Sample Category Title

U.K. Slowdown Could Hasten BoE Easing, But By How Much?

Summary

- The U.K. economic environment remains challenging, with Q3 GDP contracting slightly and the fourth quarter starting on a subdued note. Even with some improvement in consumer fundamentals and sentiment surveys, we believe a mild technical recession for the U.K. remains more likely than not.

- Stubborn persistence in U.K. price and wage inflation has started to break, with both prices and wages surprising to the downside in recent months. While these are clearly welcome developments, wage inflation is likely still too high to sustainably achieve the central bank's 2% inflation target, and it's not yet clear how long the more muted pace of price increases will persist.

- The U.K. growth and inflation slowdown suggests the risks are tilted towards an earlier rate cut than our current base case of the August meeting. An initial rate cut could perhaps come in June, possibly May.

- Nonetheless, we still think the risks are tilted towards more gradual easing than reflected in current market pricing, which already sees around a 75% chance of an initial rate cut by the time of the May meeting. Against this backdrop, we think U.K. bond yields could drift higher from current levels. It could also mean moderate gains in the pound against the U.S. dollar as 2024 progresses, especially if—as we expect—the U.S. economy moderates and the Fed eases monetary policy as well.

U.K. Economy Flirting With Recession

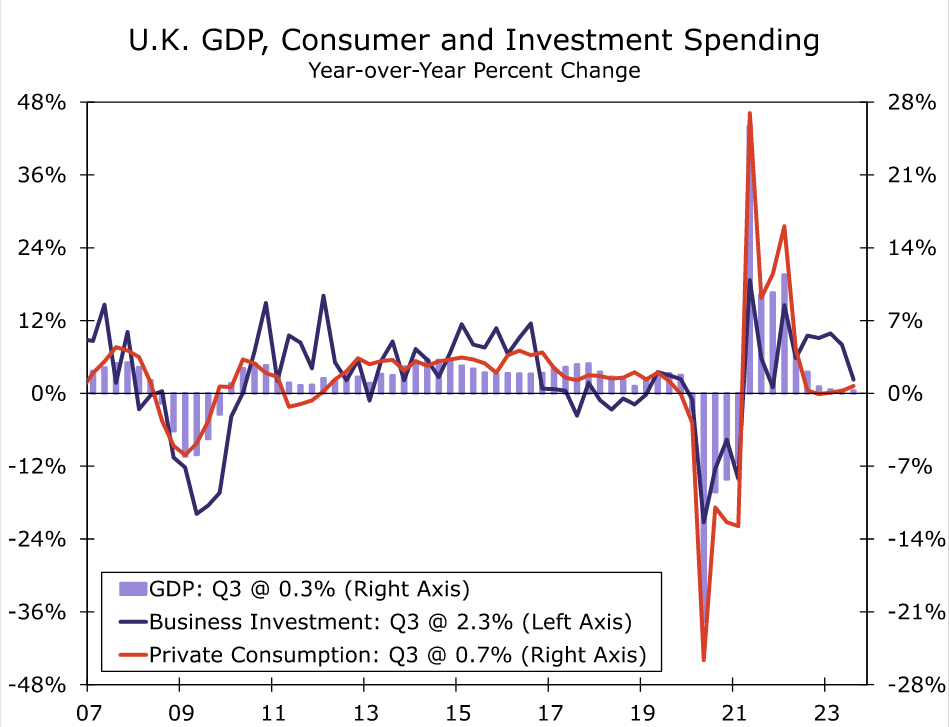

Recent data have highlighted the challenging environment still facing the U.K economy. After avoiding the threat of contraction over the past few quarters, revised data for Q3-2023 GDP showed the economy finally shrank by 0.1% quarter-over-quarter, compared to the previously reported flat outcome. The downward revision was due in part to consumer spending which fell 0.5%, a larger than initially reported decline, while exports were revised to show a modest fall in Q3. Finally, with downward revisions also evident in prior quarters, Q3 GDP rose just 0.3% year-over-year, down from an initially reported 0.6% increase.

The final quarter of 2023 started on an equally soft footing. For October, U.K. GDP fell a larger-than-forecast 0.3% month-over-month, as services activity fell 0.2% and industrial output fell 0.8%. While unusually wet weather likely crimped activity in some sectors, the level of October GDP was still 0.1% below its Q3 average. That suggests the U.K. is still dangerously close to a (mild) technical recession—that is, two consecutive quarters of negative GDP growth.

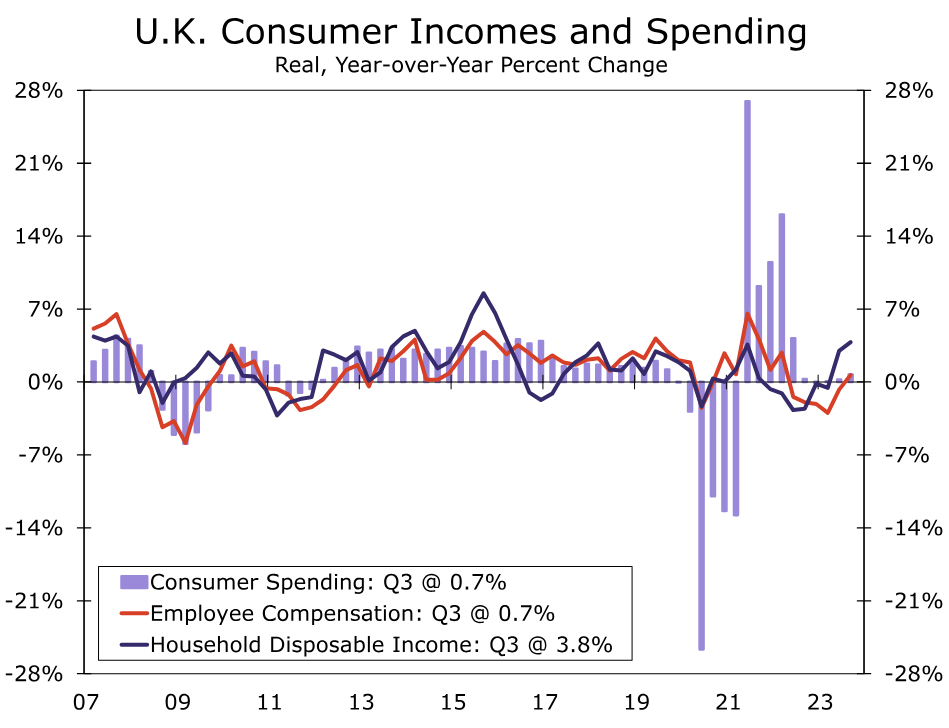

While a technical recession is possible and, indeed, perhaps more likely than not, such a downturn is not yet inevitable. Consumer fundamentals, while mixed, hint that the worst of the U.K consumer slowdown may be behind us. For the third quarter the rise in nominal household incomes outpaced the increase in prices, meaning that Q3 real household disposable income rose 0.4% quarter-over-quarter and is now up 3.8% year-over-year. Combined with subdued consumer spending, that also led to an increase in the household savings rate to 10.1% of disposable income in Q3. The savings rate is up from 9.5% in Q2, and well above the levels that prevailed prior to the pandemic. On a less encouraging note, and something of an offset to these improving fundamentals, the Bank of England's interest rate hikes are increasingly flowing through to household budgets and cash flows. For Q3-2023, interest costs represented 5.5% of household income, around four times the1.4% of income as recently as Q3-2021. Still, considering the improving trends in real incomes and household savings, further declines in U.K. consumer spending may be limited, even given the backdrop of sharply higher interest rates over the past several quarters.

