Sample Category Title

In a World Gone Bananas, Don’t Squash the Other Fruit

Policy interest rates needed to increase from their pandemic lows, but there is a question of how far central banks really need to lean against apparently strong demand. What appears to be demand-driven could be a ripple effect from supply shocks affecting other products.

When Cyclone Larry hit North Queensland in 2006, most of Australia’s banana crop was knocked out. Banana prices increased around 400%. This was enough to add more than ½ a percentage point to inflation in the June quarter of that year. It was also one of the cleanest examples of a supply shock that monetary policy should look through. (And at the time resulted in me uttering the sentence, “Of course we can see through bananas!”. But that’s another story.)

Less well known is that prices of other fruit increased in that period, even though those crops were not damaged by the cyclone. This happened because, at those prices, people stopped buying bananas and substituted into other fruit, pushing their prices up. As banana supply normalised, prices of those fruit normalised too.

The question is, should we interpret the impact on prices of those other fruit as “demand-driven”? After all, their prices increased and so did the quantity consumed, the pattern you would expect to see with a positive demand shock.

Through the pandemic period and following Russia’ s invasion of Ukraine, supply shocks were prominent. Factories and other businesses were closed, shipping was disrupted, and domestic logistics were constrained. But there was also stimulus to demand coming from the extraordinary fiscal and monetary policy support. If the prescription for monetary policy is to look through temporary supply shocks to the extent one can without inflation expectations rising, but respond to demand-driven inflation, how do you tell the difference in this situation? This issue becomes especially relevant given the RBA’s assessment that inflation is becoming “increasingly homegrown and demand driven”.

One approach to this is simply to follow the logic that if price went up and quantity consumed went down, it must be supply-driven, while if both increased, it was demand-driven. This is the essence of a methodology developed at the Federal Reserve Bank of San Francisco and used by the RBA. It implies that about half the surge in inflation of recent years stemmed from supply shocks, with the rest coming from strong demand. Different methods using model-based estimates attribute a bit more of the increase in inflation to supply shocks, but the conclusions are qualitatively similar. But is this the right way to interpret recent price moves? Or, with apologies to Jeanette Winterson, is this another case of bananas not being the only fruit?

The complicated way to assess this would be to estimate how much of the price movements in the “demand-driven” components of the CPI reflected demand shifting from supply-constrained components, and how much was from stronger underlying demand. This would become intractable faster than you can say “estimate cross-elasticities of demand”. Another way would be to estimate how much of the increase in overall inflation is explained by the usual drivers of demand, such as income, for example using standard demand-driven models such as a Phillips Curve. The RBA have done this calculation using their own models. As noted above, these exercises do suggest that supply shocks were a bit more important than the San Francisco Fed approach, with demand-driven inflation playing a smaller, but still important, role. But these estimates are only as good as your model.

The simpler way is to remember that inflation is an aggregate phenomenon that should abstract from relative price shifts. It is the balance of aggregate demand and supply that matters. One way to assess aggregate demand for consumption goods and services is by looking at total consumption. Unlike in some peer economies, it has been weak of late in Australia, especially in per capita terms. After initially bouncing back to its pre-pandemic trend when the economy opened up, more recently consumption has been weaker than many expected. This is largely because real household incomes have gone backwards, squeezed by inflation itself, rising taxation and higher interest rates. There are clearly pockets of strong demand and some households are still cashed up with pandemic-related extra savings. But there is always a diversity of experience across households, and these distributional issues should not entirely overthrow an assessment of the aggregate situation.

Last week we saw the November monthly CPI indicator surprise a little on the downside. As our Westpac Economics colleague Senior Economist Justin Smirk noted, the categories that were lower than expected included personal services categories that the RBA had previously been pointing to as evidence of resilient demand.

Slower demand for discretionary services might be a response to the squeeze on household incomes, including from high inflation. But it could also be partly an adjustment as overseas travel patterns normalise. The international borders reopened in 2022, but airline capacity has taken longer to recover. On some metrics, it has still not done so completely. As long as supply in this industry is constrained and airfares higher than pre-pandemic, we should not be surprised to see domestic holidaying and other domestic services demand pushed up as a substitute. And just like the other fruit, we should not be surprised if demand for these services slows as supply constraints on international travel subside.

One upside surprise in the month was in homebuilding costs, which reached 35% above their level four years previously in November 2019. Growth in this component actually picked up in the month. Given the low level of dwelling investment, it is hard to attribute this to strong demand. But neither can we point to global supply chain issues as the culprit anymore. In Canada, one of the few other countries that include homebuilding costs in their CPI, this component has been falling for some months and is up 24% over the same four-year period. Rather, the domestic homebuilding industry remains supply-constrained. The backlog of already approved projects remains high. Meanwhile some capacity has exited, either through bankruptcy or the bid from infrastructure and other non-residential construction projects.

The rapid inflation of rents can, by contrast, be seen as the effect of strong demand. The population surge has strained this market. Vacancy rates are low, and it is hard to see how supply could have kept up, even if the building industry had not been as constrained as it is. But we do not expect this surge to be repeated in 2024. While still elevated by historical standards, demand pressures will gradually subside. Over time this will take some pressure off rental inflation without further action from monetary policy.

Even if the inflation surge had been driven solely by supply shocks, central banks would still have needed to raise policy rates. Both fiscal and monetary policy had been extremely accommodative. This extraordinary pandemic-era support was no longer needed. It was also important to demonstrate resolve and prevent inflation expectations rising. In thinking about how contractionary policy needs to be – and for how long – this expectations channel is important, and there is more to say about it. But it is just as important to be clear on how much of the current inflation is truly demand-driven. Otherwise, policymakers risk squashing the other fruit, to no real benefit.

A Black Friday Technical Aside

This “other fruit” issue is different from the well-known “substitution bias” issue in CPIs. Substitution bias arises because the CPI is compiled using fixed weights for each category. It does not allow for shifting spending patterns in response to large price changes, at least not at first. The spike in banana prices therefore fed through to the CPI as if people were still buying the same number of bananas. The ABS does reweight the CPI to account for these changes, and in recent years it has done so more often than it did back when Cyclone Larry hit, especially for fruit and vegetables, where it now has access to supermarket scanner data. But even with this improvement in data collection methods, measured CPIs tend to overstate people’s experience of this kind of price spikes.

A similar issue is becoming more prominent recently, with the increasing shift of pre-Christmas spending from December into the Black Friday sales in November. This time, the substitution is across time not fruit: people are buying the cheaper on-sale item instead of the full-price item the following month. Retail sales data show that spending is increasingly shifting into the discounted period. Even if household goods prices were being measured monthly, a quarterly CPI would miss the dampening effect on prices of spending being increasingly concentrated in the sales periods. The situation is even worse than that in Australia, though: many goods prices are currently only measured in the first month of the quarter, so Australia’s monthly and quarterly CPI data entirely miss the discounting in November. Prices come back in December, so longer-term trends are less distorted. But these measurement issues will matter for interpretation of December quarter CPI results.

