Sample Category Title

Yen Traders Exercise Caution Ahead of BoJ

Japanese Yen is extending its broad-based pullback today. This movement appears to be a strategic response from traders lightening their positions in anticipation of the upcoming BoJ policy decision. Although a rate hike by the BoJ seems highly unlikely at this stage, there is speculation about potential adjustments in the central bank's communication. These changes are anticipated to lay the groundwork for concluding the yield curve control policy in January, followed by a possible rate hike in April to exit the prolonged phase of negative interest rates. However, given the BoJ's history of unexpected moves, traders are bracing themselves for substantial volatility, regardless of the decision made.

In other parts of the currency markets, US Dollar, Sterling, and Euro are displaying signs of weakness. Notably, Euro remains unfazed by the recent, worse-than-expected German Ifo business climate data. On the other end of the spectrum, New Zealand Dollar and the Australian Dollar are showing marked strength. Meanwhile, Swiss Franc and Canadian Dollar are exhibiting mixed performances.

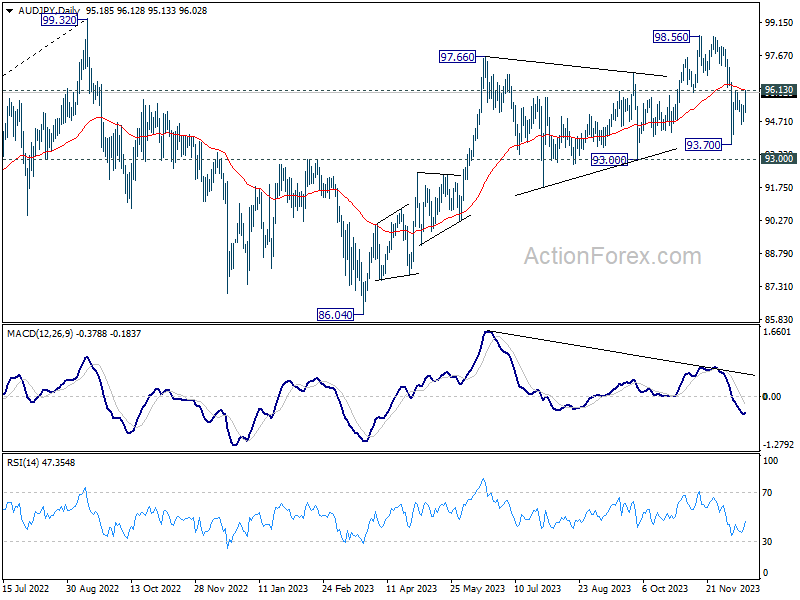

One currency pair of particular interest is AUD/JPY, especially in the context of the upcoming RBA minutes in the Asian session, in addition to BoJ. From a technical standpoint, decisive break of 96.13 resistance, which is close to 55 D EMA, will argue that corrective fall from 98.56 is completed at 93.70, ahead of 93.00 support. This development would keep the rally from 86.04 intact, for further rise through 98.56 next. Nevertheless, rejection by 96.13 will likely resume the fall from 98.56, probably through 93.00 support, as reversing the rise from 96.04.

In Europe, at the time of writing, FTSE is up 0.65%. DAX is down -0.43%. CAC is down -0.35%. Germany 10-yaer yield is up 0.024 at 2.043. UK 10-year yield is up 0.001 at 3.690. Earlier in Asia, Nikkei fell -0.64%. Hong Kong HSI fell -0.97%. China Shanghai SSE fell -0.40%. Singapore Strait Times fell -0.11%. Japan 10-year JGB yield fell -0.0403 to 0.670.

Fed's Mester: The next phase is not when to reduce rates

In a Financial Times interview, Cleveland Fed President Loretta Mester put emphasis on the duration of maintaining restrictive monetary policy to ensure that inflation reliably returns to the 2% target. That's contrary to market expectations, which centers on timing and extent of rate cuts.

Mester's key statement, "The next phase is not when to reduce rates... It's about how long do we need monetary policy to remain restrictive in order to be assured that inflation is on that sustainable and timely path back to 2%,"

"The markets are a little bit ahead. They jumped to the end part, which is 'We're going to normalize quickly', and I don't see that," she added.

When the discussion eventually shifts to the timing and pace of rate cuts, Mester highlighted the importance of one-year forward inflation expectations and their alignment towards the 2% target.

"If you don't take action as expected inflation comes down, then you're really firming policy," she warned. "You don't want to inadvertently become more restrictive than you think is appropriate."

