Sample Category Title

US Headline Inflation Could Rise Modestly from 3.1% to 3.2% in December

Optimism is on the menu ahead of today’s much-awaited US inflation report. The US 10-year yield tipped a toe below the 4% level, the S&P500 came at a spitting distance to the December peak level as technology stocks led gains. Nvidia hit a fresh record, MAMA stocks advanced to an ATH as well, as Meta jumped more than 3.50%.

Optimism in the stock markets will likely continue if today’s US inflation report comes in sufficiently soft. A consensus of analyst estimates on Bloomberg hints that US headline inflation may have gently increased from 3.1% to 3.2% in December, while core inflation has certainly eased from 4% to 3.8% - the slowest pace since May 2021. Data in line, or ideally softer than expected, will keep the Federal Reserve (Fed) doves in charge of the market and could further boost appetite in stocks and bonds. The ongoing tensions in the Red Sea region and the rising cost of moving goods – and their potential impact on consumer prices – will remain on the back of our minds, but disinflation remains the base case scenario for 2024 due to weakening demand, and until there is stronger data-based evidence that the geopolitical situation is bad for inflation, investors won’t let go of the beautiful upside swing that the market caught into last year’s end.

In summary, if inflation data from the US turns out to be suitably mild, it could serve as the final element needed to propel the S&P500 to a new record.

The US dollar is softer across the board this morning. The EURUSD could find a suitable reason to surpass the 1.10 mark, with weak potential to extend gains above this level, however, given the morose economic outlook in the eurozone and the sputtering German growth. The USDJPY rallied past the 145 level as a former Bank of Japan (BoJ) board member said that the BoJ is completely ready to exit the negative rates but that the normalization won’t be like the aggressive ones that we saw in the rest of the developed world; it will likely be very slow instead. Regardless, the upside potential in the USDJPY is seen limited and the long Japanese yen is pointed at as the most obvious trade of the year. But when everyone is looking somewhere, action tends to happen elsewhere.

Exploding debt issuance

Appetite for newly issued bonds is very strong at the start of this year as investors continue to rush into the bond markets in expectation of interest rate cuts. In this context, Spain received a record EUR 130bn of bids for its 10-year bond earlier this week, this Tuesday was also a record day of bond issuance in the primary market across Europe and the US’ $52bn auction for 3-year notes also setlled at 4.10% - some 100bp below the October peak.

Furthermore, the global debt supply will increase in the next few months, with the US, the UK, the Eurozone and Japan due to sell a net $2.1 trillion worth of new bonds to finance their 2024 spending plans. That’s a 7% increase compared to last year. The problem is, the central banks are no longer buying the new government debt – on the contrary, they reduce their massive balance sheets. Therefore, the over-supply of bonds could soon overweigh the rate cut bets – which are already more than fully priced in – and the latter could throw a floor under the bond yields, shift focus to the exploding debt levels and oblige stock investors to look elsewhere to extend the equity rally – like earnings.

Earnings

Big US banks will be going to the earnings confessional today. They are expected to annouce an increase in bad loans, and results will likely be mixed. But overall, earnings expectations are encouraging for the S&P500 stocks, and first results from the semi conductors look encouragin for today’s most hyped AI and chip stocks. Samsung posted its smallest proft decline in the last five quarters and TSM’s Q4 revenue beat estimates of a decline. Yes, it’s not excellent, but it’s encouraging, because at the same time, the global chip sales rose for the first time in more than a year as the chip glut eased, investors expect demand for high performance, AI chips to pick up momentum as every company from L’Oreal to Walmart are now rushing to AI to propose new and more efficient services to their clients, and high estimates point that Nvidia’s sales could go up to $20bn in the latest quarter. So yes, Nvidia keeps climbing like my fave free solo climber Alex Honnold.

Keep selling

Crude oil gains remained limited yesterday as the EIA data posted a surprise 1.3-mio-barrel build in US oil inventories last week – a report that was not in line with the API – and it happens. Oil traders look to sell the tops in an effort to push the price of barrel below the $70pb mark.

All Eyes on US Inflation

In focus today

The most important release today will be the US December CPI. We look for a modest uptick in headline inflation to +0.2% m/m SA (Nov +0.1% m/m) driven mostly by less negative energy contribution while core inflation is set to remain relatively stable at +0.3% m/m SA (Nov +0.3% m/m). The main focus will be on underlying components of inflation, especially on the services sector.

In Sweden, Riksbank vice governor Per Jansson who - as we read it - has shifted from being the most hawkish member to becoming the most dovish member, is scheduled for a speech on the economy and current monetary policy at 15:00 CET.

