Sample Category Title

GBP/JPY Weekly Outlook

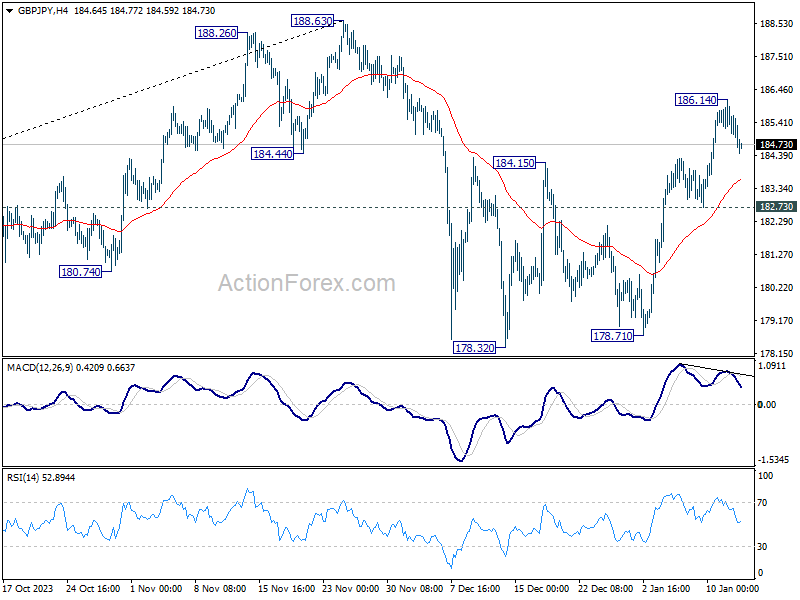

GBP/JPY's strong break of 184.15 resistance last week indicates that corrective fall from 188.63 has completed at 178.32. But as a temporary top was formed at 186.14, initial bias is neutral this week first. Further rally is in favor as long as 182.73 minor support holds. Break of 186.14 will target 188.63 high next.

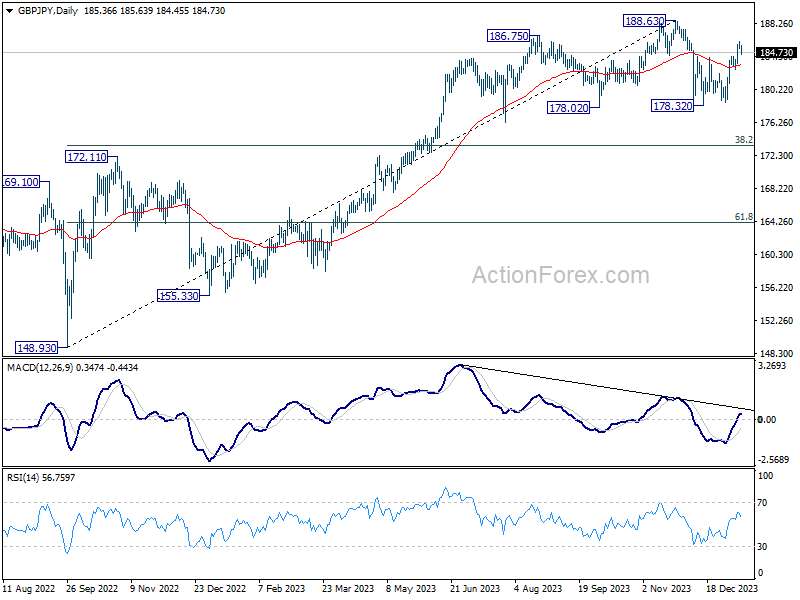

In the bigger picture, price actions from 188.63 medium term top are seen as a correction to the up trend from 148.93 (2022 low) only. As long as 172.11 resistance turned support holds, larger up trend from 123.94 (2020 low) is still in favor to resume through 188.63 at a later stage.

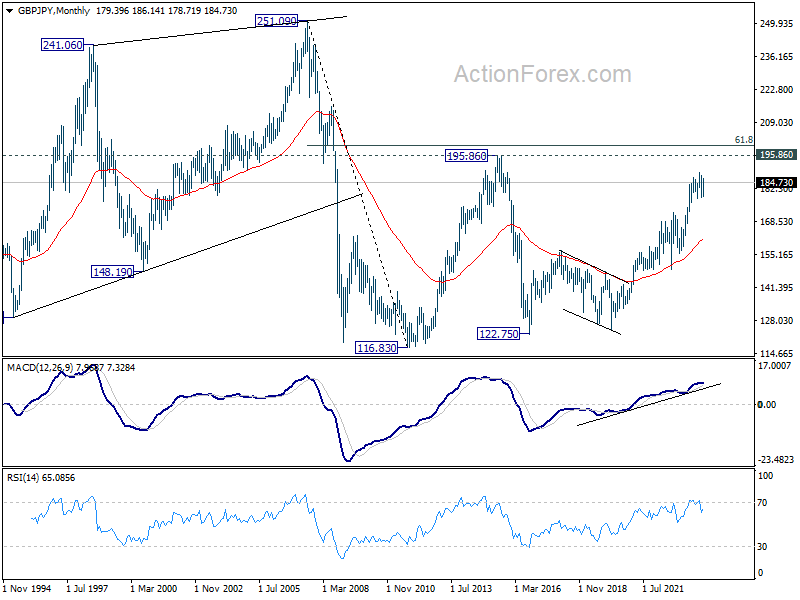

In the longer term picture, rise from 122.75 (2016 low) in still in progress despite loss of upside momentum as seen in W MACD. Further rise will remain in favor, as long as 172.11 support holds, to retest 195.86 (2015 high).

