Sample Category Title

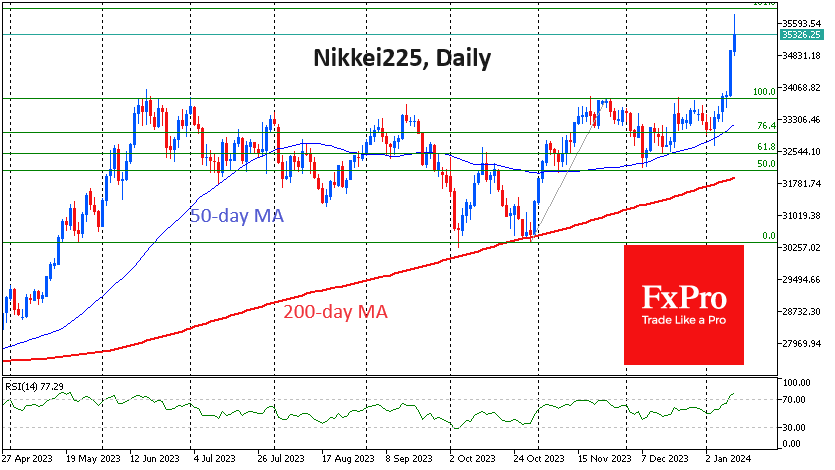

Nikkei225 Needs a Breather But Hardly Done Ascending

Japan’s Nikkei225 index hit new highs since February 1990 on Thursday morning and climbed above 35000. The rise accelerated sharply this week after breaking above the 34000 level, which acted as resistance in the second half of 2023.

The fundamental reason for buying was the dramatic drop in expectations that the Bank of Japan would unwind its ultra-soft monetary policy. The 1 January earthquake and a faster slowdown in consumer inflation have reversed sentiment in the markets.

On the tech analysis side, the Nikkei225 reversed to the upside after touching the 50-day moving average, as it has done repeatedly since November.

However, the move became excessive on Wednesday and Thursday due to likely short covering after breaking important resistance.

In the short term, the index looks overbought, setting up for a local correction in the coming days. However, the big bull cycle in Japanese equities seems to be far from over.

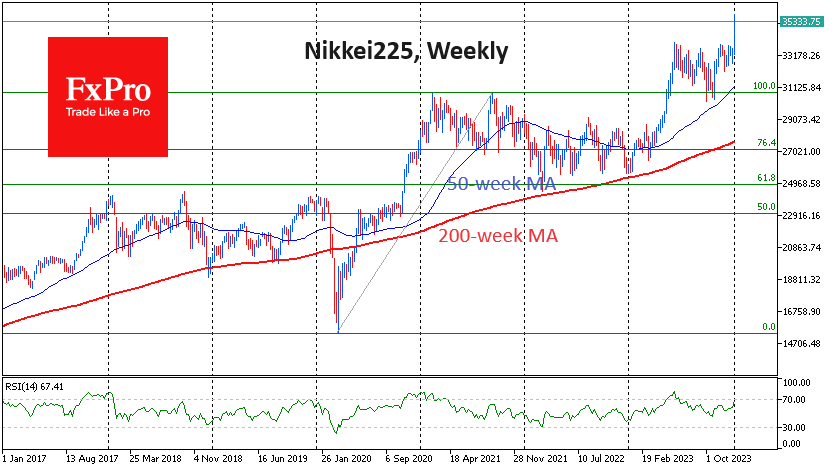

The Nikkei225 doubled from the 2020 lows to the 2021 highs, and the 2022 decline has corrected this rally to a classic 61.8% of the original rise. The buying intensification in 2023 marked a renewal of multi-year highs and a correction to the 2021 peaks.

The development of this pattern opens the door for gains above 40,300 (+14% from current levels) within 12-18 months.