Economic and market news

What happened overnight: Things were generally quiet overnight, as markets look ahead to the release of the US CPI. On geopolitics, the UN Security Council has passed a resolution that calls for an immediate stop to the Houthi attacks on Red Sea vessels. The Nikkei 225, Japan's benchmark equity index, had another strong day. As of this morning, it was up by 2%, hitting a 34-year high. Bitcoin found support on the back of the US Securities and Exchange Commission approving ETFs holding the digital asset.

What happened yesterday: Markets continued to temper expectations on a March rate cut by the ECB, after ECB Vice-President Guindos said in a speech that he expected the pace of disinflation to "slow down in 2024, and to pause temporarily at the beginning of the year", and ECB member Isabel Schnabel said it was "too early to discuss rate cuts" in a Q&A on X. In December, a March-cut was fully priced in, while markets now attach a 40% probability of a cut. We stick to our expectations of a first rate cut in June.

The yen continued to weaken against major currencies during yesterday's session, with USD/JPY breaking above the 145 level after data showed weak wage growth in November.

We got a range of Scandinavian data yesterday. In Sweden, November data showed the GDP indicator advancing (+0.2 % mom) for the second month in a row, suggesting the Q4 print will eventually show an expanding economy. That said, retail sales, consumption and production all fell back, but note October data instead was revised higher. Norwegian core inflation was slightly lower than expected at 5.5% y/y (consensus: 5.6%). The initial market reactions were fairly muted with EUR/NOK continuing to trade around the 11.30 mark. In Denmark, headline inflation was 0.7% y/y in December, with food prices in particular posing a drag.

Equities: Risk appetite picked up a bit on Wednesday. Equities were generally higher, led by the US (S&P 0.6% vs Stoxx 600 -0.2%). The reason for the US outperformance was once again a growth-driven preference. Again, big tech were the stand-outs. This was not an overly risky session. Other cyclicals, such as industrials, materials and banks, did only okay. Likewise, small caps continued to underperform. The wait-and-see mode will be over today as US inflation figures are due and earnings results kick off tomorrow. US futures are slightly higher into the numbers. The Japanese rally continues, with Nikkei 225 gaining another 2% this morning (+5% so far this year!).

FI: Global yields ended marginally higher in a quite uneventful macro session. The high level of issuance remains a main driver for FI markets these days. Short-end EGB yields rose as the pricing of ECB rate cuts in 2024 continues to fade, while the long end of the curve was close to unchanged. The 5Y5Y EUR inflation swap rate faded some 3bp as prices for natural gas and oil continued declining.

FX: Yesterday's FX session was primarily characterised by the weakening of the JPY amid higher rates and disappointing Japanese data. The EUR was among the best performers yet EUR/USD remained below the 1.10 figure. In the Scandies both EUR/NOK and EUR/SEK ended the sessions slightly higher.

