Sample Category Title

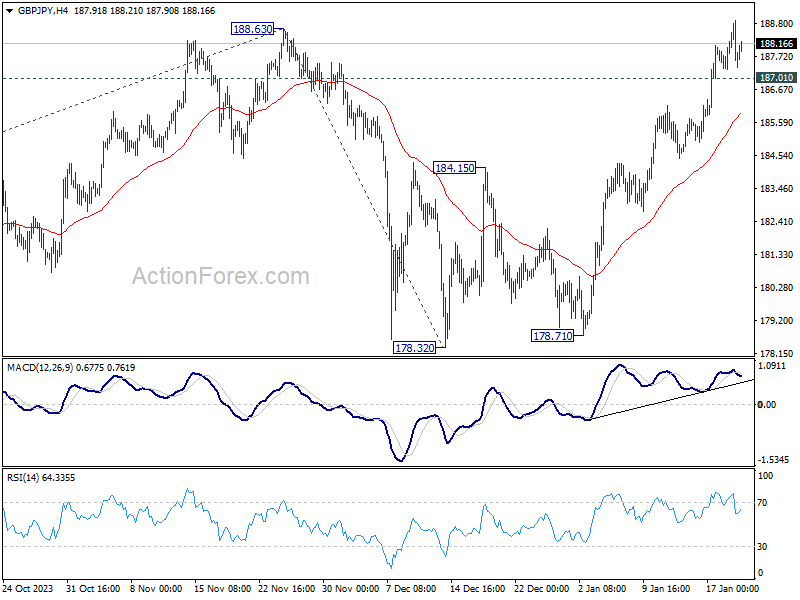

GBP/JPY Weekly Outlook

GBP/JPY's rise from 178.32 continued last week and breach of 188.63 argues that larger up trend is resuming. Initial bias stays on the upside this week. Sustained trading above 188.63 will confirm this case and target 38.2% projection of 155.33 to 188.63 from 178.32 at 191.04. On the downside, below 1187.01 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 184.15 resistance turned support holds, in case of retreat.

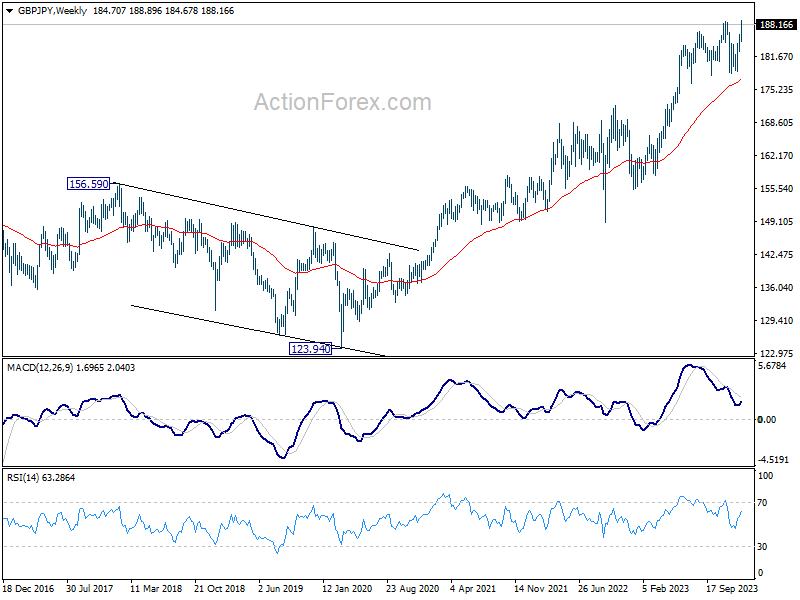

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

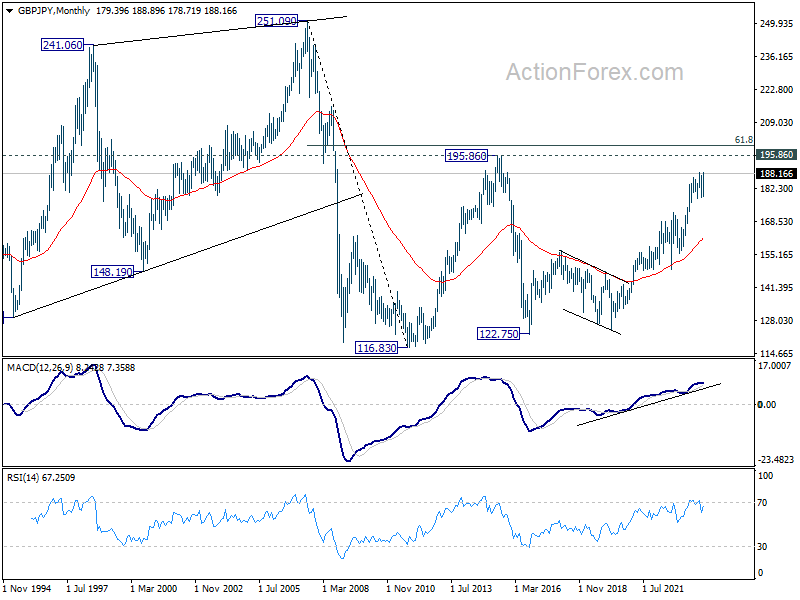

In the longer term picture, rise from 122.75 (2016 low) in still in progress despite loss of upside momentum as seen in W MACD. Further rise will remain in favor, as long as 172.11 support holds, to retest 195.86 (2015 high).

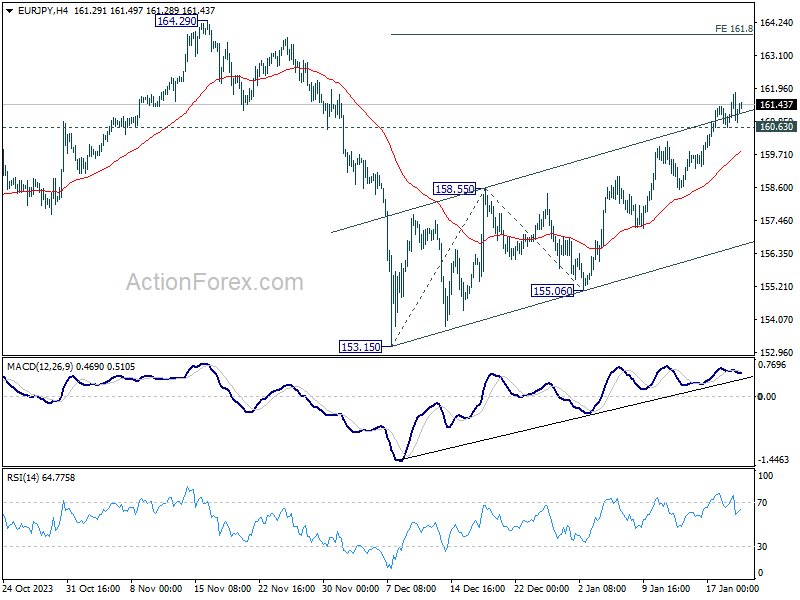

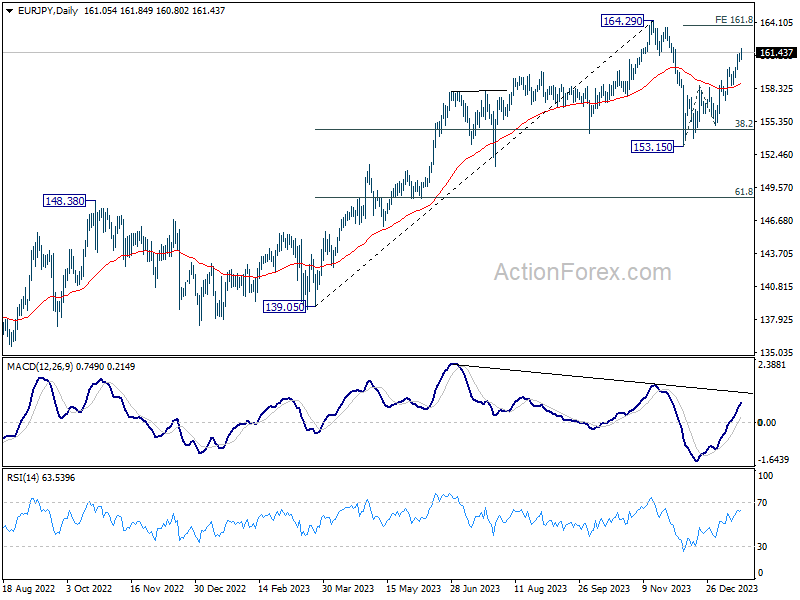

EUR/JPY Weekly Outlook

EUR/JPY's rise from 153.15 extended higher last week. Initial bias stays on the upside this week for 161.8% projection of 153.15 to 158.55 from 155.06 at 163.79, which is close to 164.29 high. On the downside, below 160.03 minor support will turn intraday bias neutral first. But further rally is expected as long as 158.55 resistance turned support holds.

