Sample Category Title

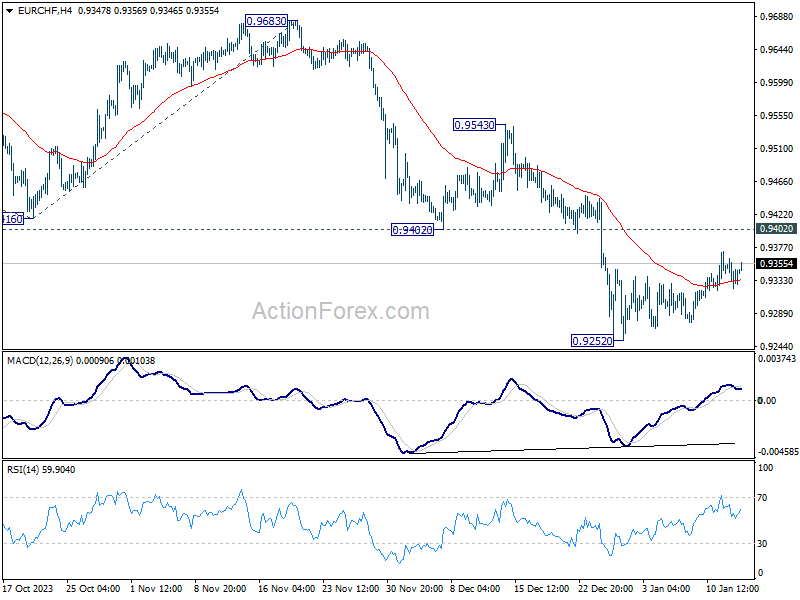

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9319; (P) 0.9342; (R1) 0.9359; More...

No change in EUR/CHF's outlook as consolidation from 0.9252 is extending. Intraday bias remains neutral and outlook stays bearish with 0.9402 support turned resistance intact. On the downside, break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

Gold: Potential Bullish Breakout from 6-Week Range

- Positive price actions in Gold (XAU/USD) as it reintegrated back above its 20-day moving average.

- A continuation of the medium-term bearish trend on the US 10-year Treasury real yield below 1.82% key resistance may add further bullish impetus for Gold.

- A rise in geopolitical risk premium may also support a firmer Gold.

- Watch the US$2,015 key short-term support on Gold (XAU/USD).

Since our last analysis, Gold (XAU/USD) has traded sideways and held firm above the prior US$1,997 key short-term support and its upward-sloping 50-day moving average.

After a slew of key economic data that was released last week (US CPI & PPI for December), Gold (XAU/USD) has managed to hold above the 50-day moving average and reintegrated back above its 20-day moving average last Friday, 12 December with a daily close of US$2,049 over the 20-day moving average value of US$2,044.

There are two other intermarket positive developments on top of the sole positive price actions that may support a bullish tone in Gold (XAU/USD) in the short to medium-term time frame.

Lower opportunity cost for holding Gold

Fig 1: US 10-year Treasury real yield medium-term trend as of 12 Jan 2024 (Source: TradingView, click to enlarge chart)

The US 10-year Treasury real yield has shaped a bearish reaction right at its 1.82% key medium-term pivotal resistance and reintegrated back below the 200-day moving average.

In addition, the daily RSI momentum indicator has failed to break above the 50 level after a retest which suggests that medium-term bearish momentum is likely to have resurfaced.

These observations suggest that the price actions of the US 10-year Treasury real yield may trend lower towards the next medium-term support of 1.38% which in turn lowers the opportunity cost of holding long positions in Gold.

