Sample Category Title

UK PMIs to Reveal How the British Economy Entered the New Year

- Investors scale back BoE rate cut bets after CPI data

- But disappointing retail sales revive some recession fears

- Pound traders may now turn attention the UK flash PMIs

- The data comes out on Wednesday at 09:30 GMT

Hotter-than-expected inflation, but disappointing retail sales

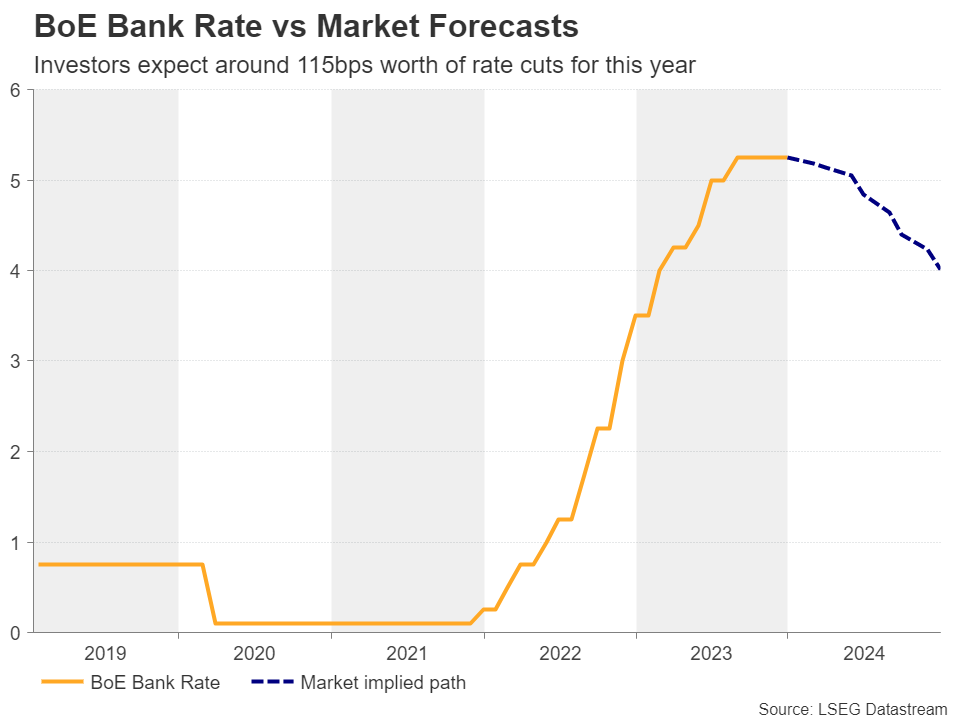

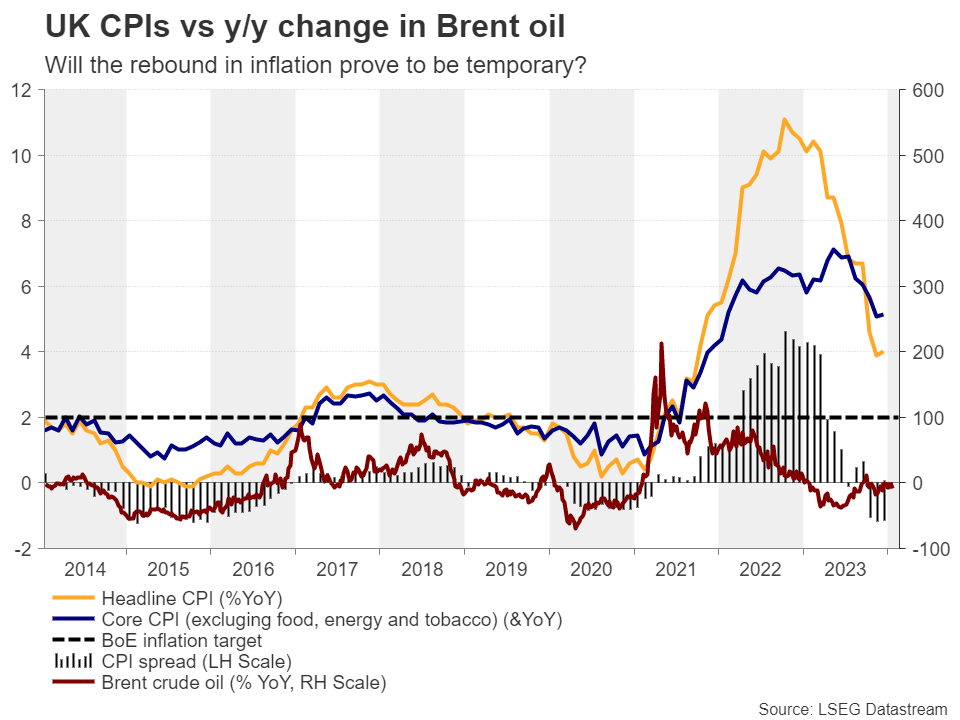

After the hotter than expected UK CPI data for December, investors scaled back their Bank of England rate cut bets, lowering the total basis points worth of reductions expected by the end of the year to 115 from 125 and the probability of the first quarter-point reduction to be delivered in May to 55% from around 90%.

That said, on Friday, retail sales for the same month disappointed and according to the Office of National Statistics (ONS), they are likely to subtract 0.04 percentage points from the UK economic output in the fourth quarter. Given that the National Institute of Economic and Social Research (NIESR) tracker has been pointing to a stagnant economy ahead of the release, this could make the difference between a flat or a negative figure.

