Sample Category Title

Brent is Stressed Again

For the last month and a half, the crude oil market has been under a constant stress. Sentiment changes mostly because of the supply and demand forecasts. A Brent barrel price dropped to 75.65 USD yesterday.

The decline was triggered by the decision of Saudi Arabia to decrease prices for its buyers starting February, regardless of the region. The discount will amount to 2 USD, which is quite a lot.

The market thinks that the Saudis have either noticed a demand slump and are now trying to run ahead of it, or they have decided to shove away the competitors, such as the US crude oil producers.

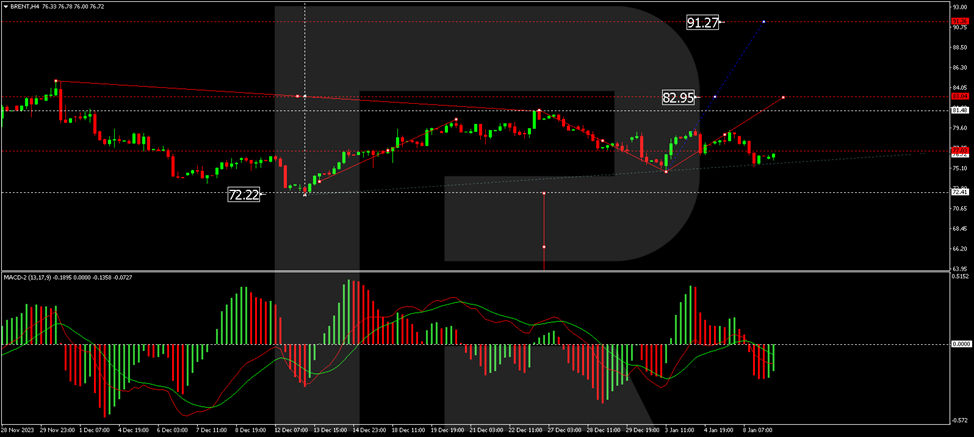

Brent technical analysis

On the H4 Brent chart, the quotes have corrected to 74.74. A consolidation range is now forming around the 78.15 level. An escape from the range upwards might open the potential for a growth wave to 81.50. This is a local target. With an escape from the range downwards, the correction could continue to 70.00. Technically, this scenario is confirmed by the MACD, whose signal line is under zero, preparing to start growing.

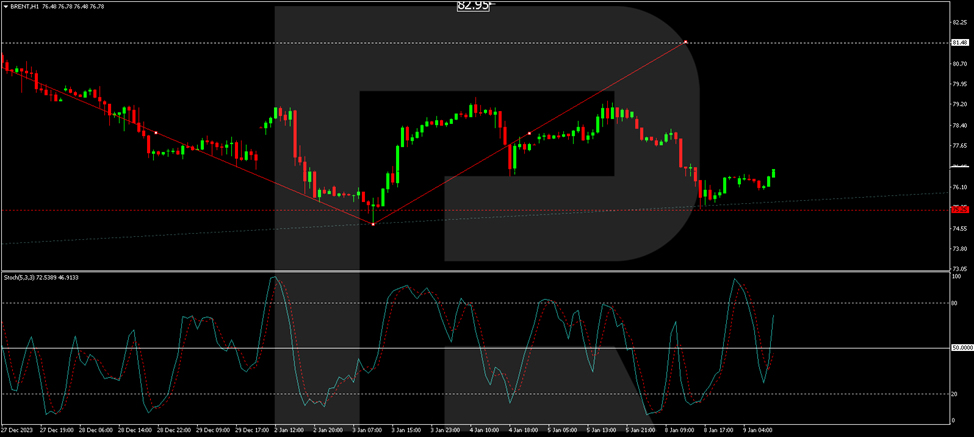

On the H1 Brent chart, the quotes have completed a growth wave to 79.45 and a correction to 75.25. Today a growth link to 80.00 is expected to develop. If this level breaks, the wave could continue to 81.50. Technically, this scenario is confirmed by the Stochastic oscillator: its signal line is under 50, aimed strictly upwards to 80.