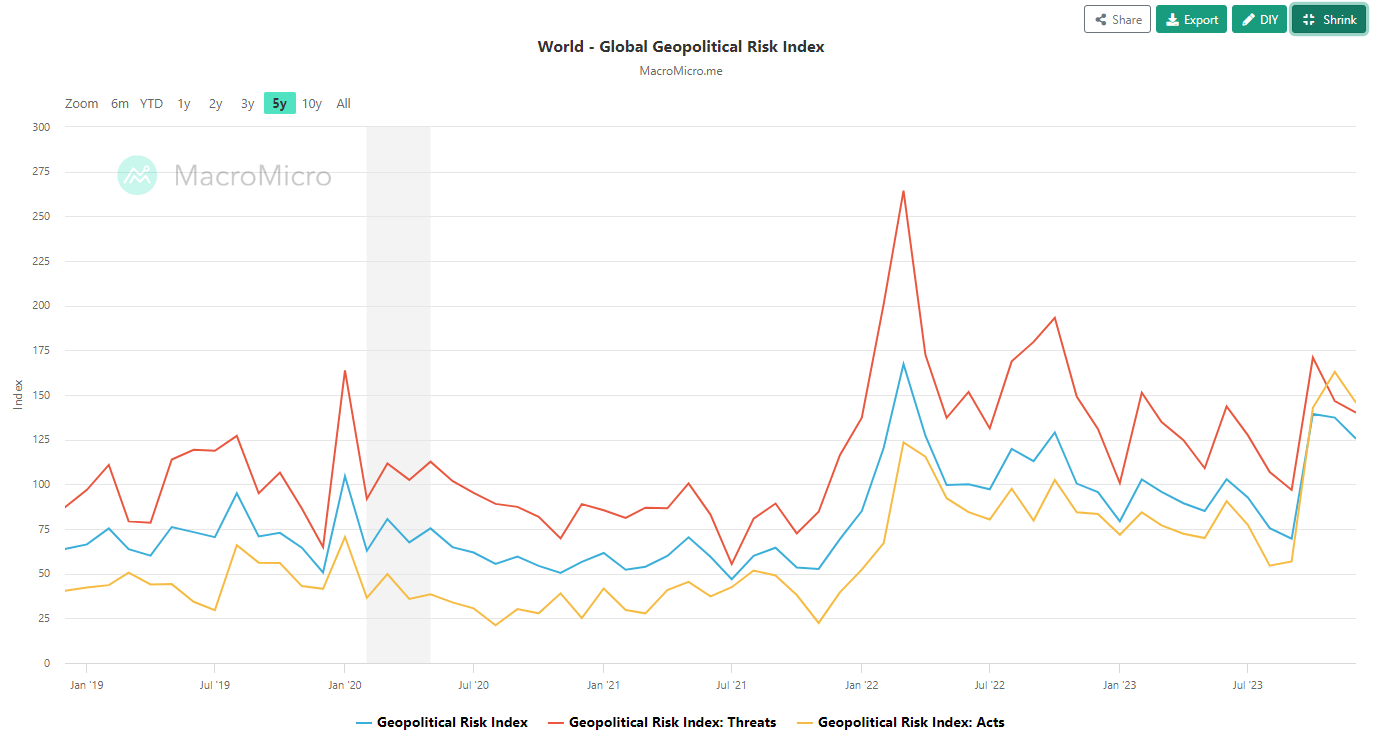

Rising geopolitical risk premium

Fig 2: World Geopolitical Risk Index as of Dec 2023 (Source: Macro Micro, click to enlarge chart)

Secondly, rising geopolitical risk premium as hostilities escalate in the Red Sea shipping route while Yemen’s Houthi rebels are showing no signs of backing down from their series of attacks since late October 2023 that targeted Southern Israel and ships in the Red Sea that were linked to Israel in the ongoing Israel-Hamas war.

The current uptick in geopolitical tension from the Middle East region is also reflected in the Global Geopolitical Risk Index (GPR) compiled by US Federal Reserve economists Dario Caldara and Matteo lacoviello. The GPR Index has been trending up since September 2023 with its current December 2023 reading of 125.47, the highest level since March 2022’s reading of 167.29 during the onset of the Russian invasion of Ukraine.

Potential bullish range breakout for Gold

Fig 3: Gold (XAU/USD) medium-term trend as of 15 Jan 2024 (Source: TradingView, click to enlarge chart)

Fig 4: Gold (XAU/USD) minor short-term trend as of 15 Jan 2024 (Source: TradingView, click to enlarge chart)

The price actions of Gold (XAU/USD) have staged a “V-shaped” bullish reversal in the latter half of last week right at the lower boundary of the medium-term ascending channel in place since the 6 October 2023 swing low that is acting as a support at US$2,015 coupled with a bullish momentum condition flashed out by the daily RSI momentum indicator at around the 50 level.

In the shorter term as seen on the 1-hour chart, it has staged a clearance above the upper boundary of a former minor descending channel in place since 28 December 2023, and the 20-day moving average.

The next intermediate resistance to watch will be at US$2,090; a 6-week range resistance since 4 December 2023. A clearance above it sees the next intermediate resistance coming in at US$2,117.

On the flip side, failure to hold at the US$2,015 short-term pivotal support negates the bullish tone to expose the medium-term support zone of US$1,990/1,975 (also close to the 200-day moving average).

DPP Secures Presidency in Taiwanese Election

In focus today

Today, the US election year kicks off with the Iowa Republican Caucuses. Prediction markets see Trump as the clear favourite to win the Republican candidacy, and he is projected to win over half of all votes in Iowa according to the latest polls. The Iowa caucuses are often seen as a bellwether for the rest of the spring, and either of Trump's closest challengers, Ron DeSantis or Nikki Haley, would likely have to come up as a close runner-up to maintain their hopes of clinching victory in the end.

In the euro area, we receive the November industrial production figures. The industry has been stuck in contractionary territory in 2023. Recently, soft indicators like the manufacturing PMIs and leading indicators from Asia have started to show a bottoming out in manufacturing activity. It will be interesting to see if the hard data confirms this. However, the risks are tilted towards another benign euro area print as data released last week showed German industrial production falling 0.7% m/m in November.

We also receive German GDP figures for 2023. The figures will show how the economy ended 2023 in Q4 where activity likely declined judging by data released on industrial production as well as soft indicators. The release includes the 2023 data and not the official seasonally adjusted real q/q growth rate for Q4 - this is scheduled in two weeks.

In Sweden, we expect the December inflation data to show a decline in primarily CPIF inflation, which likely has temporarily dropped below the 2% target. That said, core CPIF excl. energy is expected to continue to undershoot the Riksbank's November forecast as we forecast CPIF and CPIF excl. energy to print 1.9% y/y and 5.0% y/y, respectively, which is -0.2 and -0.6 percentage points below Riksbank's dittos. We note that December inflation in Denmark and Norway suggest lower prints on food, clothing, transportation services and recreation than what is assumed in our forecast, which may suggest a downside risk to the overall forecast.

For the remainder of the week focus we will look out for inflation data from the UK and Japan. We also have several central bank speakers on the wire.

The World Economic Forum in Davos also kicks off Monday. The WEF runs till Friday 19 January.

Economic and market news

What happened overnight

Chinese central bank surprises with unchanged rates: PBOC surprisingly kept rates on hold this morning in contrast with ours and consensus expectations of a 10bp cut. The central bank has signalled further easing recently but apparently not already today. It may also be a signal they will prefer to reduce the reserve requirement ratio (RRR) instead and we will be looking out for that in the coming weeks. They normally do not change the RRR rate at the same time as the rate decisions so it could happen any time in our view. The CNH strengthened slightly after the rate announcement this morning but USD/CNH is unchanged from the levels Friday afternoon around 7.18.

Oil prices rose slightly this morning with Brent having gained around 0.20% trading at USD78.45/barrel.

What happened over the weekend

Taiwan election points to status quo: As expected, the independence-leaning DPP secured the presidency for the third time in a row as their candidate Lai Ching-te won by a 6.7 percentage points margin to KMT's Hou Yu-ih. However, Lai's victory was smaller than his predecessor Tsai Ing-wen and DPP lost the majority in the parliament. Hence Lai is ruling with a weaker mandate than Tsai Ing-wen. Lai's victory was also secured by keeping a more moderate tone on independence than before he became presidential candidate suggesting that he is unlikely to increase confrontations with China. It also reflects a mood among the Taiwanese where polls show a clear majority in favour of the status quo - and more so over the past year, see also Research China - Taiwan election points to status quo, but not further escalation, 15 January. The market reaction to the election this morning has been very muted.