The short-term outlook is less certain as Nikkei225 is overbought to the maximum since May 2022 on RSI on daily charts. Also, the Japanese equity index is close to the 161.8% point of the October-November upside amplitude. This sets up a new wave of profit-taking on the approach to 36000, which is quite close to Thursday’s peaks, forming a not-so-attractive risk/reward ratio.

Sunset Market Commentary

Markets

Trading initially was a long-drawn countdown to today’s US December CPI. Investors tentatively positioned for a rather soft report, with US yields easing 3-4 bps before publication of the data. The report brought a modest upside ‘surprise’. Headline inflation increased 0.3% M/M and 3.4% Y/Y from 3.1% in November (3.2% expected). Core inflation excluding food and energy was close to expectations at 0.3% M/M and 3.9% Y/Y (4.0% in November, 3.8% expected). Looking into the details, food price inflation eased to 0.2% M/M. Energy prices rose 0.4%. Services prices still added 0.5% M/M with shelter an important contributor (0.5% M/M). A 0.3% M/M dynamics for both core and headline measures, suggests that a deceleration to bring inflation sustainably back to the 2.0% target isn’t guaranteed yet. Aside from the higher than expected CPI, weekly jobless claims (202 k) remained at very low levels, suggesting ongoing labour market tightness. Even so, the reaction on US interest rate markets remained modest. Yields briefly jumped into green territory, but the move had no strong momentum. US yields currently are again trading little changed across the curve. Markets still see a >60% chance of a 25 bps Fed rate cut already in March. The US 10-y yield still struggles to hold north the 4.0% barrier (4.03%). Late today, governors Mester and Barkin have a chance to give an instant assessment. The US Treasury will conclude this week’s auctions with the sale of $21 bln 30-y bonds. With few important data scheduled on this side of the Atlantic, German yields are ceding between 4 bps (2-y) and 2.0 bps (30-y). A mild reaction on global bond markets also prevented a sustained decline in major equity indices. The Eurostoxx 50 moved into negative territory post the CPI release, but currently trades little changed. US equites struggle to maintain small opening gains.

On FX, the soft bond market reaction also capped a tentative attempt of the dollar to move higher. The DYX index (102.46) is going nowhere. EUR/USD eased to 1.0950, but first important support at 1.0877 stays out of reach. USD/JPY (146.10) again outperforms; with the pair setting a new YTD top. After a nice rebound of sterling against the euro last week, EUR/GBP today held a tight sideways range, close to, mostly slightly north of the 0.86 big figure.

News & Views

The Czech koruna slipped today. EUR/CZK moved from 24.58 to 24.63 though left intraday highs of around 24.68. CZK weakness followed a big miss in December CPI numbers. The monthly pace dropped from 0.1% in November to -0.4% vs an expected stagnation. This drove the yearly figure down from 7.3% to 6.9%, matching the September 2023 low before inflation accelerated again due to statistical base effects. The CNB was expecting 7%. Core inflation slowed in line with the CNB’s autumn forecast, to 3.6%. The monthly decline was driven by easing prices in domestic fuels (-4.7%), seasonal goods (-2.3%), transport (-1.1%) as well as food (-1.4%). Housing and utility costs inflation decelerated to 0.2%. These carry a big weight in the index. Today’s release brings another CNB rate cut closer in February although the real litmus test will be in January, when companies implement their usual repricing. As the previously mentioned base effects fall out of the equation, however, the CNB expects CPI to drop towards to the upper bound of the 2% +/- 1 ppt target range. Czech swap yields tumble up to 13 bps at the front end of the curve with money markets all but pricing in a 50 bps cut in February. In December last year, the CNB started cautiously with a 25 bps step.

Oil prices jumped towards $78/b (Brent) today. The UK Maritime Trade Operations said an oil tanker was hijacked by people in military-style uniforms before altering course to Iran. It’s a reminder of the tense situation in the broader Middle East region, where frequent attacks by Yemen’s Houthi militants also forced shipping companies to change their usual trajectory via the Red Sea and Suez Canal to go via the much longer route around South Africa. The CEO of a shipping giant responsible for about a fifth of ocean freight said the situation could last for months with implications for global supply. Container freight benchmark rates have risen sharply over the recent weeks. These indicators were closely watched back in the Covid driven supply chain disruption days. While they still trade well below the peak levels back then, freight rates have more than doubled from what were historically more normal levels end 2023.