Swiss National Bank Suffered Losses of 3 Billion Francs in 2023

The Swiss National Bank (SNB) reported an annual loss of 3 billion Swiss francs (USD 3.54 billion) in 2023 and said it would not make payments to Switzerland's central or local government or pay dividends to investors.

The loss is believed to have occurred as a result of interest rate hikes aimed at fighting inflation.

Although in Switzerland, perhaps, inflation is at the lowest level: according to yesterday's Core Price Index data, the actual value is = 0.0% (expected = 0.1%, a year ago = -0.2%, the highest actual value in 2023 was = +0.7 %). However, the SNB raised the rate to 1.75% twice in 2023, and this led to it making more payments to deposit account holders.

Note that the loss for 2023 is much less than the record minus 133 billion for 2022. Reuters writes that the losses will not affect the bank's current monetary policy, and interest rates could be cut during 2024.

On November 2, we wrote that the franc could continue to strengthen. Since then, USD/CHF has fallen about 6%, setting its 2023 low on December 28 at 0.83327.

The graph shows that:

→ during 2023, the price moved within the descending channel;

→ at the 2023 low, the price was unable to reach its lower limit — a sign of a lack of selling pressure;

→ the median line of the channel still serves as resistance (as shown by the arrow);

→ level 0.845 changed its role from resistance to support;

→ in the area of the 2023 lows, long lower shadows were formed on the candles (a sign of aggressive demand). At the same time, the RSI indicator showed that the market was strongly oversold.

Taking into account the above arguments, it can be assumed that the USD will be able to strengthen against the franc, stopping the pace of the downward trend in 2023. A bullish breakdown of the median line (or failure of the price to consolidate below the 0.845 level) will provide more arguments in favor of the presence of demand in the market in question.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Japanese Yen Shrugs as Tokyo Core CPI Slows

- Tokyo Core CPI eases to 2.1%

The Japanese yen has posted slight gains for a second straight day. In the European session, USD/JPY is trading at 144.10, down 0.09%.

Tokyo Core CPI dips to 2.1%

Tokyo Core CPI rose 2.1% y/y in December, down from 2.3% in November and matching the estimate of 2.1%. This marked the lowest reading since June 2022. At the same time, the indicator has exceeded the Bank of Japan’s target of 2% for 19 straight months.

There has been speculation that persistent inflation the BoJ will tighten policy and BoJ meetings have become closely-watched events, with investors on the alert for a shift in the BoJ’s ultra-loose policy. The BoJ meets next on Jan. 22-23. BoJ Governor Ueda has hinted at a change in policy but has stressed that wages must first rise if the BoJ is to achieve its goal of sustainable inflation at 2%.

The BoJ’s ultra-loose policy took a massive toll on the yen in 2023. The yen plunged 15% between January and October but managed to recover about half of those losses by the end of the year, as the US dollar retreated on expectations that the Federal Reserve would lower rates in 2024.

Japan’s economy remains weak, which is another reason that the BoJ is hesitant to tighten policy. Household spending, released earlier today, declined 1% in November, compared to -0.1% in October and lower than the estimate of 0.2%. On a yearly basis, household spending fell 2.9% in November, down from -2.5% in October and shy of the estimate of -2.3%. Since November 2022, household spending has posted only one gain as consumers continue to hold tight to the purse strings due to the difficult economic conditions.

USD/JPY Technical

- USD/JPY tested resistance at 144.27 earlier. Above, there is resistance at 144.89

- There is support at 143.63 and 143.01

Pound Looks to UK GDP Rebound to Keep Bears at Bay

- UK GDP likely expanded in November, potentially dashing hopes for early rate cut

- But any disappointment would increase the odds of a technical recession

- Data due at 07:00 GMT, Friday, will be key to sustaining pound’s uptrend

Confounding expectations

The British pound was the second best performing major currency of 2023, ending the year with gains of 5.2% against the US dollar. Unfortunately, the pound’s bullish streak had more to do with out-of-control inflation than an exceptionally strong economy, but nevertheless, the Bank of England looks set to be one of the least dovish central banks in 2024.

On the bright side, the UK economy has been able to withstand several major headwinds far better than anyone anticipated. So although growth has been near stagnant for the past two years, it’s steered clear of a recession. But the risk of one is rising and the fourth quarter of 2023 could be when the economy succumbs to the pain of high interest rates and weak global demand and slips into recession.

