Sample Category Title

Global Implications of a Soft U.S. Landing

Summary

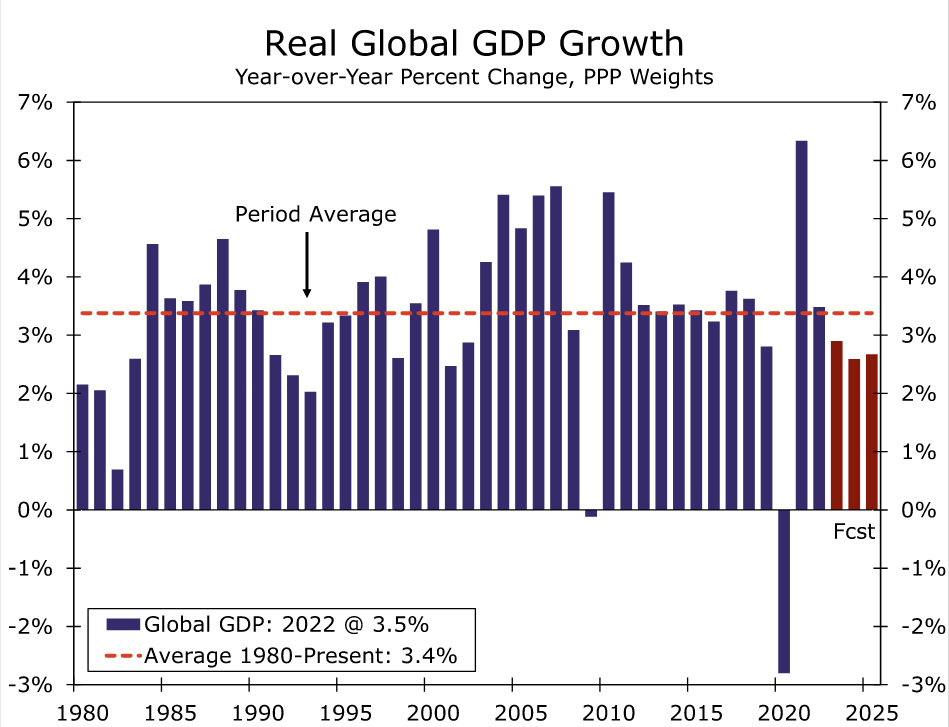

The continued resilience in U.S. activity has prompted a significant shift in our outlook for the U.S. economy. Our U.S. economics colleagues now believe the U.S. economy will avoid recession, achieve a “soft landing”, and experience continued expansion through 2025. This more resilient outlook for U.S. growth has implications for our global economic outlook. Stronger U.S. growth should allow the Eurozone and United Kingdom to recover more quickly from recession conditions, and given extensive trade linkages, should also offer support to activity in Canada and Mexico. Overall, we now see a more mild slowdown in global GDP growth from 2.9% in 2023 to 2.6% in 2024. Amid a firmer global growth backdrop, we also believe select central banks will adopt a more gradual approach to lowering interest rates. For the European Central Bank, Bank of England, Bank of Canada and Bank of Mexico, we expect rate cuts to now proceed at a more measured pace, with policy interest rates not leveling out until the second half of 2025.

U.S. Resilience to Cushion the Global Economic Slowdown

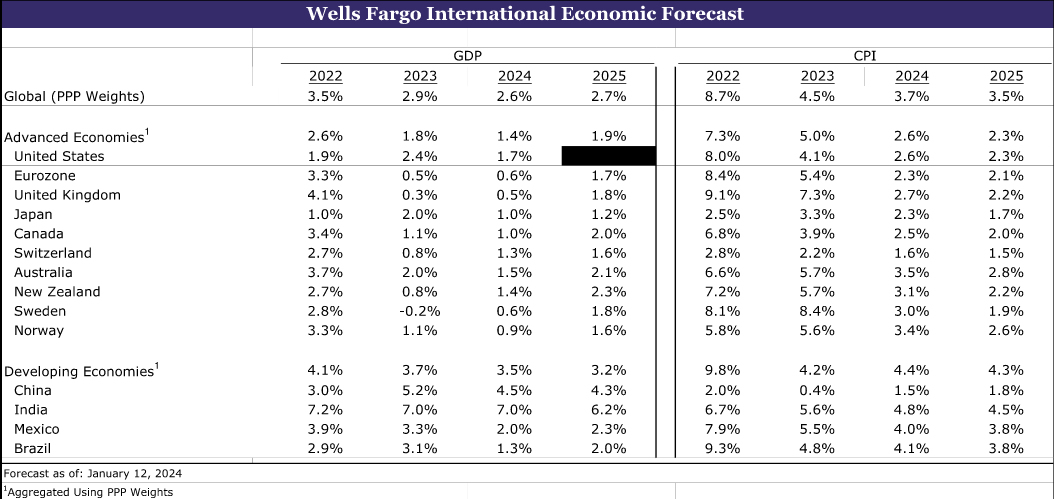

The continued resilience in U.S. activity has prompted a significant shift in our outlook for the U.S. economy. Even amid an aggressive monetary tightening campaign that saw the Fed's policy rate increase by a cumulative 525 bps over the past couple of years, ongoing employment gains and a sharp deceleration in inflation have seen real household disposable income growth return to positive territory. Expectations of Fed monetary easing and a relaxation of financial conditions are also exerting less restraint on activity and the U.S. economy. As a result, while still acknowledging that risk of a downturn exists, we now believe the most likely outcome is for the U.S. economy to continue growing through the end of 2025 and achieve the hoped for “soft landing.” We now forecast U.S. GDP growth of 1.7% for calendar 2024 (previously 0.9%) and 1.7% for calendar 2025 (previously 1.5%).

This more-resilient outlook for U.S. growth has implications for our global economic outlook. To be sure, Europe's economic environment will likely remain challenging for the time being. For key economies such as the Eurozone and United Kingdom, the previous spike in inflation and subsequent central bank monetary policy tightening means we still believe those economies experienced mild technical recessions during the second half of 2023. Still, with U.S. activity helping underpin global demand, we believe the Eurozone and United Kingdom economies can recover more quickly in 2024. While still far from robust, we have revised our 2024 GDP growth forecasts modestly higher to 0.6% for the Eurozone and 0.5% for the United Kingdom. For Canada and Mexico, both economies have very significant trade linkages with the United States. The U.S. represents the end destination for 70% or more of overall merchandise exports from both countries. As a result, a firmer outlook for the U.S. should also mean better growth prospects in Canada and Mexico, prompting us to lift our 2024 GDP growth forecasts for Canada and Mexico to 1.0% and 2.0% respectively. However, not all countries will necessarily benefit from more resilient U.S. economic trends. In China, for example, we believe structural headwinds such as a declining working age population and a highly leveraged property sector will continue to restrain overall economic growth. Despite a U.S. soft landing, we have maintained our China GDP growth forecast for 2024 at 4.5%.

Altogether, a U.S. soft landing should moderate the extent of the global economic slowdown this year. We now forecast a milder global economic slowdown and believe the global economy can experience growth of 2.6% in 2024 relative to our previous forecast of 2.4% (Figure 1).