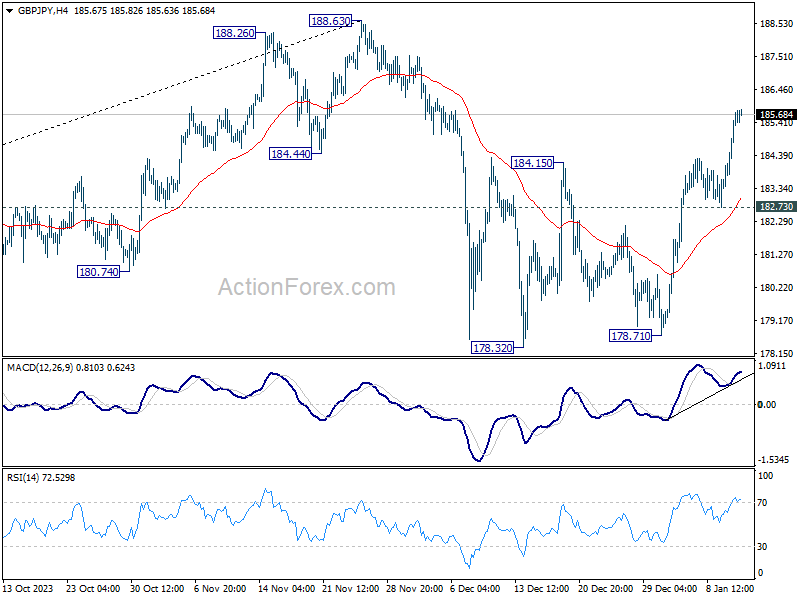

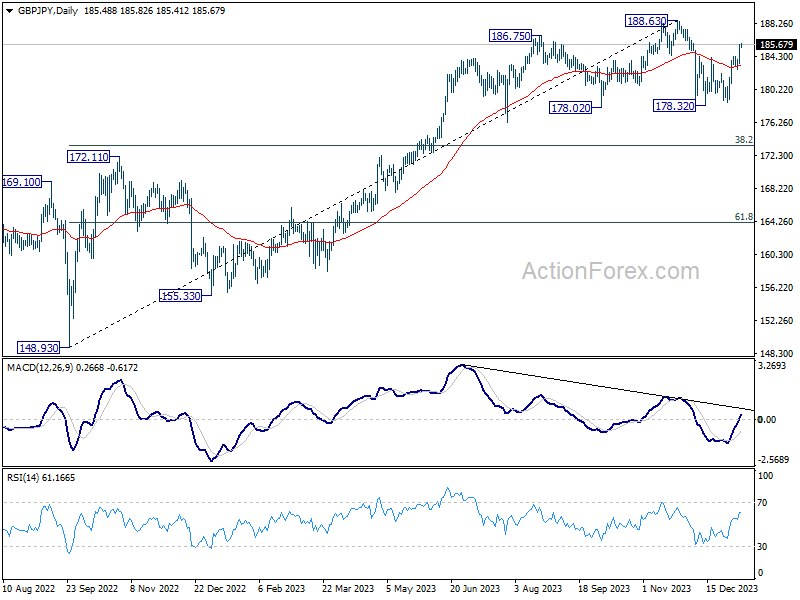

GBP/JPY Daily Outlook

Intraday bias in GBP/JPY remains on the upside at this point. Rebound from 178.32 is in progress for retesting 188.63 high. On the downside, break of 182.73 support is needed to indicate completion of the rebound. Otherwise, further rally will remain in favor in case of retreat.

In the bigger picture, price actions from 188.63 medium term top are seen as a correction to the up trend from 148.93 (2022 low) only. As long as 172.11 resistance turned support holds, larger up trend from 123.94 (2020 low) is still in favor to resume through 188.63 at a later stage.

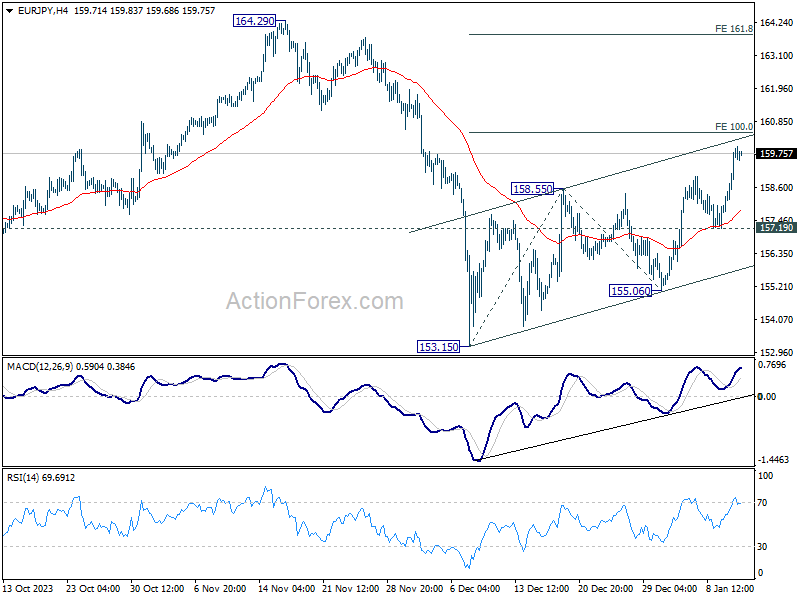

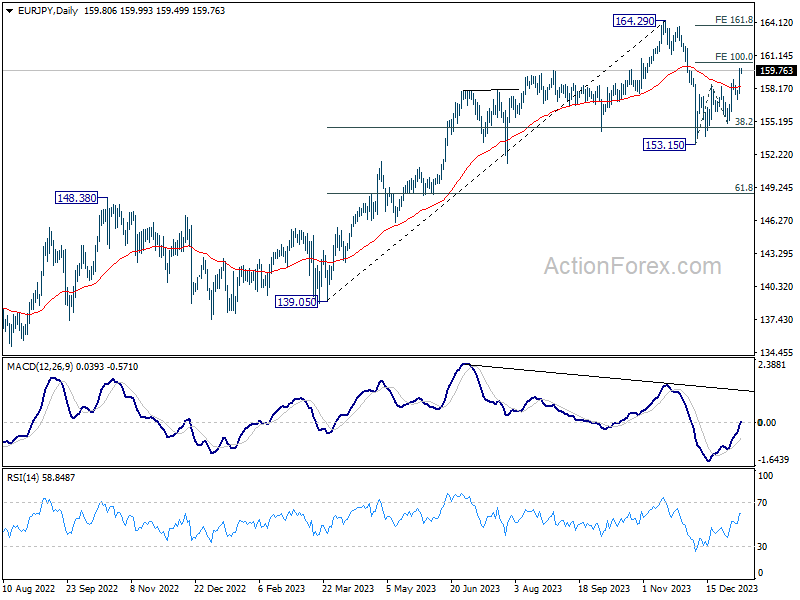

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.47; (P) 159.22; (R1) 160.68; More...