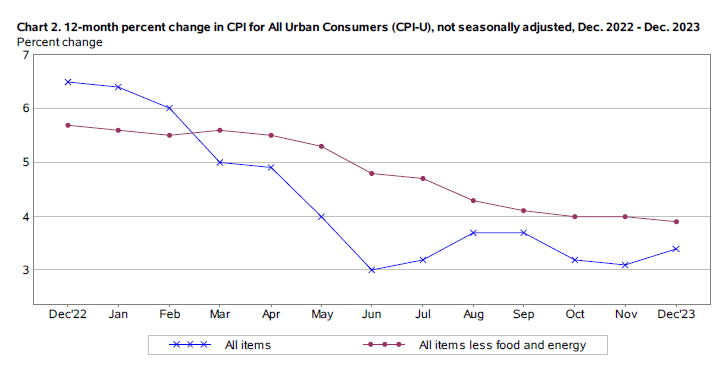

US: Core Inflation Inches Down to 3.9% in December

The Consumer Price Index (CPI) rose 0.3% month-on-month (m/m) in December, ahead of the consensus forecast calling for a more modest gain of 0.1% m/m. CPI rose 3.4% on a year-over-year basis – up from 3.1% in November.

- After having declined in each of the two months prior, energy prices inched higher by 0.4% m/m in December, due to in uptick in electricity costs (1.3% m/m) and slightly higher prices at the pump (+0.2% m/m). Food prices matched last month's gain of 0.2% m/m, pushing the 12-month change down to 2.7%.

Excluding food & energy, core prices rose 0.3% m/m, in line with the consensus forecast. The twelve-month change fell 0.1 percentage points to 3.9% – the slowest pace of growth since May 2021 – while the three-month annualized rate of change dipped to a softer 3.3%.

Core service prices rose 0.4% m/m – a modest deceleration from November's 0.5% gain. Shelter costs were up a 'soft' 0.5% m/m – unchanged from November – as rent of primary residence (+0.4% m/m) and owners' equivalent rent (+0.5% m/m) both notched sizeable gains. Non-housing services decelerated on a monthly basis, but still grew by a relatively strong 0.4%, while the 12-month change continues to hover at an elevated 3.9%.

Goods prices were flat in December, snapping six consecutive months of declines.

Key Implications

No huge surprises in the December CPI report. While the monthly gain on headline inflation came in a touch above expectations, the more important core measure was bang-on consensus. Importantly, both the three-and-six-month annualized rates of change (at 3.3% and 3.2%, respectively) on core sit well below the twelve-month change, suggesting a further deceleration in the months ahead.

Today's inflation report is unlikely to alter the FOMC's near-term policy stance. Although considerable progress on the inflation front has been made over the past year, imbalances in the labor market remain and if left unchecked, threaten to stall the disinflationary process. As a result, Fed officials will likely need to see more compelling evidence that the labor market is cooling, and that inflation remains on a sustained downward path towards 2% before pulling the trigger on rate cuts. This is unlikely to happen until mid-year.