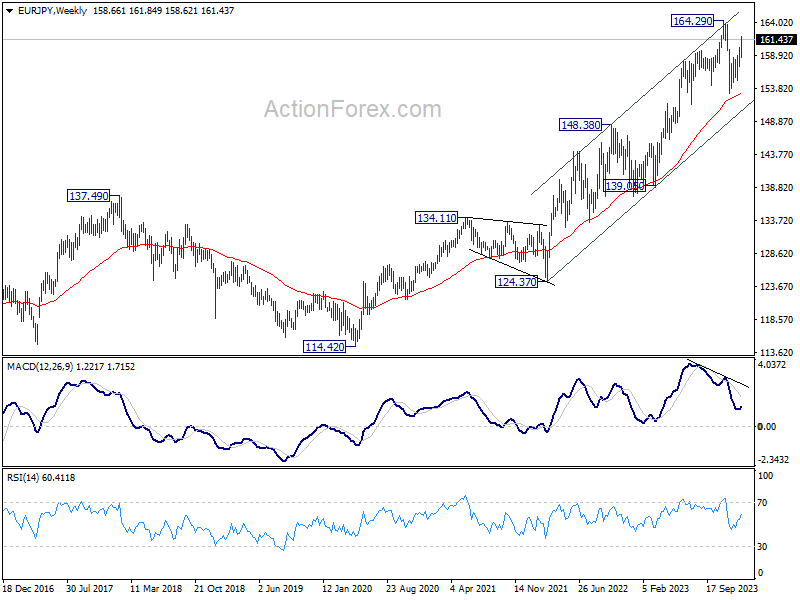

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.

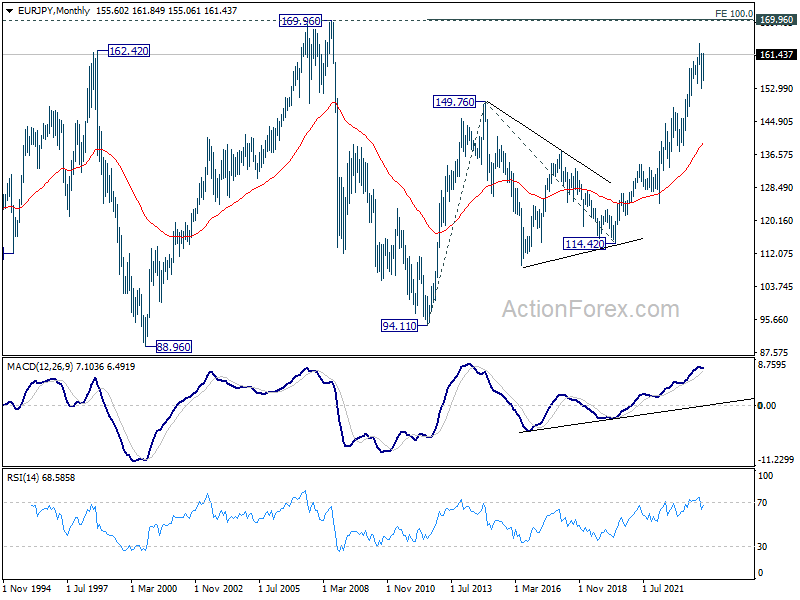

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 148.48 resistance turned support holds.

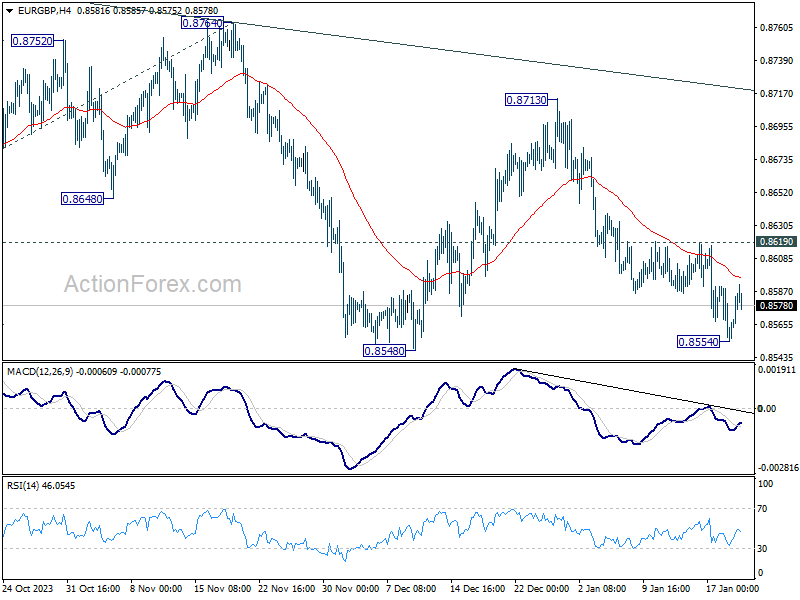

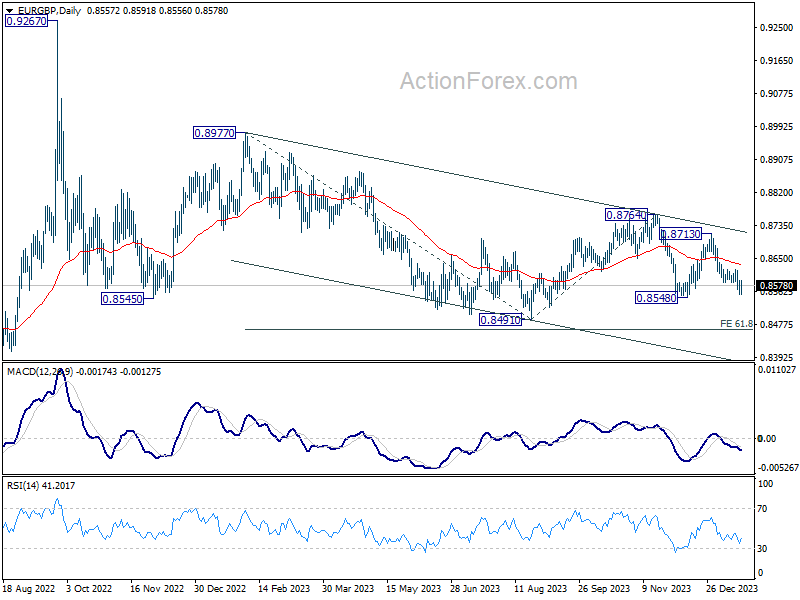

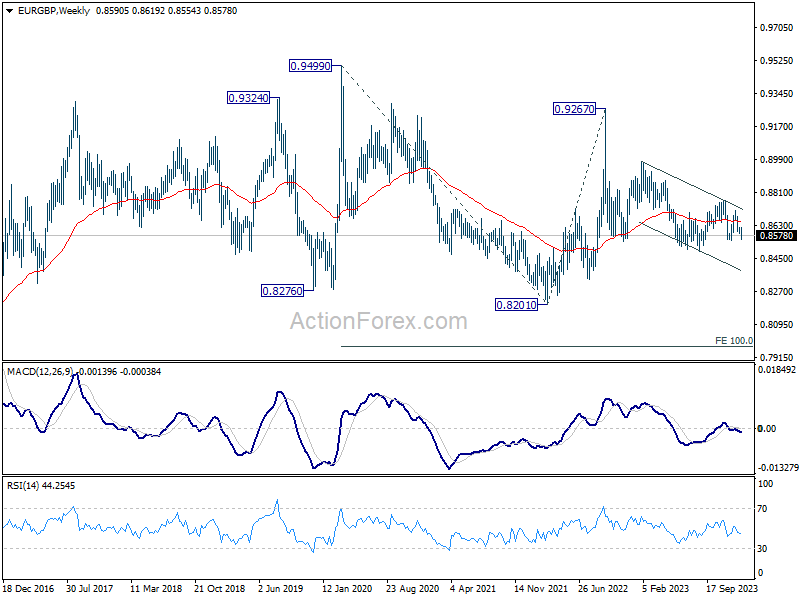

EUR/GBP Weekly Outlook

EUR/GBP's decline from 0.8713 extended to 0.8554 last week but recovered ahead of 0.8548 support. Initial bias remains neutral and some consolidations could be seen first. Deeper fall is expected as long as 0.8619 resistance holds. Firm break of 0.8548 will indicate that larger down trend is ready to resume through 0.8491 low. However, break of 0.8619 will dampen this view and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Fall from 0.9267 is the third leg of the pattern from 0.9499. Break of 0.8201 (2022 low) will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969.

