Sample Category Title

Cliff Notes: Labour Market Critical to Households’ Resilience

Key insights from the week that was.

The January edition of the Westpac-MI Consumer Sentiment Index showed cost-of-living pressures and concerns over elevated interested rates remain firmly entrenched in the minds of consumers. Highlighting the significance of these factors, at 81.0, the index is currently among the bottom 7% of observations since the inception of the survey in the 1970’s. Perceptions of ‘family finances versus a year ago’ are almost 30ppts below long-run average levels and expectations for the year ahead are 13ppts below average. It is unsurprising then ‘time to buy a major household item’ fell heavily in the month to be 37ppts below average. In 2023, the labour market provided a degree of insulation against cost pressures, offering opportunities to find a better job or pick up more hours. Views here are beginning to shift however, the Unemployment Expectations Index softening to 130.7 in January, a result slightly above the long-run average.

That development is consistent with the overarching tone of the December Labour Force Survey. The seasonally adjusted headline figures from the survey were impacted by shifts in seasonal patterns into year-end, perhaps a consequence of the growing prominence of Black Friday Sales. Abstracting from this volatility, both employment growth and hours worked are slowing and the unemployment rate is drifting higher. While these dynamics point to emerging slack, the labour market is still very tight versus history and remains a critical support to households. Inflation continuing to trend lower, as forecast, will allow modest policy easing by the RBA from the September quarter, aiding activity and limiting excess capacity in the labour market.

In the UK, the CPI surprised to the upside rising 4.0%yr in December driven by recreation and culture as well as alcoholic beverages and tobacco. Energy prices continued to dampen the annual number, however. Inflation’s breadth is narrowing: 71% of the CPI basket grew above 2% compared to almost 90% at the start of 2023. But services inflation remains sticky and is now responsible for almost all inflation. Wages remain a concern for the inflation outlook. Data released this week showed wages growth has eased from 7.2%yr to a still-elevated 6.5%yr. Last week’s Decision Maker Panel survey also showed wage expectations edged up to 5.2%yr at the turn of the year. The BoE arguably has the most significant challenge across the developed world in reining in inflation.

In the US, anecdotes from the Federal Reserve’s Beige Book provided evidence of balance in the labour market with contacts reporting “larger applicant pools, lower turnover rates, more selective hiring by firms, and easing wage pressures”. Sentiment around prices was benign: consumer price sensitivity causing retail firms to reconsider pushing through increases in the cost of production, insurance premium hikes having a broad impact on bunesses cost across the economy.

While a majority of Federal Reserve Districts reported “little or no change in economic activity” in the latest survey period, retail sales beat expectations in December, total sales rising 0.6%mth and the control group (which feeds into GDP) 0.8%. For consumers, there is a growing tension between greater comfort with the cost of living (given mortgage rates are fixed for 30-years and inflation is returning to target) and growing uncertainty over job prospects. The net result is likely to be a period of below-trend consumption in 2024, though bursts of activity are still likely.

Of Fed speakers this week, Governor Christopher Waller’s remarks at the Brookings Institute received the most attention. Market participants viewed his discussion of current conditions and prior rate cutting cycles as an attempt to rein in the market’s expectations vis a vis both the timing and scale of rate cuts. We instead assess his intent as being focused on the extent of easing over 2024, with Governor Waller twice noting that the 3 and 6-month rate of core PCE inflation “has been hovering close to a 2 percent annual rate”, the FOMC’s target, where it is expected to remain in coming months.

To us, an effective way to manage expectations over the policy response to a soft landing is to cut in March but then signal in revised March forecasts that the decision was one of the three cuts the FOMC projected for calendar 2024 at the December 2023 meeting. Westpac’s view remains that four cuts will be delivered by the FOMC in 2024; even after this week’s data and remarks, the market still has almost six priced.

In Asia, Q4 GDP showed that the Chinese economy expanded by 5.2%yr, meeting the government's growth target of 'around 5%'. Fixed asset investment grew by a modest 3% overall, but investment in high-tech industries was much stronger at 10%, with some key sub-sectors related to electric vehicles and green power stronger still. China has focussed on research and development for goods related to the green transition over the past decade and is now ramping up capacity to meet burgeoning global demand.

