Sample Category Title

Sunset Market Commentary

Markets

Economic data were few today. Still core bond yields continued the bottoming out process that started last week, with Europe this time taking the lead. German yields are rising between 5-6 bps across the curve. Supply obviously was the name of the game today. According to Bloomberg analyses, a record of at least (probably more) than €43 bln of bonds (financials corporates and government related paper) was to be priced today. The sale of a dual Italian 7-y (€10 bln, new syndication 2031 bond) and 30-y tap (€5 bln) enjoyed ample investor buying interest, with books of the 30-y sale reported at a record of over €91 bln. The spread on the 10-y BTP even eased marginally in a daily perspective (-2 bps). Belgium also successfully launched the new 10-y October 2034 OLO 100 bond. The Belgian debt agency sold €7 bln at MS +24 bps with investor demand said to have been in excess of €72 bln. US yields for now outperform Bunds with yields easing between 1.5 bps (2-y) and 2.5 bps (30-y) The US Treasury will start its monthly refinancing with the sale $52 bln of 3-y notes later today. For now, investors apparently didn’t ask big price concessions going into the sale. Market resilience, amongst others, probably suggests that investors prepare for rather soft US December CPI data, to be published on Thursday. Even so, investors’ appetite for credit didn’t positively inspire broader risk sentiment. On the contrary, European equities failed to build on yesterday’s quite impressive US tech rally. The EuroStoxx 50 is ceding 0.75%. US indices also open up to 0.70% at the open (Nasdaq) as investors take a more cautious approach going into the start of the earnings season. Yesterday’s setback in the oil price is partially reversed with Brent oil again trading north of $77 p/b.

On FX markets, the dollar wins in on points (DXY 102.38), but the picture remains unchanged/indecisive. EUR/USD also declines marginally (1.094), but even first minor support (1.0877) stays out of reach. The yen slightly outperforms (USD/JPY 143.85). EUR/GBP after yesterday’s decline tried to sustain below the 0.86 big figure, but further sterling gains for now are running into resistance. Poor BRC retail sales data this morning questioned more positive news from the December PMI’s.

News & Views

French President Macron named Gabriel Attal, currently education minister, as new Prime Minister in a high profile government reshuffle to boost his party’s dwindling support ratings ahead of European elections later this year. A 10-point polling gap recently opened up with Marine Le Pen’s far-right party (RN). Macron’s government was also dealt a humiliating defeat back in December on long-promised immigration reforms. Lacking a parliamentary majority since 2022 elections, opposition parties initially united to block the reforms. Macron had to toughen his proposal to eventually win the backing of Le Pen’s RN. Gabriel Attal will be the youngest French PM (34y), replacing Elisabeth Borne. He is widely considered to be Macron’s heir in 2027 presidential elections when Macron hits his term limit.

Hungary’s full-year budget deficit was 4.59tn forint in 2023. The Finance Ministry initially targeted 2.28tn HUF, but the Orban government gradually raised the target from 3.9% of GDP via 5.2% of GDP to eventually 5.9%. Economy minister Nagy already questioned whether this year’s deficit target of 2.9% of GDP was reasonable given the size of the adjustment it would require. Rating agency Fitch in December suggested that a deficit narrowing up to 4.2% of GDP was a more likely scenario given that the Ministry of National Economy plans to keep the investment rate above 25% of GDP and wants to increase the employment rate to 85% via direct government programs. The Hungarian forint trades in the defensive today with EUR/HUF rising from 377.50 to 379. Separately, the Hungarian statistical office announced that industrial production declined by 5.6% Y/Y in November. In the first eleven months of the year industrial production was 4.8% lower than in the same period of 2022.

