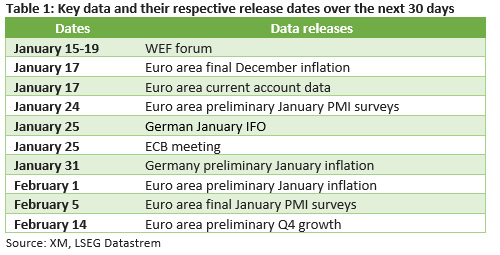

Sample Category Title

Could the Market Price in an ECB Rate Cut in March?

- Data have to turn quickly negative for the March gathering to become live

- Market assigns only 30% chance for a March move; April rate cut is a done deal

- January concludes with preliminary PMIs and the January 25 ECB meeting

Despite the upside surprise at the December inflation report, the market remains convinced that the ECB will probably be the first one to announce a rate cut in 2024. The market is currently pricing in a 30% probability of a March 7 rate move. With President Lagarde remaining adamant that the ECB is not yet in an easing mood, what needs to happen for the ECB to cut rates in March?

1. Inflation falling aggressively

Contrary to the Fed's dual mandate, the ECB’s only target remains price stability i.e. 2% inflation over the medium term. Hence, an unexpected drop in inflation, particularly in the core indicator, would clearly open the door to a more dovish stance. The next CPI release for the month of January comes on January 31 and February 1 for Germany and the euro area respectively.

Energy prices played a massive role in pushing inflation to double digits. As our colleague Marios Hadjikyriacos wrote in a recent special report, downside risks for oil prices are mounting with a price war possibly around the corner. Such an outcome would mean much lower oil prices going forward with inflation dropping aggressively due to the negative base effects. Of course, lower oil prices would potentially fuel growth and consumer spending but that would be a problem for another day.

2. Growth tanking

Last year was a difficult one in terms of growth. The Euro area on the whole managed to grow but Germany has probably contracted. The IMF, the OECD and the European Commission agree that 2024 will be a stronger year with Germany returning to positive growth territory. However, these forecasts were made before the German debt shenanigans with the resulting fiscal tightening further complicating the outlook. The ECB’s own projection for euro area growth is a mere 0.8%. The next German IFO survey will be published on January 25 with the preliminary PMI surveys for January scheduled for a February 5 release.

3. Fiscal tightness = no more energy support programmes

Following four years of fiscal relaxation, the euro area countries agreed to reactivate the Stability and Growth Pact. In layman terms, euro area countries must have a credible plan of cutting their debt and should aim mostly for balanced budgets. In case of another strong oil rally, the euro area governments would be unable to offer financial support to consumers, with the crashing consumer spending appetite causing an acute economic slowdown.

4. External events

An escalation in Ukraine and/or the Middle East, or even a flare-up in one of the world's troubled areas would impact world trade routes and investment appetite, thus resulting in a significant drop in growth. As mentioned earlier, Europe is already barely growing. Should such an event occur, the ECB will be forced to cut interest rates in order to stop the economy from falling off in a recession.