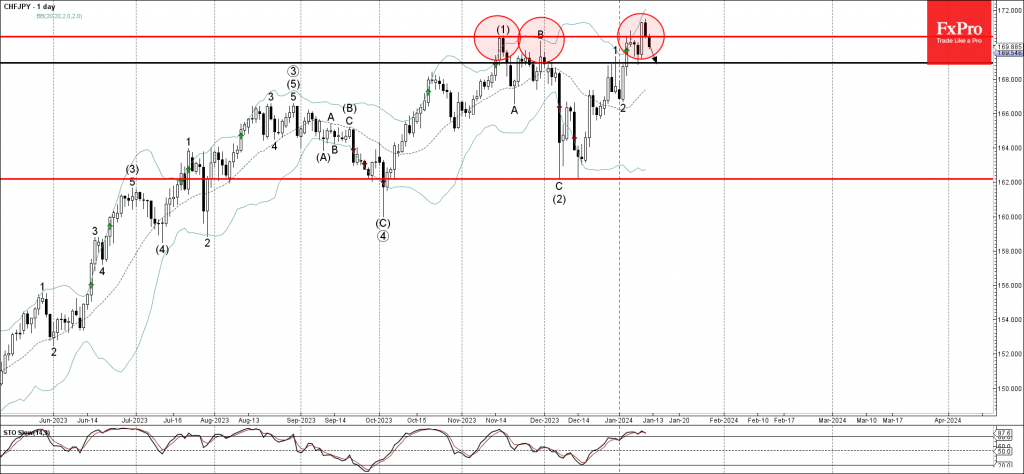

CHFJPY Wave Analysis

- CHFJPY reversed from resistance level 170.50

- Likely to fall to support level 168.95

CHFJPY currency pair recently reversed down from the key resistance level 170.50 (former double top from November).

The downward reversal from the resistance level 170.50 created the daily candlesticks reversal pattern Dark Cloud Cover.

Given the overbought daily Stochastic, CHFJPY currency pair can be expected to fall further to the next support level 168.95.

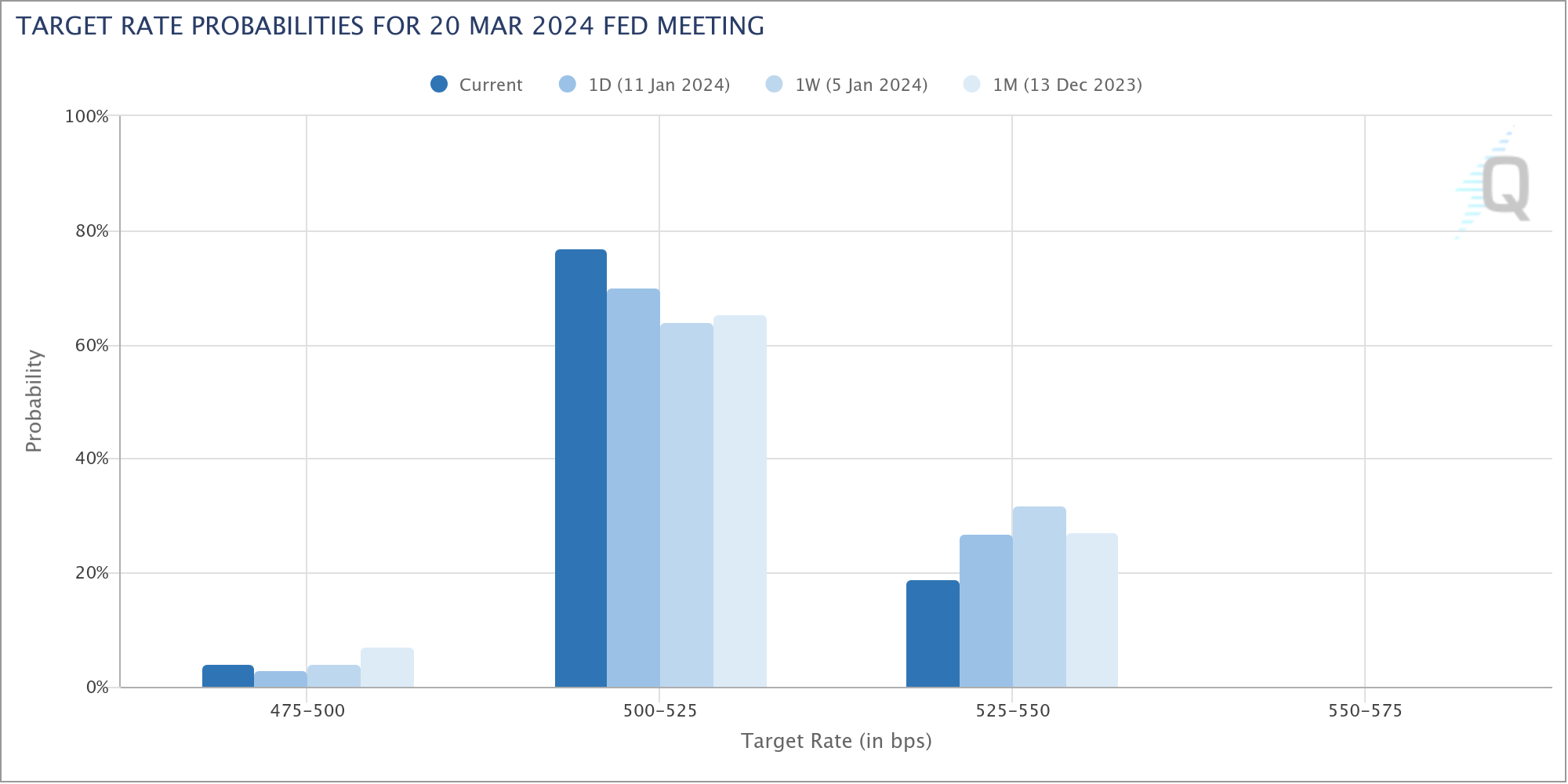

Dollar’s Indecisive Week, Rate Cut Bets Hold Despite Inflation Surprises

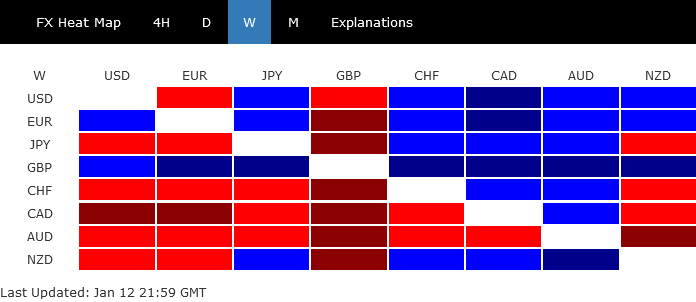

Dollar demonstrated a distinct lack of decisiveness in its trading last week, encapsulating a theme of uncertainty that has become characteristic since the start of the year. The greenback has indeed close the week within prior week's range against most major counterparts, with Canadian Dollar being the only exception.

This pattern of indecision is largely rooted in the lack of clarity over Fed's rate path, even though monetary easing is widely expected this year. The stronger-than-expected inflation data has not deterred market participants from bettering on a rate cut in March. However, this viewpoint is not uniformly held, as economists present a divided front.

The overall development also led to cautious and subdued risk sentiment across financial markets. This ongoing ambiguity could continue to maintain a low volatility environment for Dollar in the near term.

Meanwhile, Japanese Yen experienced varied fortunes, initially facing downward pressure due to receding speculation of an imminent rate hike by BoJ. The week was riddled with mixed messages from various media sources regarding BoJ's stance, contributing to market confusion and volatility. Despite this, Yen managed to mount a recovery towards the week's end, benefiting from decline in global benchmark treasury yields.

The broader currency markets saw British Pound emerged as the standout performer, receiving a mild boost from GDP data that surpassed expectations. Euro followed closely as the second strongest, trailed by Dollar.

Conversely, Australian Dollar bore the brunt of market skepticism, ending the week as the weakest link. Its performance was influenced by the downturn in Chinese stock markets and a tepid response to slightly better-than-expected Chinese economic data. Canadian Dollar and the Swiss Franc also found themselves on the weaker end of the spectrum.

Dollar's indecision persists amid Fed's policy uncertainty

Dollar has been characterized by a notable lack of clear direction, oscillating between brief rallies and selloffs without establishing a sustained trend. This indecision in greenback's movement is largely attributed to the mixed signals from recent economic data and the uncertainty surrounding Fed's monetary policy path for the year ahead.