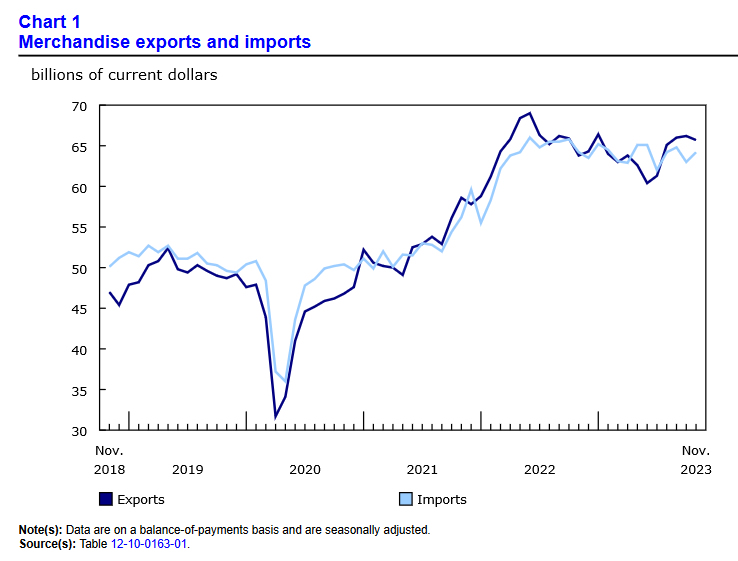

Canada’s Trade Accounts Register a $1.6 Billion Surplus in November

Canada’s merchandise trade surplus notched its fourth consecutive month in black ink. However, November's surplus narrowed to $1.6 billion as imports rose and exports edged lower. This comes after October's surplus was revised upward to $3.2 billion.

Exports fell slightly by 0.6% month-on-month (m/m) in November, the first decline in four months. The contribution to the drag was narrowly-based, driven by a -16.8% decrease in aircraft and other transportation equipment exports. In fact, 7 of 11 sectors posted a rise in exports, including a 1.3% m/m increase in energy product exports and a 4.4% m/m increase in industrial machinery exports.

Meanwhile, total imports increased by 1.9% m/m in November, with 8 of 11 sectors rising on the month. Imports of energy products (11.6% m/m) posted its first increase after two consecutive monthly declines. Meanwhile, imports of machinery and equipment were up by 4.9% m/m and imports of electronic and electrical equipment rose by 4.7% m/m.

In volume terms, overall imports increased by 1.6% m/m in November (after a large 3.5% m/m drop the month prior), while exports edged down slightly by 0.1% m/m.

Canada's trade surplus with the United States narrowed from $12.1 billion in October to $11.7 billion in November.

Key Implications

October and November trade data suggests that net trade may shape up to be a tailwind for fourth quarter growth. This would mark a reversal from last quarter's significant growth revisions that hit net trade more than any other GDP component. The solid performance of the Canadian dollar at the end of 2023 (up over 2% versus the USD in December), may potentially dampen export activity in next month's trade reading.

Despite the potential positive effects from trade in the fourth quarter, overall Canadian economic growth is expected to be weak as domestic and international activity slows. Imports, a barometer for domestic demand, have been effectively flat (in real terms) over 2023.

U.S. Small Business Optimism Improved Moderately at End of 2023

NFIB's Small Business Optimism Index rose 1.3 points to 91.9 in December, coming in above market expectations for a modest increase. Despite the increase, the index was still 6 points below its historical average of 98 points.

Five of the ten subcomponents improved on the month, three deteriorated, and two remained unchanged. Leading the gains were earning trends (up 7 points to -25%), along with expectations about an improvement in the economy (up 6 points to -36%) and higher real sales (up 4 points to -4%). On the other hand, current inventory took a notable step back, falling 5 points to -5%.

The share of businesses planning to increase employment fell 2 points to a still-decent 16%, while the share of firms with unfilled job openings held steady for the second consecutive month at 40%. Of note, quality of labor concerns fell 4 points, with 20% of business owners identifying this as their top business problem. Given the sharp drop in the latter, inflation replaced labor quality as the top concern among small business owners (up 1 point to 23%).

The share of firms increasing compensation was unchanged at 36%, the same as in the pre-pandemic period. Meanwhile, the share of firms planning to raise compensation over the next three months fell one point to 29%, which is not far off the 32% historical high set earlier in the pandemic. The share of businesses 'raising' average selling prices was unchanged at 25%, while the share of firms planning price hikes in the next three months fell 2 points to a still elevated 32%.