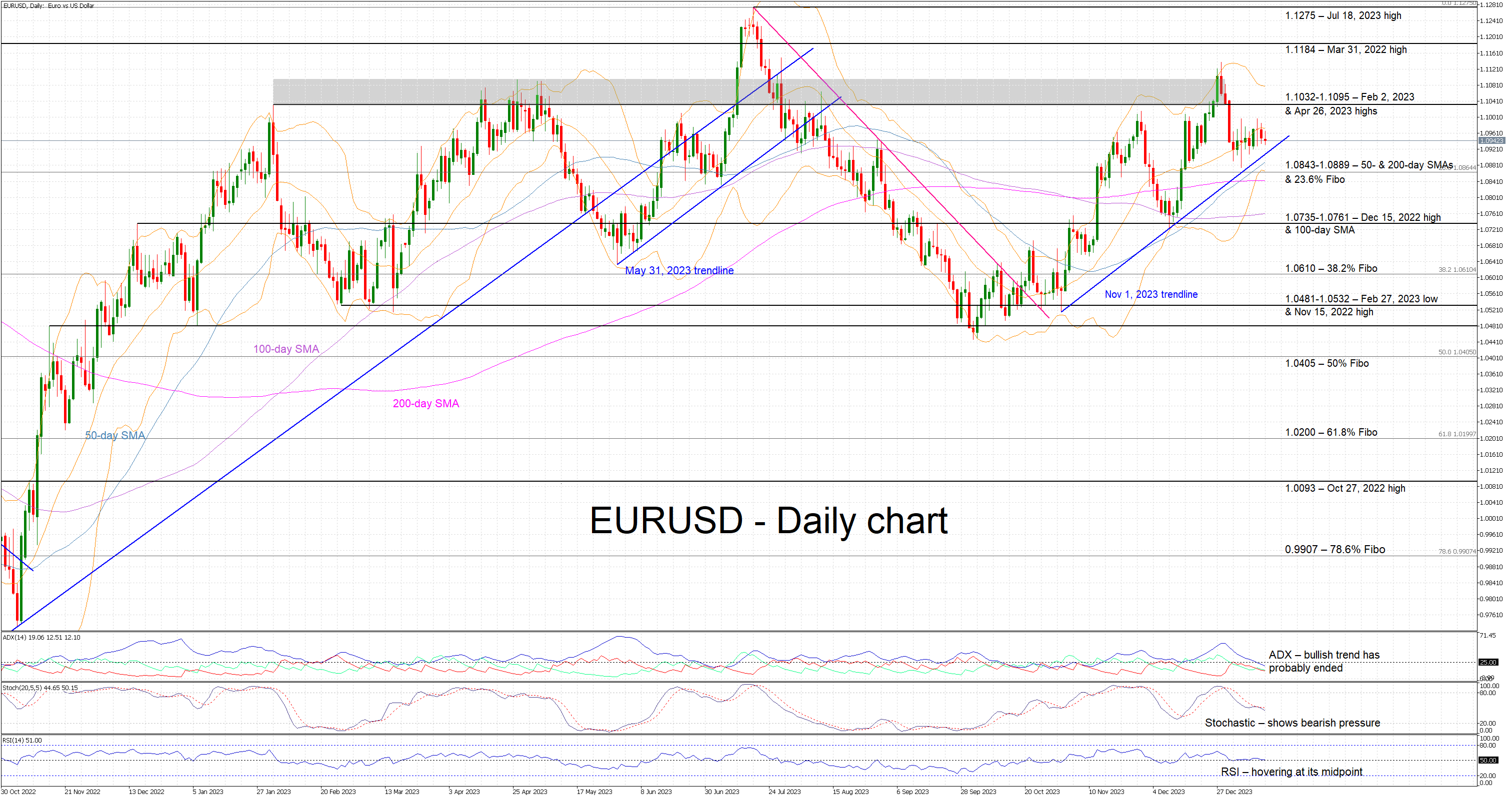

Euro to suffer from an early rate cut?

Despite the evident divergence between the decent growth seen in the US and the continued economic weakness recorded in the Euro area, euro-dollar has been enjoying an upleg from the October lows. The contradictory rhetoric at the December central banks meetings supported this rally but data releases will probably determine the short-term outlook.

A gradual build-up of market expectations for a March ECB rate cut could open the door for correction towards the 1.0735 area. On the flip side, with the market continuing to inflate the expected rate cuts by the Fed, euro bulls could feel more confident in targeting another rally towards the recent peak of 1.1139.

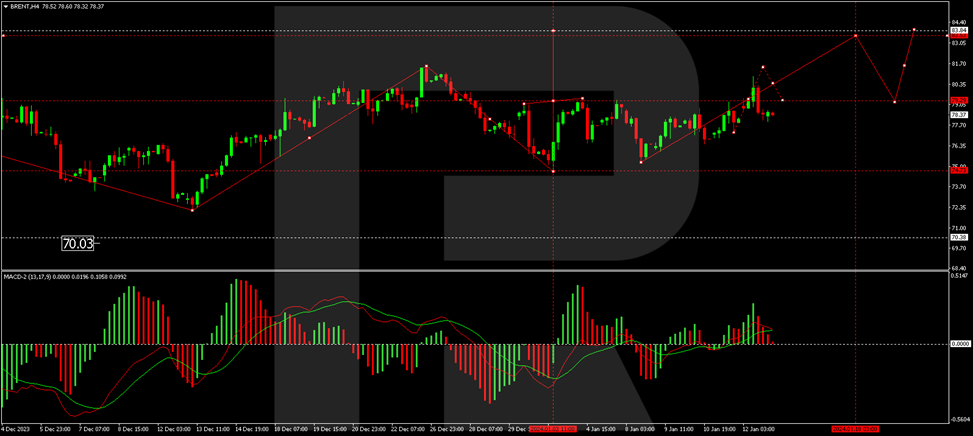

Brent Crude Oil Experiences Upward Trend

Brent prices have been rising for three consecutive days as of this Monday. The price of a Brent barrel has climbed to 79.00 USD, and there are underlying reasons for this surge.

The focal point of attention is the unfolding events in the Red Sea, where the situation is challenging. This holds significant importance for the crude oil market as numerous tankers with energy carriers pass through these waters. Any disruptions in transportation accessibility could potentially impact the crude oil supply. The market incorporates this concern into its quotes. While some tankers have already altered their routes, others continue passing through the Red Sea.

The Libyan factor also supports oil bulls. Protests in the country might lead to a shutdown of two additional oil and gas organisations. Earlier, operations were halted at the Sharara field, causing the market to lose approximately 300 thousand barrels of crude oil daily.

Meanwhile, various drivers exert pressure on the market. Increasing crude oil production among non-OPEC+ members, including the US, is one such factor. Additionally, there is uncertainty in Chinese crude oil demand.