On the brink of a recession

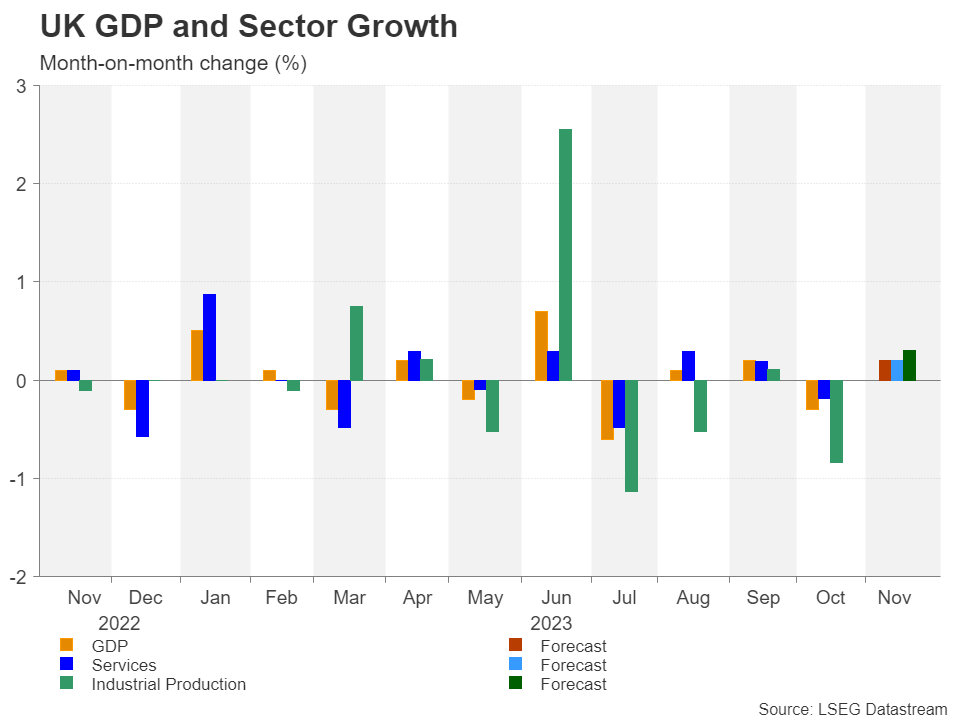

Revised data for the third quarter showed that GDP contracted by 0.1% q/q, while in the first month of the fourth quarter, output declined by 0.3% m/m. However, it appears that the economy started regaining some momentum towards the end of the year, driven primarily by a rebound in the services sector, as indicated by the S&P Global PMI surveys. Thus, the British economy may narrowly avoid a recession if the actual data follows in the PMIs’ footsteps.

Analysts expect GDP to have grown by 0.2% m/m in November. This would put the 3-month average at -0.1% so a positive figure is also needed for December to dodge a negative print for the full quarter. But it seems that the recent sharp drop in inflation combined with the BoE putting the brakes on further rate hikes have lifted optimism among UK businesses, raising hopes that GDP eked out modest growth in the final three months of 2023.

Looking at the breakdown of the GDP components, the services sector is expected to have expanded by 0.2% m/m, and manufacturing by 0.3%, while broader industrial output is forecast to have risen by 0.3%.

Can the pound stay on an uptrend?

If the economy fails to expand in November, or even contracts, there would be little chance of any pickup in December being substantial enough to turn quarterly GDP growth positive. The pound is therefore likely to come under pressure from any disappointing figures.

Having bounced off the ascending trendline only last week, cable could again test this crucial support line in such a scenario, putting strain on the $1.26 handle. A break below the trendline would turn the attention on the 50- and 200-day moving averages, which just achieved a golden cross in the $1.2540 region. A steeper selloff could see cable tumbling all the way to the historically congested $1.2375 zone.

However, if the November GDP estimate exceeds expectations, the timing of any recession is bound to be pushed back again along with that of the first rate cut. The pound could extend its latest upswing towards the December high of $1.2827. A successful break above it would quickly bring the $1.3000 mark into scope, which would then raise the prospect of cable surpassing the July peak of $1.3144.

