Sample Category Title

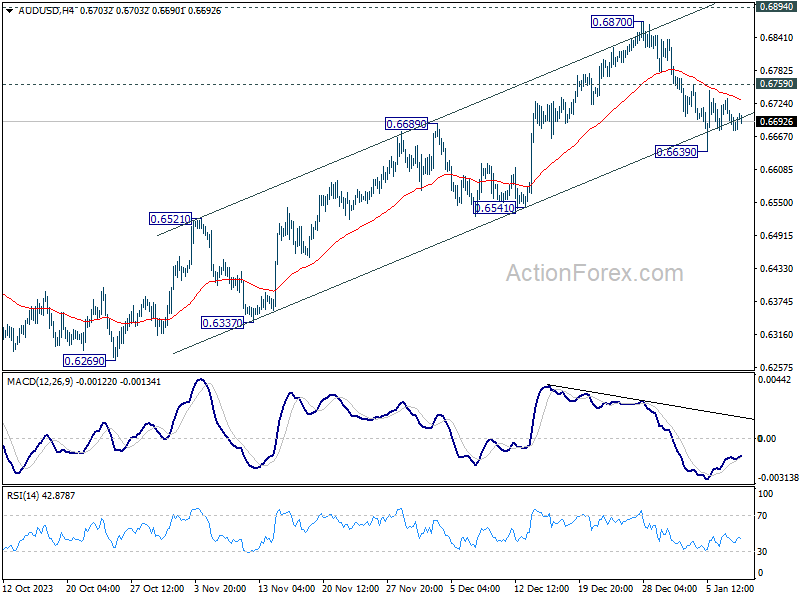

AUD/USD Daily Report

Daily Pivots: (S1) 0.6664; (P) 0.6700; (R1) 0.6722; More...

Intraday bias in AUD/USD is neutral as sideway trading continues. On the downside, break of 0.6639 will resume the fall from 0.6870 short term top to 0.6541 support next. On the downside, though, break of 0.6759 minor resistance will suggest that the pull back has completed already. Intraday bias will be turned back to the upside for 0.6870 resistance.

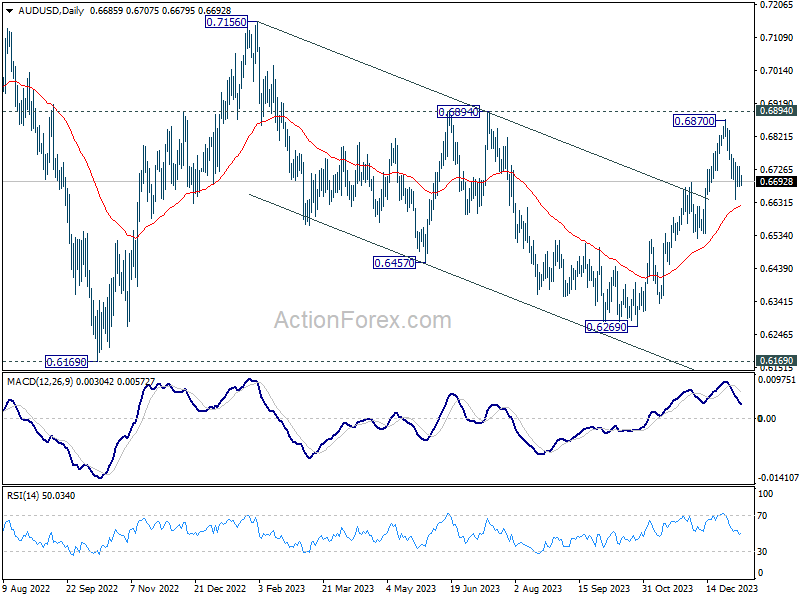

In the bigger picture, price actions from 0.6169 (2022 low) could be just a medium term corrective pattern to the down trend from 0.8006 (2021 high). Rise from 0.6269 is seen as the third leg of the pattern that could target 0.7156 on break of 0.6894 resistance. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

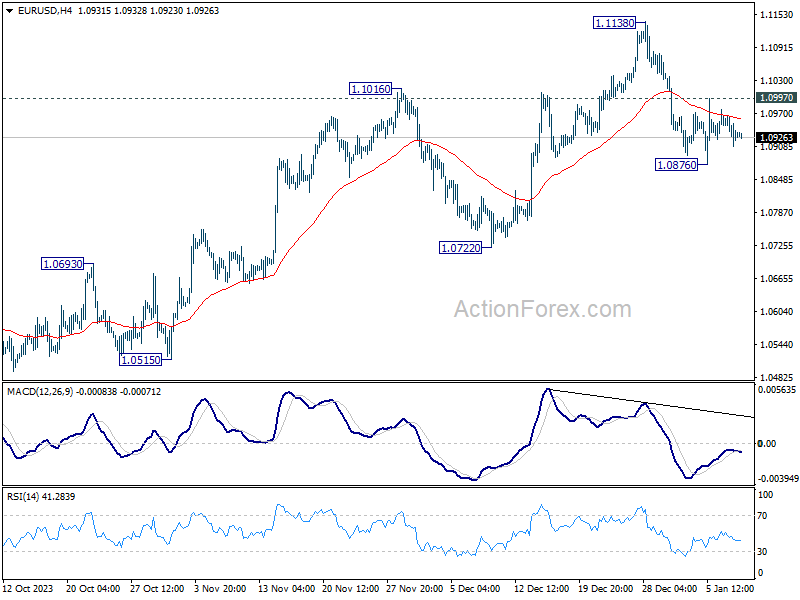

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0906; (P) 1.0936; (R1) 1.0961; More...

Intraday bias in EUR/USD remains neutral as range trading continues. On the downside break of 1.0876 will resume the fall from 1.1138 short term top to 1.0722 support next. However, break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

