Sample Category Title

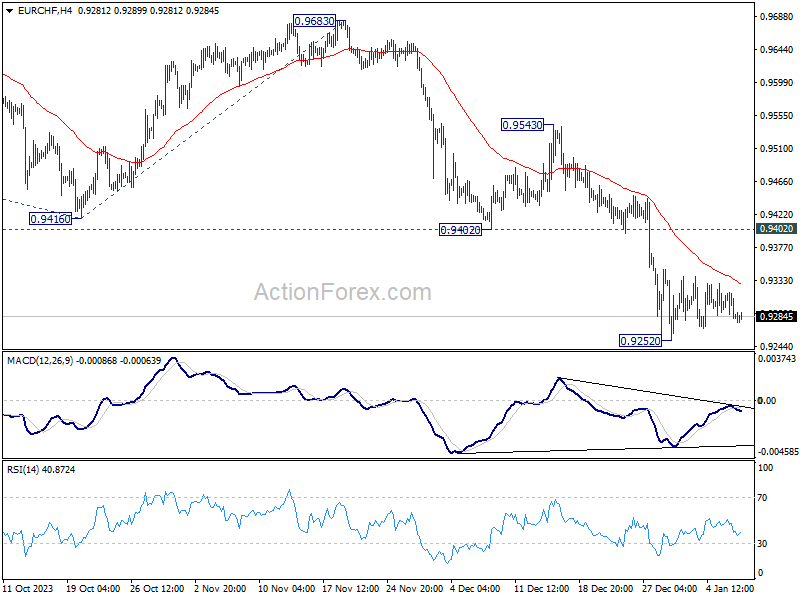

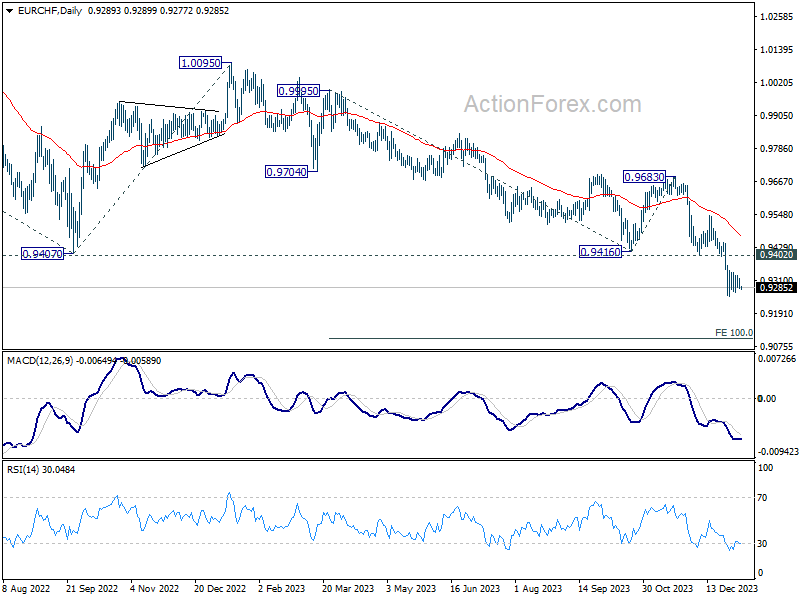

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9274; (P) 0.9296; (R1) 0.9309; More...

EUR/CHF is still bounded in consolidation above 0.9252 and intraday bias remains neutral for the moment. While another recovery cannot be ruled out, outlook will stay bearish as long as 0.9402 support turned resistance holds. On the downside, break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

Shaky optimism

The US equities followed up on the European stock market gains on Monday; technology stocks gained the most and their precious contribution to the S&P 500 pushed the latter up by more than 1.40% yesterday, as Nasdaq 100 rallied past 2%. Boeing and Spirit AeroSystems were heavily hit by a after Boeing’s 737 Max 9 model got temporarily grounded amid an Alaska Air flight incident over the weekend, but apart from these two, the overall sentiment was positive at the start of the week.

Yesterday’s optimism could be attributed to a couple of factors. First, the US politicians agreed on a 2024 spending deal, a key step to avoiding a government shutdown. The latter helped pull the US 10-year yield back toward the 4% mark.

Additionally, Chinese authorities pledged to lower reserve requirements to boost lending, and their commitment to increasing liquidity through open market operations and the MLF may have stimulated appetite in global risk assets, even though Chinese stocks barely benefited from the People's Bank of China (PBoC) comments. Shanghai's Composite remained under decent selling pressure after Zhongzhi filed for bankruptcy, and Xi Jinping promised to deepen China's anti-corruption crackdown on finance, energy, infrastructure, and pharma.

Chinese stimulus measures might not significantly boost appetite for Chinese stocks, but they should fuel bullish bets on industrial metals like iron ore and copper, given the surging Chinese demand for metals to support industries and real estate.