Key Implications

The improvement in small business confidence at the end last year – albeit from low levels – is encouraging, especially since it was accompanied by enhanced outlooks on the economy, earnings trends and sales. What's more, labor market indicators continue to show resilience, with job opening still plentiful and businesses continuing to place a focus on hiring workers. Nonetheless, it's worth noting that this latter theme is gradually losing some of its luster. This is evidenced by a gradual easing in plans to boost employment, and the fact that quality of labor concerns pulled back notably in December.

With the labor market still tight, the share of businesses planning to raise compensation in order to retain and attract new workers remains elevated. The share of businesses planning to raise average selling prices has also trended higher, which points to some upside risk for inflation over the near-term – a factor that would work in favor of the Fed showing some patience before it begins to lower interest rates later this year.

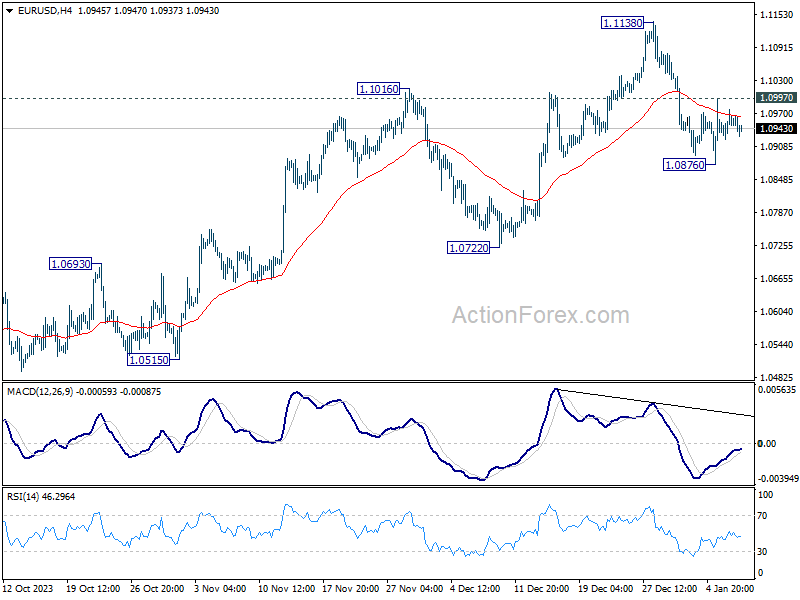

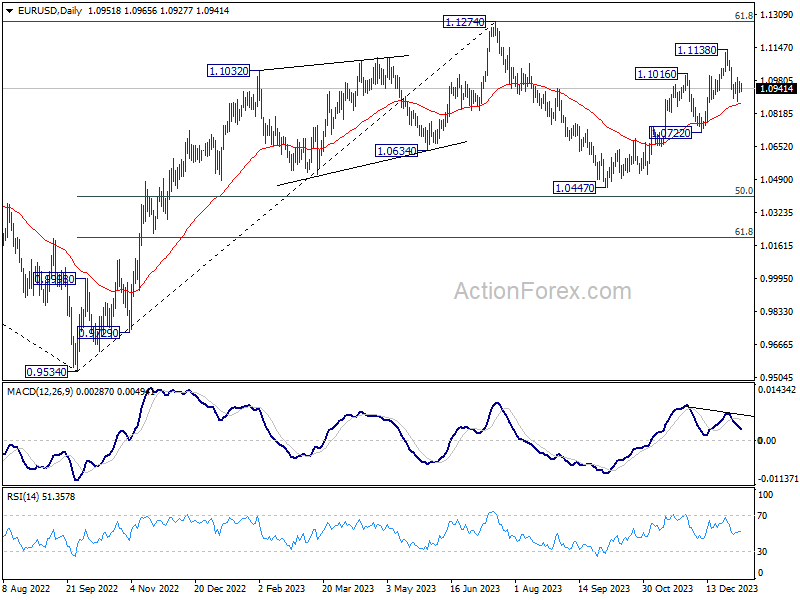

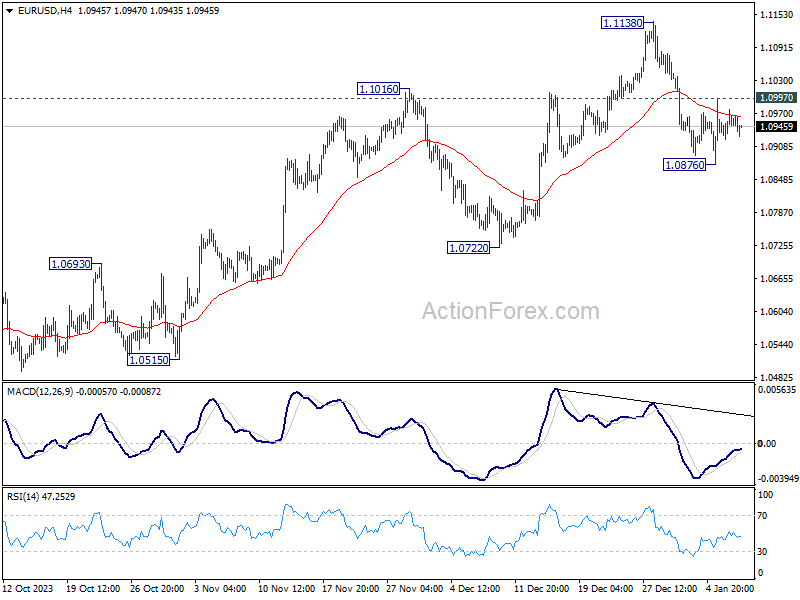

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0922; (P) 1.0951; (R1) 1.0978; More...

Range trading continues in EUR/USD and intraday bias remains neutral at this point. On the downside break of 1.0876 will resume the fall from 1.1138 short term top to 1.0722 support next. However, break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