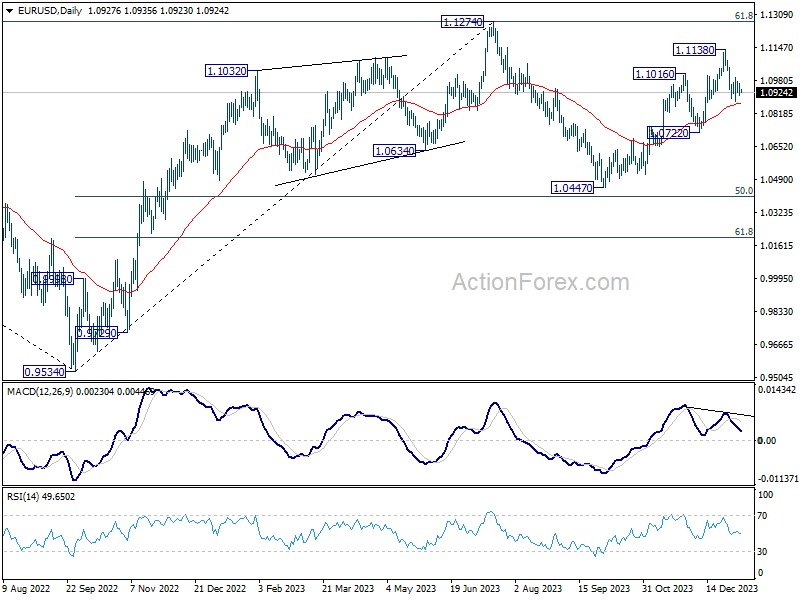

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

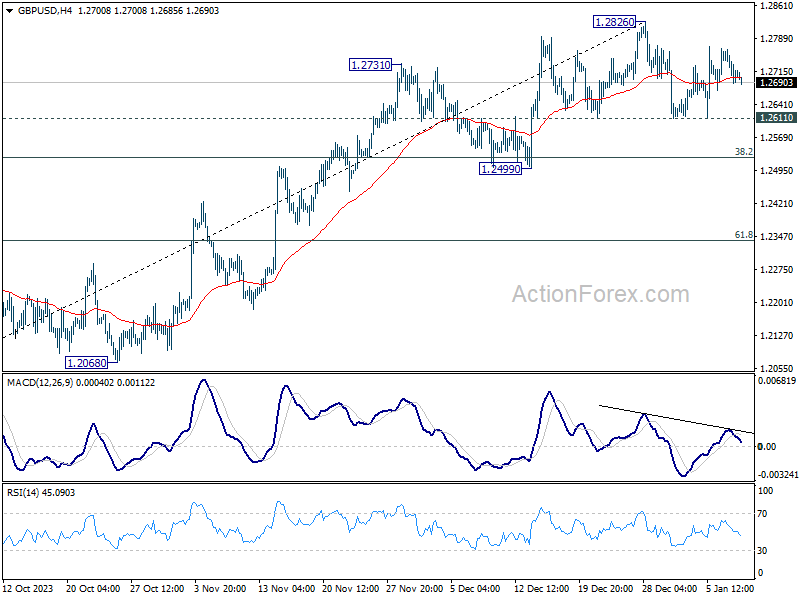

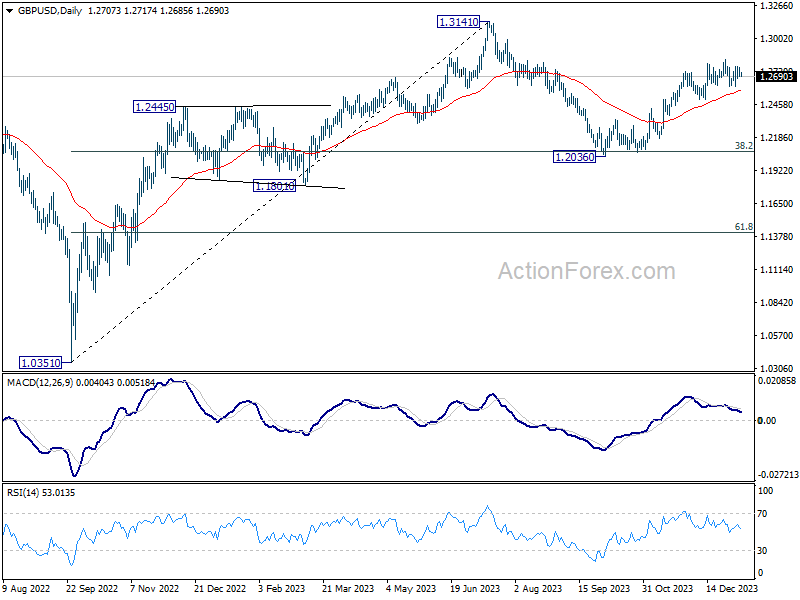

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2678; (P) 1.2722; (R1) 1.2753; More...

Intraday bias in GBP/USD remains neutral as range trading continues. On the upside, decisive break of 1.2826 high will resume whole rally from 1.2036. Nevertheless, break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

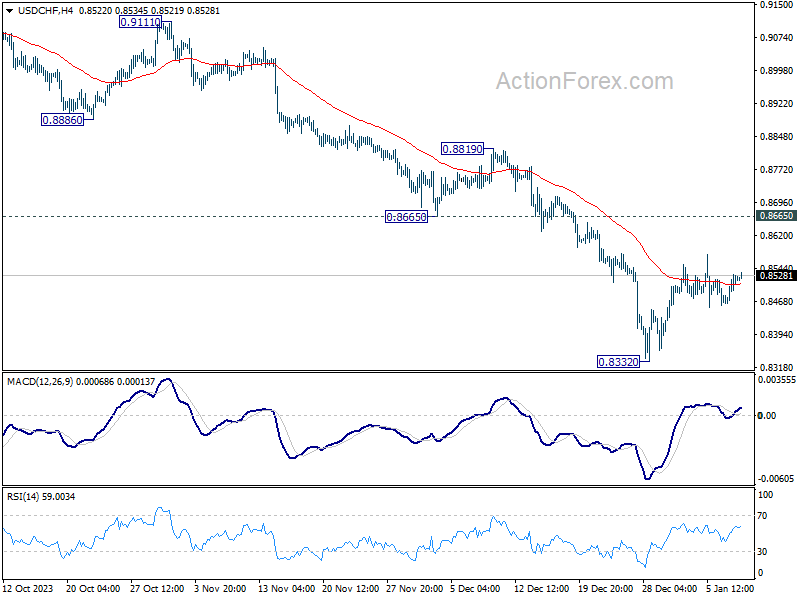

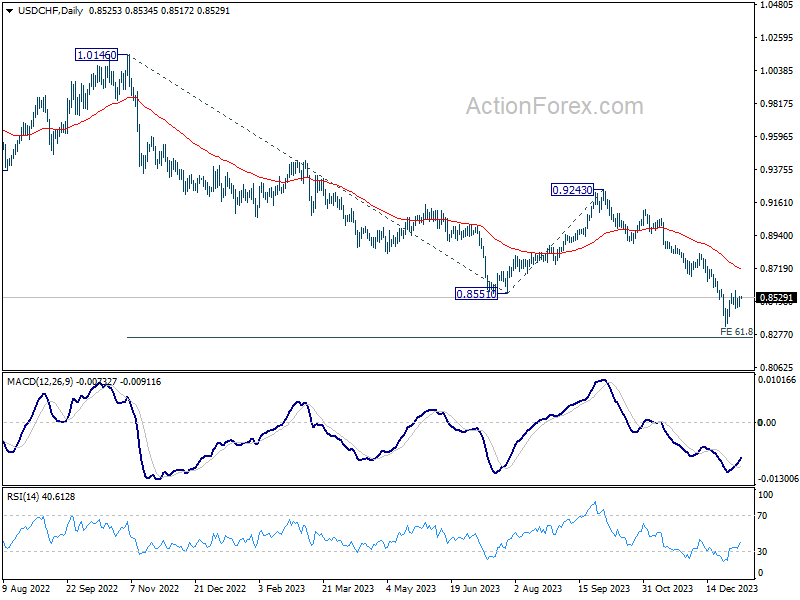

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8482; (P) 0.8507; (R1) 0.8549; More....