Finally, the expectation of a sufficiently soft CPI report from the US this Thursday, and the persistent fall in crude oil prices continue to soothe investors nerves regarding the future of inflation despite the exploding shipping costs due to the Red Sea tensions.

In this context, the barrel of American crude sank more than 4% yesterday, to nearly $70pb, as Saudis cut the price of their Arab Light crude to Asian customers citing rising global supply, growing global competition in the crude market and concerns regarding a slowing global growth and slowing demand. The negative momentum in oil prices persists and a slide below the $70pb will likely pave the way toward the $65/67pb level, the range that acted as a decent support last year.

Returning to inflation discussion, as oil prices have been one of the major contributors to inflation, their inability to rebound soothes inflation worries, keeping the Federal Reserve (Fed) doves in charge of the market – and that’s somewhat positive for the stock valuations.

In the FX, the US Dollar remains offered. There is now a death cross formation on the daily US Dollar Index chart: the 50-DMA crossed below the 200-DMA conforming a negative technical formation. The latter is, however, a lagging formation and does not necessarily mean that we won’t see the US Dollar rebound. On the contrary, I believe that the dovish Fed expectations have been well ahead of themselves since the end of last year and there is room for some positive correction in the US Dollar.

In this context, the EURUSD will likely continue to see resistance into the 1.10 level, and clearing the 140 support for the USDJPY won’t be a piece of cake. Even less so as inflation in Tokyo slowed from 2.7% to 2.4% in December, hinting that the Bank of Japan (BoJ) has little urge to exit its negative rate policy. Price rallies in USDJPY remain interesting opportunities to sell the tops, because a slide below 140 will certainly trigger a rally on stops and gather a worthy downside momentum, but getting the time right is crucial. The BoJ is now expected to exit the negative territory by April, but nothing is less sure. If inflation is bearable – which still is - the BoJ will remain seated on its negative rates for a longtime, especially when the global economic outlook sours.

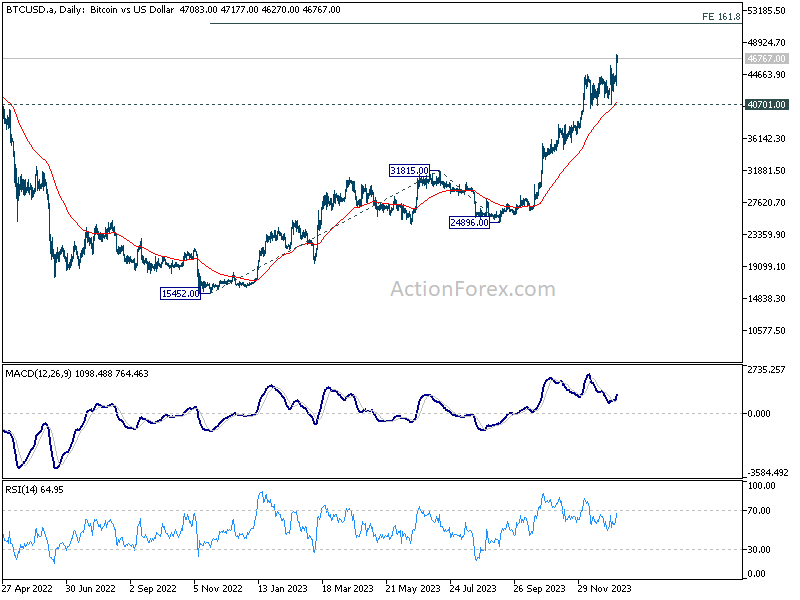

Elsewhere, Bitcoin extends gains to $47K as Bitcoin ETFs get closer to approval, which will allow the finance giant names like Blackrock to invest massively in cryptocurrency. Gold, on the other hand, has been under a decent pressure since the start of the year as the rebounding US yields and stronger US dollar weigh on the precious metal. However, gold could well reverse its negative trend if Thursday’s US inflation report comes in sufficiently soft and could return past the $2050 level.

Hard Eurozone Data, Soft US Data

In focus today

Today, from the US, the NFIB's Small Business Optimism index will be released for December. Markets will focus especially on businesses' perception of upcoming price changes and the outlook for labour markets.

In the euro area, focus is on the unemployment figures and German industrial production for November. In October, the euro area unemployment rate remained at historic lows of 6.5%. Based on signals from PMIs and country releases we expect that it remained at 6.5% in November. Going forward, we foresee a slow and muted rise in the unemployment rate due to the previous weak economic activity. It will be interesting to follow the German industrial production figures as the hard data for the German industry has not showed a bottom out of activity yet.

The National Bank of Poland concludes its two-day monetary policy meeting. We expect an unchanged policy rate at 5.75%, in line with consensus.

In Sweden, the December budget balance is expected (SNDO) at a deficit of SEK92bn. Year to date, the budget surplus stands at approximately SEK120bn, set to decline to SEK28bn if the December forecast proves correct. For the coming two years however, SNDO expects deficits for the full years and thus a higher funding need.

