Sample Category Title

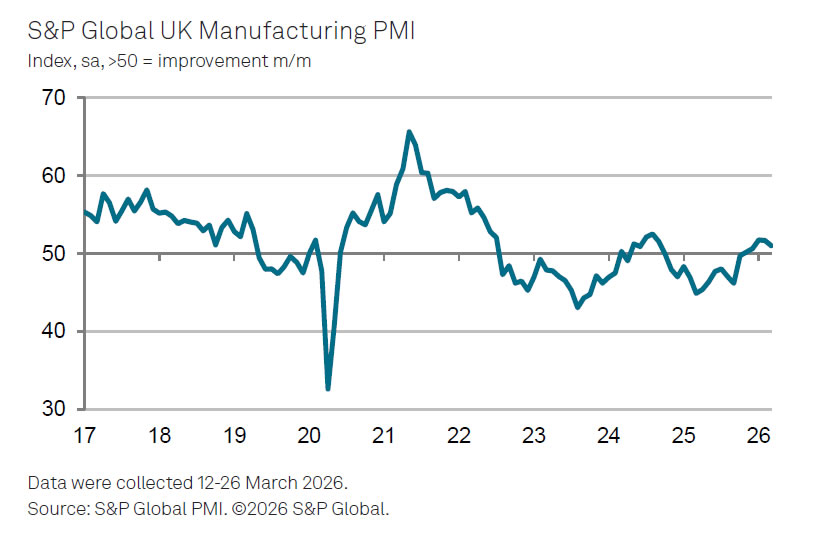

UK PMI Manufacturing Finalized at 51.0, Input Costs Surge and Confidence Drops

UK PMI Manufacturing was finalized at 51.0 in March, down from February's 51.4, signaling a modest slowdown in factory activity. The data suggests that while demand conditions are holding up, momentum in production is beginning to soften amid a more challenging operating environment.

According to Rob Dobson, Director at S&P Global Market Intelligence, the Middle East war is reshaping cost and supply dynamics. He noted that delivery times lengthened to the greatest extent since mid-2022, while input price inflation surged at the fastest pace since the aftermath of the UK’s ERM exit in 1992. The resulting high-cost environment, combined with input shortages, has started to weigh directly on production volumes.

Dobson also highlighted that the broader economic and geopolitical backdrop is denting confidence, with business optimism falling to a six-month low and job cuts accelerating to their fastest pace since last September. However, he pointed out that new orders have held up better than output, suggesting that the weakness in production is currently driven more by supply constraints than a collapse in demand, leaving the outlook sensitive to how long cost pressures persist.

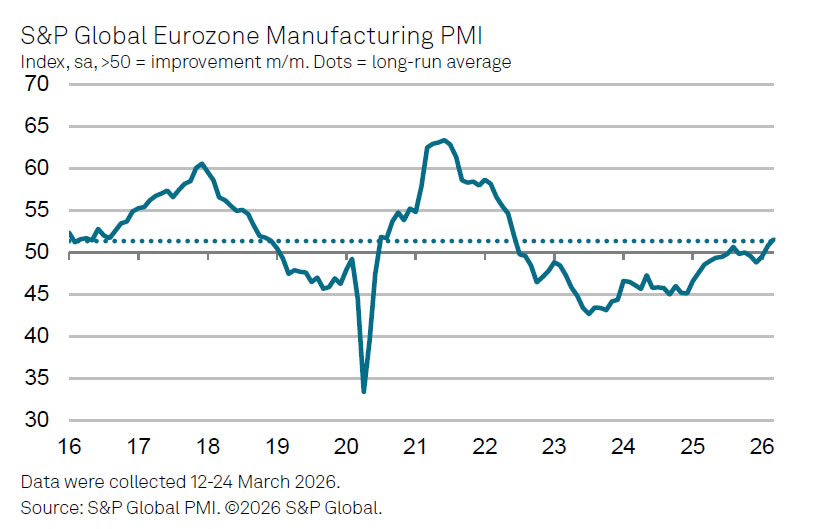

Eurozone PMI Manufacturing Finalized at 45-Month High But War-Fueled Inflation Clouds Outlook

Eurozone PMI Manufacturing was finalized at 51.6 in March, up from 50.8, marking a 45-month high and signaling continued, albeit modest, expansion in the sector.