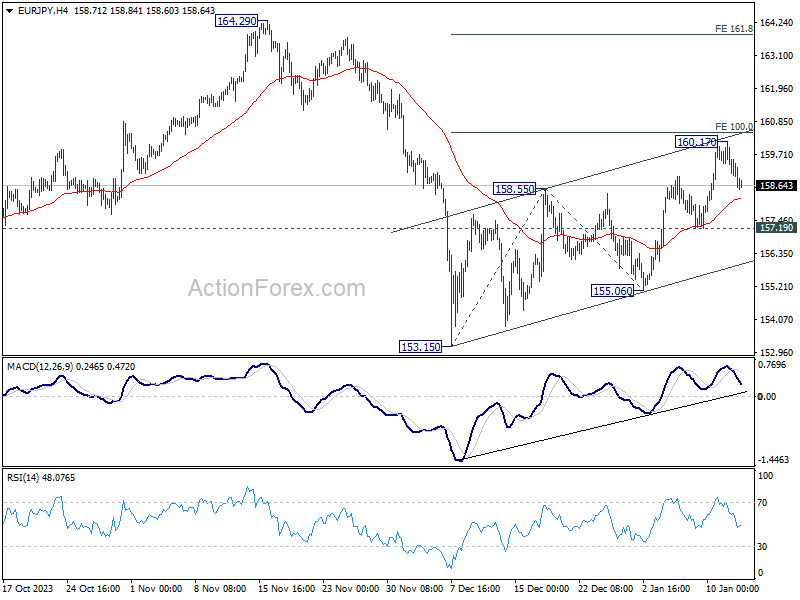

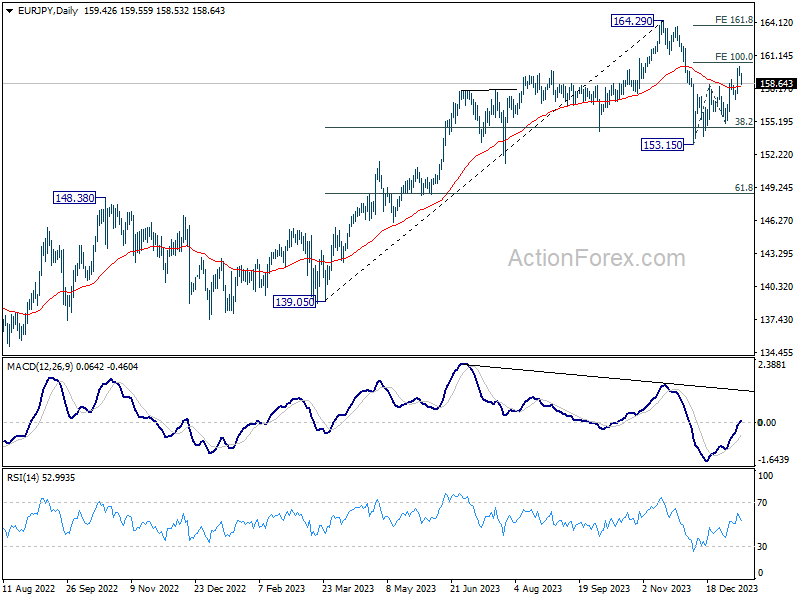

EUR/JPY Weekly Outlook

EUR/JPY roses further to 160.17 last week but retreated ahead of 100% projection of 153.15 to 158.55 from 155.06 at 160.46. Initial bias remains neutral this week first. Further rise is mildly in favor as long as 157.19 minor support holds. Firm break of 160.46 will pave the way to 161.8% projection at 163.79. However, break of 157.19 support will argue that the rebound has completed, and turn bias back to the downside.

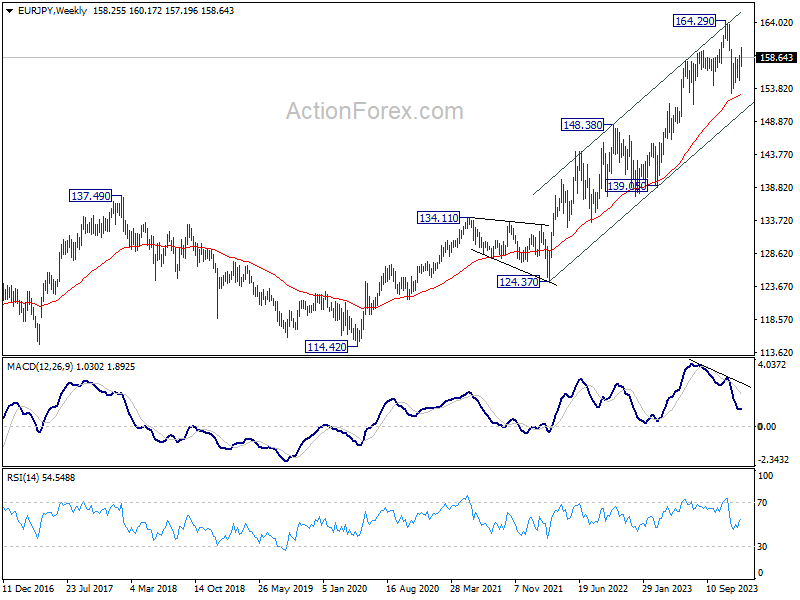

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

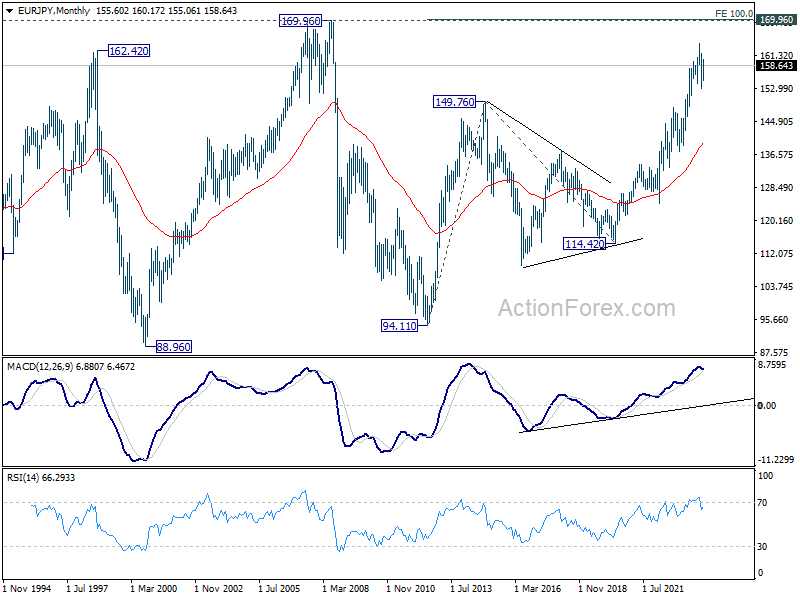

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 148.48 resistance turned support holds.

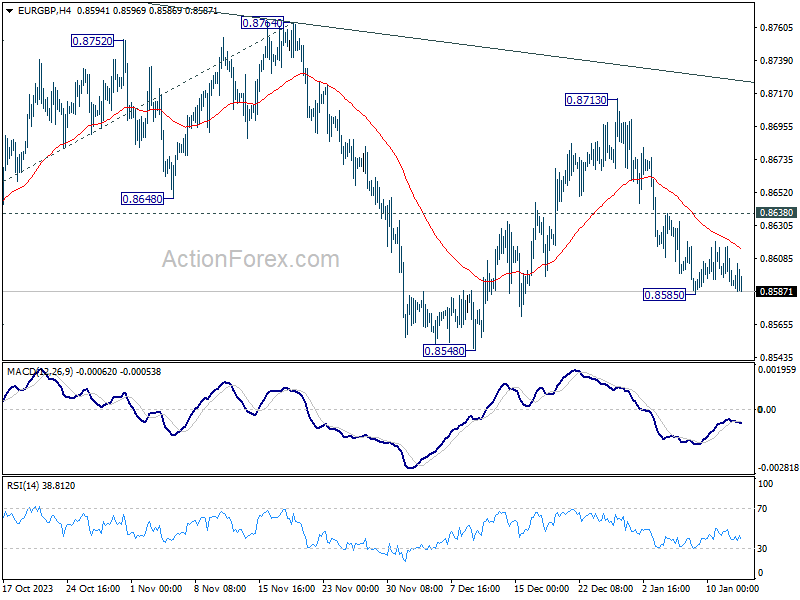

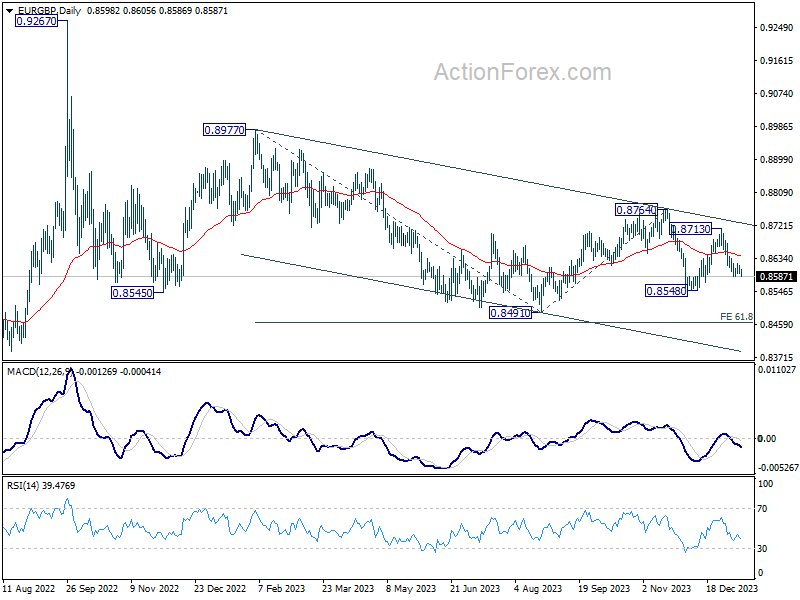

EUR/GBP Weekly Outlook

EUR/GBP fell to 0.8585 last week but turned sideway since then. Initial bias stays neutral this week and more consolidations could be seen. But further decline is expected as long as 0.8638 minor resistance holds. On the downside, below 0.8585 will resume the fall from 0.8713 to 0.8548 support. Firm break there will target 0.8491 low next.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8764 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

