Sample Category Title

ECB Review: Didn’t Rock the Boat, But Sailing Towards a Rate Cut

ECB Review: Didn't Rock the Boat, But Sailing Towards a Rate Cut

- As widely expected, the ECB left its three policy rates unchanged at today's meeting, leaving its key policy rate (deposit rate) at 4%. Today's meeting was expected to be a stocktaking meeting with no new policy signals and the ECB delivered just that. The ECB confirmed that the incoming information was broadly in line with the staff projections laid out at the December meeting. We view today's assessment from the ECB as necessary but not sufficient for a rate cut.

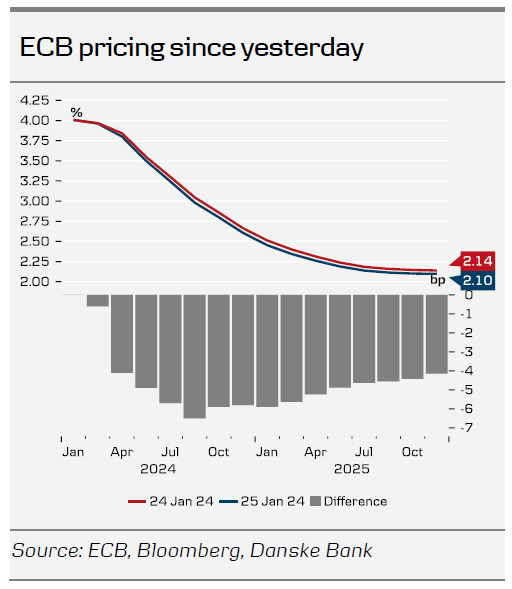

- While Lagarde said it was premature to discuss rate cuts, markets sent yields lower from the front end. Markets are pricing 20bp by the April meeting, which must be considered a live meeting. We stick to our call of a first rate cut coming in June, but highlight our long held risk bias of an April meeting cut. The question now is when/ how many there will come.

The road to rate cuts

The ECB gave no new policy signals today and Lagarde said that she stood by her comments made last week. Last week she said that the next rate change would likely be a cut and when asked whether this would be in the summer, she acknowledged that. Today's meeting will be remembered as another step in the process of the ECB delivering a rate cut.

Incoming data as expected but wage pressure is easing

Lagarde acknowledged that the incoming data since the December meeting have been broadly as expected. Hence, the ECB has not changed its assessment of the economic situation and the inflation outlook since the last meeting. Aside from the energy-related upward base effect on headline inflation, the declining trend in underlying inflation continued as past interest rates were transmitted forcefully into financial conditions. Yet, Lagarde noted that wage pressure has started to ease and that firms are absorbing wage increases by reducing profit margins instead of increasing prices. This was a slight change of communication in the soft direction compared to the December meeting. Regarding the wage growth, Lagarde highlighted that Indeed's wage growth tracker had stabilised at higher levels (and is primarily backward looking), and she also added that 40% of workers' wages will be renegotiated in the near term.

On the growth side the ECB expects that the economy stagnated in Q4 23, and Lagarde said that incoming data continue to signal weakness. However, she also noted that forward looking indicators point to a pickup in growth later this year but that the risks to the growth outlook are tilted to the downside.

April meeting may be a live meeting

Based on today's meeting, we stick to our call for the ECB to deliver its first 25bp rate cut at the June meeting, but we also repeat our long-held bias for risk of an earlier rate cut. We believe that if the ECB staff projections are revised lower, the ECB may deliver a cut already at the April meeting. The incoming data until then is plentiful with in particular inflation prints and wage growth being important, as well as the profit margin/ wage growth discussion (see above). If the January inflation next week surprises on the downside, markets will likely add to its already 20bp rate cut (cumulative). Today, Lagarde had the opportunity to push back on the market pricing and she choose not to, which led to a front-end driven rally. Markets are pricing 140bp of rate cuts until the end of this year. Lagarde said that the operational framework review will most likely be concluded by the end of spring.

EUR/USD moved lower to around the 1.0850 mark after the relatively dovish ECB meeting, which has made the April meeting live, combined with US macro data continuing to surprise to the upside, including strong Q4 flash GDP figures. We have recently discussed the possibility of a USD rally in Q1 due to stronger-than-expected US figures relative to the rest of the world. So far, this has played out well with strong US PMIs and Q4 GDP figures. We will have more clarity next week with releases such as ISM and nonfarm payrolls, in addition to the Fed meeting. Additionally, while we recognise that our Fed (first cut in March) and ECB (first cut in June) forecasts, all else equal, are positive for EUR/USD in H1, we believe that the broader pricing in the G10 could be more decisive for the cross, as we perceive current market expectations for rate cuts to be excessive. We still maintain our bias towards selling EUR/USD on rallies in the near term, and we forecast EUR/USD at 1.07/1.05 on a 6/12M horizon. We also remain short EUR/USD via a 6M put spread as part of our FX Top Trades 2024.