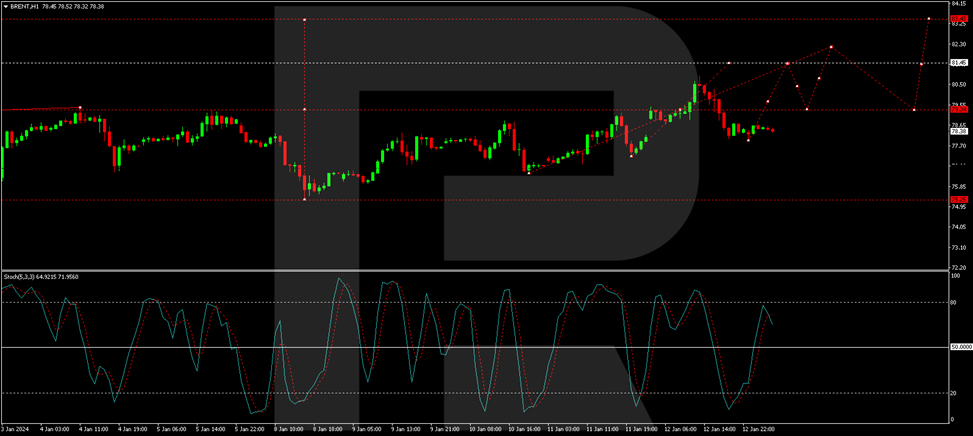

Brent technical analysis

On the H4 Brent chart, a growth wave structure is emerging towards 82.15. Once this level is reached, a correction link to 79.30 is expected, followed by a rise to 83.43. This is a local target. Technically, this scenario is confirmed by the MACD: its signal line is above zero, strictly pointing upwards.

On the H1 Brent chart, a consolidation range is developing around 79.35. A growth structure to 81.45 is expected, followed by a correction to 79.40 and a rise to 82.15. This is a local target. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line above 50, aiming strictly upwards to 80.

Sunset Market Commentary

Markets

US markets are closed today for Martin “I have a dream” Luther King Day. That brought Europe at the center of attention today and that’s what we’ll do in this report as well. Our angle is German, as the country reported a first, very early estimate of growth in 2023. The Federal Statistic’s Office (Destatis) reported GDP to be -0.3% lower last year than in 2022. Elevated prices put a damper on economic growth, as did unfavourable financing conditions due to rising interest rates and weaker domestic and foreign demand. In the sectoral divide, industry (ex. construction) contracted 2% while most service branches expanded their economic activities, be it at a weaker pace than in the two preceding years. Construction saw a modest 0.2% growth. Household consumption was down 0.8% in the expenditure based approach, with the statistics office citing high consumer prices as the key reason for this. Gross fixed capital formation tanked 2.1%. Trade supported the economy but only because imports experienced a greater contraction (-3%) than exports (-1.8%). From the yearly estimate, Destatis also derived a first preliminary Q4 quarterly reading at -0.3%. Because of an upward revision to Q3 growth from -0.1% to +0.1%, Germany did avoid a technical recession. It's a meager consolation to what is the first contraction over a full 12 months since the pandemic and (one of) the weakest performances in the landscape of major advanced economies.

We switch from the economy to monetary policy. Central bank interviews in the sidelines of the WEF in Davos already prove interesting. ECB’s/Buba’s Nagel questioned by Bloomberg said it’s too early to talk about rate cuts as inflation is still too high. He called markets over-optimistic and suggested the ECB can wait for the summer break before mulling cuts. Holzmann joined his hawkish colleague a bit later and took it even further. The Austrian policy member said one shouldn’t count on rate cuts at all in 2024, even as the economy has disappointed. He referred a.o. to the geopolitical situation in which the Houthi rebel threat in the Red Sea region could boost inflation anew. Both ECB policymakers reinforced the earlier German yield rise, leading to changes between +5.4 (30-y) and +7.6 bps (2-y). Euro area money markets still discount 150 bps of rate cuts by end 2024 though. The euro is doing pretty well against major peers in FX space. But an equally solid dollar bid is keeping EUR/USD locked in the mid 1.09/1.10 area. European stocks slip about half a percent but JPY is unable to profit from that minor risk off with the rise in core rates weighing more heavily. USD/JPY bounces to 145.86, EUR/JPY to 159.66.

News & Views

Statistics Sweden reported inflation in December to have slowed slightly less than expected. Headline inflation still rose 0.7% M/M but positive base effects allowed the Y/Y measure to decline from 5.8% to 4.4% (4.3% was expected). CPIF inflation (with fixed interest rates), the preferred target measure of the Riksbank, printed at 0.6% M/M and 2.3% Y/Y (from 3.6%). Core CPIF inflation excluding energy remains high at 0.7% M/M and 5.3% Y/Y (from 5.4%). The decline in headline inflation was mainly due to significantly lower electricity prices compared to December 2022. The interest rates for household’s mortgages rose substantially Y/Y and contributed with 2.3 percentage points to annual CPI inflation. Regarding the monthly dynamics, price rises still remained broad-based. Prices for clothing and footwear rose 2.8% M/M, housing and utilities added 1.1%. Healthcare and medicine as well as prices for transportation rose 0.8% compared to November. The Riksbank in its end November forecasts left the door open for an additional rate hike, but recent comments of MPC members suggested that this won’t be necessary. Even so, higher core inflation might delay a first Riksbank rate cut to the August meeting rather than a first step in May or June. Any SEK gains post the release were limited and short-lived. EUR/SEK currently trades little changed near 11.27.