Intraday bias in USD/CHF remains neutral and outlook is unchanged. Consolidation from 0.8332 is in progress and stronger recovery cannot be ruled out. But outlook will stay bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, the down trend from 1.0146 (2022 high) is in progress. Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

Weakest Growth Since 1990s

The World Bank said yesterday that it expects growth to fall to 2.2% for the period that includes 2020 and 2024 and that’s the slowest 5-year period since 1990-1994. The slowing global growth expectations somehow keep the global yields subdued, but at 4% yield, the US 10-year bond is expensive and may not have much upside potential left unless fresh data points at softening activity, and ideally a further weakness in consumer prices.

The S&P500 and Nasdaq consolidate a touch below the December high – and both very close to their ATH. The uncertainty and the lack of clear direction will likely be on the menu until the US inflation report is released tomorrow. In case of a soft, and ideally a softer-than-expected report, the rally in both stock and bonds could carry on. Otherwise, profit taking is perhaps what’s best at the actual levels.

On the individual level, the Boeing shares continue to be abated on the Alaska Air incident. Even the news that Boeing posted its largest-ever monthly sales for its 737 Max couldn’t cheer up investors as all 737 Max 9 jets are now grounded until further notice. Boeing’s misfortune is Airbus’ fortune, however, as the Airbus stock hit a record yesterday in Paris.

In the FX, the dollar index is better bid before tomorrow’s US inflation report; the consolidation in US yields prevents a further selloff in the greenback before more clarity on inflation. The downside risks to the dollar prevail as the higher shipping costs due to Red Sea tensions may not show in the December data, hence we may not see the Federal Reserve (Fed) doves take a break this week, but the trade disruptions in the Suez Canal and the rising shipping costs remain a major threat to inflation in the next few months, and that’s a good reason to scale back the Fed rate cut expectations which – with or without the trade disruptions – have become overstretched after the past two-month rally.

Of course, the rising shipping costs concern Europeans as much – if not more – than they concern the Americans. In this context, geopolitical tensions’ relative impact on US and euro area will play a key role in how the central banks would respond to an eventual rise in inflation and how the currencies will settle relative to each other. The European Central Bank (ECB) is much less convinced than the Fed regarding the end of the inflation battle, but the European economies are significantly softer than the US. This means that, even though the ECB continues to fight inflation, the weak economic fundamentals may not let the ECB remain this hawkish for long. And that’s one reason which will likely hold back the euro bulls from loading above the 1.10 level.

Speaking of inflation, inflation in Australia eased to 4.30% in November thanks to a slowdown in food and energy prices. The AUDUSD eased on a softer-than-expected inflation read, yet at 4.30%, inflation in Australia remains well above the Reserve Bank of Australia’s (RBA) 2-3% target range, hence any selloff in AUDUSD should remain limited and could present interesting dip buying opportunities given that the Chinese stimulus measures – that push iron ore prices higher – should also continue to support an appreciation in the AUDUSD to 68-70 cents range.

In energy, the barrel of US crude rebounded 2% yesterday to past $72pb, as the API reported a 5-mio barrel decline in US crude inventories last week and some 600K barrels of increase in US strategic reserves. But the weak global economic outlook, combined with the rising global supply concerns - despite OPEC’s efforts to restrict production – will likely keep the bearish trend intact below the $74/75 resistance range. Besides the record US shale production, Russia is also drilling more activity to keep its production levels intact. PS: in the long term, Russia’s frenetic pace of drilling is a red flag about inefficiencies.

In cryptocurrencies, Bitcoin fell after approaching the $48K level on news that the SEC’s post on X, claiming that the commission granted approval of spot Bitcoin ETFs, was fake. Tension among crypto investors is very high right now provided that it’s just a matter of hours before the SEC is expected to announce approval of spot ETFs. Yet, because investors have been buying the rumours of spot Bitcoin ETFs for months, the actual news could trigger a sell-the-fact reaction. Price pullbacks could be interesting entry opportunities for long-term traders, and hodlers, as the approval of spot ETFs will attract a significant amount of capital in the sector and should have a potentially massive impact on the valuations across the sector.

Focus Turns to Scandinavia

In focus today

Today is a light day on the international data front, but we get a lot of Nordic data.

In Denmark, we get CPI inflation for December 2023. We expect to see that inflation has continued to climb higher to 1.1% y/y, due to base effects from December 2022's decline in fuel and electricity prices. We expect the underlying price pressure to remain low, as it has for the last 3-4 months.

We also watch out for core CPI inflation in Norway for December 2023. Inflation has been more persistent in Norway than in many other countries, in part due to a weakening of the NOK, which has triggered direct and indirect price impulses, and we expect that core inflation will hold up at 5.6% y/y in December.

Finally, we get a slew of November indicators for Sweden. Retail sales should shed some light on how Black Friday sales might have affected consumer spending, while the production value indicator and new orders will shed light on supply-side developments. The broader economy will be summarized by the GDP-indicator, also set to release today.

Economic and market news

What happened overnight: Overnight, wage data from Japan surprised to the downside with a mere 0.2% y/y increase in total cash earnings for November. In real terms, this corresponds to a decline of 3.0% y/y, which highlights the erosion of purchasing power the past years. Looking at the details however, growth in regular workers' core pay only slowed marginally to 1.9% y/y. JPY weakened slightly on the release, as wage growth is a key criteria for the BoJ to be ready to hike the policy rate. We are not likely to see significant growth until the annual Shunto wage negotiations have concluded in the spring. We expect the BoJ to be ready to hike the policy rate out of negative territory and release the grip on the yield curve in Q2 this year.

On geopolitics, US foreign secretary Antony Blinken said Israel must stop undercutting Palestinian governance. Likewise David Cameron expressed concerns that Israel may have broken international law during the Gaza conflict. This on the same day as the Houthis reportedly undertook their largest attack on merchant vessels to date in the Red Sea. As of last night, however, no ships reported having taken damage.