US: Economic Resilience Remains on Full Display in Q4 GDP Data

Real GDP expanded by 3.3% quarter-over-quarter (q/q, annualized) in the fourth quarter of 2023 – well ahead of the consensus forecast calling for a more modest gain of 2%. For the year, real GDP grew by an impressive 2.5%.

Consumer spending remained hot, rising 2.8% – a very modest deceleration from the 3.1% gain recorded in the third quarter. Gains were spread across both goods (+3.8%) and services (+2.4%).

Non-residential business investment rose 1.9%, with structures (+3.2%), equipment (+1.0%) and intellectual property products (+2.1%) all chipping in with modest gains. Residential investment also ticked higher by just over a percentage point.

Government spending increased 3.3%, as outlays rose at both the federal (+2.5%) and state & local (+3.7%) level.

After an outsized contribution in Q3, inventory investment slowed but still added a tenth of a percentage point to Q4 GDP.

Net exports also chipped in 0.4 percentage points to headline growth, as a healthy gain in exports (+6.3%) was eclipsed by a smaller gain in imports (+1.9%).

Key Implications

Wow! Economic growth ends 2023 with a bang, smashing expectations and stringing together two of the strongest back-to-back quarters in two-years. The details of the report were very supportive of the ongoing resilience, with domestic demand accounting for most of last quarter's gain.

With the economy holding up remarkably well and the labor market still tight by historical standards, policymakers can afford to proceed carefully over the coming months. Economic growth is still running well above its long-run potential, implying the near-term risks to the inflation outlook are skewed to the upside. From the Fed's standpoint, this means any imminent rate cuts are off the table, and policymakers are likely to remain on hold until at least this summer.

