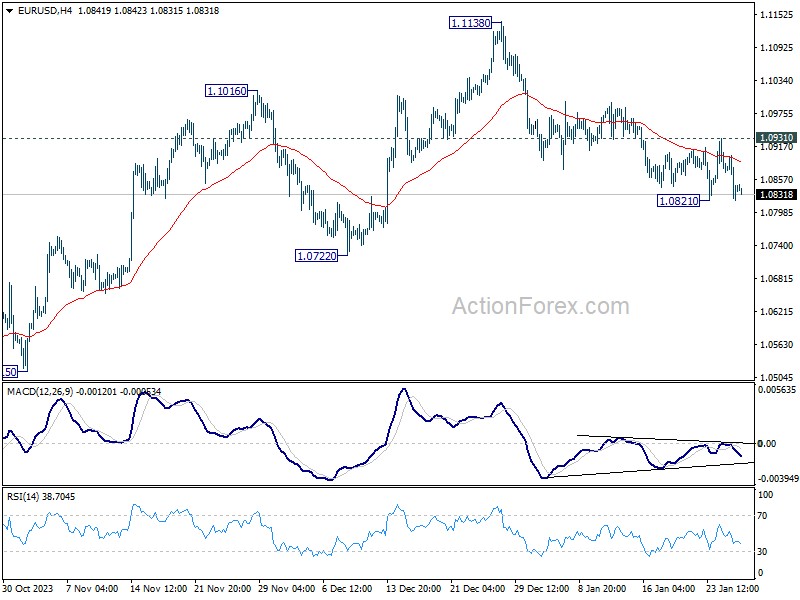

EURUSD remains rangebound

The euro has drifted lower after the ECB press conference and US data but it hasn’t broken out of the range it’s traded in over the last week or so.

The correction we’ve seen since the turn of the year appears to be running on fumes but there’s still a question of whether this is just that, and will turn higher and look to break the highs, or just a continuation of the longer-term sideways trend. There are some important support levels between 1.07 and 1.0850 which could tell us which is the case.