Despite an initial surge at the outset of 2023, Dollar has struggled to sustain its momentum. Recent economic releases, including the surprisingly strong CPI and solid non-farm payroll data, failed to catalyze a lasting rally. Equally, weaker-than-anticipated ISM services data did not trigger a significant downturn.

The anticipation of Fed's monetary policy path remains a central theme. Fed fund futures have been aggressive, pricing in over 80% likelihood of a rate cut as early as March, with an expected total easing of 1.50% by the end of 2024. This aggressive stance contrasts with more conservative forecasts from some economists, who anticipate the initiation of rate cuts in June, followed by potentially two more within the year, aligning more closely with Fed's own projections

Federal Reserve officials have maintained a balanced stance in their recent communications. While acknowledging the forecasts for rate cuts in 2024, they have emphasized the prematurity of fixing a timeline and pace for policy adjustments, especially considering the current month is only January. The lack of clear expectations on Fed's path could keep Dollar's movement indecisive for some time.

Dollar index stayed in tight range below 103.10 temporary top last week. Overall outlook is unchanged that fall from 107.34 is seen as the second leg of the consolidation pattern from 99.57. Below 101.90 minor support would bring deeper selloff through 100.61. But downside should be contained by 99.57 low to bring rebound. Meanwhile, break of 55 D EMA (now at 103.24) is the first sign that fall from 107.34 has completed. Sustained trading above 104.26 resistance will argue that rise from 100.61 is already the third leg of the pattern and target 107.34.

Meanwhile, 10-year yield closed notably lower at 3.95 last week after failing to stay firm above 4% handle. Nevertheless, outlook is unchanged that a short term bottom was formed at 3.785 and the consolidation pattern from there is going to extend for a while. Any retreat at this stage should be contained above 3.785. Another rise is expected to 55 D EMA (now at 4.170), and possibly higher, until meeting strong resistance from 38.2% retracement of 4.997 to 3.785 at 4.247.

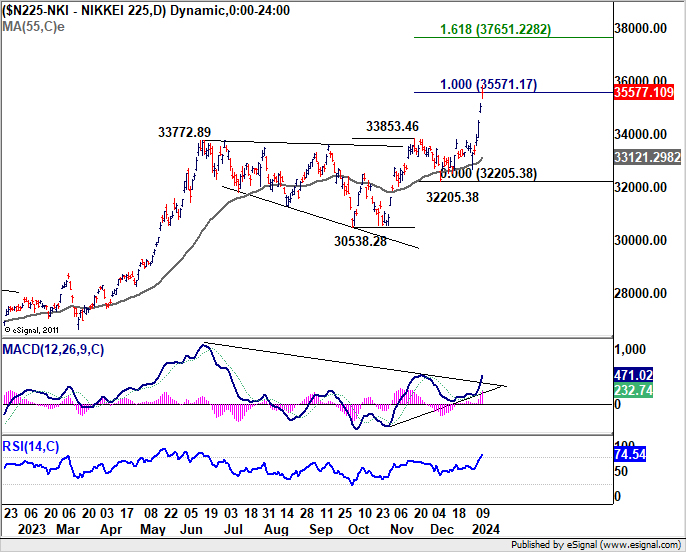

Nikkei soars to 30-year high amid speculation of BoJ's hesitance on rate hike

Japanese financial market has seen significant movements this week, with Nikkei index reaching its highest level in over three decades. This surge is primarily attributed to growing speculation around BoJ's monetary policy, as latest reports of unexpectedly muted wage growth in November have fueled doubts about the emergence of a wage-price cycle robust enough for the central bank to consider an interest rate increase.

Several media reports have further influenced market perceptions. Bloomberg, citing unnamed sources, reported that BoJ officials might be contemplating a downward revision of core CPI forecast for the fiscal year starting April 2024. The forecast could be adjusted from the previous 2.8% to 2.5%, owing to the recent decline in oil prices.

Channel News Asia also provided insights from their sources, suggesting that while core inflation forecast for fiscal 2024 might be lowered, CPI core-core forecast would likely remain close to 2% target, at 1.9% for both fiscal 2024 and 2025. According to CNA's sources, consumer spending is holding up well, and there is a growing conviction that wage hikes will continue and possibly broaden this year. Another source indicated that the overall uptrend in inflation and wages remains intact.

These conflicting reports and the ambiguity they bring could limit any significant recovery attempts by Yen in the short term. The market is keenly awaiting BoJ's updated quarterly projections, scheduled to be released during its meeting on January 22-23. Moreover, the outcomes of Spring wages negotiations will play a crucial role in shaping BoJ's decision-making, particularly regarding a potential rate hike in April.

In the meantime, Nikkei finally broke out of its six-month range and surged to highest level in more than three decades, on speculation that BoJ is not ready to hike interest soon. For the near term, outlook in Nikkei will stay bullish as long as 33853.25 resistance turned support holds. Sustained trading above 100% projection of 30538.28 to 33853.46 from 32205.38 would prompt upside acceleration to 61.8% projection at 37651.22.

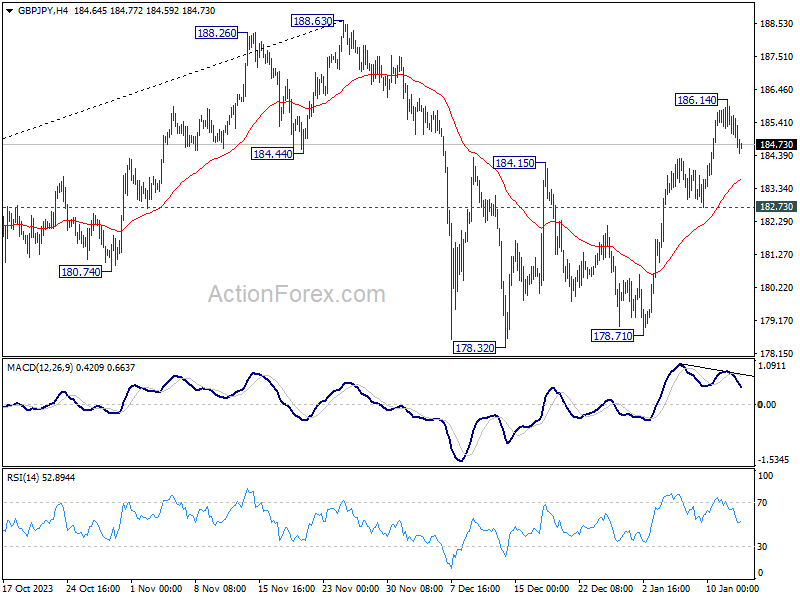

In the currency markets, GBP/JPY's strong rally confirmed that corrective fall from 188.63 has completed at 178.32 already. Rise from there could be the second leg of the corrective pattern from 188.63. But even in this less bullish case, further rally is expected as long as 182.73 support holds. Above 186.14 will resume the rebound to retest 188.63 high.

