Sample Category Title

Hang Seng Index Technical: Countertrend Rebound in Play But Not Major Bottoming

- Short-term positive animal spirits have resurfaced in China and Hong Kong stock markets stoked by additional liquidity injection from PBoC and the creation of a “stabilization fund”.

- Long-term prospects are still dim as a liquidity trap scenario cannot be ruled out in the real economy due to weak consumer and business sentiment.

- Watch the next intermediate resistances at 16,525 and 17,130 on the Hang Seng Index.

“Desperate times, calling for desperate measures” as China’s top policymakers are trying to stall the continuation of the horrendous decline seen in the China and Hong Kong stock markets since the start of the new year reinforced by China Premier Li Qiang’s speech in Davos last week that implied that China leadership is comfortable with the current pace of growth trajectory in China which in turn has dampened hopes of more forceful fiscal and monetary stimulus measures in 2024.

At the start of this week, the China and Hong Kong benchmark stock indices extended their losses with a decline of -2.3% seen on the Hang Seng Index, almost hitting the October 2022 low.

Additional liquidity injection from PBoC

Thereafter, a slew of stimulative policies has been announced in the past two days; the step-up progress of the establishment of a 2 trillion yuan “stabilization fund” to prop up China equities, and the upcoming 50 basis points cut on China’s major banks’ reserve requirement ratio (RRR) on 5 February before the Lunar New Year holidays; the steepest single RRR cut implementation in the past two years.

China and Hong Kong equities have managed to see a minor positive turnaround since Tuesday, 23 January as the CSI 300 has gained by +2.7% with the Hang Seng Index (+5.2%), Hang Seng TECH Index (+5%), and Hang Seng China Enterprises Index (+5.9%) triggered by the return of short-term positive animal spirits and possible short covering activities as a media outlet reported yesterday that China’s securities regulator had asked some hedge fund managers to restrict short selling via the stock index futures.

Potential countertrend rebound sequences in progress

In the short term from a technical analysis perspective, the China and Hong Kong benchmark stock indices may see a series of countertrend rallies within their respective major downtrend phases as all of them are still trading below their respective key 200-day moving averages. Also, their current year-to-date performances are still reflecting losses at this time of the writing; CSI 300 (-3.3%), Hang Seng Index (-5.1%), Hang Seng TECH Index (-12%), and Hang Seng China Enterprises Index (-5.3%).

A liquidity trap scenario cannot be ruled out

In a longer-term perspective, there is still no clarity at this juncture to indicate that China and Hong Kong benchmark stock indices have hit major bottoming inflection points as additional liquidity injections need to be accompanied by fiscal stimulus policies (direct subsidies) that can directly trigger a boost to consumer and business sentiment that is causing the crux of this ongoing deflationary risk spiral in China.

Hence, additional liquidity created in the banking system without an uptick in consumer & business sentiment (demand-pull effect) may lead to a lack of demand for bank loans which can create a “liquidity trap” scenario in China that reinforces the current deflationary risk spiral.

Watch the next intermediate resistances at 16,525 and 17,130

Fig 1: Hang Seng Index long-term secular trend as of 25 Jan 2024 (Source: TradingView, click to enlarge chart)

Fig 2: Hang Seng Index minor short-term trend as of 25 Jan 2024 (Source: TradingView, click to enlarge chart)

Current price actions of the Hang Seng Index are now attempting to reintegrate back above the 16,100 key long-term pivotal support (also the ascending trendline in place since the August 1998 Asian Financial Crisis low).

In the shorter term as depicted by the hourly chart, there are positive elements to support a further potential extension of the ongoing countertrend rebound, the Index has staged a bullish breakout above its minor descending trendline from the 2 January 2024 high and the hourly RSI momentum indicator is still exhibiting positive configuration without a bearish divergence condition at its overbought region.

Watch the 15,660/530 key short-term pivotal support with the next intermediate resistances coming in at 16,525 and 17,035/130 (also close to the 38.2% Fibonacci retracement of the major downtrend from the 31 July 2023 high to 22 January 2024 low).

However, failure to hold at 15,530 invalidates the bullish tone to expose the next intermediate support at 15,000.