More Gradual Monetary Policy Easing From Major Central Banks

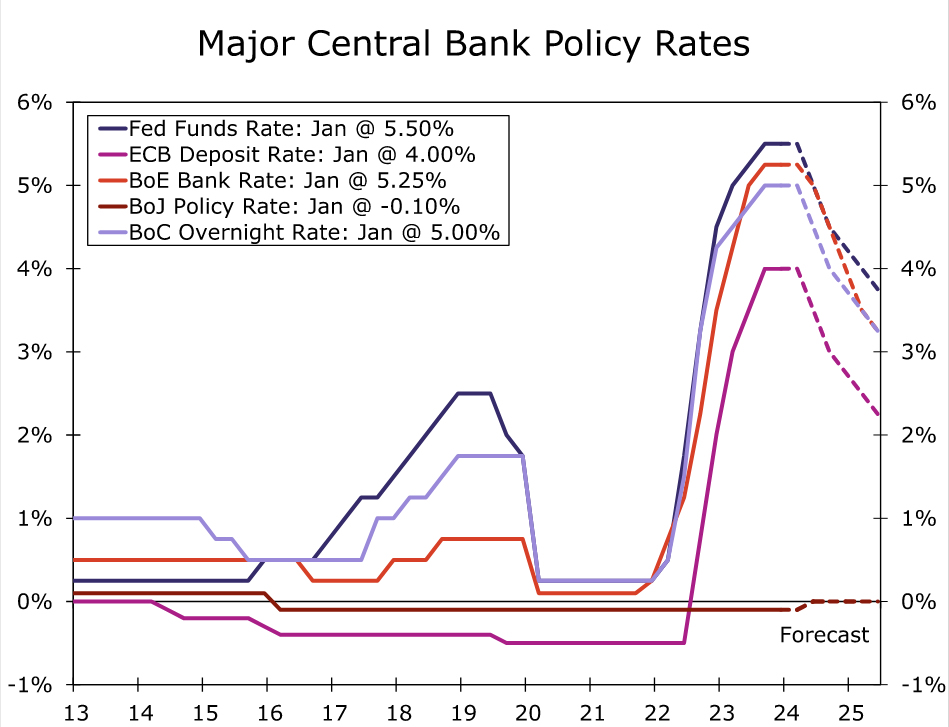

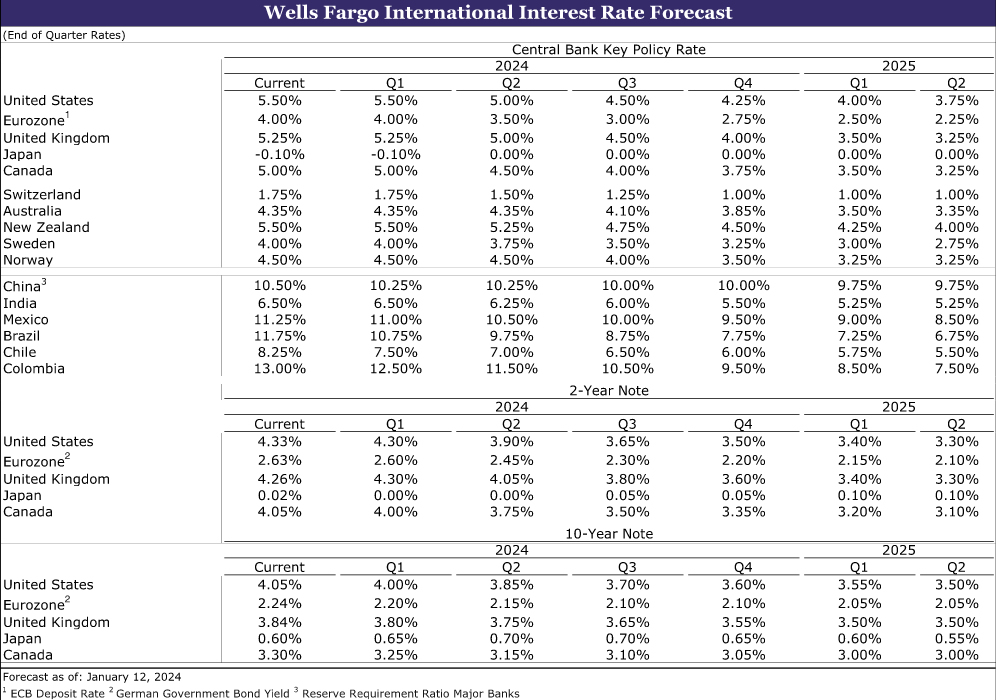

Amid a backdrop of firmer growth prospects, we also believe key central banks will adopt a more gradual approach to lowering interest rates. In the case of the Federal Reserve, we forecast the FOMC will cut rates by 125 bps by the end of 2024, commencing with a 25 bps reduction at the May meeting. That cumulative rate decline in 2024 is less than we forecast last month. A gradual and steady approach from the Federal Reserve means monetary easing will likely continue through much of the following year as well. Altogether, we look for a total of 225 bps of Fed rate cuts, which would put the target for the fed funds rate at 3.00%-3.25% by the end of 2025 (Figure 2).

For the European Central Bank (ECB), we still expect soft growth and an improving inflation outlook will see the ECB deliver an initial rate cut in April, initially proceeding at a 25 bps per meeting clip. As Eurozone growth recovers, we expect the ECB to downshift to 25 bps per quarter from Q4-2024, and not reach a terminal policy rate of 2.00% until the second half of 2025. For the United Kingdom, with inflation still elevated, we forecast Bank of England (BoE) rate cuts to begin slightly later than the ECB, at the BoE's June meeting. Given a moderately stronger U.K. growth outlook, we no longer see an accelerated pace of BoE rate cuts, but rather anticipate rate cuts continuing at a steady 25 bps per meeting clip until well into 2025. Given this backdrop, we do not see the Bank of England's policy rate reaching 3.00% until the second half of next year. Turning to Canada, given the progress to date in reducing inflation, we forecast the Bank of Canada (BoC) to deliver an initial rate cut in April and proceed at a 25 bps per meeting pace. However, with steadier Canadian growth, we see the Bank of Canada slowing to 25 bps per quarter from Q4-2024 and not reaching a terminal policy rate of 3.00% until the second half of 2025. Finally, we still forecast an initial Bank of Mexico rate cut in March, but expect Mexico's central bank to proceed only in 25 bps rate cut increments thereafter. To that point, Banxico policymakers will not reach a policy rate of 8.25% until the second half of next year.

A U.S soft landing also has implications for our 2024 U.S. dollar outlook. As of now, we still anticipate depreciation in the U.S. dollar in 2024 as the Federal Reserve lowers interest rates. In addition, we believe a relatively more optimistic global growth outlook can potentially lead to a loss of “safe-haven” support for the greenback. Lower interest rates and lesser demand for the "safe-haven" characteristics of the U.S. dollar can lead to broad-based greenback depreciation against both G10 and EM currencies this year. However, given a firmer outlook for U.S. economic growth and a slower pace of Fed easing than previously envisaged, the magnitude of U.S. dollar depreciation could be less than we previously expected. We will provide a full set of FX forecasts in our January International Economic Outlook, but given our revised view on the U.S. and global growth outlook, as well as evolving views on monetary policy in key economies, the dollar could also experience a “soft landing” of its own.

Global Forecast Tables

Weekly Focus – Taiwan Election Key for Geopolitical Tensions

The main release this week was US inflation, which surprised slightly to the upside with core inflation coming in at 3.9% y/y (consensus 3.8% y/y) as service inflation is still proving sticky. It contrasts with the signals in the euro area where we have seen a clearer decline in core inflation, see Global Inflation Watch - diverging signals in December. Recently, a rise in freight rates poses moderate upside risks to goods price inflation. An airstrike on Houthi rebels in Yemen by the US and UK on Friday marked an escalation of the situation in the Middle East and a risk of further widening of the conflict in the region.

German industrial production (IP) dropped 0.7% in November, the seventh monthly decline, highlighting the strong underperformance of German industry this year. French IP increased 0.5% m/m in November. Despite the manufacturing woes, euro area unemployment declined to a new record low in November, at 6.4%, illustrating a still very tight labour market. EU sentiment data showed a rise in service confidence, and decent activity in the service sector partly explains the robust labour market. It also puts the ECB in a dilemma, as inflation momentum is broadly in line with its 2% target but tight labour markets and high wage growth make it too early to declare victory on inflation.