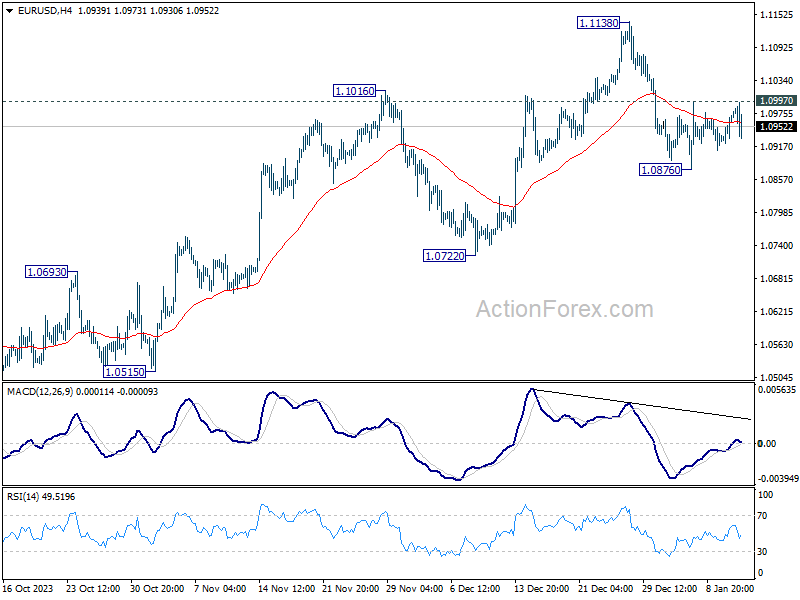

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0939; (P) 1.0957; (R1) 1.0990; More...

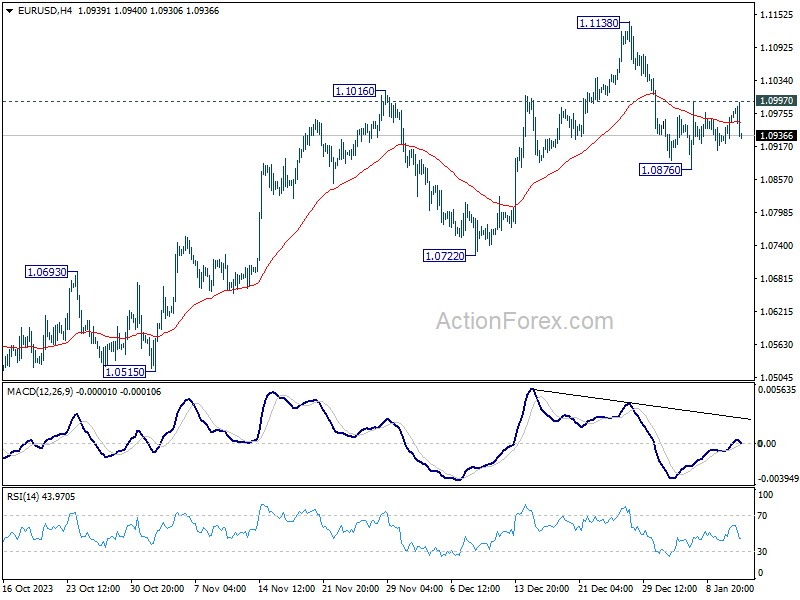

Intraday bias in EUR/USD remains neutral at this point. On the downside break of 1.0876 will resume the fall from 1.1138 short term top to 1.0722 support next. However, break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2704; (P) 1.2724; (R1) 1.2762; More...

Range trading continues in GBP/USD and intraday bias stays neutral for the moment. On the upside, decisive break of 1.2826 high will resume whole rally from 1.2036. Nevertheless, break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8498; (P) 0.8518; (R1) 0.8528; More....

No change in USD/CHF and intraday bias stays neutral. Consolidation from 0.8332 is extending. Stronger recovery cannot be ruled out. But outlook will stay bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, the down trend from 1.0146 (2022 high) is in progress. Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