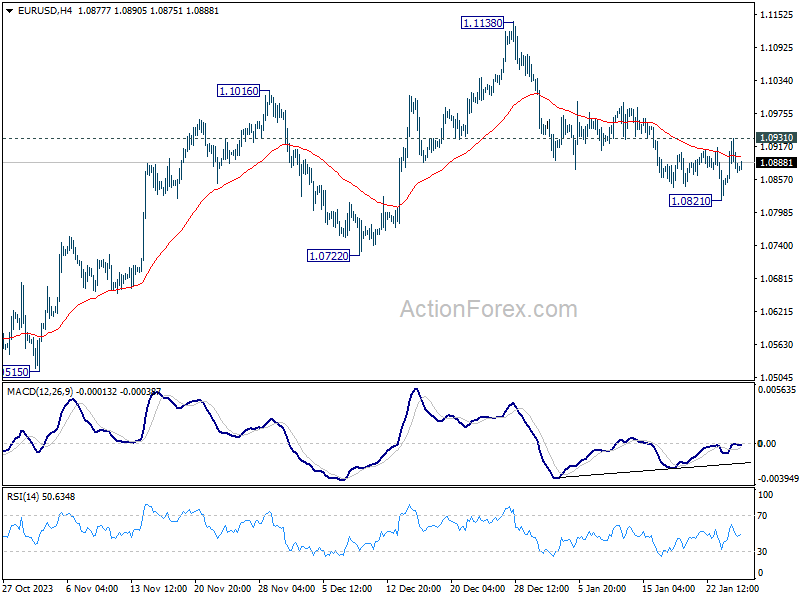

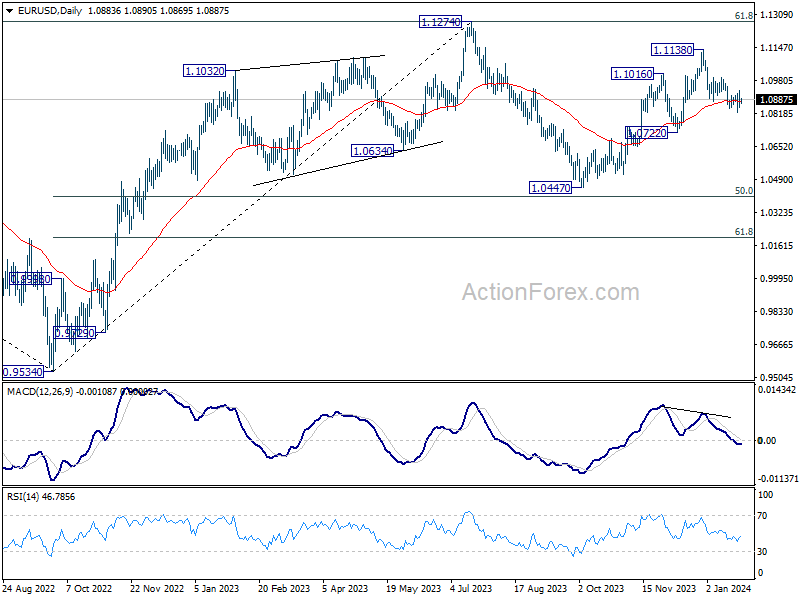

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0843; (P) 1.0888; (R1) 1.0929; More...

Intraday bias in EUR/USD stays neutral first, as it quickly retreated after brief breach of 1.0915 minor resistance. On the downside, break of 1.0821 will resume the fall from 1.1138 to 1.0722 support. On the upside, above 1.0931 will resume the rebound towards 1.1138 resistance.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

