Sample Category Title

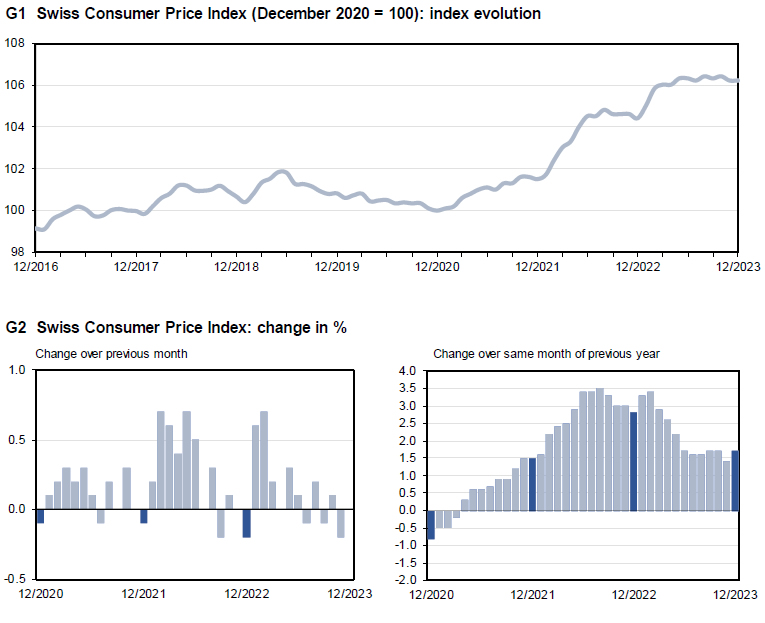

Swiss CPI rises to 1.7% yoy in Dec, matches expectations

Swiss CPI was flat at 0.0% mom in December, above expectation of -0.1% mom. Core CPI (fresh and seasonal products, energy and fuel) rose 0.2% mom. Domestic products prices rose 0.3% mom. Import products price fell -0.7% mom.

For the 12-month period, CPI rose from 1.4% yoy to 1.7% yoy, matched expectations. Core CPI rose from 1.4% yoy to 1.5% yoy. Domestic products prices rose from 2.1% yoy to 2.3% yoy. Imported products prices from also rose from -0.6% yoy to -0.2% yoy.

Also published, retail sales rose 0.7% yoy in November, above expectation of 0.0% yoy.

Reconsidering the Dovish Fed Expectations

The New Year unsurprisingly kicked off with a hangover for both stock and bond markets, as investors began the year by closing their positions and taking profit following an impressive two-month rally that was boosted by the expectation that the Federal Reserve (Fed) would soon start cutting the interest rates and cut them thoroughly throughout this year. We begin the new year with the expectation that the Fed will cut the rates 5 times, by 25bp each, and the first rate cut will be announced by March, with around 64% probability. Note that this probability was standing somewhere around 80% by the end of last year and it’s come down, as investors probably realized that the expectations, and the market rally went well ahead of themselves. And of course, the minutes from the Fed’s last meeting, released last week, didn’t give any clarity other than the general thinking that the Fed rates are certainly ‘at or near their peak’ for this cycle, but that there is an ’unusually elevated degree of uncertainty’ meaning that the expectation of around 75bp cut this year is certainly not a done deal. And indeed, the strength of the US economy, and its jobs market wouldn’t justify an imminent start of the Fed cuts this spring.

In this context, last week’s jobs data from the US came in stronger than expected, yet again. The US economy added more than 200’000 new nonfarm jobs in December, and the average earnings accelerated more than expected, above 4%. Some saw a bit of weakness in the US job metrics pointing at the falling job openings and the falling participation rate, but rationally speaking, an NFP figure above 200K is not pointing at a severe slowdown which would urge the Fed to start cutting the rates in two-and-something month and cut by 150bp to the end of the year. Even Janet Yellen said it – in quite an unusual declaration after Friday’s jobs report –said that ‘what we are seeing now I think we ca describe as soft landing’, and again a soft landing doesn’t justify a 150bp cut from the Fed this year.