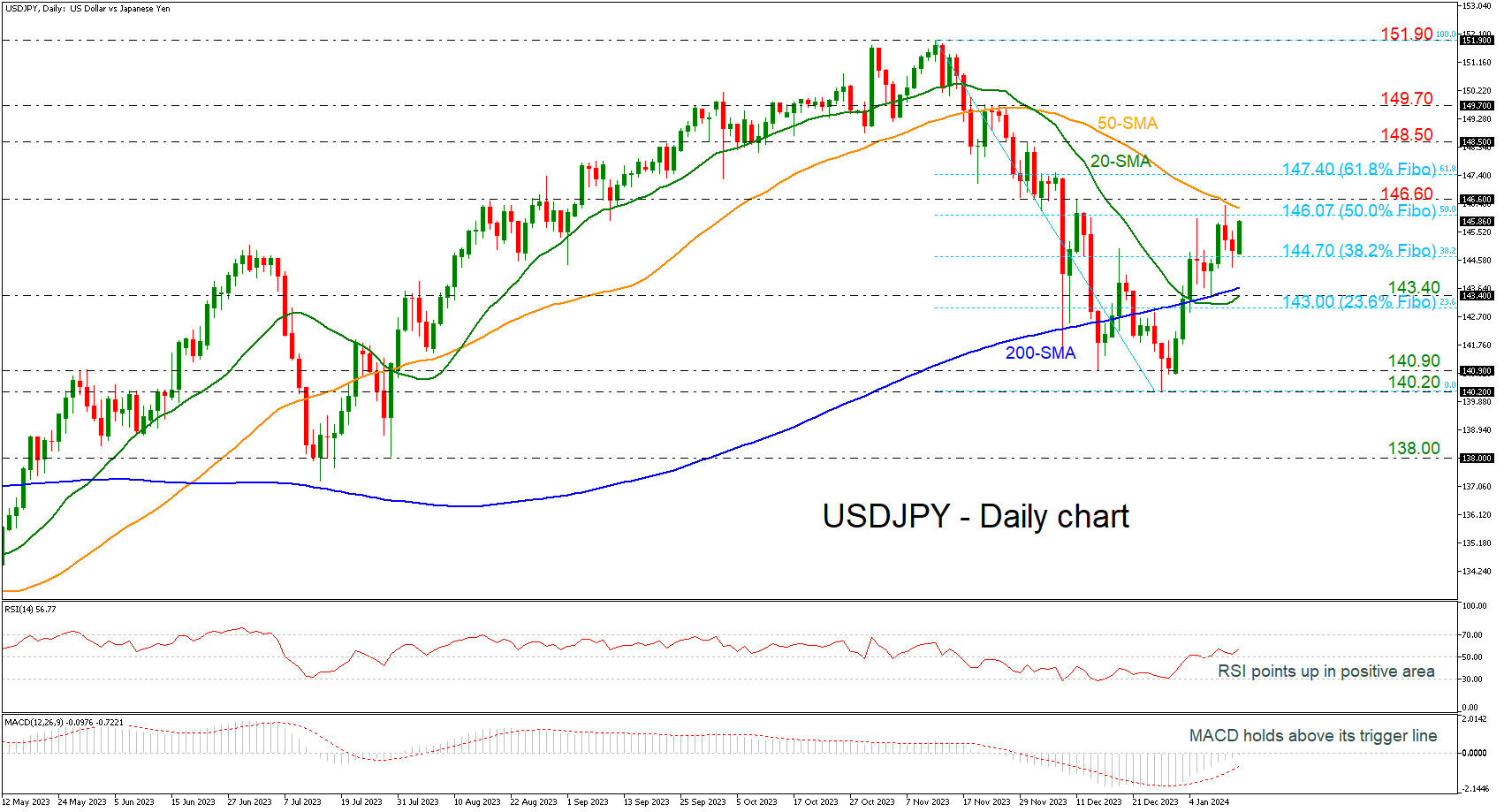

USDJPY on the Rise Again

- USDJPY tries to switch medium-term outlook to bullish

- Prices hold within Fibonacci levels

- Technical signals are positive

USDJPY is looking to resume its bullish trend, having softly pivoted near the 50.0% Fibonacci retracement level of the down leg from 151.90 to 140.20 at 146.07.

To attract new buyers, the bulls will have to surpass the aforementioned resistance of 146.07 and move beyond the 146.60 barrier. In this case, the price could pick up steam towards the important resistance at 148.50. Another successful battle there could see the price jumping towards the 149.70 line, taken from the highs at the end of November.

Nevertheless, a downside correction could still be possible in the coming sessions. If the pair slumps below the 38.2% Fibonacci of 144.70 ahead of the 200-day simple moving average (SMA) at 143.70, it could stabilize near the 143.40 support, which coincides with the 20-day SMA. Otherwise, the sell-off could expand towards the 23.6% Fibonacci of 143.00. However, only a clear close below 140.90 would disappoint medium-term traders.

The technical oscillators seem to be able to convince traders of the bullish scenario. The RSI is pointing upwards in the bullish region, while the MACD is standing above its trigger line and is ready for a cross above the zero level.

Summing up, USDJPY has not eliminated downside risks yet, despite marking a positive start to the week. To boost buying confidence, the pair will need to crawl above the 61.8% Fibonacci of 147.40.