Politics and inflation path will be key for sterling

Investors have pared back some of their dovish expectations for the Bank of England in January following a similar shift in Fed rate cut bets. Nonetheless, a 25-basis-point cut is nearly fully priced in for May, with further similar-sized reductions seen in almost all the remaining meetings of the year.

This would likely keep GBP bulls in check as cumulative rate cut bets for the Fed aren’t significantly higher, although even if UK CPI does fall in line with market expectations, looser fiscal policy domestically is one factor that could compromise the BoE’s fight against inflation.

With a general election likely to take place sometime in the second half of the year, there is speculation the ruling Conservative party will announce fresh tax cuts in the government’s March 6 budget, in addition to those announced in the Autumn Statement. But a Labour win in the election wouldn’t necessarily mean tighter fiscal policy as any reversal in tax cuts would probably be replaced by higher spending.

So to sum up, although the pound’s uptrend lost some steam at the start of the year, the risks in the medium term remain tilted to the upside.

EUR/GBP Technical: Short-Term Relative Weakness of EUR Reasserts Against GBP

- Persistent underperformance of the EUR against GBP as the EUR/GBP cross pair reintegrated below the 200-day moving average.

- The hourly RSI momentum indicator of EUR/GBP has flashed out a bearish momentum condition.

- Watch the 0.8615 key short-term resistance with intermediate supports coming in at 0.8550 and 0.8500.

In the long term, the EUR/GBP cross pair is still evolving within a major downtrend phase as depicted by its price actions’ oscillations within a descending channel in place since the 3 February 2023 swing high of 0.8979 (see Fig 1)

The major downtrend phase has remained intact since 3 February 2023

Fig 1: EUR/GBP medium-term trend as of 9 Jan 2024 (Source: TradingView, click to enlarge chart)

Short-term downside momentum has resurfaced

Fig 2: EUR/GBP minor short-term trend as of 9 Jan 2024 (Source: TradingView, click to enlarge chart)

Recent price actions have staged a bearish breakdown below its 200-day moving average at the start of 2024 on 3 January.

On the hourly chart, the price actions have taken the form of a minor descending channel with a bearish momentum reading seen in the hourly RSI momentum indicator as it staged a bearish reaction right below its parallel resistance at the 50 level.

These observations suggest that the EUR/GBP is likely to be staging a potential bearish impulsive downmove sequence within its major descending channel.

Watch the 0.8615 key short-term pivotal resistance with the next intermediate supports coming in at 0.8550 and 0.8500 (psychological & the swing low areas of 11 July/23 August 2023) next.

On the other hand, a clearance above 0.8615 negates the bearish tone for a minor corrective bounce to see the next intermediate resistance coming in at 0.8650 (also the 200-day moving average).