On Friday UK monthly GDP November figures came out slightly better than expected at 0.3% m/m (consensus: 0.2%, prior: -0.3%). A slight rebound, as expected following the upbeat PMIs the past months which showed composite and services in expansionary territory. The 3m/3m was however lower than expected at -0.2% after downward revisions almost across the entire board for October.

Oil prices initially rose after the US and UK had conducted airstrikes against the Houthis in Yemen with Brent briefly trading north of USD80.5/barrel but settling at USD78.29/barrel. Between Friday and Saturday, the US conducted another air strike against the Houthis. US president Biden later said the US had delivered a private message to Iran regarding the Tehran-backed Houthis and their attacks on commercial ships in the Red Sea.

US PPI numbers for December came in at -0.1% m/m and 1.0% y/y, which was lower than expected (consensus: 0.2% m/m and 1.4% y/y). November PPI was revised down to -0.1% m/m from being unchanged, hence headline PPI m/m dropped for the third consecutive month in December. Core PPI for December stood at 0.2% m/m and 2.5% y/y.

The 10y UST was down by 3.6bp by end of Friday's session, as investors digested the week's inflation numbers.

In the equity space Microsoft seized the throne from Apple as the largest public company by market cap. Microsoft had briefly overtaken Apple in Thursday's session, however this marks the first time Microsoft stands as number one by closing bell since November 2021. Microsoft which gained 1.00% in Friday's session now has a market cap of USD2,887bn, whereas Apple which gained 0.18% in Friday's session has a market cap of USD2,875bn.

Geopolitics: On Friday, we published a note discussing the tensions in the Red Sea. For now, we are not overly concerned that the events would affect global markets. Although freight rates have increased significantly over the past few weeks, energy markets remain calm. In a late business cycle environment, supply side issues are not as inflationary as in an environment where the economy is booming. We do acknowledge though that the situation warrants close monitoring. Risks rise in a scenario where the war in Gaza expands. Lebanon's involvement would raise the risk of Iran also drawing in, and such a scenario could be a game changer for the energy markets, for inflation and for the major central banks. Read more on Research Global: Tensions rise in the Red Sea - should we worry? 12 January.

Equities: Global equities were higher Friday and last week despite a lacklustre start to the US earnings season. As always, US banks were the first ones to report and the combination of both disappointing earnings and for some weaker than expected guidance dragged down banks and made US indices underperform. The energy sector was the best performer after oil price rose as a result of the US and British attack on Houthis. Asian markets are mixed this morning. Japanese indices are continuing higher on the back of further yen softening. European and US futures are mostly higher this morning.

FI: Global yields in the front end went sharply lower on the back of the US PPI miss, which added to easing expectations from central banks. The 2y US yield ended 10bp lower, which took the Schatz (Germany) 7bp lower along the way. Markets are now pricing 154bp of rate cuts for the rest of the year, which is 14bp more than on Thursday last week. This weekend, ECB Chief Economist pushed back on the expectations for a rate cut in Spring, but saying that by June, ECB will have the important wage data for Q1, which will only become available by the end of April.

FX: Despite elevated geopolitical risks with the air strike in Yemen by the US and UK on Friday, market sentiment is positive - also helped by soft US December PPI figures on Friday. EUR/USD is still range trading in the mid 1.09-1.10 level, while USD/JPY declined below 145. EUR/GBP had a fairly quiet session on Friday, staying just below the 0.86 mark. EUR/NOK and EUR/SEK are hovering just below 11.25, bringing NOK/SEK near parity.

Mixed Feelings

The US stock markets ended last week on a cautiously positive note. Friday’s producer price inflation came as a certain relief to inflation worries as the latest data showed an unexpected contraction in the monthly figure. The jump in oil prices, following the US and UK airstrikes in areas in Yemen controlled by the Houthis, which sent the barrel of American crude to past the $75pb level, didn’t last long. The barrel of US crude starts the week below the $73pb level. The risks are tilted to the upside as conflict news continues to flow in this Monday. Rishi Sunak will address Parliament as his government is ready to intensify strikes on Houthi targets. Yet there is a strong barricade into the $74/75pb level in the US crude and near $80pb level in Brent, as the rising global supply, increasing competition to OPEC and the globally weak economic outlook weigh heavier and convince the bears to sell every geopolitically supported rallies.

Rising tensions in the Red Sea and the rising shipping costs are a boon for shipping companies like AP Moeller-Maersk that see their stock prices being pushed higher. Bank stocks on the other hand traded mixed on Friday as the first Q4 earnings from some US banking giants were mixed. JP Morgan for example had a blast last year. The banking crisis that hit the smaller, regional banks drove capital to big banks like JP Morgan, and combined with the rising interest rates, JP announced the most profitable year of its history. The bank posted more than $250nb net interest income last year – its 7th consecutive quarter of record net interest income (NII). Together, the 4 major US banks made $80bn more last year than in 2021. Wells Fargo beat estimates but its prediction of 7-9% fall in NII next year sent the stock price more than 3% lower on Friday, while BAC fell 1% after missing estimates.

Despite a mixed set of results and record NII, the big banks share the same forecast for next year: their net interest income will fall next year as the Federal Reserve (Fed) is expected to cut interest rates.

Elsewhere

The People’s Bank of China (PBoC) held its policy rate steady this Monday - defying the expectation of a 10bp cut - while pumping more cash into the financial system to reverse the selloff and boost asset prices, and eventually growth. But in vain. The Chinese CSI 300 index barely reacted to the news after China posted a third negative CPI read on a yearly basis. China is still expected to hit its official 5% target this year, but the confidence crisis and the slump in property prices are not going to reverse overnight. Outlook for Chinese equities is not bright.