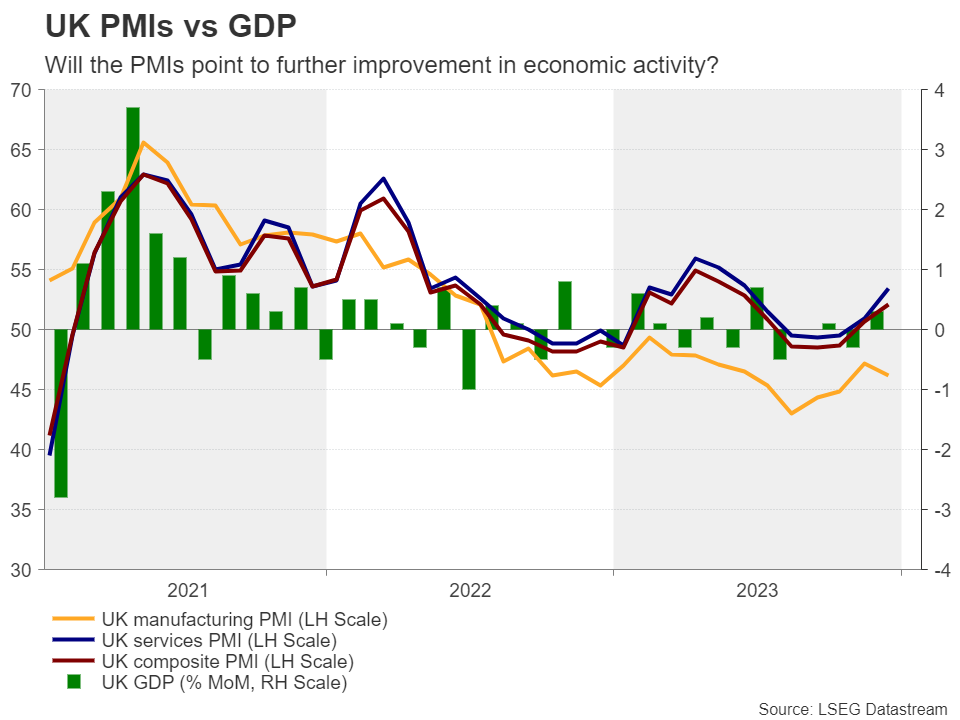

Although retail sales may have revived concerns with regards to a potential recession, investors did not add back to their BoE rate cut bets. Perhaps the rebound in the November monthly GDP and the improvement in the December composite PMI acted as safety barriers.

UK Flash PMIs the next focal point for pound traders

With all that in mind and taking into account that the NIESR is forecasting GDP to grow by 0.2% in the first quarter of 2024, on Wednesday, pound traders may focus on the preliminary PMIs for January, as this would be the first information on how the UK economy entered the new year.

Apart from the headline prints, the employment and prices sub-indices may also be of high importance as they could provide a glimpse of whether the rebound in the December inflation prints was only due to base effects and will prove to be temporary, or whether inflation will prove to be stickier than previously anticipated.

Will the data help the pound gain more ground?

Numbers suggesting that the economic activity is faring better than it did during the second half of 2023 and sub-indices pointing to still-sticky inflation may convince investors that the BoE is right in not discussing the prospect of lower interest rates so soon. The probability of a May cut could further decline, and the pound could gain some more ground.

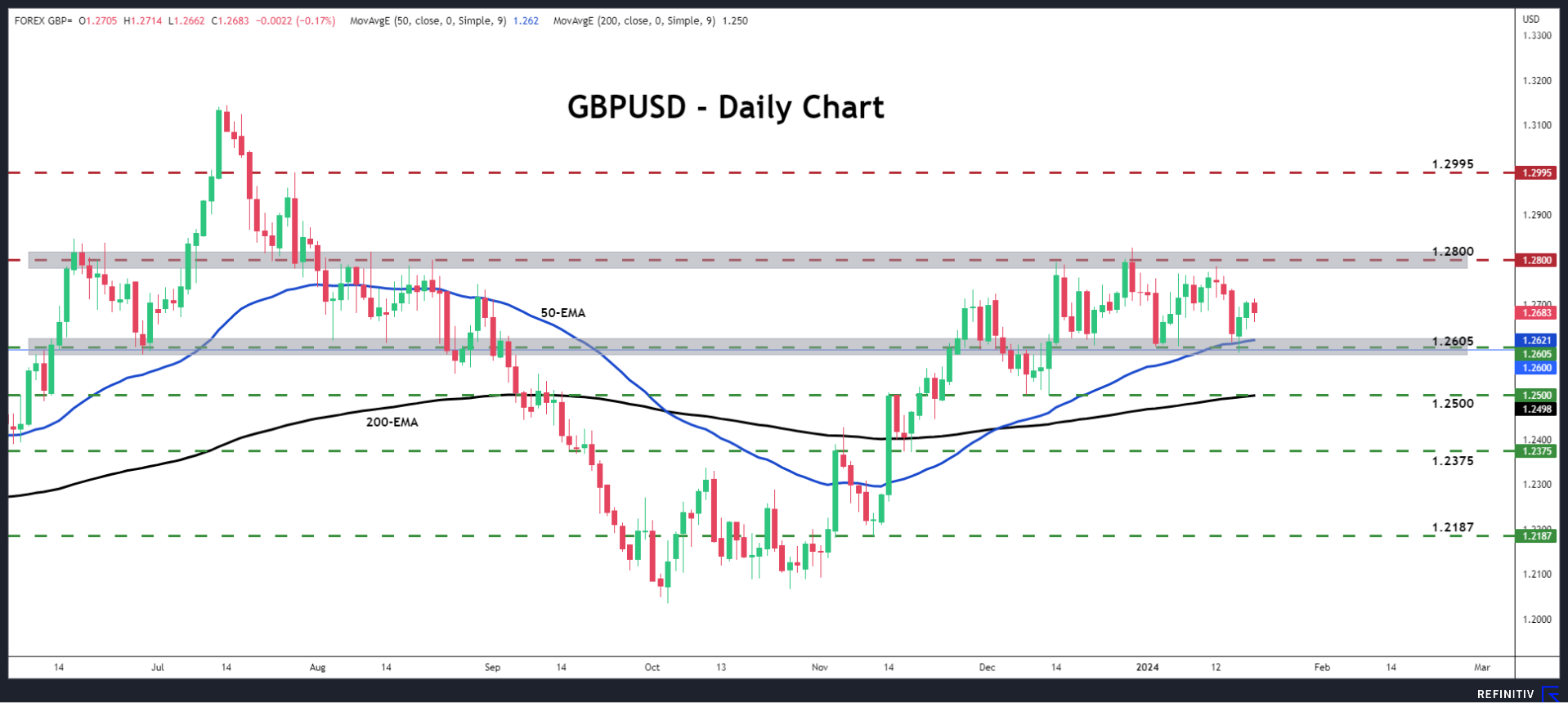

Pound/dollar has been oscillating between 1.2605 and 1.2800 since December 14, two barriers that acted as support and resistance several times in the past. After the hotter-than-expected CPI numbers, the pair rebounded from the lower end of that range and despite the pullback on the worse-than-expected retail sales data, encouraging PMIs may allow another round of advances, perhaps towards the upper bound at around 1.2800.

Nonetheless, for the outlook of this pair to turn positive again, a break above that zone may be needed. Such a move would confirm a higher high on the daily chart and may carry extensions towards the high of July 27 at around 1.2995. Alternatively, a dip below 1.2605 may turn the picture bearish and encourage the sellers to push the action towards the 1.2500 area.

Week Ahead – ECB and BoJ Meetings in the Spotlight

- Japanese yen loses ground ahead of BoJ decision on Tuesday

- ECB meets on Thursday, will it push back against rate cut bets?

- Bank of Canada decides too, while the US releases GDP stats

BoJ unlikely to rescue battered yen

The Japanese yen started the new year on the wrong foot, losing 5% of its value against the US dollar in the space of three weeks as cooling inflation and a sharp slowdown in wage growth convinced investors that the Bank of Japan will delay its plans to exit negative interest rates.

For a long time, market pricing suggested the BoJ would end negative rates in April. However, traders have now pushed back the timing of this move to July, dealing a heavy blow to the yen.