As such, there is no surprise that we see the US 2-year yield rebound to 4.40% and the 10-year yield return past the 4% - its biggest weekly advance of the US 10-year yield since October. The rising yields halted the dollar’s bleeding. The EURUSD sank below the 1.10 mark as soon as the year started. The rising US yields also stopped the rally in equities. The S&P500 dipped below 4700 – having been unable to post a fresh record at the end of the latest rally, and the rate-sensitive Nasdaq 100 fell more than 4% since its December peak – which was an ATH. And because the correlation between the US treasuries and Nasdaq 100 stocks remains high, a further rise in the US yields will likely cause a deeper retreat for the US stocks – and especially the most-loved tech stocks. But note that this correlation will likely decline with the start of the earnings season this week, as the company results will give investors a various range of reasons to buy or sell stocks. Overall, according to FactSet, the estimated yoy earnings growth rate for the S&P 500 is 1.3% for the Q4. If that’s the case, it will mark the second straight quarter of year-over-year earnings growth for the index, and it’s another evidence that the US economy doesn’t need the Fed’s help to stay afloat.

Inflation

This week’s major economic data is the US inflation data due Thursday. The headline inflation in the US is expected to have slowly accelerated to 3.2% from 3.1% printed a month earlier, while core inflation is expected to have further eased to 3.8% from 4% printed a month earlier. Soft inflation numbers, ideally softer-than-expected, could slow the corrective selloff in both stock and bond markets, yet the inflation risks are now tilted to the upside. Tensions in the Red Sea region explode the price of shipping goods from Asia to Europe and America. The cost of shipping goods from Asia to Europe doubled since last December, and that’s a bad indication of what’s to come for inflation numbers in the coming months. Remember, the last time we saw the shipping costs surge – that was during the pandemic – had followed a significant rise in a very wide range of consumer prices. Therefore yes, inflation figures in US and Europe have come significantly down last year, but the easing could slow or reverse. And that’s the biggest risk to the dovish Fed and European Central Bank (ECB), and Bank of England (BoE) expectations this year.

Happily, though, the oil prices continue to see strong resistance despite the Red Sea tensions. The barrel of US crude couldn’t clear the $74 offers last week and we start the week below the $73pb level. The geopolitical risks prevail, but traders continue to see the tops in an effort to force the price of a barrel of American crude to below $70pb again.

Monday’s Focus Will Be on Inflation Data

In focus today

Today we get a string of tier-2 data from the euro area. The most important ones are the euro area retail sales and German factory orders. The euro area November retail sales will provide important information about how consumption fared in Q4. German factory orders will shed light on the German industry ahead of the industrial production figures tomorrow. Moreover, we receive a bunch of confidence indicators including the Sentix investor confidence indicator for December.

In Switzerland, we get inflation numbers for December. The past months, inflation has surprised to the downside both compared to the SNB's forecast and consensus expectation with headline and core now within the SNBS's target range. Today's print will prove important as to whether the SNB will opt for a rate cut soon, possibly already in March.

Finally, we will look out for Tokyo inflation data for December after price pressures moderated quite a bit in Japan in November. The print is released overnight.

Economic and market news

What happened overnight: Oil prices fell more than 1% overnight due to Saudi Arabia cutting prices coupled with rising OPEC output, outweighing upward price pressure amid geopolitical jitters in the Middle East. In the US, Congress agreed on a new spending deal for the current fiscal year, mitigating risks of a partial government shutdown on January 20.

What happened on Friday: The first trading week of 2024 concluded with the broad dollar index (DXY) gaining 1.1% on a weekly basis, proving to be the largest weekly gain since mid-July. This move follows sour global risk sentiment coupled with data releases indicating that the US economy is still proving fairly resilient. Bond yields moved higher approaching three-week highs, with the 10Y UST yield rising 6bp to 4.05%. In equity space, European markets closed lower and US stock indices climbed marginally higher, rounding off a choppy first week of 2024.