Taiwan’s stock exchange, on the other hand, which diverged positively from the mainland stocks last year, had a cheery start to the week after the ruling DPP’s Lai – who is pointed at as a ‘separatist’ by Beijing - won presidency and his party lost its legislative majority. The latter was seen as a good compromise for relations between China and Taiwan – as the outcome was clearly not over-provocative for Beijing. The Japanese Nikkei 225, on the other hand, hit the 36K mark on the back of a softer yen, and waning expectations that the BoJ will be normalizing at a decent speed this year.

In the FX, the US dollar kicks off the week on a slightly negative note, the AUDUSD struggles to find buyers near the lower bound of its October to now ascending channel, as the PBoC could’ve been more supportive. The EURUSD couldn’t clear the 1.10 resistance last week, and the failure to break above the crucial psychological could weaken the euro bulls’ hands this week. Across the Channel, Cable remains cautiously bid after Friday’s GDP printed a better-than-expected growth number. The UK will release its latest inflation report on Wednesday. UK inflation is expected to have further eased from 3.9% to 3.8% in December, and core inflation is seen slipping below the 5% mark. A softer-than-expected set of inflation figures could prevent Cable from making a sustainable move above the 1.28 level.

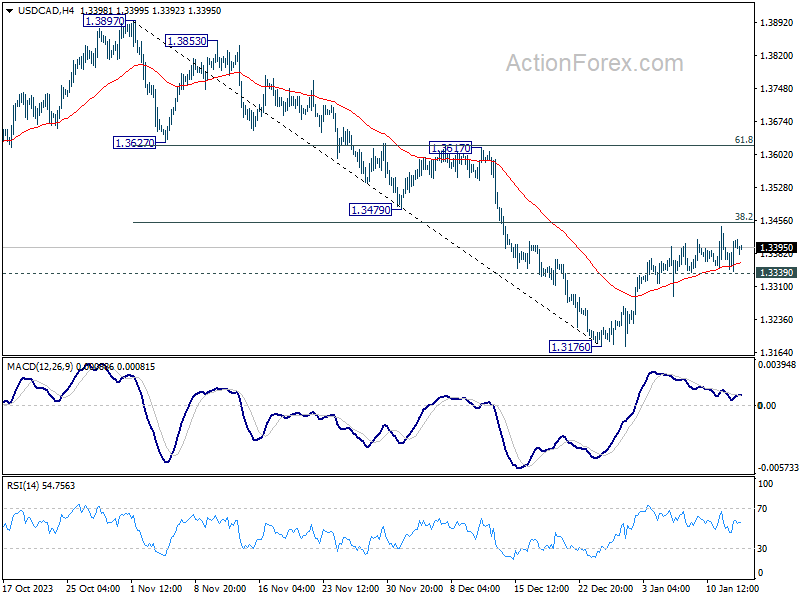

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3362; (P) 1.3387; (R1) 1.3431; More...

Intraday bias in USD/CAD stays neutral first. But further rise is mildly in favor as long as 1.3339 minor support holds. Decisive break of 38.2% retracement of 1.3897 to 1.3176 at 1.3451 will pave the way to 61.8% retracement at 1.3622. On the downside, however, break of 1.3339 will turn bias back to the downside for 1.3176 low instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. While fall from 1.3897 could still extend through 1.3091, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage.

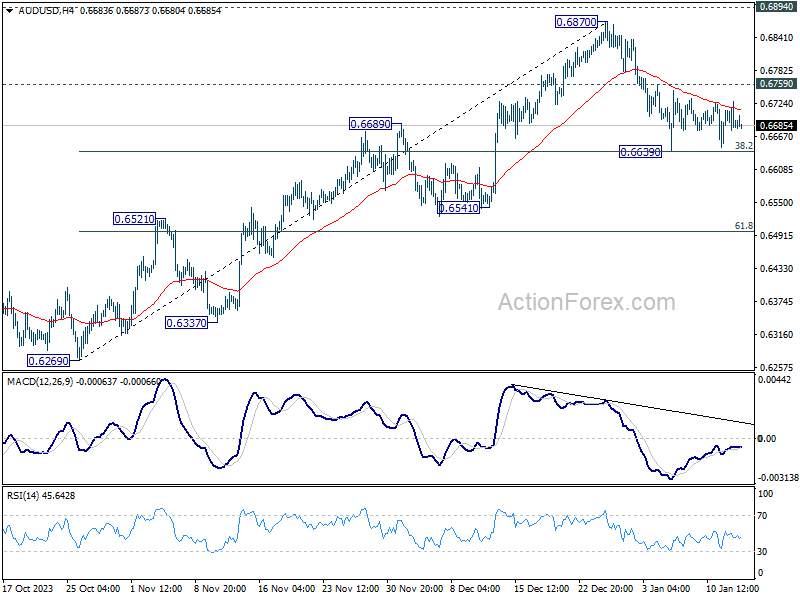

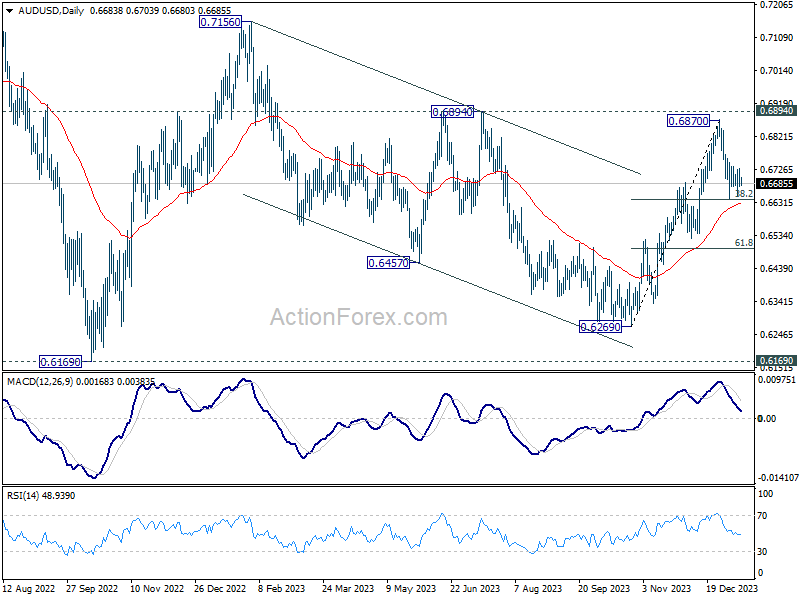

AUD/USD Daily Report

Daily Pivots: (S1) 0.6666; (P) 0.6698; (R1) 0.6717; More...