Intraday bias in EUR/JPY stays on the upside at this point. Current rebound from 153.15 is in progress for 100% projection of 153.15 to 158.55 from 155.06 at 160.46. Firm break there will target 161.8% projection at 163.79. For now, further rise will remain in favor as long as 157.19 support holds, in case of retreat.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

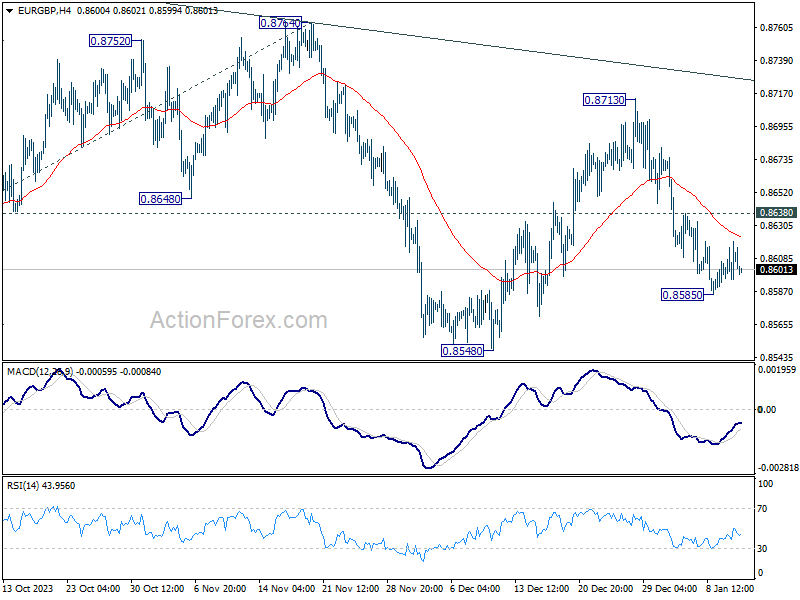

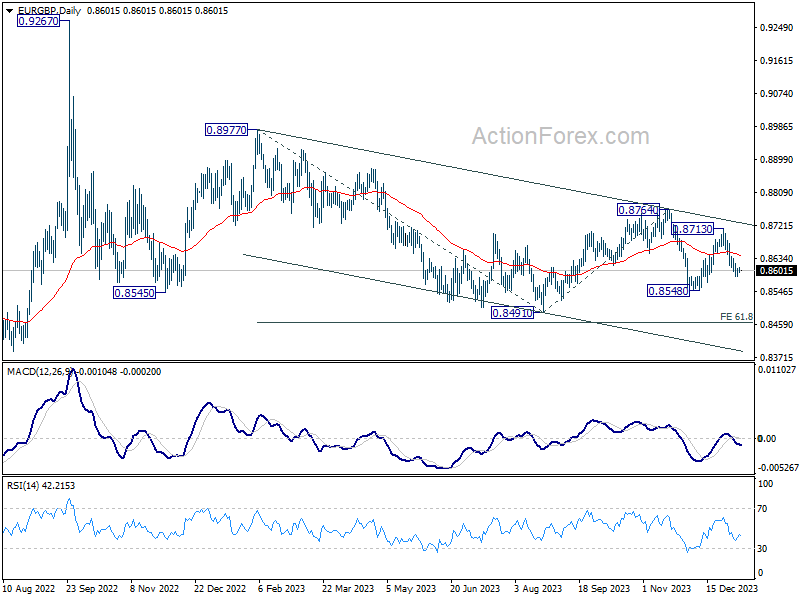

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8598; (P) 0.8609; (R1) 0.8623; More...