However, according to Joe Hayes, Principal Economist at S&P Global Market Intelligence, the Middle East war has already begun to leave a clear imprint on the sector. He noted that suppliers’ delivery times have risen sharply as logistics adjust to maritime disruption, while surging oil prices have pushed input cost inflation to its highest level since late 2022.

Hayes also highlighted that firms have started passing these higher costs through to customers, "reducing the Eurozone's competitiveness and this will likely put demand under renewed pressure."

Despite steady output and order growth, Hayes emphasized that expansions remain "tepid" and vulnerable. He warned that it may not take much for output and sales to turn lower, particularly if the conflict persists and cost pressures intensify.

EUR/USD Aims Recovery While USD/JPY Gives Back Recent Gains

EUR/USD is recovering losses from 1.1450. USD/JPY is correcting gains from 160.50 and might decline further below 158.00.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro struggled to stay in a positive zone and declined below 1.1600 before finding support.

- There is a key bearish trend line forming with resistance at 1.1575 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY rallied significantly before the bears appeared near 160.45.

- There is a major bearish trend line forming with resistance near 159.20 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair started a fresh decline from 1.1640. The Euro declined below 1.1600 and 1.1520 against the US Dollar.

The pair even declined below 1.1500 and the 50-hour simple moving average. Finally, it tested the 1.1445 zone. A low was formed at 1.1443, and the pair is now recovering losses. There was a move above 1.1500 and the 50-hour simple moving average.

The pair surpassed the 50% Fib retracement level of the downward move from the 1.1639 swing high to the 1.1443 low. On the upside, the pair is now facing resistance near the 61.8% Fib retracement and 1.1575. There is also a key bearish trend line forming with resistance at 1.1575.

The first major hurdle for the bulls could be 1.1605. An upside break above 1.1605 could set the pace for another increase. In the stated case, the pair might rise toward 1.1640.

If not, the pair might drop again. Immediate support is near 1.1520. The next key area of interest might be 1.1480 or the 50-hour simple moving average. If there is a downside break below 1.1480, the pair could drop toward 1.1445. The main target for the bears on the EUR/USD chart could be 1.1400, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a steady decline from well above the 160.00 zone. The US Dollar gained bearish momentum below 159.50 against the Japanese Yen.

The pair even settled below 159.00 and the 50-hour simple moving average. A low was formed at 158.44, and the pair is now consolidating losses. On the downside, the first major support is near 158.45.

The next key region for the bulls might be 158.00. If there is a close below 158.00, the pair could decline steadily. In the stated case, the pair might drop toward 156.80. Any more losses might send the pair toward 155.00.

Immediate resistance on the USD/JPY chart is near the 23.6% Fib retracement level of the downward move from the 160.46 swing high to the 158.44 low at 158.90.

If there is a close above 158.90 and the hourly RSI moves above 50, the pair could rise toward 159.20. There is also a major bearish trend line forming with resistance near 159.20. The next major barrier for the bulls could be near the 50% Fib retracement level at 159.45, above which the pair could test 160.00 in the coming days.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

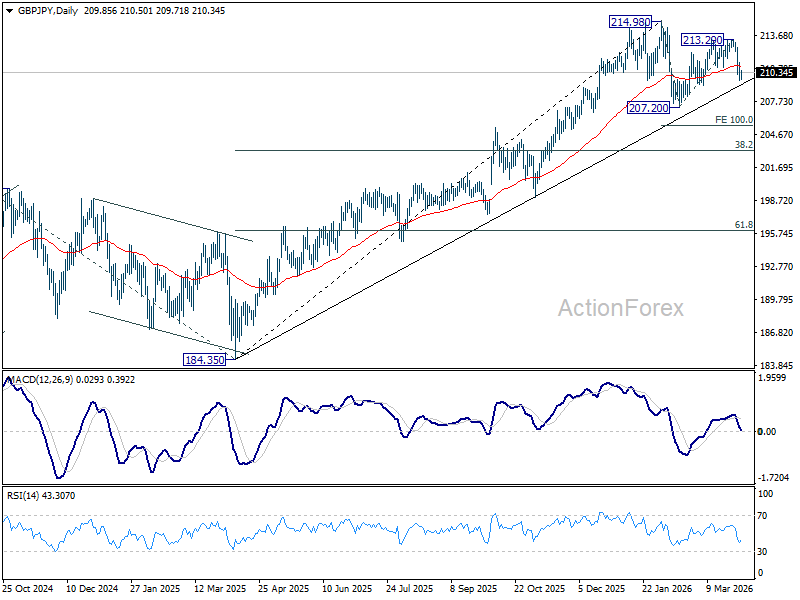

GBP/JPY Daily Outlook

Daily Pivots: (S1) 209.29; (P) 210.26; (R1) 210.89; More...