Despite a US inflation print on the high side US bond yields declined this week whereas German yields increased. Stock markets regained some positive momentum after the small setback in the first week of 2024. EUR/USD moved broadly sideways at just below 1.10.

EU-China trade tensions continue to simmer as China this week started an anti-dumping investigation on EU brandy. It looks like retaliation for the EU's anti-subsidy investigation on Chinese EVs and an attempt to temper EU restrictions on China.

Over the weekend, focus will turn to the Taiwan election on Saturday with the election of a new President as well as the parliament (Legislative Yuan). Polls are not allowed 10 days before the election but the most recent surveys show a tight margin between the ruling party DPP's Lai Ching-te (36%) and KMT's Hou Yu-ih (31%). A victory for Lai would point to more of the same, with an independence-leaning stance, whereas a victory by Hou could ease tensions in the Taiwan Strait, as KMT has a less confrontational stance towards Beijing. However, even if Lai wins, China-Taiwan tensions might ease, as Lai will have a weaker mandate to confront China than the current president Tsai Ing-wen, who got support from close to 60% of the voters in 2020. DPP will likely also lose its majority in the Taiwanese parliament, as a fairly new Party, Taiwan's People's Party (TPP), and its leading candidate, Ko Wen-je, have close to 25% support in the polls.

In the US, politics will also be in focus next week as the US election year kicks off Monday with the Iowa Republican Caucuses. Prediction markets see Trump as the clear favourite to win the Republican candidacy, and he is projected to win over half of all votes in Iowa according to the latest polls. The Iowa caucuses are often seen as a bellwether of the rest of the spring, and either of Trump's closest challengers, Ron DeSantis or Nikki Haley, would likely have to come out as a close runner-up to maintain their hopes of clinching victory in the end. On the economic front, US retail sales and Chinese GDP for Q4 23 will be in the spotlight. China will also release home sales for December, a key gauge of the state of the housing crisis which so far has shown no signs of bottoming. On inflation, Japan will take centre stage on Friday with the December CPI print.

Will the UK Inflation Data Pour Cold Water on BoE Rate Cut Bets?

- BoE highlights “higher for longer” message in December

- Yet, investors are penciling in aggressive rate reductions

- CPI inflation data for December could well impact that view

- The numbers are scheduled for Wednesday at 07:00 GMT

Investors don’t pay attention to BoE’s signals

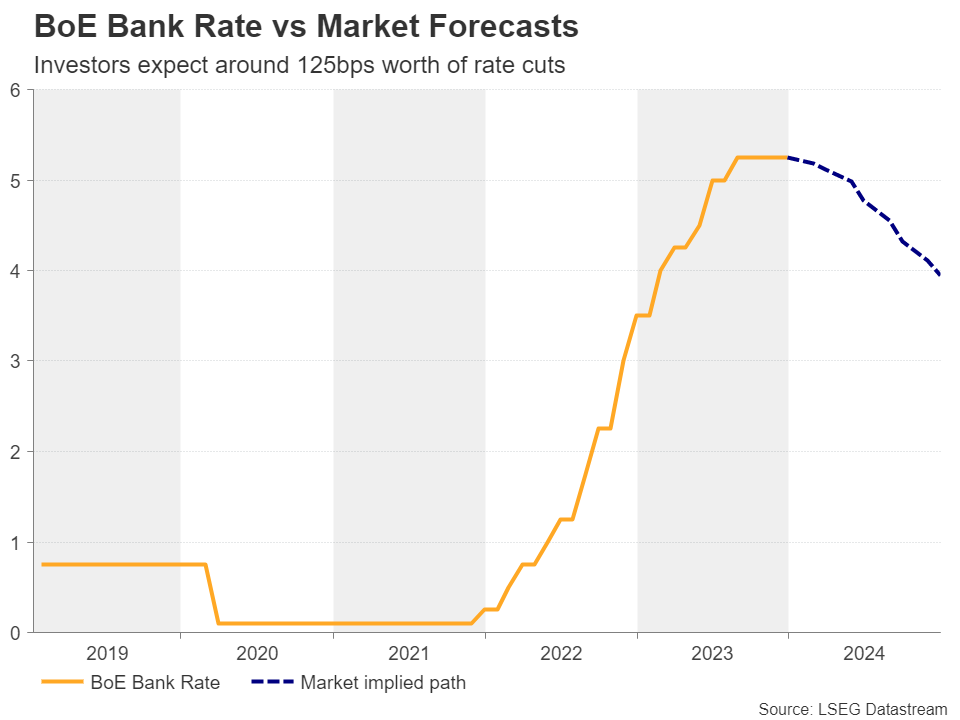

At its December policy gathering, the Bank of England kept interest rates unchanged via a 6-3 vote, with the three dissenters preferring to increase the Bank rate by another 25bps to 5.5%. In the accompanying statement it was noted that policy “will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term,” with Governor Bailey highlighting that view at the press conference following the decision.

Yet, investors are penciling in around 125bps worth of rate reductions for this year, assigning an 80% probability for the first quarter-point reduction to be delivered in May. Perhaps they were concerned about the state of the UK economy after the quarterly GDP rate for Q3 was revised down to -0.1% and the October monthly print revealed a contraction of -0.3%, thereby ringing the recession alarm bells.

That said, even with the November data pointing to a 0.3% m/m rebound and the NIESR tracker forecasting GDP to remain flat in the fourth quarter, in other words avoiding a recession, investors stubbornly are maintaining their rate cut bets. Perhaps they believe that the BoE may be forced to agree with them after the Oxford Economics consultancy and analysts at Investec and Deutsche Bank forecasted that UK inflation will fall below 2% by April. The BoE’s November projections suggested that CPI inflation will return to the target by the end of 2025.

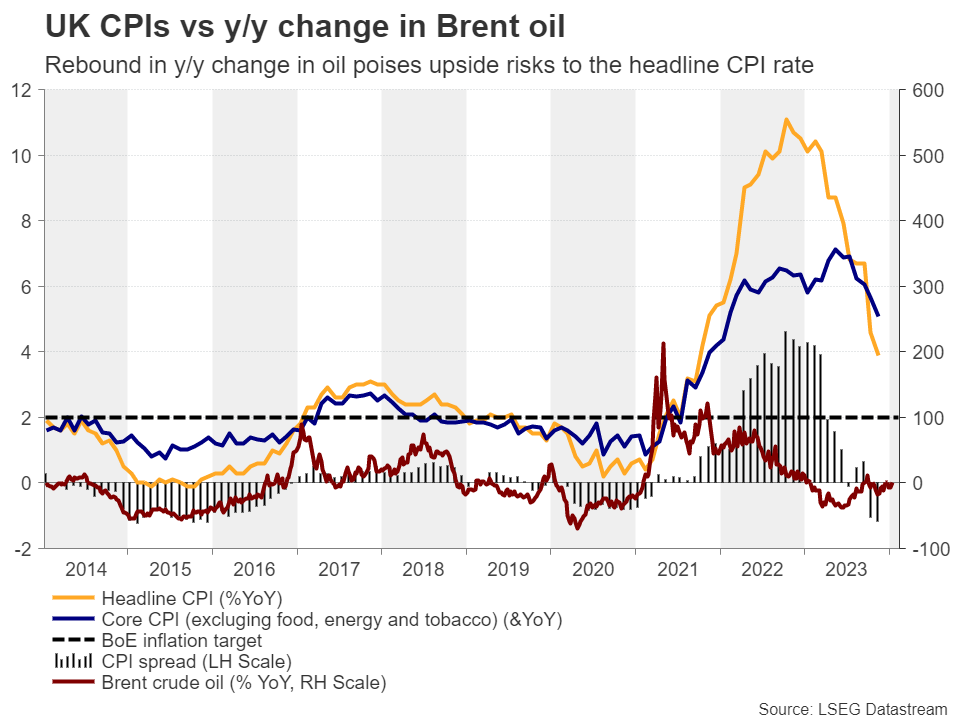

Upside risks surround December CPI data

With all that in mind, pound traders may now lock their gaze on next week’s CPI numbers for December, due out on Wednesday. The employment report for November, due out the previous day, may also attract attention as average weekly earnings could provide a glimpse of where inflation may be headed in the months to come. The UK retail sales are scheduled to be released on Friday.