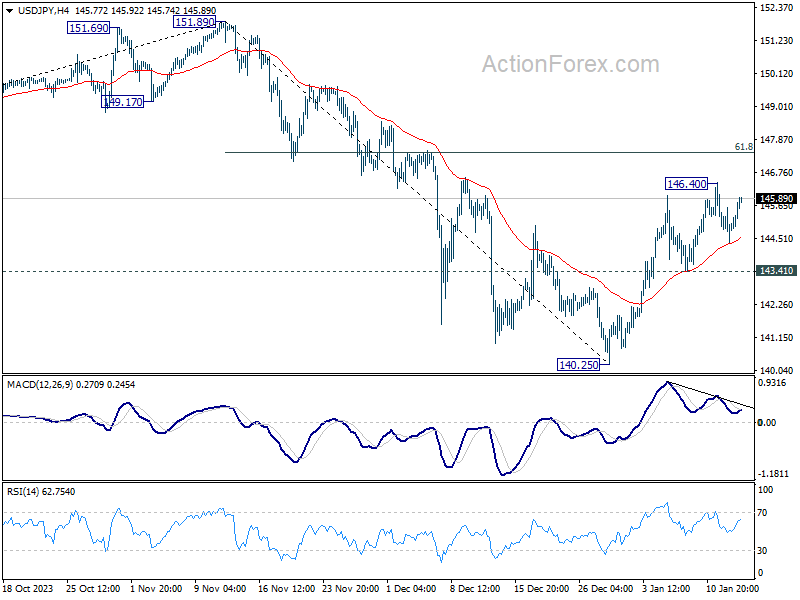

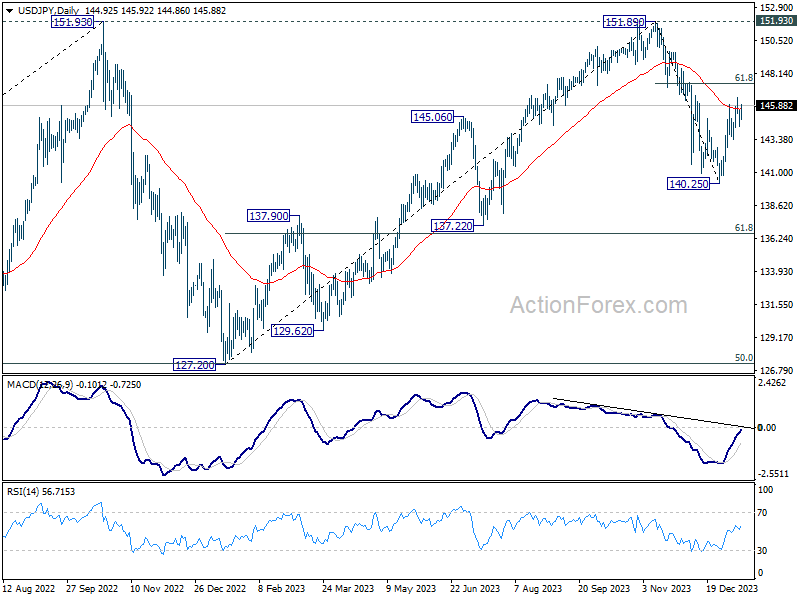

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.32; (P) 144.95; (R1) 145.54; More...

Intraday bias in USD/JPY stays neutral and outlook is unchanged. Rebound from 140.25 could extend through 146.40, but upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. On the downside, break of 143.41 will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