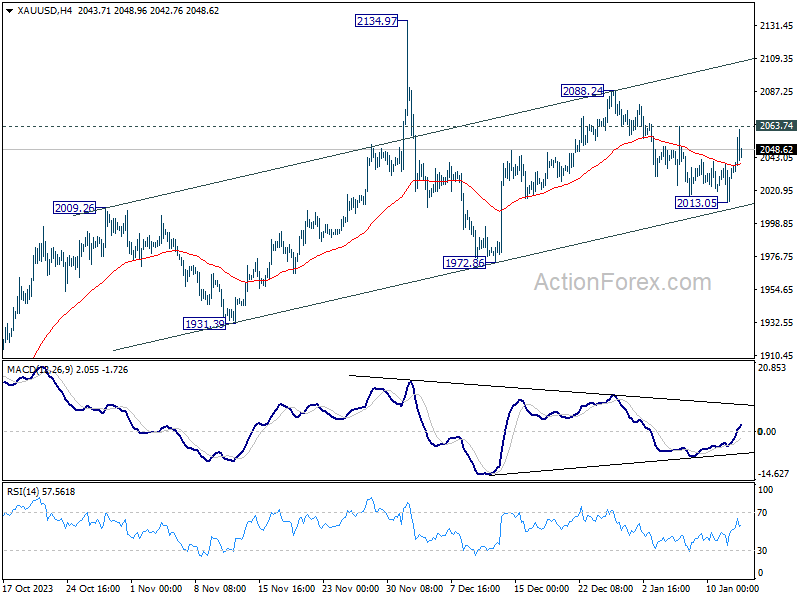

Safe haven demand boosts Gold in wake of US-led Yemen strikes

Gold rebound strongly, driven by escalating geopolitical tensions in the Middle East. The pivotal catalyst for this rally was the US and UK-led military actions against Houthi rebel targets in Yemen. The airstrikes, involving approximately 70 strikes, aimed to disrupt the Iran-backed Houthi group's aggressive activities in the critical Red Sea shipping lanes.

The response from the Houthis was one of defiance, as they threatened to intensify their attacks and declared all US and UK interests as "legitimate targets." This bold declaration raises the specter of a broader conflict, potentially drawing Western powers further into the complex Middle East situation.

From a technical analysis standpoint, Gold's rebound argues that corrective pull back from 2088.24 has completed at 2013.05 already, after defending near term rising channel support. Immediate focus is now on 2063.74 resistance. Firm break there should push Gold through 2088.24 to retest 2134.97 record high.

In the bigger picture, upside momentum hasn't been convincing as seen in D MACD. But Gold is holding above rising 55 D EMA, and maintaining near term bullishness. Current up trend is still in favor to continue to 100% projection of 1614.6o t0 2062.95 from 1810.26 at 2258.61.

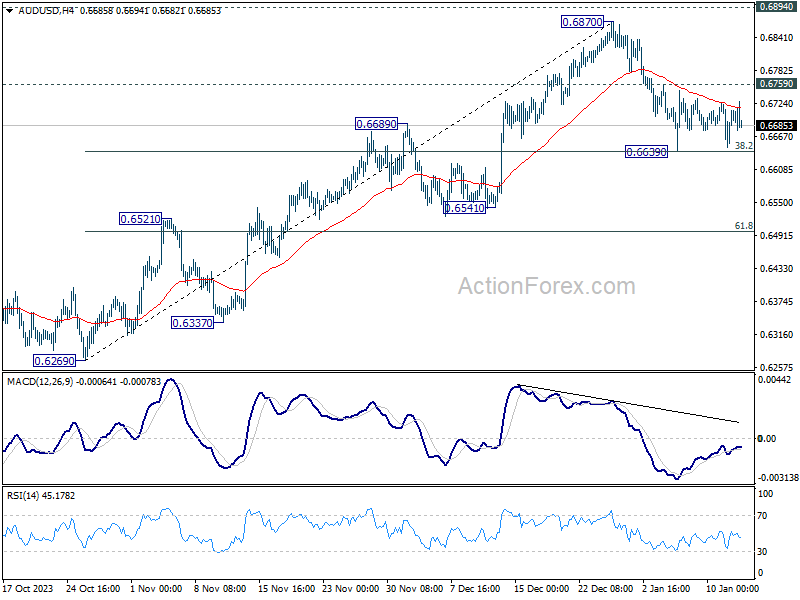

AUD/USD Weekly Report

AUD/USD turned into sideway trading above 0.6639 last week. Initial bias remains neutral this week and further decline is expected as long as 0.6759 minor resistance holds. Firm break of 0.6639 will resume the fall from 0.6870 to 61.8% retracement of 0.6269 to 0.6870 at 0.6497 next. On the upside, break of 0.6759 will bring retest of 0.6870 resistance instead.

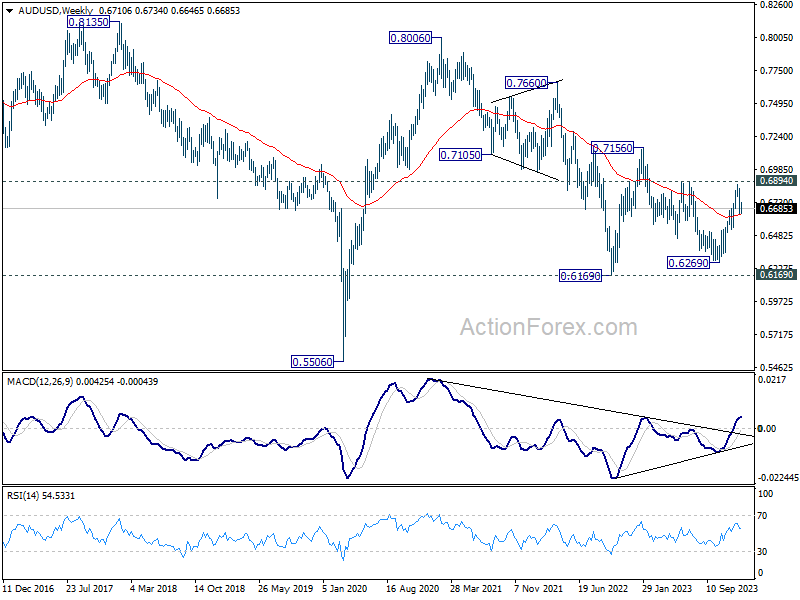

In the bigger picture, price actions from 0.6169 (2022 low) could be just a medium term corrective pattern to the down trend from 0.8006 (2021 high). Rise from 0.6269 is seen as the third leg of the pattern that could target 0.7156 on break of 0.6894 resistance. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

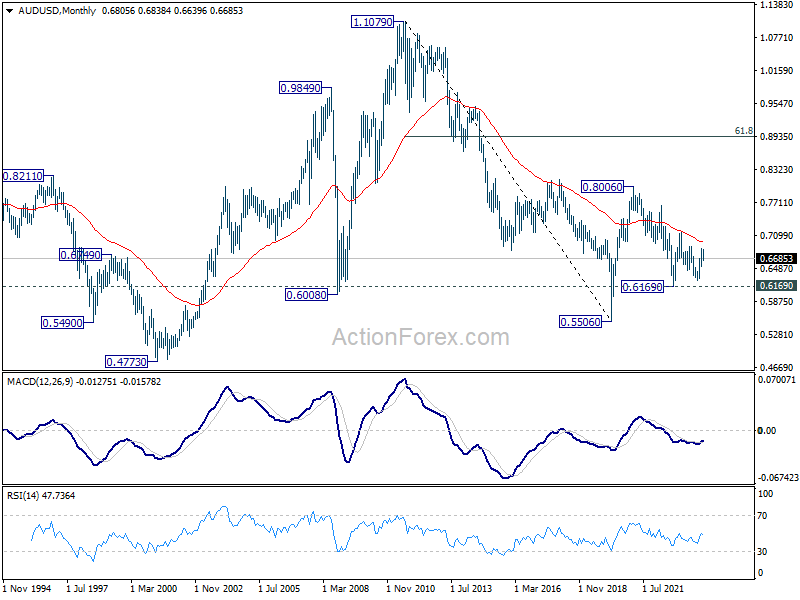

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen the second leg of the pattern. Hence, in case of deeper decline, downside strong support should emerge above 0.5506 to bring reversal.