BoJ officials are unlikely to rock the boat when they meet on Tuesday. Governor Ueda has already downplayed the prospect of raising rates, stressing that there is no rush. The economic data pulse has weakened further since he made those comments, so the BoJ will most likely maintain a cautious stance.

In fact, some media reports suggest the BoJ will cut its inflation forecasts for this year. That would signal even less urgency to normalize policy, which in turn could keep the yen under pressure.

On the data front, the inflation stats for Tokyo will hit the markets on Friday.

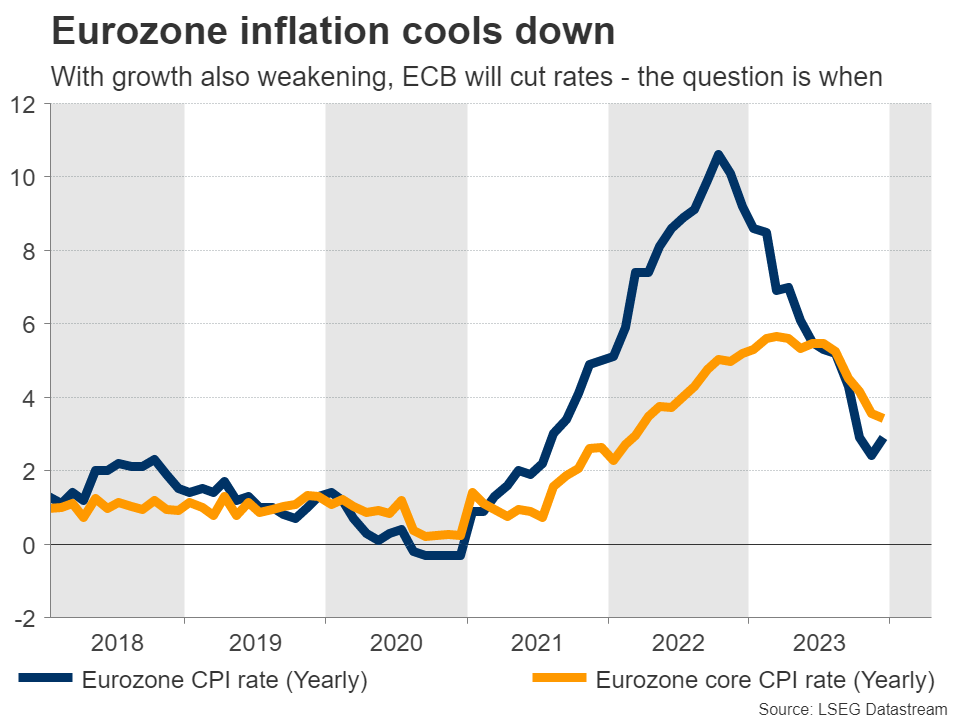

Will the ECB push back on rate cuts?

In the euro area, the European Central Bank decision will take center stage on Thursday. Market pricing suggests the central bank will do nothing, so the action will come mostly from the commentary by President Lagarde.

Several ECB officials have tried to dampen speculation about imminent rate cuts lately. Markets currently assign an 85% probability that the ECB will slash rates in April, but various policymakers including Lagarde have warned that’s too early, pointing to a summer rate cut instead.

If the ECB hammers this message home next week, the euro could briefly spike higher as some rate-cut bets are unwound. That said, it might be difficult for the single currency to sustain any advances, amid stagnant economic growth. With business surveys warning about a technical recession, the picture for the euro appears grim overall.

Speaking of business surveys, the next batch will be released on Wednesday, one day ahead of the ECB decision.

Bank of Canada decides, US publishes GDP data

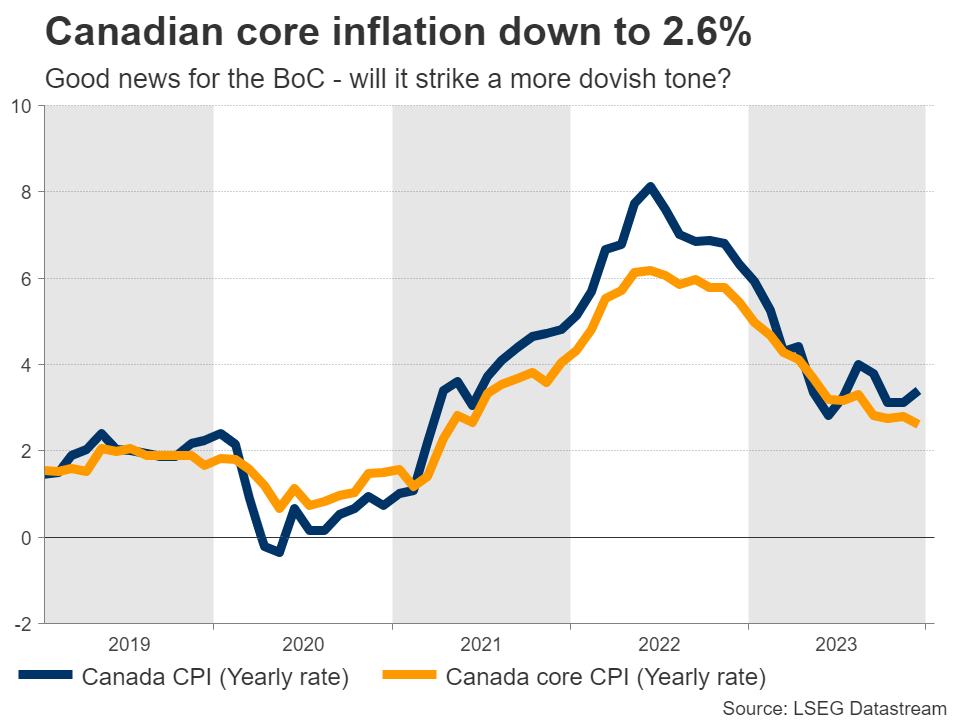

Over in Canada, the central bank will announce its own decision on Wednesday. Markets assign a 15% probability for an immediate rate cut, so it’s going to be an interesting event.

The Canadian economy has been flashing mixed signals lately. With wage growth firing up and record levels of immigration boosting housing prices, there is a concern that inflation could remain elevated for some time.

However, core inflation has declined dramatically, falling to 2.6% in annual terms in December. The BoC aims to keep inflation in a target range of 1% - 3%, so there is an argument that the job is almost done. Similarly, the latest business survey from the BoC warned about a weaker demand outlook, which could dampen inflation further.

Bearing everything in mind, the central bank will most likely hold interest rates steady at this meeting, but it might strike a more dovish tone, softly opening the door for an easing cycle later this year.