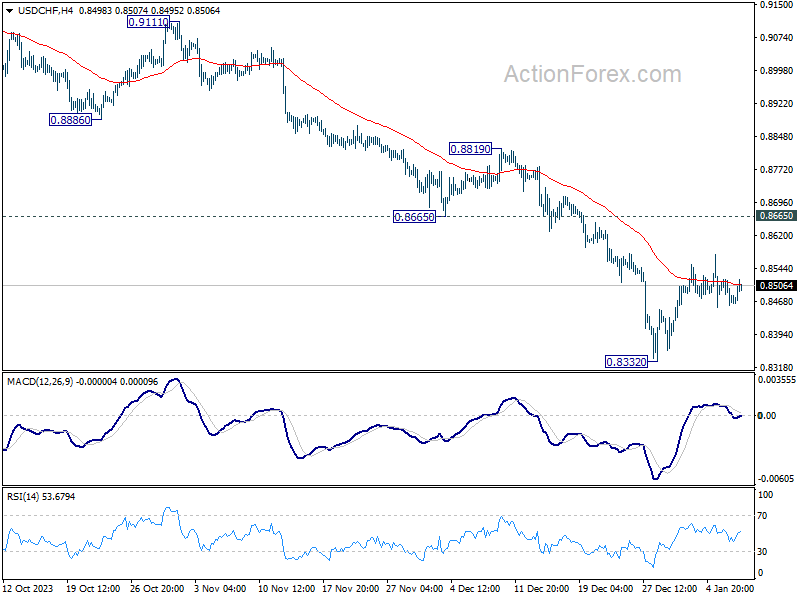

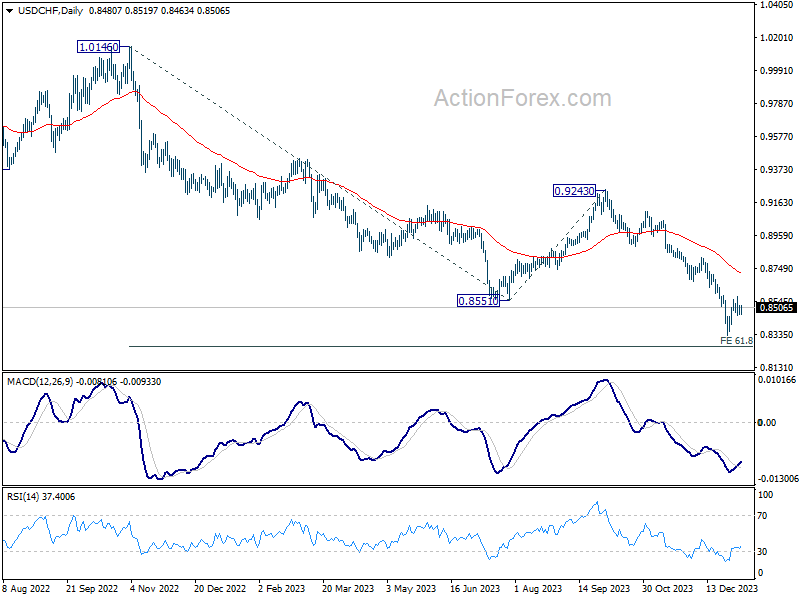

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8453; (P) 0.8488; (R1) 0.8516; More....

USD/CHF is extending the consolidation from 0.8332 and intraday bias stays neutral. While recovery could extend higher, outlook will stay bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, the down trend from 1.0146 (2022 high) is in progress. Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

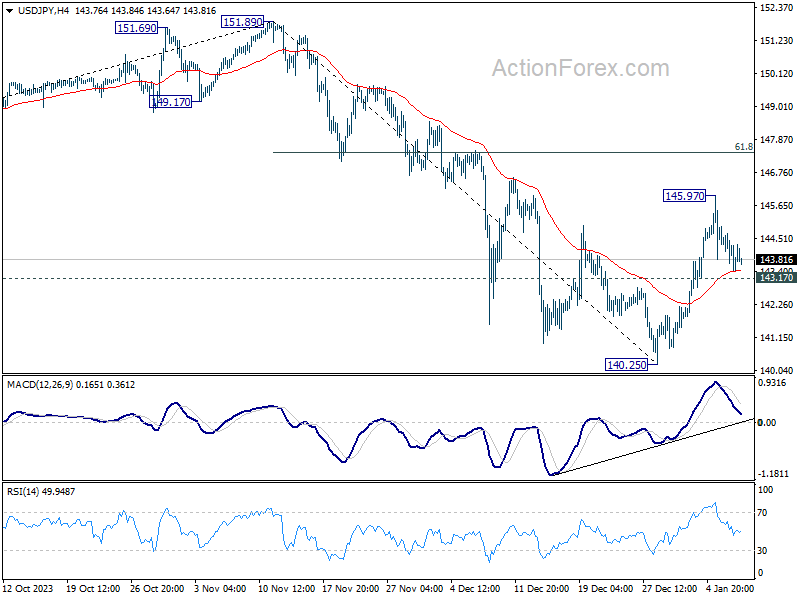

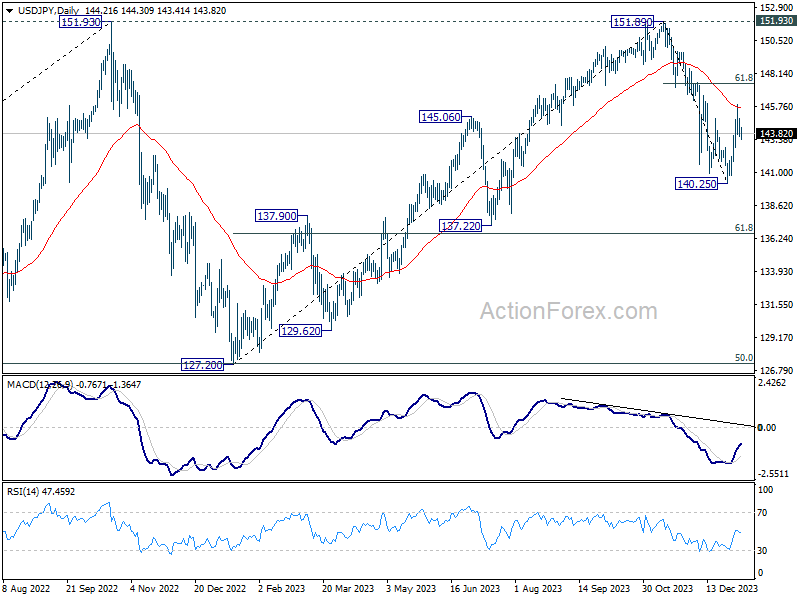

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.63; (P) 144.27; (R1) 144.89; More...