This industrial strength is a striking contrast to the uncertainty that continues to burden consumers. There are promising signs regarding discretionary consumption, but households remain very cautious on housing’s outlook. An end to the now two-year contraction in house prices and investment will need additional support from authorities. Until this transpires, consumer demand will remain at risk given the hit household wealth has taken. All told, we remain of the view that China can achieve growth at or above 5% in 2024 and 2025 but, at least in the near-term, downside risks bear careful monitoring.

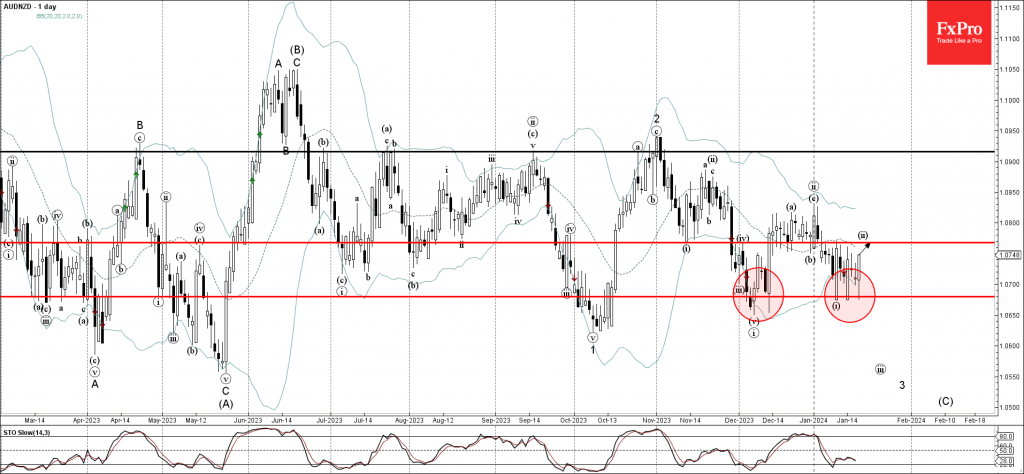

AUDNZD Wave Analysis

- AUDNZD reversed from support level 1.0680

- Likely to rise to resistance level 1.0770

AUDNZD currency pair recently reversed up from the strong support level 1.0680, which has been reversing the price from the start of December.

The support level 1.0680 was strengthened by the lower daily Bollinger Band.

Given the bullish divergence on the daily Stochastic indicator, AUDNZD can be expected to rise further to the next resistance level 1.0770, target for the completion of the active minor wave ii.

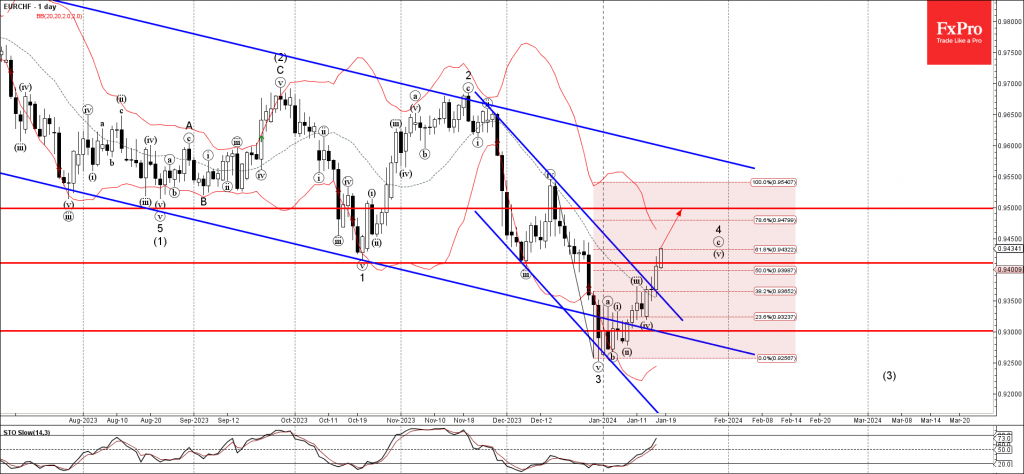

EURCHF Wave Analysis

- EURCHF broke resistance level 0.9410

- Likely to rise to resistance level 0.9500

EURCHF currency pair recently broke the key resistance level 0.9410 intersecting with the 50% Fibonacci correction of the previous downward impulse from December

The breakout of the resistance level 0.9410 accelerated the active short-term ABC correction 4.