ECB's Vasle cautions against premature rate cut expectations

ECB Governing Council member Bostjan Vasle expressed skepticism about market expectations for imminent interest rate cuts, considering them "premature," both in terms of timing and the overall scope of such moves. This perspective challenges the market's anticipation of monetary easing, which currently sees 50-50 chance of a rate cut by March, with a full cut expected by April

Vasle emphasized that the current market pricing "has lowered the level of restriction". Additionally, the accommodation priced into by interest rate expectations seems to be at odds with the monetary stance required to steer inflation back to the target.

Additionally, Vasle indicated that ECB would likely wait until at least the end of Q1 before considering any changes to its stance. This approach is grounded in the need for more comprehensive data, which will only be available around March or April. he added, "We will need to understand the underlying trends better, and we need the new projections, too."

On the inflation front, Vasle posited that inflation could rebound at the year's turn, potentially hovering between 2.5% to 3% through the first half of the next year. Vasle said, "So it's appropriate to wait and observe price growth through this period and reassess our outlook."

Germany's Ifo business climate dips to 86.4, economy remains weak

Germany' Ifo Business Climate fell from 87.3 to 86.4 in December, below expectation of 87.8. Current Assessment index fell from 89.4 to 88.5, below expectation of 89.5. Expectations index fell from 85.2 to 84.3, below expectation of 85.8.

By sector, manufacturing fell from -13.8 to -17.2. Services rose from -2.5 to -1.7. Trade fell from -22.2 to -26.6. Construction fell from -29.5 to -33.1.

The Ifo Institute's statement encapsulates the current sentiment, noting that "companies were less satisfied with their current business" and expressing a more skeptical view of the first half of 2024. The acknowledgment that "the German economy remains weak as the year draws to a close" is telling of the challenges facing Europe's largest economy.

NZ BNZ services rises to 51.2, maintains oscillating course

New Zealand BusinessNZ Performance of Services Index rose from 49.2 to 51.2 in November, crossing the threshold from contraction to expansion. However, it's crucial to note that this figure remains below the long-term average of 53.5, suggesting that recovery is still in its nascent stages.

Looking at more details, activity/sales rose from 47.5 to 48.7. Employment rose from 49.5 to 51.0. New orders/business rose from 52.1 to 52.3. Stocks/inventories jumped from 51.5 to 55.0. Supplier deliveries rose from 50.1 to 52.9.

BusinessNZ Chief Executive Kirk Hope's observation that the sector has been oscillating between contraction and expansion in recent months underscores the volatility and uncertainty still prevalent in the business environment.

The proportion of negative comments from businesses decreased from 58.2% in October to 54.0%. This reduction, though modest, is a positive sign, indicating a slight improvement in business sentiment. Hope added, "negative comments continued to be pinpointed on key areas such as the economy, inflation and cost of living".

New Zealand Westpac consumer confidence rises to 88.9 in Q4, encouraging sign

New Zealand Westpac Consumer Confidence Index rose notably from 80.2 to 88.9 in Q4, hitting the highest level in nearly two years. Present Conditions Index rose from 69.5 to 77.1. Expected Conditions Index also rose from 87.4 to 96.7.

However, Westpac noted that the index is still below historical average. This means "many more New Zealanders [are] feeling pessimistic about economic conditions." But it's important to recognize the positive trajectory reflected in these recent months. The rise in the Consumer Confidence Index is an "encouraging sign," as noted by Westpac.