Range trading continues in USD/JPY and intraday bias stays neutral. On the upside, above 145.97 will resume the rebound from 140.25. But upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. On the downside, below 143.17 minor support will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

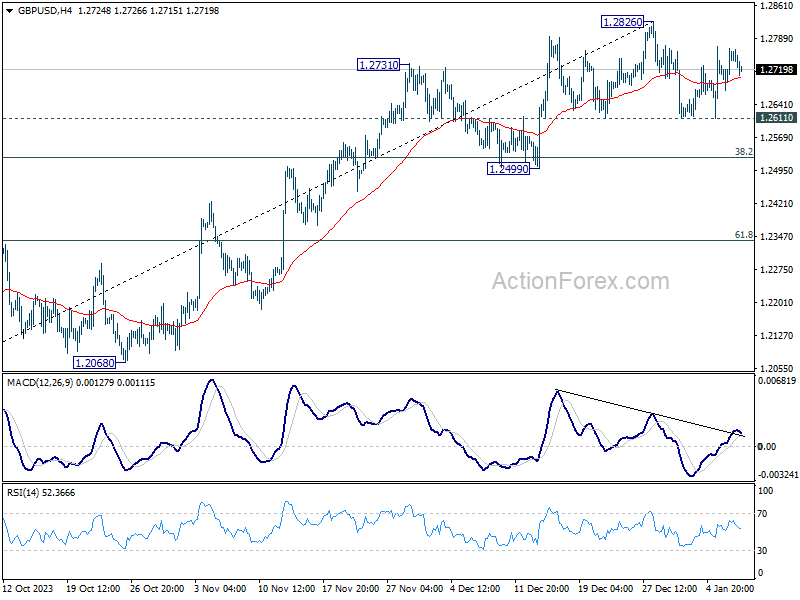

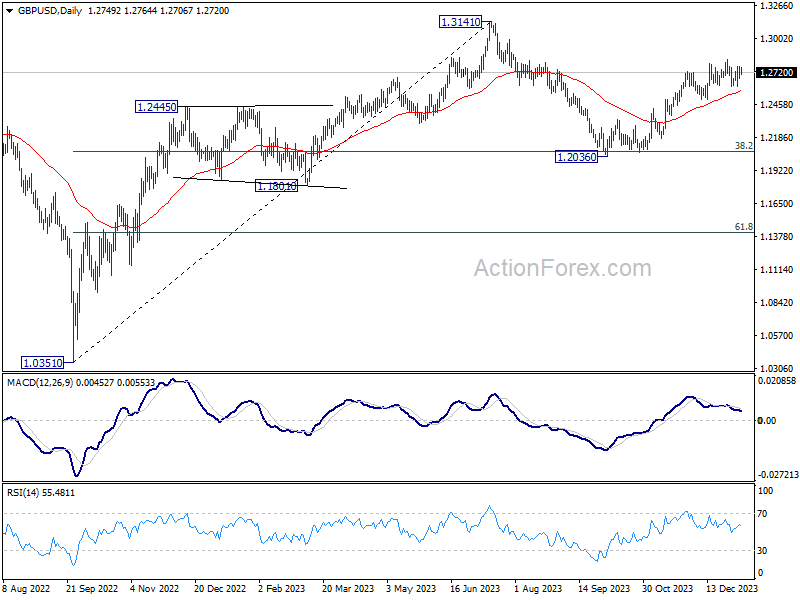

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2692; (P) 1.2729; (R1) 1.2786; More...

GBP/USD is extending sideway trading below 1.2826 and intraday bias remains neutral. On the upside, decisive break of 1.2826 high will resume whole rally from 1.2036. Nevertheless, another fall and break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Lackluster Trading in Forex as Economic Data Fails to Stir Major Movements

Currency trading today remained lackluster, characterized by limited movements across major pairs and crosses. Key economic data releases, ranging from Japan's Tokyo CPI, and retail sales figures from Australia and the Eurozone, to trade balance data from Canada and US, failed to significantly influence the markets.