Finally, overnight we get November wage data from Japan. Wage growth is key to the outlook for Bank of Japan tightening, but we will probably have to wait for the spring wage negotiations to see wages move much higher.

Economic and market news

What happened overnight: U.S. tech stocks were off to a good start of the week as the Nasdaq composite gained 2.2%.

Tokyo CPI inflation for December was broadly in line with expectations with CPI excl. fresh food slowing to 2.1% y/y (from 2.3%) and CPI excl. fresh food and energy slowing to 3.5% y/y (from 3.6%). Note, Tokyo CPI acts as a leading indicator for national CPI data, which is due to be released next week. The key missing piece of the puzzle for the Bank of Japan (BoJ) is higher wage growth. We expect to get more hard evidence of that during the spring after which we expect the BoJ to be ready to hike the policy rate out of negative territory and release the grip on the yield curve.

What happened yesterday: Oil prices continued to decline during the day in reaction to the price cut by Saudi's Aramco, with the Brent ending yesterday's session at around 76 USD/bbl, a fall of more than 3 per cent. Combined with general underperformance of the energy complex, this weakened the commodity sensitive NOK.

Higher electricity, gas and housing rental prices contributed to a slight upside surprise in Swiss December CPI, with headline inflation printing at 1.7% y/y. This moved EUR/CHF slightly lower during the day.

In their remarks last night, the Fed's Bostic and Bowman remained optimistic that inflation continues to cool in 2024, but Bowman underscored that the approach to cutting rates would have to be a 'cautious' one. In line with his earlier views, Bostic called for the first cut in Q3 and a total of two cuts in 2024, which contrasts markets pricing in as much as 132bp of cuts for this year as a whole (Danske forecast: quarterly 25bp cuts from March). As a positive sign, consumers' inflation expectations continued to decline in the NY Fed's December survey released last night, 1-year expectations fell to 3.0% (the lowest since Dec 2020, from 3.4%) and 3-year to 2.6% (the lowest since June 2020, from 3.0%).

Equities rebounded on Monday and quite forcefully in the US. S&P 500 jumped 1.4% and Nasdaq a full 2.2%, while Europe edged up 0.4%. Small caps were suddenly back in favour with Russell 2000 gaining 2%. This was mainly a positioning driven bounce story, after the sell-off last week. Scrapping to find other triggers, one could blame yields being a notch lower on positive inflation news and falling oil prices. Growth outperformance was the big investor theme, with rotation into FANMAG+ (tech, consumer discretionary and communication). Yield sensitive sectors such as real estate and health care also performed well. Clear cut cyclicals, such as banks, materials or industrials, however lagged. Asian markets are mostly higher this morning but US futures have dipped back into negative.

FI: There was a modest decline in global bond yields yesterday ahead of the US inflation data that are released on Thursday. The focus in the European fixed income market is on the activity in the primary market. Here we continue with Italy and Belgium that coming to the market.

FX: In a fairly uneventful beginning to the week, the NOK has been the worst performer in G10 space with EUR/NOK rising to the mid 11.30s amid a general underperformance in the energy complex incl. a decline in oil prices. EUR/USD remained unchanged around 1.0950 while EUR/GBP has edged just below the 0.86 threshold.