No change in GBP/JPY's outlook and intraday bias stays on the downside. Corrective pattern from 214.98 should be in the third leg. Deeper decline would be seen to 209.15. Firm break there will target 207.20 and below. On the upside, above 211.20 minor resistance will turn bias neutral first. But risk will stay on the downside as long as 213.29 resistance holds, in case of recovery.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.13) holds, even in case of another deep pullback.

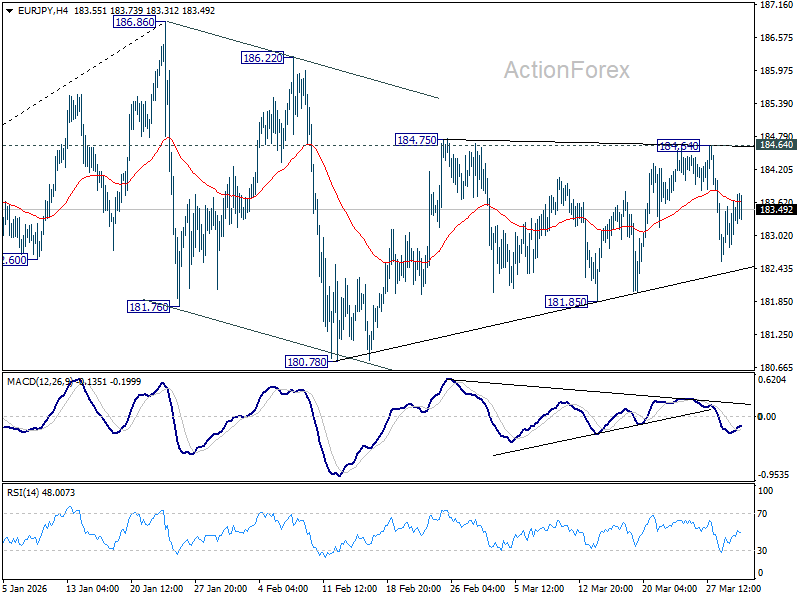

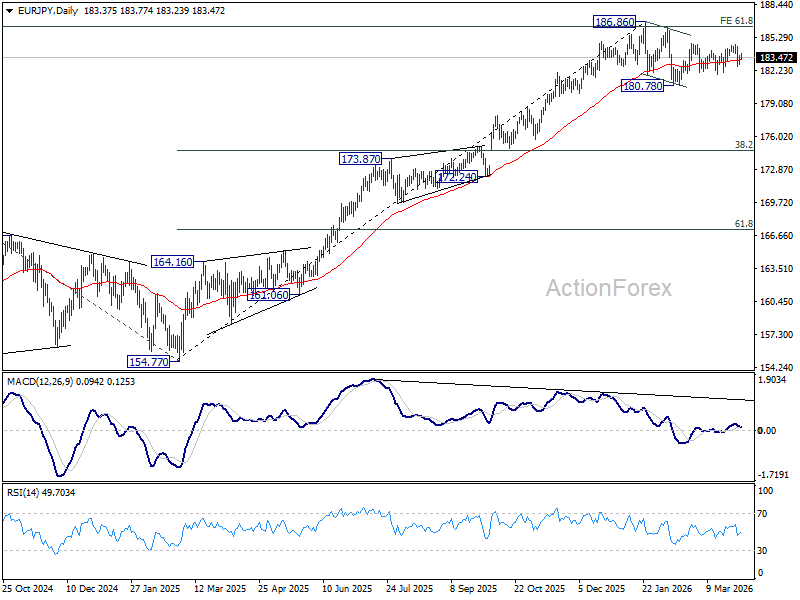

EUR/JPY Daily Outlook

Daily Pivots: (S1) 182.92; (P) 183.28; (R1) 183.74; More...