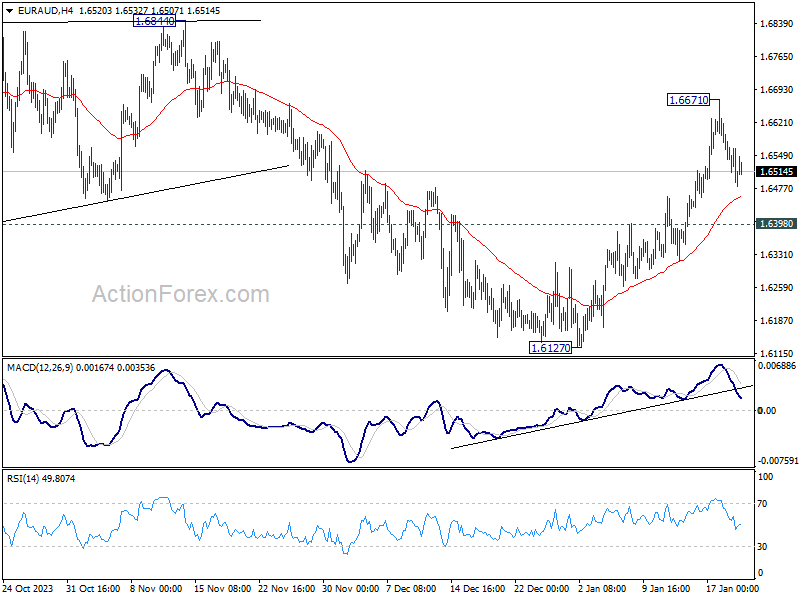

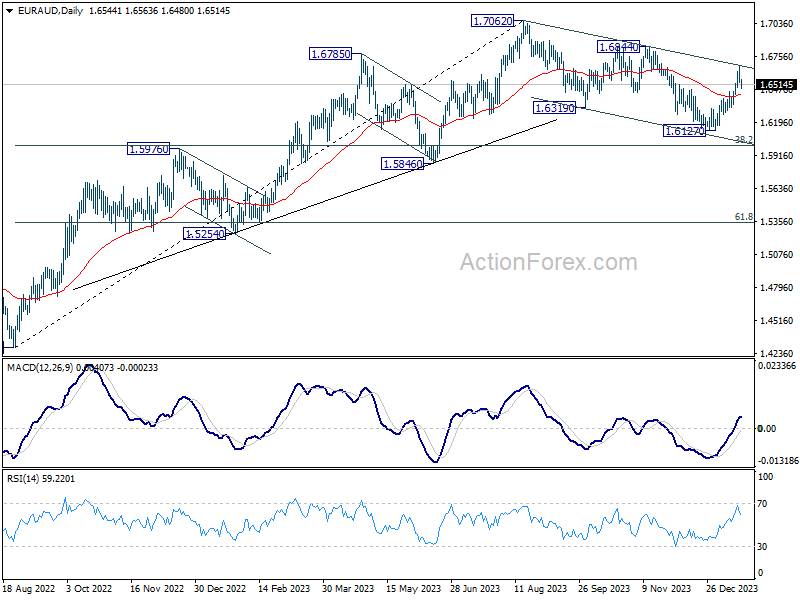

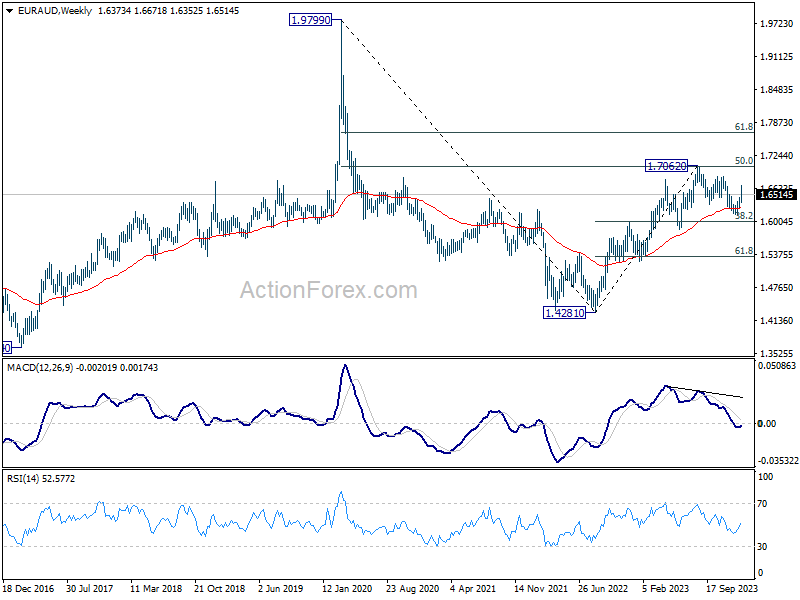

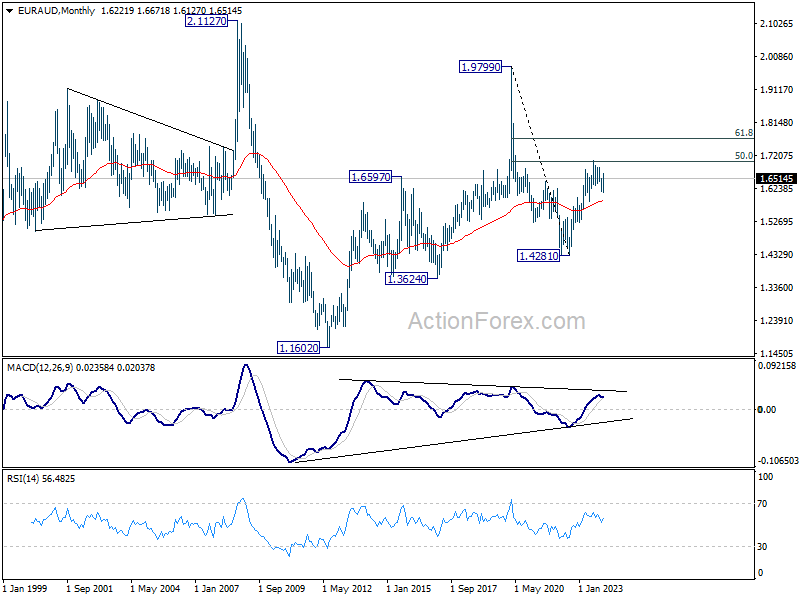

EUR/AUD Weekly Outlook

EUR/AUD's rises further to as high as 1.6671 last week before retreating. The development suggests that corrective fall from 1.7062 has completed with three waves down to 1.6127 already. Further rise is expected as long as 1.6398 support holds. Above 1.6671 will target 1.6844 resistance to confirm this bullish case.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

In the longer term picture, price actions from 1.9799 (2020 high) is seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5858) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