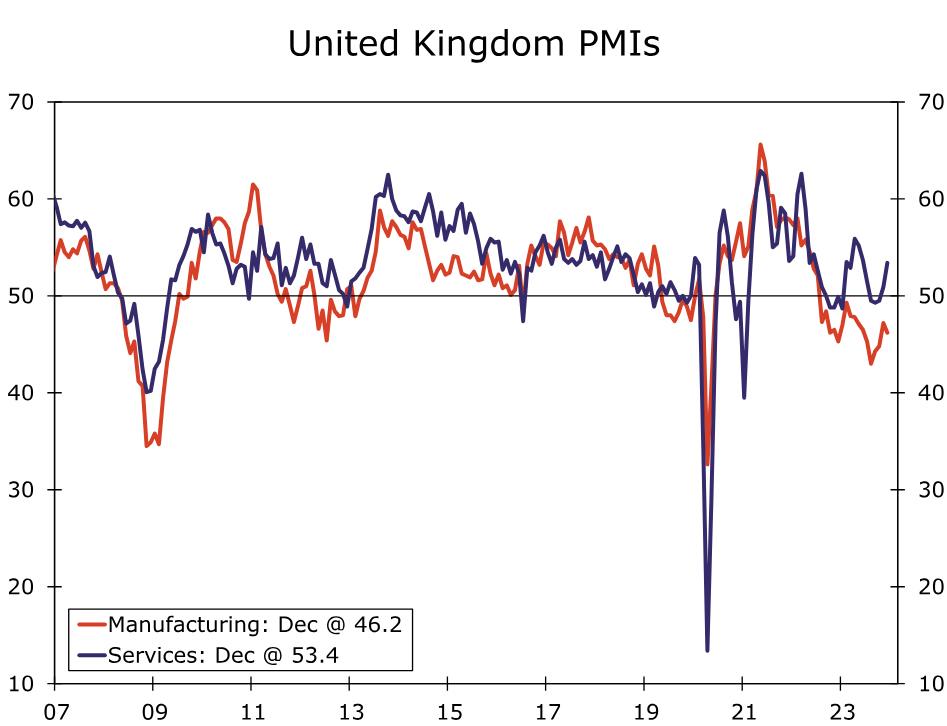

Sentiment surveys also offer hope that the U.K. economy could end the fourth quarter on a better note than it started. The U.K. manufacturing PMI slipped to 46.2 in December, and has been contraction territory since mid-2022. However, for the more economically dominant service sector, the services PMI has improved in recent months. The U.K. services PMI rose to 53.4 in December, a level consistent with moderate expansion. Overall, recent economic indicators are mixed, and we still lean towards a mild U.K. recession. But regardless of whether that recession occurs, our outlook for the U.K. economy is decidedly subpar. Our base case forecast is for U.K. GDP growth of 0.5% in 2023 and 0.1% for 2024, even if improving sentiment surveys hint at modest upside risk to the 2024 outlook.