Intraday bias in EUR/GBP remains neutral for the moment. Further decline is in favor with 0.8638 minor resistance intact. On the downside, break of 0.8585 will resume the fall from 0.8713 to 0.8548 support first. Break there will target 0.8491 low next. However, break of 0.8638 will turn bias to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8764 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

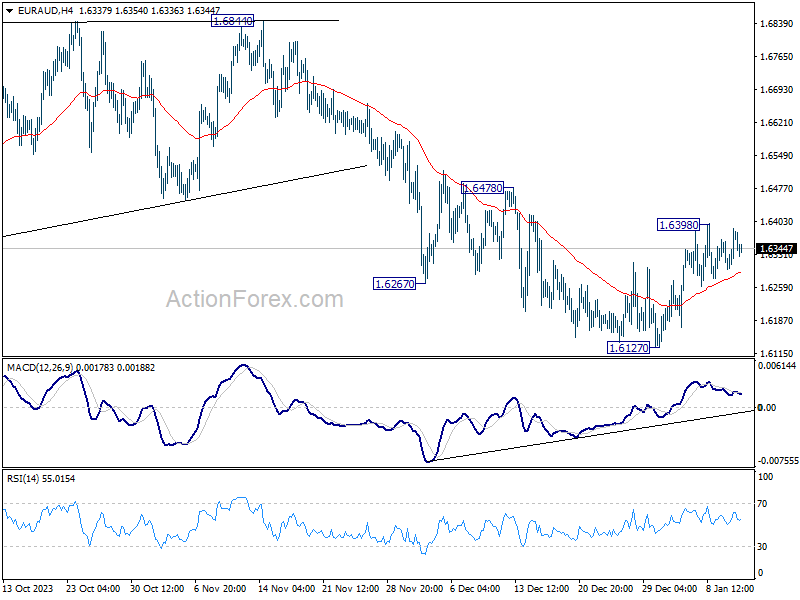

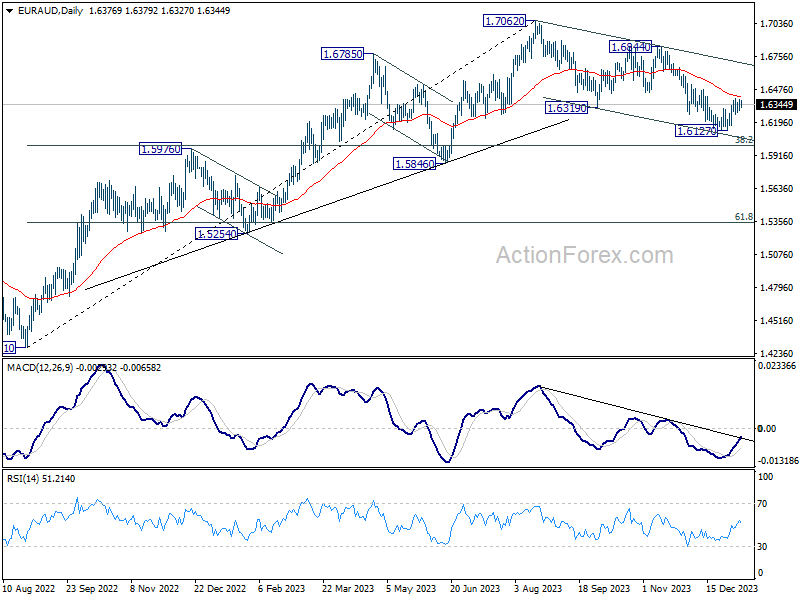

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6297; (P) 1.6331; (R1) 1.6382; More...

Intraday bias in EUR/AUD remains neutral and risk stays on the upside as long as 1.6127 support holds. Above 1.6398 will resume the rebound to 1.6478 resistance. Firm break there will argue that whole correction from 1.7062 has completed, and target 1.6844 resistance for confirmation. Nevertheless, break of 1.6127 will resume the corrective fall to 1.6000 fibonacci level.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 bring rebound. Break of 1.6844 will argue that this up trend is ready to resume through 1.7062 high.