Although the manufacturing PMI showed that selling prices rose only slightly in December, the services survey revealed that input cost inflation accelerated to a three-month high, contributing to the fastest rise in prices charged since July. With the service sector accounting for around 80% of the total UK economic output, there are risks of a reacceleration in Wednesday’s data. And if the core CPI rate rebounds, the headline rate may rise by more as the 2022 downtrend in oil prices is dropped out of the y/y calculation, pushing the yearly change of oil from negative close to zero.

Will the pound extend its prevailing uptrend?

Combined with signs that the UK economy may have once again dodged a recession, accelerating inflation may eventually convince market participants to push back their BoE rate cut bets, thereby allowing the pound to extend its latest recovery and perhaps its prevailing near-term uptrend.

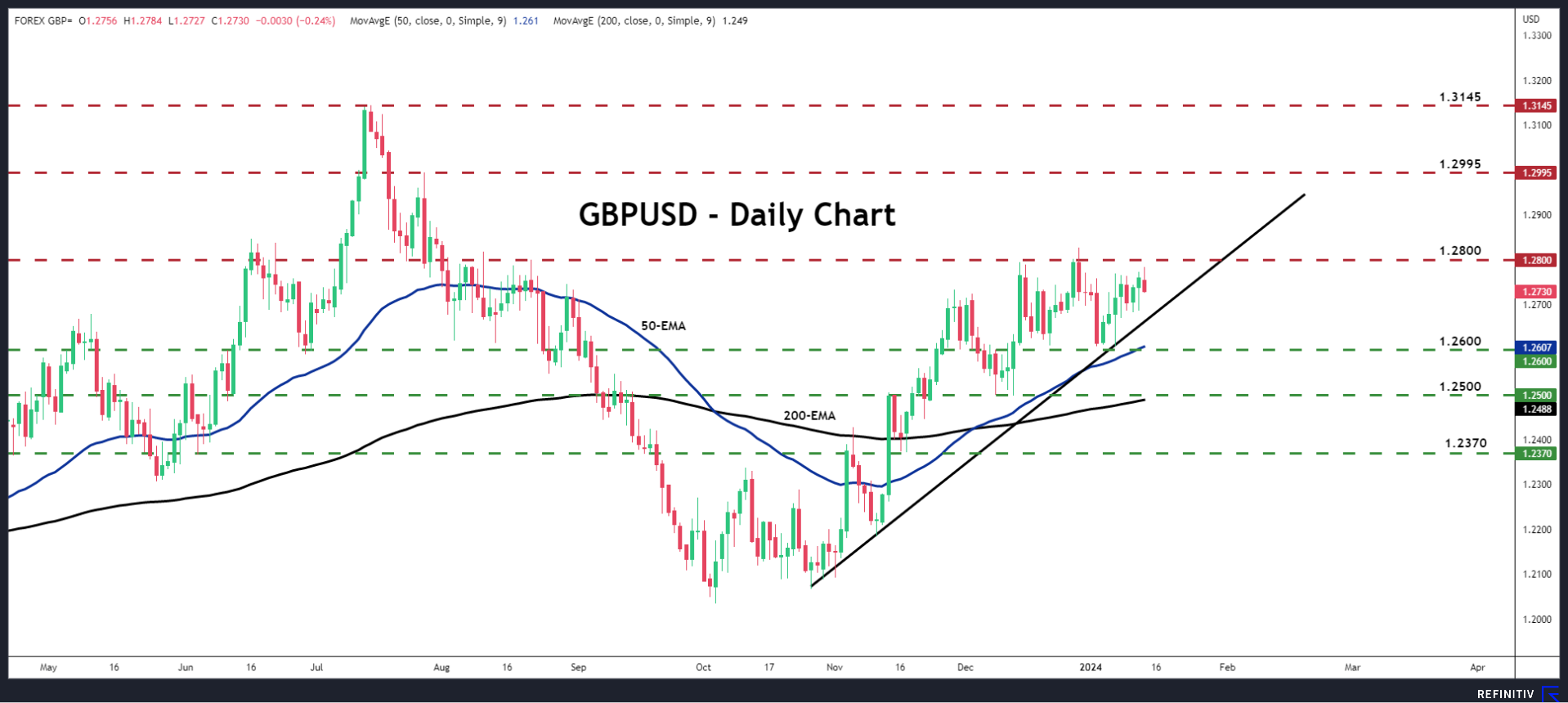

From a technical standpoint, pound/dollar has been in a recovery mode since January 3, with the pair remaining above the uptrend line drawn from the low of November 1, as well as above both the 50- and 200-day exponential moving averages.

Accelerating UK inflation may push the pair higher, with a clear close above the key resistance zone of 1.2800 signaling the resumption of the prevailing uptrend. Such a break may encourage the bulls to climb all the way up to the peak of July 27 at 1.2995.

Now, in case the CPI figures miss their estimates, the pair may slide and even fall below the aforementioned uptrend line, but for a near-term reversal to start being discussed, a fall below 1.2600 may be needed.

Week Ahead – China GDP and UK December CPI Reports Eyed Amid Rate Cut Frenzy

- China reports Q4 GDP data on Wednesday; is a rebound in store?

- CPI numbers due in UK, Japan and Canada

- Retail sales to be the main focus in the US

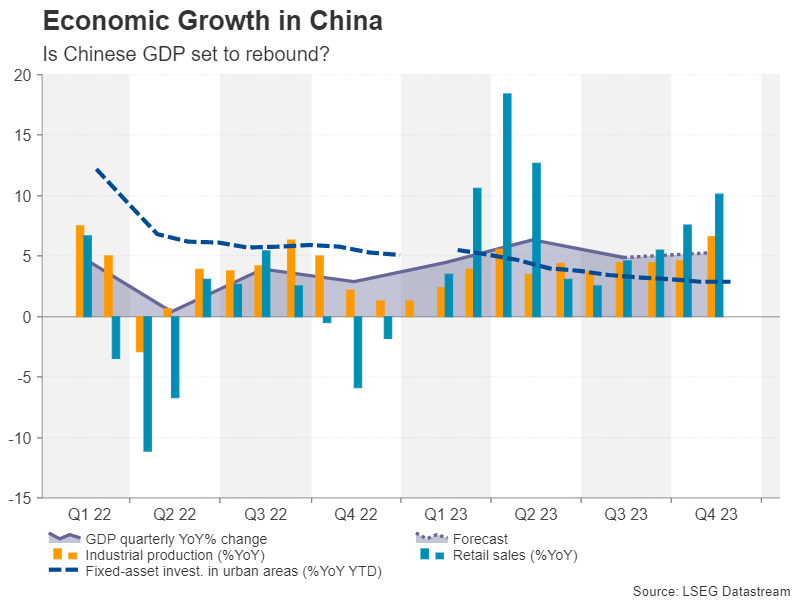

Is China’s recovery getting back on track?

The Chinese economy suffered several wobbles in 2023, as the property crisis went from bad to worse. Markets held their breath for a major stimulus announcement, but with one eye on deleveraging, authorities’ response only went as far as offering targeted drip-feed measures, leaving investors flabbergasted and disappointed.