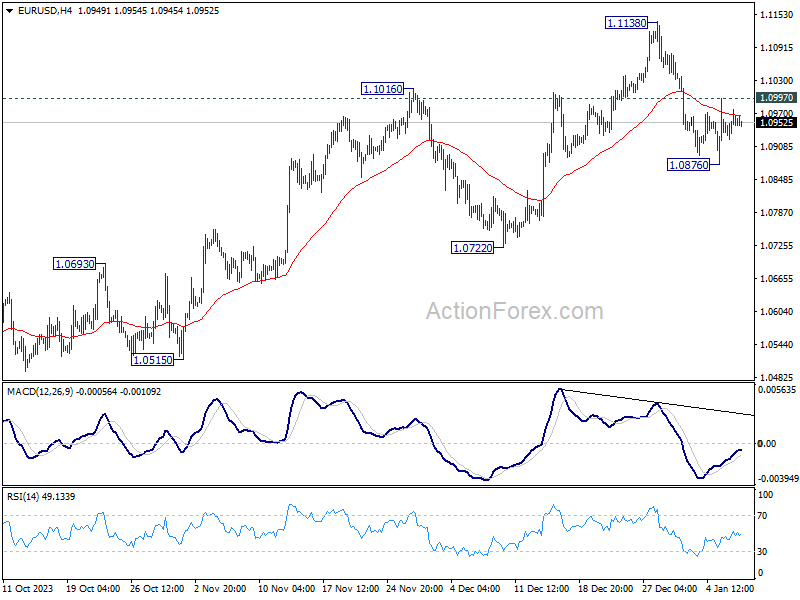

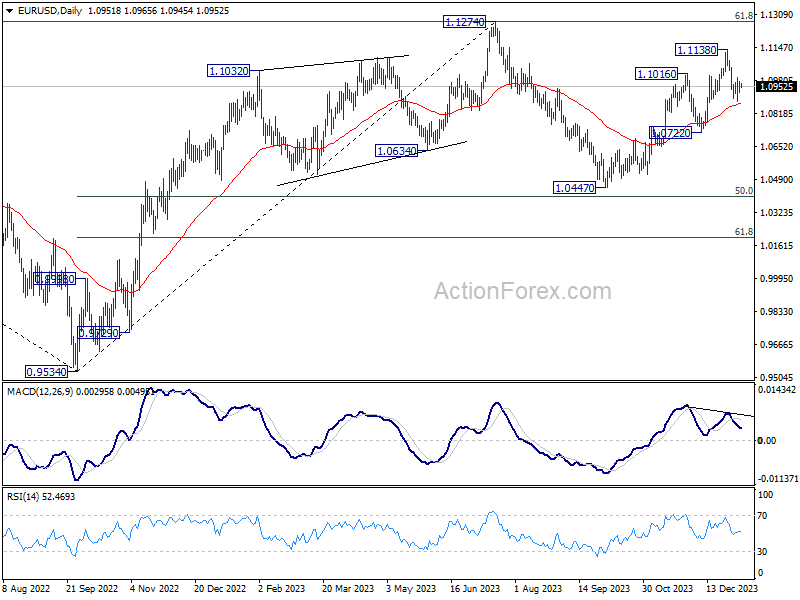

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0922; (P) 1.0951; (R1) 1.0978; More...

Intraday bias in EUR/USD stays neutral for the moment, and outlook is unchanged. On the downside break of 1.0876 will resume the fall from 1.1138 short term top to 1.0722 support next. However, break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

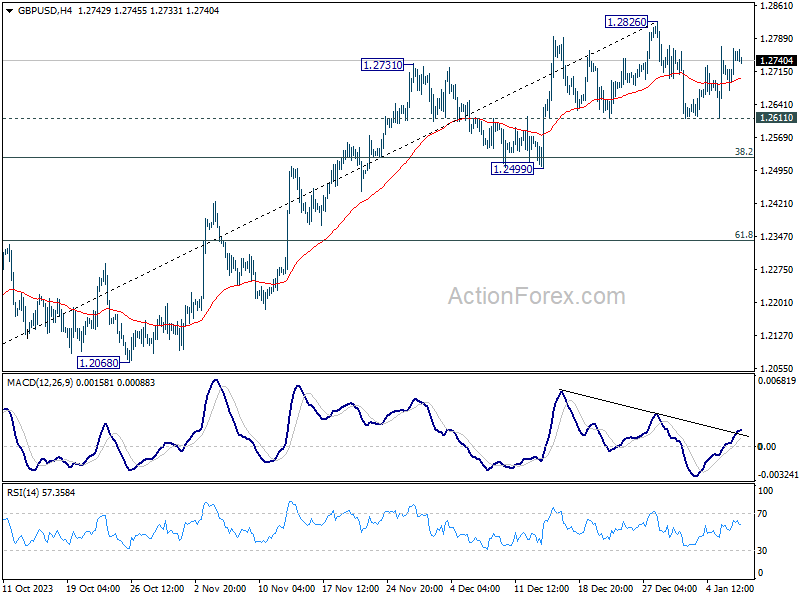

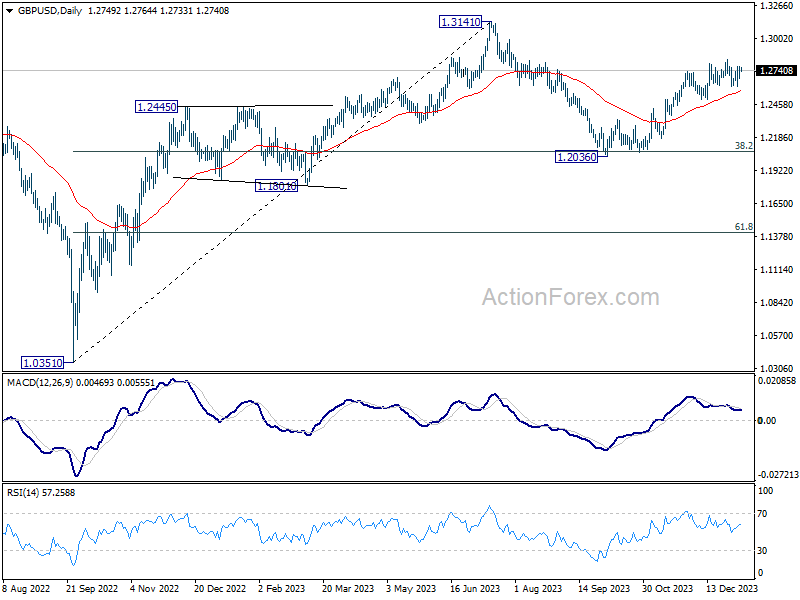

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2692; (P) 1.2729; (R1) 1.2786; More...