Bitcoin (BTCUSD) Looking for Support Soon

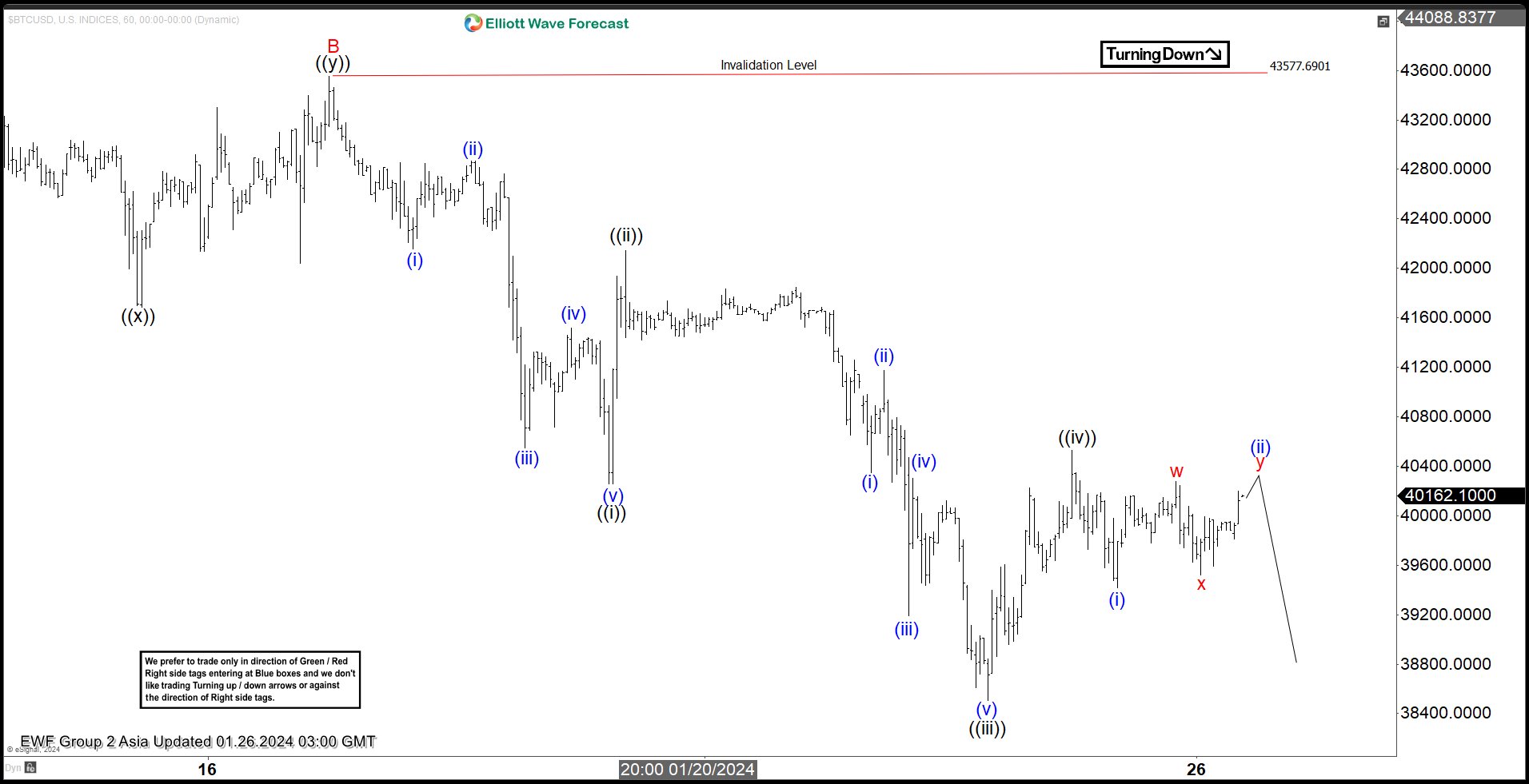

Short Term Elliott Wave view in Bitcoin (BTCUSD) suggests it is currently doing a pullback starting from 1.11.2024. The decline is taking the form of a zigzag Elliott Wave structure. Down from 1.11.2024 high, wave A ended at 41339 and wave B rally ended at 43577.69 as the 1 hour chart below shows. Wave C lower is currently in progress as a 5 waves. Down from wave B, wave (i) ended at 42158.6 and rally in wave (ii) ended at 42868.4. Wave (iii) lower ended at 40549.3 and wave (iv) rally ended at 41518.5. The instrument then resumed wave (v) lower which ended at 40256.6 and completed wave ((i)) in larger degree.

Rally in wave ((ii)) ended at 42143.3 and the crypto currency has resumed lower in wave ((iii)). Down from wave ((ii)), wave (i) ended at 40349.9 and rally in wave (ii) ended at 41173.8. Wave (iii) lower ended at 39190.1 and rally in wave (iv) ended at 40305.4. Bitcoin extended lower again in wave (v) towards 38503.2 which completed wave ((iii)). Rally in wave ((iv)) ended at 40526.3. The crypto currency is now in wave ((v)) lower and as far as pivot at 43577.69, 1 more leg lower still can’t be ruled out at this stage to end wave ((v)) of C. The right side / main trend for Bitcoin still remains bullish and thus we do not like short selling the instrument.

Bitcoin (BTCUSD) 60 Minutes Elliott Wave Chart

BTCUSD Elliott Wave Video

https://www.youtube.com/watch?v=qzhh5iV0y0U

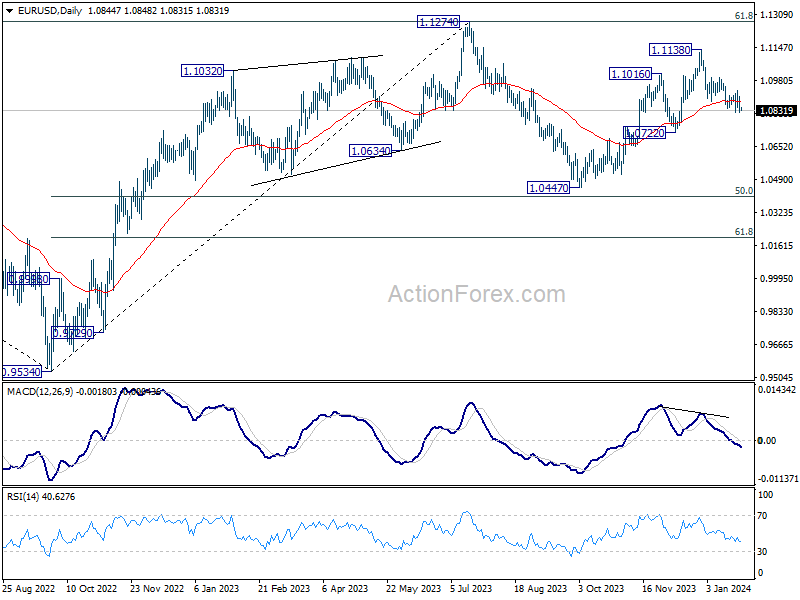

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0811; (P) 1.0857; (R1) 1.0891; More...