U.K. Inflation Fever Is Breaking

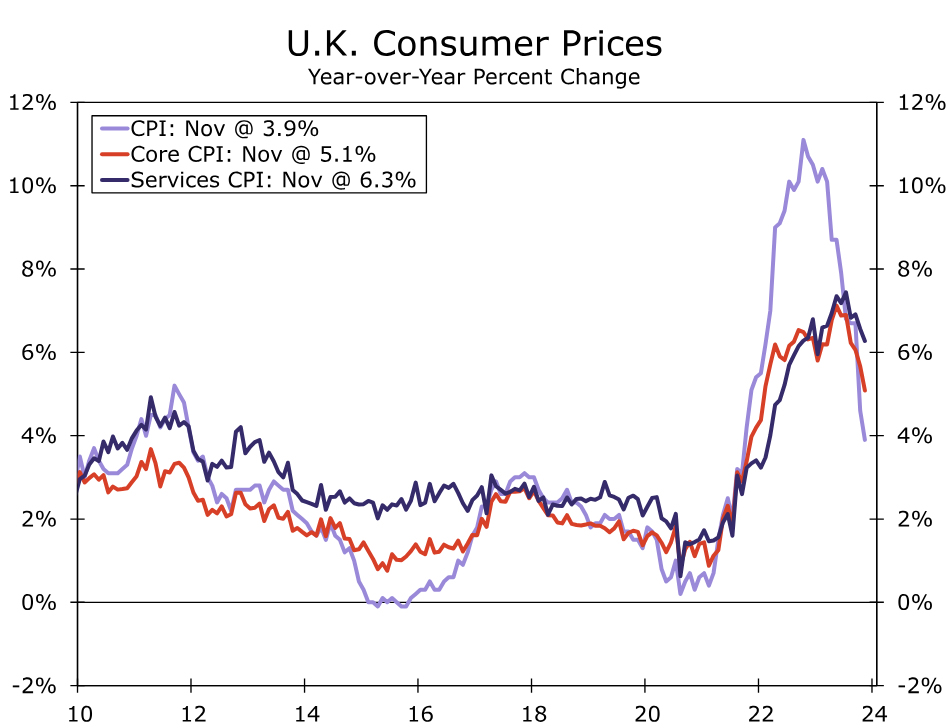

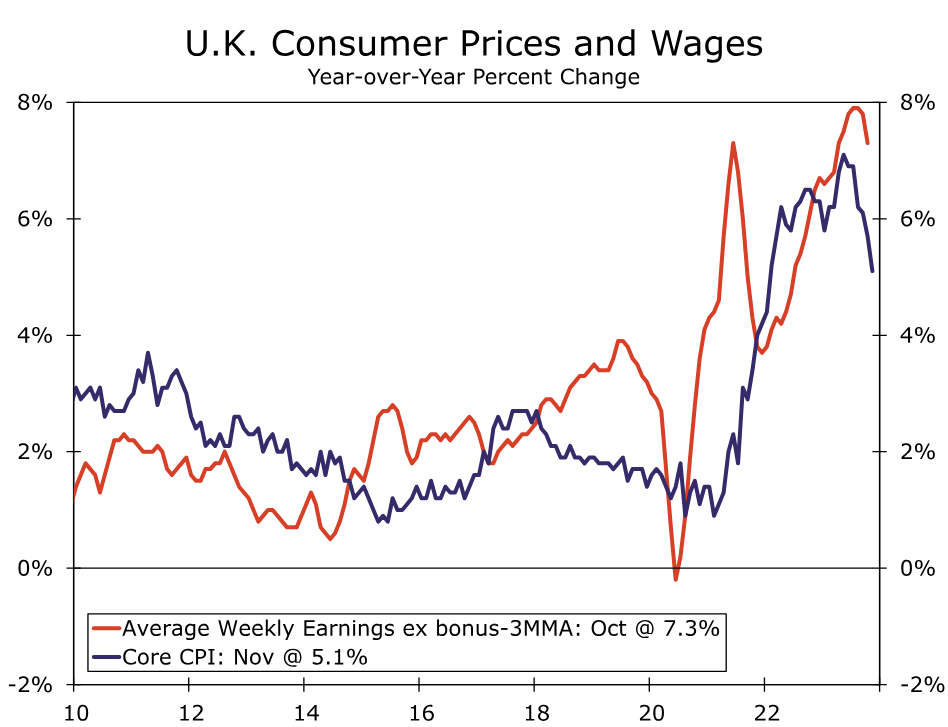

Just as U.K. economic growth has apparently come under increasing pressure, a more welcome development has been a significant improvement in U.K. inflation trends. U.K. price inflation and wage inflation trends have been stubbornly elevated for an extended period, and more so than for peer economies such as the Eurozone and United States. In recent months, however, the U.K. has started to enjoy favorable surprises on the price and wage front, at least as it pertains in returning CPI inflation towards its 2% inflation target. For November, U.K. headline inflation slowed more than forecast to 3.9% year-over-year, the slowest pace since late 2021. U.K. core inflation and services inflation similarly surprised to the downside, slowing to 5.1% and 6.3% respectively. In fact, we estimate that on a three-month annualized basis the U.K. core CPI has slowed below a 2% pace, although it is not yet clear that muted rate of price increase will continue.

In addition, stubbornly persistent wage growth has also shown some signs of easing in recent months. In particular, growth in average weekly earnings slowed more than expected to 7.2% year-over-year for the three months to October, while growth in average weekly earnings excluding bonuses slowed to 7.3% for the same period. While that slower wage growth is clearly a welcome development from an inflation-fighting perspective, for now the pace of wage growth is probably still at a level that is inconsistent with CPI inflation returning to and staying at the 2% target over a long term horizon.

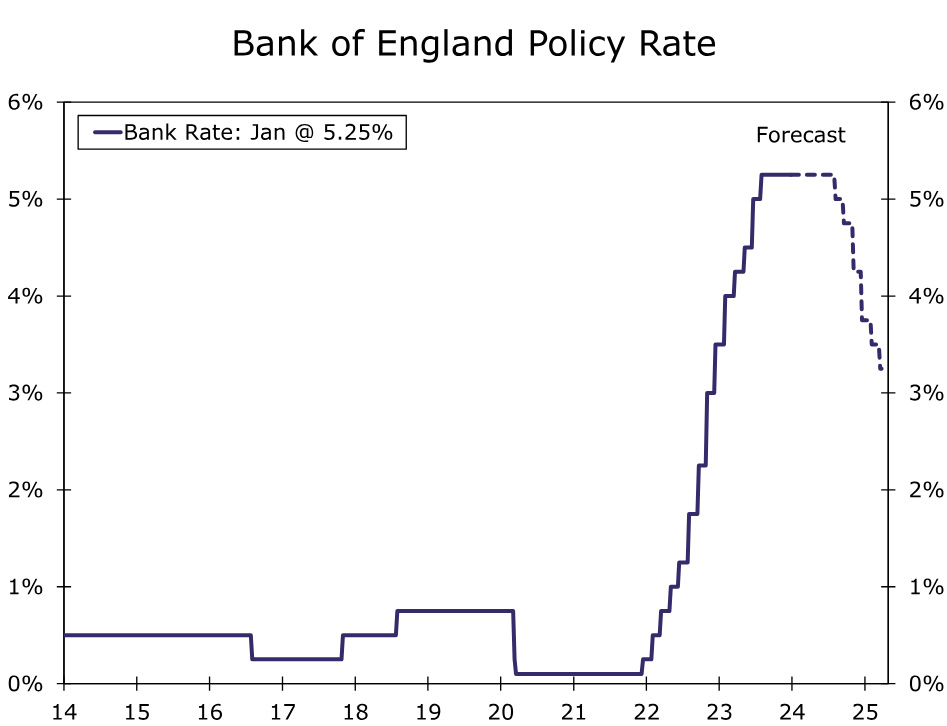

Before the most recent slowing and in U.K. growth and inflation, and amid a backdrop of hawkish comments from Bank of England (BoE) policymakers who had pledged to keep interest rates “higher for longer”, we took the opportunity to adjust our BoE monetary policy outlook, anticipating a later initial rate cut in August. That timing adjustment now appears to be somewhat inopportune, and the latest deceleration in the U.K. economy could still elicit earlier rather than later Bank of England monetary easing.

Nonetheless, the outlook remains quite uncertain at this point. As we highlighted above, it is not clear how long the recent muted pace of price increases will last, and we still view the current level of wage inflation as inconsistent with achieving the 2% inflation target on a sustainable basis, suggesting that even with the softening in U.K. data, BoE rate cuts are not imminent. That is, BoE rate cuts could occur earlier than our base case of the August meeting, but not much earlier—perhaps June, and certainly no earlier than May. The BoE's monetary policy announcement on 1 February, which will include updated policy guidance and economic projections in the accompanying Inflation Report, should provide further clarity into the outlook for U.K. monetary policy. That is, whether an initial August rate cut still seems likely, or a June or May cut seem more probable.

Even if the outlook is not entirely certain, we still believe the risks are tilted towards more gradual easing than market participants currently expect. At this time a May BoE rate cut is already 75% priced in by market participants. While we think an initial cut in May is possible, we also think initial moves in June or August also remain in play. The risk of more gradual Bank of England easing than currently expected by market participants could see U.K. bond yields drift higher from current levels. Higher bond yields and gradual easing could also see moderate gains in the pound against the U.S. dollar as 2024 progresses, especially if—as we expect—the U.S. economy moderates and the Fed eases monetary policy as well.

Will US CPIs Help Dollar Extend Its Recovery?

- Dollar’s recovery pauses after NFP and ISM data

- Investors continue to price in aggressive rate cuts by the Fed

- Attention now turns to CPI inflation on Thursday, at 13:30 GMT

- Will the dollar resume its upside trajectory?

Friday’s data halt the dollar’s rebound

The dollar entered the new year on a strong footing, but soon after the US jobs data was out, its march north came to a halt. The world’s reserve currency extended its rally at the time the better-than-expected headline numbers were out, but after digging into the details of the report, they abandoned their long dollar positions as the story was not as exciting as they initially thought.