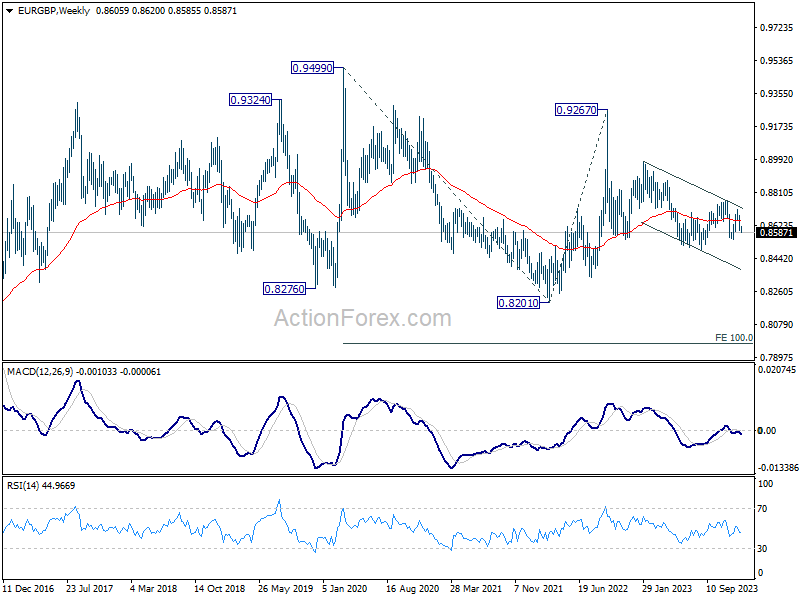

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Fall from 0.9267 is the third leg of the pattern from 0.9499. Break of 0.8201 (2022 low) will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969.

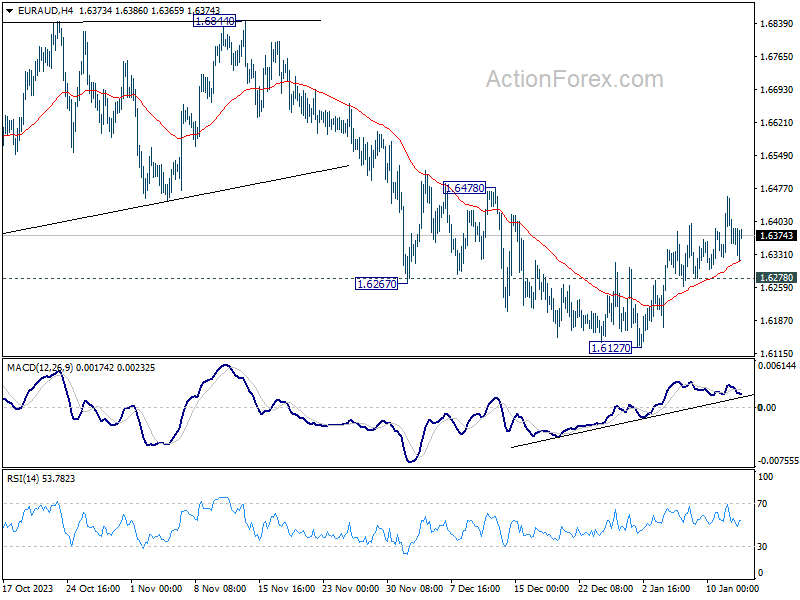

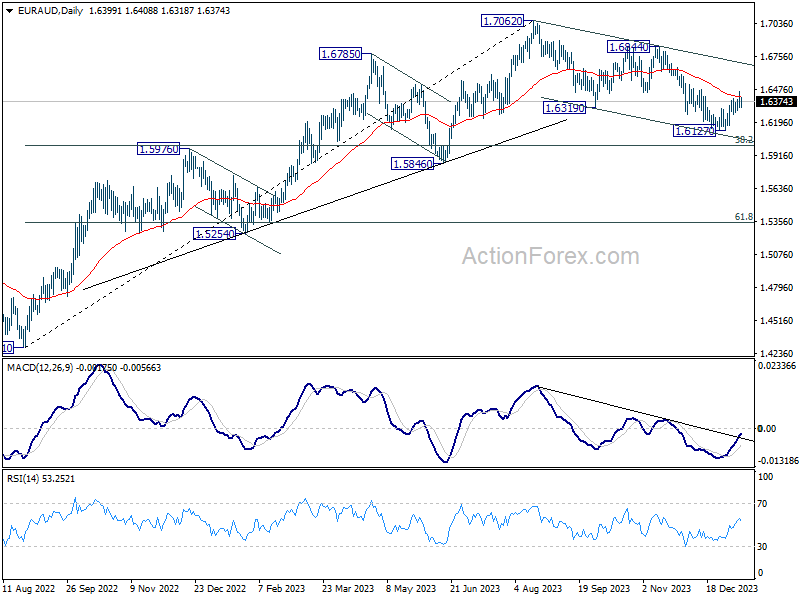

EUR/AUD Weekly Outlook

EUR/AUD's rebound from 1.6127 short term bottom extended higher last week, but failed to break through 1.6478 resistance and retreated. Initial bias is neutral this week first, but further rise is in favor as long as 1.16278 minor support holds. On the upside, firm break of 1.6478 will argue that whole correction from 1.7062 has completed, and target 1.6844 resistance for confirmation. Nevertheless, break of 1.6278 minor support will turn bias back to the downside for retesting 1.6127 low.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 bring rebound. Break of 1.6844 will argue that this up trend is ready to resume through 1.7062 high.

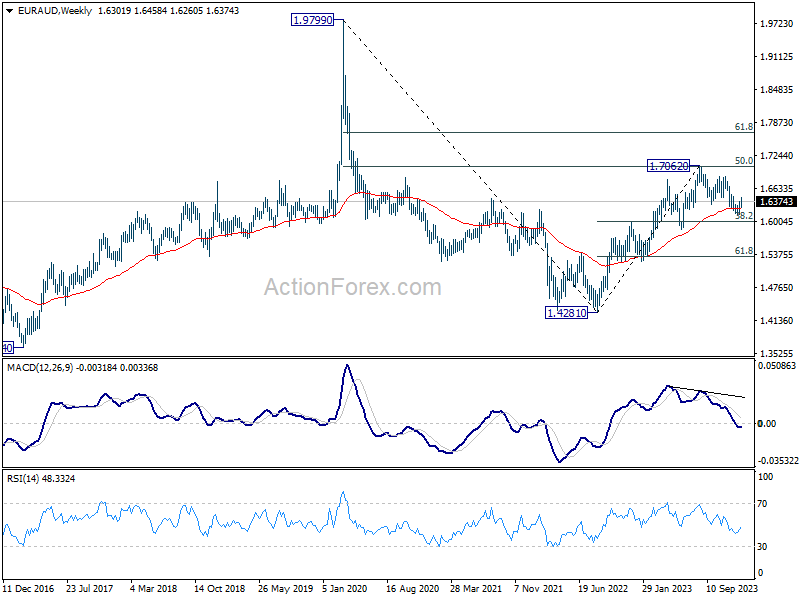

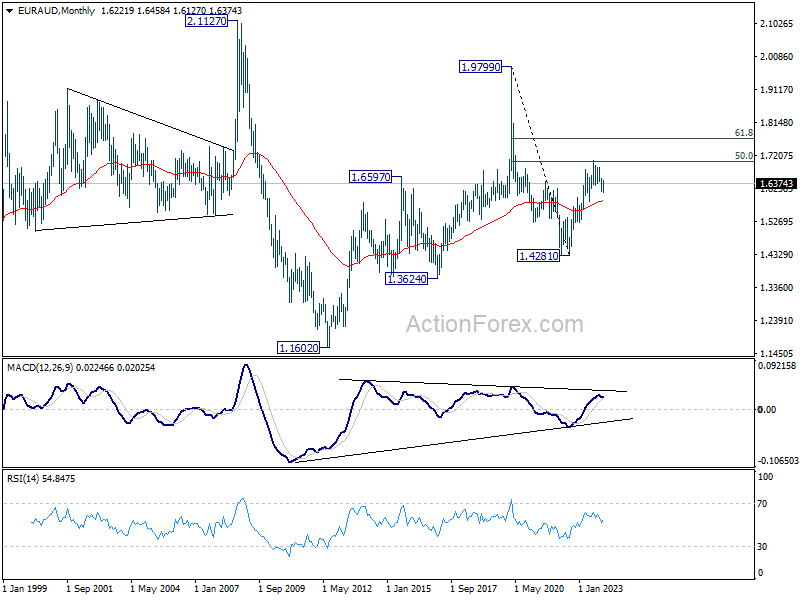

In the longer term picture, fall from 1.9799 (2020 high) is seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5874) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