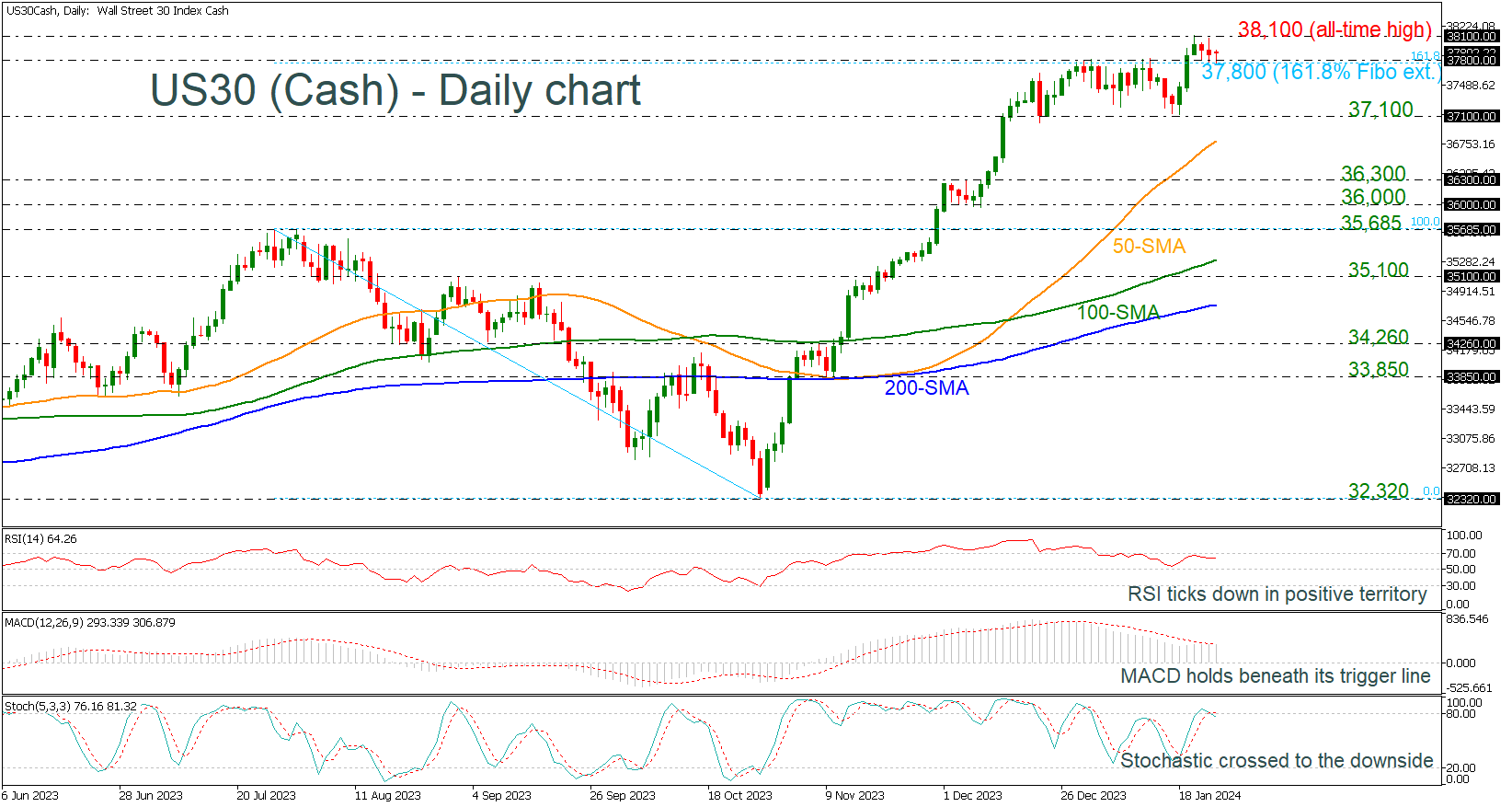

US 30 Index Retreats from Record Peak

- US 30 index finds support at 161.8% Fibonacci

- Technical indicators suggest bearish retracement

The US 30 index is easing from the all-time high of 38,108 and is meeting again the 161.8% Fibonacci extension level of the down leg from 35,685 to 32,320 at 37,800, which had acted as strong resistance over the last month.

Technically, the oscillators are indicating a negative correction. The RSI is retreating from the 70 level, while the MACD fell beneath its trigger line in the positive region. Moreover, the stochastic oscillator posted a bearish crossover within its %K and %D lines in the overbought area.

The market structure is negative in the very short-term picture as the price is currently moving lower. If the bears take the upper hand and the index, meets the 37,100 support. Selling forces could intensify towards the 50-day simple moving average (SMA) at 36,800. Then, additional losses from there could retest the 36,000 round number.

In the event the price stays resilient above the 161.8% Fibonacci extension of 37,800, the bulls might push for a close above the record high of 38,100. Therefore, a successful move higher could immediately shift the attention to the next round number of 39,000.

In a nutshell, the US 30 index may remain supported in the coming sessions, though room for improvement could be limited before the next bearish round takes place.

Sunset Market Commentary

Markets

The key events to watch today were the ECB policy decision and important US data. The main conclusion of the latter is that they, once again, underscore the resilience of the world’s largest economy. Quarterly growth in the last three months of 2023 came in at 3.3%, easily beating a 2% estimate. Beneath the headline figure, more strength appears with personal consumption contributing 1.91% to growth. Government consumption came in second (0.56%) and net exports third (adding 0.43%). Goldilocks supporters get exactly what they came for with the price indices showing a bigger deceleration than hoped-for. The GDP deflator decelerated from 3.3% to 1.5% in Q4 (2.2% expected). Core PCE came in at the anticipated 2% (unchanged vs the previous quarter). Durable goods data printed to the soft side of expectations in terms of the headline figure but printed a tad stronger in the core (and more important) readings. Weekly jobless claims rose a bit more than foreseen, to back above 200k. All of the latter data played second fiddle obviously. US yields quickly erased a kneejerk uptick (on the headline GDP outcome) after the market digested the inflation gauges. US rates lose between 4.4 and 5.5 bps across the curve. A May cut is cemented deeper.

The ECB policy decision was no surprise with steady rates and no tweaks to the statement or official guidance whatsoever. Its (December) medium-term inflation outlook has been broadly confirmed by incoming data. The central bank can stay put for the time being with “rates at levels that, maintained for a sufficiently long duration, will make a substantial contribution to this [reaching the 2%] goal.” The recent uptick in CPI was dismissed as energy-related while the underlying trend in core inflation has continued. Lagarde noted how almost all underlying gauges fell further in December in a remark that was picked up as dovish by markets. The ECB chair during the press conference reiterated that the discussion about rate cuts was considered premature. She said she stands by her comments made in the Bloomberg interview, referring to the summer as a broad timing for a first cut. However, she distanced herself from “the conclusions made by others” following that comment. Bloomberg, for one, afterwards reported that a consensus was building for a June cut. Considering Lagarde’s pushback today was not at all as convincing as it was last week, markets took that as another dovish hint. Total easing priced in for 2024 is now 140 bps compared to 129 bps prior to the press conference with chances for an April move rising to >80%. That’s despite Lagarde saying that she’s still waiting on important data which could take months before reaching Frankfurt, the outcome of wage negotiations to mention a critical one. The ECB does see encouraging signs of company profits absorbing the wage push higher. All in all, investors mainly draw some soft conclusions from the meeting. Supported by US spillovers, German yields decline between 2.5 and 8.1 bps. The front end outperforming. European stocks bottom out and even trade in the green (+0.3% for the EuroStoxx50). The euro loses ground against most peers. EUR/USD eases towards 1.086 and is probably lucky the US dollar is losing interest rate support as well.