The December payrolls may have well beat the consensus, but the October and November numbers were revised down by a combined 71k. On top of that, although the unemployment rate held steady and did not rise as anticipated, the labor force participation rate slid, which means that fewer unemployed Americans are encouraged to start actively looking for a job.

What pushed the greenback even lower was the ISM non-manufacturing PMI for the same month, which fell to the lowest reading since May. More importantly, the survey’s employment sub-index tumbled from 50.7 to 43.3, the lowest since July 2020, when the globe had to deal with the first wave of the coronavirus pandemic.

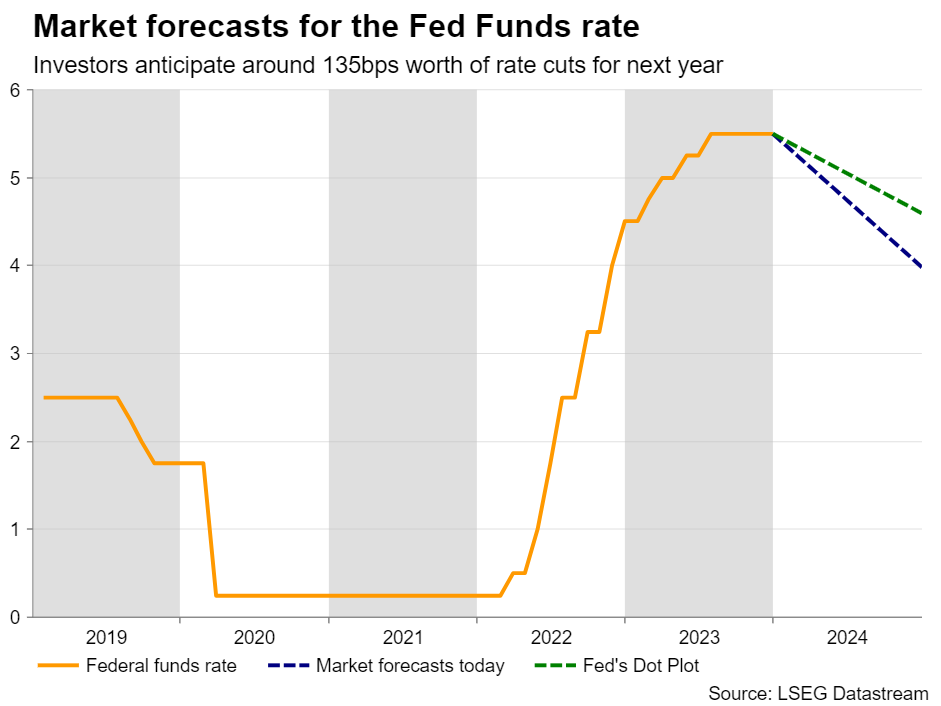

Investors still see a decent chance for a March rate cut

All these economic numbers allowed market participants to maintain bets of aggressive rate cuts by the Fed, and a nearly 70% probability that the first quarter-point reduction will be delivered in March, despite the Fed pointing to much fewer reductions through its December dot plot and the minutes of that meeting revealing that most policymakers wanted to keep borrowing costs high “for some time.”

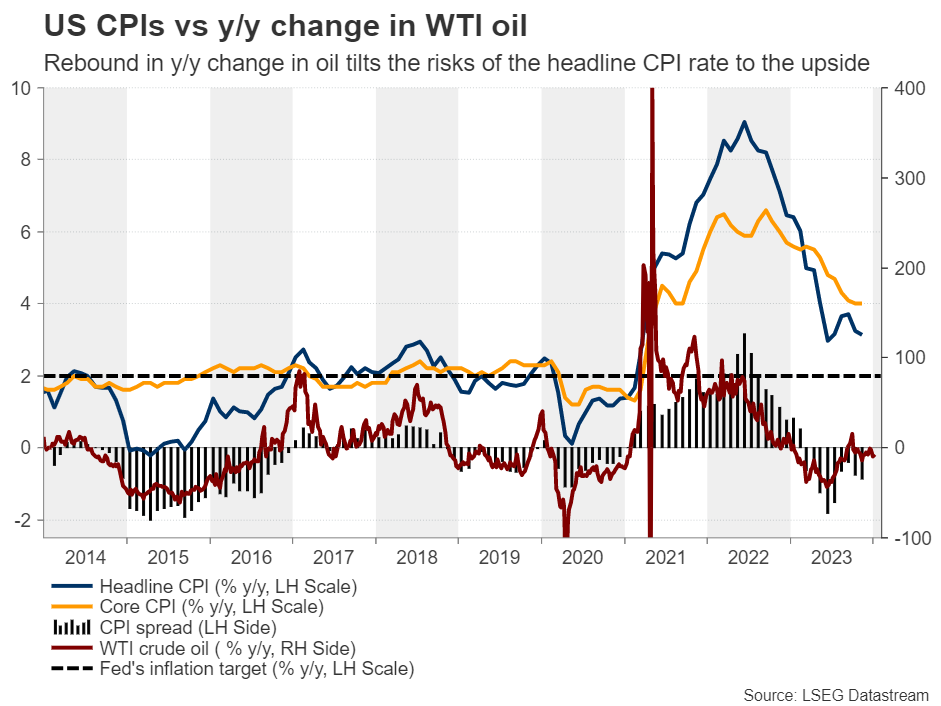

Base effects suggest a rebound in headline inflation

Now, the next release that will lock dollar traders in front of their screens will most likely be the US CPI numbers for December, due out on Thursday. Inflation has come down quickly in recent months due to weaker goods prices and moderating costs of services, including travel, even as rent increases remained elevated. Headline inflation saw a faster slowdown than underlying price pressures as energy prices began drifting south in September, erasing nearly all the gains posted during the summer months.

However, with the 2022 downtrend now dropping out of the year-on-year calculation, oil prices are close to their opening levels for 2023, which means that the y/y change has moved from well into negative territory close to zero. And with the headline CPI rate resting well below the core one, even if the latter softens a bit more, this means that there are risks for a rebound in headline inflation. Indeed, the forecasts support this logic. Although the core rate is expected to have declined to 3.8% y/y from 4.0%, the headline one is seen ticking up to 3.2% y/y from 3.1%.

Will a higher CPI recharge the greenback’s engines?

Ergo, a rebound in the headline CPI rate and a core one still nearly double the Fed’s objective may convince investors to push back their bets regarding a March rate reduction, even if they don’t materially reduce the total amount of basis points expected to be cut by the end of the year. This could allow the dollar to rebound as Treasury yields continue to recover.

From a technical standpoint, the dollar’s comeback at the turn of the year has resulted in a strong downside correction in aussie/dollar, and a rebound in US inflation may allow that retreat to continue for a while longer. However, with the price structure still pointing to higher highs and higher lows above the uptrend line drawn from the low of October 26, and with the RBA expected to cut interest rates by only 40bps by the end of the year, calling for a bearish reversal in this exchange rate may be unwise and premature.