What happened yesterday: It was generally a quiet day in the US, as investors brace for Thursday's CPI release. European yields rose slightly with the 10Y German government bond yield rising some 5-6bp, while 10Y US Treasuries were more stable. Eurozone unemployment surprised to the downside, declining to an all-time low of 6.4% in November. Conversely, the malaise in the German industry continued in November, where production declined 0.7% m/m in real, seasonally adjusted terms. We expect that the German industry will eventually rebound, as leading Asian indicators suggest that the global manufacturing cycle has bottomed out, but it might take longer than in the rest of the Euro area as German industry is more affected by the shutdown of Russian gas supplies.

In line with expectations the Polish central bank yesterday kept their policy rate unchanged at 5.75%.

In China, the PBOC signalled that more monetary easing is on the way, as the head of the monetary policy department said it will use a variety of tools to provide "strong support" for a reasonable growth in credit. Markets reacted by raising the expectations of a cut in the Medium Lending Facility rate, where consensus is for a 10bp cut.

Equities: Equities mostly retreated after the Monday rally. US and European equities shaved off around -0.2%. Despite the small moves, risk off re-emerged behind the surface. The defensive rotation returned, this time financed with materials and energy selling off 1-2%. Small caps also came under renewed pressure (Russell 2000 -1.1%). The sentiment is improving in Asia, and primarily Japan, rallying another 2% this morning. US futures are mildly negative.

FI: There was an upward pressure on European yields with the 10Y German government bond yield rising some 5-6bp, while 10Y US Treasuries were more stable, but still closing just above 4%. There has been a modest tightening of the 10Y spread between Italy and Germany after it initially widened since late December. The spread was trading around 155bp before x-mas and then widened to almost 170bp, but are now back to 165bp after yesterday's successful syndicated deal from Italy.

FX: After a poor Monday the NOK was yesterday's outperformer in Majors space with EUR/NOK moving back to the low 11.30s. EUR/USD edged lower while both EUR/SEK and EUR/GBP moved modestly higher in an overall quiet session. The biggest underperformers were found in the CEEs and in MXN. JPY weakened slightly following lower than expected wage data for November.

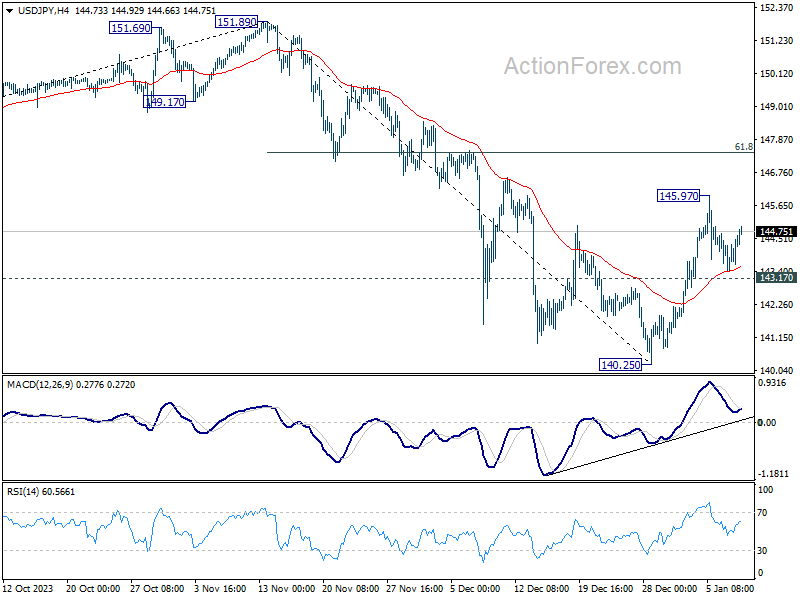

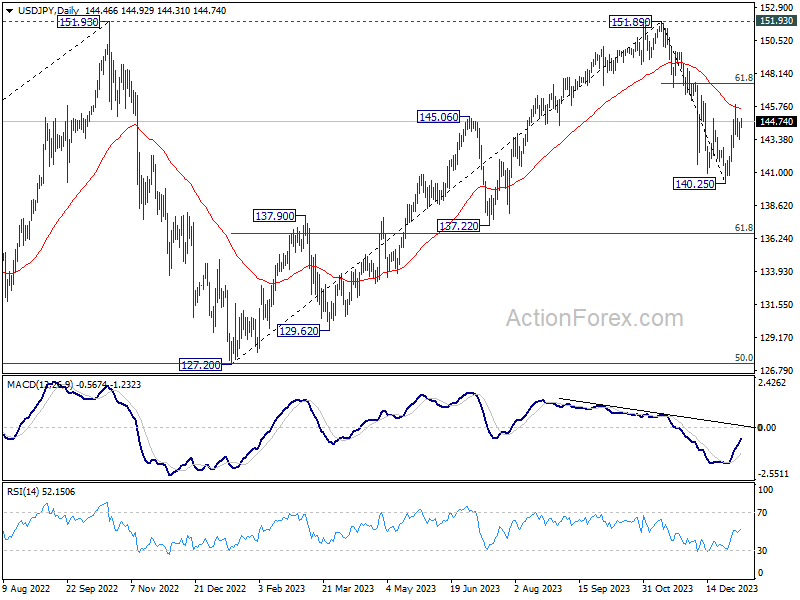

USD/JPY Daily Outlook

Daily Pivots: (S1) 143.73; (P) 144.17; (R1) 144.93; More...

USD/JPY recovered ahead of 143.17 minor support but stays well below 145.97 resistance. Intraday bias remains neutral at this point. On the upside, above 145.97 will resume the rebound from 140.25. But upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. On the downside, below 143.17 minor support will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

Yen Weakens on Disappointing Wage Growth Data, Nikkei Soars to 33-Year High

Release of Japan's disappointing wage growth data led markets to scale back expectations of an imminent rate hike by BoJ. The continued lag in wages growth behind inflation undermines the prospects of establishing a virtuous cycle of wages and prices, which is a prerequisite to a BoJ policy shift. Although a rate hike in April by BoJ remains a possibility, the foundation for such a move is increasingly uncertain given the latest wages data. This development has resulted a broad-based weakening of Japanese Yen, although the decline has been somewhat contained. Concurrently, Nikkei capitalized on this sentiment, reaching new 33-year highs following an upside breakout from a six-month trading range this week.

Elsewhere in the currency markets, commodity currencies are showing signs of recovery, led by Australian Dollar, which seems to be largely unaffected by economic data. Australia's monthly CPI slowed more than anticipated, reinforcing the view that RBA's tightening cycle may have concluded. However, the decisive factor will still be Q4 CPI data, due for release at the end of January. Dollar and European major currencies are currently the weaker ones, continuing to engage in range-bound trading against each other.