News & Views

The Norwegian central bank kept its policy rate unchanged at 4.5% today, a level at which it will likely be kept for some time ahead. Both inflation and economic activity have been broadly in line with the projections in the December 2023 Monetary Policy Report. The krone is stronger than expected. If cost inflation remains elevated, or the krone depreciates again, inflation may remain high for longer than previously projected. In that case, the Monetary Policy Committee (MPC) is prepared to raise the policy rate again. If there is a more pronounced slowdown in the Norwegian economy or inflation declines more rapidly, the policy rate may be lowered earlier than envisaged in December. Norwegian markets didn’t respond to the decision. EUR/NOK changes hands around 11.37 with money markets attaching a 70% probability to a rate cut as soon as June.

The Turkish central bank (CBRT) raised its policy rate from 42.50% to 45%. Taking into account the lagged impact of monetary tightening, the MPC assesses that the monetary tightness required to establish the disinflation course is achieved and that this level will be maintained as long as needed. That is until there is a significant decline in the underlying trend of monthly inflation (2.93% M/M and 64.77% Y/Y in December for headline CPI) and until inflation expectations converge to the projected forecast range. The Turkish lira holds steady near record low levels just above EUR/TRY 33.

Risk Sentiment Revives on Strong US GDP, Euro Holds Its Ground Against Dollar Post-ECB

Commodity currencies bounce in early US session, spurred by unexpectedly robust US GDP data that has invigorated stock futures. This surge in risk appetite is exerting some pressure on Dollar, although the impact remains relatively contained for the moment. The sustainability of this risk-on sentiment is still in question, which will be critical for the next move in currencies too. Yen, meanwhile, is also rebounding, benefiting from retreat in benchmark US and European treasury yields. Despite these movements, major currency pairs involving the Yen remain within familiar ranges, indicating ongoing market caution.

Euro is maintaining its ground against Dollar but is showing signs of weakness against other major currencies, which is mirrored by Sterling and Swiss Franc too. ECB President Christine Lagarde noted, at the post-meeting press conference, there was consensus in the Governing Council that it's "premature" to start discussing interest rate cuts. Furthermore, when probed about potential rate cuts in the summer, Lagarde emphasized that ECB is "data-dependent" rather than "time-dependent".

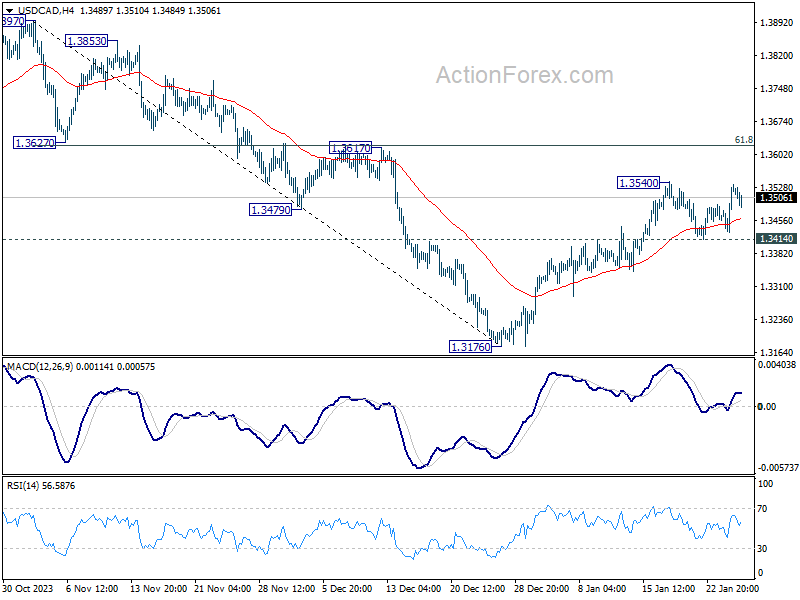

Technically, USD/CAD dips mildly after failing to break through 1.3540 resistance, but stays well above 1.3414 support. Further rally is in favor for now, and break of 1.3540 will resume the rebound from 1.3176 to 1.3617 cluster resistance next. However, break of 1.3414 will risk deeper pull back towards 1.3176 low instead.

In Europe, at the time of writing, FTSE is up 0.16%. DAX is up 0.04%. CAC is down -0.02%. UK 10-year yield is down -0.035 at 3.977. Germany 10-year yield is down -0.052 at 2.288. Earlier in Asia, Nikkei rose 0.03%. Hong Kong HSI rose 1.96%. China Shanghai SSE rose 3.03%. Singapore Strait Times fell -0.18%. Japan 10-year JGB yield rose 0.0269 to 0.749.