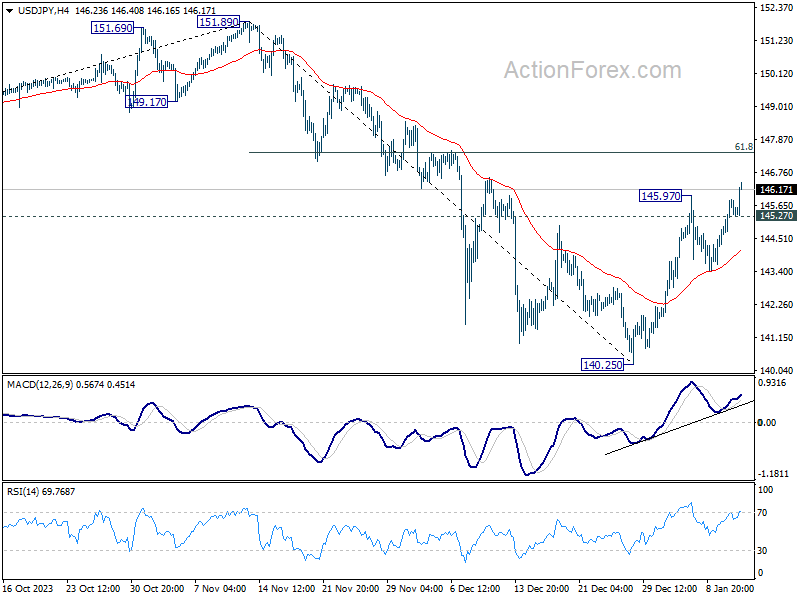

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.78; (P) 145.31; (R1) 146.29; More...

USD/JPY's rebound from 140.25 resumed by breaking through 145.97. Intraday bias is back on the upside for 61.8% retracement of 151.89 to 140.25 at 147.44. Upside should be limited there to bring reversal. On the downside, below 145.27 minor support will turn intraday bias neutral first.

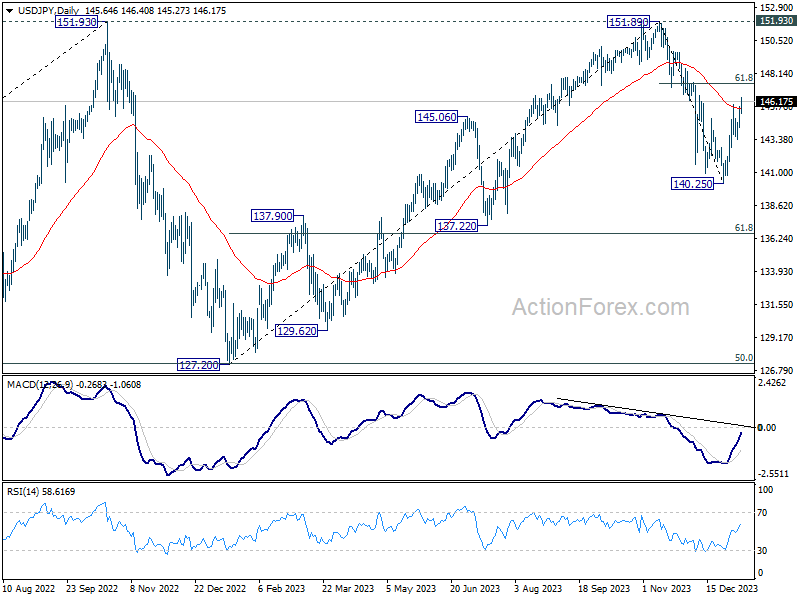

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

Dollar Gains Post-US CPI, But Momentum Subdued

The financial markets' initial reactions to stronger than expected US CPI readings are relatively subdued. While there was an immediate response with Dollar and yields rising, and stock futures dipping, these movements lacked significant follow-through. The exception in the currency markets was USD/JPY, which broke through last week's high. However, this move is attributed to a combination of Dollar's strength and Yen's ongoing weakness. The restrained market response suggests that traders and investors may require more time to reassess their views on Fed's path toward policy loosening and adjust their market positions accordingly.

As for the week, Euro is currently leading as the strongest currency, followed by British Pound and Dollar. However, the greenback holds potential to surpass others and take the top position. Conversely, Japanese Yen remains the weakest performer, with Australian Dollar and New Zealand Dollar also trailing. Swiss Franc is showing signs of weakness against European majors today, indicating a possible shift down in its relative market position.