Given the strong Swiss franc sales seen today, EURCHF can be expected to rise further to the next resistance level 0.9500 (target for the completion of the active wave 4).

ECB Preview: Stocktaking

Next week’s ECB meeting is set to see few, if any, new policy signals, given the limited

new information that has been released since the December meeting. We expect

President Lagarde to confirm that the next policy rate change is most likely a cut, which

may happen in summer. It remains to be seen whether the June meeting will be singled

out as the key meeting to watch, similar to Lane’s comments this weekend. We expect

Lagarde to repeat the three key criteria for setting the policy rates, which should point

to the new staff projections in March as key.

Markets are pricing the first ECB policy rate cut for April, and a total of 135bp through

to the end of 2024. The policy rates are priced to trough at 2% in two years’ time.

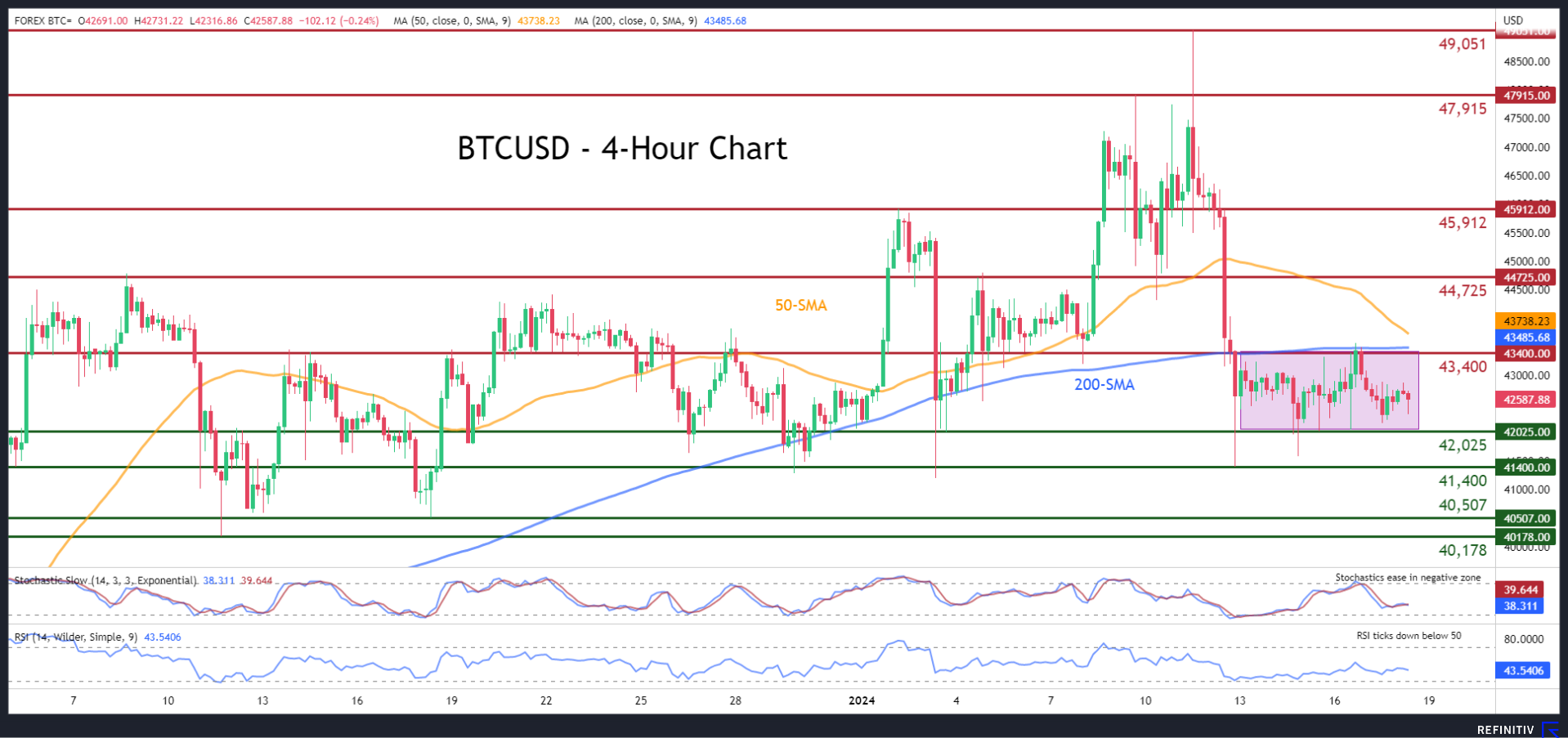

BTCUSD Stuck in Tight Range

- BTCUSD extends sideways move in narrow range

- The 200-period SMA rejects any upside attempts

- Momentum indicators deep in their negative zones

BTCUSD (Bitcoin) has experienced a strong decline from its recent two-year peak of 49,051, dropping to as low as 41,400. Although the short-term oscillators have been tilted to the downside for the past few four-hour sessions, the digital coin managed to recoup some losses and adopt a neutral pattern.

Should the bears attempt to push the price lower, immediate support could be found at 42,025. Sliding beneath that floor, Bitcoin could test the recent low of 41,400, a region that provided support multiple times in December. Further retreats may then cease around the December hurdle of 40,507.

Alternatively, if the price reverses back higher, attention could fall to 43,400, which has not only acted as both resistance and support in recent months but also lies very close to the 200-period simple moving average (SMA). Conquering this barricade, the bulls might attack the January resistance of 44,725 that also held strong in December. Even higher, the January resistance of 45,912 may curb any upside attempts.

Overall, BTCUSD has been in a consolidation mode following the steep fall from its two-year high. However, the impending completion of a death cross between the 50- and 200-period SMAs could reignite downside pressures.

Sunset Market Commentary

Markets