On Friday, US macro data provided mixed signals of the labour market. The US December Jobs Report surprised to the upside as non-farm payrolls grew by 216k (cons: 170k) although the November figure was revised down by 26k. Moreover, the labour force participation rate reversed, edging down to 62.5% and average hourly earnings remained at 0.4% m/m, which historically is uncomfortably quick for the Fed. In general, the report indicates that US labour markets are still tight. Conversely, the ISM services index ticked down to 50.6, notably lower than expectations (52.6) - and in contrast to the more upbeat PMIs released earlier in the day. Business activity improved, but prices, new orders and employment weakened. Markets are currently pricing around 140bp of Fed cuts for 2024. However, FOMC member Lorie Logan provided some pushback on the market pricing on cuts on Saturday stating that premature easing of financial conditions could reignite inflation pressure, signalling that rate hikes cannot be ruled out.

In line with our call, euro area headline inflation came in at 2.9% y/y in December (prior: 2.4%, cons: 2.9%), with the uptick primarily driven by energy base effects. Core inflation increased by 3.4% y/y (prior: 3.6%, cons: 3.4%). Using ECB's seasonal adjustments, the 3m/3m seasonally adjusted annualized inflation was 1.4%, warranting that the underlying momentum in core prices is still declining. Despite inflationary momentum easing, service inflation remains too high for the ECB's, printing at 2.3%. Hence, we believe that the ECB needs more data to be convinced of a sustainable convergence back to the 2% target.

Equities: Job market data all over the place sent equities for a volatile ride on Friday. Equities were mixed but closed lower for the week, thereby snapping a nine-week winning streak. Last week was all about reversal: Small caps suddenly underperformed large caps, value outperformed growth and defensives made a grand comeback. Global defensives outperformed cyclicals by 4 p.p. last week. Same story held on Friday. S&P 500 closed up 0.2% while Stoxx 600 managed to recover to -0.3%. We see the de-risking last week as a symptom of positioning and overbought conditions short-term and do not read too much into it. However, there is a macro aspect of it as well, and hence we recommend decreasing cyclicals exposure. Asian markets are continuing lower this morning, particularly in Hong Kong after renewed regulation fear in the gaming sector. US and European futures are lower as well.

FI: Global yields reacted sharply lower to the US labour market report on Friday, but quickly reverted back to the outset of the release. The euro area flash inflation report did not change market dynamics. 10y German Bunds were up 2-3bp on the day, and intra euro-area spreads were broadly constant on the day. Markets have taken out almost 25bp of the rate cuts from ECB and Fed since late last year, with now 144bp and about 140bp priced until year end. In particular for ECB, we find market pricing too aggressive.

FX: In a quite unusual whipsaw-session on Friday EUR/USD tested both the 1.09 support- and later the 1.10 resistance level before ending the session virtually unchanged around 1.0950. With EUR/SEK edging higher and EUR/NOK remaining more stable we are now close to parity in NOK/SEK while EUR/GBP has moved down to the 0.86-level.

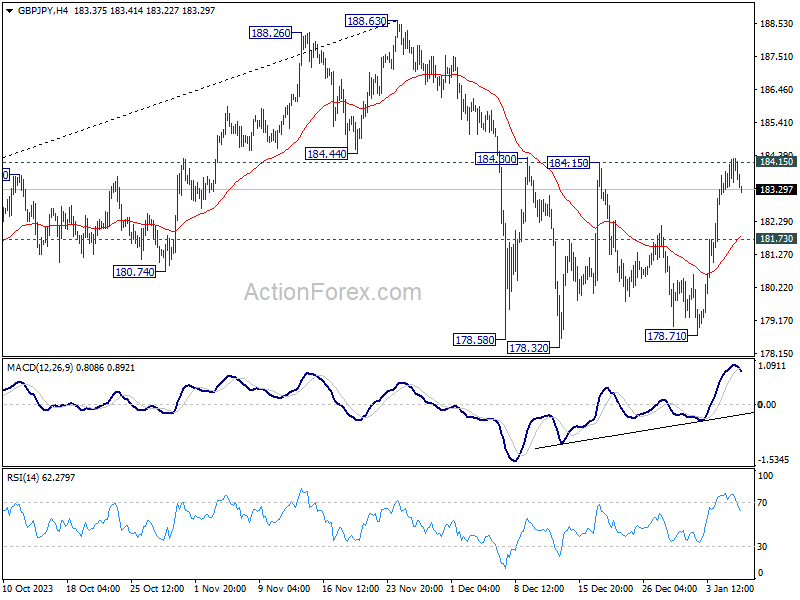

GBP/JPY Daily Outlook

Daily Pivots: (S1) 183.43; (P) 183.87; (R1) 184.41; More...