Technically, EUR/USD's failure to surpass 1.0997 minor resistance earlier today suggests a mild bias towards a potential break below 1.0876 support level. Should this occur, the decline from 1.1138 should then target 1.0722 support. Ideally, for the bearish scenario to strengthen, GBP/USD and AUD/USD should also follow suit, breaking through their respective supports at 1.2611 and 0.6639.

In Europe, at the time of writing, FTSE is down -0.06%. DAX is up 0.05%. CAC is up 0.17%. Germany 10-year yield is up 0.0049 at 2.220. UK 10-year yield is up 0.018 at 3.845. Earlier in Asia, Nikkei surged 1.77%. Hong Kong HSI rose 1.27%. China Shanghai SSE rose 0.31%. Singapore Strait Times rose 0.67%. Japan 10-year yield rose 0.0189 to 0.606.

US CPI rises to 3.4%, CPI core down to 3.9%, both above expectations

In December, US CPI rose 0.3% mom, up from prior month's 0.1% mom, above expectation of 0.2% mom. CPI core (all items less food and energy) rose 0.3% mom, unchanged from prior month's, above expectation of 0.2% mom. Energy index rose 0.4% mom while food index rose 0.2% mom.

For the 12 months period, CPI accelerated from 3.1% yoy to 3.4% yoy, above expectation of 3.2% yoy. CPI core slowed from 4.0% yoy to 3.9% yoy, above expectation of 3.8% yoy. Energy index fell -2.0% yoy while food index rose 2.7% yoy.

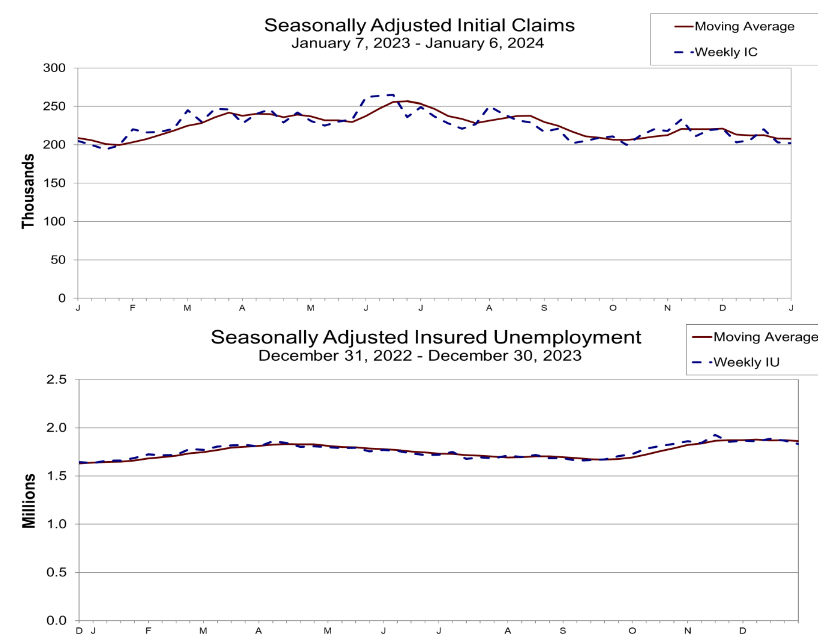

US initial jobless claims down slightly to 202k, vs exp 215k

US initial jobless claims fell -1k to 202k in the week ending January 6, lower than expectation of 215k. Four-week moving average of initial claims fell -250 to 207.75k.

Continuing claims fell -34k to 1834k in the week ending December 30. Four-week moving average of continuing claims fell -8k to 1862k.

BoJ Regional Report: Mixed economic recovery and varied wage hike plans

BoJ's latest Regional Economic Report noted that all nine regions have experienced an uptick in their economies, albeit with variations in pace and extent. This improvement is happening despite challenges posed by the global economic slowdown and domestic price increases. The report categorizes the regional economies as either picking up, recovering moderately, or steadily improving.