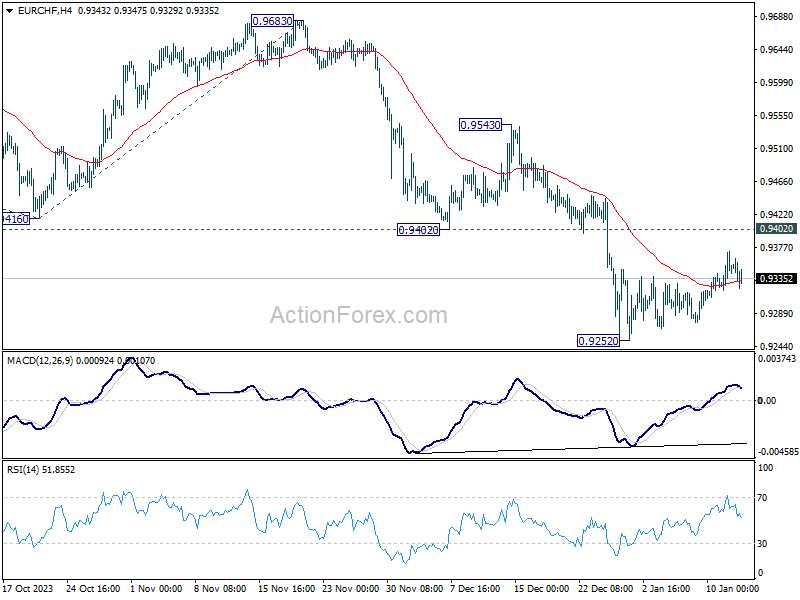

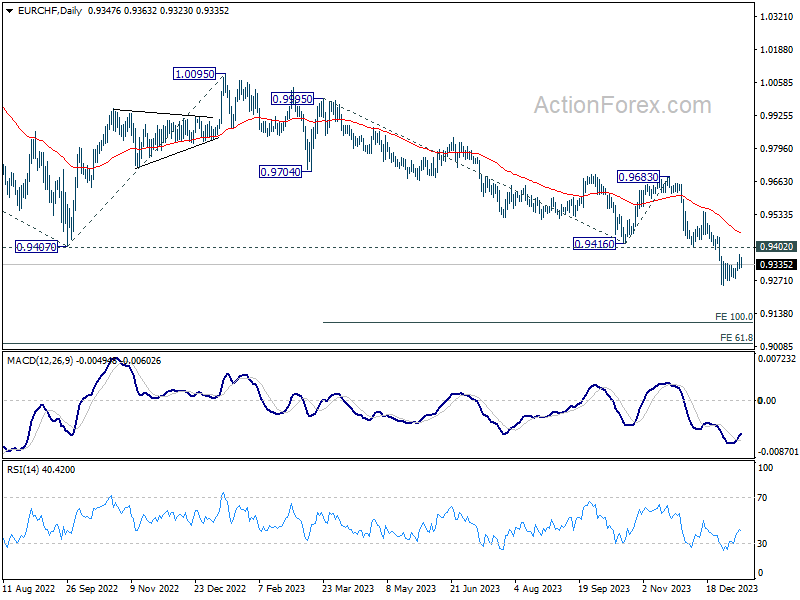

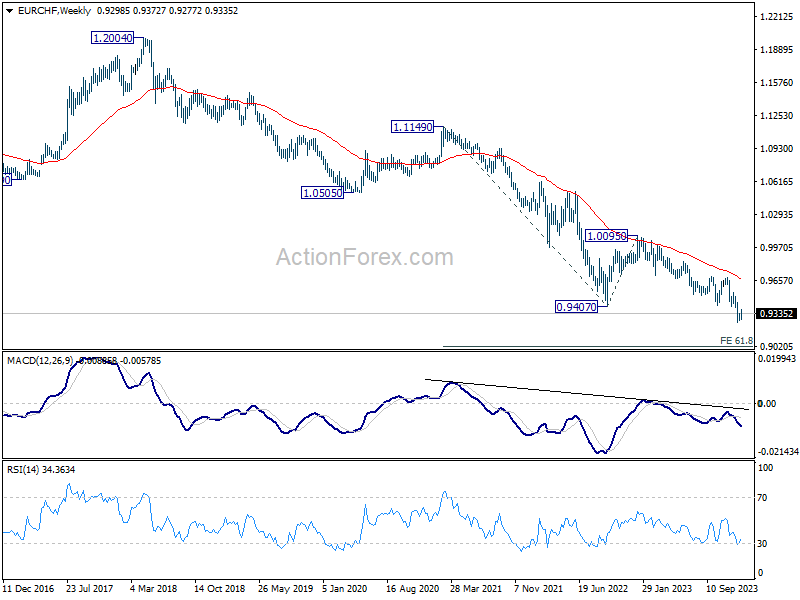

EUR/CHF Weekly Outlook

EUR/CHF's recovery from 0.9252 short term bottom extended higher last week, but upside was capped below 0.9402 support turned resistance. Initial bias remains neutral this week and outlook staying bearish. On the downside, break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next.

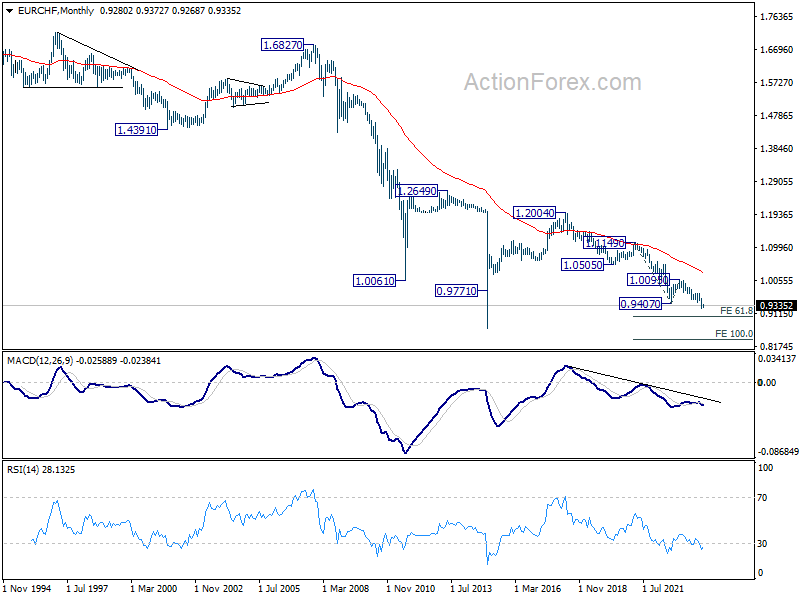

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0265). Larger down trend from 1.2004 (2018 high) is in progress.