Intraday bias in GBP/JPY stays neutral first. On the upside, sustained break of 184.15 resistance will argue that whole pull back from 188.63 has completed and bring further rally to retest this high. However, break of 181.73 minor support will indicate rejection by 184.15, and retain near term bearishness. Intraday bias will be back on the downside for 178.71 support instead.

In the bigger picture, price actions from 188.63 medium term top are seen as a correction to the up trend from 148.93 (2022 low) only. As long as 172.11 resistance turned support holds, larger up trend from 123.94 (2020 low) is still in favor to resume through 188.63 at a later stage.

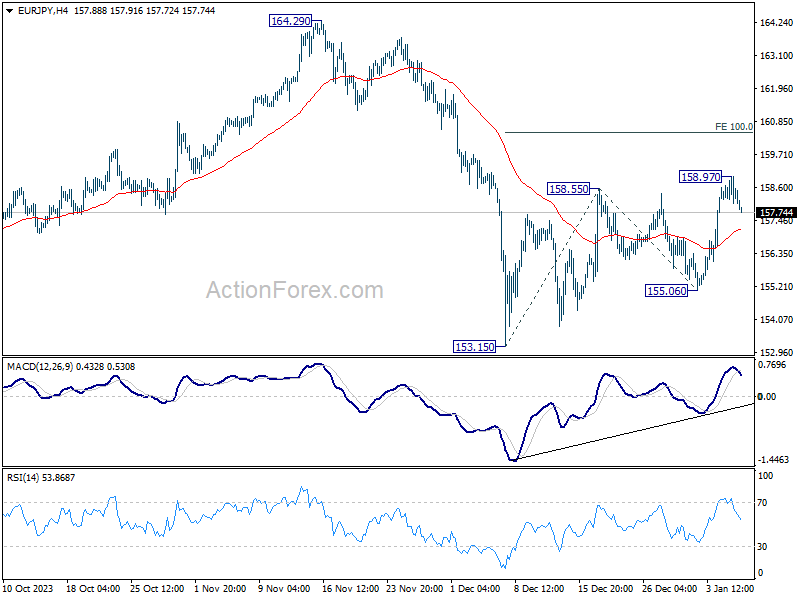

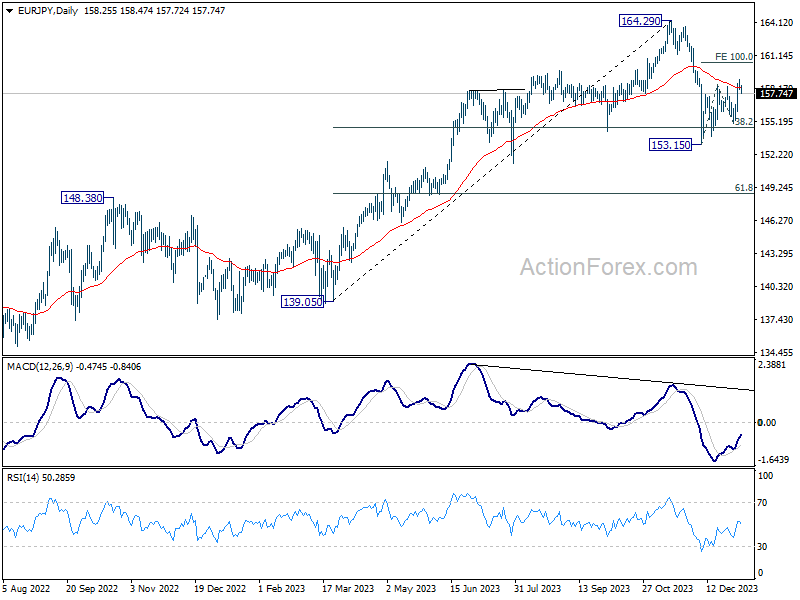

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.87; (P) 158.43; (R1) 158.82; More...