Intraday bias in GBP/USD remains neutral as range trading continues below 1.2826. On the upside, decisive break of 1.2826 high will resume whole rally from 1.2036. Nevertheless, another fall and break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

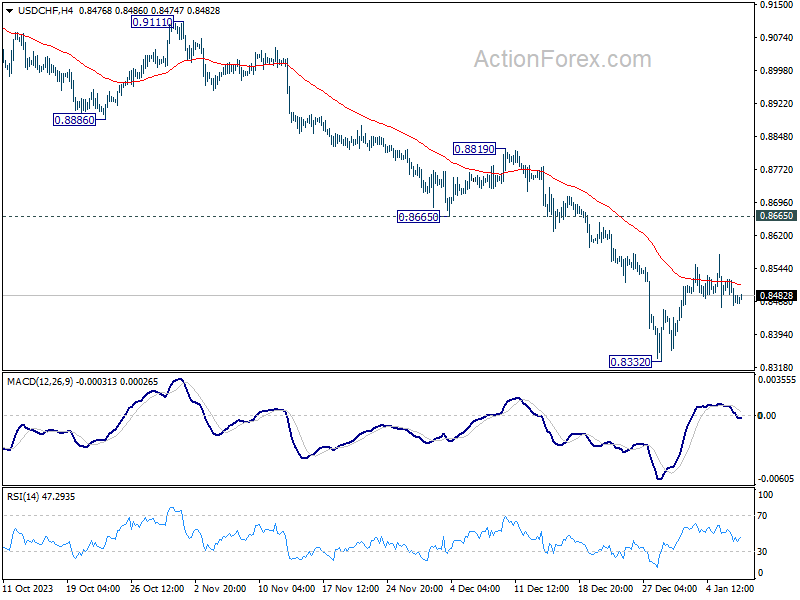

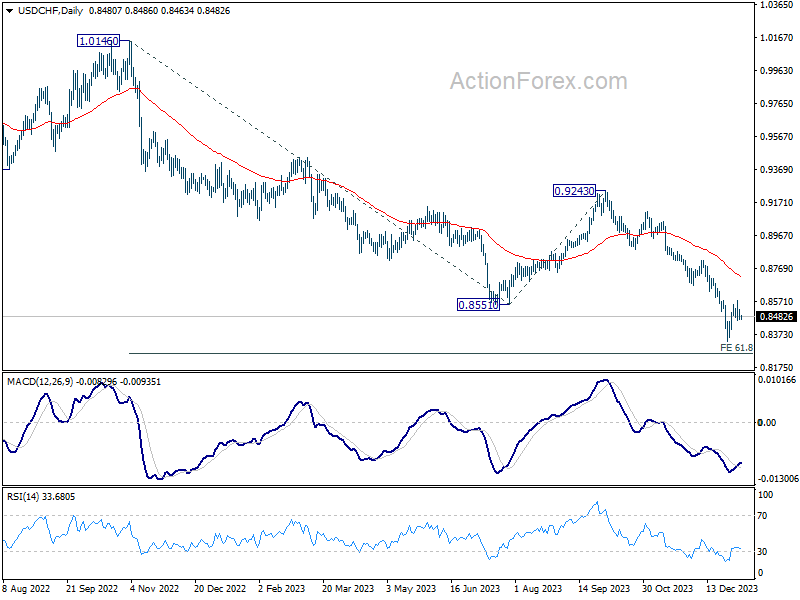

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8453; (P) 0.8488; (R1) 0.8516; More....

Intraday bias in USD/CHF remains neutral and outlook is unchanged. While recovery from 0.8332 short term bottom could extend higher, outlook will stay bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, the down trend from 1.0146 (2022 high) is in progress. Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

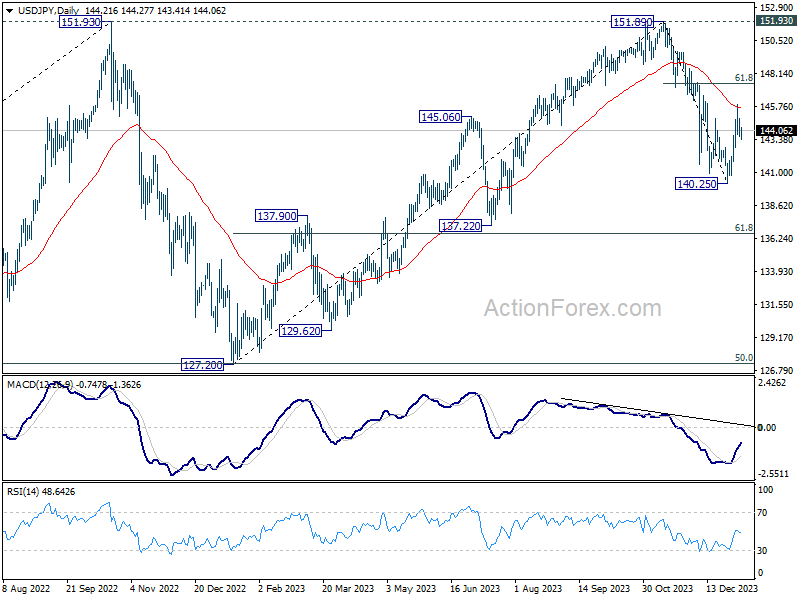

USD/JPY Daily Outlook

Daily Pivots: (S1) 143.63; (P) 144.27; (R1) 144.89; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. On the upside, above 145.97 will resume the rebound from 140.25. But upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. On the downside, below 143.17 minor support will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