If the setback continues, the bulls may find the 0.6570 zone an attractive entry point for resuming the prevailing near-term uptrend. However, in case the CPI figures miss their forecasts, the correction may come to an end sooner as the bulls become willing to jump into the game at even higher levels.

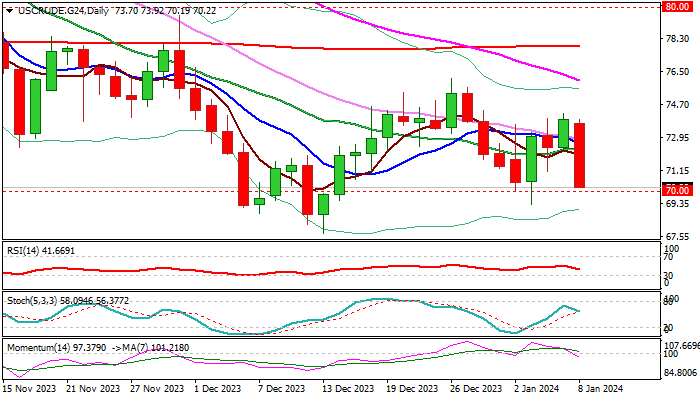

WTI Oil Price Falls Sharply, On Track for Biggest Daily Loss Since Mid-November

WTI oil price fell nearly 5% on Monday, deflated by decision of top oil exporter, Saudi Arabia, to cut February selling price to Asia to the lowest in over two years and rise in OPEC output.

The measures partially counter persisting supply fears over rising geopolitical tensions in the Middle East and may limit the latest price drop.

Fresh weakness has so far retraced the largest part of last week’s $69.27/$74.22 recovery leg and pressuring psychological $70 support.

Loss of pivots at $70/$69.27 (psychological / Jan 3 low) would further weaken near-term structure on completion of failure swing pattern on daily chart and risk retest of Dec 13 low at $67.70 (five-month low).

Weakening structure on daily chart (MA’s turned to full bearish setup / falling 14-d momentum broke into negative territory) support the action, with limited upticks (under $72.00 zone) to keep bears in play and offer better selling levels, in the environment of favorable fundamentals.

Res: 70.93; 71.93; 72.22; 72.93.

Sup: 70.00; 69.70; 69.27; 68.79.

Sunset Market Commentary

Markets

This week’s opening session had little to offer, especially not coming on the heels of last week’s spectacular opening week including US activity/labour data and EMU inflation numbers. Their outcome and the market reaction to them suggests that the bullish bond correction since the early November FOMC meeting is over, making way for more neutral, sideways action ahead. EMU EC confidence data for December were today’s sole economic highlight. Sentiment improved unexpectedly (96.4 from 94; highest since May) on the back of a rebound in services confidence. Central bank comments were scarce with ECB Vujcic the sole on the wire. He expects inflation to slow gradually and believes that the ECB probably won’t be discussing rate cuts before Summer. That contrasts sharply with money markets discounting a first 25 bps rate cut as soon as April, taking the cumulative amount of rate cuts as high as 150 bps by year-end. German Bunds underperform US Treasuries today. German yields add 3.5 bps to 4 bps across the curve whereas daily US yield changes are broadly flat at the moment. The US Treasury’s mid-month refinancing operation (including 10y & 30y sales) and CPI inflation numbers (Thursday) are this week’s key talking points across the Atlantic. EUR/USD is currently changing hands near 1.0960 after spending most of the day just below 1.0950. Key European and US stock benchmarks record gains of up to 0.50%.

The Kingdom of Belgium is expected to launch its 100th OLO benchmark via syndication tomorrow. The bond will have a 10yr maturity (Oct2034) and is the debt agency’s first initiative to fund this year’s €52.92bn gross financing requirement. This covers a €21.48bn deficit (net financing), €29.27bn maturing debt and €1.50bn of planned pre-funding. Gross borrowing is €5.62bn higher than last year. A €4bn decline in the cash deficit is more than offset by an €8bn uptick in debt redemptions. The bulk of this year’s funding will be raised through OLOs for an amount of €41.00bn with the option to fund another €2bn under EMTN & Schuldscheine programmes. The debt agency expects to raise €2bn through retail State Notes, of which the maturities vary between 3, 5, 8 and 10 year. Doing so, the Belgian debt agency realizes a long-term funding comparable to 2023. To fill the remaining gap, the agency turns to short term debt instruments. The outstanding stock of Treasury Certificates is expected to increase by €4.72bn (to €25bn) while there will made almost full use of the structurally higher cash surpluses for an amount of €11.60bn. The anticipated issuance of a new €13.5bn 1-yr State Note compensates for the sharp outflow when the September 2023 one (€21.9bn) expires later this year. The Note needs to be launched before June 30 if the preferential fiscal regime is retained.

News & Views

Swiss inflation stagnated month-on-month in December. In defying expectations for a minor 0.1% decline, the yearly figure accelerated slightly more than anticipated, from 1.4% to 1.7%. The speedier price rises are no major surprise and are in part the result of ongoing rent hikes after the key reference rate rose twice. Electricity and gas prices also added. Inflation is seen higher for some months to come, also supported by a VAT boost in force since January this year. That said, it’s still comfortably within the Swiss National Bank’s 0-2% target. Together with a historically strong CHF dampening (imported) prices, there’s probably little need for the central bank to move from the sidelines. It has hit the pause button at a policy rate of 1.75% since September last year. EUR/CHF marginally loses ground today. The pair has been extensively testing the 0.93 big figure over the past few days and trades around the strongest CHF levels since the huge spike higher following the removal of the price cap in January 2015.

Brent oil declines more than $2/b today, trading around $76. The drop was triggered by Saudi Arabia announcing a bigger-than-expected reduction for its Middle Eastern flagship Arab light crude supplies. The move underscores the soft nature of the physical market, which in this case also includes China. The fact that it’s the de facto OPEC+ leader doing so carries great signaling power. One of the assets suffering collateral damage from the oil price drop is the Norwegian krone. EUR/NOK extends a bottoming out process that started end 2023 with a 0.8% advance today to 11.365. The EUR/NOK 11.40 area serves as a first resistance before 11.60 pops up as the more daunting test.