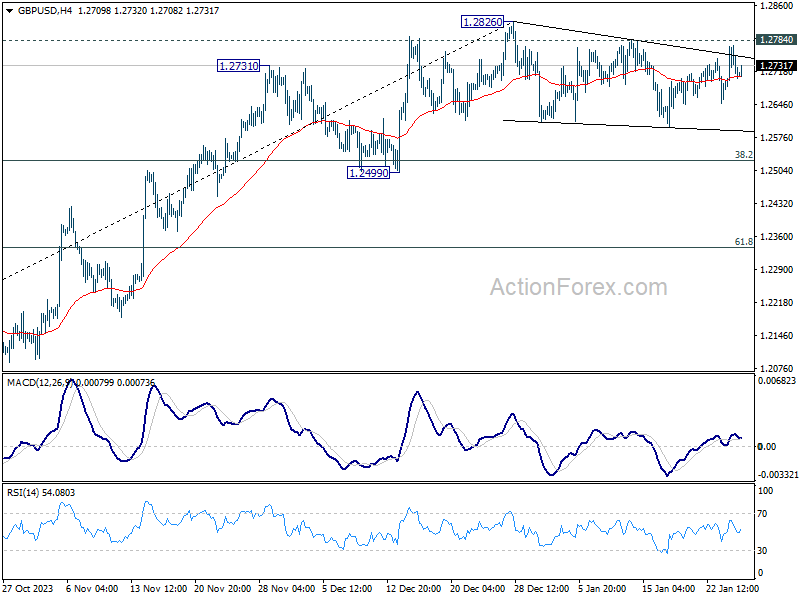

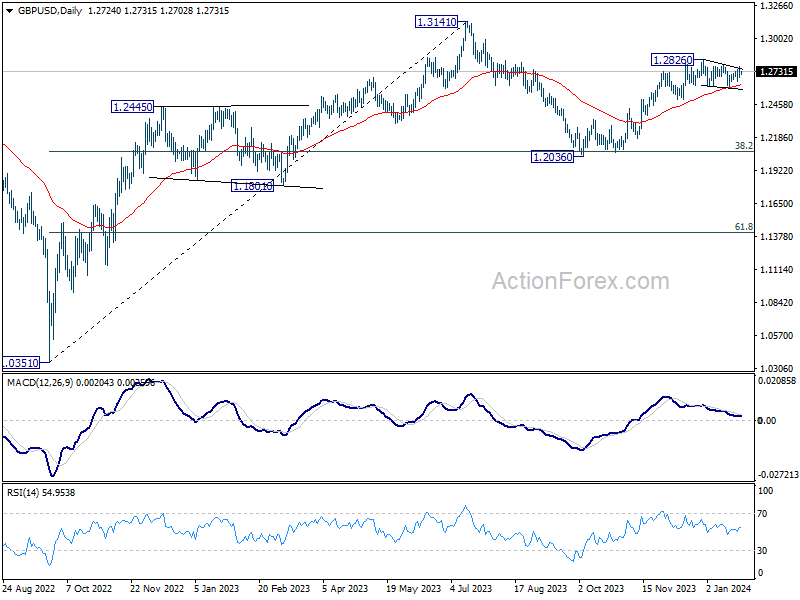

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2676; (P) 1.2726; (R1) 1.2774; More...

Intraday bias in GBP/USD stays neutral first as consolidation from 1.2826 is still extending. Deeper pull back cannot be ruled out. But downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2784 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rise from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

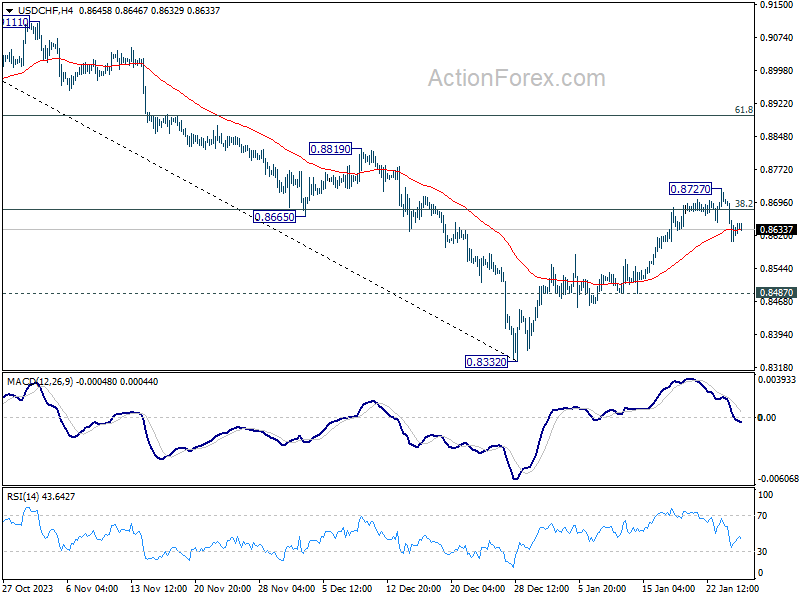

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8587; (P) 0.8648; (R1) 0.8690; More....

Intraday bias in USD/CHF remains mildly on the downside for 0.8487 minor support. Break there will argue that rebound from 0.8332 has completed at 0.8727, after rejection by 55 D EMA (now at 0.8686). Deeper fall would be seen to retest 0.8332 low. On the upside, firm break of 0.8727 will resume the rebound to 61.8% retracement of 0.9243 to 0.8332 at 0.8995.