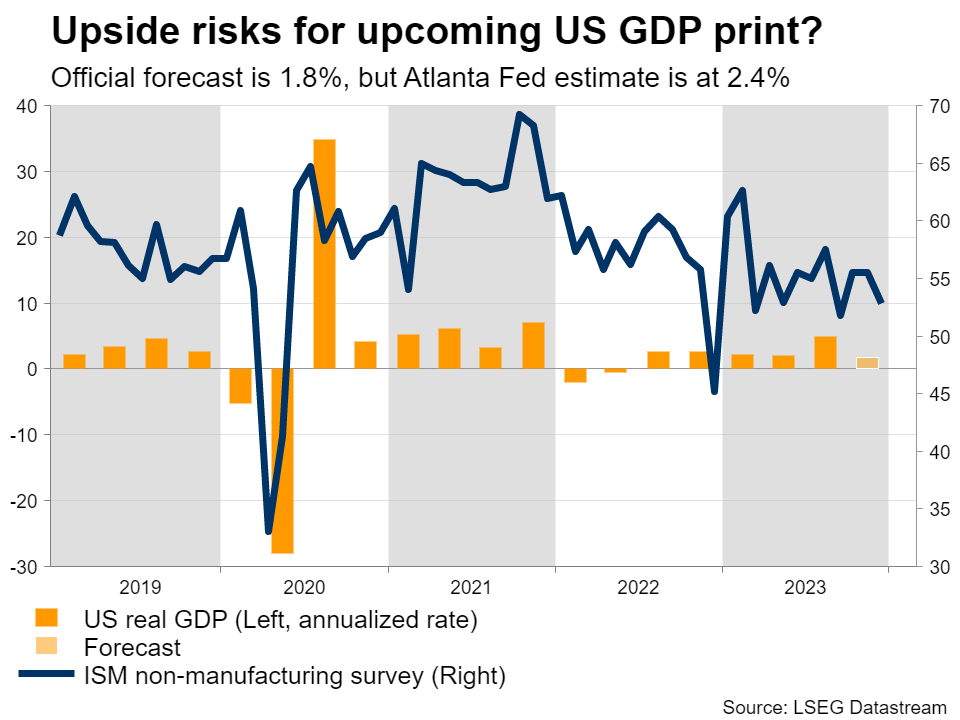

Across the border, the main event in the United States will be the release of preliminary GDP stats for Q4 on Thursday. The forecast is for the American economy to have grown by an annualized rate of 1.8% in the final quarter.

As for any surprises, a stronger-than-expected GDP print seems more likely than a disappointment. That’s mostly because of the Atlanta Fed GDPNow model, which estimates growth at 2.4% instead, much higher than the official forecast.

As for any surprises, a stronger-than-expected GDP print seems more likely than a disappointment. That’s mostly because of the Atlanta Fed GDPNow model, which estimates growth at 2.4% instead, much higher than the official forecast.

This model has a solid track record, and if it proves accurate this time as well, the dollar could benefit as traders scale back bets of rapid-fire Fed rate cuts this year. The core PCE price index for December will follow on Friday and could also be important in shaping Fed expectations.

Finally in New Zealand, inflation stats for Q4 will see the light on Tuesday.

Weekly Focus – Managing Expectations

While the past week has been a quiet one on the macro data front, central bankers sent some hawkish signals ahead of the January rate decisions. The Fed's Waller remained confident that sustainable 2% inflation is within 'striking distance', but he also underscored that there is no reason to cut rates as quickly as in the past. Just ahead of the ECB's silent period, Lagarde noted that rates will likely be cut only by summer and Knot cautioned that markets have been 'getting ahead of themselves'.

As a result, yields edged higher throughout the week as market pulled back on expectations of rapid rate cuts. We expect the ECB to cut rates by a total of 75bp in 2024 and the Fed by 100bp, so with around 130-140bp of cumulative cuts still priced in for both central banks, we generally see further upside risks to pricing from here. We expect few, if any new policy signals from next week's ECB meeting but we will look out for signals on the most likely timing of the first cut, which we have pencilled in for June. Read more details from our full ECB Preview - Stocktaking, 18 January.

Rising yields were also reflected in weaker equities and cyclical currencies while the broad USD regained strength. In the FX markets, we expect similar trends to continue also later in the year, as we see EUR/USD heading towards 1.05 and EUR/SEK rising to 11.60 on a 12M horizon in our latest FX Forecast Update - 2024 to prove a good year for the USD, 15 January. One key argument for our bullish USD view has been the continuing US economic outperformance vis-à-vis peers and, this week, the December retail sales data confirmed that consumer demand has remained solid. Widely followed control group sales growth surprised clearly to the upside at +0.8% m/m SA.

US election year kicked off with Republican Iowa caucuses, where Donald Trump clinched a convincing victory with 51% support over Ron DeSantis (21%) and Nikki Haley (19%). While the result was well in line with polling averages, it marked a disappointment especially for DeSantis who had put significant campaigning effort into Iowa. Primaries will continue next Tuesday in New Hampshire, where the pressure is on Haley, who has been performing relatively well in recent local polls. Read more on the primary elections and the US fiscal and foreign policy outlook in Primer for 2024 elections, 15 January.

Besides the ECB, also the Bank of Japan will have a monetary policy meeting where we expect an unchanged rate decision. Wage growth remains the missing piece of the puzzle before the BoJ can look towards rate hikes and letting go of the yield curve, but we will likely have to wait for the spring wage negotiations for hard evidence. The People's Bank of China will also likely make no changes to the Loan Prime Rate on Monday after the Medium-term Lending Facility rates were left unchanged this week. Finally, we also expect an unchanged rate decision from Norges Bank on Thursday.

On the data front, January Flash PMIs will provide the first hints on how major economies have fared at the beginning of 2024. Generally, leading data has suggested that global manufacturing activity might have reached a trough in late 2023, while services growth momentum remains muted. We will also keep an eye on the US Q4 Flash GDP and December PCE data.

Sunset Market Commentary

Markets

Attention turned to central bank speeches again in absence of key eco data in the US and EMU. Chicago Fed Goolsbee had the biggest market impact. He said that markets may have put the cart before the horse on cuts. He’s seen surprising progress on services inflation, but want to see more progress on housing inflation. It triggered a new sell-off in US Treasuries with the front end of the curve underperforming. US yields add 4.7 bps (2-yr) to 0.5 bps (30-yr). German Bunds shadow the move to a lesser extent with yields rising up to 2.5 bps at the front end. The dollar fails to profit with EUR/USD going nowhere at 1.0875. Sterling slightly underperforms following the release of very weak December retail sales. EUR/GBP moves from 0.8560 towards 0.8590.'