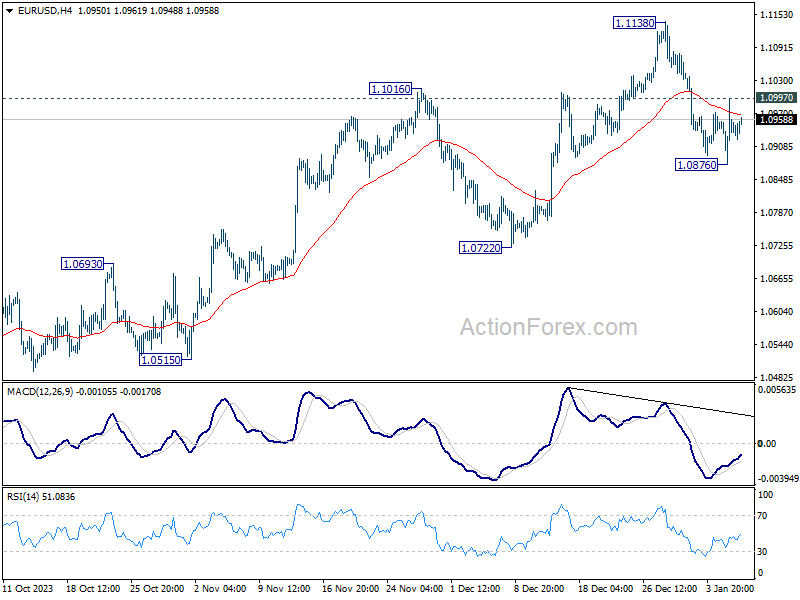

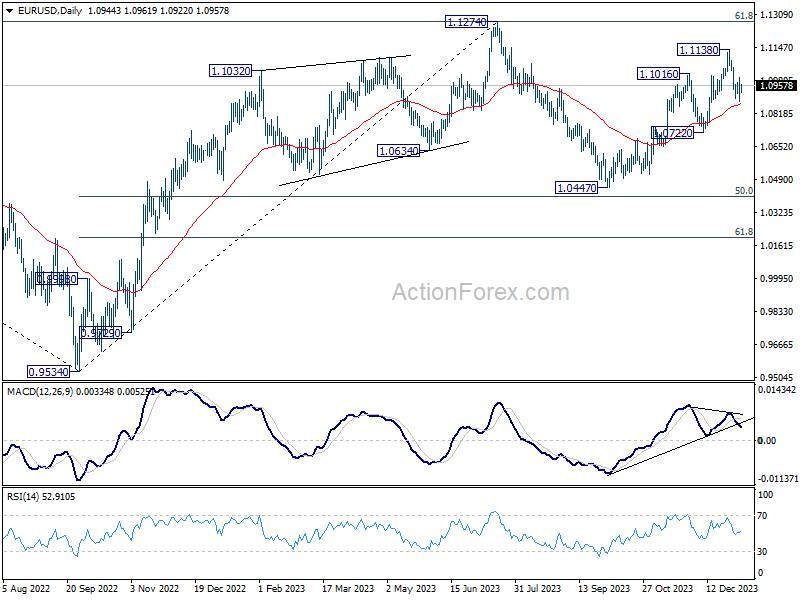

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0881; (P) 1.0939; (R1) 1.1002; More...

Outlook in EUR/USD is unchanged and intraday bias stays neutral. On the downside break of 1.0876 will resume the fall from 1.1138 short term top to 1.0722 support next. However, break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

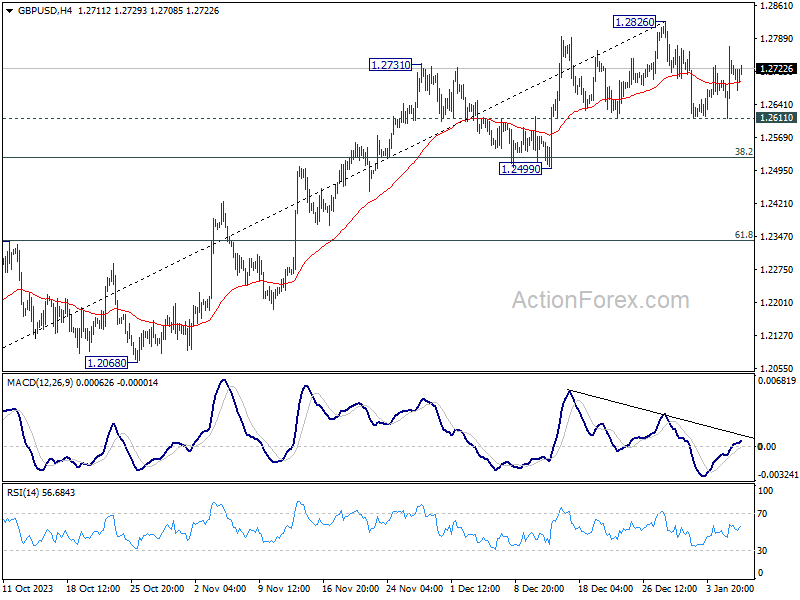

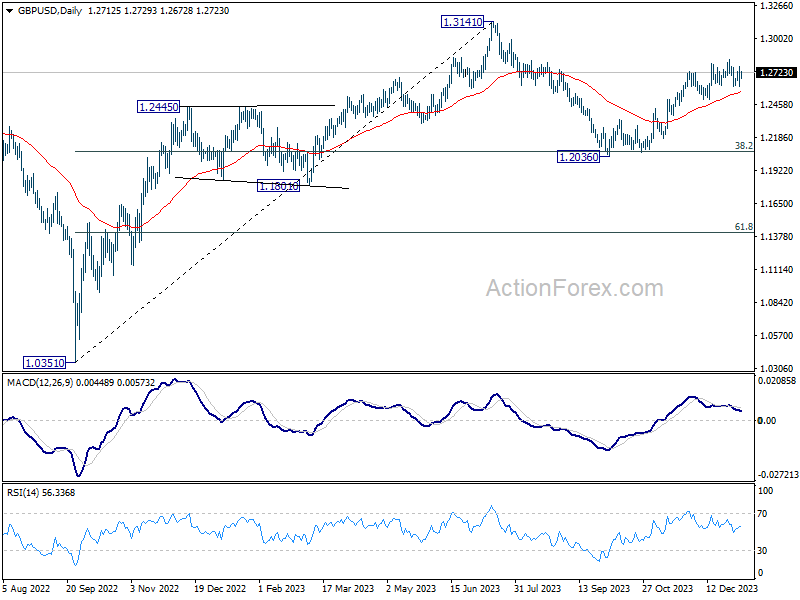

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2630; (P) 1.2701; (R1) 1.2789; More...