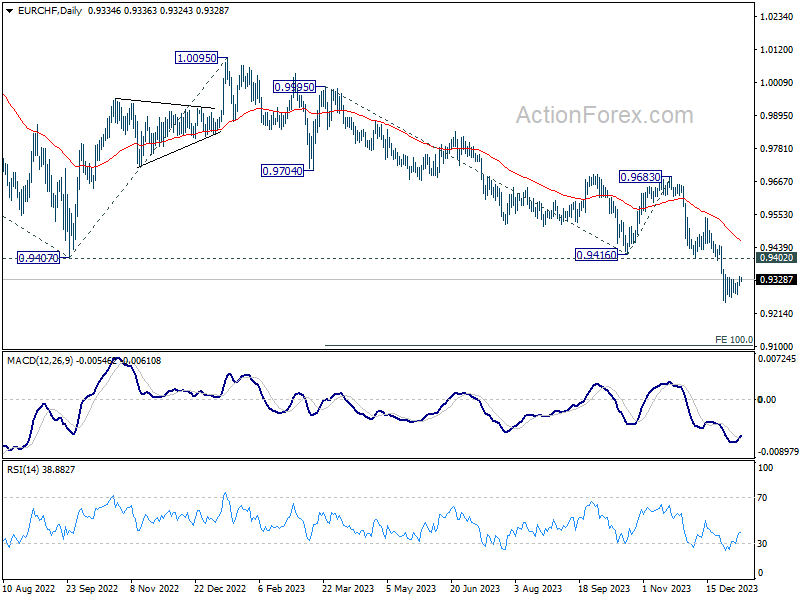

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9317; (P) 0.9331; (R1) 0.9349; More...

No change in EUR/CHF's outlook as consolidation from 0.9252 is still in progress. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 0.9402 support turned resistance holds. On the downside, break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

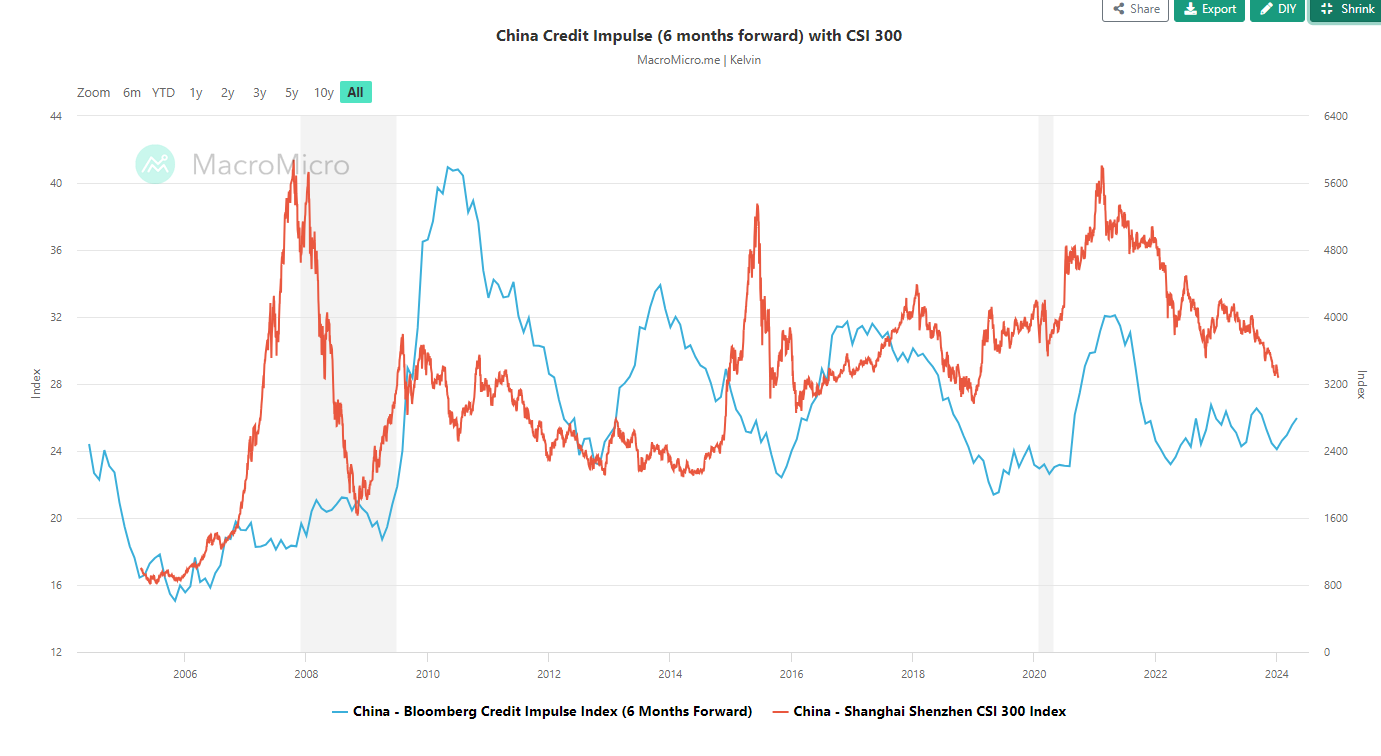

Easing Liquidity Conditions May Provide Interim Support for China and Hong Kong Stock Markets

- China’s credit impulse has remained on a slow upward trajectory since July 2023.

- Key China’s central bank (PBoC) official has signalled a further accommodating monetary policy in 2024.