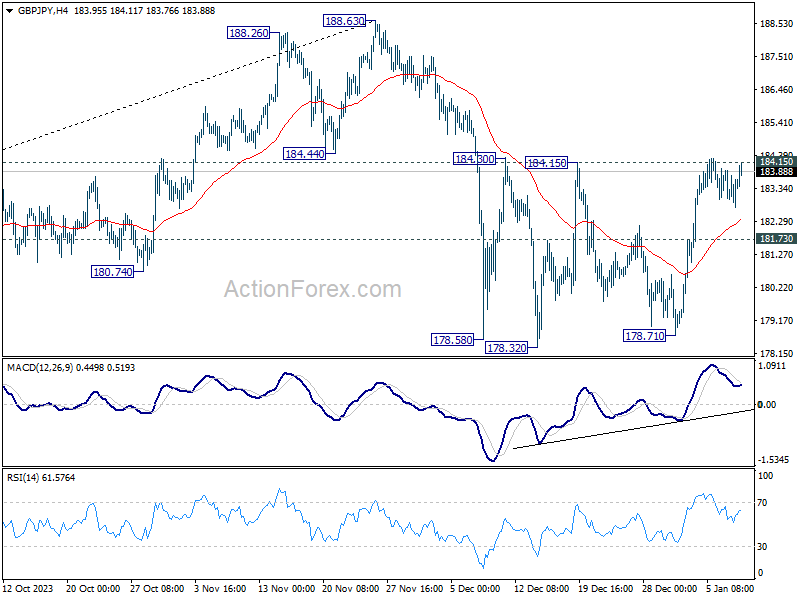

From a technical analysis standpoint, GBP/JPY is back pressing 184.15 resistance after brief retreat. Decisive break there will argue that whole corrective fall from 188.63 has completed, and bring stronger rally back to retest this high. If realized, this upside breakout could be accompanied by break of 158.97 temporary top in EUR/USD, as well as 145.97 resistance in USD/JPY.

In Asia, at the time of writing, Nikkei is up 2.17%. Hong Kong HSI is down -0.45%. China Shanghai SSE is down -0.27%. Singapore Strait Times is down -1.04%. Japan 10-year JGB yield is down -0.0019 at 0.585. Overnight, DOW fell -0.42%. S&P 500 fell -0.15. NASDAQ rose 0.09%. 10-year yield rose 0.017 to 4.019.

ECB's Villeroy advocates for caution over haste or rigidity

ECB Governing Council member Francois Villeroy de Galhau, in an address to France's financial sector overnight, stated, "We will cut rates this year when the inflation outlook is solidly anchored at 2% with effective and durable data."

However, Villeroy did not specify a timeline for these potential rate cuts, emphasizing instead the ECB's reliance on economic data to guide their decisions. He asserted, "Our decisions will not be guided by a calendar, but by data."

Villeroy's statement, "We must demonstrate neither obstinateness nor haste," further highlights the ECB's approach as the central bank is keen on avoiding premature actions that could destabilize the disinflation process.

Japan's labor cash earnings rises only 0.2% yoy, real wages down for 20th month

Japan's labor market showed a notable slowdown in nominal cash earnings growth in November, increasing by only 0.2% yoy, which was significantly below market expectation of 1.5% yoy. This rate marks the slowest growth in nearly two years and represents a considerable decrease compared to 1.5% yoy growth in October.

A closer look at the components of earnings reveals mixed trends. Regular or base salaries saw modest increase of 1.2% yoy, slightly down from previous month's 1.3% yoy. Overtime pay, which had been declining, showed a positive shift with 0.9% yoy increase, marking the first rise in three months. However, special payments, such as bonuses, experienced a significant drop of -13.2% yoy.

More concerning that real wages fell sharply by -3.0% yoy in November, exceeding expectations of -2.0% yoy decline. This drop marks the 20th consecutive month of contraction.

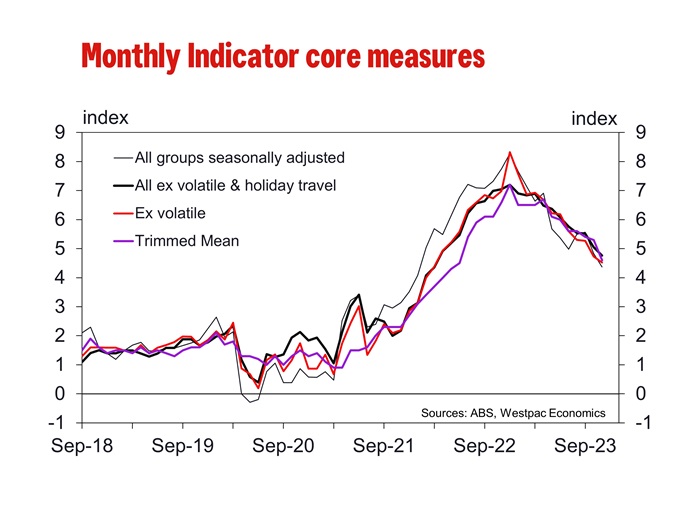

Australia's monthly CPI eases to 4.3% yoy, lowest since Jan 2022

Australia's monthly CPI saw notable deceleration in November, dropping from 4.9% yoy to 4.3% yoy, which was below expectation of 4.5% yoy. This represents the lowest reading since January 2022, as easing of the inflationary pressures continued

CPI excluding volatile items and holiday travel also slowed from 5.1% yoy to 4.8% yoy. Additionally, Trimmed Mean CPI, which removes the most volatile components to provide a clearer picture of underlying inflation trends, decelerated from 5.3% yoy to 4.6% yoy.

The primary drivers of the annual increase in November were in housing , which witnessed a significant rise of 6.6. Food and non-alcoholic beverages also saw a notable increase of 4.6%, Insurance and financial services recorded an 8.8% increase, and Alcohol and tobacco category experienced a 6.4% rise.

Looking ahead

France industrial production and Italy retail sales will be released in European session. Later in the day, US will release wholesale inventories final and crude oil inventories.

USD/JPY Daily Outlook

Daily Pivots: (S1) 143.73; (P) 144.17; (R1) 144.93; More...