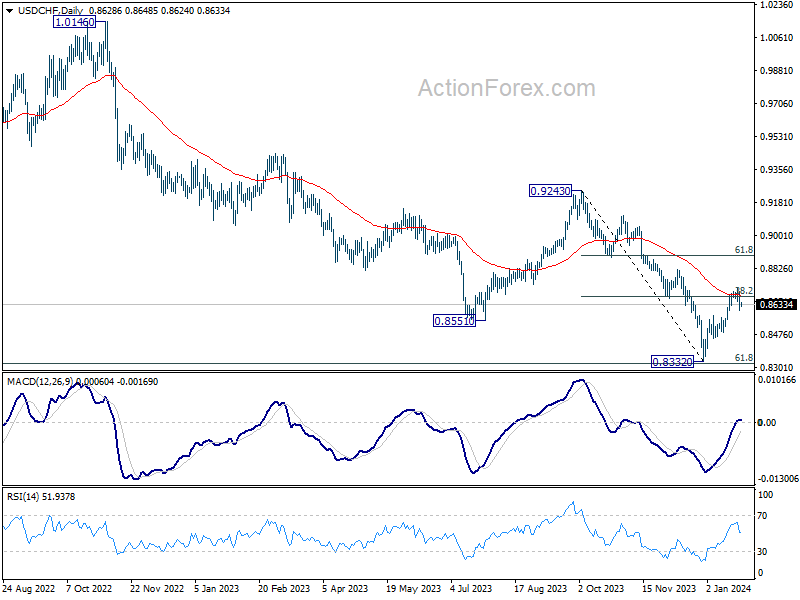

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

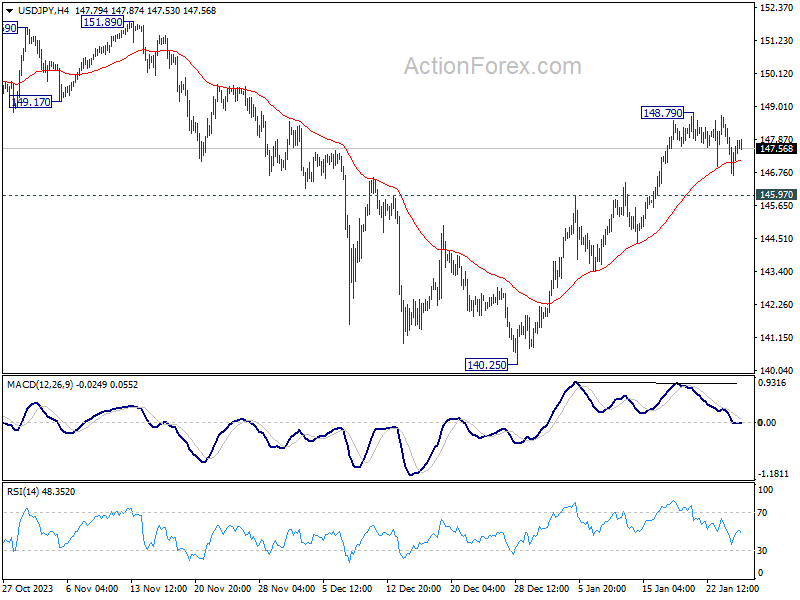

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.63; (P) 147.54; (R1) 148.44; More...

Intraday bias in USD/JPY remains neutral as consolidation from 148.79 is extending. As long as 145.97 support holds, further rally is in favor. Corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