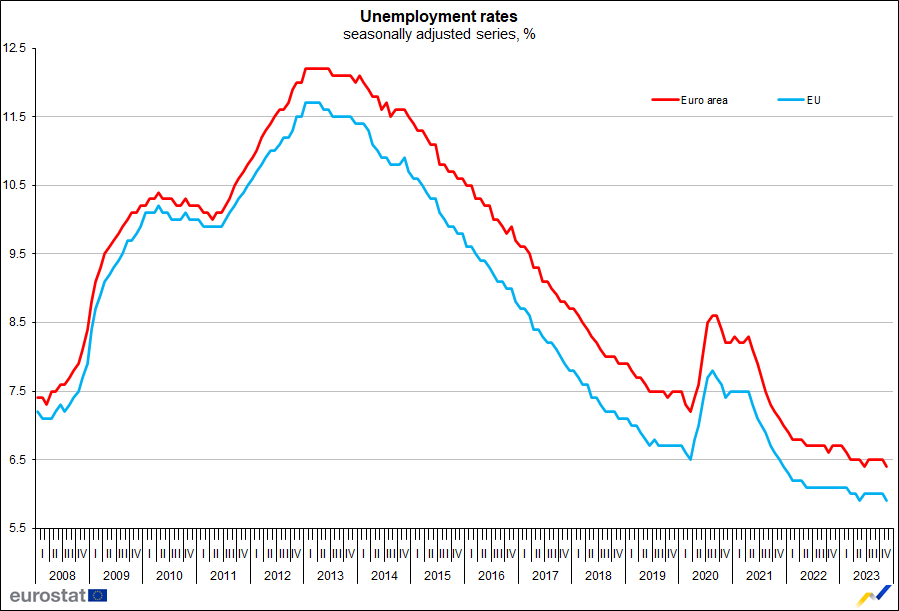

Eurozone unemployment rate falls to 6.4% in Nov, EU down to 5.9%

Eurozone unemployment rate fell from 6.5% to 6.4% in November, below expectation of 6.5%. EU unemployment rate fell from 6.0% to 5.9%.

According to Eurostat, total number of unemployed individuals in EU stood at approximately 12.954m, with around 10.970m of in Eurozone. This figure represents a decrease of -144k unemployed persons in EU and -99k in Eurozone compared to October.