Intraday bias in AUD/USD remains neutral at this point. Further decline is expected as long as 0.6759 minor resistance holds. Firm break of 0.6639 will resume the fall from 0.6870 to 61.8% retracement of 0.6269 to 0.6870 at 0.6497 next. On the upside, break of 0.6759 will bring retest of 0.6870 resistance instead.

In the bigger picture, price actions from 0.6169 (2022 low) could be just a medium term corrective pattern to the down trend from 0.8006 (2021 high). Rise from 0.6269 is seen as the third leg of the pattern that could target 0.7156 on break of 0.6894 resistance. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

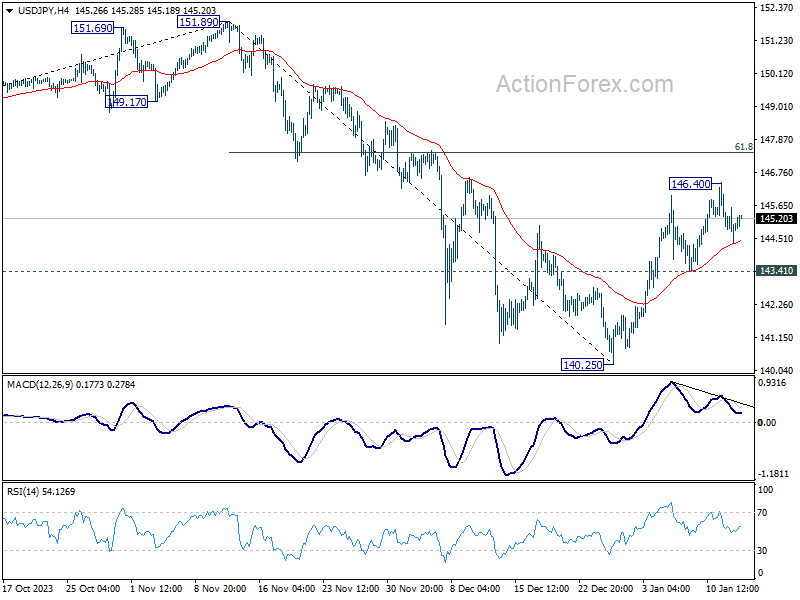

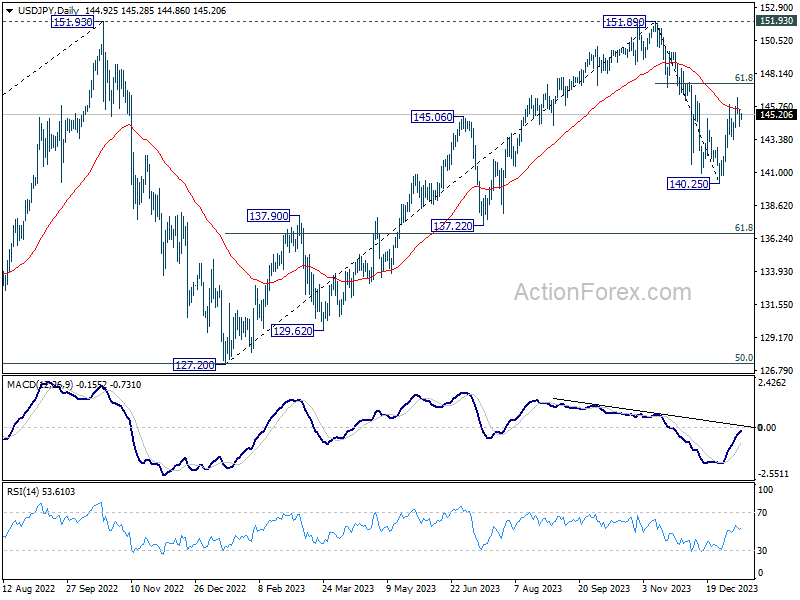

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.32; (P) 144.95; (R1) 145.54; More...

Intraday bias in USD/JPY remains neutral at this point. Rebound from 140.25 could extend through 146.40, but upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. On the downside, break of 143.41 will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

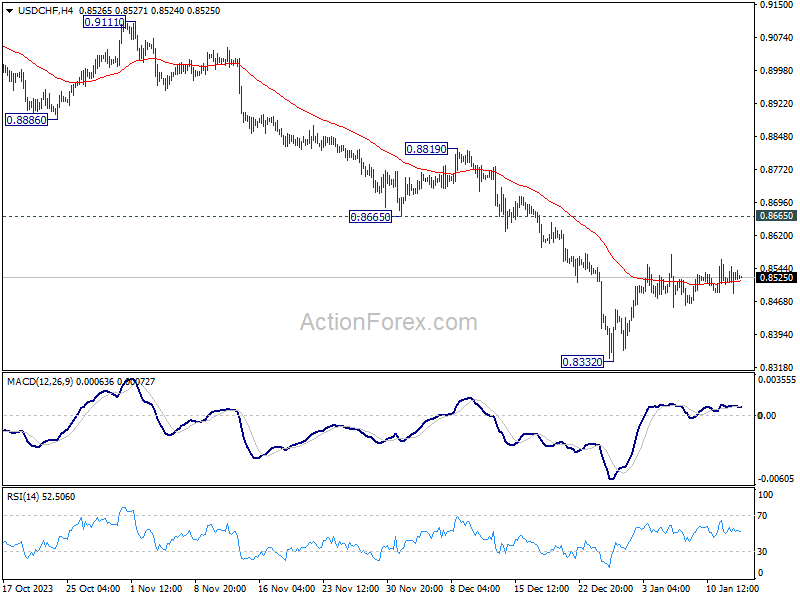

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8498; (P) 0.8518; (R1) 0.8528; More....