Intraday bias in EUR/JPY is turned neutral first with current retreat. But rise will stay on the upside as long as 155.06 support holds. On the upside, above 158.97 will resume the rebound from 153.15 to 100% projection of 153.15 to 158.55 from 155.06 at 160.46.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

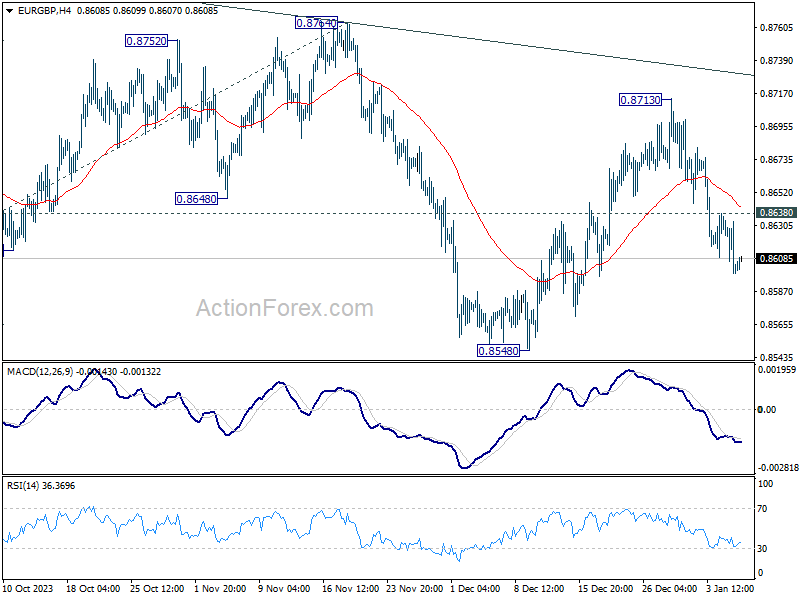

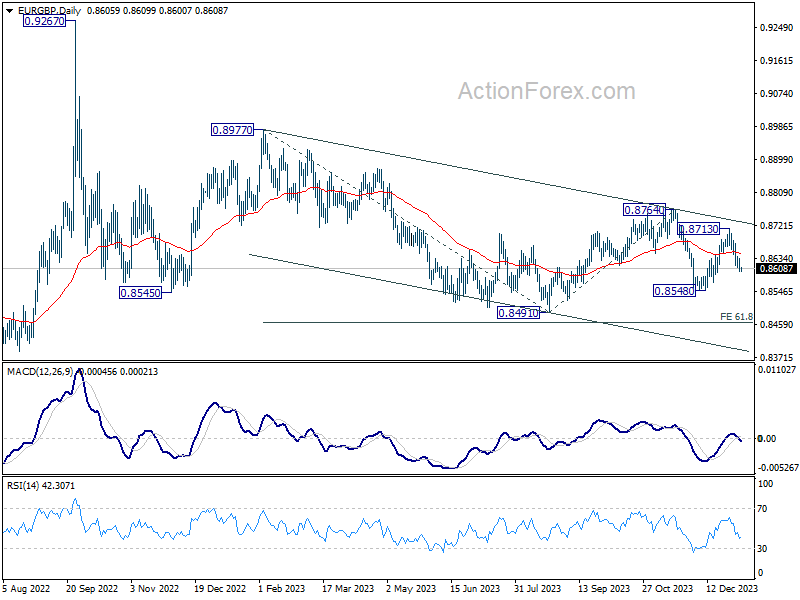

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8590; (P) 0.8613; (R1) 0.8625; More...