Focus shifts to first major central bank gatherings of the year next week, excluding the National Bank of Poland’s status quo on January 9. Chronologically, the Bank of Japan has a first go on Tuesday. Rumours suggested downward revisions to the near term growth outlook and the near/medium term inflation outlook. Together with uncertainty related to external events like the severe earthquake, it suggests that the BoJ is in no hurry to implement a real policy U-turn (ending negative policy rates). The Japanese yen is the biggest victim of this continued soft stance in combination with new weakness in core bonds. It prompted first verbal interventions by Finance Minister Suzuki this morning as USD/JPY approaches the key 150-handle. We fear that an even weaker Japanese currency is the preferred market mechanism to push the BoJ with the back against the wall. The Bank of Canada convenes on Wednesday. December Canadian inflation data unexpectedly showed new momentum in underlying price trends, suggesting the BoC won’t be able to flag a rapid start to policy rates cuts. They could nevertheless turn somewhat more neutral as they still vowed to raise the policy rate (5%) further if needed. On Thursday, the duo of Norges Bank and ECB decide on monetary policy. The Norwegian disinflation process went faster than expected at the end of 2023. In combination with a slightly stronger Norwegian krone, this could prompt the Norges Bank to pull its December 2024 first rate cut call somewhat forward in time. Last but not least, there’s the ECB. ECB President Lagarde pushed back against aggressive market expectations at the World Economic Forum in Davos. She suggested a first rate cut only in Summer. Media concluded that European central bankers are preparing a June rate cut, with the jury still out whether June 6 can already be labelled “Summer”. If not, our view, we’re talking about a July rate cut at the very earliest with markets still convinced about an April move. We expect Lagarde to hold this week’s line which should underpin this year’s trend (higher) on interest rate markets.

News & Views

In an interview with the website 300Gospodraka.pl MPC member Ludwik Kotecki of the National Bank of Poland indicated that the NBP won’t cut interest rates according the path that markets currently discount. He advocates that interest rates will have to stay longer at current level. He admits that Polish inflation might drop below 3% in March, but it may rebound to 6%-7% in H2, even as forecasting inflation is difficult due to uncertainty over food and energy prices. Kotecki sees the September and October rate cuts as a mistake, but the NBP can’t reverse them as this would be inefficient and incomprehensible. At the same time he also rejects the option of the NBP selling bonds from its portfolio as it could disrupt the treasury market and weaken the zloty. It would also make it more difficult for the government to finance its budget expenditures.

According to data published by the Swedish Riksbank, the central bank is gradually moving towards the targets of the FX reserves hedging program its started end September last year. In the first week of the year, they sold $70mn and €350mn. It completed $6.67bn of the intended $8bn and €1.56bn of the targeted sales of €2bn. The Riksbank planned to complete the sales over a six month horizon. The krone since mid-September strengthened from the EUR/SEK 11.90 area to a top of EUR/SEK 11 in the last week of the year. Since then it again weakened to currently trade near EUR/SEK 11.40. The price pattern suggests that the price moves in the krone are mainly determined by global financial conditions (fall and rise in core bond yields) rather than by the flows related to the Riksbank hedging.

Canada: November Retail Sales Surprise to the Downside, But Expect a Rebound in December

Retail sales declined by 0.2% month-on-month (m/m) in November, coming in weaker than Statistics Canada's advance estimate for a flat reading. October's print was revised slightly to +0.5% m/m from +0.7% m/m.

Adjusted for inflation, the volume of retail sales reported a loss of 0.2% in November, reversing course from last month's robust 1.0% m/m reading.

Sales at motor vehicle and parts dealers continued to recover from weak summer sales. This category was up by 0.5% m/m in November, but last month's gains were revised down from 1.1% to 0.7% m/m.

Receipts at gasoline stations and fuel vendors were up 0.3% m/m, after a loss of 3.1% m/m in October.

Excluding sales at car dealerships and gas stations, core retail sales were down 0.6% m/m, following a solid gain of 1.2% m/m in October.

- This month's loss was led by declines at food and beverage retailers (-1.4% m/m) and general merchandise stores (-1.8% m/m). However, accounting for October's gain of 1.0% m/m, core sales are tracking 1.2% in the fourth quarter (quarter-on-quarter, annualized).

- The two categories with positive readings were clothing and clothing accessories stores (+1.5% m/m) and health and personal care stores (+0.3% m/m).

E-commerce sales turned negative this month, losing 1.5% m/m after an upwardly revised gain of 2.4% m/m in October (from +1.8 m/m, reported earlier)

Statistics Canada's advance reading suggests that retail sales rebounded in December by an estimated +0.8% m/m (with 49.4% of companies surveyed providing responses).

Key Implications

We don't read too much into today's negative print in retail sales, which is bookended by a solid October reading and a resilient flash estimate for December. There are two major factors at play: the recovery in auto production, which supported auto sales and stronger-than-expected housing activity, which was aided by warmer weather and strong population growth. All this points to a solid finish to 2023. As a result, we think there is an upside risk to our Q4 spending forecast of 2.0% quarter-on-quarter growth (annualized).

The real question is will this resilience last? Not according to the Bank of Canada's Survey of Consumer Expectations. Canadians are increasingly feeling the pain of both inflationary pressures and higher cost of borrowing. Consequently, they are making plans to reduce spending on large items while also looking for bargains when shopping for essential. This suggests that the need for accommodative policy will come sooner rather than later, despite the recent improvement in consumer spending and stubbornness of inflation. We expect the first rate cut in the second quarter of 2024.