USD/CHF is extending the consolidation above 0.8332 and intraday bias remains neutral. Also, outlook stays bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, down trend from 1.0146 (2022 high) is in progress. Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

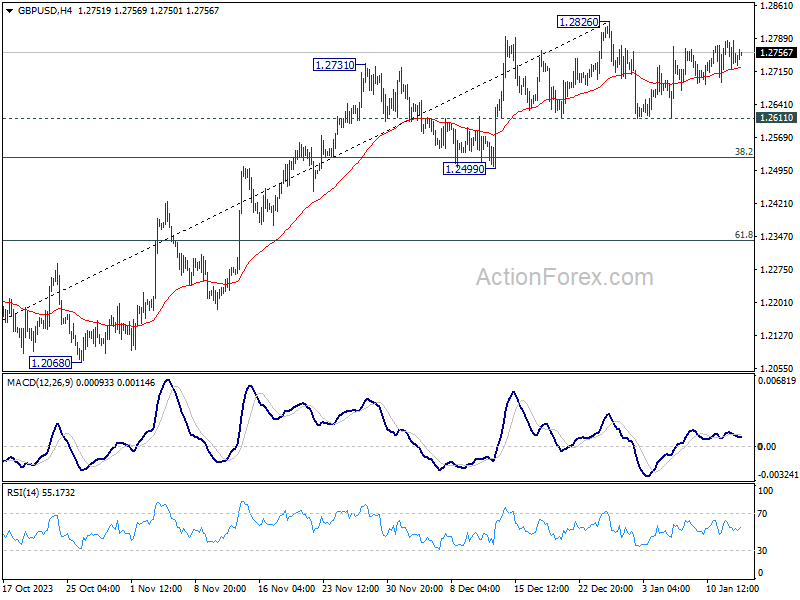

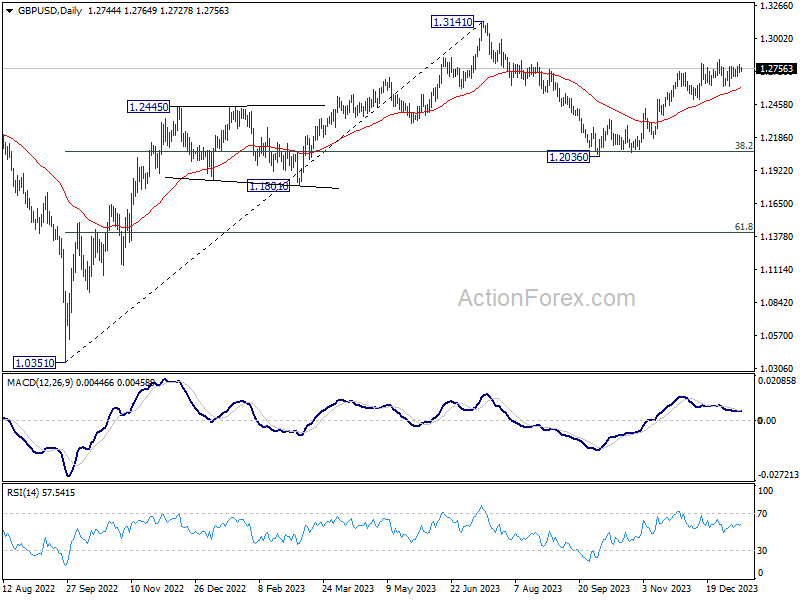

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2721; (P) 1.2753; (R1) 1.2787; More...

Intraday bias in GBP/USD remains neutral as it's still bounded in range below 1.2826. More sideway trading could be seen. On the upside, decisive break of 1.2826 will resume whole rally from 1.2036. Nevertheless, another fall and break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Tranquil Opening to a Data-Heavy Week: Major Data from US, UK, Japan Featured

The forex markets commenced the week on a relatively quiet note, despite generally positive risk sentiment. This was highlighted by Japan's Nikkei, which continued its impressive performance, breaking above 35k mark to reach new three-decade highs. The robust momentum could continue until the eagerly awaited BoJ meeting later in the month, where fresh economic forecasts are set to be revealed.

On the other hand, stocks in China and Hong Kong, meanwhile, presented a picture of stability, seemingly unaffected by PBoC's decision to keep the key policy interest rate unchanged. This decision, while unexpected, did not cause significant ripples in the markets, possibly due to a wait-and-see approach among investors in these regions.

Currency markets, meanwhile, displayed a notable lack of dynamism. Major currency pairs and crosses were largely confined within the trading ranges established last Friday. Within this context, Sterling stands out as the month's strongest performer so far, a position followed by Dollar and then Euro. Conversely, Japanese Yen finds itself at the bottom of the performance ladder, with Australian and New Zealand Dollars also underperforming. Swiss Franc and Canadian Dollar are positioned in the middle.

Subdued trading atmosphere is likely to persist through the day, with stock and bond markets closed for Martin Luther King Day. Eurozone's industrial production and trade balance, alongside Canada's manufacturing sales figures, are the main featured which might not trigger much reactions. Nevertheless, the week promises to ramp up in volatility with a barrage of crucial economic data scheduled for release, spanning all major currencies. This includes impactful releases from US, UK, Canada, Australia, Japan, and China.

Technically, Copper is worth a watch in the coming days. As fall from 3.9346 extends, immediate focus is now on 3.6833 support. Decisive break there will confirm that whole rebound from 3.5021 has completed at 3.9436. Deeper fall would be seen back to retest 3.5021, even if it's just in sideway consolidation. This development, if realized, could drag AUD/USD through 0.6639 support.

In Asia, at the time of writing, Nikkei is up 0.89%. Hong Kong HSI is down -0.10%. China Shanghai SSE is up 0.19%> Singapore Strait Times is up 0.25%. Japan 10-year JGB yield is down -0.0285 at 0.562.