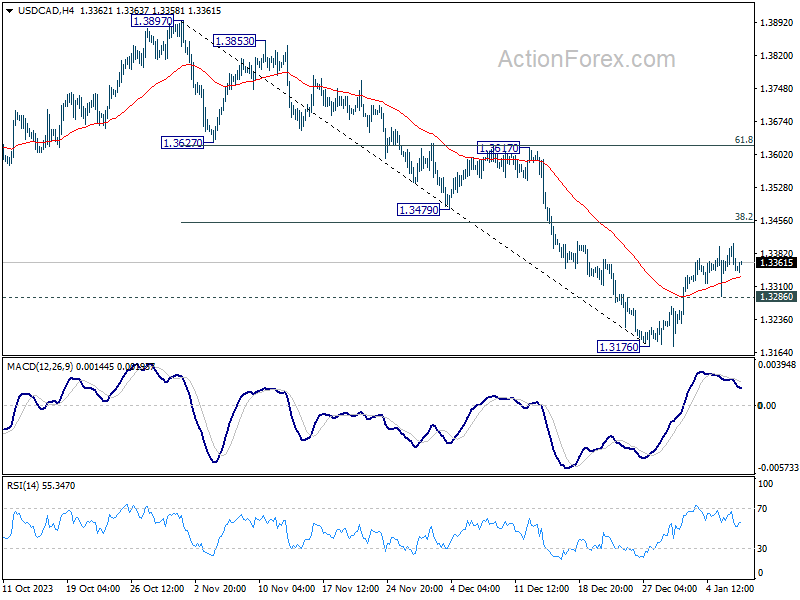

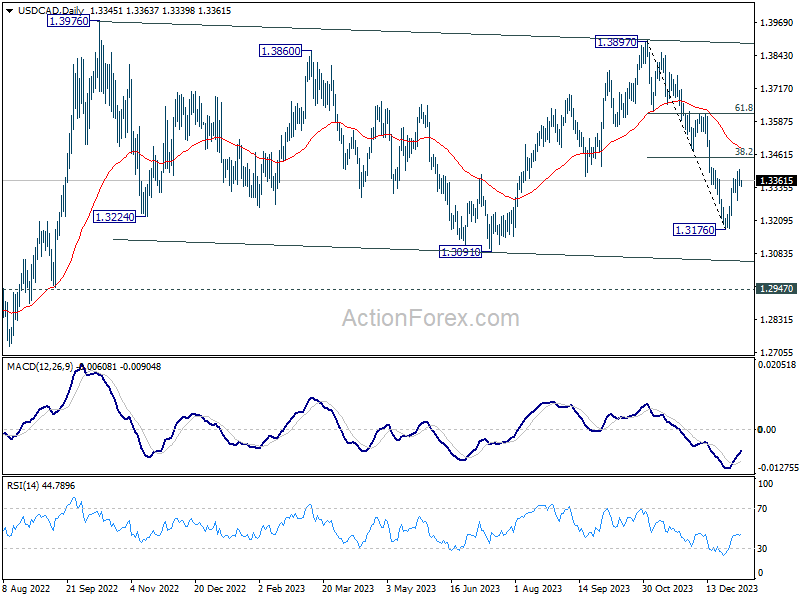

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3327; (P) 1.3366; (R1) 1.3387; More...

While USD/CAD is losing upside momentum, further rise remains mildly in favor with 1.3286 minor support intact. Current rise from 1.3176 short term bottom would target 38.2% retracement of 1.3897 to 1.3176 at 1.3451. Firm break there will pave the way to 61.8% retracement at 1.3622. On the downside, however, break of 1.3286 will turn bias back to the downside for 1.3176 low instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. While fall from 1.3897 could still extend through 1.3091, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage.