Intraday bias in EUR/JPY is turned neutral again with current recovery. On the downside, firm break of 181.85 support should confirm that the correction from 186.86 is already in the third leg. Deeper fall should be seen to 180.78 and below. For now, risk will stay on the downside as long as 184.86 resistance holds.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 175.93) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

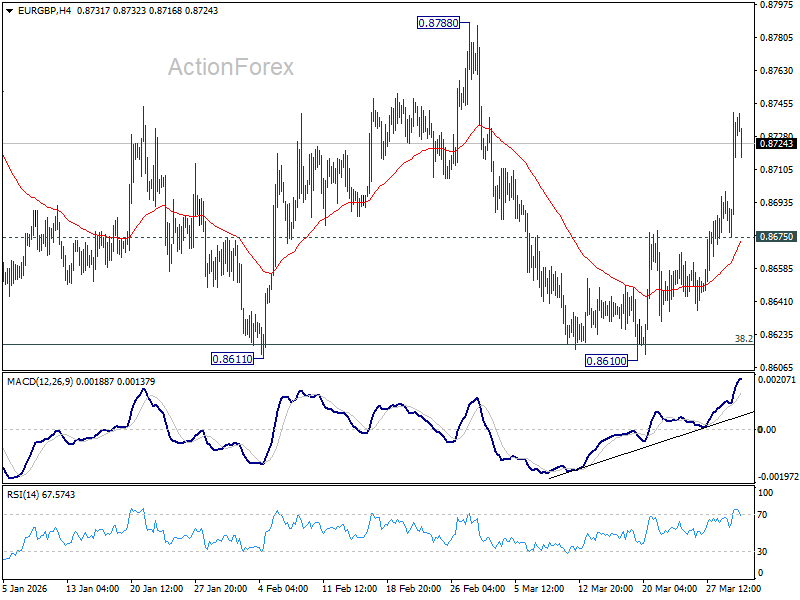

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8693; (P) 0.8718; (R1) 0.8760; More…

Intraday bias in EUR/GBP remains on the upside as rebound from 0.8610 support extends. Further rally should be seen to 0.8788 resistance. Firm break there should confirm completion of the correction from 0.8863, and bring retest of this high. On the downside, below 0.8675 support will turn bias neutral first.

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be resume to resume through 0.8863. Nevertheless, sustained trading below 0.8618 should confirm reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.