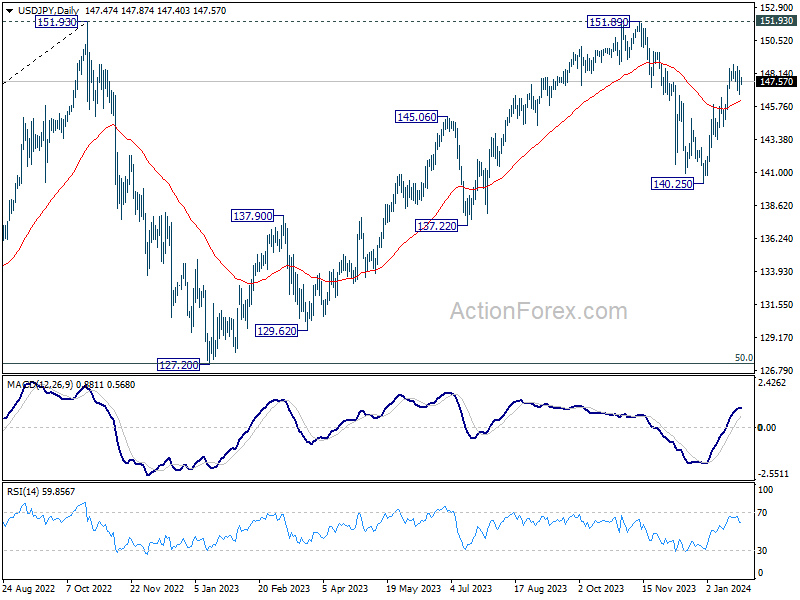

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

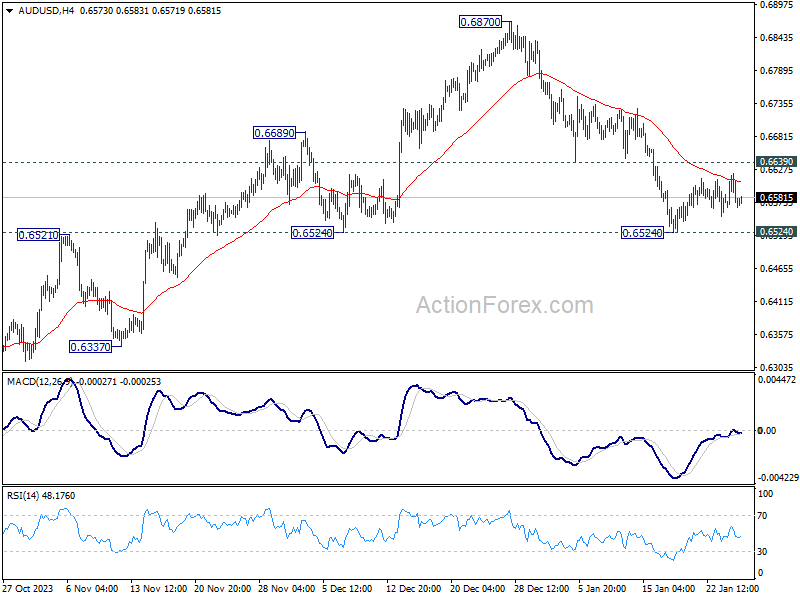

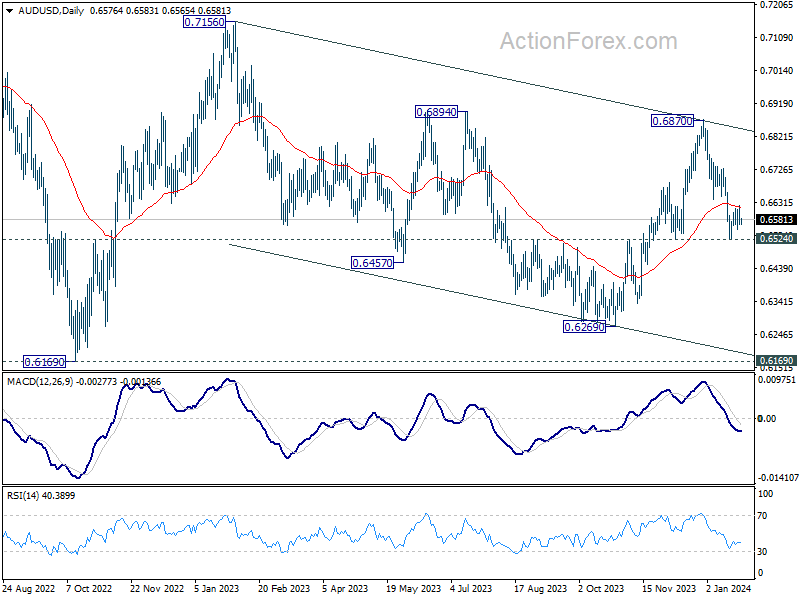

AUD/USD Daily Report

Daily Pivots: (S1) 0.6554; (P) 0.6588; (R1) 0.6610; More...

AUD/USD is still bounded in consolidation from 0.6524 and intraday bias stays neutral at this point. With 0.6639 support turned resistance intact, further decline is expected. Firm break of 0.6524 support will argue that whole rebound from 0.6269 has completed, and bring deeper fall to this support.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Dow Futures (YM) Pullback Should Find Support in 3, 7, 11 Swing

Short Term view on Dow Futures suggests rally from 10.27.2023 low ended at 38113 as wave (3). Pullback in wave (4) unfolded as a double three Elliott Wave structure. Down from wave (3), wave W ended at 37470 and wave X ended at 38038. Wave Y lower ended at 37298 as the 1 hour chart below shows. This completed wave (4) in higher degree. The Index has resumed higher in wave (5).