- Growth in China’s services activities expanded in December 2023.

- Watch the 16,100 key long-term secular support on the Hang Seng Index.

China and Hong Kong stock markets have been in the doldrums for the past four years since the pandemic crisis added by a heightened deflationary risk inflicted on China’s economy due to persistent weakness in the property market in the past two years.

Both have started the new year on a weak footing with China’s CSI 300 benchmark stock index slipping to a year-to-date loss of -4.2% at this time of the writing and hitting its lowest level since 2018. Similar dismal performances are seen in the Hong Kong stock market; Hang Seng Index (-4.2%), Hang Seng Tech Index (-7.3%), and Hang Seng China Enterprises Index (-4.6%) over a similar period.

Despite the lingering risk of the entrenched deflationary spiral, ongoing corruption, and regulatory clampdowns in China’s private and public sectors that spooked foreign investors, there has been some sign of “economic light shining in the dark tunnel”; the official NBS Non-Manufacturing PMI and Caixin Services PMI for December indicated a slight growth uptick in services activities for December with new orders grew the most in seven months in the report compiled by Caixin.

Secondly, the Bloomberg Credit Impulse Index for China, a measurement of credit/liquidity growth has been on a slow upward trajectory since July 2023 (24.10 in July to 25.97 printed on November 2023).

China’s credit impulse is on the rise

Fig 1: Bloomberg China Credit Impulse Index & CSI 300 as of 11 Jan 2024 (Source: Macro Micro, click to enlarge chart)

Interestingly, if we shift the Bloomberg Credit Impulse Index for China six months forward, its movement does exhibit a direct correlation with the CSI 300 Index which implies a continuation uptick in credit impulse may translate to a similar upward directional movement in the CSI 300 going forward (see Fig 1).

In addition, a key China’s central bank (PBoC) official signalled earlier this week that PBoC may lower the reverse ratio requirements for Chinese banks in 2024 which translates to a potential further accommodative monetary policy stance. Also, the downside pressure inflicted on the yuan via an accommodating monetary policy is likely to be reduced in 2024 as the US central bank, the Fed may start to embark on a dovish pivot path for interest rate cuts in the US.

Hence, it may lead to a further rebound in credit impulse which in turn stokes potential bullish short-term animal spirits back into the China and Hong Kong stock markets.

16,100 remains the key long-term secular support on the Hang Seng Index

Fig 2: Hang Seng Index long-term secular trend as of 11 Jan 2024 (Source: TradingView, click to enlarge chart)

The ongoing weakness seen in the Hang Seng Index (HSI) has managed to be contained above the 16,100 key long-term secular pivot support which is defined by its ascending trendline that led to a prior significant recovery after every major bearish correction since August 1998, the onslaught inflicted by the Asian Financial Crisis.

To see a much more potentially heightened bullish animal spirits feedback loop in the Hong Kong stock market, the HSI needs to clear above its major resistance at 18,460 which is the descending trendline in place since the February 2021 major swing high where the two important events took shaped around that period; the strict business practices regulations imposed on China Big Tech firms and a series of Covid related lock-down measures enacted in China.

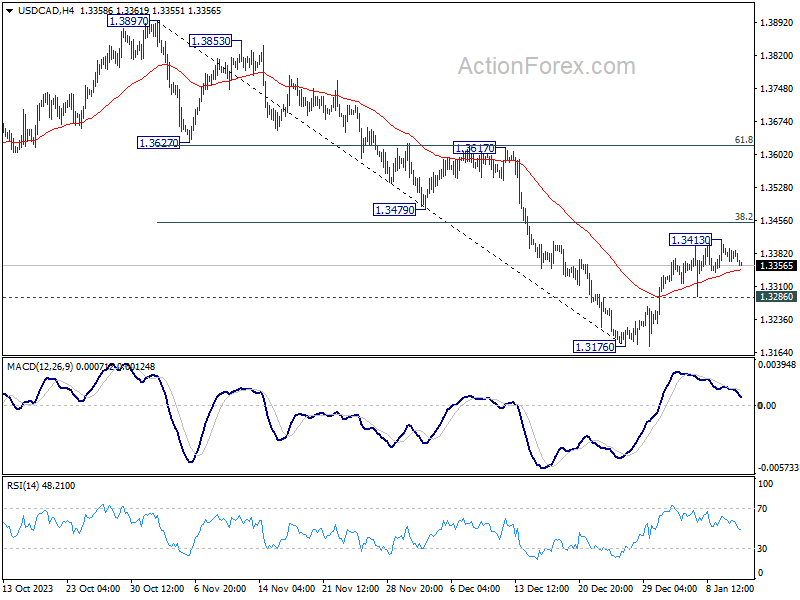

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3363; (P) 1.3383; (R1) 1.3399; More...