Summary 1/15 – 1/19

Monday, Jan 15, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Dec | 2.20% | 2.30% |

| 00:00 | AUD | TD Securities Inflation M/M Dec | 0.30% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Dec | -13.60% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Nov | -0.30% | -0.70% |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Nov | 11.2B | 10.9B |

| 13:30 | CAD | Manufacturing Sales M/M Nov | 0.90% | -2.80% |

| 13:30 | CAD | Wholesale Sales M/M Nov | 0.80% | -0.50% |

| 15:30 | CAD | BoC Business Outlook Survey | ||

| 21:00 | NZD | NZIER Business Confidence Q4 | -52 | |

| 23:30 | AUD | Westpac Consumer Confidence Jan | 2.70% | |

| 23:50 | JPY | PPI Y/Y Dec | -0.30% | 0.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Dec | |

| Forecast: 2.20% | Previous: 2.30% | ||

| 00:00 | AUD | TD Securities Inflation M/M Dec | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Dec | |

| Forecast: | Previous: -13.60% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Nov | |

| Forecast: -0.30% | Previous: -0.70% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Nov | |

| Forecast: 11.2B | Previous: 10.9B | ||

| 13:30 | CAD | Manufacturing Sales M/M Nov | |

| Forecast: 0.90% | Previous: -2.80% | ||

| 13:30 | CAD | Wholesale Sales M/M Nov | |

| Forecast: 0.80% | Previous: -0.50% | ||

| 15:30 | CAD | BoC Business Outlook Survey | |

| Forecast: | Previous: | ||

| 21:00 | NZD | NZIER Business Confidence Q4 | |

| Forecast: | Previous: -52 | ||

| 23:30 | AUD | Westpac Consumer Confidence Jan | |

| Forecast: | Previous: 2.70% | ||

| 23:50 | JPY | PPI Y/Y Dec | |

| Forecast: -0.30% | Previous: 0.30% | ||

Tuesday, Jan 16, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | GBP | Claimant Count Change Dec | 18.1K | 16K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Nov | 4.30% | 4.20% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Nov | 6.60% | 7.30% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Nov | 6.80% | 7.20% |

| 07:00 | EUR | Germany CPI M/M Dec F | 0.10% | 0.10% |

| 07:00 | EUR | Germany CPI Y/Y Dec F | 3.70% | 3.70% |

| 10:00 | EUR | Germany ZEW Economic Sentiment Jan | 12.7 | 12.8 |

| 10:00 | EUR | Germany ZEW Current Situation Jan | -77 | -77.1 |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Jan | 21.9 | 23.0 |

| 13:15 | CAD | Housing Starts Dec | 244K | 213K |

| 13:30 | CAD | CPI M/M Dec | -0.30% | 0.10% |

| 13:30 | CAD | CPI Y/Y Dec | 3.30% | 3.10% |

| 13:30 | CAD | CPI Median Y/Y Dec | 3.40% | 3.40% |

| 13:30 | CAD | CPI Trimmed Y/Y Dec | 3.50% | 3.50% |

| 13:30 | CAD | CPI Common Y/Y Dec | 3.80% | 3.90% |

| 13:30 | USD | Empire State Manufacturing Index Jan | -5 | -14.5 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | GBP | Claimant Count Change Dec | |

| Forecast: 18.1K | Previous: 16K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Nov | |

| Forecast: 4.30% | Previous: 4.20% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Nov | |

| Forecast: 6.60% | Previous: 7.30% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Nov | |

| Forecast: 6.80% | Previous: 7.20% | ||

| 07:00 | EUR | Germany CPI M/M Dec F | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 07:00 | EUR | Germany CPI Y/Y Dec F | |

| Forecast: 3.70% | Previous: 3.70% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Jan | |

| Forecast: 12.7 | Previous: 12.8 | ||

| 10:00 | EUR | Germany ZEW Current Situation Jan | |

| Forecast: -77 | Previous: -77.1 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Jan | |

| Forecast: 21.9 | Previous: 23.0 | ||

| 13:15 | CAD | Housing Starts Dec | |

| Forecast: 244K | Previous: 213K | ||

| 13:30 | CAD | CPI M/M Dec | |

| Forecast: -0.30% | Previous: 0.10% | ||

| 13:30 | CAD | CPI Y/Y Dec | |

| Forecast: 3.30% | Previous: 3.10% | ||

| 13:30 | CAD | CPI Median Y/Y Dec | |

| Forecast: 3.40% | Previous: 3.40% | ||

| 13:30 | CAD | CPI Trimmed Y/Y Dec | |

| Forecast: 3.50% | Previous: 3.50% | ||

| 13:30 | CAD | CPI Common Y/Y Dec | |

| Forecast: 3.80% | Previous: 3.90% | ||

| 13:30 | USD | Empire State Manufacturing Index Jan | |

| Forecast: -5 | Previous: -14.5 | ||

Wednesday, Jan 17, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | CNY | GDP Y/Y Q4 | 5.20% | 4.90% |

| 02:00 | CNY | Industrial Production Y/Y Dec | 6.80% | 6.60% |

| 02:00 | CNY | Retail Sales Y/Y Dec | 8.10% | 10.10% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Dec | 2.90% | 2.90% |

| 07:00 | GBP | CPI M/M Dec | 0.20% | -0.20% |

| 07:00 | GBP | CPI Y/Y Dec | 3.80% | 3.90% |

| 07:00 | GBP | RPI M/M Dec | 0.40% | -0.10% |

| 07:00 | GBP | RPI Y/Y Dec | 0.40% | 5.30% |

| 07:00 | GBP | PPI Input M/M Dec | -0.30% | |

| 07:00 | GBP | PPI Input Y/Y Dec | -2.60% | |

| 07:00 | GBP | PPI Core Output M/M Dec | 0.00% | |

| 07:00 | GBP | PPI Core Output Y/Y Dec | 0.20% | |

| 07:00 | GBP | PPI Output M/M Dec | -0.10% | |

| 07:00 | GBP | PPI Output Y/Y Dec | -0.20% | |

| 07:00 | GBP | Core CPI Y/Y Dec | 4.90% | 5.10% |

| 10:00 | EUR | Eurozone CPI Y/Y Dec F | 2.90% | 2.90% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec F | 3.40% | 3.40% |

| 13:30 | CAD | Industrial Product Price M/M Dec | -0.70% | -0.40% |

| 13:30 | CAD | Raw Material Price Index Dec | -2.10% | -4.20% |

| 13:30 | USD | Retail Sales M/M Dec | 0.40% | 0.30% |

| 13:30 | USD | Retail Sales ex Autos M/M Dec | 0.20% | 0.20% |

| 13:30 | USD | Import Price Index M/M Dec | -0.50% | -0.40% |

| 14:15 | USD | Industrial Production M/M Dec | -0.10% | 0.20% |

| 14:15 | USD | Capacity Utilization Dec | 78.70% | 78.80% |

| 15:00 | USD | Business Inventories Nov | -0.10% | -0.10% |

| 15:00 | USD | NAHB Housing Index Jan | 39 | 37 |

| 19:00 | USD | Fed's Beige Book | ||

| 23:50 | JPY | Machinery Orders M/M Nov | -0.80% | 0.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | CNY | GDP Y/Y Q4 | |

| Forecast: 5.20% | Previous: 4.90% | ||

| 02:00 | CNY | Industrial Production Y/Y Dec | |

| Forecast: 6.80% | Previous: 6.60% | ||

| 02:00 | CNY | Retail Sales Y/Y Dec | |

| Forecast: 8.10% | Previous: 10.10% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Dec | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 07:00 | GBP | CPI M/M Dec | |

| Forecast: 0.20% | Previous: -0.20% | ||

| 07:00 | GBP | CPI Y/Y Dec | |

| Forecast: 3.80% | Previous: 3.90% | ||

| 07:00 | GBP | RPI M/M Dec | |

| Forecast: 0.40% | Previous: -0.10% | ||

| 07:00 | GBP | RPI Y/Y Dec | |

| Forecast: 0.40% | Previous: 5.30% | ||

| 07:00 | GBP | PPI Input M/M Dec | |

| Forecast: | Previous: -0.30% | ||

| 07:00 | GBP | PPI Input Y/Y Dec | |

| Forecast: | Previous: -2.60% | ||

| 07:00 | GBP | PPI Core Output M/M Dec | |

| Forecast: | Previous: 0.00% | ||

| 07:00 | GBP | PPI Core Output Y/Y Dec | |

| Forecast: | Previous: 0.20% | ||

| 07:00 | GBP | PPI Output M/M Dec | |

| Forecast: | Previous: -0.10% | ||

| 07:00 | GBP | PPI Output Y/Y Dec | |

| Forecast: | Previous: -0.20% | ||

| 07:00 | GBP | Core CPI Y/Y Dec | |

| Forecast: 4.90% | Previous: 5.10% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Dec F | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec F | |