Intraday bias in GBP/USD is turned neutral again with current retreat. On the upside, decisive break of 1.2826 high will resume whole rally from 1.2036. Nevertheless, another fall and break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

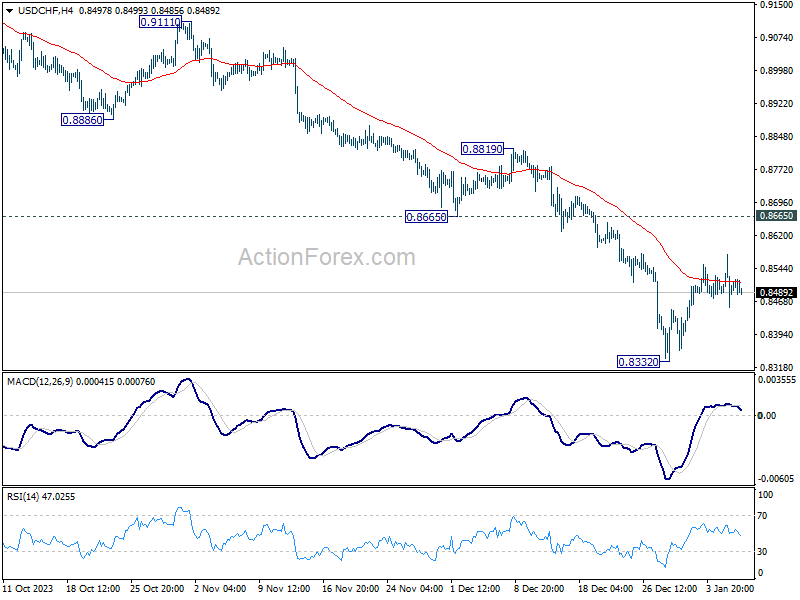

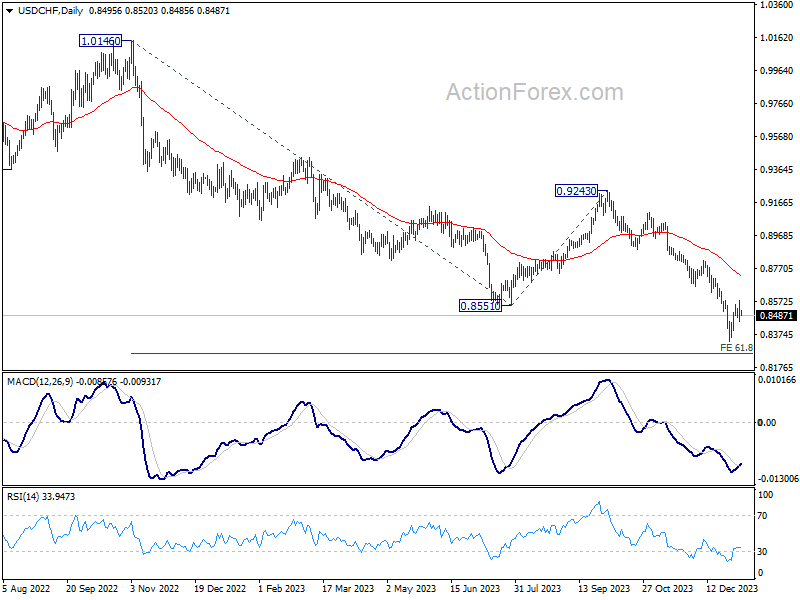

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8447; (P) 0.8512; (R1) 0.8568; More....

No change in USD/CHF's outlook and intraday bias stays neutral at this point. While recovery from 0.8332 short term bottom could extend higher, outlook will stay bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, the down trend from 1.0146 (2022 high) is in progress. Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

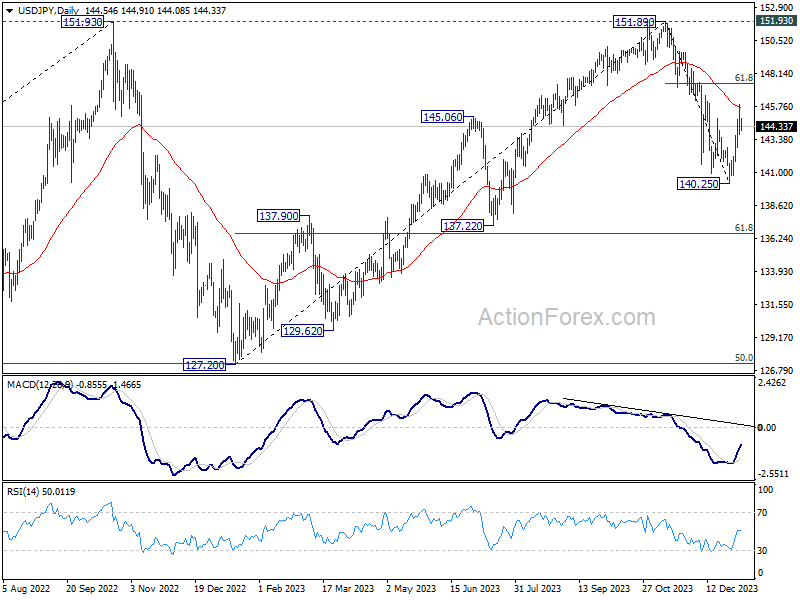

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.63; (P) 144.80; (R1) 145.80; More...

Intraday bias in USD/JPY stays neutral at this point. On the upside, above 145.97 will resume the rebound from 140.25. But upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. On the downside, below 143.17 minor support will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

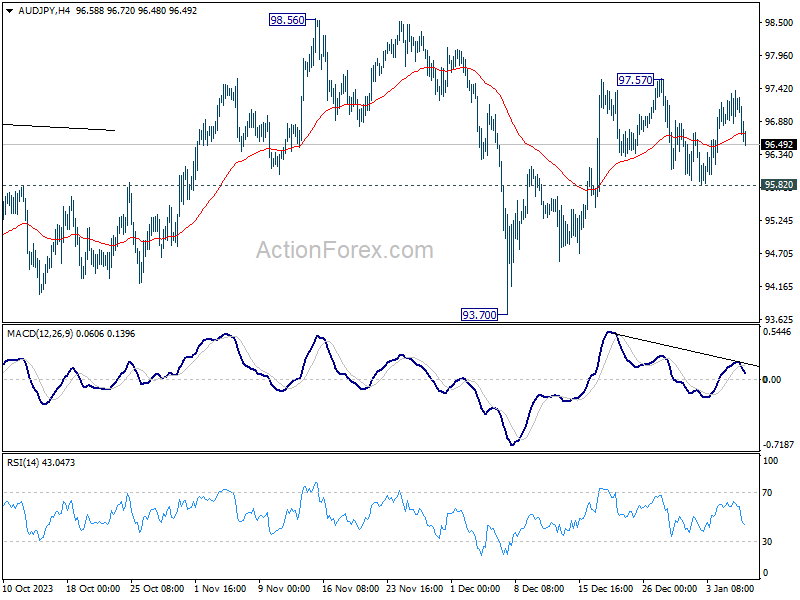

Commodity Currencies Weaken; Focus on AUD/JPY Ahead of Australia and Japan Data

In today's relatively subdued markets, the notable development is weakness in commodity currencies, led by Australian Dollar. This decline comes amid a drop in oil prices following Saudi Arabia's decision to cut official selling prices across all regions. Additionally, precious metals have softened in response to rebound in global benchmark treasury yields. The downward trend also extends to industrial metals, which are affected by worsening global economic outlook.