USD/JPY recovered ahead of 143.17 minor support but stays well below 145.97 resistance. Intraday bias remains neutral at this point. On the upside, above 145.97 will resume the rebound from 140.25. But upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. On the downside, below 143.17 minor support will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Nov | 0.20% | 1.50% | 1.50% | |

| 00:30 | AUD | Monthly CPI Y/Y Nov | 4.30% | 4.50% | 4.90% | |

| 07:45 | EUR | France Industrial Output M/M Nov | 0.00% | -0.30% | ||

| 15:00 | USD | Wholesale Inventories Nov F | -0.20% | -0.20% | ||

| 15:30 | USD | Crude Oil Inventories | -0.2M | -5.5M |

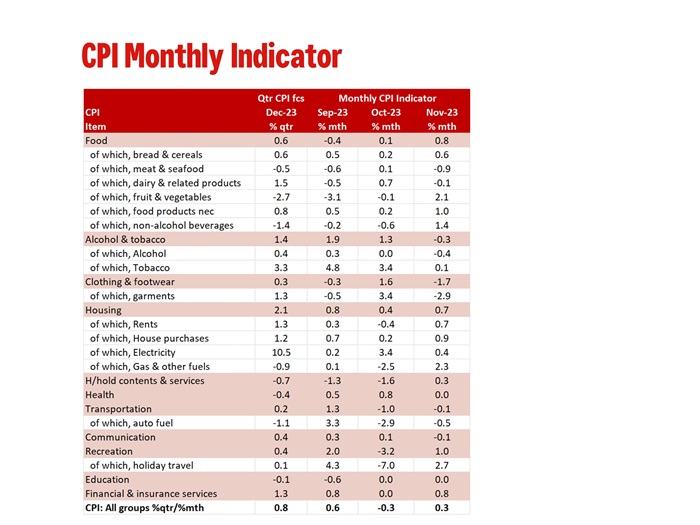

Australia: Inflation Continues to Moderate in November

While dwelling and rents may still be of concern, the increase in household services prices was less than expected while many household goods are not measured in November, the month for the increasingly significant Black Friday/Cyber Monday sales.

The Monthly CPI Indicator rose 4.3% in the year to November, down from 4.9%yr in October and a recent peak of 8.4%yr in December 2022. The November print was a touch softer than Westpac’s forecast and the market’s median forecast of 4.4%yr. At face value the November Monthly CPI Indicator suggests that if there are any risks to our current December quarter CPI forecast of 0.8%qtr it is very slightly to the downside.

As noted in our preview, the second month of the quarter provides us with an update for most of the quarterly surveys of household services. In this regard the overall tone for household services inflation was softer than expected outside the sizable jump in insurance premiums.

But the mid-month does not include many household goods which are surveyed in the first month of the quarter, so the November survey would have missed some of the price declines associated with the Black Friday/Cyber Monday sales.

To give you a feel for the impact of Black Friday sales, in 2022 garment prices rose 2.2% in October, fell 4.1% in November to then lifted 2.1% in December. So far this year garment prices rose 3.4% in October then fell 2.9% in November.

In the month, the Monthly CPI was up 0.3% compared to our forecast for 0.5% increase. The most significant surprises were.

- A 0.3% fall in alcohol & tobacco compared to a +0.1% forecast.

- A 1.7% fall in clothing & footwear led by a 2.9% fall in garments. The fall in garment prices would have been associated with the Black Friday sales. All other components of this group are surveyed in the first month of the quarter so their data misses the Black Friday sales. Had they been surveyed in November, the reported fall in clothing & footwear would have been larger.

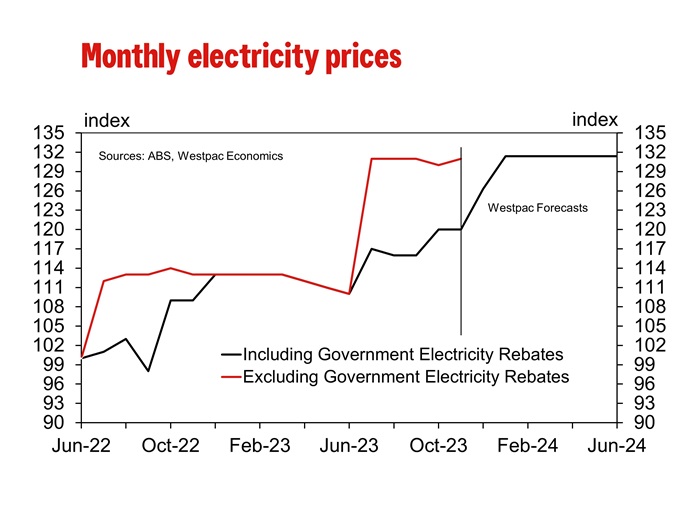

- Total housing costs rose close to expectations at 0.7%. However, the mix was a surprise. Rents rose as expected at 0.7% but dwelling prices were stronger than expected lifting 0.9% in the month, the strongest monthly increase in almost a year. Offsetting this, electricity prices rose just 0.4% (we expected a larger number due to the unwinding of government energy rebates as we did not account for the application further rebates). Gas & other fuels did jump 2.3% but this followed a 2.5% decline in October.

- Household contents & services were softer than anticipated lifting just 0.3% in the month. Outside of non-durable goods no household goods were survey this month missing the Black Friday sales. However, while hairdressing did lift 1.7% other household services prices rose just 0.5% holding back the increase in household services to just 0.7%.

- Recreation was also softer than expected at 1.0% in the month due to holiday travel, up 2.7% vs 5.1% forecast with a domestic travel lifting just 1.8% in the month following a 1.9% decline in October. In addition, other recreation, sport & culture fell 0.1% in the month with the quarterly surveys for equipment for sport & camping plus games, toys & hobbies picking up the Black Friday sales effect.

- Also, it is worth noting the 3.8% rise in insurance premiums. Insurance premiums are up 16.3% in the year. The ABS notes that higher reinsurance and natural disaster costs contributed to higher premiums for house, home contents and motor vehicle insurance.

The Monthly Indicator Trimmed Mean printed 4.6%yr, down from 5.3%yr in October and well down from the recent peak of 7.2% in December 2022. The quarterly Trimmed Mean printed 5.2%yr in September and our current forecast for the December quarter is 4.4%yr. As you can see in the chart below all the monthly core annual inflation measures continued to soften in November.

We are reviewing the full data set for the Monthly CPI Indicator to see if there any implications for our December quarter CPI forecast for both headline and core inflation.

Technical Outlook and Review

DXY:

The DXY (US Dollar Index) chart currently shows a neutral overall momentum, suggesting a lack of strong directional bias in the US Dollar. As a result, there is potential for price to fluctuate between the 1st support and 1st resistance levels.

The 1st support at 101.77 is considered significant as it aligns with an overlap support level. This level may act as a potential area where buying interest could emerge, providing temporary support to the DXY.

The 2nd support at 100.71 is identified as a swing low support, further reinforcing its significance as a potential support zone.