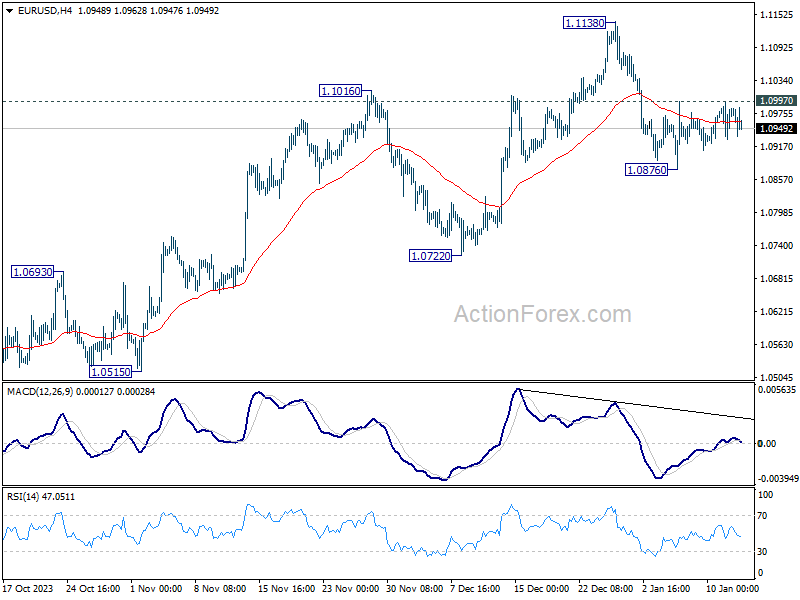

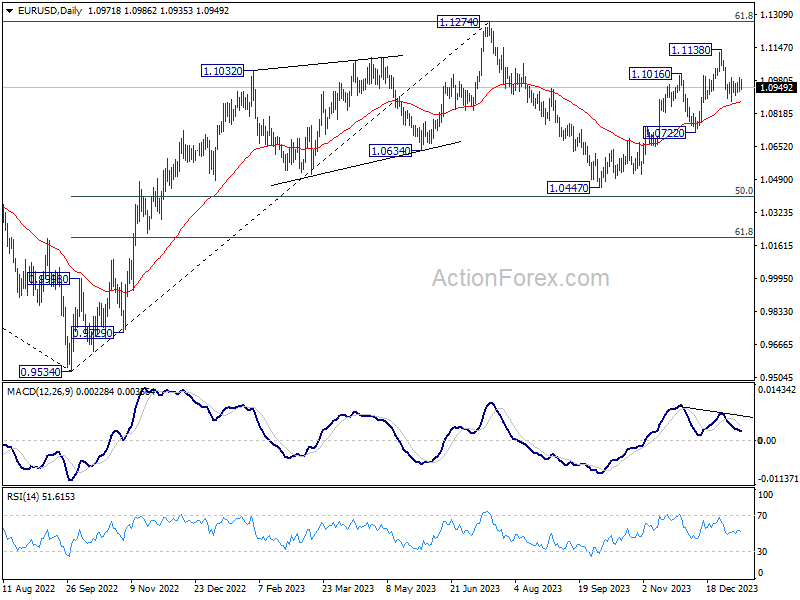

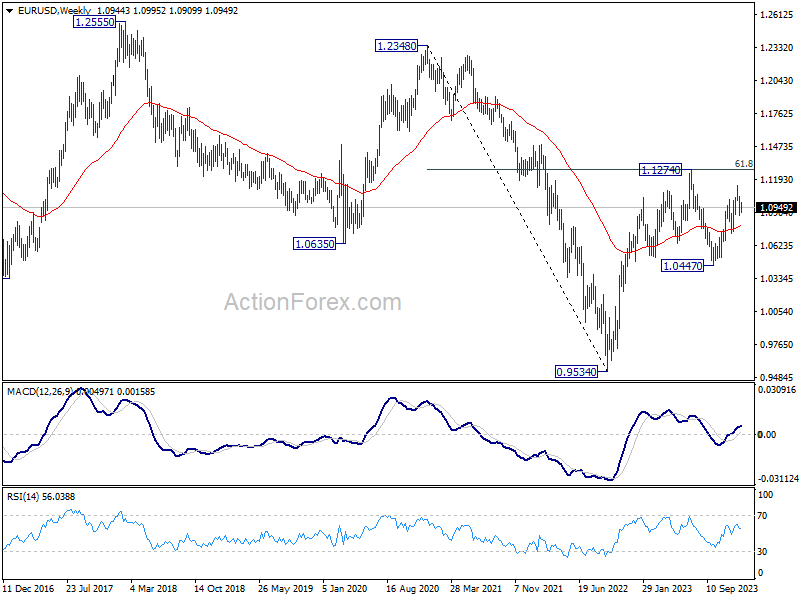

EUR/USD Weekly Outlook

EUR/USD turned into range trading above 1.0876 last week. Initial bias stays neutral this week first, but further fall is in favor as long as 1.0997 minor resistance intact. Break of 1.0876 will resume the fall from 1.1138 to 1.0722 support next. Nevertheless, firm break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

In the long term picture, a long term bottom is in place at 0.9534 on bullish convergence condition in M MACD. It's still early to call for bullish trend reversal with the pair staying inside falling channel in the monthly chart. Nevertheless, sustained trading above 55 M EMA (now at 1.1078) and break of 1.1274 resistance will raise the chance of reversal and target 1.2348 resistance for confirmation.