However, the government’s efforts may not have been totally in vain as Chinese consumers have been spending more since the summer and industrial production has also been rebounding. The property sector remains a significant risk but there are signs that the market is stabilizing. Hence, GDP growth likely quickened in the final quarter of 2023 to 5.3% y/y after slowing to 4.9% y/y in the third quarter. A Q4 reading of slightly above 5.0% y/y would ensure that the government meets its growth target of around 5.0% for the full year.

The GDP data will be released on Wednesday alongside the monthly prints on industrial output, retail sales and fixed asset investment.

Global equities as well as the Australian dollar, which is considered a liquid proxy for the China risks, could gain on the back of stronger-than-expected growth in the world’s second largest economy.

Australian jobs data will also be key for the aussie

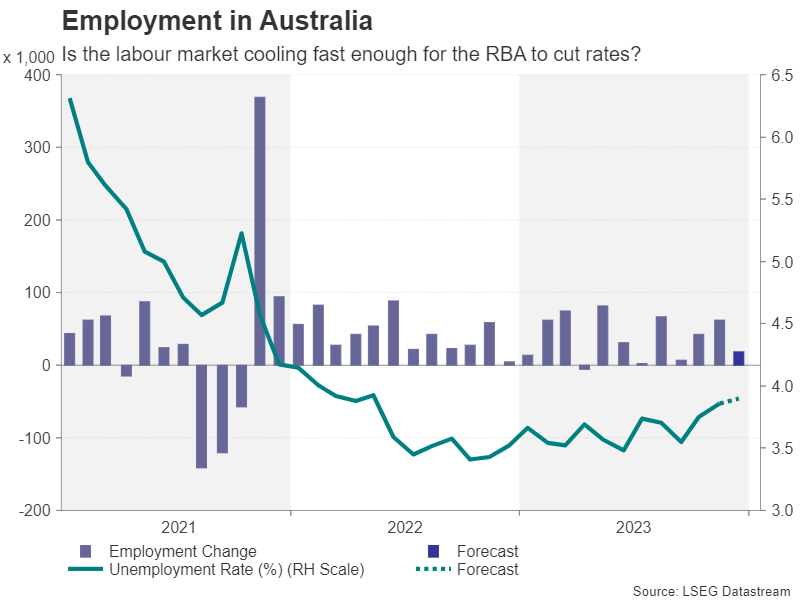

However, China’s economic performance will not be the only thing on the aussie traders’ minds as Australian employment numbers are due on Thursday. Australia’s labour market has cooled off slightly in recent months, with the unemployment rate inching up to 3.9%.

If the employment report points to further weakness in December, investors will likely up their bets of expected rate cuts by the Reserve Bank of Australia in 2024. At the moment, the RBA is seen to be the least dovish among the major central banks – something that contributed to the local dollar’s revival last autumn.

But if those bets are scaled back, the aussie could struggle against its US counterpart, especially if optimism about China remains in short supply.

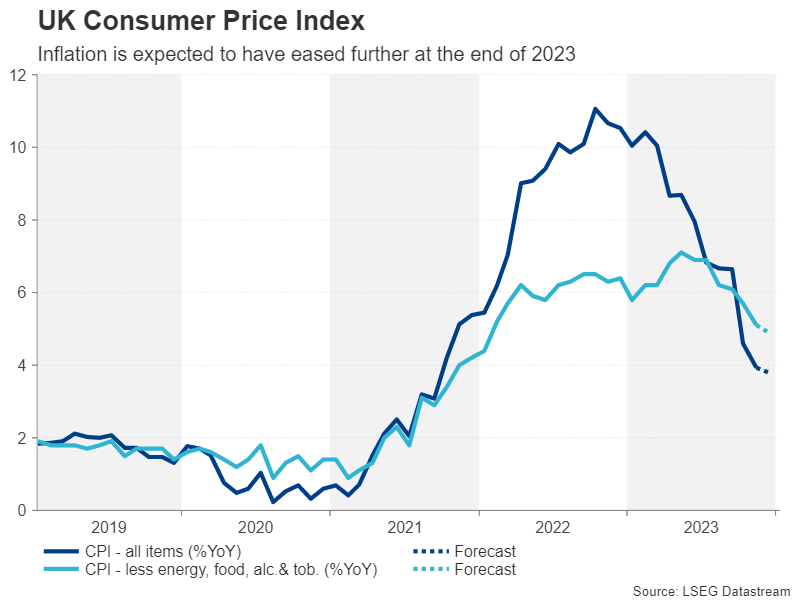

CPI to headline busy data week for the pound

Another currency that’s been supported by expectations of fewer rate cuts than other central banks is the British pound. Although the Bank of England is predicted to slash rates by at least 100 basis points, the ECB and Fed are expected to cut even more aggressively.

As in Australia, inflation in the UK has taken longer to come down from the 2022 highs, but there’s been a marked improvement in this trend in the last couple of reports. The headline rate of CPI in the UK fell to 3.9% y/y in November and is forecast to have cooled marginally to 3.8% y/y in December.

Core CPI will also be watched on Wednesday as it remains above 5.0%, while a day earlier, UK jobs and wage numbers are due for November.

Retail sales figures for December will round up the week for sterling on Friday. The pound has been consolidating after briefly flirting with the $1.28 level in December. If inflation continues to surprise to the downside, cable’s uptrend will likely come under question. However, the retail sales stats will be important too as an upbeat set of numbers would ease concerns of the UK economy entering a technical recession at the end of 2023.

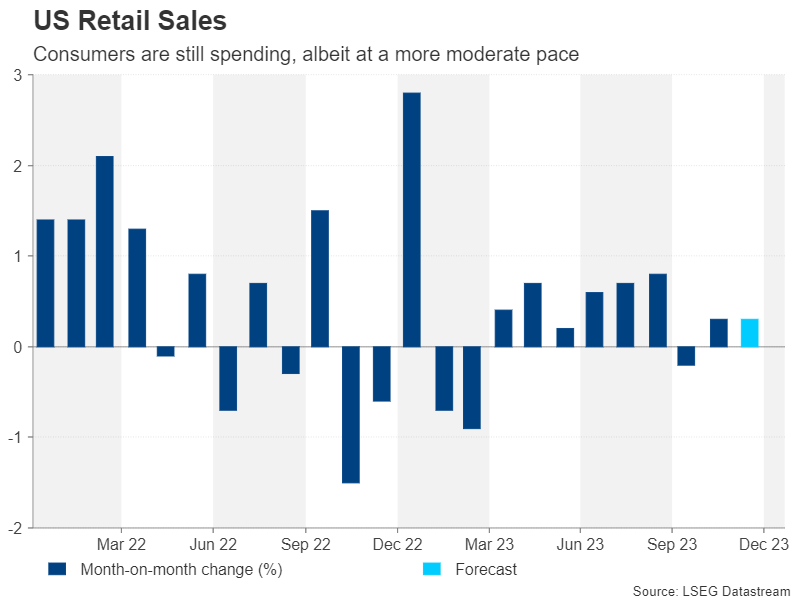

Fed rate cut bets face more tests

Retail sales will also be the highlight in the United States, with the remaining releases being mostly second-tier data. Whilst US consumer spending has slowed after the summer surge, it isn’t about to fall off a cliff either. Retail sales grew by 0.3% m/m in November and the December readings due on Wednesday are expected to show a similar pace for the month.

Industrial production figures are out on Wednesday too, while on Thursday, building permits and housing starts for December might attract some attention. Existing home sales will follow on Friday.

Regional Fed surveys will shed some light on the manufacturing sector on Monday (New York Fed) and Thursday (Philly Fed), and finally on Friday, investors will be monitoring the University of Michigan’s vital consumer sentiment survey.