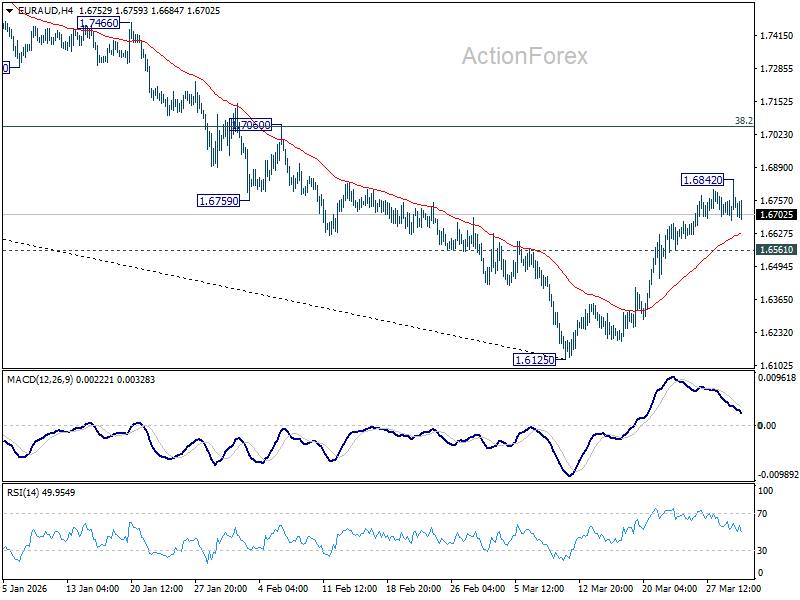

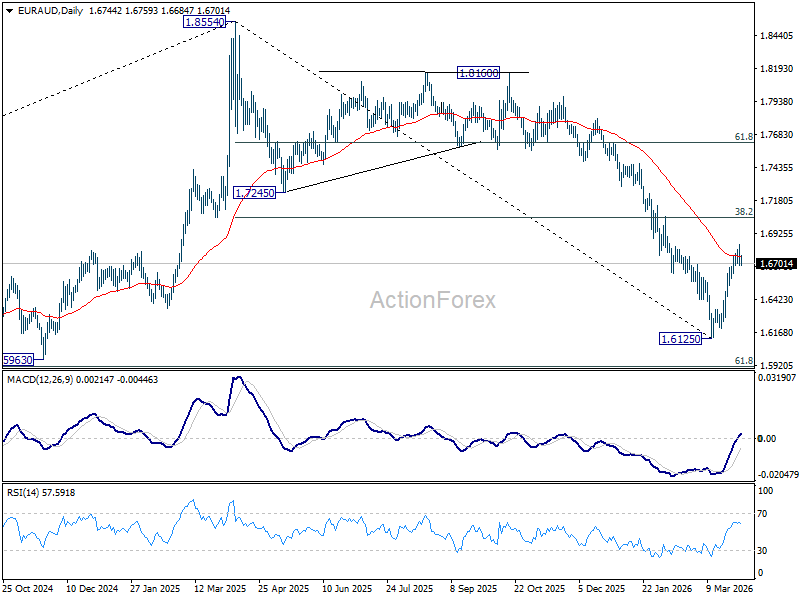

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6668; (P) 1.6757; (R1) 1.6833; More...

EUR/AUD edged higher to 1.6842 but quickly retreated. Intraday bias remains neutral first. On the upside, above 1.6842 will extend the rebound from 1.6125 to 38.2% retracement of 1.8554 to 1.6125 at 1.7053. However, break of 1.6561 minor support will argue that the rebound has completed, after rejection by 55 D EMA (now at 1.6754). Retest of 1.6125 low should be seen next.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7226) holds, even in case of strong rebound.

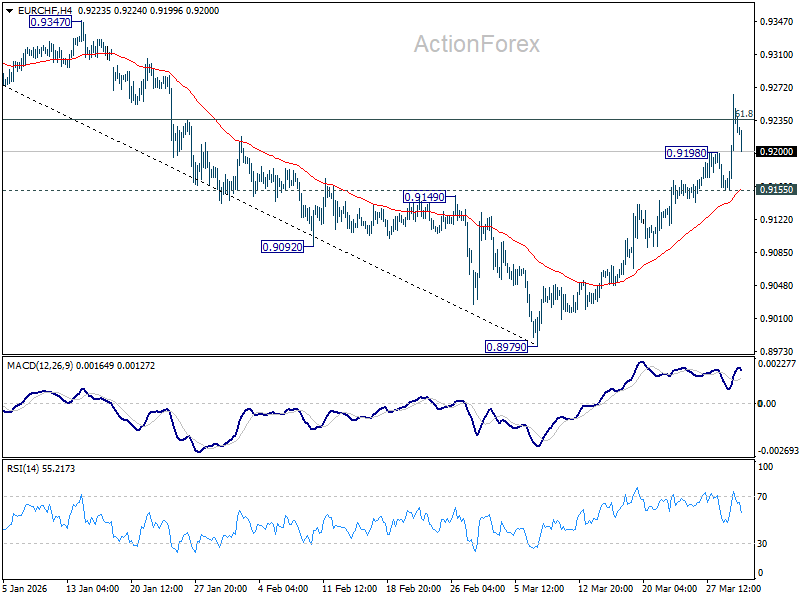

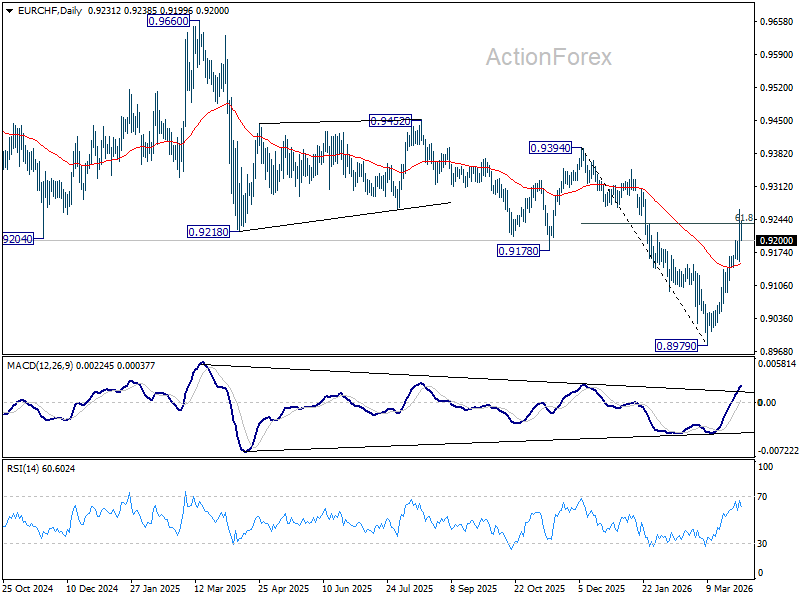

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9160; (P) 0.9213; (R1) 0.9289; More....