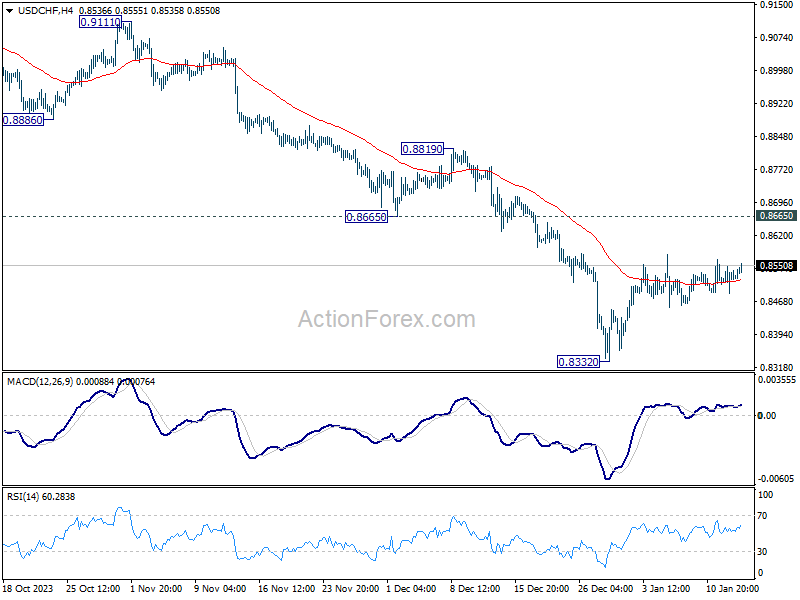

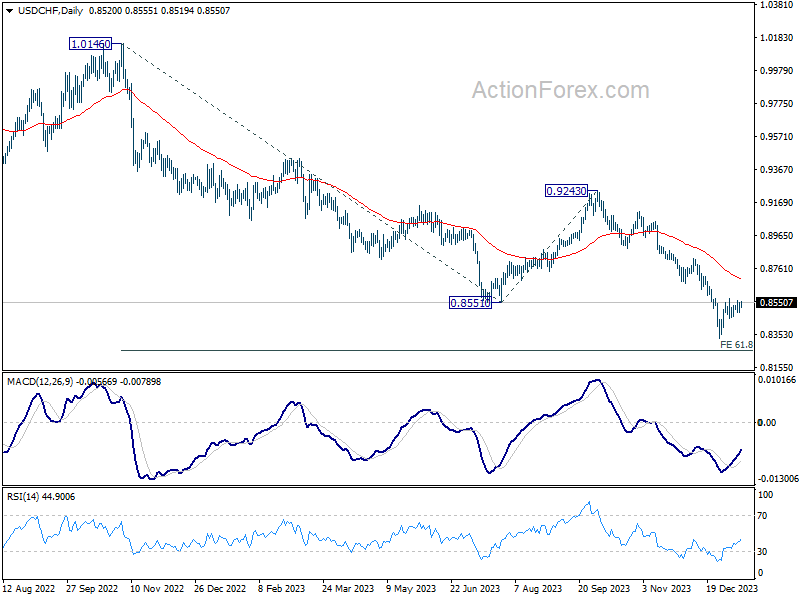

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8498; (P) 0.8518; (R1) 0.8528; More....

Intraday bias in USD/CHF remains neutral as consolidation from 0.8332 is extending. Also, outlook stays bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, down trend from 1.0146 (2022 high) is in progress. Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

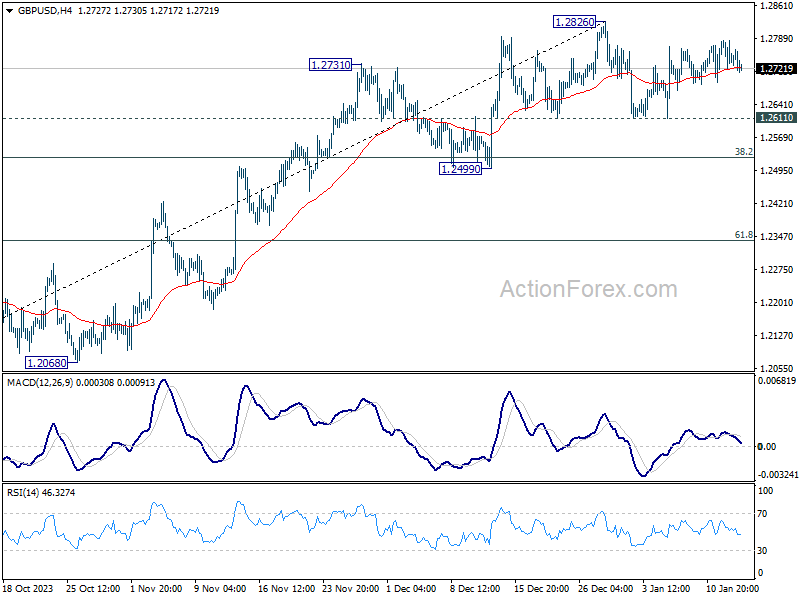

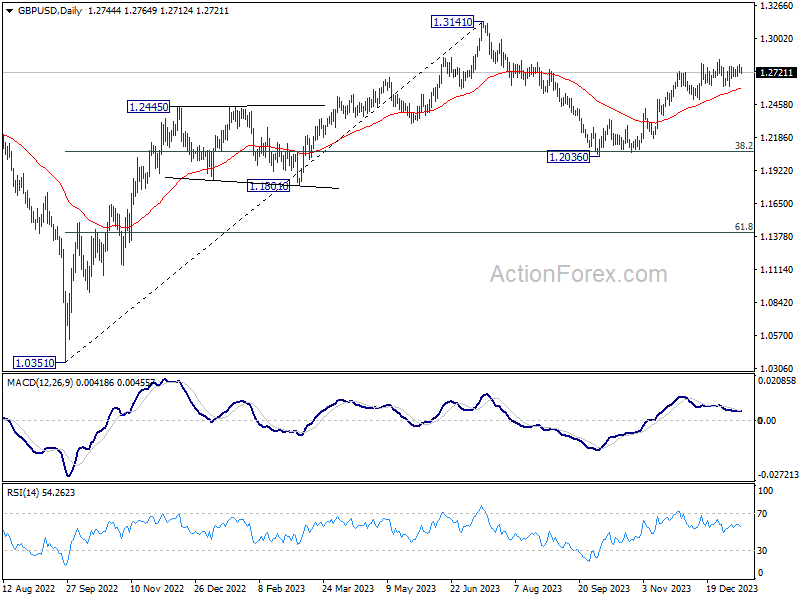

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2721; (P) 1.2753; (R1) 1.2787; More...

GBP/USD is extending consolidation from 1.2826 and intraday bias remains neutral. On the upside, decisive break of 1.2826 will resume whole rally from 1.2036. Nevertheless, another fall and break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