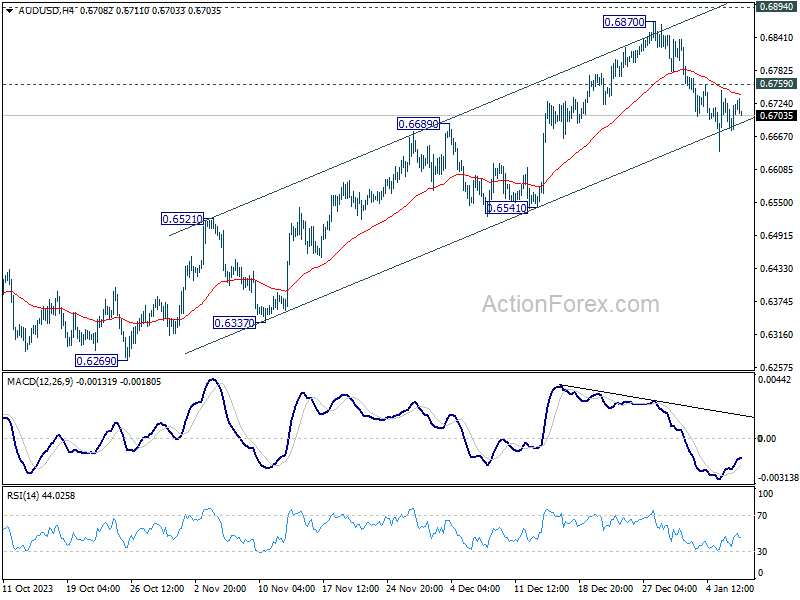

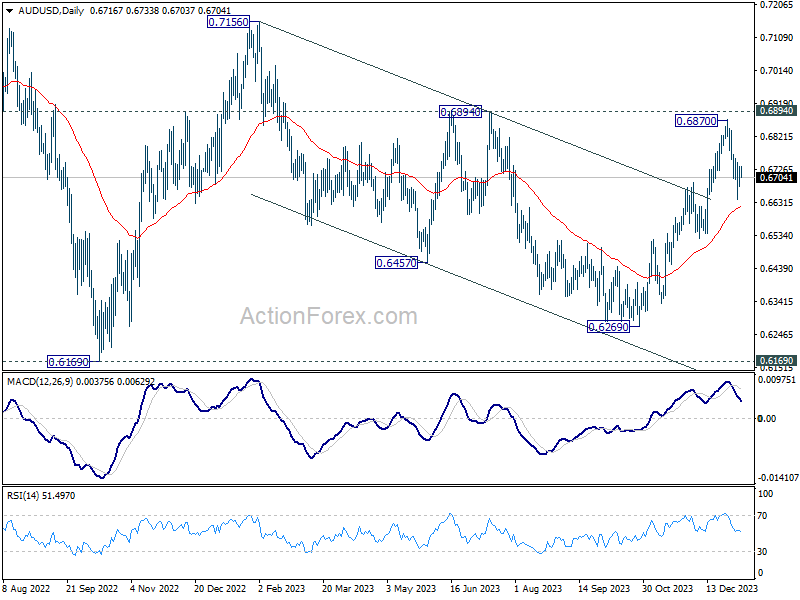

AUD/USD Daily Report

Daily Pivots: (S1) 0.6687; (P) 0.6711; (R1) 0.6744; More...

No change in AUD/USD's outlook as further decline is in favor with 0.6759 minor resistance intact. Fall from 0.6870 short term top would target 55 D EMA (now at 0.6619). Some support could be seen there to bring rebound on first attempt. On the upside, however, break of 0.6759 minor resistance will suggest that the pull back is over, and bring retest of 0.6870 instead.

In the bigger picture, price actions from 0.6169 (2022 low) could be just a medium term corrective pattern to the down trend from 0.8006 (2021 high). Rise from 0.6269 is seen as the third leg of the pattern that could target 0.7156 on break of 0.6894 resistance. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

Markets Unmoved by Japan and Australia Data, Bitcoin Surges

Today's Asian trading session has been relatively subdued. Japan reported deeper-than-expected contraction in household spending, while Tokyo CPI core showed slowdown in line with market expectations. However, Yen's near-term rebound seems to be losing steam as these data releases have not provided significant market impetus. Meanwhile, Nikkei index returned from holiday with a bounce, though other Asian stock markets exhibited mixed performance.

In contrast, Australian Dollar appeared unaffected by the much stronger-than-expected retail sales data. Commodity currencies are generally weak, but the extent of the selloff has been limited. In other currency markets, Euro and Swiss Franc are showing mild strength after Yen, while Dollar and the British Pound are mixed.

Several secondary tier economic data are slated for release today, including Germany's industrial production, Eurozone unemployment rate, and trade balance figures from Canada and US. However, market volatility might remain low until the next Asian session, which will feature Japan's labor cash earnings and Australia's monthly CPI data.

Technically, Bitcoin's rally resumed after brief setback and hits as high as 47294 so far. Further rise is expected as long as 40701 support holds. Next target is 161.8% projection of 15452 to 31815 from 24896 at 51371, which is above 50k level.

In Asia, Nikkei closed up 1.16%. Hong Kong HSI is up 0.17%. China Shanghai SSE is up 0.17%. Singapore Strait Times is up 0.45%. Japan 10-year JGB yield is down -0.0144 at 0.591. Overnight, DOW rose 0.58%. S&P 500 rose 1.41%. NASDAQ rose 2.20%. 10-year yield fell -0.040 to 4.002.