| Forecast: 3.40% | Previous: 3.40% | ||

| 13:30 | CAD | Industrial Product Price M/M Dec | |

| Forecast: -0.70% | Previous: -0.40% | ||

| 13:30 | CAD | Raw Material Price Index Dec | |

| Forecast: -2.10% | Previous: -4.20% | ||

| 13:30 | USD | Retail Sales M/M Dec | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Dec | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 13:30 | USD | Import Price Index M/M Dec | |

| Forecast: -0.50% | Previous: -0.40% | ||

| 14:15 | USD | Industrial Production M/M Dec | |

| Forecast: -0.10% | Previous: 0.20% | ||

| 14:15 | USD | Capacity Utilization Dec | |

| Forecast: 78.70% | Previous: 78.80% | ||

| 15:00 | USD | Business Inventories Nov | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 15:00 | USD | NAHB Housing Index Jan | |

| Forecast: 39 | Previous: 37 | ||

| 19:00 | USD | Fed's Beige Book | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Machinery Orders M/M Nov | |

| Forecast: -0.80% | Previous: 0.70% | ||

Thursday, Jan 18, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Jan | 4.50% | |

| 00:01 | GBP | RICS Housing Price Balance Dec | -43% | |

| 00:30 | AUD | Employment Change Dec | 15.4K | 61.5K |

| 00:30 | AUD | Unemployment Rate Dec | 3.90% | 3.90% |

| 04:30 | JPY | Industrial Production M/M Nov F | -0.90% | -0.90% |

| 09:00 | EUR | Eurozone Current Account (EUR) Nov | 33.8B | |

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||

| 13:30 | USD | Initial Jobless Claims (Jan 12) | 207K | 202K |

| 13:30 | USD | Housing Starts Dec | 1.43M | 1.56M |

| 13:30 | USD | Building Permits Dec | 1.47M | 1.47M |

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Jan | -6.9 | -10.5 |

| 15:30 | USD | Natural Gas Storage | -140B | |

| 16:00 | USD | Crude Oil Inventories | 1.3M | |

| 21:30 | NZD | Business NZ PMI Dec | 46.7 | |

| 23:30 | JPY | National CPI Y/Y Dec | 2.80% | |

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Dec | 2.30% | 2.50% |

| 23:30 | JPY | National CPI ex Food & Energy Y/Y Dec | 3.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Jan | |

| Forecast: | Previous: 4.50% | ||

| 00:01 | GBP | RICS Housing Price Balance Dec | |

| Forecast: | Previous: -43% | ||

| 00:30 | AUD | Employment Change Dec | |

| Forecast: 15.4K | Previous: 61.5K | ||

| 00:30 | AUD | Unemployment Rate Dec | |

| Forecast: 3.90% | Previous: 3.90% | ||

| 04:30 | JPY | Industrial Production M/M Nov F | |

| Forecast: -0.90% | Previous: -0.90% | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Nov | |

| Forecast: | Previous: 33.8B | ||

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | |

| Forecast: | Previous: | ||

| 13:30 | USD | Initial Jobless Claims (Jan 12) | |

| Forecast: 207K | Previous: 202K | ||

| 13:30 | USD | Housing Starts Dec | |

| Forecast: 1.43M | Previous: 1.56M | ||

| 13:30 | USD | Building Permits Dec | |

| Forecast: 1.47M | Previous: 1.47M | ||

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Jan | |

| Forecast: -6.9 | Previous: -10.5 | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -140B | ||

| 16:00 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 1.3M | ||

| 21:30 | NZD | Business NZ PMI Dec | |

| Forecast: | Previous: 46.7 | ||

| 23:30 | JPY | National CPI Y/Y Dec | |

| Forecast: | Previous: 2.80% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Dec | |

| Forecast: 2.30% | Previous: 2.50% | ||

| 23:30 | JPY | National CPI ex Food & Energy Y/Y Dec | |

| Forecast: | Previous: 3.80% | ||

Friday, Jan 19, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Nov | 0.20% | -0.80% |

| 07:00 | GBP | Retail Sales M/M Dec | -0.50% | 1.30% |

| 07:00 | EUR | Germany PPI M/M Dec | -0.50% | -0.50% |

| 07:00 | EUR | Germany PPI Y/Y Dec | -7.90% | -7.90% |

| 07:30 | CHF | Producer and Import Prices M/M Dec | -0.90% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Dec | -1.30% | |

| 13:30 | CAD | Retail Sales M/M Nov | 0.00% | 0.70% |

| 13:30 | CAD | Retail Sales ex Autos M/M Nov | -0.10% | 0.60% |

| 15:00 | USD | Existing Home Sales Dec | 3.82M | 3.82M |

| 15:00 | USD | Michigan Consumer Sentiment Index Jan P | 69.6 | 69.7 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Nov | |

| Forecast: 0.20% | Previous: -0.80% | ||

| 07:00 | GBP | Retail Sales M/M Dec | |

| Forecast: -0.50% | Previous: 1.30% | ||

| 07:00 | EUR | Germany PPI M/M Dec | |

| Forecast: -0.50% | Previous: -0.50% | ||

| 07:00 | EUR | Germany PPI Y/Y Dec | |

| Forecast: -7.90% | Previous: -7.90% | ||

| 07:30 | CHF | Producer and Import Prices M/M Dec | |

| Forecast: | Previous: -0.90% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Dec | |

| Forecast: | Previous: -1.30% | ||

| 13:30 | CAD | Retail Sales M/M Nov | |

| Forecast: 0.00% | Previous: 0.70% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Nov | |

| Forecast: -0.10% | Previous: 0.60% | ||

| 15:00 | USD | Existing Home Sales Dec | |

| Forecast: 3.82M | Previous: 3.82M | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Jan P | |

| Forecast: 69.6 | Previous: 69.7 | ||

The Weekly Bottom Line: The Long and Bumpy Road

U.S. Highlights

- An upside inflation surprise didn’t do much to move markets, as the details of the report fell in line with expectations.

- The focus remains firmly on the services sector, where housing costs continue to prop up price growth.

- Looking forward, the Fed will need to see more consistent evidence of disinflation – likely delaying any policy changes to mid-year.

Canadian Highlights

- The week’s limited economic calendar was centered around merchandise trade, where the surplus extended into the fourth consecutive quarter. We expect trade to be a positive contribution to real GDP in Q4.

- Likewise, consumer spending is tracking stronger than previously expected, with recent readings of TD spend data showing a notable contribution from both goods and services. We expect this uptick in spending to be short-lived.

- Next week we’ll get critical insights from consumer and business surveys, CPI, housing markets and retail sales. These updates will help the BoC fine tune its communication strategy ahead of delivering its first rate cut in the spring of 2024.

U.S. – The Long and Bumpy Road

Taming inflation is never easy, and usually proceeds in fits and starts. So, given the experience of the past year, this week’s hotter-than-expected print to consumer price index (CPI) inflation doesn’t come as all that much of a surprise. Indeed, the details of the report left room for optimism and meant that markets brushed off the surprise – leaving ten-year U.S. treasury yields virtually unchanged on the news. The positive developments under the hood (so to speak) fell in line with consensus expectations and meant that the focus could be kept firmly on the timing of possible Fed cuts.

Headline CPI inflation rose 0.3% month-on-month (m/m), taking the annual reading for December to 3.4%. While the print did exceed market expectations, it was the more closely watched core measure that drove the muted market response. The price index excluding food and energy matched the headline gain at +0.3% m/m – a pace it has logged in four of the past five months. This is the interesting bit, on a three-month annualized basis core CPI inflation is running at 3.3%, roughly unchanged since October and still clear of the Fed’s target.