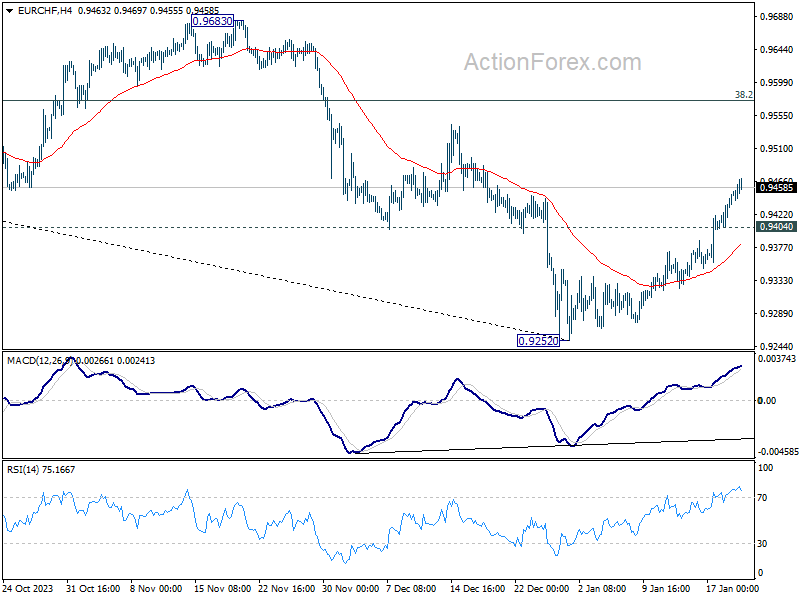

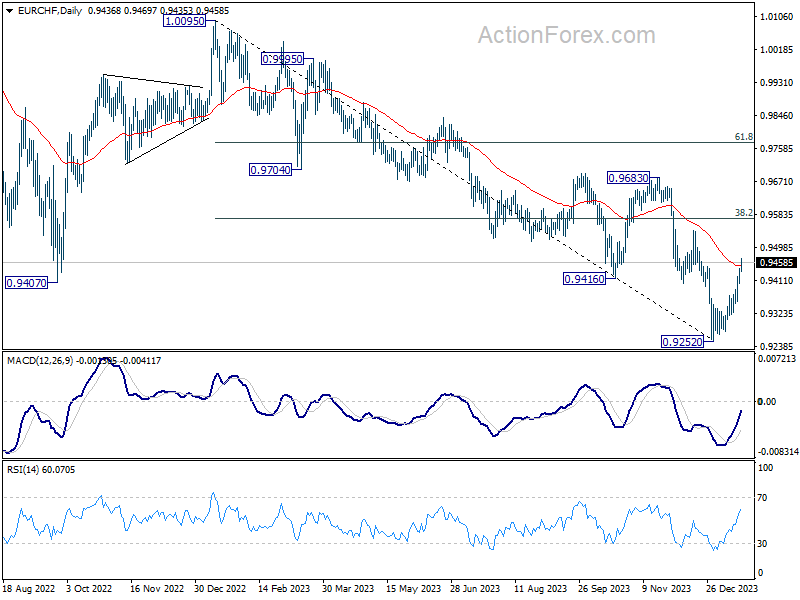

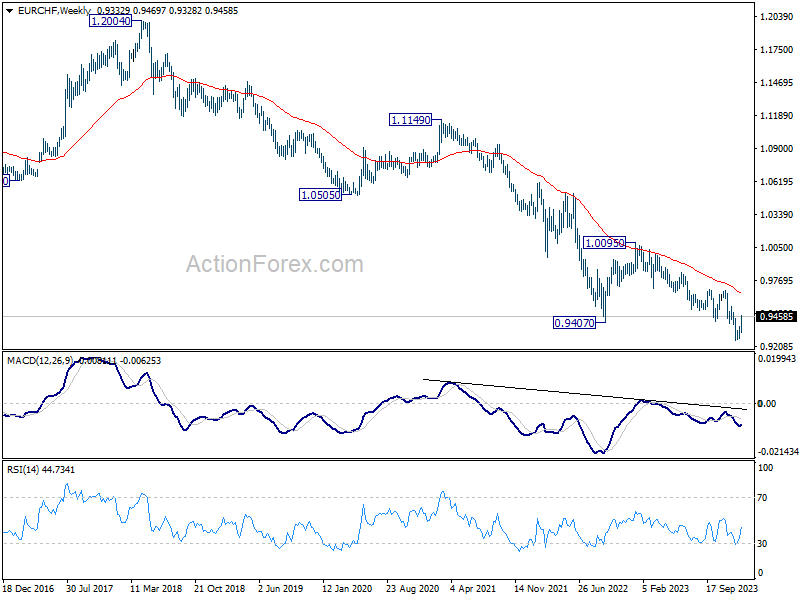

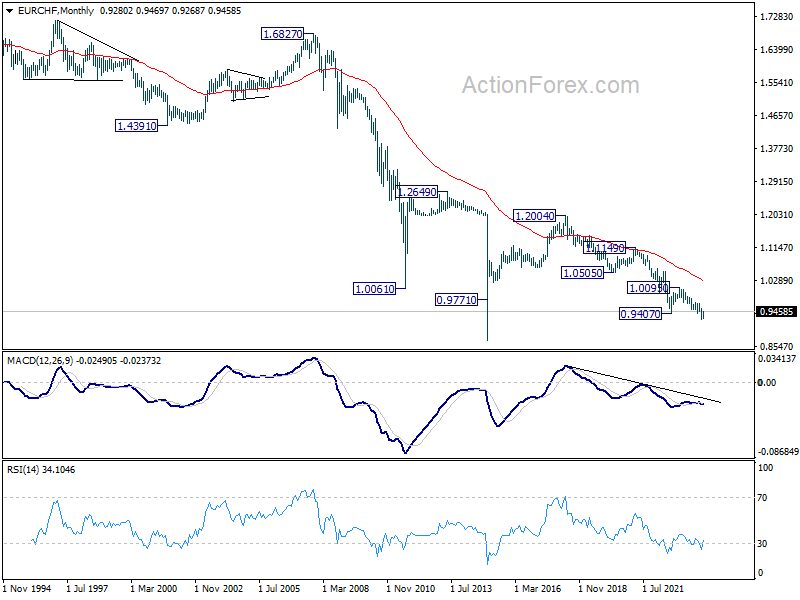

EUR/CHF Weekly Outlook

EUR/CHF's rebound from 0.9252 short term bottom extended higher last week. The break of 55 D EMA (now at 0.9449) argues that it's correcting whole down trend from 1.0095. Initial bias stays on the upside this week for 38.2% retracement of 1.0095 to 0.9252 at 0.9574. On the downside, below 0.9404 minor support will turn intraday bias neutral first.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Another decline is in favor after rebound from 0.9252 completes. However, firm break of 0.9683, and sustained trading above 55 W EMA (now at 0.9666) will argue that EUR/CHF is already in a medium term rally, even as a corrective move.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0265). Larger down trend from 1.2004 (2018 high) is in progress.

Summary 1/22 – 1/26

Monday, Jan 22, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 15:00 | USD | Leading Index M/M Dec | -0.30% | -0.50% |

| 21:30 | NZD | Business NZ PSI Dec | 51.2 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 15:00 | USD | Leading Index M/M Dec | |

| Forecast: -0.30% | Previous: -0.50% | ||

| 21:30 | NZD | Business NZ PSI Dec | |

| Forecast: | Previous: 51.2 | ||

Tuesday, Jan 23, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | |

| 00:30 | AUD | NAB Business Conditions Dec | 9 | |

| 00:30 | AUD | NAB Business Confidence Dec | -9 | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Dec | 11.2B | 13.4B |

| 13:30 | CAD | New Housing Price Index M/M Dec | 0.00% | -0.20% |

| 15:00 | EUR | Eurozone Consumer Confidence Jan P | -14 | -15 |

| 21:45 | NZD | CPI Q/Q Q4 | 0.50% | 1.80% |

| 21:45 | NZD | CPI Y/Y Q4 | 4.70% | 5.60% |

| 22:00 | AUD | Manufacturing PMI Jan P | 47.6 | |

| 22:00 | AUD | Services PMI Jan P | 47.1 | |

| 23:50 | JPY | Trade Balance (JPY) Dec | -0.45T | -0.41T |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: -0.10% | Previous: -0.10% | ||

| 00:30 | AUD | NAB Business Conditions Dec | |

| Forecast: | Previous: 9 | ||

| 00:30 | AUD | NAB Business Confidence Dec | |

| Forecast: | Previous: -9 | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Dec | |

| Forecast: 11.2B | Previous: 13.4B | ||

| 13:30 | CAD | New Housing Price Index M/M Dec | |

| Forecast: 0.00% | Previous: -0.20% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Jan P | |

| Forecast: -14 | Previous: -15 | ||

| 21:45 | NZD | CPI Q/Q Q4 | |

| Forecast: 0.50% | Previous: 1.80% | ||

| 21:45 | NZD | CPI Y/Y Q4 | |

| Forecast: 4.70% | Previous: 5.60% | ||

| 22:00 | AUD | Manufacturing PMI Jan P | |

| Forecast: | Previous: 47.6 | ||

| 22:00 | AUD | Services PMI Jan P | |

| Forecast: | Previous: 47.1 | ||

| 23:50 | JPY | Trade Balance (JPY) Dec | |

| Forecast: -0.45T | Previous: -0.41T | ||

Wednesday, Jan 24, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Dec | 0.10% | |

| 00:30 | JPY | Manufacturing PMI Jan P | 48.2 | 47.9 |

| 00:30 | JPY | Services PMI Jan P | 51.5 | |

| 08:15 | EUR | France Manufacturing PMI Jan P | 42.5 | 42.1 |

| 08:15 | EUR | France Services PMI Jan P | 46.0 | 45.7 |

| 08:30 | EUR | Germany Manufacturing PMI Jan P | 43.7 | 43.3 |

| 08:30 | EUR | Germany Services PMI Jan P | 49.5 | 49.3 |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan P | 44.8 | 44.4 |

| 09:00 | EUR | Eurozone Services PMI Jan P | 49.1 | 48.8 |

| 09:30 | GBP | Manufacturing PMI Jan P | 46.7 | 46.2 |

| 09:30 | GBP | Services PMI Jan P | 53.5 | 53.4 |

| 14:45 | CAD | BoC Interest Rate Decision | 5.00% | 5.00% |

| 14:45 | USD | Manufacturing PMI Jan P | 47.7 | 47.9 |

| 14:45 | USD | Services PMI Jan P | 51.1 | 51.4 |

| 15:30 | USD | Crude Oil Inventories | -2.5M | |

| 15:30 | CAD | BoC Press Conference |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Dec | |