Intraday bias in EUR/USD remains neutral at this point, as range trading continues above 1.0821 temporary low. On the downside, break of 1.0821 will resume the fall from 1.1138 to 1.0722 support. On the upside, above 1.0931 will resume the rebound from 1.0821 towards 1.1138 resistance.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

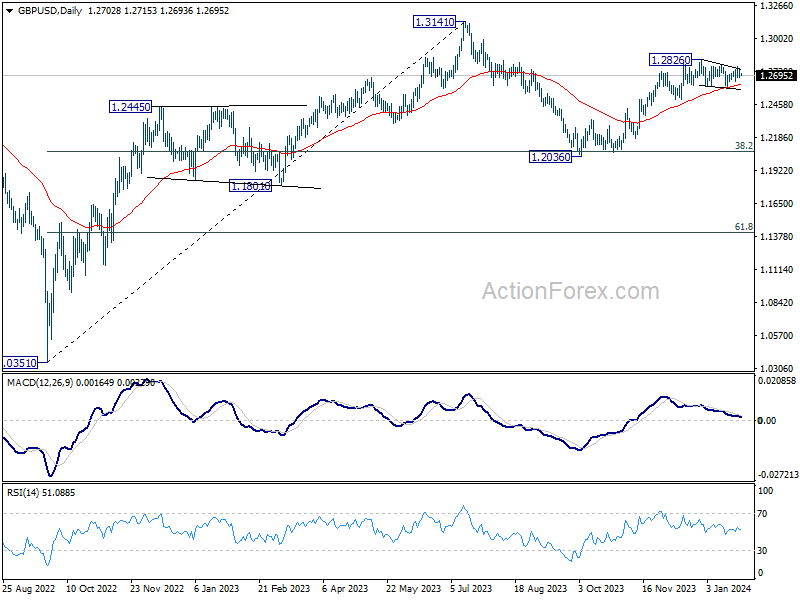

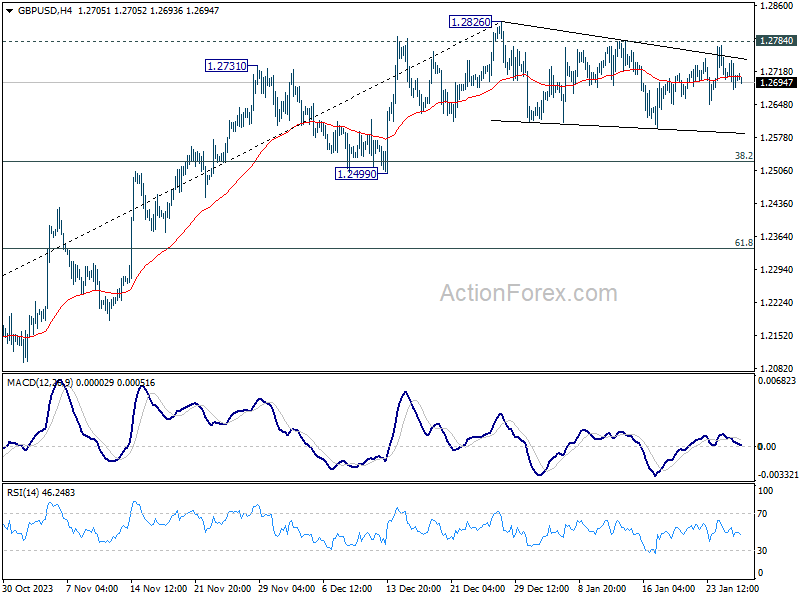

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2679; (P) 1.2711; (R1) 1.2740; More...

Range trading continues in GBP/USD and intraday bias remains neutral. Deeper pull back cannot be ruled out. But downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2784 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rise from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.