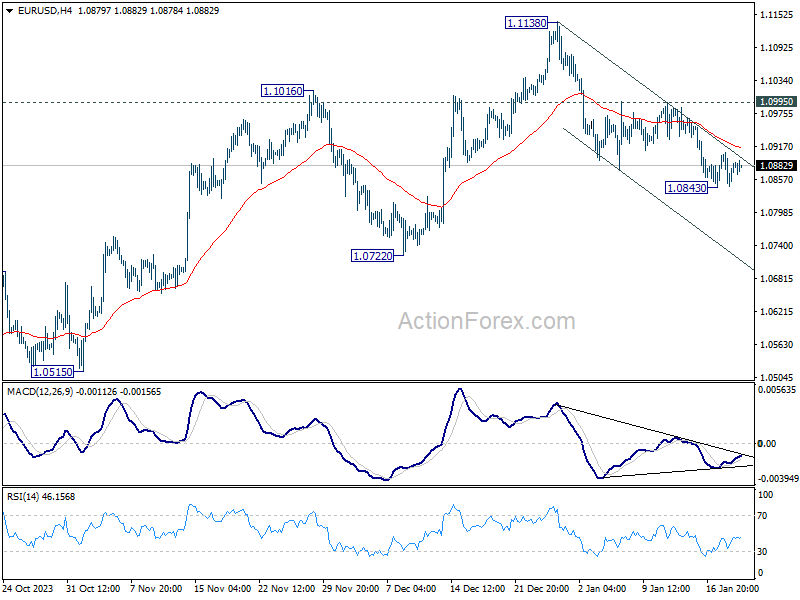

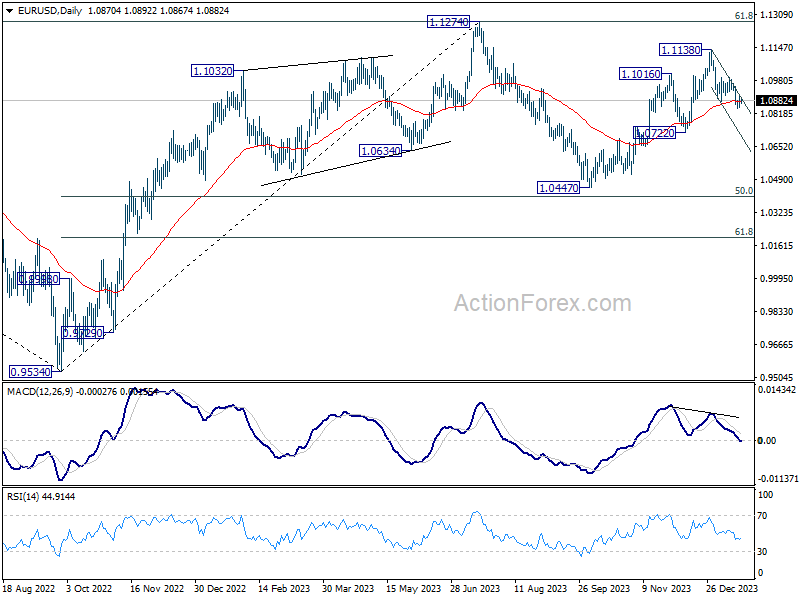

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0846; (P) 1.0877; (R1) 1.0906; More...

EUR/USD is extending consolidation above 1.0843 temporary low and intraday bias stays neutral. Outlook remains bearish with 1.0995 resistance intact. On the downside, break of 1.0843 will resume the fall from 1.1138 to 1.0722 support. Sustained break there will argue that whole rise from 1.0447 has completed, and target this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

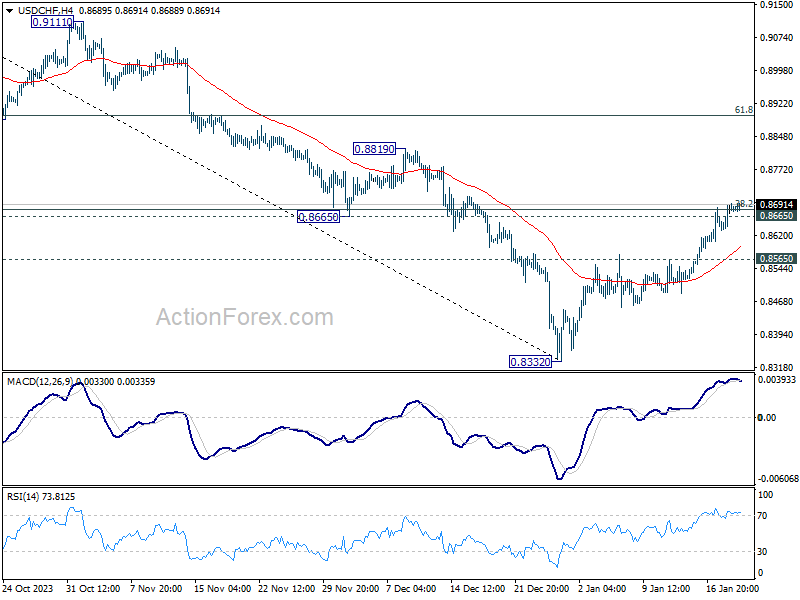

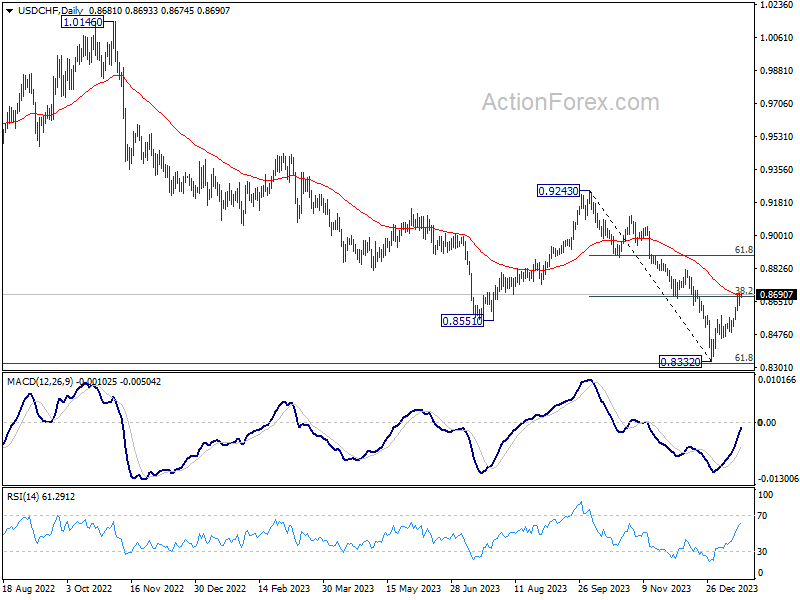

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8644; (P) 0.8670; (R1) 0.8707; More....

No change in USD/CHF's outlook as focus remains on 0.8665 support turned resistance. Decisive break there will turn near term outlook bullish for 61.8% retracement of 0.9243 to 0.8332 at 0.8995. Nevertheless, break of 0.8565 minor support will turn intraday bias back to the downside for retesting 0.8332 low.

In the bigger picture, outlook in USD/CHF will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