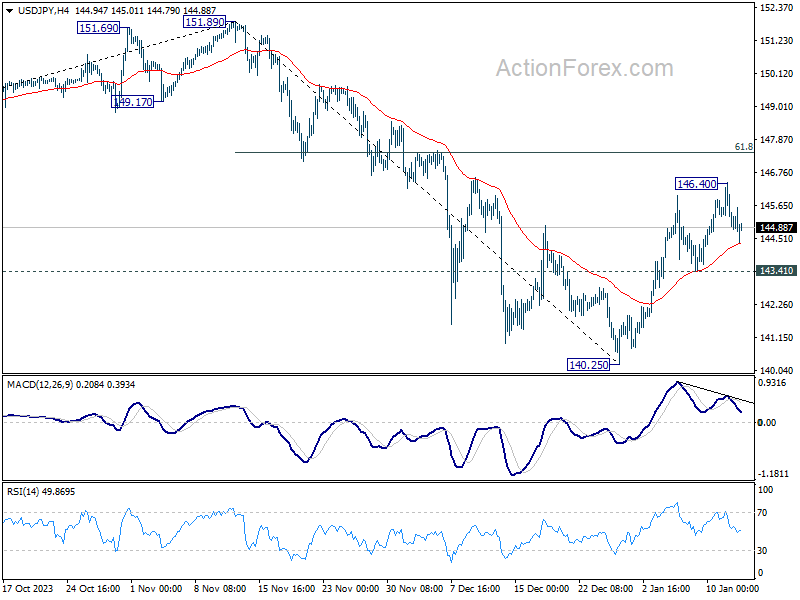

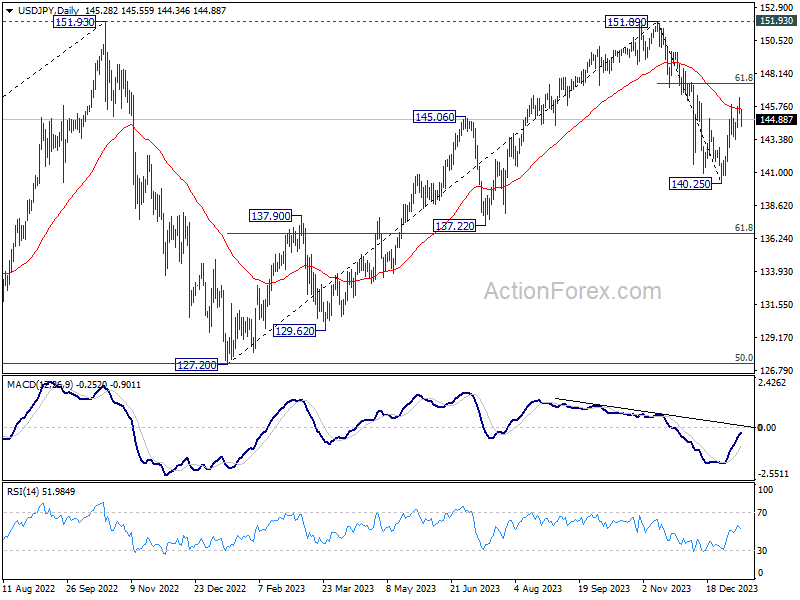

USD/JPY Weekly Outlook

USD/JPY's rebound from 140.25 resumed last week and edged higher to 146.40. But subsequent retreat indicates temporary topping. Initial bias is neutral this week first. Further rise is mildly in favor as long as 143.41 minor support holds. Above 146.40 will target 61.8% retracement of 151.89 to 140.25 at 147.44. Upside should be limited there to bring reversal. On the downside, break of 143.41 will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

In the long term picture, as long as 125.85 resistance turned support holds (2015 high), up trend from 75.56 (2011 low) is still in favor to continue through 151.93 (2022 high) at a later stage.

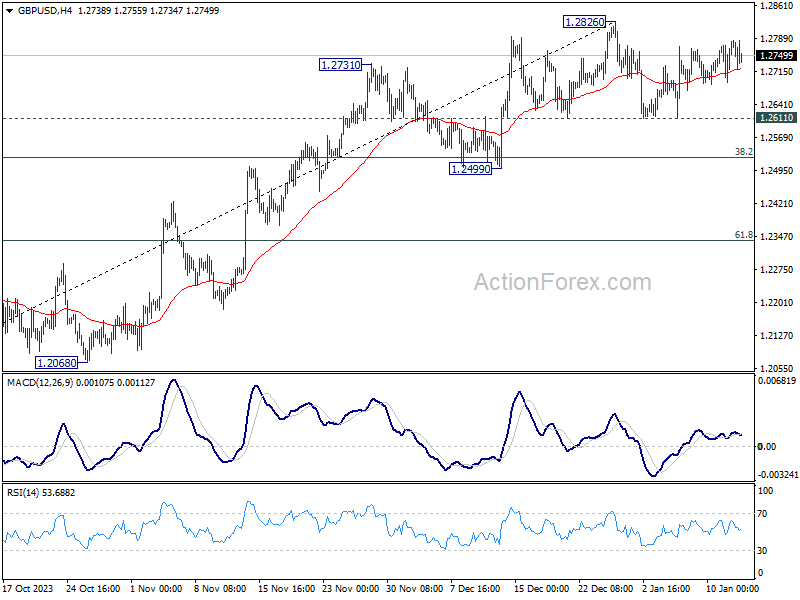

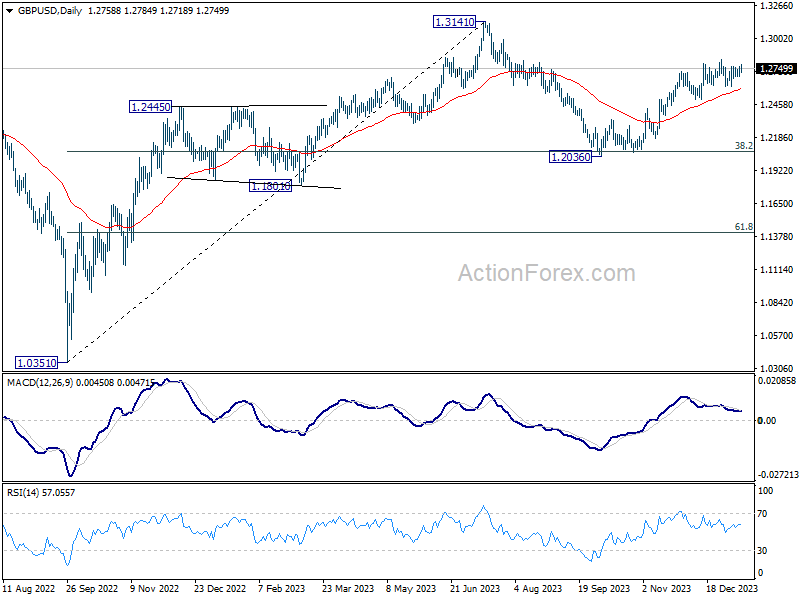

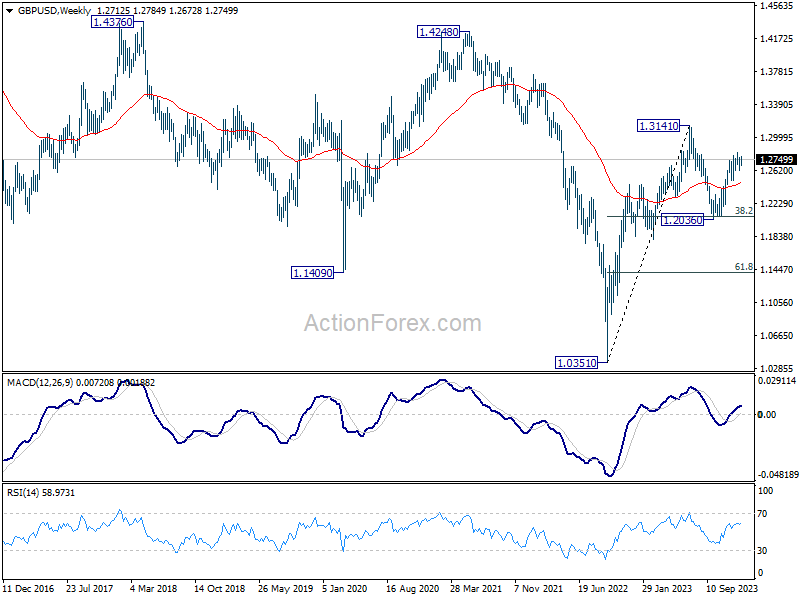

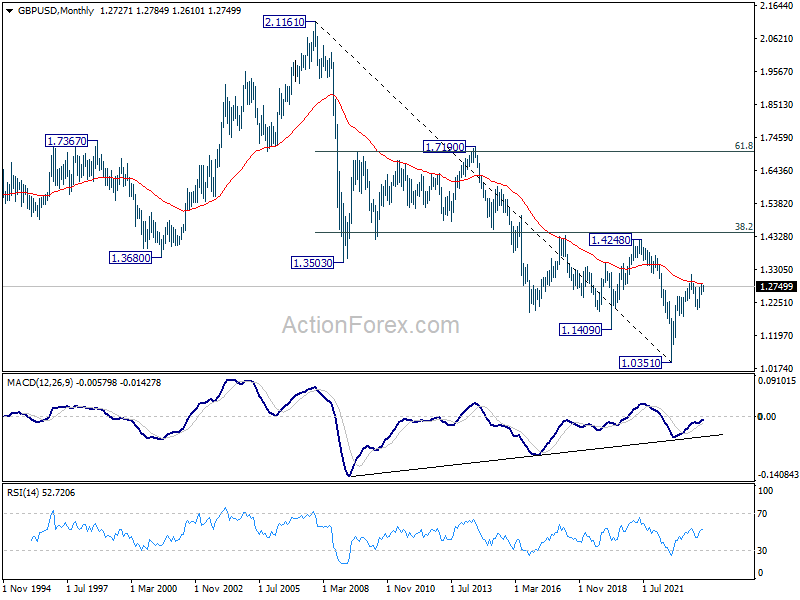

GBP/USD Weekly Outlook

GBP/USD gyrated higher last week but upside is capped below 1.2826 resistance. Initial bias stays neutral this week first, and more sideway trading would be seen. On the upside, decisive break of 1.2826 will resume whole rally from 1.2036. Nevertheless, another fall and break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

In the long term picture, a long term bottom should be in place at 1.0351 on bullish convergence condition in M MACD. But momentum of the rebound from 1.3051 argues GBP/USD is merely in consolidation, rather than trend reversal. Range trading is likely between 1.0351/4248 for some more time.