Markets received another dose of realism in the form of solid US economic data. US December housing data came in on the strong side of expectations. Building permits, seen as a leading indicator for the sector, rose by 1.9% m/m (1495k) vs 0.7% expected. Shovel-in-the-ground housing starts, the next step in the process, declined far less than expected (-4.3%) after a bumper November month, even with the downward revision (10.8%). Simultaneously published weekly jobless claims dropped below the 200k mark. The 187k marked the smallest increase since September 2022, which in turn printed some of the lowest figures since 1969. The disclaimer that the series is notoriously volatile doesn’t alter the fact that it has been steadily trending lower since June of last year. The strong shape of the US (service) economy’s backbone makes investors think twice about their aggressive Fed positioning. A poor Philly Fed business outlook did take some of the shine away, only recovering to -10.6 vs -6.5 expected. US yields in the run-up to the data eased a few bps after yesterday’s surge before reversing course afterwards. Changes vary between -1.4 (2-y) to +2.8 bps (30-y). This compared to moves of -5 bps to -2 bps for the same maturities before data release. The 10-y yield extends gains beyond the 4.07% resistance area (23.6% recovery on the EoY decline).

The ECB minutes of the December 13-14 policy meeting are worth mentioning, even if they come just a week before the next gathering takes place. President Lagarde at the time noted several times how the fresh forecasts due to an earlier cut-off date assumed a rate path that was higher than markets were pricing in. The minutes showed frustration among policymakers about markets frontrunning too much and they agreed on the need to push back. Before declaring victory over inflation and deciding on a rate cut, the ECB first needs evidence of wage growth easing. With negotiations ongoing this could take some time, ie. the summer as said by Lagarde yesterday. German rates barely reacted. They trade a choppy sideways pattern, leading to changes of -1.1 bps at the front and +3.3 bps at the long end of the curve.

EUR/USD (1.0868) in FX space aborted an early morning attempt to recoup the 1.09 big figure. Technical return action is pushing the pair now towards the lowest levels since mid-December around 1.085 even as equities get a solid bid. The Japanese yen licks its wounds after some serious three-day beating against the USD and euro. Sterling ekes out some additional gains (EUR/GBP 0.857), building on yesterday’s momentum after a CPI beat lifted gilt yields by more than 20 bps. The latter do ease several basis points today though.