Intraday bias in EUR/GBP stays on the downside for the moment. Deeper decline should be seen to 0.8548 support first. Firm break there will target 0.8491 low next. On the upside, above 0.8638 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.8713 resistance holds, in case of recovery.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8764 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

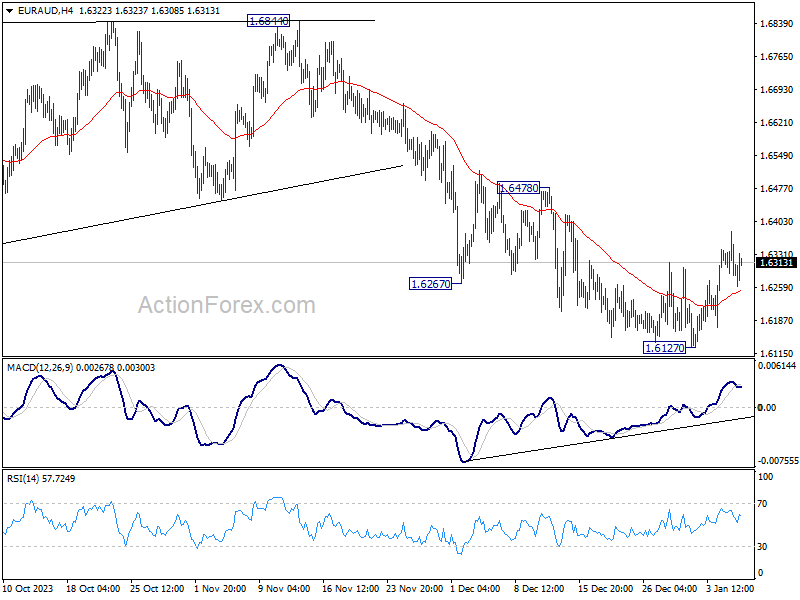

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6259; (P) 1.6322; (R1) 1.6356; More..

Intraday bias in EUR/AUD remains mildly on the upside for the moment. Rebound from 1.6127 short term bottom would target 1.6478 resistance. Firm break there will argue that whole correction from 1.7062 has completed, and target 1.6844 resistance for confirmation. Nevertheless, break of 1.6127 will resume the corrective fall to 1.6000 fibonacci level.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 bring rebound. Break of 1.6844 will argue that this up trend is ready to resume through 1.7062 high.