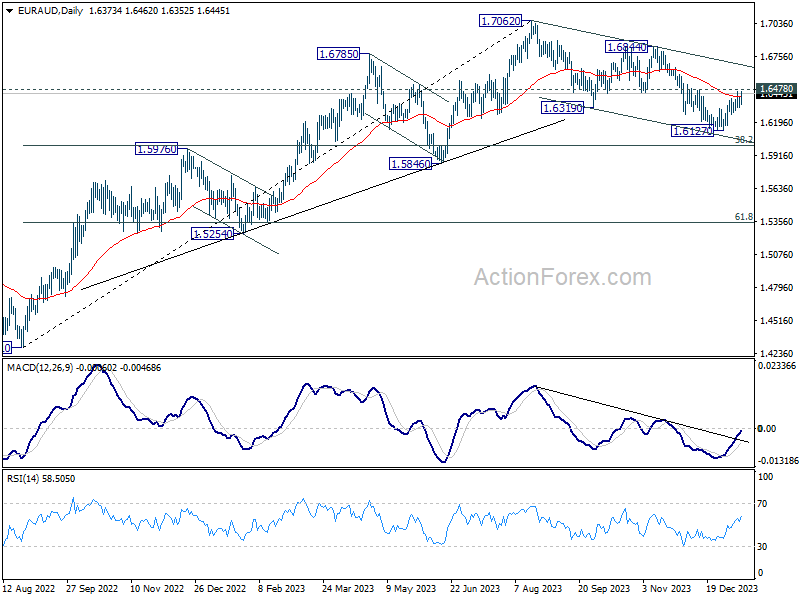

Euro Edges Up on ECB Hawks’ Comments, But Momentum Limited

Euro trades mildly higher today after two known ECB hawks raised skepticism about a near term rate cut. Yet, upside momentum is somewhat tempered by weak trade and production data. Also, Euro is outshone slightly by Dollar, but the latter is also struggling to break out from familiar range other major currencies. Subdued trading could continue for the rest of the day with US on holiday.

Meanwhile, Sterling, Australian Dollar, and New Zealand Dollar are trading on the softer side. Overall markets in Europe are mildly on the risk-off side. Yen is also among the worst performers, apparent on speculations that BoJ isn't ready to hike yet, which also boosts Nikkei. Swiss Franc and Canadian Dollar are mixed like pedestrians.

Technically, EUR/AUD is trying to resume the rebound from 1.6127 today, with sight set on 1.6478 resistance. Decisive break there will strength the case that whole correction from 1.7062 has completed with three waves down. Further rise should then be seen to 1.6844 resistance for confirmation. However, any significant movesmight only materialize following the release of China's economic data on Wednesday or Australia's employment data on Thursday.

In Europe, at the time of writing, FTSE is down -0.34%. DAX is down -0.43%. CAC is down -0.67%. Germany 10-year yield is up 0.032 at 2.238. UK 10-year yield is up 0.009 at 3.809. Earlier in Asia, Nikkei rose 0.91%. Hong Kong HSI fell -0.17%. China Shanghai SSE rose 0.15%. Singapore Strait Times rose 0.24%. Japan 10-year yield fell -0.0331 to 0.558.

ECB's Nagel signals caution, rate cuts possible after summer break

In an interview with Bloomberg TV, ECB Governing Council member and Bundesbank President Joachim Nagel hinted at the possibility of delaying interest rate cuts until after the summer, stating, "Maybe we can wait for the summer break." However, he was cautious not to delve into speculation, emphasizing, "I don't want to speculate." He also empahsized, "it's too early to talk about cuts."

Further elaborating on the current market expectations, Nagel addressed the speculations of six 25 basis points rate cuts by ECB this year. He noted, "The markets from time to time are optimistic. Sometimes they are overly optimistic." This acknowledgment highlights a divergence between market expectations and the ECB's internal assessments. Nagel's observation, "I have a different view," underscores a more cautious and less aggressive approach towards monetary easing.

ECB's Holzmann cautions against premature rate cuts amid uncertainty

During the World Economic Forum in Davos, ECB Governing Council member Robert Holzmann expressed skepticism about the possibility of rate cuts in the near term. He told CNBC, "I cannot imagine that we'll talk about cuts yet, because we should not talk about it."

His asserted, "Everything we have seen in recent weeks points in the opposite direction, so I may even foresee no cut at all this year."

"Unless we see a clear decline towards 2%, we won't be able to make any announcement at all when we're going to cut," he explained.

Holzmann also highlighted the potential for structural changes in the economy, which could have longer-term implications for pricing. He mentioned, "Prices on a day-to-day basis may increase, but it may also risk to change the way we do business." This comment points to the possibility of enduring economic shifts that could affect pricing dynamics and, consequently, ECB's monetary policy decisions.

Eurozone goods exports fell -4.7% yoy in Nov, imports down -16.7% yoy

Eurozone goods exports to the rest of the world fell -4.7% yoy to EUR 252.5B in November. Goods imports fell -16.7% yoy. A EUR 20.3B goods trade surplus was recorded. Intra-Eurozone trade fell -9.4% yoy to EUR 227.2B.

In seasonally adjusted term, goods exports rose 1.0% mom to EUR 236.8B. Imports fell -0.6% mom to EUR 222.1B. Trade surplus widened from prior month's EUR 11.1B to EUR 14.8B, above expectation of EUR 11.2B.

Eurozone industrial production down -0.3% mom in Nov, EU down -0.2% mom

Eurozone industrial production fell -0.3% mom in November, match expectations. Industrial production fell by -2.0% mom for durable consumer goods, by -0.8% mom for capital goods and by -0.6% mom for intermediate goods, while production grew by 0.9% mom for energy and by 1.2% mom for non-durable consumer goods.

EU industrial production fell -0.2% mom. Among Member States for which data are available, the largest monthly decreases were registered in Greece (-4.1%), Slovakia (-4.0%) and Belgium (-3.8%). The highest increases were observed in Denmark (+9.1%), Slovenia (+3.7%) and Portugal (+3.4%).