Fed's Bostic reiterates importance to staying on path to 2% inflation

Atlanta Fed President Raphael Bostic, in a moderated discussion yesterday, reiterated his expectation of two rate cuts by the Fed this year. He anticipates the first rate cut to occur in the third quarter.

For now, he's "comfortable" with Fed's "restrictive stance". "I just want to see the economy continue to evolve with us in that stance and hopefully see inflation continue to get to our 2% level," he added.

The US is "on a path to 2%" inflation and "the goal is to make sure we stay on the path," he said.

Fed's Bowman: Current monetary policy deemed sufficiently restrictive

Fed Governor Michelle Bowman indicated yesterday her willingness to consider the possibility that the current policy rate might be adequately restrictive to further reduce inflation.

"My view has evolved to consider the possibility that the rate of inflation could decline further with the policy rate held at the current level for some time," she said in a speech yesterday.

She added that if inflation continues to decrease towards the 2% target, "it will eventually become appropriate to begin the process of lowering our policy rate."

However, she also emphasized "While the current stance of monetary policy appears to be sufficiently restrictive to bring inflation down to 2 percent over time, I remain willing to raise the federal funds rate further at a future meeting should the incoming data indicate that progress on inflation has stalled or reversed."

Japan's Tokyo CPI core down for the second month to 2.1%

Japan's Tokyo CPI core, which excludes fresh food, slowed from 2.3% yoy to 2.1% yoy in December, aligning with market expectations. This figure represents the lowest reading since June 2022 and marks the second consecutive month of decline.

Additionally, CPI core-core, which excludes both food and energy, also slipped from 3.6% yoy to 3.5% yoy. This marks the fourth consecutive month of cooling in this measure. Headline CPI, similarly fell from 2.6% yoy to 2.4% yoy. T

Tokyo's CPI figures are often regarded as precursors to the national data, suggesting that a similar trend might be observed in the broader Japanese economy.

In separate report, households reduced their spending in November -by 2.9% yoy, worst than expectation of -2.3% yoy. This decrease in consumer spending is attributed to the rising costs of living, which have led to more selective purchasing behaviors among shoppers.

Australia's retails sales rises 2.0% mom in Nov on Black Friday boost

Australia retail sales rose 2.0% mom to AUD 36.5B in November, above expectation of 1.2% mom. That followed a fell of -0.4% mom in October.

Robert Ewing, ABS head of business statistics, attributed this surge to the impact of Black Friday sales. He noted, "Black Friday sales were again a big hit this year, with retailers starting promotional periods earlier and running them for longer, compared to previous years."

Ewing further explained: "The strong rise suggests that consumers held back on discretionary spending in October to take advantage of discounts in November." Additionally, he observed that shoppers might have advanced some of their Christmas shopping to November, which typically occurs in December.

Looking ahead

Swiss unemployment rate and foreign currency reserves, Germany industrial production, France trade balance, and Eurozone unemployment rate will be released in European session. Later in the day, US will release trade balance. Canada will release trade balance and building permits.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6687; (P) 0.6711; (R1) 0.6744; More...

No change in AUD/USD's outlook as further decline is in favor with 0.6759 minor resistance intact. Fall from 0.6870 short term top would target 55 D EMA (now at 0.6619). Some support could be seen there to bring rebound on first attempt. On the upside, however, break of 0.6759 minor resistance will suggest that the pull back is over, and bring retest of 0.6870 instead.

In the bigger picture, price actions from 0.6169 (2022 low) could be just a medium term corrective pattern to the down trend from 0.8006 (2021 high). Rise from 0.6269 is seen as the third leg of the pattern that could target 0.7156 on break of 0.6894 resistance. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Dec | 2.40% | 2.60% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Dec | 2.10% | 2.10% | 2.30% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Dec | 3.50% | 3.60% | ||

| 00:30 | AUD | Retail Sales M/M Nov | 2.00% | 1.20% | -0.20% | -0.40% |

| 00:30 | AUD | Building Permits M/M Nov | 1.60% | -2.00% | 7.50% | 7.20% |

| 06:45 | CHF | Unemployment Rate M/M Dec | 2.20% | 2.10% | ||

| 07:00 | EUR | Germany Industrial Production M/M Nov | 0.40% | -0.40% | ||

| 07:45 | EUR | France Trade Balance (EUR) Nov | -7.9B | -8.6B | ||

| 10:00 | EUR | Eurozone Unemployment Rate Nov | 6.50% | 6.50% | ||

| 11:00 | USD | NFIB Business Optimism Index Dec | 90.9 | 90.6 | ||

| 13:30 | USD | Trade Balance (USD) Nov | -64.8B | -64.3B | ||

| 13:30 | CAD | Trade Balance (CAD) Nov | 2.5B | 3.0B | ||

| 13:30 | CAD | Building Permits M/M Nov | 2.00% | 2.30% |