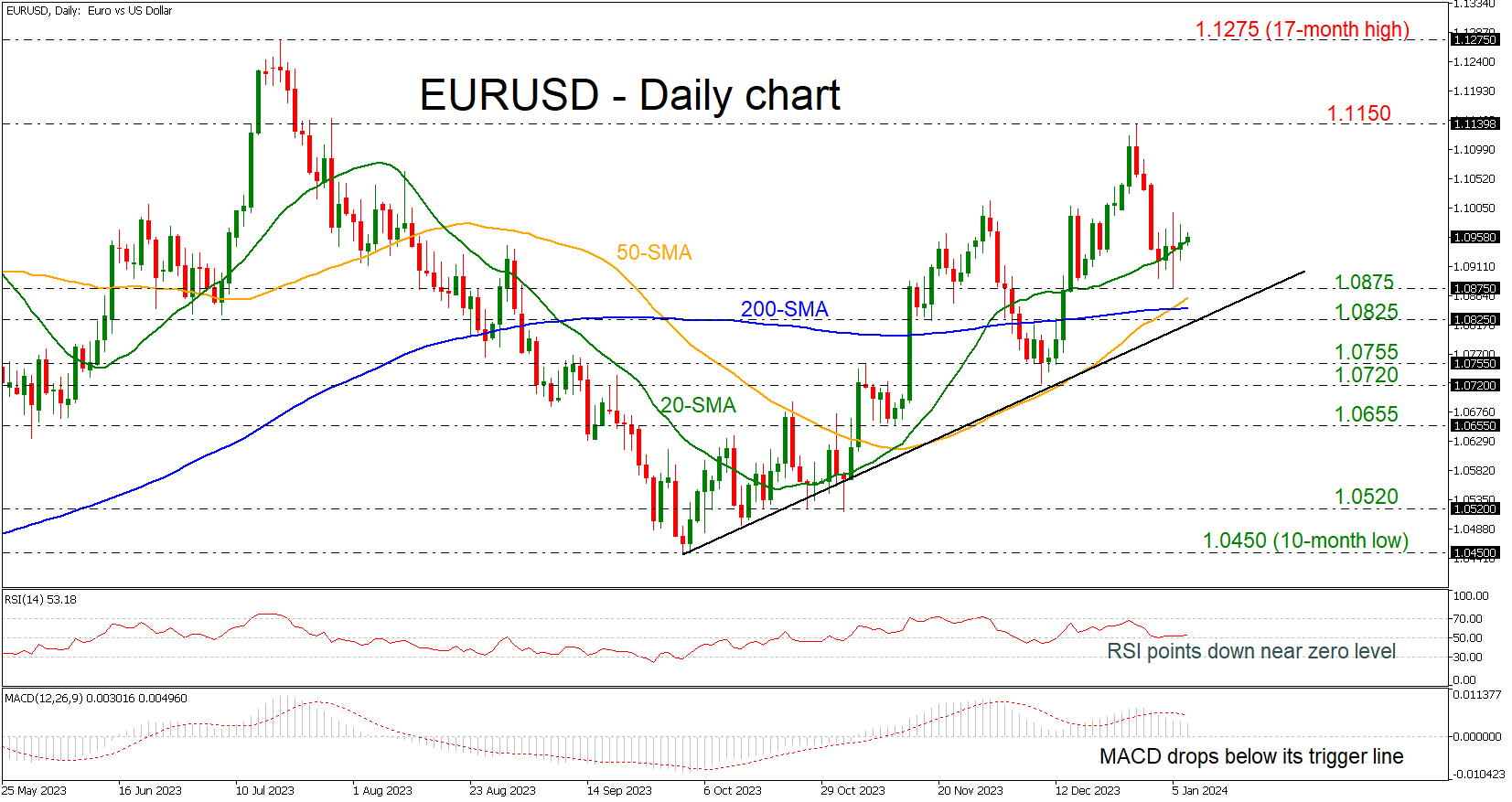

EURUSD Flirts With 20-day SMA

- EURUSD rebounds off 1.0875

- 50- and 200-SMAs post golden cross

- Price is still well above uptrend line

EURUSD is rising somewhat after the pullback off the 1.0875 support level and has been battling with the 20-day simple moving average (SMA) over the last four sessions.

It is worth mentioning that the 50- and the 200-day SMAs posted a golden crossover suggesting more gains in the next few sessions, while the technical oscillators are contradicting each other. The RSI is pointing slightly up above the neutral level of 50; however, the MACD is holding beneath its trigger line and above the zero level, indicating that the bearish correction from 1.1150 may continue.

If the bulls continue to have control, then the market could touch the 1.1150 barrier, taken from the previous peak ahead of the 17-month high of 1.1275, registered back in July 2023.

Alternatively, a potential drop below the immediate 20-day SMA and the 1.0875 barricade could send the market until the important 200-day SMA at 1.0840 ahead of the medium-term ascending trend line near the 1.0825 support. Penetration of these lines may change the outlook to bearish, leading the price towards the 1.0720-1.0755 restrictive region.

All in all, EURUSD is looking bullish in the medium-term outlook and only a fall below the uptrend line may switch the outlook to negative.

GBPUSD Gains Some Confidence for New Higher High

- GBPUSD returns above key support trendline, reduces negative risks

- Technical signals are encouraging for a continuation to 1.2850-1.2900

GBPUSD stepped on the 20-day simple moving average (SMA) and climbed back above the broken short-term support trendline from October at 1.2720, reviving hopes that the soft four-day bullish wave could gain extra legs in the coming sessions.

The positive trajectory in the RSI and the stochastic oscillator is endorsing the bullish case, increasing the odds for a bounce towards the 1.2850-1.2900 resistance region. Note that the short-term ascending line from November 2023 is passing through this area. Hence, a decisive close above it could encourage a direct flight towards the 1.3000 psychological mark and the tentative ascending line, which connects the highs from October and November.

On the downside, the 20-day SMA will remain under the spotlight at 1.2686. A break below that line is expected to see a test near the crucial floor of 1.2610. If the bears drive below that base, confirming a negative head and shoulders pattern, the price could tumble towards its 50- and 200-day SMAs, which are currently trying to complete a golden cross around 1.2532. Additional declines from there might last till the 2020 upward-sloping trendline at 1.2400, unless the 1.2460 barrier blocks the way down.

All in all, GBPUSD has restored some optimism in the short-term picture after the close above the 1.2720 bar. Overall, the outlook may not deteriorate unless the 1.2610 floor cracks.

Dow Futures (YM) Doing Elliott Wave Corrective Pullback

Short-term Elliott Wave View in Dow Futures (YM) suggests that the rally to $38115 high has ended the cycle from the 10.27.2023 low in wave (3) as 5 wave impulse structure. Down from there, the index is doing a corrective pullback in wave (4) against the October 2023 low cycle. And is expected to find buyers in 3, 7, or 11 swings looking for more upside. We will explain the forecast in 30 Minutes chart below:

Down from $38115 high the index is doing a corrective pullback when the initial decline to $37664 low ended wave (w) in a lesser degree 3 wave. Then a bounce to $37985 high ended wave (x) in another 3 waves. Below from there, the (y) leg lower ended at $37504 low after reaching the extreme area at $37534- $37427 area. Thus completed wave ((w)) as a double correction. Since then, the index is doing a short-term bounce in wave ((x)) as the Elliott wave expanded flat correction. Whereas small wave (a) ended at $37882 high. Wave (b) ended at $37470 low and wave (c) is expected to fail against $38115 high.