News & Views

The International Energy Agency published its monthly oil market report today. They expect that global oil demand growth will continue to slow. The trend was already visible in Q4 2023 (1.7 mb/d YoY) coming from levels of around 3.2 mb/d in Q2-Q3 2023 2023. Growth is projected to ease from 2.3 mb/d in 2023 to 1.2 mb/d in 2024, as macroeconomic headwinds, tighter efficiency standards and an expanding EV fleet compound the baseline effect. World oil supply is forecast to rise by 1.5 mb/d to a new high of 103.5 mb/d, fueled by record-setting output from the US, Brazil, Guyana and Canada. This would result in a surplus for most of 2024. The IEA view contrasts with the one presented by OPEC yesterday. The Organization of Petroleum Exporting Countries expects robust oil demand growth next year (1.8 mb/d) driven by China and the ongoing economic recovery, eventually leaving the oil market in deficit through to the end of 2025 unless Saudi Arabia and its allies, which are currently cutting production, boost output significantly. Brent crude prices continue to hover just below $80/b where they have been trading for most of the fresh year.

The Bank of England published its Q4 2023 quarterly credit conditions survey today. Lenders reported that the availability of secured credit to households increased in the three months to end-November and is expected to be unchanged over the next three months. Demand for such lending for house purchases and remortgaging decreased in Q4 but both are expected to rise again in Q1. Overall spreads on this secured lending widened in Q4, but are set to narrow back. Default rates and loss given default were higher and set to rise further. The overall availability of credit to the corporate sector slightly increased in Q4, but demand from SME’s and large firms decreased as well. Default rates were expected to increase slightly for SME’s.

GBP/USD Eyes UK Retail Sales

- UK retail sales expected to dip by 0.5% on Friday

The British pound has edged lower on Thursday. In the European session, GBP/USD is trading at 1.2655, down 0.20%.

Markets brace for retail sales downswing

What goes up must come down. That has the markets fretting ahead of the UK retail sales report on Friday. Retail sales growth was brisk in November, with an impressive gain of 1.3% m/m. This followed zero growth in October and marked the strongest gain since April 2022.

The problem with the strong November release was that consumers were enticed to spend big due to Black Friday sales in late November. This is expected to dampen December retail sales, with many shoppers taking advantage of the discounted prices and attending to their Christmas shopping a few weeks early. The market estimate for December retail sales stands at -0.5%.

The Bank of England will be keeping a close look at the retail sales report, as it digests this week’s inflation data with an eye to the next policy meeting on February 1. Inflation in December rose unexpectedly, climbing from 3.9% to 4.0%.

The BoE has tried to dampen market expectations of up to six rate cuts this year, with Governor Bailey sticking to a script of “higher for longer”. The BoE won’t be entertaining rate cuts until it is convinced that inflation is closer to the 2% target and key economic releases point to an improving economy. The unexpected rise in inflation did not support talk of a rate cut, and all eyes are now on Friday’s retail sales report.

GBP/USD Technical

- GBP/USD tested support at 1.2656 earlier. Next, there is support at 1.2616

- There is resistance at 1.2715 and 1.2755

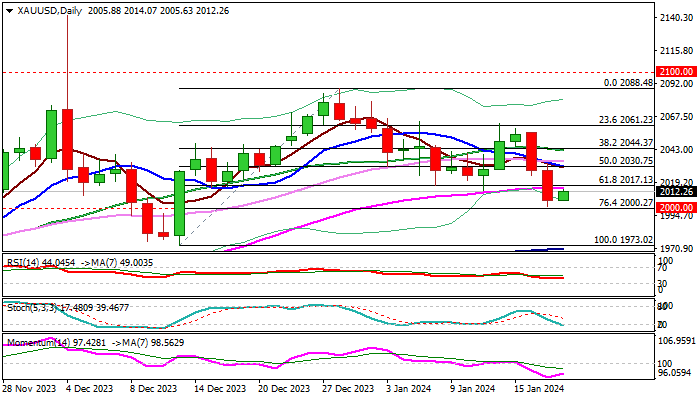

Gold Outlook: Bears Likely to Consolidate Before Fresh Attack at Psychological $2000 Support

Gold price edged higher from five-week low after 2.4% drop in past two days found firm ground just above psychological $2000 level, now acting as solid support.

Yellow metal was deflated by hawkish comments from the US policymakers and recent upbeat economic data, which partially sidelined expectations for early rate cuts this year.