ECB's Lane: Wage increases as determinants for rate cut timing and extent

In an interview with Corriere della Sera, ECB Chief Economist Philip Lane acknowledged that the December inflation data was "broadly in line with our projections". He highlighted a "continued progress" in easing of core inflation, yet pointed out existing "headwinds to services inflation."

A critical point raised by Lane concerns wage growth, which he notes is still rising well above any kind of long-run equilibrium rate". ECB is expecting "high wage increases" to continue in 2024. "the scale of that will determine the timing and the scale of rate adjustment this year," he added.

Lane also touched upon ECB's reliance on data. He mentioned that while new wage data is received weekly, the "most complete dataset" from Eurostat's national accounts will only be available at the end of April.

This timeline suggests that key policy decisions, especially those pertaining to rate cuts, are likely to be heavily influenced by data available by June meeting.

Finally, Lane's projection of a "significant recovery" in the European economy this year is tempered with caution, as he acknowledges downside risks to their forecasts. The question of whether 2024 will see a recovery or a continuation of the stagnation experienced in 2023 remains a "big data question" for ECB.

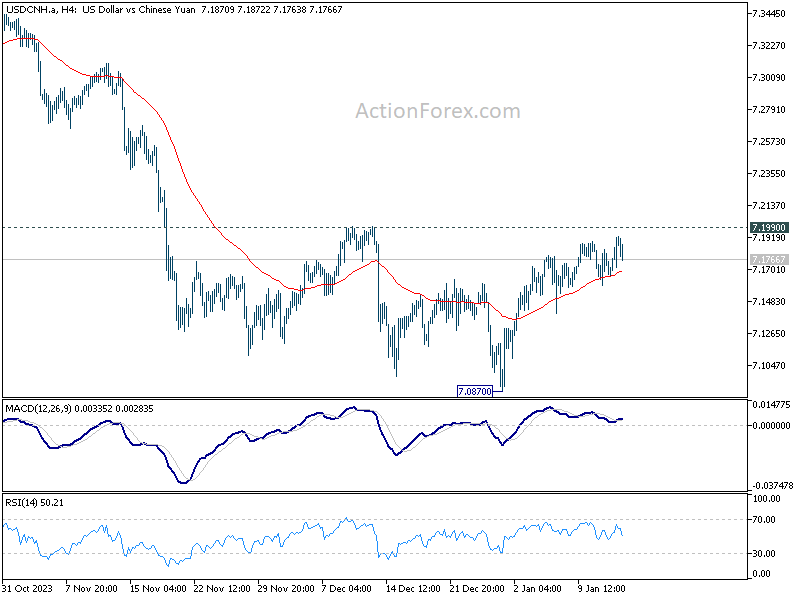

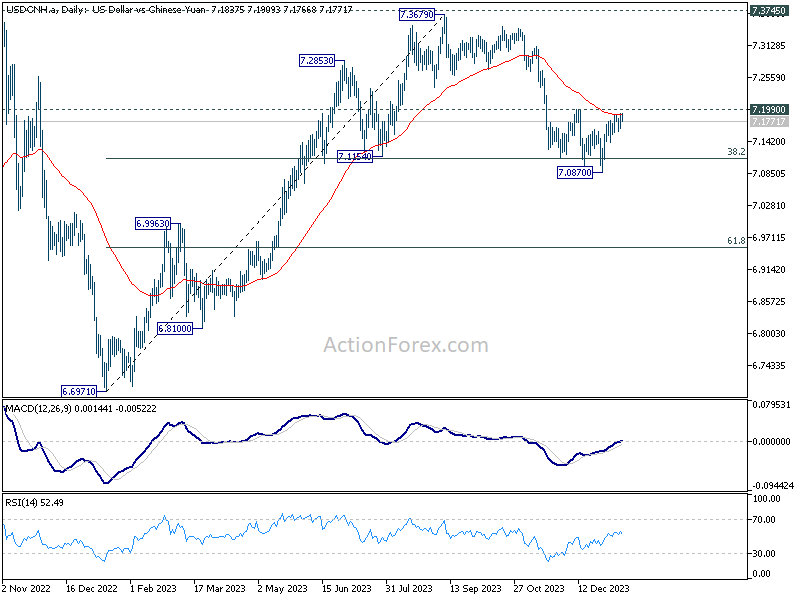

Contrary to market expectations, PBoC maintains MLF rate but increases liquidity

Despite the anticipation of a rate cut to bolster the weakening economy, currently grappling with deflation for the past three months, PBoC held firm, keeping the rate on CNY 995B worth of one-year medium-term lending facility loans steady at 2.50%. This decision defied the general expectation of a 0.1% cut to 2.40%.

Opting not to alter the policy rate, the central bank instead chose to enhance liquidity in the banking system. This is seen from the net injection of CNY 216B of fresh funds, following the expiration of CNY 779B worth of MLF loans this month. Moreover, PBoC also infused CNY 89B yuan through seven-day reverse repos, maintaining a stable borrowing cost at 1.80%.

There is little reaction from USD/CNH to PBoC's announcement. Technically, USD/CNH is now at a critical juncture, pressing 55 D EMA, just ahead of 7.199 near term resistance. Near term outlook is staying bearish. Another decline and break of 7.0870 short term bottoming will resume the whole fall from 7.3679 to 61.8% retracement of 6.6971 to 7.3679 at 6.9533.

However, firm break of 7.1990 will argue that the fall from 7.3679 has completed and turn near term outlook bullish for retesting this high.

A hectic week Ahead: Gauging the path of global monetary easing through key economic data

A plethora of crucial economic data sets the stage for volatility in the currency markets this week. The dataset encompasses a wide range from inflation, retail sales, employment, to investor confidence across majorly traded currencies. The pivotal question at this juncture is identifying which data could potentially be the most influential in swaying currency movements.