With markets betting so heavily for around 150 basis points of rate cuts by December 2024, a broadly solid set of indicators could spark some repricing in Fed fund futures, potentially pushing up Treasury yields and in turn, the US dollar.

Loonie to take cues from Canadian CPI

The Canadian dollar staged an impressive rebound at the end of 2023, even though oil prices retreated during this period. Much of the loonie’s gains were driven by the broader pullback in the US dollar, as well as the improvement in risk appetite.

The focus in the coming week will switch back to the domestic economy as the latest consumer price index is due on Tuesday. Canada’s CPI rate stood unchanged at 3.1% y/y in November, which is a worsening from the 2.8% figure recorded back in June, signalling a stalling of the progress in getting inflation all the way down to the Bank of Canada’s 2% target midpoint.

On the bright side, underlying measures of inflation have continued to decline, so any further drop in the core figures could offset an unexpectedly hot headline number.

The loonie could recoup its slight year-to-date losses against the greenback if CPI heads in the wrong direction again. But for the currency to be able to resume its medium-term uptrend, this will depend more on how Fed expectations and oil prices evolve in the coming weeks.

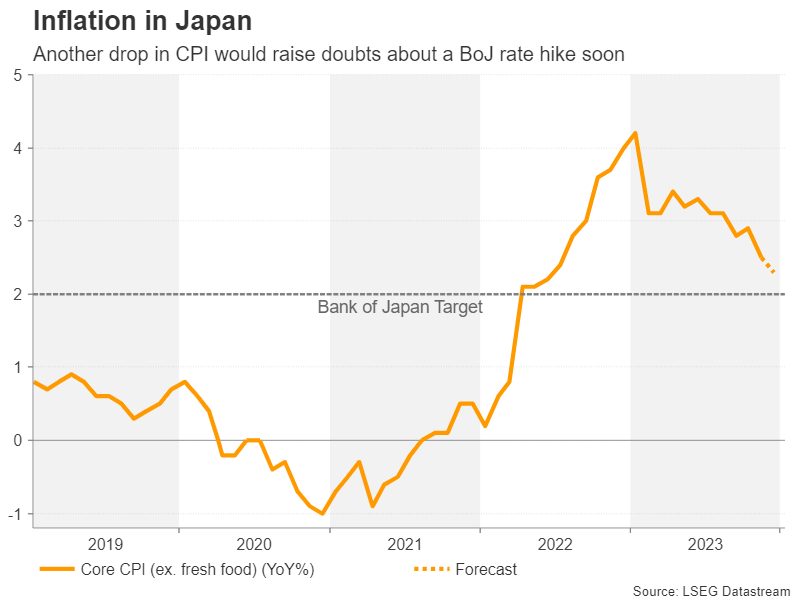

Can Japanese CPI put the yen on the front foot?

The Japanese yen hasn’t had a very good start to 2024, as expectations of an imminent policy shift by the Bank of Japan dwindled after the earthquake that struck the country on New Year’s Day.

There could be a further setback for the yen on Friday as CPI is projected to have eased from 2.5% to 2.3% y/y in December. Although it’s unlikely that inflation in Japan will reaccelerate much over the next few months, as long as it holds above 2%, that would be enough for the BoJ to call time on negative interest rates. But for that to happen, policymakers will want to see stronger wage growth, which will only become evident after the spring wage negotiations.

For now, the yen will probably not react much to the December CPI data and at best, the incoming data can only provide some support. The other releases next week include corporate goods prices on Tuesday and machinery orders on Thursday.

Sunset Market Commentary

Markets

The US/UK air strikes against Houthi targets in Yemen retaliating for shipping attacks in the Red Sea dominated media, but their market impact remained rather limited for now. The biggest move came on the oil market with Brent crude rising from $77/b before the first strikes to as high as $80.5/b. Traditional risk-related mechanisms weren’t at play. Correlation trades via distorted supply chains or potential inflationary effects neither. German Bunds gapped open higher but that was mainly catching up with US Treasuries’ performance yesterday. Failure to push the front end of the US yield curve higher after above-consensus CPI yesterday eventually triggered rebound action lower. The move accelerated with the front end of the curve outperforming following US December PPI figures. They fell by 0.1% M/M in December (vs +0.1% M/M expected) with core PPI flat (vs +0.2% M/M consensus). Both headline PPI (+1% Y/Y) and core PPI (+1.8% Y/Y) were lower than forecast. US yields lose up to 10 bps at the front end of the curve with the long end down <2 bps. German yields fall between 10 bps (2-yr) and 4.2 bps (30-yr). The new bond rally is quite surprising given that central bankers are pushing back against premature rate cuts by central banks and with inflation proving to be a little more sticky. EUR/USD fell from the 1.0980 area towards 1.0940 ahead of the PPI release. Afterwards, the pair returned again towards opening levels but a test of the psychologic 1.10 area doesn’t seem to be in the cards ahead of the US long weekend. The Japanese yen profits from core bond yields falling, erasing early losses on rumours that the BoJ in January will cut its inflation outlook for next year. Markets are closed on Monday for Martin Luther King Day. Stock markets initially doubted because of rising tensions in the Middle East but eventually got lifted by the bond rally. Key European indices gain up to 1%. US stock markets open less enthusiastic with 0.5% gains.

Next week’s eco calendar contains US retail sales and January Michigan consumer confidence. Key UK data are on tap with labour market figures and CPI inflation. The Q4 earnings seasons gets going with a lot of media attention going to the World Economic Forum in Davos. ECB Lagarde is one of the prominent guests and speakers. News & Views

Hungarian inflation retreated sharply in December, from 7.9% to 5.5% thanks to a monthly drop of 0.3%. Expectations were for a slower decline by -0.2% m/m to 5.9%. Electricity, gas and other fuels continued to depress price pressures, both y/y (-13.9%) and m/m (-1.1%). Food prices still rose 4.8% y/y but fell on a monthly basis (-0.1%). Core CPI extended its decline as well. A 0.3% m/m advance resulted in a y/y figure of 7.6%, down from 9.1%. For the whole of 2023, inflation amounted to 17.6% on average compared to 2022. The sharpest increase came on the account of food (25.9%). A price rise of 22.1% was recorded for electricity, gas and other fuels, 18.6% for other goods, including motor fuels and lubricants, 15.4% for alcoholic beverages and tobacco, 13.2% for services, 8.3% for clothing and footwear and 5.6% for consumer durables. Today’s outcome brings the real central bank policy rate further into positive territory (>5%), straining the economy much to the frustration of president Orban and economy minister Nagy. It increases risks for a bigger rate cut by the central bank when it meets January 30. The MNB already discussed the option to step up the pace in December from 75 bps to 100 bps before sticking to the former. Hungarian swap yields drop but it’s the long end that’s greatly outperforming. Changes vary between -6.7 bps (2-y) and -30.8 bps (20-y). The Hungarian forint temporarily dipped before trading unchanged on the day again around EUR/HUF 379.1.

Germany’s statistics office said many companies in the country slid into insolvency at the end of last year. The amount of insolvencies filed in rose by 12.3% in December compared to the same period a year before. The statistics office said they had been recording double digit growth rates in the number since June 2023 and expect the figures to continue to rise in coming months. A weak economy and high interest rates were mentioned as the key reasons.

USD/CAD – Technical Analysis Forecast

- Canada CPI and BOC Overnight Rate schedule

- Technical Analysis for Monthly, Daily, and 4-hour charts

The Canadian Dollar opened 2024 with a decline against the US Dollar, the Forex pair USD/CAD rose from 1.3180 in late December 2023 to its current average price of 1.3380 and has been trading near this level for a few days. The pair held steady throughout the US CPI data release as well as the recent upside move in oil prices. Next week, markets are looking forward to December’s 2023 CPI data from Canada, the previous median CPI y/y was 3.4%, and the m/m was 0.1%. Traders will be watching the CPI data closely as the release is scheduled ahead of the Bank of Canada Monetary Policy Report, Overnight Rate, and Rate Statement scheduled on the morning of January 24th, 2024 local time. It is also important to bear in mind the potential risks that may arise due to the recent developments in the Middle East and its potential impact on Oil Prices.