Internal subdivision of wave (5) takes the form of a 5 waves impulse structure. Up from wave (4), wave ((i)) ended at 37897 and pullback in wave ((ii)) ended at 37633. Index then resumes higher in wave ((iii)) towards 38157. Pullback in wave ((iv)) ended at 38061 and final leg wave ((v)) ended at 38302. This completed wave 1 in higher degree. Expect Index to pullback in wave 2 in 7 swing as a double three Elliott Wave structure. The first 3 swing lower is in progress and can reach 37731 – 37930 where wave ((w)) should end. Afterwards, it should rally in wave ((x)) before turning lower again in 3 waves to complete wave ((y)) of 2. As far as pivot at 37298 low stays intact, expect dips to find support in 3, 7, 11 swing for further upside.

Dow Futures (YM_F) 60 Minutes Elliott Wave Chart

YM_F Elliott Wave Video

https://www.youtube.com/watch?v=VlmOnu4HJqk

ECB Will Keep Key Parameters of Monetary Policy Unchanged

Markets

January PMI surveys went from a moderating downturn with intensifying price pressures (EMU) over a recovery in the private sector gaining momentum coupled with higher input costs related to the Red Sea crisis (UK) to the Goldilocks combination of rapid output growth with cooling price pressure (US). The latter nevertheless came with the important disclaimer that cost pressures will need to be monitored closely in the coming months as supply delays have intensified while labour markets remain tight. Core bond markets reacted especially to the UK and the US outcomes. In the UK because the data together with sticky inflation suggest that the BoE doesn’t even have to start thinking about thinking to start cutting policy rates. It showed in a bear flattening move with UK Gilt yields adding up to 4 bps at the front end of the curve. In the US, markets especially responded to size of the positive surprise which suggests a positive start of the year following already a stellar Q3 2023 and a likely decent Q4 (release today, consensus expects 2% Q/Q annualized). US yields added 4 to 5 bps across the curve in a more parallel shift higher. German Bunds were yesterday’s outperformers with German yields ending up to 1.5 bps lower. The dollar profited only in the second half of yesterday’s dealings from the PMI-driven interest rate support. Earlier on, the greenback was overwhelmed by an impressively bullish market sentiment which sent the EuroStoxx50 up to 2.2% higher in the close with the index escaping the corrective downward trend channel in place since the start of the year. Strong Q4 corporate earnings and massive fiscal and monetary support from Chinese authorities buoyed stock markets. EUR/USD closed at 1.0885 from a start at 1.0854 (intraday top 1.0932).

The ECB will keep the key parameters of its monetary policy unchanged today. ECB President Lagarde set the tone at last week’s World Economic Forum in Davos where she (together with her colleagues) pushed back against aggressive market pricing of policy rate cuts. She labelled “summer” as a potential start, whereas markets still attach a 70% probability to an April move. This is highly unlikely as ECB chief economist Lane for example pointed out that key Q1 wage data won’t be available by then. We expect Lagarde to echo this view, with the ECB for the moment sticking to forward guidance saying that future decisions will ensure that policy rates will be set at sufficiently restrictive levels for as long as necessary. From a market point of view, we think that such outcome would be only marginally negative for bonds with the long end even the most vulnerable. Any EUR-gains would be capped.

News & Views

The Bank of Canada yesterday left its policy rate unchanged at 5% while continuing quantitative tightening. The economy has stalled since the middle of 2023 and the BoC expects growth close to zero in Q1 2024 before picking up in H2 2024. Full year forecast for 2024 (0.8%) and 2025 (2.4%) are broadly unchanged. The BoC now reckons the economy to be operating in modest excess supply. Labour markets conditions have eased, but wages are still rising 4% to 5%. The BoC pinpointed shelter costs as the main reason for inflation staying above target. It expects inflation to hold near 3% in H1 2024 before gradually returning to 2% in 2025. The persistence of underlying inflation is a major concern, but the BoC dropped guidance that it is prepared to raise rates further. Governor Macklem kept a balanced approach at the press conference. The discussion is shifting to how long the policy rate needs to be kept at the current level if the economy evolves as expected. It remains premature to discuss reducing the policy rate. The money market discounts a first 25 bps rate cut in June. The Canadian dollar closed the session with a substantial loss (USD/CAD 1.3525 vs 1.343 before the BoC decision).

The US Federal Reserve announced to raise the rate on bank loans under the Bank Term Funding Program (BTFP) that was launched last year during the US banking crisis, but will retire on March 11. From now on the rate for borrowing under the program will be ‘no lower’ than the rate on the reserve of balances on the day that the loan is made. The rate on reserve balances (currently 5.4%) moves in line with the Fed fund target rate while pricing of loans under the BTFP until now was based on lower markets rates which already are discounting Fed rate cuts later this year. The Fed wants to further prevent this arbitrage.