ECB stands pat, declining trend in underlying inflation continues

ECB left monetary policy unchanged as widely expected. Main refinancing, marginal lending and deposit rates are held at 4.50%, 4.75%, and 4.00% respectively.

In the accompanying statement, ECB noted that incoming information has "broadly confirmed its previous assessment of the medium-term inflation outlook. "Aside from an energy-related upward base effect", the declining trend in underlying inflation "has continued.

The central bank also maintained that current interest rates, "maintained for a sufficiently long duration", will make substantial contribution to bringing down inflation to target. Future policy decisions will follow a "data-dependent approach" to determine both the level of duration of monetary restriction.

US GDP grows 3.3% annualized in Q4, core PCE prices unchanged at 2%

US GDP grew 3.3% annualized in Q4, well above expectation of 2.0%. Looking at some details, consumer spending slowed from 3.1% to 2.8%. Goods spending slowed from 4.9% to 3.8%, but services spending growth rose from 2.2% to 2.4%. Gross private domestic investment growth slowed notably from 10.0% to 2.1%. Headline PCE prices slowed notably from 2.6% to 1.7%. Meanwhile, PCE core prices was unchanged at 2.0%.

Also released, initial jobless claims rose from 189k to 214k in the week ending January 19, above expectation of 199k. Goods trade deficit narrowed from USD -90.3B to USD -88.5B, versus expectation of USD -88.7B. Durable goods orders rose 0.0% mom in December, below expectation of 1.0% mom. But ex-transport orders rose 0.6% mom, above expectation of 0.2% mom.

Germany Ifo business climate falls to 85.2, stuck in recession

German Ifo Business Climate fell from 86.3 to 85.2 in January, below expectation of 86.7. Current Assessment Index fell from 88.5 to 87.0, below expectation of 88.6. Expectations Index fell from 84.2 to 83.5, below expectation of 84.9.

But sector, manufacturing rose from -17.4 to -16.0. Services fell from -1.7 to -4.9. Trade fell from -26.7 to -29.7. Construction fell from -33.5 to -35.9.

Ifo said, sentiment among German companies has deteriorated further at the beginning of the year. The German economy is "stuck in recession".

Japan downgrades export outlook, raises concerns over earthquake impacts

In the new Monthly Economic Report, the Japanese Government continues to observe that the economy is “recovering at a moderate pace”, even though it’s “pausing in part”. A significant shift in this report is the revised perspective on exports, now viewed as “appearing to be pausing for picking recently”. The report also calls for heightened vigilance regarding the economic repercussions of the 2024 Noto Peninsula Earthquake.

Apart from the change in export assessment and the earthquake’s impact, the report’s overall tone remained consistent with previous evaluations. Key economic indicators such as private consumption is characterized as “picking up”, although business investment appears to be “pausing”. Industrial production is also showing signs of recovery.

The report paints a positive picture of corporate health, noting improvements as a whole. The employment scenario reflects positive trends, with signs of ongoing improvement. Lastly, consumer prices have been identified as “rising moderately”