Contrary to market expectations, PBoC maintains MLF rate but increases liquidity

Despite the anticipation of a rate cut to bolster the weakening economy, currently grappling with deflation for the past three months, PBoC held firm, keeping the rate on CNY 995B worth of one-year medium-term lending facility loans steady at 2.50%. This decision defied the general expectation of a 0.1% cut to 2.40%.

Opting not to alter the policy rate, the central bank instead chose to enhance liquidity in the banking system. This is seen from the net injection of CNY 216B of fresh funds, following the expiration of CNY 779B worth of MLF loans this month. Moreover, PBoC also infused CNY 89B yuan through seven-day reverse repos, maintaining a stable borrowing cost at 1.80%.

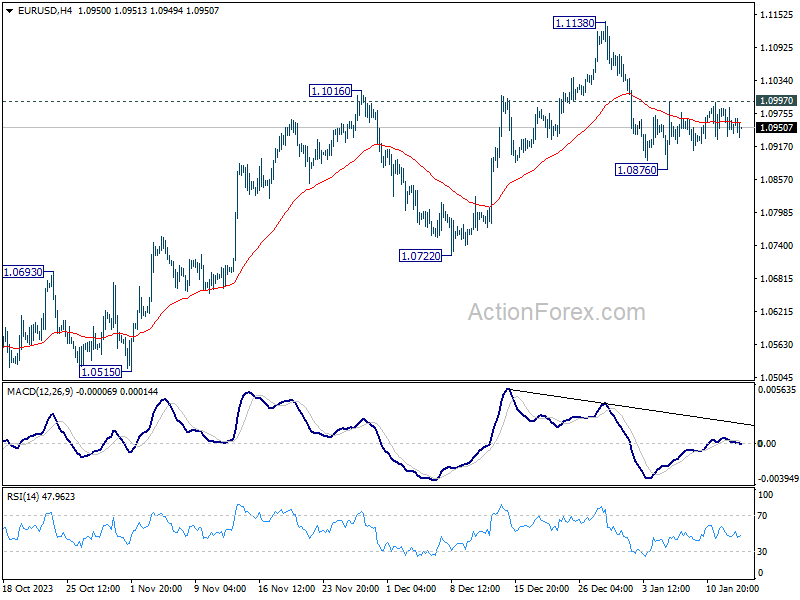

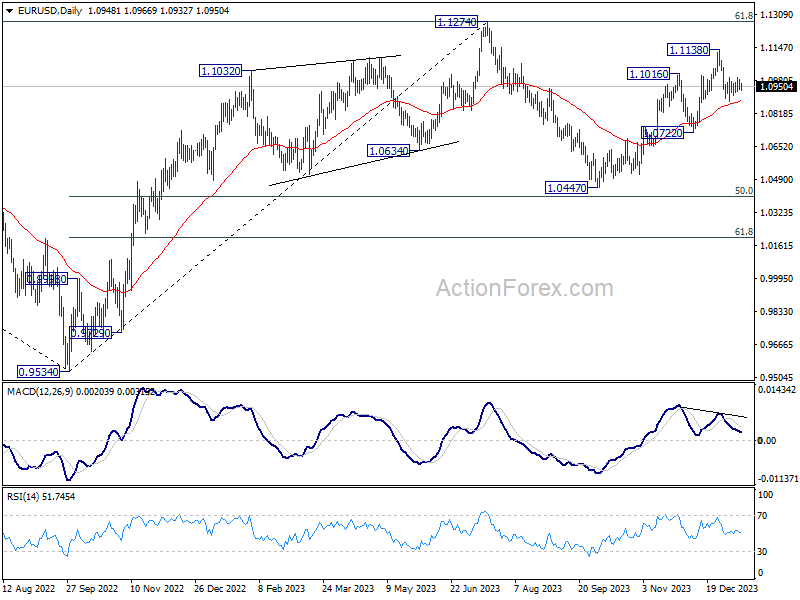

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0929; (P) 1.0958; (R1) 1.0980; More...

No change in EUR/USD's outlook as it's staying in very tight range. Intraday bias stays neutral at this point. Further fall is in favor as long as 1.0997 minor resistance intact. Break of 1.0876 will resume the fall from 1.1138 to 1.0722 support next. Nevertheless, firm break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Dec | 2.30% | 2.20% | 2.30% | |

| 00:00 | AUD | TD Securities Inflation M/M Dec | 1.00% | 0.30% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Dec | -15.50% | -13.60% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Nov | -0.30% | -0.30% | -0.70% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Nov | 14.8B | 11.2B | 10.9B | 11.1B |

| 13:30 | CAD | Manufacturing Sales M/M Nov | 1.20% | 0.90% | -2.80% | |

| 13:30 | CAD | Wholesale Sales M/M Nov | 0.90% | 0.80% | -0.50% | |

| 15:30 | CAD | BoC Business Outlook Survey |

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0929; (P) 1.0958; (R1) 1.0980; More...

No change in EUR/USD's outlook as it's staying in very tight range. Intraday bias stays neutral at this point. Further fall is in favor as long as 1.0997 minor resistance intact. Break of 1.0876 will resume the fall from 1.1138 to 1.0722 support next. Nevertheless, firm break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.