Japanese Yen is currently a marginally stronger currency, continuing its near-term recovery. Dollar follows closely, ranking as the second strongest . Conversely, Australian Dollar remains at the lower end of the performance chart, facing additional downward pressure due to selling against Canadian Dollar and New Zealand Dollar. Meanwhile, Euro experienced a mild uplift, primarily driven by its recovery against British Pound and Swiss Franc.

Looking ahead, the overall risk sentiment in the markets could become a key driver in forex, especially today, if there are sustainable movements in the stock markets. US futures are indicating lower open, with NASDAQ leading the decline. This is partly fueled by warnings from South Korea's tech giant Samsung, which projected a potential drop of up to 35% in its Q4 operating profit.

From a technical perspective, Dollar may have the potential to extend its near-term rebound against Euro and Australian Dollar, especially if the risk-off sentiment persists. For EUR/USD, a break below 1.0876 temporary low could resume the decline from 1.1138, targeting 1.0722 support level next.

In Europe, at the time of writing, FTSE is down -0.13%. DAX is down -0.60%. CAC is down -0.64%. Germany 10-year yield is up 0.053 at 2.188. UK 10-year yield is up 0.034 at 3.806. Earlier in Asia, Nikkei rose 1.16%. Hong Kong HSI fell -0.21%. China Shanghai SSE rose 0.20%. Singapore Strait Times rose 0.34%. Japan 10-year yield fell -0.0184 to 0.587.

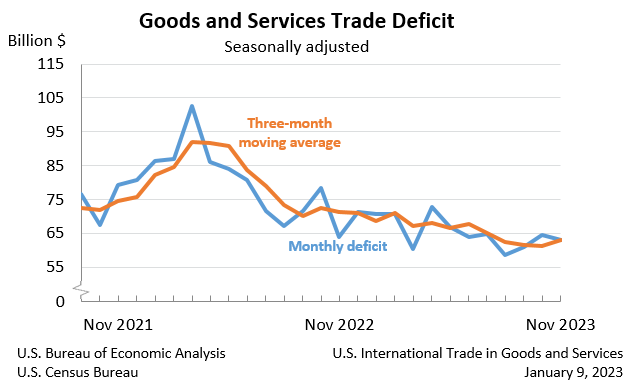

US goods and services exports down -1.9% mom in Nov, imports down -1.9% mom

US goods and services exports fell -1.9% mom to USD 253.7B in November. Imports fell -1.9% mom to USD 316.9B. Trade deficit narrowed slightly from USD -64.5B to USD -63.2B, smaller than expectation of USD -64.8B.

Canada's merchandise exports down -0.6% mom in Nov, imports up 1.9% mom

In November, Canada's merchandise exports fell -0.6% mom to CAD 65.74B. This decrease occurred despite increases in 7 of the 11 product sections. Merchandise imports rose 1.9% mom to CAD 64.17B, with increases in 8 of the 11 product sections.

Merchandise trade surplus narrowed from CAD 3.2B to CAD 1.6B, smaller than expectation of CAD 2.5B.

Services exports rose 1.0% mom to CAD 16.6B. Services imports fell -0.1% mom to CAD 17.6B.

Combining goods and services, exports decreased -0.3% mom to CAD 82.4B. Imports rose 1.5% mom to CAD 81.8B. Trade surplus fell from CAD 2.0B to CAD 594m.

Eurozone unemployment rate falls to 6.4% in Nov, EU down to 5.9%

Eurozone unemployment rate fell from 6.5% to 6.4% in November, below expectation of 6.5%. EU unemployment rate fell from 6.0% to 5.9%.

According to Eurostat, total number of unemployed individuals in EU stood at approximately 12.954m, with around 10.970m of in Eurozone. This figure represents a decrease of -144k unemployed persons in EU and -99k in Eurozone compared to October.

Japan's Tokyo CPI core down for the second month to 2.1%

Japan's Tokyo CPI core, which excludes fresh food, slowed from 2.3% yoy to 2.1% yoy in December, aligning with market expectations. This figure represents the lowest reading since June 2022 and marks the second consecutive month of decline.