EUR/CHF's rebound from 0.8979 resumed by breaking through 0.9198 temporary top. Intraday bias is back on the upside. Sustained trading above 61.8% retracement of 0.9394 to 0.8979 at 0.9235 will pave the way to 0.9394 key resistance next. On the downside, below 0.9155 minor support will turn intraday bias neutral first.

In the bigger picture, as long as 55 W EMA (now at 0.9286) holds, the larger down trend from 0.9928 (2024 high) is still expected to continue through 0.8979 at a later stage. However, sustained break of 55 W EMA should confirm medium term bottoming, and bring stronger rise through 0.9394 resistance, even as a corrective move.

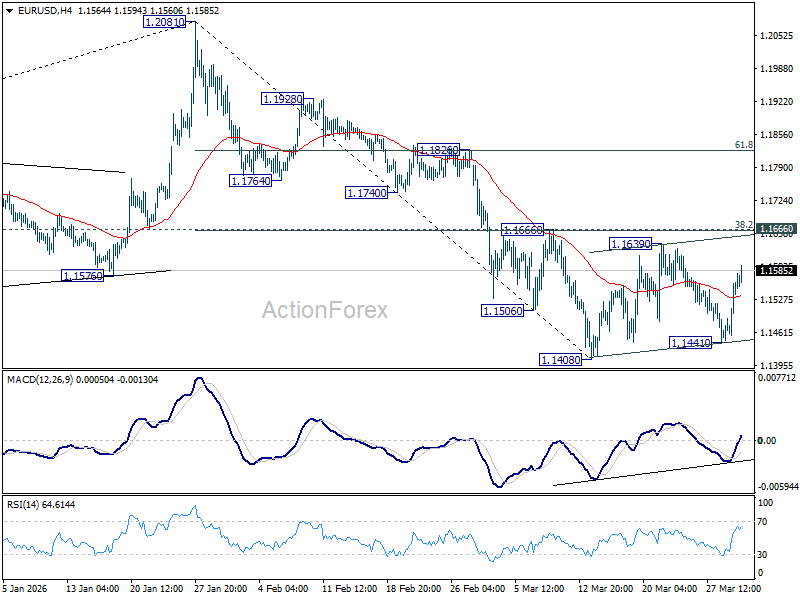

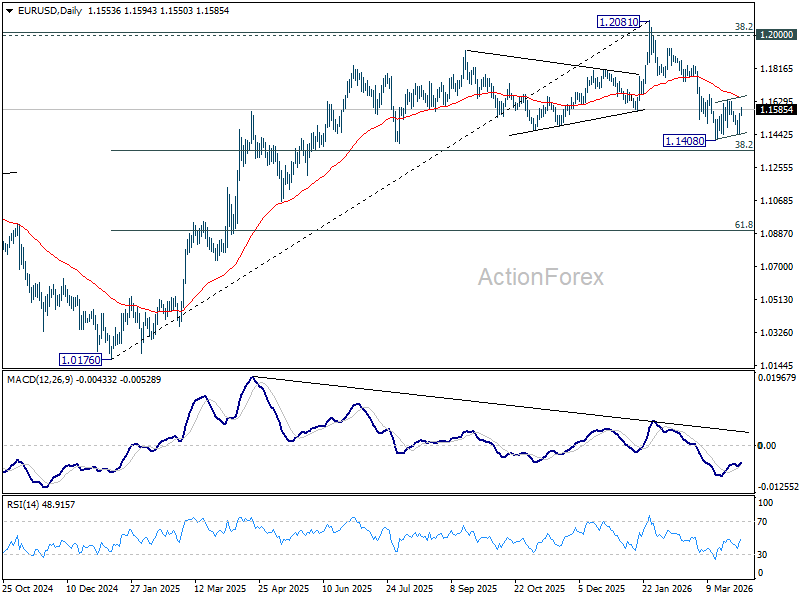

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1479; (P) 1.1521; (R1) 1.1596; More….