Notably, Tokai and Kyushu-Okinawa regions received upgrades in their economic assessments. Kinki region, on the other hand, was downgraded, noted for showing "some weakness in part."

Regarding wages, BoJ report highlights a divergence in approaches among firms. It acknowledges that "some big firms have already announced plans to hike wages this year at or above the pace of last year," suggesting a proactive response to inflation and economic recovery.

However, the situation is not uniform across all business sizes. The report points out that "many firms have yet to firm up their plans on the pace of wage hikes." This uncertainty is particularly pronounced among small and medium-sized enterprises, which remain cautious about increasing wages due to profit constraints.

OECD calls for BoJ rate hike and flexible YCC

OECD has suggested that BoJ should consider implementing a gradual rise in short-term interest rates and introduce more flexibility into its Yield Curve Control policy. This recommendation comes at a time when Japan appears to be at a crucial economic juncture, with inflation trends potentially stabilizing around BoJ's 2% target, a goal set in 2013 but not consistently achieved since then.

In its report, OECD stated, "Japan is at a turning point, with inflation more likely to settle durably around the 2% inflation target than at any time since its inception." To adapt to this changing economic landscape, OECD advised that "greater flexibility in the conduct of yield curve control and a gradual modest increase in the short-term policy interest rate are warranted." This advice is predicated on projections of sustained inflation and evolving wage dynamics in Japan.

However, OECD also issued a cautionary note regarding the uncertainty surrounding Japan's inflation outlook, which it described as "exceptionally large." This uncertainty presents a significant challenge for BoJ as it navigates toward its inflation target. OECD emphasized the delicate balance BoJ must maintain, stating, "The key challenge facing the BoJ is how to durably achieve its inflation target without significantly overshooting."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.78; (P) 145.31; (R1) 146.29; More...

USD/JPY's rebound from 140.25 resumed by breaking through 145.97. Intraday bias is back on the upside for 61.8% retracement of 151.89 to 140.25 at 147.44. Upside should be limited there to bring reversal. On the downside, below 145.27 minor support will turn intraday bias neutral first.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Nov | -10.60% | 8.70% | 8.50% | |

| 00:30 | AUD | Trade Balance (AUD) Dec | 11.44B | 7.50B | 7.13B | 7.66B |

| 05:00 | JPY | Leading Economic Index Nov P | 107.7 | 107.9 | 108.9 | |

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 13:30 | USD | Initial Jobless Claims (Jan 5) | 202K | 215K | 202K | 203K |

| 13:30 | USD | CPI M/M Dec | 0.30% | 0.20% | 0.10% | |

| 13:30 | USD | CPI Y/Y Dec | 3.40% | 3.20% | 3.10% | |

| 13:30 | USD | CPI Core M/M Dec | 0.30% | 0.20% | 0.30% | |

| 13:30 | USD | CPI Core Y/Y Dec | 3.90% | 3.80% | 4.00% | |

| 15:30 | USD | Natural Gas Storage | -120B | -14B |

US initial jobless claims down slightly to 202k, vs exp 215k

US initial jobless claims fell -1k to 202k in the week ending January 6, lower than expectation of 215k. Four-week moving average of initial claims fell -250 to 207.75k.

Continuing claims fell -34k to 1834k in the week ending December 30. Four-week moving average of continuing claims fell -8k to 1862k.

US CPI rises to 3.4%, CPI core down to 3.9%, both above expectations

In December, US CPI rose 0.3% mom, up from prior month's 0.1% mom, above expectation of 0.2% mom. CPI core (all items less food and energy) rose 0.3% mom, unchanged from prior month's, above expectation of 0.2% mom. Energy index rose 0.4% mom while food index rose 0.2% mom.

For the 12 months period, CPI accelerated from 3.1% yoy to 3.4% yoy, above expectation of 3.2% yoy. CPI core slowed from 4.0% yoy to 3.9% yoy, above expectation of 3.8% yoy. Energy index fell -2.0% yoy while food index rose 2.7% yoy.