Monthly Chart

- Price action continues to trade within its long-term trading range established in 2015, price is currently at mid-range (Rectangular area), however, price action is still finding support above the ascending trendline established in mid-2021. (Blue line)

- Negative divergence between price action and RSI indicator (Red lines), price action made higher highs while RSI plotted a lower high for the same move. Although RSI is moving towards its oversold territory, it remains near the indicator’s neutral level.

- Price action continues to trade below its EMA9 which intersects with the annual pivot point of 1.3410, price attempted to break above this level in January but has been unsuccessful so far. On the other hand, price action remains above its SMA50 which intersects with the ascending blue trendline.

Daily Chart

- Price is trading below its SMA 50 and SMA 200, however, it recently found support above its EMA9 and has been trading above its monthly pivot point of 1.3350 for a few days so far.

- RSI is within its overbought level, inline with recent price action, while MACD line crossed above its signal line.

4-Hour Chart

- Price was trading within a descending channel and currently appears to be attempting to complete a rising wedge formation. If price action breaks below and continues to trade below the wedge pattern, it can be considered a continuation pattern for the descending channel.

- The same wedge pattern is also accompanied by a negative divergence on RSI.

- The MACD line is reflecting a negative divergence and the MACD line just crossed below the signal line

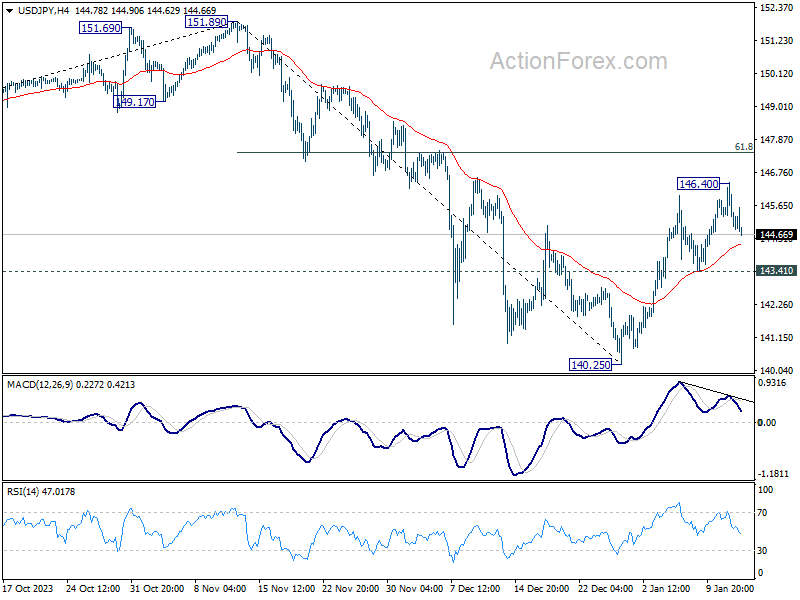

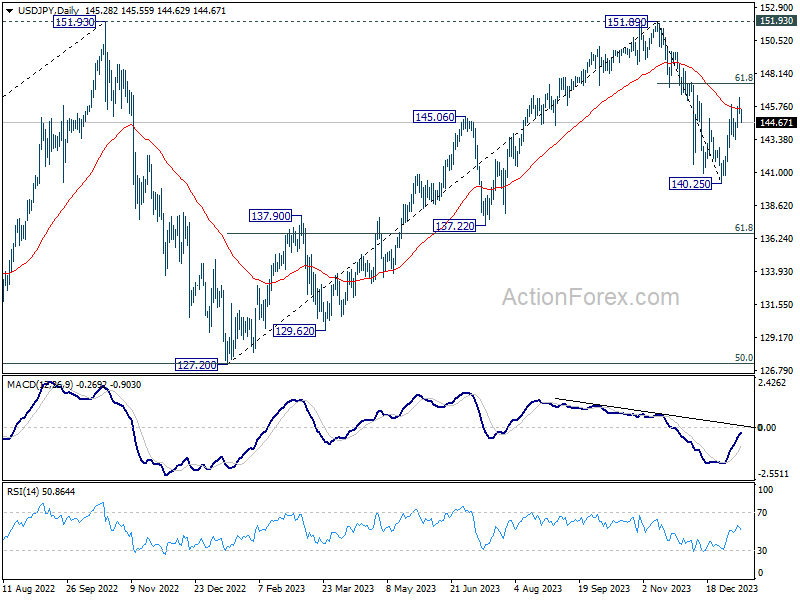

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.81; (P) 145.61; (R1) 146.08; More...

Intraday bias in USD/JPY remains neutral at this point. On the upside above 146.40 will resume the rebound from 140.25 to 61.8% retracement of 151.89 to 140.25 at 147.44. Upside should be limited there to bring reversal. On the downside, break of 143.41 will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

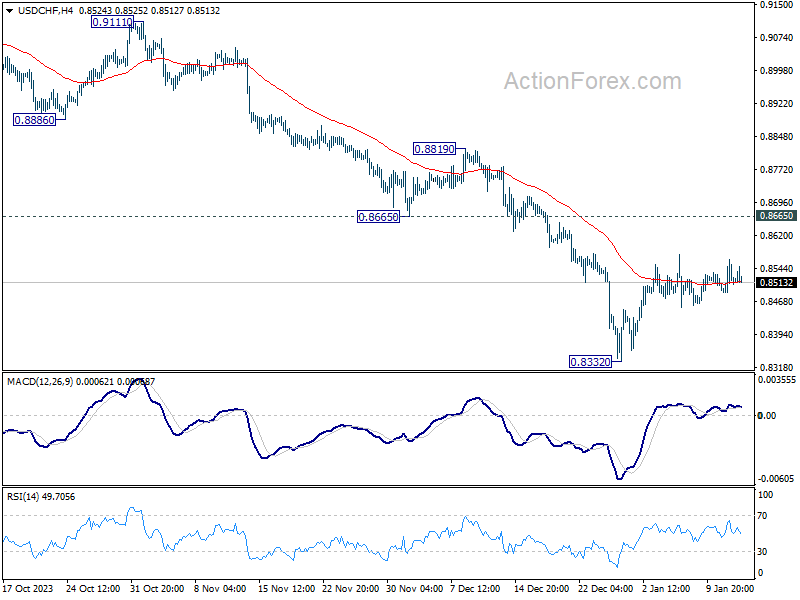

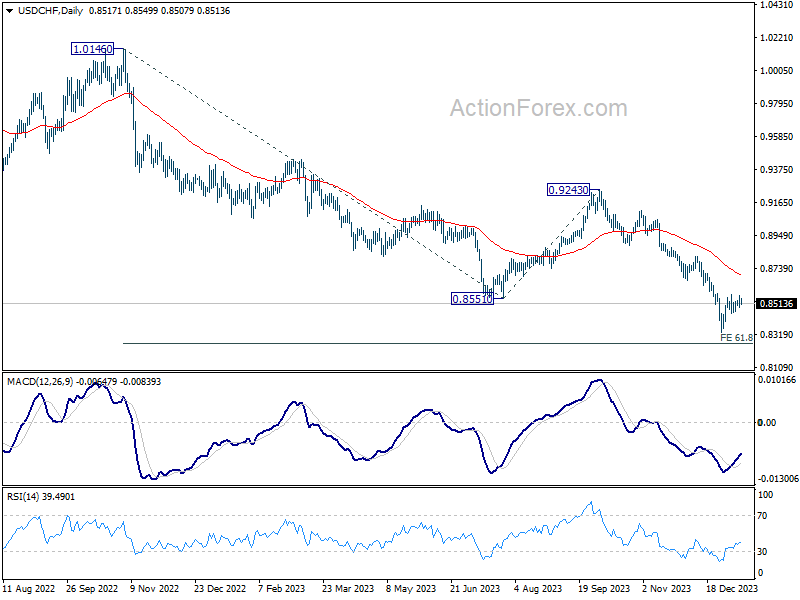

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8498; (P) 0.8518; (R1) 0.8528; More....