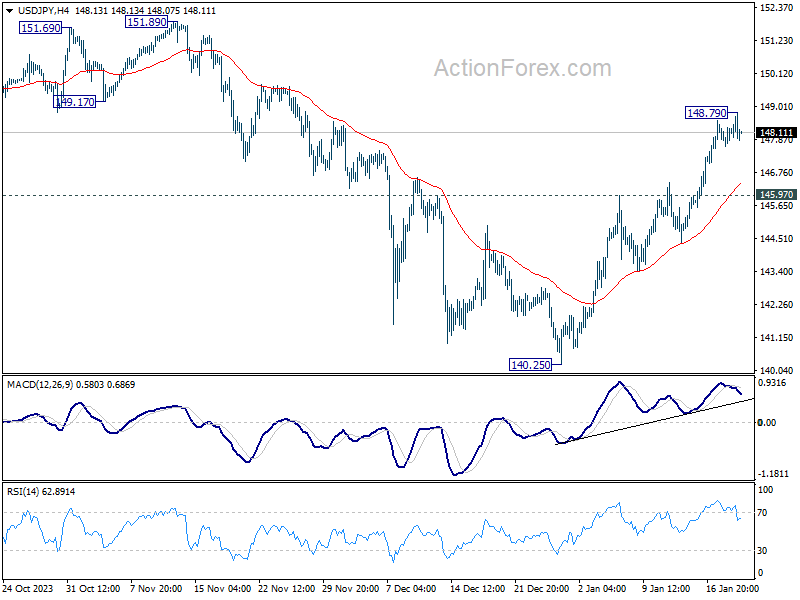

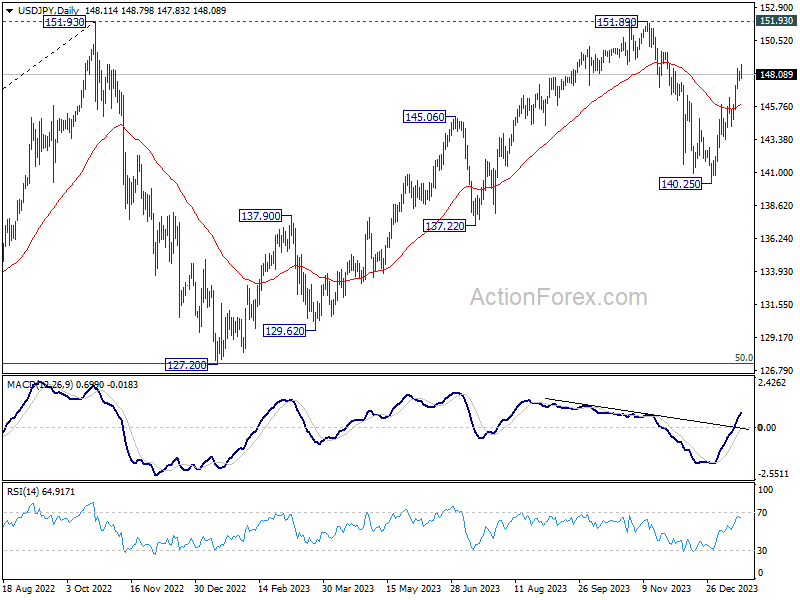

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.78; (P) 148.05; (R1) 148.44; More...

Intraday bias in USD/JPY is turned neutral with loss of momentum as seen in 4H MACD. Some consolidations could be seen, but further rally is expected as long as 145.97 resistance turned support holds. Above 148.79 will resume the whole rise from 140.25 to 151.89/93 key resistance zone.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

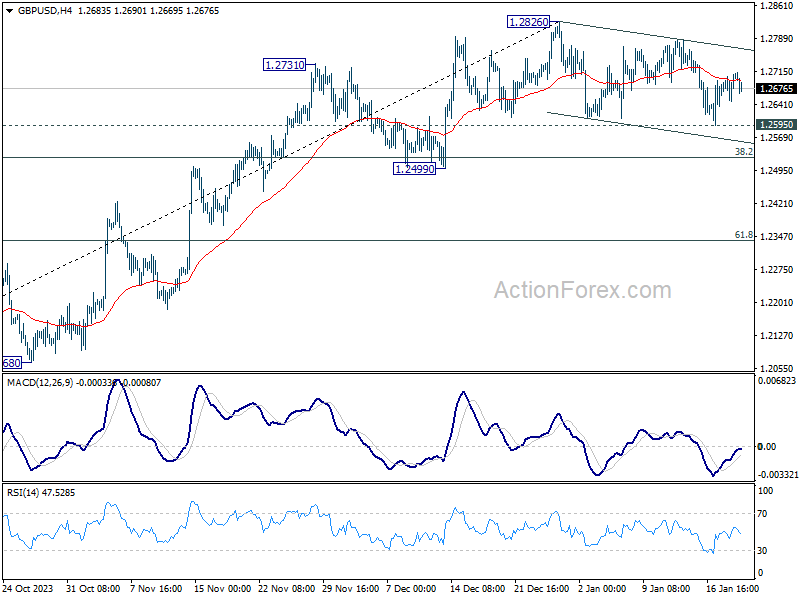

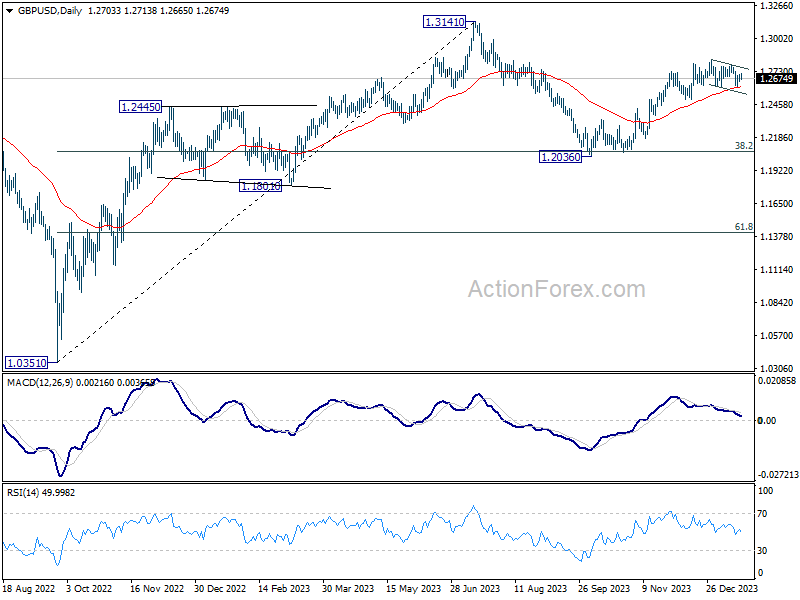

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2666; (P) 1.2688; (R1) 1.2727; More...

GBP/USD is staying in range above 1.2595 support and intraday bias remains neutral. On the downside, firm break of 1.2595 will resume the decline from 1.2826 to 1.2499 support. Nevertheless, strong rebound from current level will retain near term bullishness. Decisive break of 1.2826 will resume whole rally from 1.2036.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Sterling Sees Moderate Decline After Weak Retail Sales, Losses Contained

Sterling fell broadly today following weaker-than-expected retail sales data. Despite this, the British currency's losses have been somewhat contained, indicating a degree of resilience. Concurrently, Japanese Yen and Australian Dollar are showing attempts to recover, but these efforts lack significant follow-through momentum. The day's activities seem more reflective of temporary consolidations rather than indicative of any major shifts in market trends.

As the week draws to a close, Dollar is on track to finish as the strongest performer. Euro and Sterling, which had been contending for the second place, have now given way to Canadian Dollar. However, there is still room for some last-minute adjustments in the rankings. Yen, on the other hand, is poised to be the weakest performer for the week, followed closely by New Zealand Dollar and Swiss Franc. Australian Dollar, which was previously languishing at the bottom, has managed to climb out of the lowest ranks and is set to end the week with mixed performance.