Technical picture weakened on daily chart after the last drop, however, hopes for recovery expected to remain in play while $2000 support (also Fibo 76.4% of $1973/$2088 upleg) holds.

Initial resistance lays at $2015 (55DMA), followed by $2030 (10DMA), which should cap upticks and keep in play risk of renewed attack at $2000 and upper pivot at $2047 (daily cloud top).

Firm break of $2000 pivot would further sour the sentiment and risk drop towards supports at $1973/63 zone (Dec 13 low / 200DMA).

Res: 2015; 2024; 2030; 2042.

Sup: 2000; 1980; 1973; 1963.

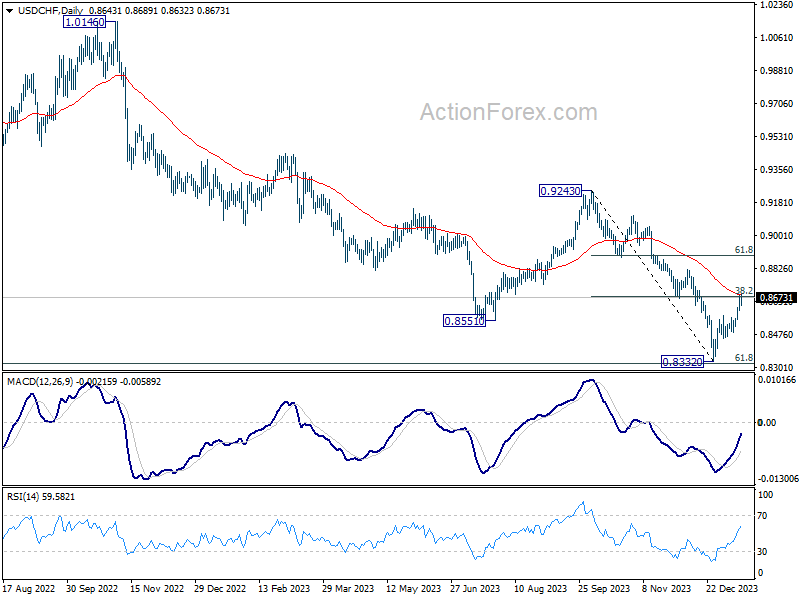

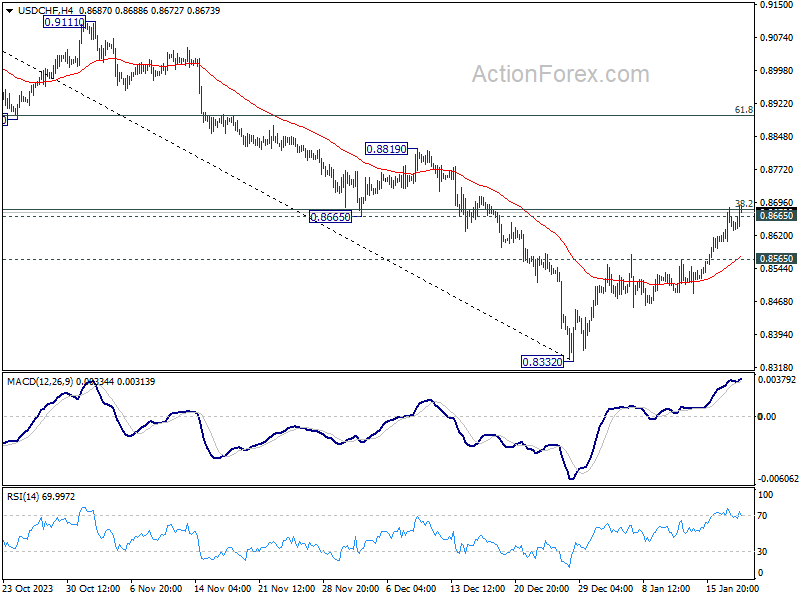

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8604; (P) 0.8645; (R1) 0.8684; More....

Focus remains on 0.8665 support turned resistance in USD/CHF. Decisive break there will turn near term outlook bullish for 61.8% retracement of 0.9243 to 0.8332 at 0.8995. Nevertheless, break of 0.8565 minor support will turn intraday bias back to the downside for retesting 0.8332 low.

In the bigger picture, outlook in USD/CHF will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.