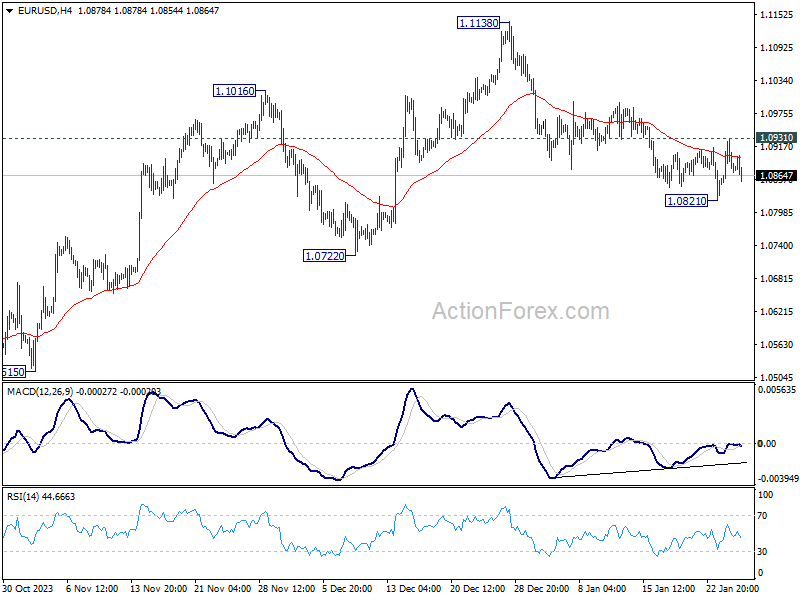

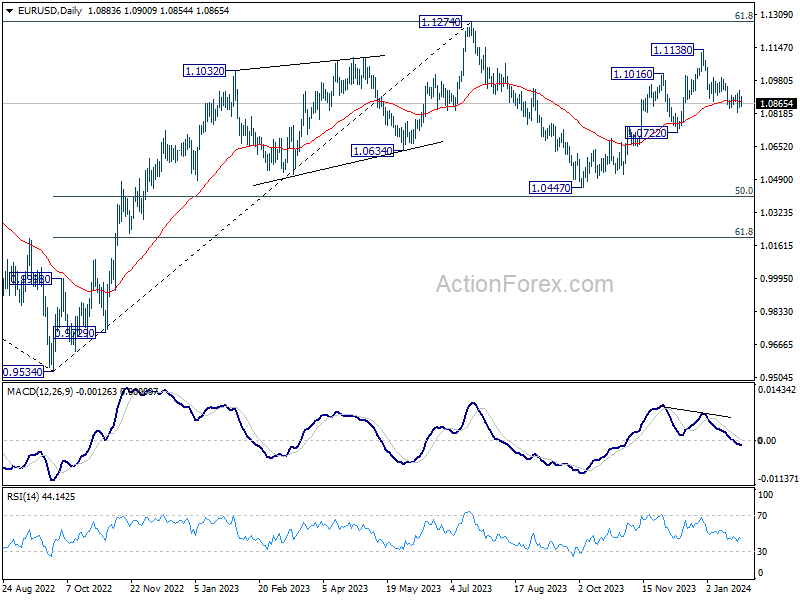

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0843; (P) 1.0888; (R1) 1.0929; More...

EUR/USD is staying in range above 1.0821 and intraday bias remains neutral. On the downside, break of 1.0821 will resume the fall from 1.1138 to 1.0722 support. On the upside, above 1.0931 will resume the rebound from 1.0821 towards 1.1138 resistance.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | RBA Bulletin Q4 | ||||

| 09:00 | EUR | Germany IFO Business Climate Jan | 85.2 | 86.7 | 86.4 | 86.3 |

| 09:00 | EUR | Germany IFO Current Assessment Jan | 87 | 88.6 | 88.5 | |

| 09:00 | EUR | Germany IFO Expectations Jan | 83.5 | 84.9 | 84.3 | 84.2 |

| 13:15 | EUR | ECB Main Refinancing Rate | 4.50% | 4.50% | 4.50% | |

| 13:30 | USD | Initial Jobless Claims (Jan 19) | 214K | 199K | 187K | 189K |

| 13:30 | USD | GDP Annualized Q4 P | 3.30% | 2.00% | 4.90% | |

| 13:30 | USD | GDP Price Index Q4 P | 1.50% | 2.20% | 3.30% | |

| 13:30 | USD | Goods Trade Balance (USD) Dec P | -88.5B | -88.7B | -90.3B | |

| 13:30 | USD | Wholesale Inventories Dec P | 0.40% | -0.20% | -0.20% | |

| 13:30 | USD | Durable Goods Orders Dec | 0.00% | 1.00% | 5.40% | |

| 13:30 | USD | Durable Goods Orders ex Transport Dec | 0.60% | 0.20% | 0.40% | |

| 13:45 | EUR | ECB Press Conference | ||||

| 15:00 | USD | New Home Sales Dec | 646K | 590K | ||

| 15:30 | USD | Natural Gas Storage | -322B | -154B |

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0843; (P) 1.0888; (R1) 1.0929; More...

EUR/USD is staying in range above 1.0821 and intraday bias remains neutral. On the downside, break of 1.0821 will resume the fall from 1.1138 to 1.0722 support. On the upside, above 1.0931 will resume the rebound from 1.0821 towards 1.1138 resistance.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