| Forecast: | Previous: 0.10% | ||

| 00:30 | JPY | Manufacturing PMI Jan P | |

| Forecast: 48.2 | Previous: 47.9 | ||

| 00:30 | JPY | Services PMI Jan P | |

| Forecast: | Previous: 51.5 | ||

| 08:15 | EUR | France Manufacturing PMI Jan P | |

| Forecast: 42.5 | Previous: 42.1 | ||

| 08:15 | EUR | France Services PMI Jan P | |

| Forecast: 46.0 | Previous: 45.7 | ||

| 08:30 | EUR | Germany Manufacturing PMI Jan P | |

| Forecast: 43.7 | Previous: 43.3 | ||

| 08:30 | EUR | Germany Services PMI Jan P | |

| Forecast: 49.5 | Previous: 49.3 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Jan P | |

| Forecast: 44.8 | Previous: 44.4 | ||

| 09:00 | EUR | Eurozone Services PMI Jan P | |

| Forecast: 49.1 | Previous: 48.8 | ||

| 09:30 | GBP | Manufacturing PMI Jan P | |

| Forecast: 46.7 | Previous: 46.2 | ||

| 09:30 | GBP | Services PMI Jan P | |

| Forecast: 53.5 | Previous: 53.4 | ||

| 14:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 5.00% | Previous: 5.00% | ||

| 14:45 | USD | Manufacturing PMI Jan P | |

| Forecast: 47.7 | Previous: 47.9 | ||

| 14:45 | USD | Services PMI Jan P | |

| Forecast: 51.1 | Previous: 51.4 | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -2.5M | ||

| 15:30 | CAD | BoC Press Conference | |

| Forecast: | Previous: | ||

Thursday, Jan 25, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | RBA Bulletin Q4 | ||

| 09:00 | EUR | Germany IFO Business Climate Jan | 86.7 | 86.4 |

| 09:00 | EUR | Germany IFO Current Assessment Jan | 88.6 | 88.5 |

| 09:00 | EUR | Germany IFO Expectations Jan | 84.9 | 84.3 |

| 13:15 | EUR | ECB Main Refinancing Rate | 4.50% | 4.50% |

| 13:30 | USD | Initial Jobless Claims (Jan 19) | 199K | 187K |

| 13:30 | USD | GDP Annualized Q4 P | 2.00% | 4.90% |

| 13:30 | USD | GDP Price Index Q4 P | 2.20% | 3.30% |

| 13:30 | USD | Goods Trade Balance (USD) Dec P | -88.7B | -90.3B |

| 13:30 | USD | Wholesale Inventories Dec P | -0.20% | -0.20% |

| 13:30 | USD | Durable Goods Orders Dec | 1.00% | 5.40% |

| 13:30 | USD | Durable Goods Orders ex Transport Dec | 0.20% | 0.40% |

| 13:45 | EUR | ECB Press Conference | ||

| 15:00 | USD | New Home Sales Dec | 646K | 590K |

| 15:30 | USD | Natural Gas Storage | -154B | |

| 23:30 | JPY | Tokyo CPI Y/Y Jan | 2.40% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jan | 1.90% | 2.10% |

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Jan | 3.50% | |

| 23:50 | JPY | Corporate Service Price Index Y/Y Dec | 2.40% | 2.30% |

| 23:50 | JPY | BoJ minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | RBA Bulletin Q4 | |

| Forecast: | Previous: | ||

| 09:00 | EUR | Germany IFO Business Climate Jan | |

| Forecast: 86.7 | Previous: 86.4 | ||

| 09:00 | EUR | Germany IFO Current Assessment Jan | |

| Forecast: 88.6 | Previous: 88.5 | ||

| 09:00 | EUR | Germany IFO Expectations Jan | |

| Forecast: 84.9 | Previous: 84.3 | ||

| 13:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 19) | |

| Forecast: 199K | Previous: 187K | ||

| 13:30 | USD | GDP Annualized Q4 P | |

| Forecast: 2.00% | Previous: 4.90% | ||

| 13:30 | USD | GDP Price Index Q4 P | |

| Forecast: 2.20% | Previous: 3.30% | ||

| 13:30 | USD | Goods Trade Balance (USD) Dec P | |

| Forecast: -88.7B | Previous: -90.3B | ||

| 13:30 | USD | Wholesale Inventories Dec P | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 13:30 | USD | Durable Goods Orders Dec | |

| Forecast: 1.00% | Previous: 5.40% | ||

| 13:30 | USD | Durable Goods Orders ex Transport Dec | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 13:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 15:00 | USD | New Home Sales Dec | |

| Forecast: 646K | Previous: 590K | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -154B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Jan | |

| Forecast: | Previous: 2.40% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jan | |

| Forecast: 1.90% | Previous: 2.10% | ||

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Jan | |

| Forecast: | Previous: 3.50% | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Dec | |

| Forecast: 2.40% | Previous: 2.30% | ||

| 23:50 | JPY | BoJ minutes | |

| Forecast: | Previous: | ||

Friday, Jan 26, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Jan | -21 | -22 |

| 07:00 | EUR | Germany Gfk Consumer Confidence Feb | -24.3 | -25.1 |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Dec | -0.70% | -0.90% |

| 13:30 | USD | Personal Income M/M Dec | 0.30% | 0.40% |

| 13:30 | USD | Personal Spending Dec | 0.40% | 0.20% |

| 13:30 | USD | PCE Price Index M/M Dec | 0.20% | -0.10% |

| 13:30 | USD | PCE Price Index Y/Y Dec | 2.60% | 2.60% |

| 13:30 | USD | Core PCE Price Index M/M Dec | 0.20% | 0.10% |

| 13:30 | USD | Core PCE Price Index Y/Y Dec | 3.00% | 3.20% |

| 15:00 | USD | Pending Home Sales M/M Dec | 1.60% | 0.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Jan | |

| Forecast: -21 | Previous: -22 | ||

| 07:00 | EUR | Germany Gfk Consumer Confidence Feb | |

| Forecast: -24.3 | Previous: -25.1 | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Dec | |

| Forecast: -0.70% | Previous: -0.90% | ||

| 13:30 | USD | Personal Income M/M Dec | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 13:30 | USD | Personal Spending Dec | |

| Forecast: 0.40% | Previous: 0.20% | ||

| 13:30 | USD | PCE Price Index M/M Dec | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 13:30 | USD | PCE Price Index Y/Y Dec | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 13:30 | USD | Core PCE Price Index M/M Dec | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 13:30 | USD | Core PCE Price Index Y/Y Dec | |

| Forecast: 3.00% | Previous: 3.20% | ||

| 15:00 | USD | Pending Home Sales M/M Dec | |

| Forecast: 1.60% | Previous: 0.00% | ||

The Weekly Bottom Line: A Resilient Consumer Dims Hopes for an Early Rate Cut

U.S. Highlights

- Higher than expected retail sales in December suggests that consumer spending remained resilient to end the year.

- Several Fed governors sought to push back against market expectations for swift and significant rate cuts.

- The housing market ended 2023 on a sour note, with both new home construction and existing home sales falling in December.

Canadian Highlights

- Bank of Canada (BoC) rate cut odds took a hit this week as stronger than expected data caused a selloff in bond markets.

- Inflation data got a lot of attention, as the BoC’s core measures moved higher in December - not the kind of move the BoC was looking for.

- Housing data also surprised higher. With sales rebounding, the average home price rose for the first time since last spring.

U.S. – A Resilient Consumer Dims Hopes for an Early Rate Cut

Just when you think the U.S. consumer might yield to mounting pressures currently buffeting their balance sheets, they surprise by closing out 2023 on a retail spending binge. The increased spending kept the economy on firm ground and suggests a solid hand off heading into the new year. It also caused investors to pare back expectations for a March rate cut and pushed U.S. Treasury yields higher.

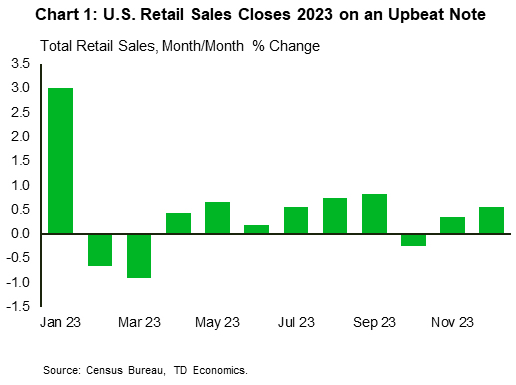

Retail sales rose 0.6% month-on-month in December, following a 0.3% gain in November (Chart 1). The breadth of the increase was also noteworthy with 9 out of the 13 categories recording gains. The “control group” which factors into the calculation of personal consumption expenditure rose an even more impressive 0.8% on the month. The stellar number suggests that consumer spending grew at a healthy clip of around 2.5% (annualized) in Q4.