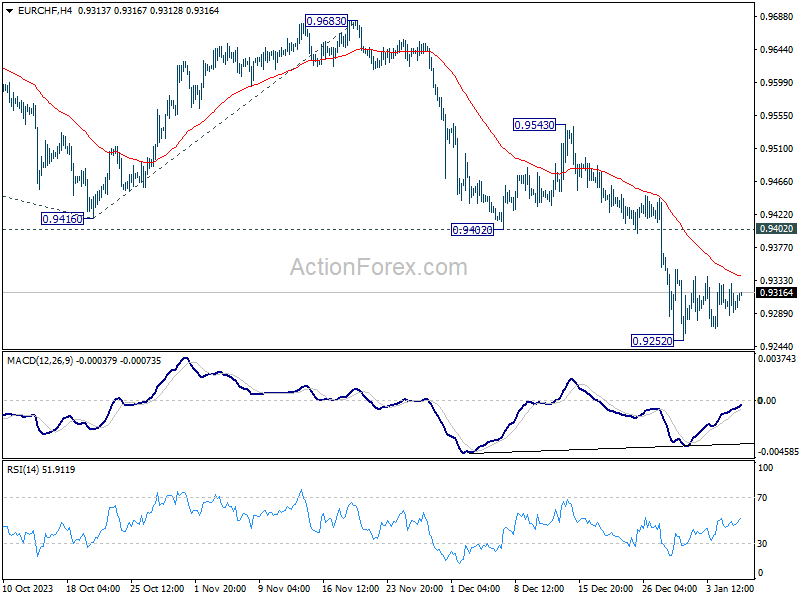

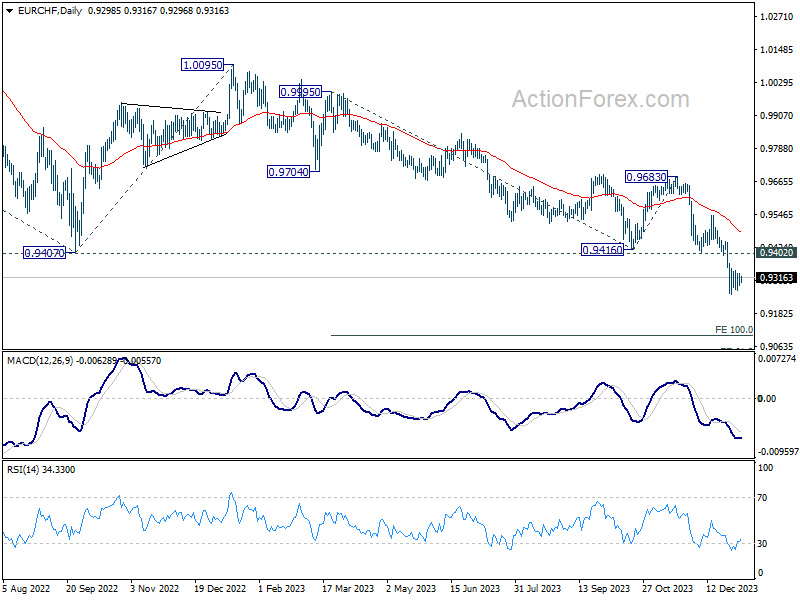

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9284; (P) 0.9308; (R1) 0.9328; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 0.9252 is extending. While another recovery cannot be ruled out, outlook will stay bearish as long as 0.9402 support turned resistance holds. On the downside, break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

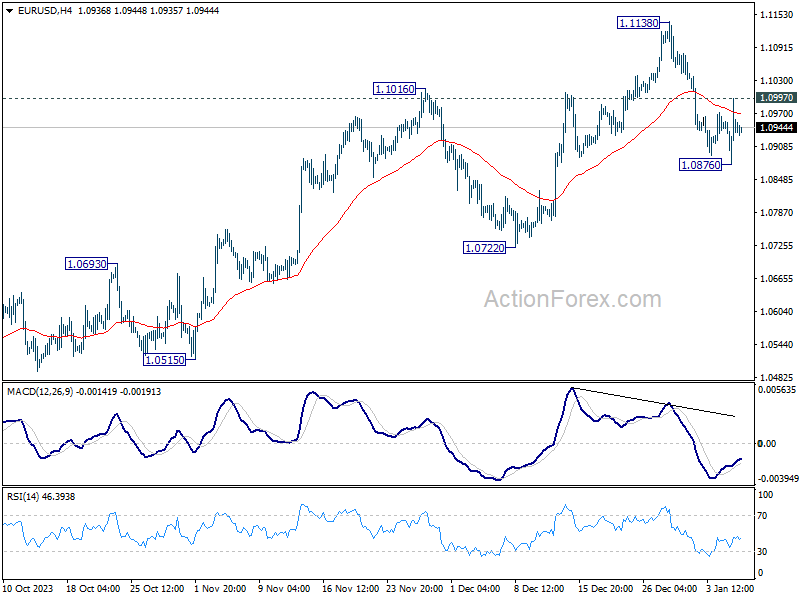

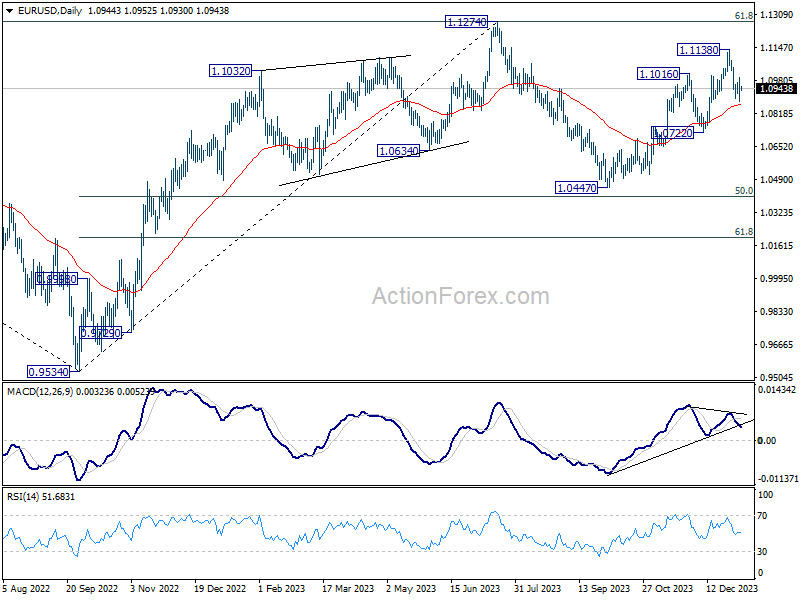

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0881; (P) 1.0939; (R1) 1.1002; More...