Dow Futures (YM) 30 Minutes Elliott Wave Chart

Dow Futures (YM) Elliott Wave Video

https://www.youtube.com/watch?v=QGlJhYmsES4

Dollar and Euro Keep Each Other Balanced

Markets

The recent core bond yield recovery ran into resistance yesterday and that had knock-on effects on other markets. Equity markets in particular enjoyed a nice run. The EuroStoxx50 ended about 0.5% higher but that followed a 1% intraday rise. The tech-heavy Nasdaq on Wall Street posted 2% gains. As for yields, they finished 1-2.7 bps lower in the US. They were down as much as 8 bps earlier on the day though, hitting the low point in the wake of the NY Fed’s consumer inflation expectations survey. The one-year ahead gauge fell to a 3-year low of 3.01% while the three-year forward looking indicator eased from 3% to 2.62%. Other subsets point at relative confidence in the US labour market (mean probability of leaving a job voluntarily rises) but the proportion expecting to miss out on a debt payment rose towards the previous post-pandemic high. German Bund yields missed out on the US bottoming out process that followed but finished no more than 3 bps lower. Addressing the economic outlook, Fed’s Bostic said inflation has eased more than expected but added he is comfortable with the current restrictive stance. He repeated his call for only 50 bps of rate reductions this year, starting in Q3. Lowering the pace of QT is an open question, Bostic added. And according to Fed’s Bowman, we’re not at the point yet where rate cuts are appropriate. Instead she warned that easing financial conditions – as seen in November and December – risk fueling inflation. The dollar lagged major peers with minor gains for EUR/USD (to 1.0950) & losses for the DXY (102.20) and USD/JPY (144.23). Sterling was once again among the better performers. It broke sub EUR/GBP 0.86 support. Norway’s krone underperformed on sliding oil prices (-3.5% for Brent). The Saudi’s cutting prices sharply for its Middle Eastern supplies underscored tepid physical demand, including (and perhaps especially) in China. Turning to Asian dealings this morning, Japan reopens after a long weekend. Bond yields ease a few bps. Tokyo inflation for December matched expectations almost perfectly. Headline prices rose 2.4% while core gauges came in at 2.1% (ex. fresh food) and 3.5% (ex. fresh food & energy). All of them marked a slight deceleration from the November readings. Initial yen gains after the BoJ indicated a cut in monthly long-term bond purchases were pared in the meantime. The dollar and euro keep each other balanced in a quiet trading session. Unfortunately, the economic calendar today again has not that much to offer. We do keep a close eye at the start of the US’ monthly refinancing with a $52bn 3-year auction. Belgium’s 10-y OLO benchmark syndication as well as Italy’s 7-y launch further add to the typical January wall of bond supply, which we in general consider to be an important driver for yields going forward but perhaps also today. We assume their downside nevertheless is well protected after the recent decline. EUR/USD for the time being remains a technical/risk sentiment trade without a clear direction.

News & Views

The British Retail Consortium (BRC) published its December retail sales monitor. Many retailers faced a disappointing December with sales growth only up 1.7% on 2022. The festive period failed to make amends for a challenging year of sluggish retail sales growth, as weak consumer confidence continued to hold back spending. Households remain cautious about making larger purchases. BRC CEO Dickinson warns that 2024 looks to be another challenging year for retailers and their customers and spending will continue to be constrained by high living costs. The rise to business rates this April is another big challenge.

The speaker of Slovak parliament and leader of the Hlas-party which joined the Smer-led coalition under PM Fico after October elections last year, Peter Pelligrini, said that he would formally announce his candidacy to run for president on January 19. Presidential elections will be held on March 23 with a potential second round on April 6 if none of the candidates gets an absolute majority. A Pelligrini victory would cement the recent (eurosceptic) power shift as the Slovak president holds more than a symbolic role. The current pro-European Slovak president, Caputova unexpectedly called new presidential elections for personal reasons.