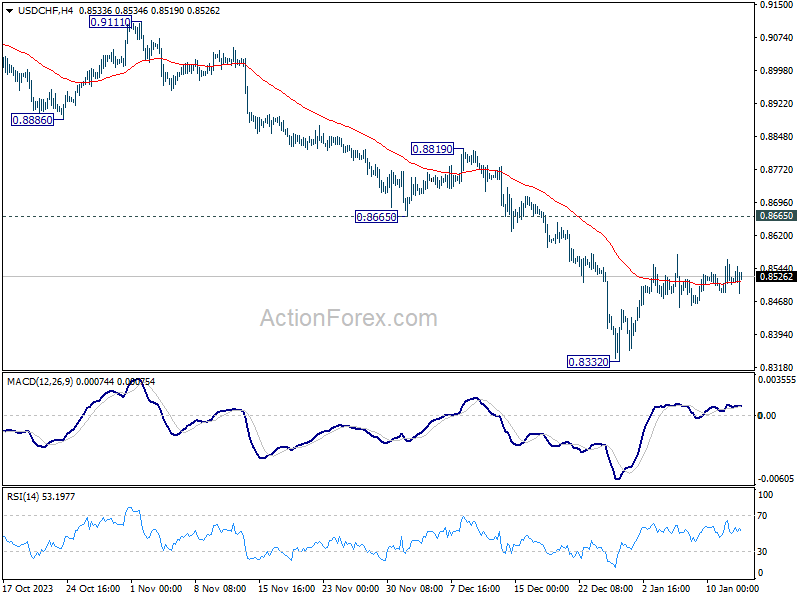

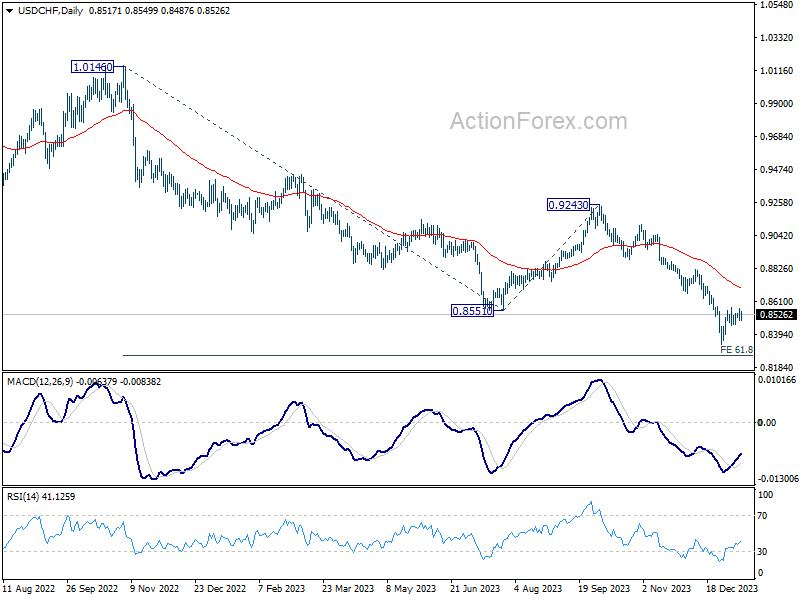

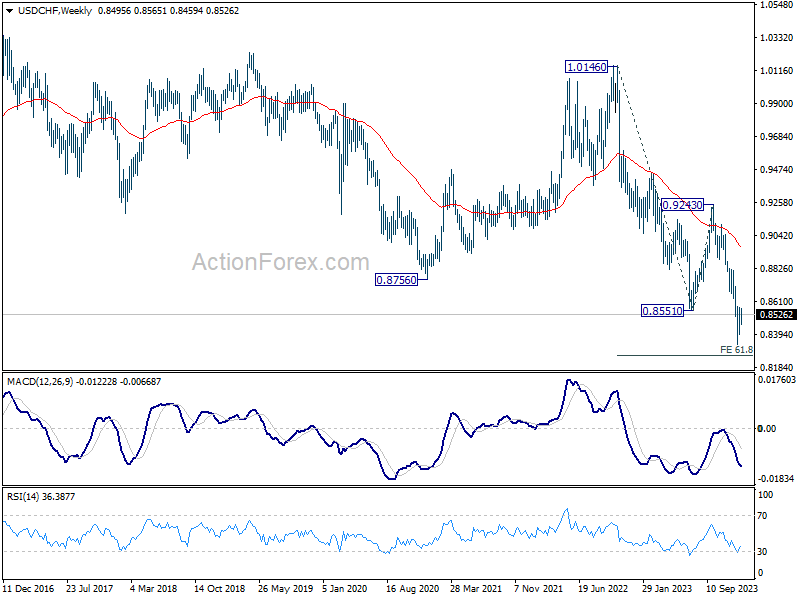

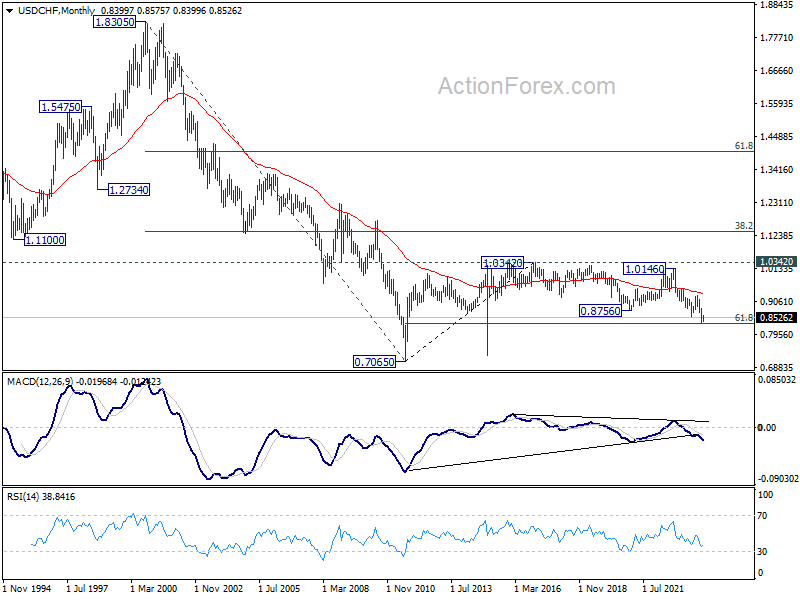

USD/CHF Weekly Outlook

USD/CHF stayed in consolidation above 0.8332 last week and outlook is unchanged. Initial bias stays neutral this week first. Outlook will also remain bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, down trend from 1.0146 (2022 high) is in progress. Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

In the long term picture, there is no clear sign that down trend from 1.8305 (2000 high) has completed. With 38.2% retracement of 1.8305 to 0.7065 at 1.1359 intact, outlook is neutral at best.