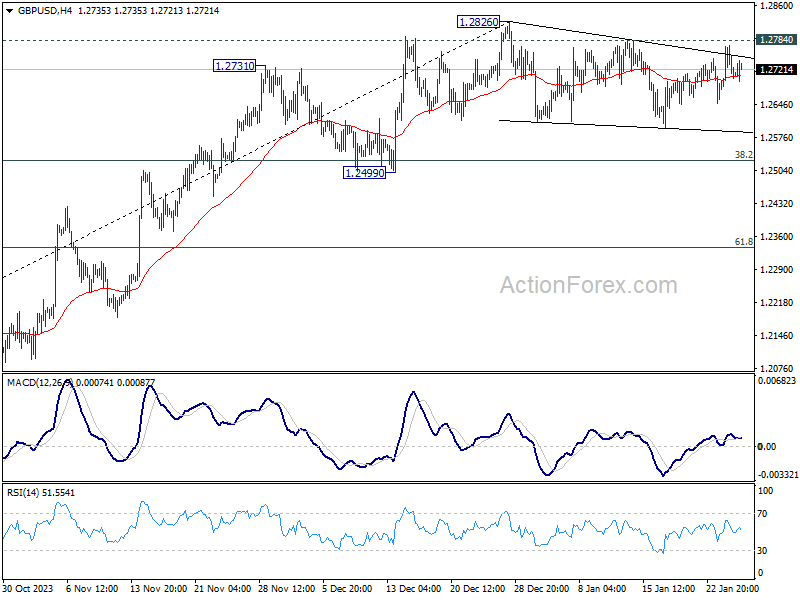

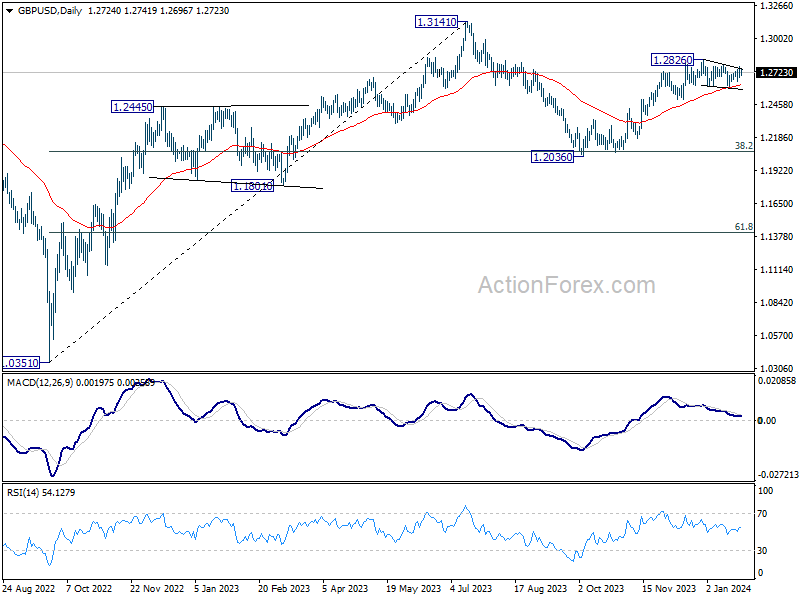

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2676; (P) 1.2726; (R1) 1.2774; More...

GBP/USD is still bounded in consolidation pattern from 1.2826 and intraday bias remains neutral. Deeper pull back cannot be ruled out. But downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2784 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rise from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