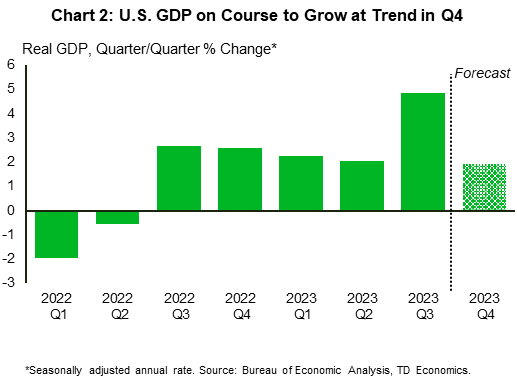

The stronger than expected retail sales report has resulted in upward revisions to expectations of Q4 GDP growth. After the report, the Atlanta Fed’s GDPNow growth estimate rose to 2.4% (from 2.2%), while our own estimate currently sits at 1.9%. (Chart 2). We won’t have to wait long to know for sure though, as the BEA is set to release the advance estimate of Q4 GDP next Thursday. Given expectations for the print to be relatively strong, there is even less pressure on the Fed to entertain rate cuts over the coming months.

The slew of Fed speakers making the rounds this week were quick to reinforce that point. “With economic activity and labor markets in good shape and inflation coming down gradually” Governor Waller sees “no reason to move as quickly or cut as rapidly as in the past.” He used terms such as “carefully calibrated and not rushed” and “lowered methodically and carefully” to push back against market expectations of sizeable cuts this year. Atlanta Fed President Bostic was on a similar page. He noted that rates could be cut earlier than Q3, “but the evidence would need to be convincing.” What’s more, he urged caution given the current uncertain environment (domestic budget battles, global conflict, elections etc.), which could have unpredictable economic impacts and re-ignite inflation pressures.

Turning to the housing sector, reports out this week showed housing activity ended a tumultuous year on a sour note. Housing starts fell in December reversing a portion of November’s gain, while existing home sales declined to a 14-year low. A dearth of available inventory and historically poor affordability are to blame for last year’s weak showing. However, with mortgage rates having come down by over 100 basis points from its mid-October peak, we’ve likely reached the bottom and should see some uptick in sales activity through 2024.

Ultimately, the timing and pace of rate cuts will depend on the strength of economic growth and inflationary pressures. This week’s data indicate that economic conditions are currently resilient. Last week’s CPI print shows there is still work to be done on the inflation front. The combination means that a policy pivot to rate cuts is unlikely to be top of mind for Fed officials just yet.

Canada – The Inflation Thorn Remains in the Side of the BoC

Bank of Canada (BoC) rate cut odds took a hit this week. Strong inflation readings alongside a surprising improvement in housing activity pushed BoC rate cut expectations from March to April. This forced a bond market selloff, as both the Canadian 2-year and 10-year yields shot-up more than 30 basis points ahead of next week's BoC decision.

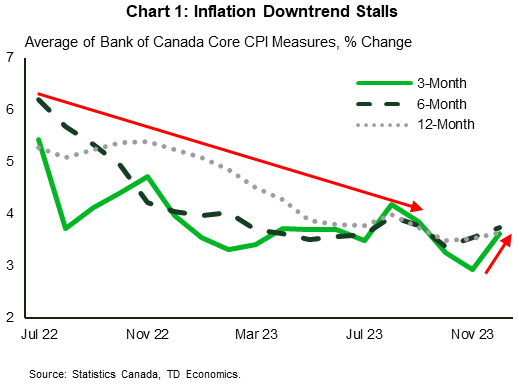

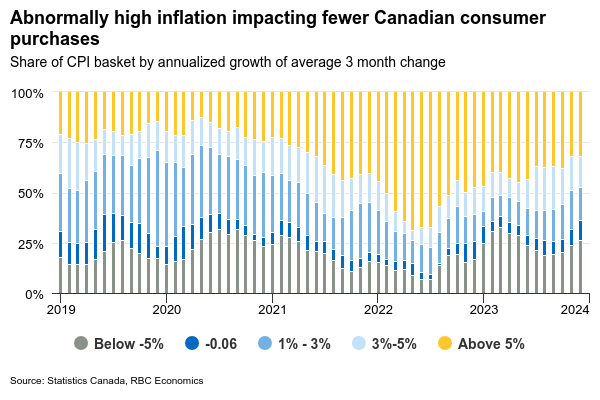

The December release of Canadian CPI got a lot of attention. Expectations were for annual inflation to move higher on base year effects (the impact of lower prices in December 2022). While this happened as expected, what took everyone by surprise was the shift higher in core inflation rates. The average of the BoC's core measures moved up a tenth, to 3.7% year-on-year (y/y). While this doesn't seem like much, the timelier three-month annualized rate rose from 2.9% to 3.6% (Chart 1). That was not the kind of move the BoC was looking for.

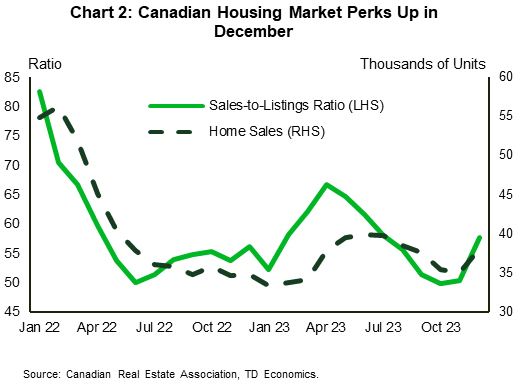

Housing data also surprised higher. Maybe it was the warmer December weather, maybe the hope that the BoC was gearing up to cut rates. Either way, home sales jumped nearly 9% month-on-month. This boost alongside a sizable drop in listings pushed market balance above its long-term average and closer to buyers' territory (Chart 2). This caused the average house price to rise for the first time since the BoC re-started rate hikes in June 2023.

Canadians have also been actively filling shopping malls. Retail sales data for November pointed to more consumers buying clothing, shoes, and jewelry - all the stuff that was in demand during the holiday shopping season. And while overall sales were held down by less spending at food retailers, it looks like December spending will more than offset any of that weakness.

This week's flow of data seems to be moving counter to the recent trend. Over the last 9 months, we had seen consumers pulling back as high mortgage rates reduced spending power. At the same time, the number of net-new job gains has come to a standstill. No surprise that the BoC's newly released surveys of consumer and business sentiment continued to weaken. Importantly, nearly 70% of consumers said they have already cut spending in the face of higher rates. Businesses echoed this sentiment, with many having reported that they are seeing outright sales declines for their products. This caused 'economic uncertainty' to become the top concern for firms in 2024.

Where does this leave the BoC for its meeting next week? Given the upturn in data, there is little impetus for the BoC to flip the script. It will maintain its cautiousness, focusing on how the job isn't done yet. That said, it can also hang its hat on how forward-looking indicators are pointing to greater weakness in the months ahead. Importantly, markets believe that this weakness will soon come through in the data. This belief has maintained expectations that the BoC will begin cutting rates by the spring, something that the Bank may try to lean against next week.

Weekly Economic & Financial Commentary: Consumers Just Keep Humming

Summary

United States: Consumers Just Keep Humming

- As market participants continue to digest last week's slightly hotter-than-expected consumer price data, activity data released this week show underlying demand was still humming along in the final stretch of 2023. Retail sales surprised to the upside and industrial production rose in December.

- Next week: GDP (Thu.), New Home Sales (Thu.), Personal Income & Spending (Fri.)

International: China's Underwhelming Economic Performance Could Continue

- China's Q4-2023 economic growth figures were modestly underwhelming, as GDP grew 1.0% quarter-over-quarter and 5.2% year-over-year, slightly below the consensus forecast.Weakness in consumption and the property sector have been constraining factors for China's economy, while a shrinking working age population and rising youth unemployment are also challenges. Against this backdrop, our view remains for China's GDP growth to be slower this year than in 2023.

- Next week: Bank of Japan Policy Announcement (Tue.), Bank of Canada Policy Rate (Wed.), European Central Bank Policy Rate (Thu.)

Interest Rate Watch: Talking Heads

- Despite it being a holiday-shortened week, five fed officials, four of whom are currently voting members of the FOMC, made public appearances. We unpack the highlights of those comments in this week’s Interest Rate Watch.

Topic of the Week: Another Punt on the FY 2024 Budget

- Lawmakers again resorted to a short-term patch to avoid a looming government shutdown this week. Congress passed a continuing resolution (CR) that pushes out the funding deadlines from January 19 to March 1 for four of the 12 annual appropriation bills, with the deadline for the remaining eight extended from February 2 to March 8.