On the resistance side, the 1st resistance at 103.09 is categorized as an overlap resistance. This level may act as a substantial barrier where selling interest could intensify.

The 2nd resistance at 103.50 is noted as a pullback resistance and is also associated with the 78.60% Fibonacci Retracement level. This level could potentially serve as a strong resistance point.

EUR/USD:

The EUR/USD chart currently exhibits a bullish overall momentum, indicating strength in the Euro relative to the US Dollar. However, the chart suggests a potential scenario where price could fluctuate between the 1st resistance and 1st support levels.

The 1st support at 1.0879 is significant for several reasons. It is identified as an overlap support and also coincides with the 61.80% Fibonacci Retracement level. This confluence of technical factors makes it a strong potential support zone, suggesting that buyers may step in at this level, providing temporary support for the EUR/USD pair.

The 2nd support at 1.0747 is also categorized as an overlap support, reinforcing its significance as a potential support area.

On the resistance side, the 1st resistance at 1.1006 is identified as an overlap resistance and is associated with the 50% Fibonacci Retracement level. This level may act as a substantial barrier where selling interest could intensify.

The 2nd resistance at 1.1130 is noted as a swing high resistance. Swing highs often mark points of reversal or resistance in price movement.

EUR/JPY:

The EUR/JPY chart currently exhibits an overall bullish momentum. In this context, there is a potential scenario for price to make a bullish continuation towards the 1st resistance.

The 1st resistance level at 158.84 is categorized as a pullback resistance, indicating a level where selling interest could intensify. The 2nd resistance level at 160.46 is marked as an overlap resistance that is associated with the 161.80% Fibonacci extension level, further reinforcing its significance as a potential barrier for the price.

On the support side, the 1st support level at 156.79 is considered as a pullback support that aligns with the 50.00% Fibonacci retracement level. The 2nd support level at 154.76 is identified as a swing-low support, adding to its significance as a potential support area.

EUR/GBP:

The EUR/GBP chart currently exhibits an overall bearish momentum. In this context, there is a potential scenario for price to make a bearish continuation towards the 1st support.

The 1st support level at 0.8587 is considered significant due to its characteristics as an overlap support. The 2nd support level at 0.8559 is identified as a multi-swing low support, further reinforcing its significance as a potential support zone.

On the resistance side, the 1st resistance level at 0.8620 is categorized as an overlap resistance that aligns with the 23.60% Fibonacci retracement level, making it a notable potential barrier where selling interest could intensify. The 2nd resistance level at 0.8651 is marked as a pullback resistance that is associated with the 50.00% Fibonacci retracement level, further reinforcing its significance as a potential resistance level.

GBP/USD:

The GBP/USD chart currently demonstrates a bearish overall momentum, suggesting weakness in the British Pound compared to the US Dollar. This momentum indicates a potential scenario where price could continue its bearish movement towards the 1st support level.

The 1st support at 1.2611 is categorized as an overlap support. It is a significant level as it suggests a potential area where buying interest may emerge, providing temporary support for the GBP/USD pair.

The 2nd support at 1.2507 is also identified as an overlap support and reinforces its importance as a potential support zone. This level is further marked by the 50% Fibonacci Retracement, adding to its significance.

On the resistance side, the 1st resistance at 1.2763 is categorized as an overlap resistance, and it is associated with the 78.60% Fibonacci Retracement level. This level may act as a substantial barrier where selling interest could intensify.

The 2nd resistance at 1.2827 is noted as a swing high resistance. Swing highs often serve as points of reversal or resistance in price movement.

An intermediate support at 1.2694 is identified as an overlap support, and it coincides with the 50% Fibonacci Retracement level, further highlighting its importance.

GBP/JPY:

The GBP/JPY chart currently exhibits an overall bullish momentum. In this context, there is a potential scenario for price to make a bullish continuation towards the 1st resistance.

The 1st resistance level at 184.20 is marked as an overlap resistance that aligns close to the 161.80% Fibonacci extension level. The 2nd resistance level at 186.35 is also identified as an overlap resistance, further reinforcing its significance as a potential resistance level.

On the support side, the 1st support level at 181.85 is categorized as a pullback support that aligns close to the 38.20% Fibonacci Retracement level, making it a notable potential support zone. The 2nd support level at 179.01 is identified as a swing-low support, further reinforcing its significance as a potential support area.

USD/CHF:

The USD/CHF chart currently exhibits a neutral overall momentum, indicating a lack of strong directional bias. In this scenario, price could potentially move within a range, fluctuating between the 1st resistance and 1st support levels.

The 1st support at 0.8451 is identified as an overlap support, and it aligns with the 50% Fibonacci Retracement level. This level is significant as it suggests a potential area where buying interest may emerge, providing temporary support for USD/CHF.

The 2nd support at 0.8352 is categorized as multi-swing low support, further reinforcing its significance as a potential support zone.

On the resistance side, the 1st resistance at 0.8554 is marked as an overlap resistance, coinciding with the 50% Fibonacci Retracement level. This level may act as a substantial barrier where selling interest could intensify.

The 2nd resistance at 0.8639 is also categorized as an overlap resistance and aligns with the 61.80% Fibonacci Retracement level, adding to its significance.

USD/JPY:

The USD/JPY chart currently exhibits a bullish overall momentum, suggesting strength in the US Dollar relative to the Japanese Yen. This momentum is supported by the potential for a bullish continuation towards the 1st resistance level.

The 1st support at 142.75 is identified as a pullback support and aligns with the 50% Fibonacci Retracement level. This level is significant as it suggests a potential area where buying interest may emerge, providing temporary support for USD/JPY.

The 2nd support at 140.73 is categorized as multi-swing low support, further reinforcing its significance as a potential support zone.

On the resistance side, the 1st resistance at 145.34 is marked as a swing high resistance. Swing highs often act as points of reversal or resistance in price movement.

The 2nd resistance at 146.56 is categorized as an overlap resistance, adding to its significance as a potential barrier for the price.

USD/CAD:

The USD/CAD chart currently exhibits an overall bullish momentum. However, the Relative Strength Indicator (RSI) is displaying a bearish divergence versus price, indicating a potential scenario for price to make a bearish reaction off the 1st resistance and drop towards the 1st support.

The 1st resistance level at 1.3403 is identified as a pullback resistance that aligns with the 50.00% Fibonacci retracement level. Higher up, the 2nd resistance level at 1.3486 is noted as a pullback resistance, further reinforcing its significance as a potential resistance zone.

To the downside, the 1st support level at 1.3319 is identified as a pullback support that aligns with the 38.20% Fibonacci retracement level. Further below, the 2nd support level at 1.3261 is marked as an overlap support that aligns with the 61.80% Fibonacci retracement level, further reinforcing its importance as a key support level.