When Do You Start to Worry About Chinese Stimulus?

The stock rally continued on both sides of the Atlantic on Wednesday; the technology and chip stocks remained in the driver seat. Sentiment in Europe was bolstered by an almost 9% rally in ASML on news that their orders more than tripled last quarter. Now, there is a catch. A third of the $10 billion dollar worth of orders came from China as Chinese companies rushed to buy these machines by the end of last year before the US and Dutch chip ban came into effect. But even if the Chinese demand will fade away, ASML says that it expects its sales to remain steady thanks to AI demand..

As such, the ASML news also boosted the stock prices of our favourite AI plays. Nvidia hit another record yesterday, TSM extended gains, Microsoft was worth $3 trillion for some time. The S&P500 and Nasdaq 100 hit a fresh record, and Netflix – which has nothing to do with AI, but which was just cheering its 13-mio new subscribers for the latest quarter - jumped 10%.

In summary, all goes well for those who are in the technology boat sailing north. For the rest, skepticism best describes how they feel about an unsustainable rise in valuations.

Tesla misses, Intel next

Tesla missed estimates in its latest quarterly earnings report and warned that its EV sales growth will be ‘notably lower’ and that the numbers will suffer until the company comes up with a cheaper model. The series of price cuts wasn’t enough to bolster demand in a way to keep the company smiling and profits rising – sufficiently. As such, Tesla refused to offer a specific growth target and its share price took a 6% hit in the afterhours trading. Intel is due to report its earnings today.

Connecting the dots

The Chinese are serious about bolstering their economy and they look like they are getting to a place where they are ready to do whatever it takes to reverse the slowing trend.

In addition to a series of market stimulus news, the People’ Bank of China (PBoC) announced yesterday that it will cut the reserve ratio for the banks by 50bp from February to release more liquidity to bolster stock valuations The latter will free up to an additional trillion yuan, which equals $139bn US dollars.

Will it help? Well, we will see. The good news is, if it doesn’t, the Chinese will continue until it does.

The CSI 300 finally sees some positive reaction, stocks in Hong Kong are up 10% since Monday, American crude is drilling above $75pb per barrel and copper futures – which are a gauge of global growth – also seem gently convinced that the Chinese will put all their weight – all they need to – to make things better.

But note that China’s supportive policies may not echo well across the developed markets’ central banks, because the Chinese stimulus – if successful – should boost global inflation and interfere with DM central banks’ plans to loosen policies.

BoC calls the end of tightening, ECB next to speak

But until we see concrete results from Chinese measures, softer policies remain the base-case scenario for the Federal Reserve (Fed) and the other major central banks (except Japan). In this context, the Bank of Canada (BoC) kept its rates unchanged at yesterday’s meeting and called the end of rate hikes. The European Central Bank (ECB) will meet today and will certainly vehicle the same message - that policy tightening is over. But that’s not enough.

When it comes to the ECB, what investors want to know is WHEN the ECB will start cutting the inteerest rates. If we had this conversation two weeks ago, I would say that the ECB would push back on expectations of premature rate cuts. But after having heard Christine Lagarde say that the first rate cut could come in summer, I am more balanced going into the meeting. Inflation has come lower – but we saw an uptick in the latest figures. The rising shipping costs and the positive pressure in oil prices mean that upside risks prevail. Yet the slowdown in European economies calls for lower rates. Released yesterday, the Eurozone PMI figures showed that aggregate activity remained in the contraction zone for the 8th straight month and slow down accelerated in January – except for manufacturing.

A hedge fund called Qube apparently built a $1 bn short position against German stocks, and Goldman Sachs says that a Trump presidency would increase risks for European businesses, and economically sensitive pockets of the market, like the German industries, would be the most exposed.

All Eyes on ECB

In focus today

Today, the main event of the week will be when ECB announce their rate decision at 14:15 CET. We see few, if any, new policy signals, given the limited new information that has been released since the December meeting. We expect President Lagarde to confirm that the next policy rate change is most likely a cut, which may happen in summer. It remains to be seen whether the June meeting will be singled out as the key meeting to watch, see ECB Preview - Stocktaking, 18 January.

Before the ECB announcement, we will follow another interesting policy meeting in Norges Bank, who will announce their rate decision at 10:00 CET. We see a close to zero probability of rate changes today and expect Norges Bank to signal that rates will most likely be kept unchanged also at the March meeting (neutral bias). We still expect the first rate cut in June 2024 and expect five 25bp rate cuts for the whole of 2024, see Reading the Markets Norway - Too early for NB to shift rhetoric, 22 January.