AUD/USD Weekly Report

AUD/USD turned into sideway trading above 0.6639 last week. Initial bias remains neutral this week and further decline is expected as long as 0.6759 minor resistance holds. Firm break of 0.6639 will resume the fall from 0.6870 to 61.8% retracement of 0.6269 to 0.6870 at 0.6497 next. On the upside, break of 0.6759 will bring retest of 0.6870 resistance instead.

In the bigger picture, price actions from 0.6169 (2022 low) could be just a medium term corrective pattern to the down trend from 0.8006 (2021 high). Rise from 0.6269 is seen as the third leg of the pattern that could target 0.7156 on break of 0.6894 resistance. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen the second leg of the pattern. Hence, in case of deeper decline, downside strong support should emerge above 0.5506 to bring reversal.

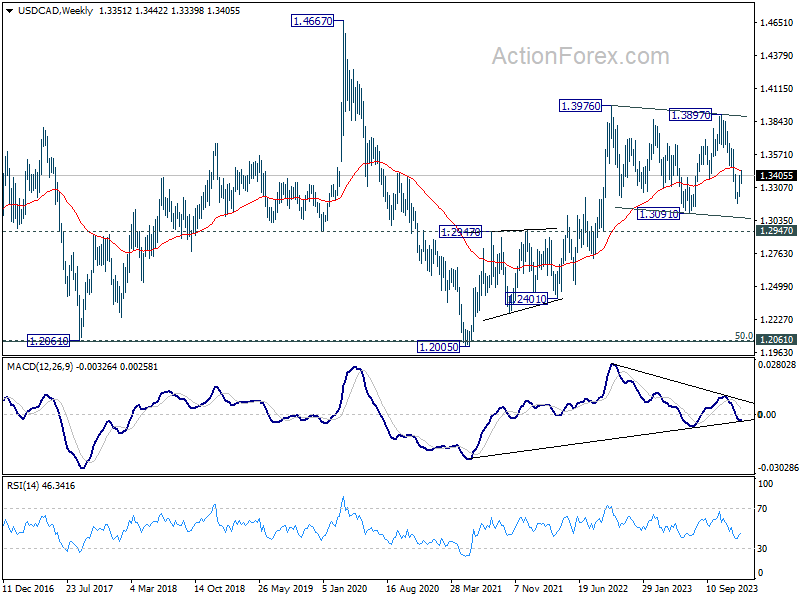

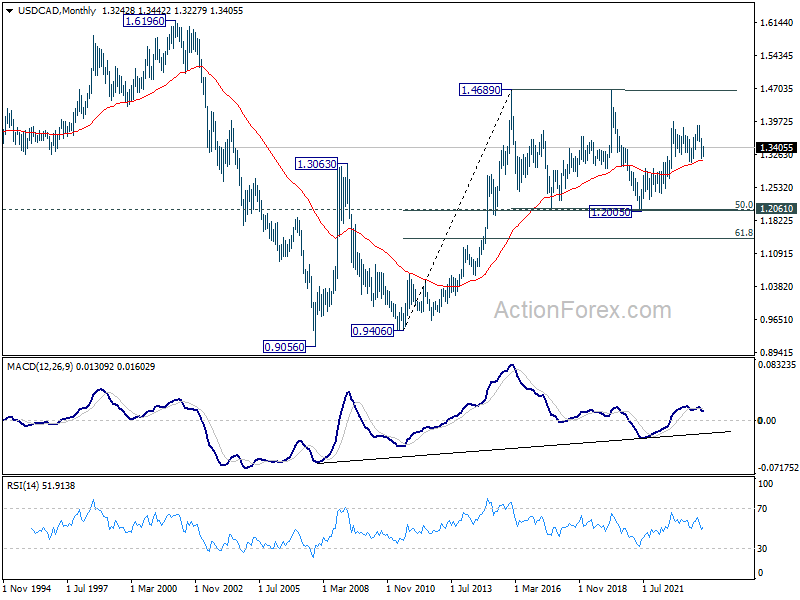

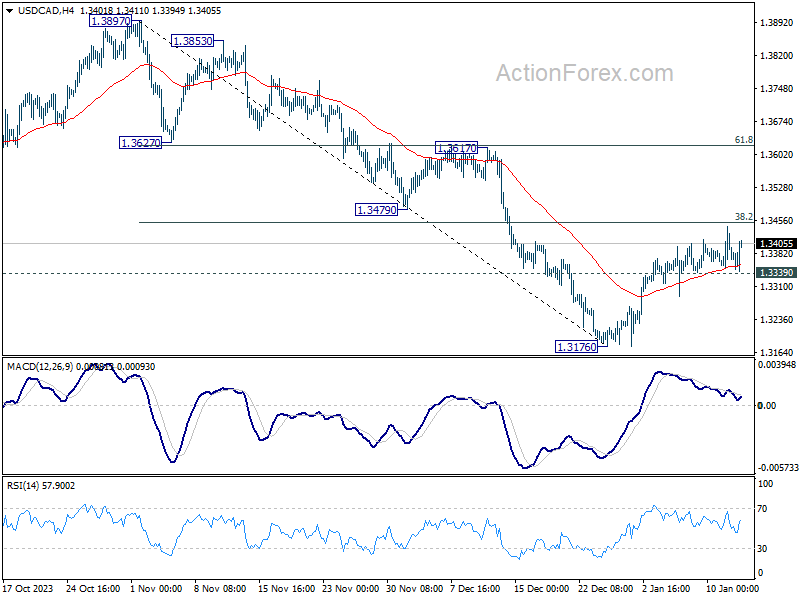

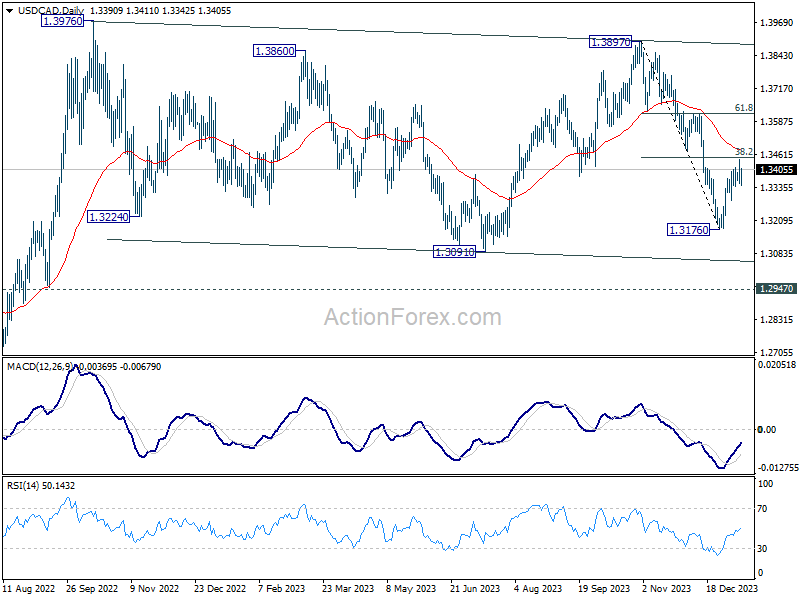

USD/CAD Weekly Outlook

USD/CAD's rebound from 1.3176 short term bottom extended higher last week but lost momentum ahead of 38.2% retracement of 1.3897 to 1.3176 at 1.3451. Initial bias is turned neutral this week first. Further rise is mildly in favor as long as 1.3339 minor support holds. Decisive break of 1.3451 will pave the way to 61.8% retracement at 1.3622. On the downside, however, break of 1.3339 will turn bias back to the downside for 1.3176 low instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. While fall from 1.3897 could still extend through 1.3091, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.