EUR/USD rebounded higher today but it's still seen as in consolidations from 1.1408. Intraday bias remains neutral, and further decline is expected with 1.1666 cluster resistance (38.2% retracement of 1.2081 to 1.1408 at 1.1665) intact. On the downside, firm break of 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. However, decisive break of 1.1666 will argue that the fall from 1.2081 has completed, and turn bias back to the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824.

In the bigger picture, prior break of 55 W EMA (now at 1.1497) should confirm rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. Deeper fall is expected to long term channel support (now at 1.0535). Meanwhile, risk will stay on the downside as long as 1.2081 holds, even in case of strong rebound.

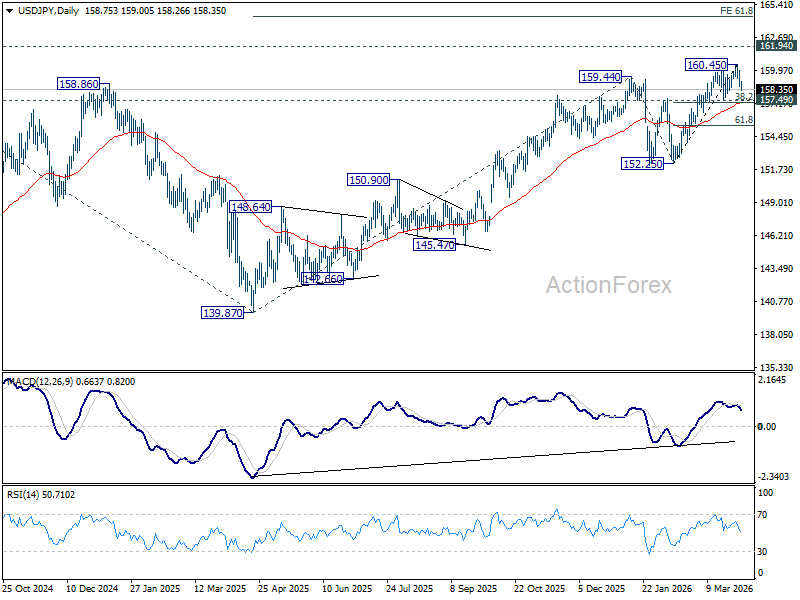

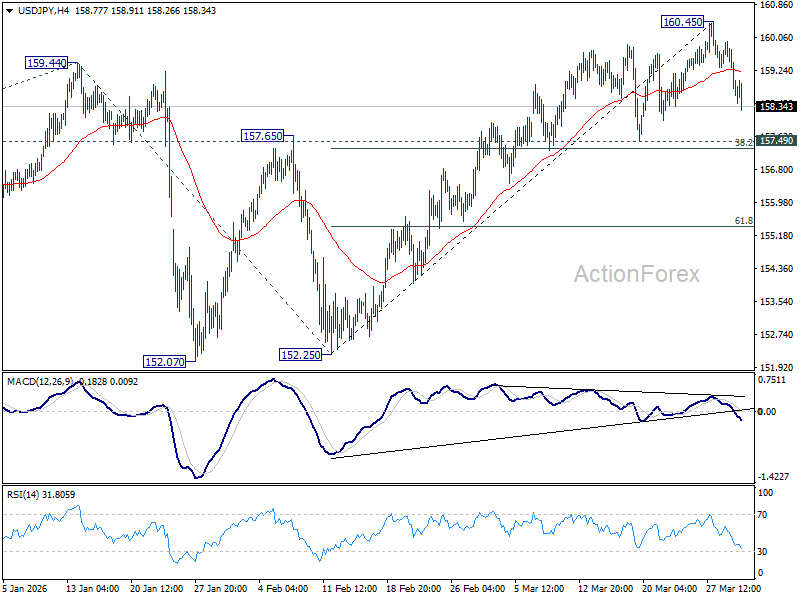

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.23; (P) 159.11; (R1) 159.62; More...

The firm break of 55 4H EMA (now at 159.18) confirms short term topping at 160.45, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31. For now, near term outlook will stay neutral as long as 160.45 resistance holds, in case of recovery.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.97) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.