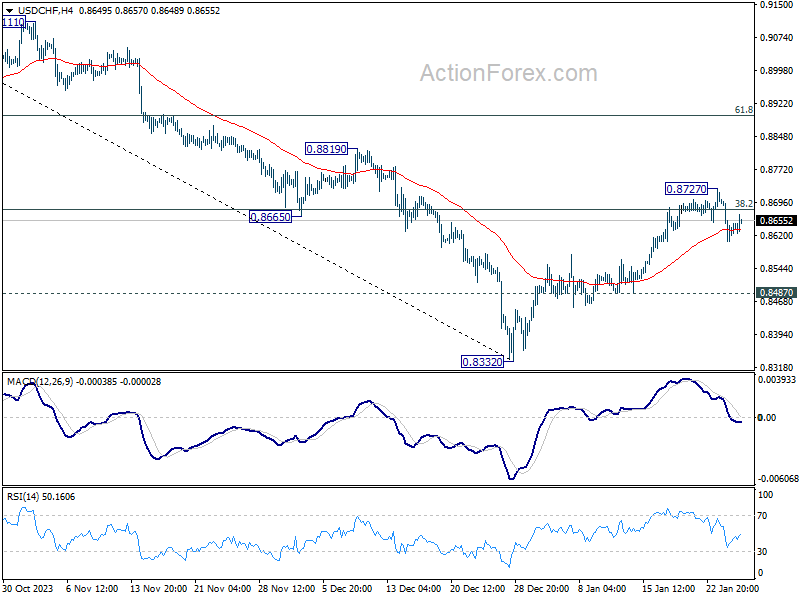

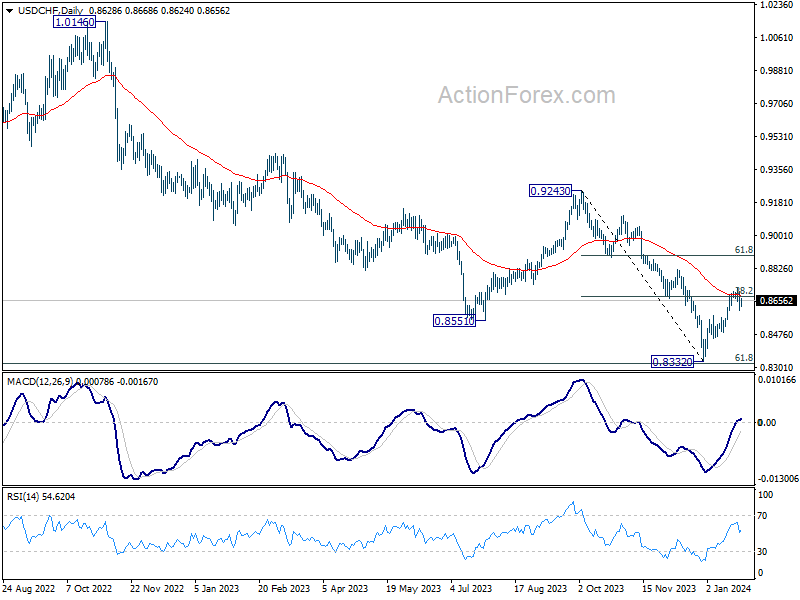

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8587; (P) 0.8648; (R1) 0.8690; More....

Intraday bias in USD/CHF is staying mildly on the downside. Fall from 0.8727 could extend to 0.8487 support. Break there will argue that rebound from 0.8332 has completed at 0.8727, after rejection by 55 D EMA (now at 0.8686). Deeper fall would be seen to retest 0.8332 low. On the upside, firm break of 0.8727 will resume the rebound to 61.8% retracement of 0.9243 to 0.8332 at 0.8995 instead.

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

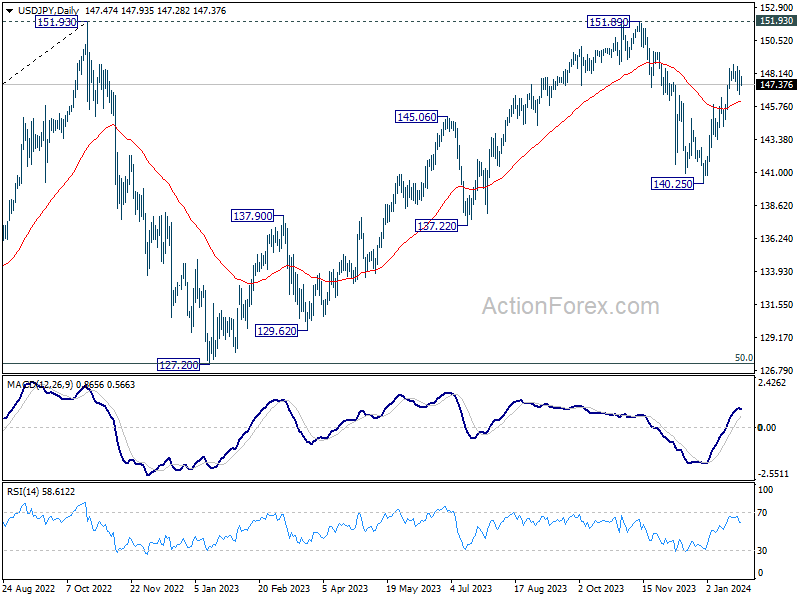

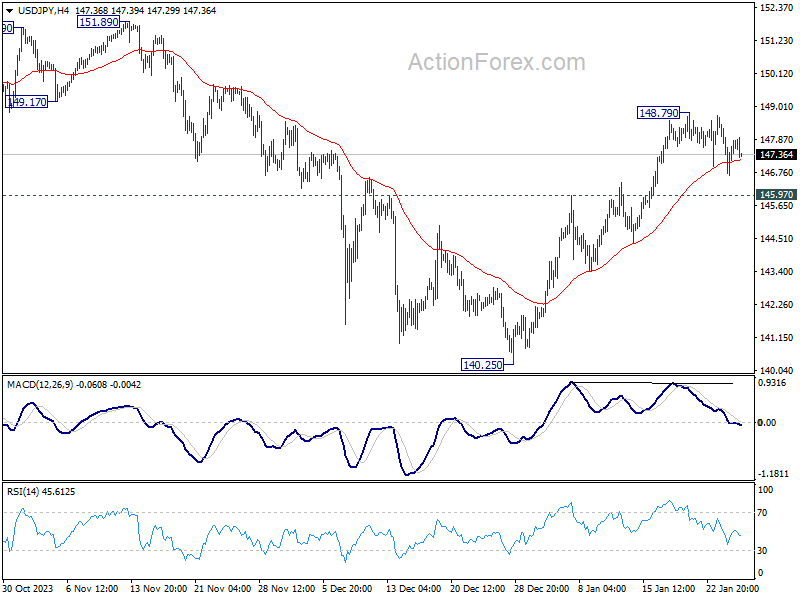

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.63; (P) 147.54; (R1) 148.44; More...

USD/JPY is still extending the consolidation from 148.79 and intraday bias remains neutral for the moment. Still, as long as 145.97 support holds, further rally is in favor. Corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.