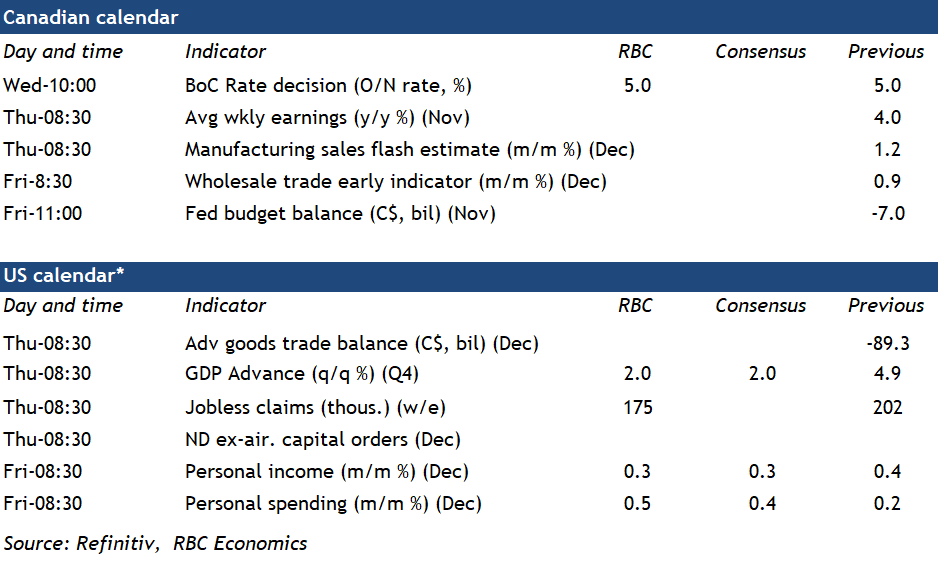

BoC to Hold Interest Rates Steady Again Next Week

The Bank of Canada is widely expected to hold the overnight rate steady at 5% in the first policy decision of 2024 – extending a pause that started following the last hike in July. The statement and press conference that follows will be watched closely for hints about how much longer the central bank expects to hold interest rates at these levels, although we expect the BoC to push back against the idea that a shift to interest rate cuts is coming soon. There is some potential that the central bank could hint at an earlier-than-expected end to quantitative tightening policy but would likely take pains to communicate the primary objective of that change would be to ensure adequate liquidity in funding markets rather than flagging a shift to easier monetary policy and imminent rate cuts.

In terms of the actual setting of monetary policy, economic developments have been soft enough to reinforce that further interest rate hikes won’t be needed, but inflation (and wage growth) have also been too sticky to push the BoC to consider starting an easing cycle yet. Consumer prices rose 3.2% year-over-year in Q4, slightly below the 3.3% increase that was last projected by the central bank in October. But the details in the December inflation report – including a reacceleration in the closely-watched 3-month average increase in the BoC’s preferred core measures to the 3.5% to 4% range – was a reminder that inflation is not yet fully back under control.

The most likely trajectory for inflation going forward is still lower. Although the BoC’s preferred core measures looked worse in December, the share of the consumer price basket seeing unusually high inflation over the last three months continued to shrink. And a disproportionate share of price growth overall is coming from a surge in mortgage interest costs that is a direct result of earlier interest rate increases. An increasingly soft economic backdrop underpinned by slowing consumer demand, declining per-capita GDP, and higher unemployment offers good reasons to expect the broader downtrend in inflation readings to persist. Total hours worked contracted in Q4 for the first time since Q2 2020, flagging downside risk to the BoC’s prior forecast for a 0.8% Q4 GDP gain. But the BoC will be cautious about declaring victory over inflation too soon. We expect the first decrease in the overnight rate to come around the middle of this year, and for that to be followed by 75 bps more later in the year to lower the overnight rate to 4% by the end of 2024.

Week ahead data watch

U.S. consumer spending (nominal) likely edged up 0.5% in December, given stronger retail sales increase during that month. Wage growth bounced back by 0.4% in December, and we expect the personal income (+0.3%) to go up as well.

We are currently tracking 2% annualized increase for U.S. GDP in Q4 2023, supported by a robust gain in consumer spending. Residential investment likely continued to grow on higher housing starts, albeit at a slower rate than in the prior quarter.

November SEPH report will be watched closely for further softening in the labour demand in Canada -we expect the level of job openings to continue to decline.

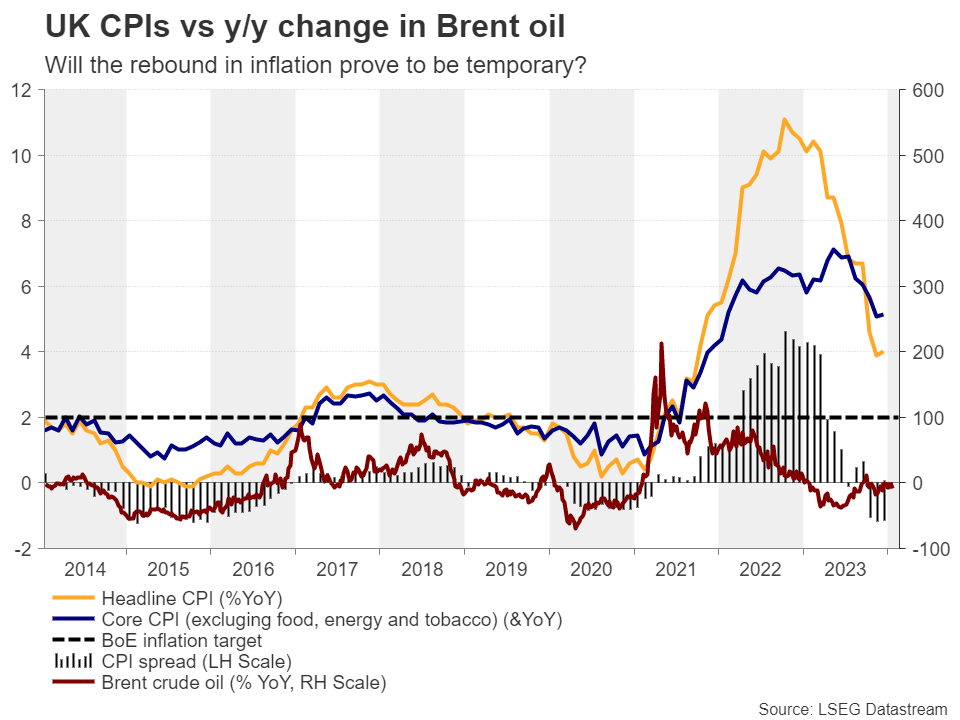

UK PMIs to Reveal How the British Economy Entered the New Year

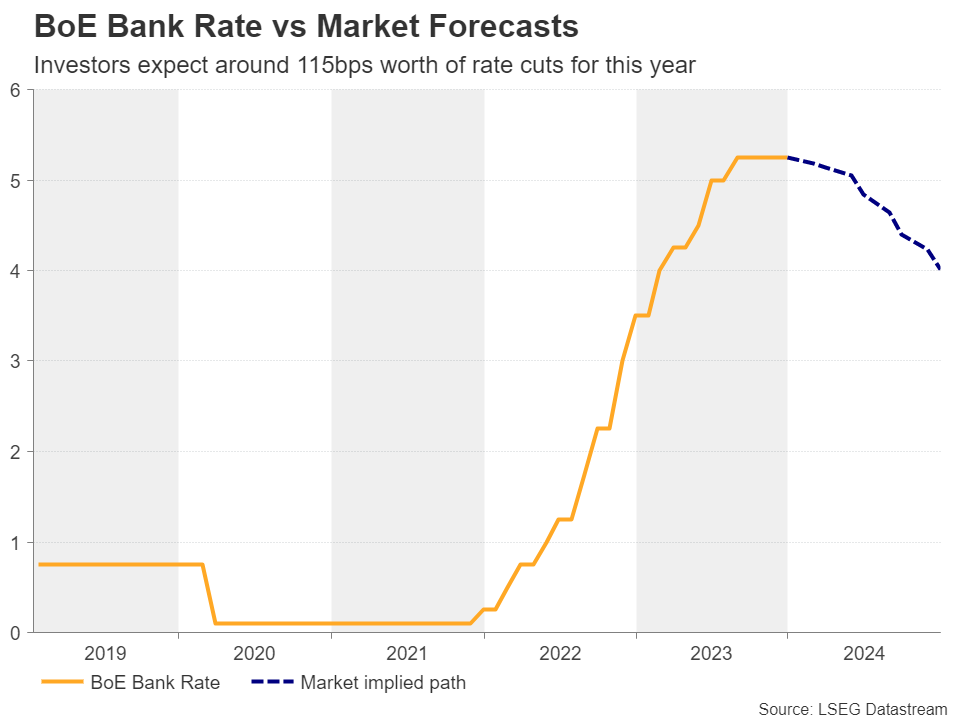

- Investors scale back BoE rate cut bets after CPI data

- But disappointing retail sales revive some recession fears

- Pound traders may now turn attention the UK flash PMIs

- The data comes out on Wednesday at 09:30 GMT

Hotter-than-expected inflation, but disappointing retail sales

After the hotter than expected UK CPI data for December, investors scaled back their Bank of England rate cut bets, lowering the total basis points worth of reductions expected by the end of the year to 115 from 125 and the probability of the first quarter-point reduction to be delivered in May to 55% from around 90%.