The year 2024 has unmistakably been earmarked as a period of interest rate reductions, with the exception of BoJ. The primary uncertainties lie in pinpointing the exact timing of the initial rate cut and the subsequent velocity of monetary policy relaxation. Current market pricing appears quite assertive, predicting up to six rate cuts by both Fed and ECB, and five cuts each by BoE and the BoC. This aggressive market stance argues that traders are bracing for potential major economic or financial shocks globally this year.

In a scenario devoid of significant shocks, the response of various currencies to economic data releases is likely to hinge on the particular phase of the disinflation cycle each region is experiencing. For US, Eurozone, and Canada, where substantial disinflationary progress has been made, any data underscoring growth shortfalls could incite speculations of earlier and more rapid policy easing. Conversely, in UK and Australia, where inflation levels remain elevated, surprises on the higher end of inflation data could limit the scope for BoE and RBA in implementing rate cuts.

Hence, the spotlight could be marginally more focused on a few key data points: US retail sales, UK CPI and wage growth figures, Canadian retail sales, and Australian employment. Additionally, Japan's CPI and China's GDP might also contribute to market volatility. In terms of central bank activities, both Fed's Beige Book and meeting accounts from ECB are not anticipated to offer any significant revelations that are not already factored into market expectations.

Here are some highlights for the week:

- Monday: Eurozone industrial production, trade balance; Canada manufacturing sales, wholesale sales, BoC business outlook survey.

- Tuesday; New Zealand NZIER business confidence; Australia Westpac consumer confidence; Japan PPI; Germany CPI final, ZEW economic sentiment; UK employment; Canada CPI, housing starts; US Empire state manufacturing.

- Wednesday: China GDP, industrial production, retail sales, fixed asset investment; UK CPI, PPI; Eurozone CPI final; Canada IPPI and RMPI; US retail sales, import prices, industrial production,business inventories, NAHB housing index, Fed's Beige Book.

- Thursday: Japan machine orders; Australia employment; ECB meeting accounts; US jobless claims, housing starts and building permits, Philly Fed survey.

- Friday: New Zealand BusinessNZ manufacturing; Japan CPI, tertiary industry index; Germany PPI, UK retail sales; Swiss PPI; Canada retail sales; US U of Michigan consumer sentiment, existing home sales

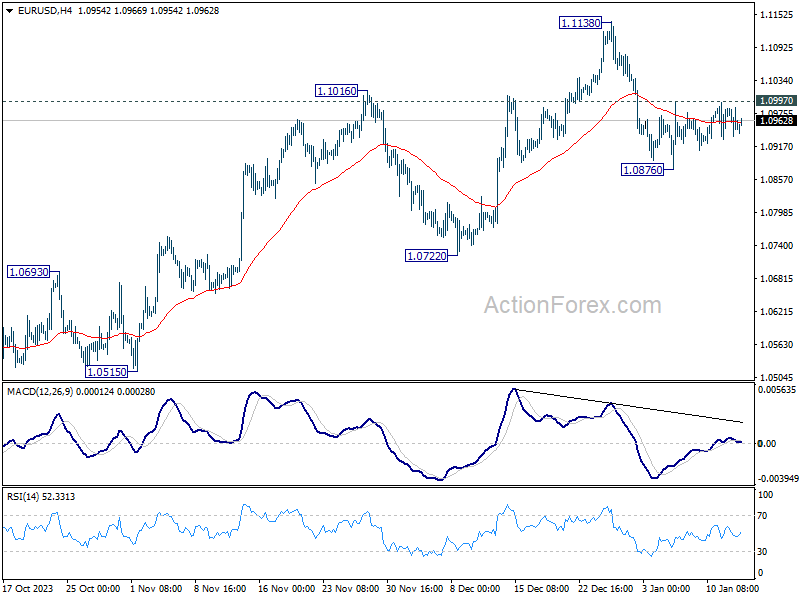

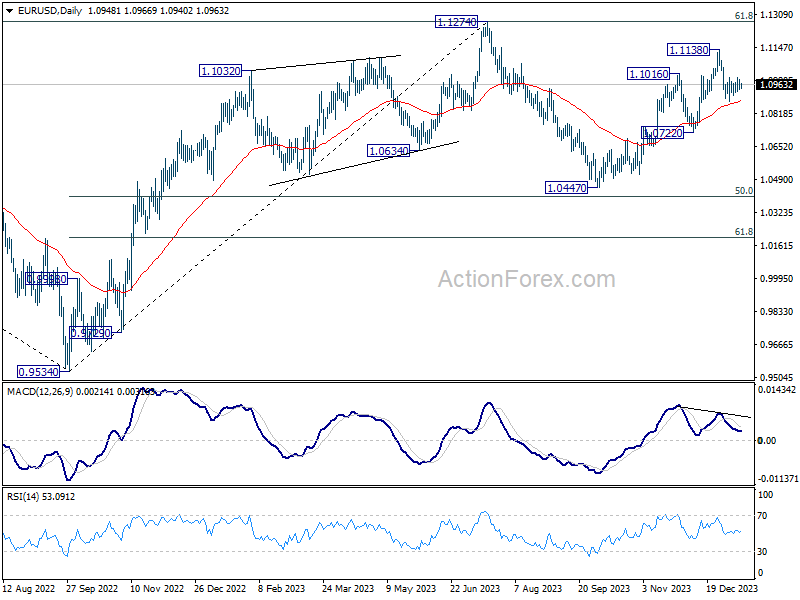

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0929; (P) 1.0958; (R1) 1.0980; More...

EUR/USD is still bounded in range trading and intraday bias remains neutral. Further fall is in favor as long as 1.0997 minor resistance intact. Break of 1.0876 will resume the fall from 1.1138 to 1.0722 support next. Nevertheless, firm break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Dec | 2.30% | 2.20% | 2.30% | |

| 00:00 | AUD | TD Securities Inflation M/M Dec | 1.00% | 0.30% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Dec | -15.50% | -13.60% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Nov | -0.30% | -0.70% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Nov | 11.2B | 10.9B | ||

| 13:30 | CAD | Manufacturing Sales M/M Nov | 0.90% |