Additionally, CPI core-core, which excludes both food and energy, also slipped from 3.6% yoy to 3.5% yoy. This marks the fourth consecutive month of cooling in this measure. Headline CPI, similarly fell from 2.6% yoy to 2.4% yoy. T

Tokyo's CPI figures are often regarded as precursors to the national data, suggesting that a similar trend might be observed in the broader Japanese economy.

In separate report, households reduced their spending in November -by 2.9% yoy, worst than expectation of -2.3% yoy. This decrease in consumer spending is attributed to the rising costs of living, which have led to more selective purchasing behaviors among shoppers.

Australia's retails sales rises 2.0% mom in Nov on Black Friday boost

Australia retail sales rose 2.0% mom to AUD 36.5B in November, above expectation of 1.2% mom. That followed a fell of -0.4% mom in October.

Robert Ewing, ABS head of business statistics, attributed this surge to the impact of Black Friday sales. He noted, "Black Friday sales were again a big hit this year, with retailers starting promotional periods earlier and running them for longer, compared to previous years."

Ewing further explained: "The strong rise suggests that consumers held back on discretionary spending in October to take advantage of discounts in November." Additionally, he observed that shoppers might have advanced some of their Christmas shopping to November, which typically occurs in December.

Looking ahead

Swiss unemployment rate and foreign currency reserves, Germany industrial production, France trade balance, and Eurozone unemployment rate will be released in European session. Later in the day, US will release trade balance. Canada will release trade balance and building permits.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2692; (P) 1.2729; (R1) 1.2786; More...

GBP/USD is extending sideway trading below 1.2826 and intraday bias remains neutral. On the upside, decisive break of 1.2826 high will resume whole rally from 1.2036. Nevertheless, another fall and break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Dec | 2.40% | 2.60% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Dec | 2.10% | 2.10% | 2.30% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Dec | 3.50% | 3.60% | ||

| 00:30 | AUD | Retail Sales M/M Nov | 2.00% | 1.20% | -0.20% | -0.40% |

| 00:30 | AUD | Building Permits M/M Nov | 1.60% | -2.00% | 7.50% | 7.20% |

| 06:45 | CHF | Unemployment Rate M/M Dec | 2.20% | 2.20% | 2.10% | |

| 07:00 | EUR | Germany Industrial Production M/M Nov | -0.70% | 0.40% | -0.40% | -0.30% |

| 07:45 | EUR | France Trade Balance (EUR) Nov | -5.9B | -7.9B | -8.6B | |

| 10:00 | EUR | Eurozone Unemployment Rate Nov | 6.40% | 6.50% | 6.50% | |

| 11:00 | USD | NFIB Business Optimism Index Dec | 91.9 | 90.9 | 90.6 | |

| 13:30 | USD | Trade Balance (USD) Nov | -63.2B | -64.8B | -64.3B | -64.5B |

| 13:30 | CAD | Trade Balance (CAD) Nov | 1.6B | 2.5B | 3.0B | 3.2B |

| 13:30 | CAD | Building Permits M/M Nov | -3.90% | 2.00% | 2.30% |

US goods and services exports down -1.9% mom in Nov, imports down -1.9% mom

US goods and services exports fell -1.9% mom to USD 253.7B in November. Imports fell -1.9% mom to USD 316.9B. Trade deficit narrowed slightly from USD -64.5B to USD -63.2B, smaller than expectation of USD -64.8B.

Canada’s merchandise exports down -0.6% mom in Nov, imports up 1.9% mom

In November, Canada's merchandise exports fell -0.6% mom to CAD 65.74B. This decrease occurred despite increases in 7 of the 11 product sections. Merchandise imports rose 1.9% mom to CAD 64.17B, with increases in 8 of the 11 product sections.

Merchandise trade surplus narrowed from CAD 3.2B to CAD 1.6B, smaller than expectation of CAD 2.5B.

Services exports rose 1.0% mom to CAD 16.6B. Services imports fell -0.1% mom to CAD 17.6B.

Combining goods and services, exports decreased -0.3% mom to CAD 82.4B. Imports rose 1.5% mom to CAD 81.8B. Trade surplus fell from CAD 2.0B to CAD 594m.