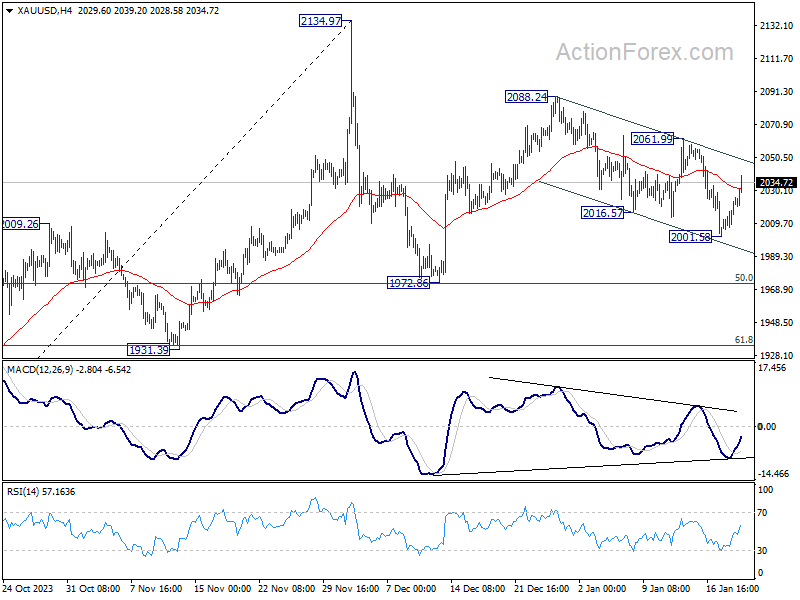

Technically, Gold surprisingly rebounded after defending 2000 handle. But overall outlook is unchanged. Price actions from 2134.97 are viewed as a corrective pattern. Rebound from 1972.86, as the second leg, might not be over yet. Break of 2061.99 will target 2088.24 and above. Nevertheless, another decline and break of 2001.58 will extend the fall from 2088.24 to 1972.86 support instead.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 0.14%. CAC is down -0.08%. UK 10-year yield is down -0.351 at 3.905. Germany 10-year yield is down -0.023 at 2.329. Earlier in Asia, Nikkei rose 1.40%. Hong Kong HSI fell -0.54%. China Shanghai SSE fell -0.47%. Singapore Strait Times rose 0.40%. Japan 10-year JGB yield rose 0.0143 at 0.669.

Canada's retail sales falls -0.2% mom in Nov, ex-auto sales down -0.5% mom

Canada's retail sales fell -0.2% mom to CAD 66.6B in November, worse than expectation of 0.0% mom. Sales declined in four of nine subsectors, led by contraction in food and beverage at -1.4% mom. Excluding autos, sales were down -0.5% mom, much worse than expectation of -0.1% mom.

Advance estimate suggests that sales rose 0.8% mom in December.

UK retail sales volume down -3.2% mom in Dec, sales value falls -3.6% mom

UK retail sales volume fell -3.2% mom in December, much worse than expectation of -0.5% mom. That's also the largest monthly fall since January 2021. Excluding fuel, sales volume fell -3.3% mom. Automotive fuel sales volumes fell by -1.9% mom. On an annual basis, sales volumes fell by 2.8% in 2023 and were their lowest level since 2018.

In value term, Retail sales value fell -3.6% mom. Ex-fuel sales value fell -3.6% mom.

Japan's CPI core dips to 2.3%, remains above BoJ's target for 21st month

Japan's CPI core, excluding fresh food, decelerated slightly in December, moving from 2.5% yoy to 2.3% yoy, aligning with market expectations. This slowdown brings core inflation rate to its lowest since June 2022, yet it notably remains above BoJ's 2% target for the 21st consecutive month.

Overall headline CPI also showed a slowdown, decreasing from 2.8% yoy to 2.6% yoy. Additionally, CPI core-core, which excludes both food and energy, saw a modest decline, moving from 3.8% yoy to 3.7% yoy.

A notable aspect of CPI data is the stability of services prices, which rose by 2.3% yoy, maintaining the pace from the previous month. This rate marks the fastest increase in services prices in three decades when periods affected by sales tax hikes are excluded.

A significant factor contributing to the slowdown in inflation was the substantial drop in energy prices, which decreased by -11.6% yoy. This decline was driven by reductions in electricity and city gas prices, which fell by -20.5% yoy and -20.6% yoy, respectively, largely due to government subsidies.

NZ BNZ manufacturing falls to 43.1, 10th month of contraction

New Zealand's BusinessNZ Performance of Manufacturing Index fell from 46.5 to 43.1 in December. This latest figure marks a continued contraction in the manufacturing sector, which has now been shrinking for ten consecutive months.

The index components reveal a widespread decline across various manufacturing activities. Production fell from 43.5 to 40.5. Employment decreased from 47.9 to 46.7. New orders dropped from 47.4 to 44.0. Similarly, finished stocks and deliveries both saw declines, from 50.4 to 45.9 and 47.8 to 43.4, respectively.

Manufacturers' feedback further underscored the industry's challenges, with 61% of the comments in December being negative. This is a slight increase from 58.7% in November, though an improvement from 65.1% in October. The predominant concerns revolved around a lack of demand and sales, which have been significant hurdles for many manufacturers.

Stephen Toplis, BNZ's Head of Research, echoed these sentiments in his assessment of the PMI data. "The December PMI reaffirms our view that economic conditions remain very difficult," he stated. Toplis anticipates that while the economy and the manufacturing sector might gain some momentum by the end of 2024, the immediate future appears challenging, particularly with pressures in retail spending and construction activity.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2666; (P) 1.2688; (R1) 1.2727; More...

GBP/USD is staying in range above 1.2595 support and intraday bias remains neutral. On the downside, firm break of 1.2595 will resume the decline from 1.2826 to 1.2499 support. Nevertheless, strong rebound from current level will retain near term bullishness. Decisive break of 1.2826 will resume whole rally from 1.2036.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Dec | 43.1 | 46.7 | 46.5 | |

| 23:30 | JPY | National CPI Y/Y Dec | 2.60% | 2.80% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Dec | 2.30% | 2.30% | 2.50% | |

| 23:30 | JPY | National CPI ex Food & Energy Y/Y Dec | 3.70% | 3.80% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Nov | -0.70% | 0.20% | -0.80% | -0.20% |

| 07:00 | GBP | Retail Sales M/M Dec | -3.20% | -0.50% | 1.30% | 1.40% |

| 07:00 | EUR | Germany PPI M/M Dec | -1.20% | -0.50% | -0.50% | |

| 07:00 | EUR | Germany PPI Y/Y Dec | -8.60% | -7.90% | -7.90% | |

| 07:30 | CHF | Producer and Import Prices M/M Dec | -0.60% | -0.60% | -0.90% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Dec | -1.10% | -1.30% | ||

| 13:30 | CAD | Retail Sales M/M Nov | -0.20% | 0.00% | 0.70% | 0.50% |

| 13:30 | CAD | Retail Sales ex Autos M/M Nov | -0.50% | -0.10% | 0.60% | 0.40% |

| 15:00 | USD | Existing Home Sales Dec | 3.82M | 3.82M | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Jan P | 69.6 | 69.7 |