On the other hand, Japanese Yen is currently the strongest among major currencies, but its gains are tempered as traders anticipate the release of Tokyo's CPI and and Japan's household spending data tomorrow. Euro is showing resilience despite weaker-than-expected investor confidence and retail sales data, trailing closely behind Yen. Swiss Franc is also performing well, supported by CPI figures that met expectations. Meanwhile, Dollar and British Pound are mixed movements.

AUD/JPY would be a pair to watch in the upcoming Asian session, considering that Australia will also release retail sales. For now, rebound from 93.70 could still extend through 97.57 resistance. However, as this rise is seen as the second leg of the consolidation pattern from 98.56, upside should be limited by the resistance. Break of 95.82 minor support will suggest that the third leg has started to 93.70 support and below.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is up 0.28%. CAC is up 0.08%. Germany 10-year yield is up 0.048 at 2.207. UK 10-year yield is up 0.038 at 3.830. Earlier in Asia, Hong Kong HSI fell -1.88%. China Shanghai SSE fell -1.42%. Singapore Strait Times rose 0.09%. Japan was on holiday.

Eurozone Sentix rises to -15.8, but German recession continues

Eurozone Sentix Investor Confidence rose from -16.8 to -15.8 in January, below expectation of -15.4. That's nonetheless the third increase in a row, and the highest reading since May 2023. Current Situation Index also rose for the third month from -23.5 to -22.5. Expectations Index rose for the fourth month, from -9.8 to -8.8, highest since February 2023.

Sentix noted that the sharp drop of -18 points in the sub-index of inflation expectations, from 16.25 to -1.75, raises concerns. This significant decrease is attributed not only to extensive administrative cost increases from tax hikes in Germany but also to a noticeable rise in freight costs, influenced by recent unrest in the Red Sea area. These factors suggest that the prevailing interest rate optimism might be misguided, potentially imposing new challenges on the already struggling Eurozone economy.

Also to be noted, Germany's overall Investor Confidence Index fell from -25.5 to -26.1. Current Situation Index fell from -35.3 to -35.5. Expectations Index fell from -15.3 to -16.3. Sentix noted, "Germany is not emerging from the recession and thus from its economic crisis."

Eurozone retail sales fall -0.3% mom in Nov, EU down -0.2% mom

Eurozone retail sales fell -0.3% mom in November, worse than expectation of -0.1% mom. Volume of retail trade decreased by -0.4% for non-food products and by -0.1% for food, drinks and tobacco, while it increased by 1.4% for automotive fuels.

EU retail sales fell -0.2% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in the Germany (-2.5%), Luxembourg (-1.4%) and Austria (-0.7%). The highest increases were observed in Portugal (+3.1%), Croatia and Slovenia (both +3.0%), Malta and Romania (both +1.7%).

Swiss CPI rises to 1.7% yoy in Dec, matches expectations

Swiss CPI was flat at 0.0% mom in December, above expectation of -0.1% mom. Core CPI (fresh and seasonal products, energy and fuel) rose 0.2% mom. Domestic products prices rose 0.3% mom. Import products price fell -0.7% mom.

For the 12-month period, CPI rose from 1.4% yoy to 1.7% yoy, matched expectations. Core CPI rose from 1.4% yoy to 1.5% yoy. Domestic products prices rose from 2.1% yoy to 2.3% yoy. Imported products prices from also rose from -0.6% yoy to -0.2% yoy.

Also published, retail sales rose 0.7% yoy in November, above expectation of 0.0% yoy.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.63; (P) 144.80; (R1) 145.80; More...

Intraday bias in USD/JPY stays neutral at this point. On the upside, above 145.97 will resume the rebound from 140.25. But upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. On the downside, below 143.17 minor support will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | Germany Factory Orders M/M Nov | 0.30% | 1.10% | -3.70% | -3.80% |

| 07:00 | EUR | Germany Trade Balance (EUR) Nov | 20.4B | 17.9B | 17.8B | 17.7B |

| 07:30 | CHF | Real Retail Sales Y/Y Nov | 0.70% | 0.00% | -0.10% | -0.30% |

| 07:30 | CHF | CPI M/M Dec | 0.00% | -0.10% | -0.20% | |

| 07:30 | CHF | CPI Y/Y Dec | 1.70% | 1.70% | 1.40% | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Jan | -15.8 | -15.4 | -16.8 | |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Dec | 96.4 | 93.8 | 94.0 | |

| 10:00 | EUR | Eurozone Industrial Confidence Dec | -9.2 | -9.5 | ||

| 10:00 | EUR | Eurozone Services Sentiment Dec | 8.4 | 4.9 | 5.5 | |

| 10:00 | EUR | Eurozone Consumer Confidence Dec F | -15.0 | -15.1 | -15.1 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Nov | -0.30% | -0.10% | 0.10% | 0.40% |

Nasdaq 100 Technical: Potential Short-Term Bounce on the Horizon

- Recent decline has almost reached the upward-sloping 50-day moving average.

- Short-term RSI momentum indicator has suggested downside momentum has eased.

- Potential short-term bounce above 16,160 key short-term support.

The US Nas 100 Index (a proxy for the Nasdaq 100 futures) has tumbled towards the 16,160/125 intermediate support as highlighted in our earlier analysis as it hit an intraday low of 16,190 last Friday, 5 January after a bearish reaction off the 16,990 intermediate resistance post-Christmas with a current all-time high level of 16,999 printed on 28 December 2023.

So far the Index has declined by -4.76% from its 28 December 2023 all-time high level in the past week, reinforced by weakness in the share price of Apple recorded a weekly loss of -6.41% last week, and underperformed within the “Magnificent 7” group of mega-capitalization US equities due to two sell-side brokerages performance degrades over potential waning demand for its latest iPhone model.

The decline almost reached the 50-day moving average

Fig 1: US Nas 100 medium-term trend as of 8 Jan 2024 (Source: TradingView, click to enlarge chart)

The 5-day slide has almost reached the 50-day moving average, the former swing high areas of 22 November/29 November 2023 now acting as a pull-back support at 16,160, and the 61.8% Fibonacci retracement of the prior minor uptrend phase from 4 December 2023 low to 28 December 2023 high.

The short-term downside momentum has dissipated

Fig 2: US Nas 100 minor short-term trend as of 8 Jan 2024 (Source: TradingView, click to enlarge chart)

The hourly RSI momentum indicator has flashed a prior bullish divergence signal at its oversold region before a bullish momentum breakout last Friday, 5 Jan which increases the odds of a minor recovery scenario at this juncture as the downside momentum of last week’s decline has eased.

Watch the 16,160 key short-term pivotal support and clearance above 16,435 near-term resistance sees the next intermediate resistance zone coming at 16,500/580 (20-day moving average, former minor ascending channel support & the 61.8% Fibonacci retracement of the decline from 28 December 2023 high to 5 January 2024 low).

However, failure to hold at 16,160 invalidates the recovery scenario to see the continuation of the minor corrective decline within its major uptrend phase to expose the next intermediate support at 15,870/820 in the first step.