From Germany, we receive the January Ifo figures. We especially look out for the economic expectations indicator as the ZEW has shown a significant rise in expectations which has not yet been mirrored in the Ifo figures.

US flash Q4 GDP is due for release this afternoon. We expect solid quarterly growth at 1.8% Q/Q AR, which will mark a slowdown after the very strong 4.9% in Q3.

Early Friday, Tokyo January CPI data will give a first indication whether price pressures have continued to moderate in the beginning og the year.

Economic and market news

What happened over night

Overnight, the Fed decided to raise the lending rate on new loans in its emergency lending program (Bank Term Funding Program or BTFP) and terminate the program from March 11. The BTFP lending rate (1Y OIS + 10bp) has declined markedly over the past couple of months as markets have priced in significant rate cuts from the Fed in 2024. By bringing the BTFP rate (currently 4.92%) in line with the rate on reserve balances (5.40%), the Fed is de facto closing an arbitrage opportunity for banks. Whether the termination of BTFP will strengthen the appetite for slowing down QT remains to be seen.

What happened yesterday

In the euro area, Service PMIs fell unexpectedly to 48.4 (cons: 49.0, prior: 48.8) while manufacturing rose more than expected to 46.6 (cons: 44.7, prior: 44.4). The price pressure in the service sector increased in January and is now at the highest level in six months while the manufacturing sector continued to lower prices. Service companies also hired staff at the fastest pace in six months highlighting continued upside risks to inflation.

In the UK, PMIs for January came in stronger than expected and remain in expansionary territory for composite and services. As result markets scaled back on expectations for cuts and are now pricing around 100bp of cuts for the remainder of the year. On price pressures, input prices continue to rise, although more moderately. Input price pressures increased in the manufacturing sector following impact from the disruptions in the Red Sea, which also triggered a sharp rise in delivery times.

US PMIs were also stronger than expected in January. Both manufacturing and services are now in growth territory (above 50). Although the PMIs have recently been more positive than the ISM figures, yesterday's outperformance emphasizes the resilience of US growth data.

People's Bank of China (PBoC) yesterday pre-announced a cut in the reserve requirement ratio (RRR) for banks of 0.5 percentage points on 5 February. PBoC also signalled more easing was on the way by stating that the RRR rate is still relatively high and that the policy pivot by the Fed would expand China's policy space. The rising US-China policy rate spread has been a concern for PBOC as it could destabilise the CNY.

Bank of Canada (BoC), left rates unchanged yesterday at their first policy meeting in 2024, which was in line with expectations. BoC expects inflation to stay around 3% in the first half of 2024 and signalled the potential rate cuts in the third quarter if inflation turns to the predicted 2.4%.

Hungary's prime minister Victor Orban said Wednesday that he will urge the Hungarian parliament to approve Sweden's NATO bid as soon as possible. After Turkey's decision to approve the Swedish bid on Wednesday, Hungary is the only remaining member country still to approve the Swedish bid.

Equities: Global equities were higher for the fifth consecutive day. Yesterday's surge was fuelled by a cyclical rotation, with Europe and Asia delivering the best performances. It is tempting to echo the theme of our 2024 outlook, "good news is good news," given the positive manufacturing news from the flash PMIs. However, some of the initial enthusiasm waned during US afternoon trading as yields reversed course and increased towards the closing bell. In the US yesterday, Dow -0.3%, S&P 500 +0.1%, Nasdaq +0.4%, and Russell 2000 -0.7%. Asian markets are broadly higher this morning, propelled by China and the substantial monetary loosening measures announced yesterday. US and European futures are mixed this morning.

FI: US government bond yields rose on the back of a weak auction in the 5Y Treasuries as well as speculation that Federal Reserve will be higher for longer. Hence, 30Y US Treasuries rose to the highest level in 2024 on the back of the weak 5Y auction, where the bid-to-cover was 2.3, which is in the lower part of the range for the bid-to-cover at the 5Y Treasury auctions seen over the past five years. Next week we get the quarterly refunding statement from the US Treasury and it will be interest to see if issuance is increasing in the long end.

FX: USD/CAD rose almost a full figure, to 1.3520, after BOC left rates unchanged, as expected, and mulled when to let go of current restrictive policies. USD gained vs most G10 currencies as US PMI data surprised on the upside and US Treasuries underperformed vs peers. However, EUR/USD has dropped over night to around 1.0880. EUR/NOK is back below 10.40 ahead of Norges Bank's rate decision at 10:00 where unchanged is widely expected.