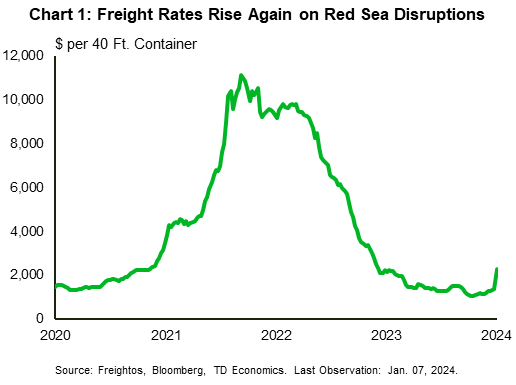

The stickiness in the core measure is slightly concerning, particularly as core goods prices remained flat, snapping a six-month run of price declines. Moreover, there is some near-term upside risk to goods prices as attacks on ships in the Red Sea affecting access to the Suez Canal have lead to a jump in freight costs (Chart 1). Despite this, what the pause in goods price deflation laid bare was the ongoing strength in services price gains.

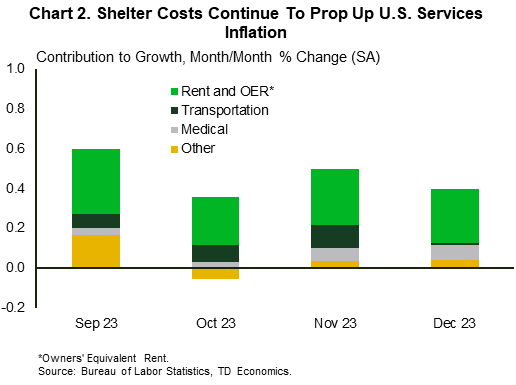

Core services prices were up 0.4% m/m in December. Moreover, the strong price gains have been persistent, with the three-month and six-month (annualized) rates of core services inflation at 5.1% and 5.2%, respectively. Yet, while these figures are significantly higher than the Fed would feel comfortable with, there are reasons to believe conditions are improving. Currently, the largest contributing factor to services inflation is the shelter component (Chart 2). On this front relief is expected as increases in observed rents (which tend to lead the measure in the CPI report) have moderated sharply in recent months – a dynamic that is still gradually working through to the shelter component of CPI. Moreover, the slowdown in home price appreciation through early-2023 also continues to gradually work its way into the CPI.

The return to two percent inflation continues to be bumpy, but progress has been tangible and signs suggest that the Fed continues to be on course. After a few months of solid progress, optimism had begun to emerge that cuts might come sooner rather than later. However, price pressures remain sticky, and the economy continues to outperform. December job growth was above trend, and the Atlanta Fed Nowcast is expecting GDP growth of over 2% (annualized) in the fourth quarter or 2023.

A packed slate of Fed speakers is on tap for next week, and should hopefully give some additional insight into how they view the recent data. However, given this week’s developments, it will likely be mid-year before officials have sufficient evidence that they can begin loosening their policy stance.

Canada – A Week of Economic Stillness

As January progresses, the Canadian economy sails through a period of relative stillness. In the world of finance, markets took cues from oil price movements and economic developments south of the border. Equity markets exhibited slight volatility, closing the week with modest gains, while bond markets were fairly steady, with the 5-year yield hovering around 3.3%.

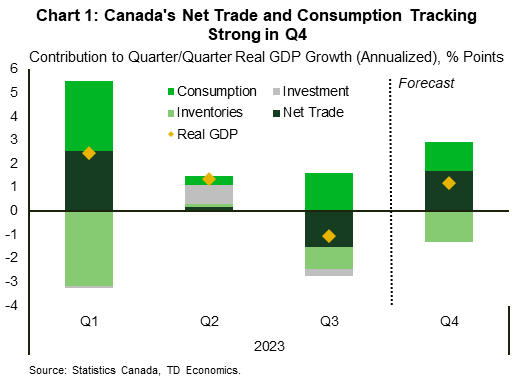

The week's limited economic calendar was centered around merchandise trade, where the surplus extended into the fourth consecutive quarter, narrowing from $3.2 billion in October to $1.6 billion in November. The decline in exports, stemming from short-term factors in aircraft and other transportation equipment exports, highlights the volatile nature of international trade. On the import front, a robust increase points to remnants of domestic demand, particularly notable in the energy sector. With two months of data under the belt, our tracking points to trade's positive contribution to real GDP in Q4 (Chart 1).

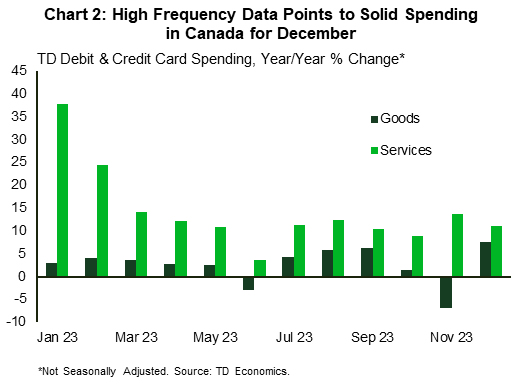

Some evidence of domestic demand presented itself in our TD's most recent debit and credit card data. December data indicates that consumer spending was up 6.2% year-on-year and largely driven by spending on services (Chart 2). Last month's notable uptick in goods spending was largely concentrated in clothing and general merchandise stores. This could reflect a strategic shift by consumers towards last-minute holiday shopping, possibly in search of attractive deals. All in all, high-frequency data points to a stronger than previously expected contribution from consumer spending in the last quarter of 2023 (Chart 1). This uptick is likely to be short-lived, however, as consumers will return to more cautious spending behaviour in the first half of 2024 (see forecast).

Consumers' quest for value may pose a challenge for the Bank of Canada (see report). As the central bank contemplates the path of rate cuts in the forthcoming year, it finds itself in a delicate dance, navigating the dual pressures of an economy not yet at its inflation target and the potential for rate cuts to rekindle inflationary forces. This is particularly pertinent in the housing sector, where lower rates could breathe new life into home prices. In Canada, households are more prone to anchoring their inflation expectations to home prices, so a premature easing in financial conditions that fuels shelter price pressures could amplify household inflation expectations, impeding the Bank's efforts to restore its credibility.

Incidentally, next week we'll get updates on Q4 Canadian Survey of Consumer Expectations together with a parallel Business Outlook Survey and the inflation data (CPI) for December. These releases will provide critical insights to help the BoC attune its communication strategy to help strike the right balance between exerting too much pressure on the economy and stoking inflationary pressures. In addition, December data on housing will shed light on recent changes in home prices, while retail sales will give a sense of consumer spending in November.

Weekly Economic & Financial Commentary

Summary

United States: Inflation's Downward Trend Remains in Place

- Inflation continues to cool. Although rising energy prices drove a hotter-than-expected change in the headline CPI, the core CPI was up 3.9% year-over-year in December, bringing the annual change below 4% for the first time in two and a half years. A soft PPI print in December provided additional evidence that price pressures are abating.

- Next week: Retail Sales (Wed.), Industrial Production (Wed.), Existing Home Sales (Fri.)

International: China's December Activity Data Underwhelm

- Structural issues have taken a toll on China's economy, and this sluggish economic momentum was on display this week when December activity data were released. Meanwhile, many large developing economies are still far from deflation.

- Next week: Taiwan Election (Sun.), China GDP (Wed.), Japan Inflation (Fri.)

Interest Rate Watch: A View from the Summit

- After an arduous ascent in interest rates over the past two years, a growing enthusiasm in financial markets is building in anticipation of the coming descent. Our soft-landing scenario is partly due to an expected policy environment that is less restrictive.

Credit Market Insights: Where Credit's Due: Credit Card Spending Surges in November

- Household borrowing rose for the third straight month in November as consumers continued to reach for their credit cards. Total consumer credit outstanding rose $23.8 billion and surpassed $5 trillion for the first time. The main driver of this increase was revolving consumer credit, which accounted for $19.1 billion of the overall increase.