Intraday bias in EUR/USD remains neutral at this point. On the downside break of 1.0876 will resume the fall from 1.1138 short term top to 1.0722 support next. However, break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

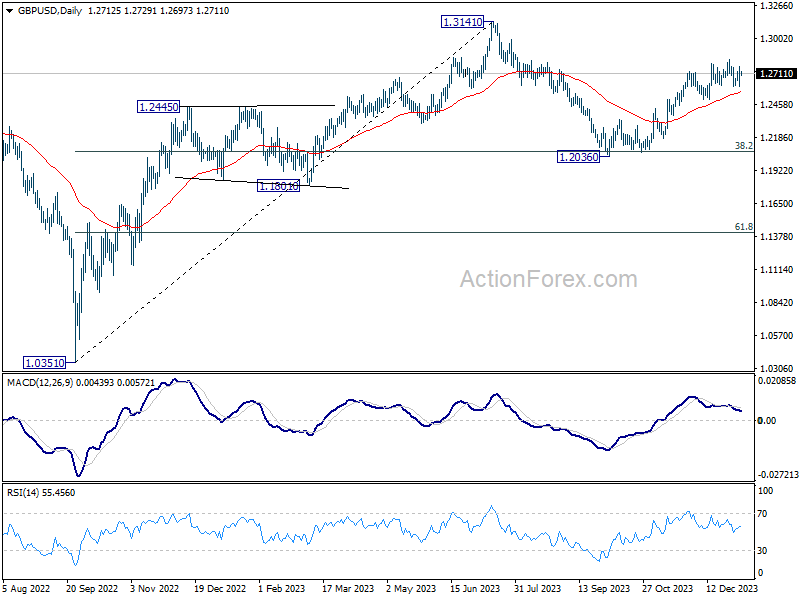

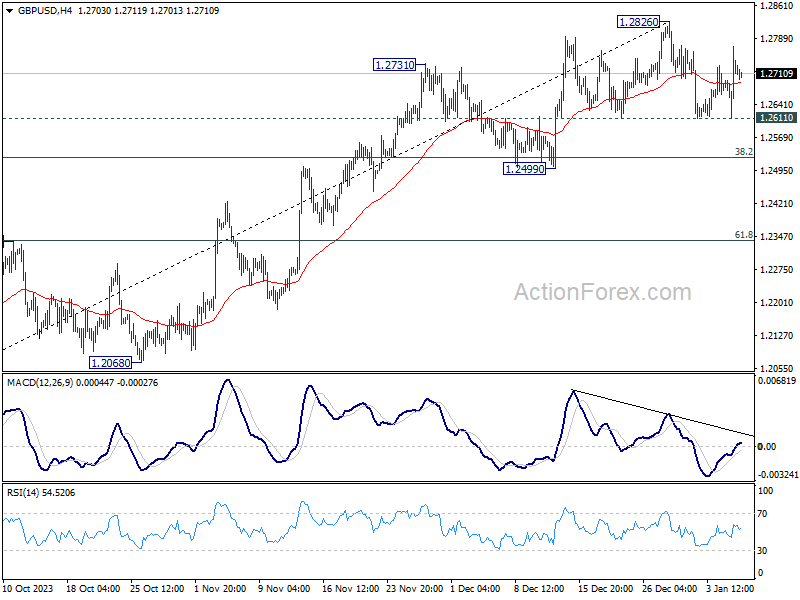

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2630; (P) 1.2701; (R1) 1.2789; More...

Intraday bias in GBP/USD is mildly on the upside for retesting 1.2826 high. Decisive break there will resume whole rally from 1.2036. Nevertheless, another fall and break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.