Intraday bias in USD/CAD is turned neutral with current retreat. But further rally is in favor as long as 1.3286 minor support holds. Above 1.3413 will resume the rebound from 1.3176 to 38.2% retracement of 1.3897 to 1.3176 at 1.3451. Firm break there will pave the way to 61.8% retracement at 1.3622. On the downside, however, break of 1.3286 will turn bias back to the downside for 1.3176 low instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. While fall from 1.3897 could still extend through 1.3091, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage.

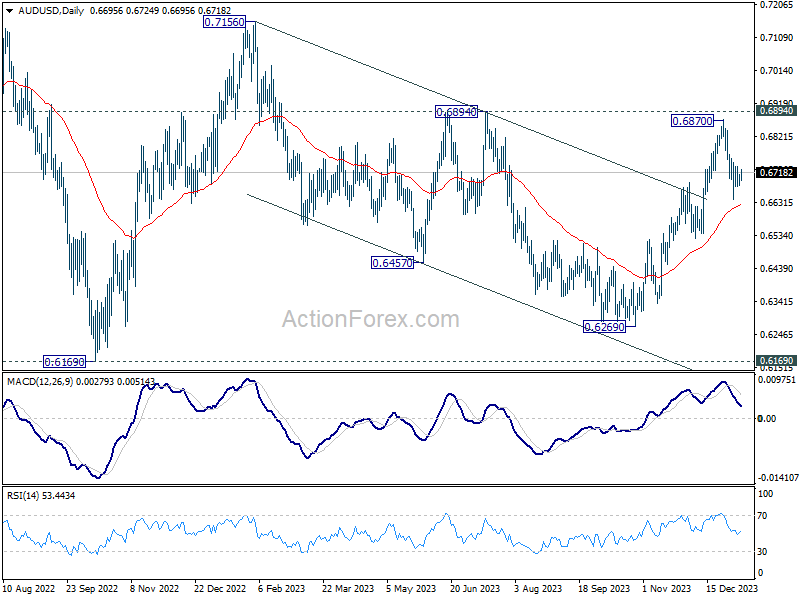

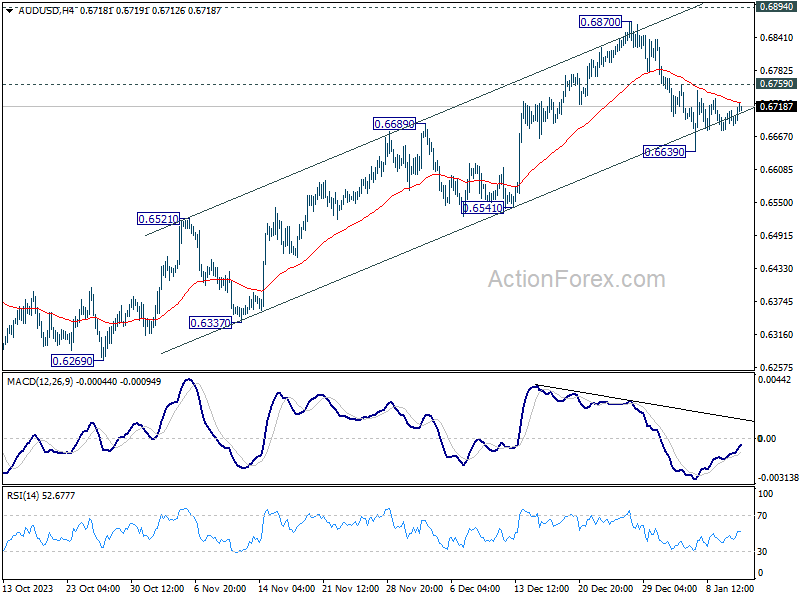

AUD/USD Daily Report

Daily Pivots: (S1) 0.6682; (P) 0.6698; (R1) 0.6715; More...

Intraday bias in AUD/USD remains neutral and outlook is unchanged. On the downside, break of 0.6639 will resume the fall from 0.6870 short term top to 0.6541 support next. On the upside, though, break of 0.6759 minor resistance will suggest that the pull back has completed already. Intraday bias will be turned back to the upside for 0.6870 resistance.

In the bigger picture, price actions from 0.6169 (2022 low) could be just a medium term corrective pattern to the down trend from 0.8006 (2021 high). Rise from 0.6269 is seen as the third leg of the pattern that could target 0.7156 on break of 0.6894 resistance. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.