Intraday bias in USD/CHF stays neutral for the moment. Consolidation from 0.8332 is extending and stronger recovery cannot be ruled out. But outlook will stay bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, the down trend from 1.0146 (2022 high) is in progress. Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

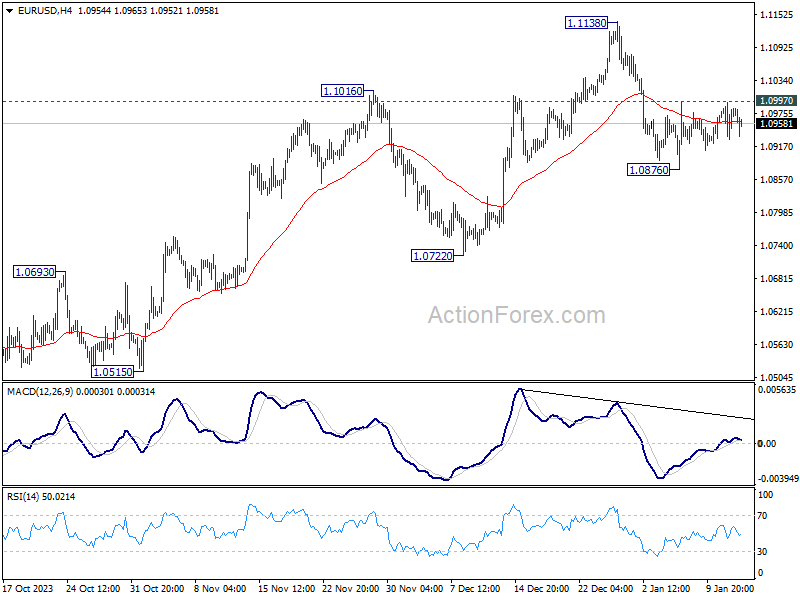

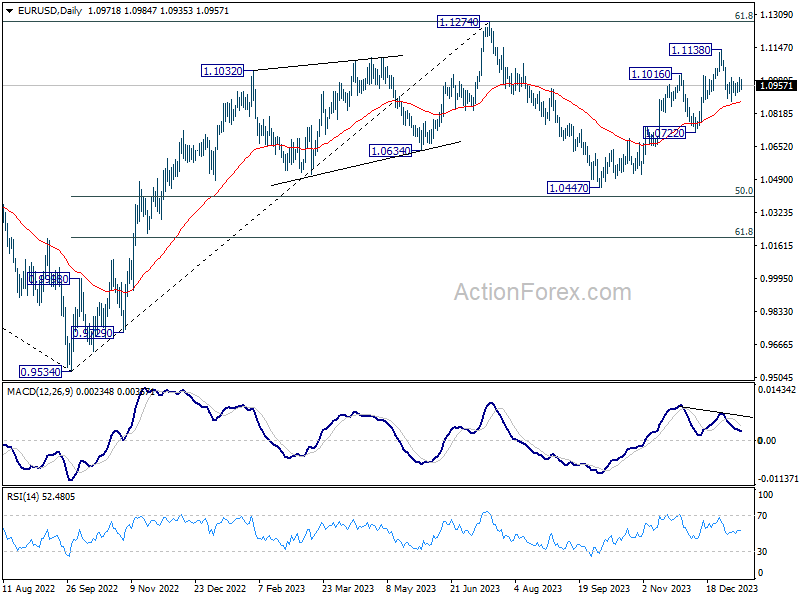

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0936; (P) 1.0967; (R1) 1.1005; More...

Intraday bias in EUR/USD remains neutral as range trading continues. On the downside break of 1.0876 will resume the fall from 1.1138 short term top to 1.0722 support next. However, break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

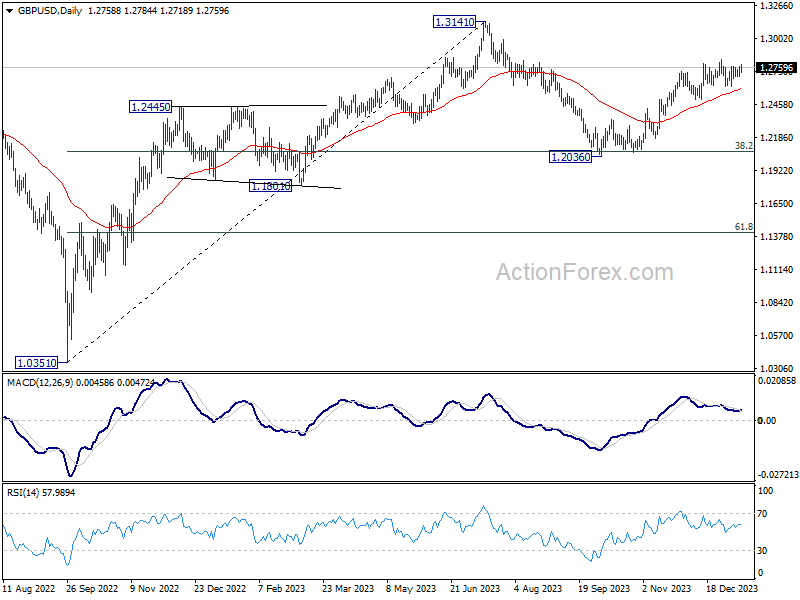

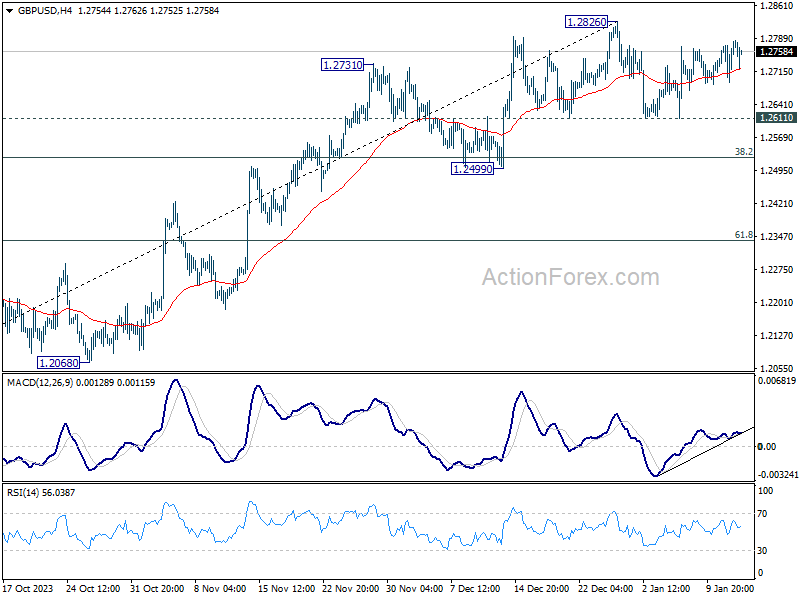

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2711; (P) 1.2742; (R1) 1.2795; More...

No change in GBP/USD's outlook as range trading continues below 1.2826. On the upside, decisive break of 1.2826 high will resume whole rally from 1.2036. Nevertheless, break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.