That said, on Friday, retail sales for the same month disappointed and according to the Office of National Statistics (ONS), they are likely to subtract 0.04 percentage points from the UK economic output in the fourth quarter. Given that the National Institute of Economic and Social Research (NIESR) tracker has been pointing to a stagnant economy ahead of the release, this could make the difference between a flat or a negative figure.

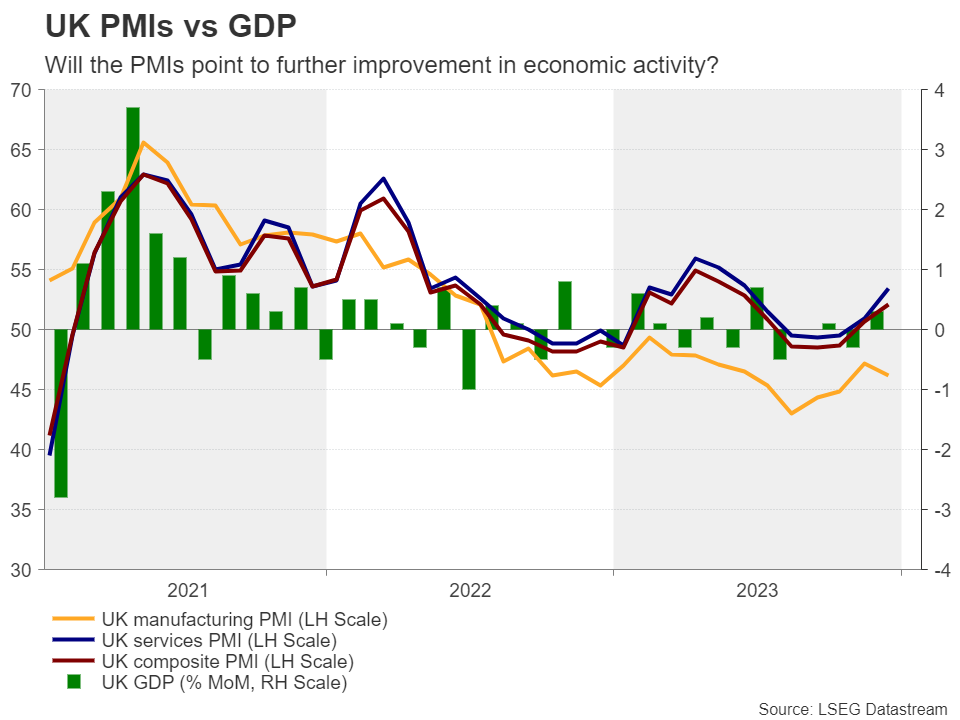

Although retail sales may have revived concerns with regards to a potential recession, investors did not add back to their BoE rate cut bets. Perhaps the rebound in the November monthly GDP and the improvement in the December composite PMI acted as safety barriers.

UK Flash PMIs the next focal point for pound traders

With all that in mind and taking into account that the NIESR is forecasting GDP to grow by 0.2% in the first quarter of 2024, on Wednesday, pound traders may focus on the preliminary PMIs for January, as this would be the first information on how the UK economy entered the new year.

Apart from the headline prints, the employment and prices sub-indices may also be of high importance as they could provide a glimpse of whether the rebound in the December inflation prints was only due to base effects and will prove to be temporary, or whether inflation will prove to be stickier than previously anticipated.

Will the data help the pound gain more ground?

Numbers suggesting that the economic activity is faring better than it did during the second half of 2023 and sub-indices pointing to still-sticky inflation may convince investors that the BoE is right in not discussing the prospect of lower interest rates so soon. The probability of a May cut could further decline, and the pound could gain some more ground.

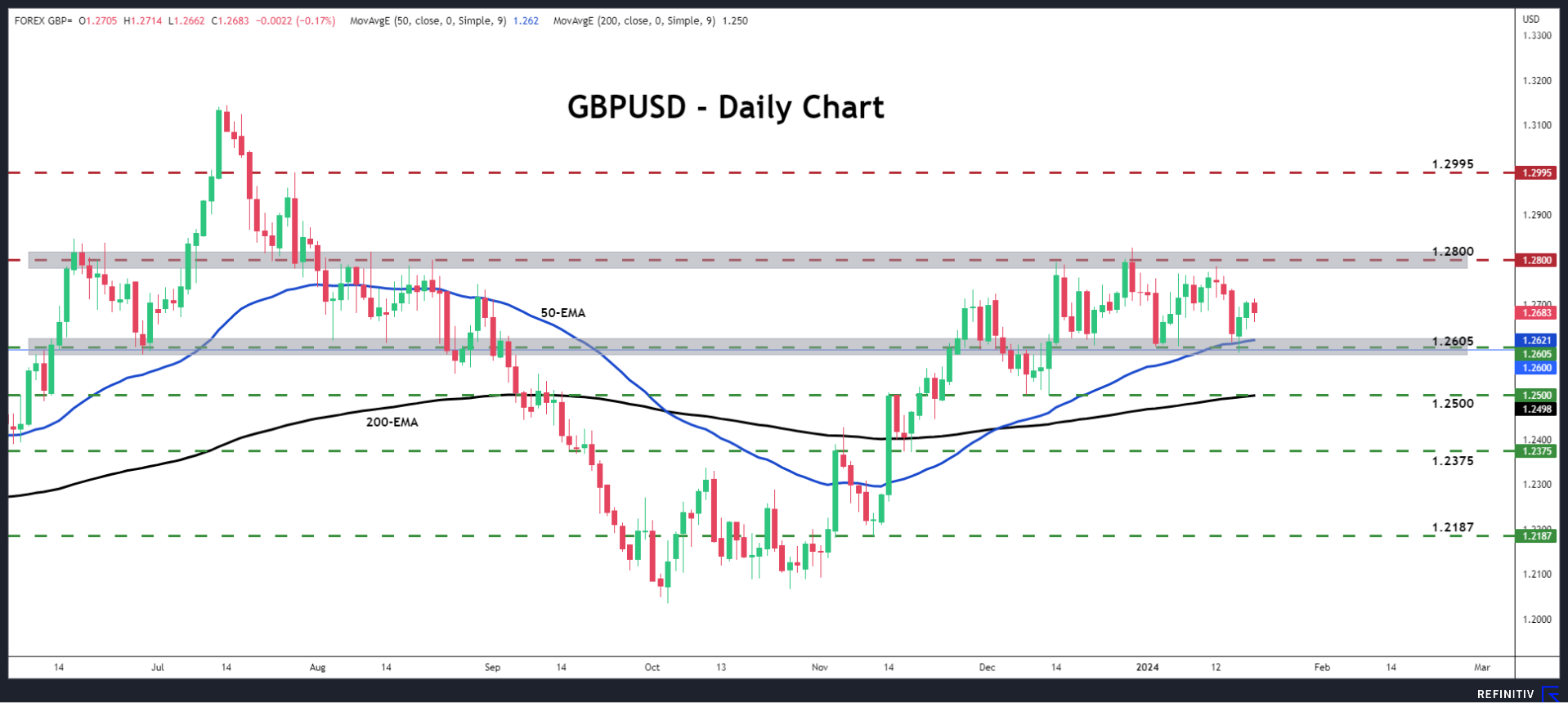

Pound/dollar has been oscillating between 1.2605 and 1.2800 since December 14, two barriers that acted as support and resistance several times in the past. After the hotter-than-expected CPI numbers, the pair rebounded from the lower end of that range and despite the pullback on the worse-than-expected retail sales data, encouraging PMIs may allow another round of advances, perhaps towards the upper bound at around 1.2800.

Nonetheless, for the outlook of this pair to turn positive again, a break above that zone may be needed. Such a move would confirm a higher high on the daily chart and may carry extensions towards the high of July 27 at around 1.2995. Alternatively, a dip below 1.2605 may turn the picture bearish and encourage the sellers to push the action towards the 1.2500 area.