Topic of the Week: Taiwan Heads to the Polls

- The 2024 global election cycle is certainly not starting off quietly. As voters across Taiwan head to the polls this weekend, the future of some of the world’s most tense geopolitical relationships may hang in the balance. The world will be watching the Taiwan election outcome for signs of what 2024 and beyond may bring for relations between Taiwan, China and the United States.

Canadian Inflation Likely Ticked Up in December But Easing Trend to Continue

December inflation numbers and the Bank of Canada’s own business and consumer surveys will headline a slew of Canadian indicators ahead of the central bank’s next interest rate decision later this month. Canadian headline CPI growth is expected to tick slightly higher (+3.4% year-over-year) from November’s 3.1% increase, but with the gain largely coming from energy price ‘base-effects’ as a large drop in gasoline prices a year ago falls out of the year-over-year growth calculation.

Food price growth likely slowed again and broader measures of inflation pressures have eased in recent months with the bulk of remaining upward price growth coming from surging mortgage interest costs due to higher interest rates. Year-over-year growth in the BoC’s preferred median and trim ‘core’ CPI measures should be little changed in December, and the more recent three-month annualized growth rate that the central bank has been watching is more likely to tick a touch higher (from 2.3% and 2.6%, respectively, growth rates in November.) Still, the breadth and magnitude of inflation have continued to edge lower on balance. Growth in mortgage interest costs is accounting for roughly a third of total price growth excluding food and energy products. The BoC will continue to look through price growth from that component because the increase is a direct result of earlier interest rate hikes, and price increases excluding that component have been running within the 1% to 3% inflation target range.

The BoC will also be watching their own Business Outlook Survey and accompanying consumer expectations survey for signs that the slowing in inflation numbers will persist in the future. Canadian business optimism about the future outlook may have ticked higher with growing expectations that the BoC is set to start easing off the monetary policy brakes later in 2024. But the policymakers will be watching for further signs that businesses are reverting back towards pre-pandemic pricing behaviour (smaller and less frequent planned price changes) and that easing in labour shortages is cooling expected wage growth.

Week ahead data watch

Statcan’s preliminary estimate for November manufacturing sales was up 1.2% on higher chemical, transportation equipment, and primary metal sales.

The advance estimate of Canadian retail sales in November was flat after a 0.7% uptick in October. Our own RBC cardholder data suggests purchases of physical merchandise (excluding motor vehicles) are tracking higher in Q4 as a whole, but December marked a slowdown in both discretionary goods and services spending.

Housing starts are expected to come in slightly stronger in December at 250K relative to November’s 213K, but still below the 3-month rolling average level of permit issuance (at 268K).

U.S. retail sales likely ticked higher in December (+0.5% month-over-month), with slightly stronger growth than November (+0.3%) thanks to strong unit auto sales and higher gasoline prices.

U.S. industrial production likely fell 0.1% in December, as manufacturing hours worked slid lower (-0.2%). Utilities output was 1.4% lower on warmer-than-usual winter weather, lowering heating demand and driving energy consumption down slightly.

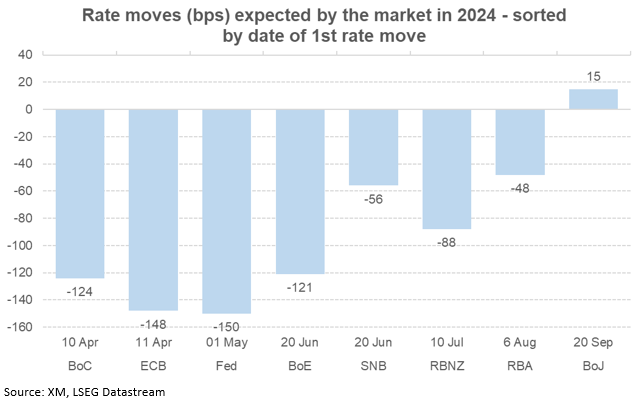

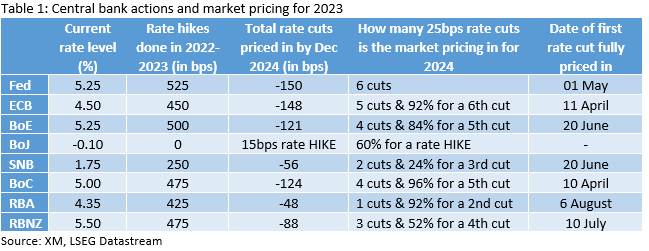

Market Continues to Price in Aggressive Rate Cuts for 2024

- The 2024 market theme remains for several rate cuts from most central banks

- Fed is seen cutting rates six times despite the November Presidential election

- ECB and the BoC to cut first; RBA the last one to join the club

- BoJ is finally seen hiking for the first time since 2007 – will it prove wishful thinking?

Last year ended with clear feelings from the market's side about the direction of rates in 2024: rate cuts across the board, apart from the Bank of Japan. Two weeks into the new year and the market is trying to digest an already busy calendar. Inflation data from both the US and the euro area, and the US labour market have already made an impact on expectations. Therefore, what is currently priced in?

ECB and Fed: 6 rate cuts?

The two most important central banks appear to be on similar paths. The ECB is expected to ease policy by 148 bps in 2024, a tad below the 150bps of Fed easing currently priced in. These market expectations do not align with the underlying economic sentiment as there seems a divergence between the strong growth recorded in the US, causing some Fed hawks to mention rate hikes lately, and the continued economic weakness seen in the Euro area, as portrayed by the PMI surveys.

One of the reasons for the current rate expectations is probably the contradictory rhetoric at the last central bank meetings in December 2023. More specifically, the Fed's Powell dovish rhetoric, which was not entirely evident at the recent minutes, and President Lagarde's hawkish stance have allowed the market to forecast any almost equal number of rate cuts.

BoE and BoC: dangerously close to 5 rates cuts

Moving down the list, the Bank of England and the Bank of Canada are fighting for the third spot with the most rate cuts currently being priced in. Currently, the BoC "wins" with 124bps of rate cuts expected by the December 19, 2024 gathering. While traditionally seen following very closely the Fed's movements, in 2024 it is expected to announce its first 25 bps easing at the April 10 meeting, ahead of the Fed. This sounds a bit extreme considering the current inflation rate and the possibly stronger oil performance during 2024 on the back of OPEC’s disagreements. Of course, there are a few dark horses, for example the housing sector, so the BoC is expected to walk on a tightrope.

Not far below, with 121bps of rate cuts currently priced in, comes the BoE. The market is expecting a slower start as the first 25bps rate cut is currently being priced in by June 20, 2024, around 2.5 months after the ECB's expected first rate move. The higher inflation rate, the pre-election shenanigans and the expected accommodative fiscal stance, which should support consumer spending, appear to affect the market expectations.

RBNZ: almost 4 rate cuts

Not far from the major central banks, the RBNZ is seen cutting rates by 88bps in 2024, unravelling only a small part of its recent tightening cycle. July is currently being touted as the likely month for the first rate cut despite the fact the RBNZ remains hawkish on the back of the latest OCR projections pointing to another rate hike in 2024.

RBA and SNB: 2 rate cuts?

The SNB and the RBA are seen following the rest of the pack with around two rate hikes priced in for 2024. The former is expected to announce a 25bps rate cut in June, mostly to counter further strengthening of its already expensive Swiss franc, especially against the euro. On the other hand, the RBA was the last one to hike in 2023 and it is thus expected to be the last one to announce a rate cut in August 2024. China’s expected growth pick-up could delay even more the start of the easing cycle, but eventually the RBA will probably be forced to follow this path.

BoJ: to finally hike in 2024?

The Bank of Japan is once again the outlier. The market expects that 2024 will be marked by a return to monetary policy normality for the BoJ. This could be wishful thinking by the market or simply a repeat of last year’s modest hiking expectations, which were not confirmed as the BoJ only tweaked its yield curve control program. A total of 15bps of rate hikes is currently priced in by the end of 2024 but even a small 10bps rate move, seen in September 2024, holds significant signaling value for the BoJ.