AUD/USD:

The AUD/USD chart currently exhibits an overall bearish momentum. However, the Relative Strength Indicator (RSI) is displaying a bullish divergence versus price, indicating a potential scenario for price to make a bullish rise towards the 1st resistance should it break above the intermediate resistance.

The intermediate resistance level at 0.6742 is identified as a pullback resistance while the 1st resistance level at 0.6771 is identified as an overlap resistance. Higher up, the 2nd resistance level at 0.6872 is noted as a swing-high resistance that aligns close to the 61.80% Fibonacci projection level, suggesting a potential barrier for further upside movement.

To the downside, the 1st support level at 0.6670 is identified as a pullback support that aligns close to the 61.80% Fibonacci retracement level. Further below, the 2nd support level at 0.6614 is also marked as an pullback support, further reinforcing its importance as a key support level.

NZD/USD

The NZD/USD chart currently exhibits an overall bearish momentum. However, the Relative Strength Indicator (RSI) is displaying a bullish divergence versus price, indicating a potential scenario for price to make a bullish rise towards the 1st resistance should it break above the descending trendline.

The 1st resistance level at 0.6294 is identified as an overlap resistance that aligns with the 61.80% Fibonacci retracement level. Higher up, the 2nd resistance level at 0.6366 is noted as a swing-high resistance that aligns close to the 61.80% Fibonacci projection level, suggesting a potential barrier for further upside movement.

To the downside, the intermediate support level at 0.6220 is identified as a pullback support. Further below, the 1st support level at 0.6182 is marked as an overlap support that aligns close to the 61.80% Fibonacci retracement level, further reinforcing its importance as a key support level.

DJ30:

The DJ30 chart currently displays a neutral bias, indicating a potential for price to fluctuate between the 1st resistance and the 1st support.

The 1st support level at 37,303.35 is considered favourable as it is identified as a pullback support that aligns close to the 78.60% Fibonacci retracement level. The 2nd support level at 37,084.50 is also recognized as a pullback support, further adding to its potential as a support level during a price retracement.

On the resistance side, the 1st resistance level at 37,665.45 is identified as a pullback resistance, which may act as a barrier where selling interest could materialize. The 2nd resistance level at 37,814.50 is recognized as a pullback resistance, adding significance to this potential resistance level.

GER40:

The GER40 chart currently displays a neutral bias, indicating a potential for price to fluctuate between the 1st resistance and the 1st support.

The 1st support level at 16,440.30 is considered favourable as it is identified as an overlap support that aligns with the 23.60% Fibonacci retracement level. The 2nd support level at 16,062.00 is recognized as a pullback support that aligns with the 38.20% Fibonacci retracement level, adding to its potential significance as a level of historical importance.

On the resistance side, the 1st resistance level at 16,828.10 is identified as a pullback resistance that coincides with the 78.60% Fibonacci retracement level, suggesting a level where selling interest could materialize. The 2nd resistance level at 16,962.70 is also noteworthy for being a pullback resistance, further reinforcing its potential as a barrier to upward movement.

US500:

The US500 chart currently displays an overall bullish momentum. In this context, there is a potential for price to make a bullish continuation towards the 1st resistance.

The 1st resistance level at 4,794.80 is identified as a pullback resistance, suggesting a level where selling interest could materialize. The 2nd resistance level at 4,831.80 is identified as a resistance that aligns with the 127.20% Fibonacci extension level.

On the support side, the 1st support level at 4,679.40 is considered favourable due to its identification as a pullback support. The 2nd support level at 4,636.60 is also recognized as a pullback support that aligns with the 23.60% Fibonacci retracement level, adding to its potential as a support level.

BTC/USD:

The BTC/USD chart currently exhibits a neutral bias, indicating a potential for price to fluctuate between the 1st resistance and the 1st support.

The 1st support level at 45,530 is considered favourable as it is identified as an overlap support, indicating historical significance as a level where buying interest has previously emerged. The 2nd support level at 44,251 is also recognized as an overlap support, adding to its potential as a support level.

On the resistance side, the 1st resistance level at 47,517 is identified as a multi-swing-high resistance while the 2nd resistance level at 49,486 is recognized as a swing-high resistance, suggesting a level where selling interest could materialize.

ETH/USD:

The ETH/USD chart currently exhibits a neutral bias, indicating a potential for price to fluctuate between the 1st resistance and the 1st support.

The 1st support level at 2,253.03 is identified as an overlap support, suggesting historical significance as a level where buying interest has previously emerged. The 2nd support level at 2,138.02 is recognized as a multi-swing-low support, adding to its potential as a support level.

On the resistance side, the 1st resistance level at 2,418.92 is identified as a multi-swing-high resistance that aligns close to the 161.80% Fibonacci extension level, suggesting a level where selling interest could materialize. The 2nd resistance level at 2,511.31 is recognized as a pullback resistance, suggesting a potential barrier for further upside movement.

WTI/USD:

The WTI (West Texas Intermediate) chart currently exhibits an overall bullish momentum. In this context, there is a potential scenario for price to make a bullish continuation towards the 1st resistance.

The 1st resistance level at 74.03 is identified as a swing-high resistance that aligns with the 78.60% Fibonacci projection level. Higher up, the 2nd resistance level at 76.08 is also noted as a swing-high resistance, suggesting a potential barrier for further upside movement.

To the downside, the intermediate support level at 70.58 is identified as a pullback support while the 1st support level at 69.96 is noted as a swing-low support that aligns close to the 78.60% Fibonacci retracement level. Further below, the 2nd support level at 68.17 is also marked as a swing-low support, further reinforcing its importance as a key support level.

XAU/USD (GOLD):

The XAU/USD (Gold/US Dollar) chart currently exhibits a bearish overall momentum, indicating weakness in the price of gold relative to the US Dollar. This momentum suggests the potential for a bearish continuation towards the 1st support level.

The 1st support at 2006.29 is categorized as a pullback support. This level is significant as it implies a potential area where buying interest may emerge, providing temporary support for XAU/USD.

The 2nd support at 1976.72 is identified as multi-swing low support, further reinforcing its significance as a potential support zone.

On the resistance side, the 1st resistance at 2049.03 is marked as an overlap resistance, indicating a level where selling interest could intensify, potentially triggering a bearish reversal or resistance.

The 2nd resistance at 2065.75 is also categorized as an overlap resistance, further adding to its significance as a potential barrier for the price.

Additionally, there is an intermediate support level at 2018.64, identified as multi-swing low support. This level may also play a role in providing support to the XAU/USD pair.