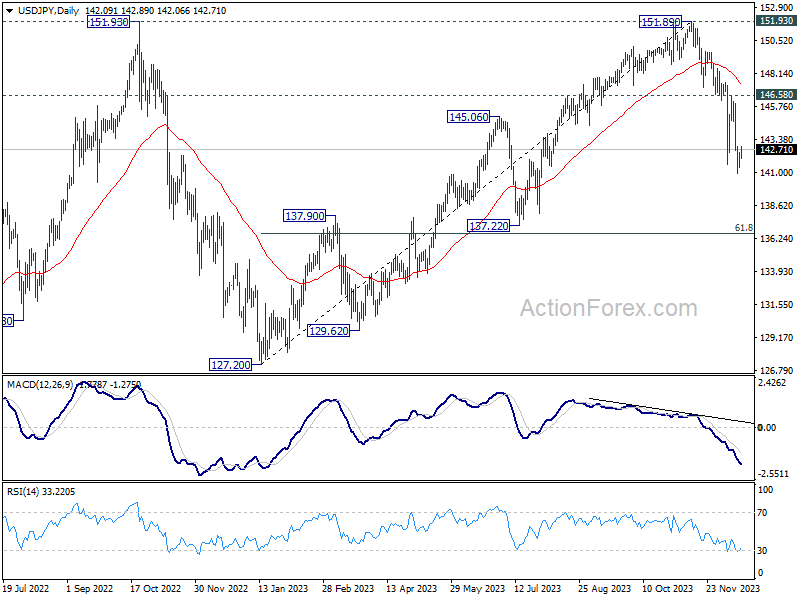

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.57; (P) 142.02; (R1) 142.61; More...

USD/JPY is still extending consolidation from 140.95 and intraday bias remains neutral. Stronger recovery cannot be ruled out. But upside should be limited well below 146.58 resistance to bring another decline. On the downside, break of 140.94 will resume the fall from 151.89 to next fibonacci level at 136.63.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | Westpac Consumer Survey Q4 | 88.9 | 80.2 | ||

| 21:30 | NZD | Business NZ PSI Nov | 51.2 | 48.9 | 49.2 | |

| 09:00 | EUR | Germany IFO Business Climate Dec | 86.4 | 87.8 | 87.3 | |

| 09:00 | EUR | Germany IFO Current Assessment Dec | 88.5 | 89.5 | 89.4 | |

| 09:00 | EUR | Germany IFO Expectations Dec | 84.3 | 85.8 | 85.2 | |

| 13:30 | CAD | New Housing Price Index M/M Nov | -0.20% | 0.10% | 0.00% | |

| 15:00 | USD | NAHB Housing Market Index Dec | 37 | 34 |

USD/JPY – Yen Climbs to 4.5 Month High, BoJ Next

- BoJ to make rate announcement on Tuesday

- Fed’s Williams says no rate cuts planned

The Japanese yen is lower at the start of the week. In the European session, USD/JPY is trading at 142.77, up 0.44%.

The yen continues to power higher and surged 1.9% last week. It marked a fifth straight winning week for the yen, which has climbed 6.2% during that time. The yen strengthened to 140.95 on Friday, its highest level since July 31.

Will BoJ make a move?

Bank of Japan policy meetings have become must-see events, with investors on edge over speculation that the central bank is planning to tighten policy. Tuesday’s meeting will be closely watched, especially after hints from senior BoJ officials that it could phase out negative rates, which would be a sea-change in policy that would likely boost the yen. The BoJ might not announce any changes at the meeting, but I doubt that will quell speculation that a policy change is coming. The BoJ tends to hold its cards close to its chest, maximizing the surprise effect of any policy moves.

The BoJ has been an outlier among central banks in sticking to an ultra-loose policy while its peers were busy raising rates, and the BoJ is expected to tighten policy next year while other major central banks are looking to cut rates. The BoJ has long insisted that inflation is not sustainable, but that position has become difficult to defend, as inflation has remained above the 2% target month after month.

New York Fed President John Williams said on Friday that the Fed was not discussing rate cuts and that the Fed could tighten policy if inflation stalled or reversed directions. The markets don’t seem to be listening, however, and have priced in six rate cuts next year, starting as soon as March. At last week’s meeting, Fed Chair Jerome Powell finally jumped on the rate-cut bandwagon and said that the Fed would cut rates three times in 2024.

USD/JPY Technical

- USD/JPY is testing resistance at 142.61. Above, there is resistance at 143.06

- There is support at 142.02 and 141.57

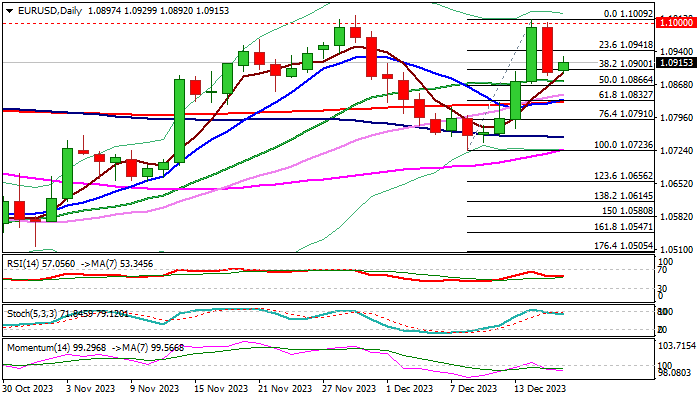

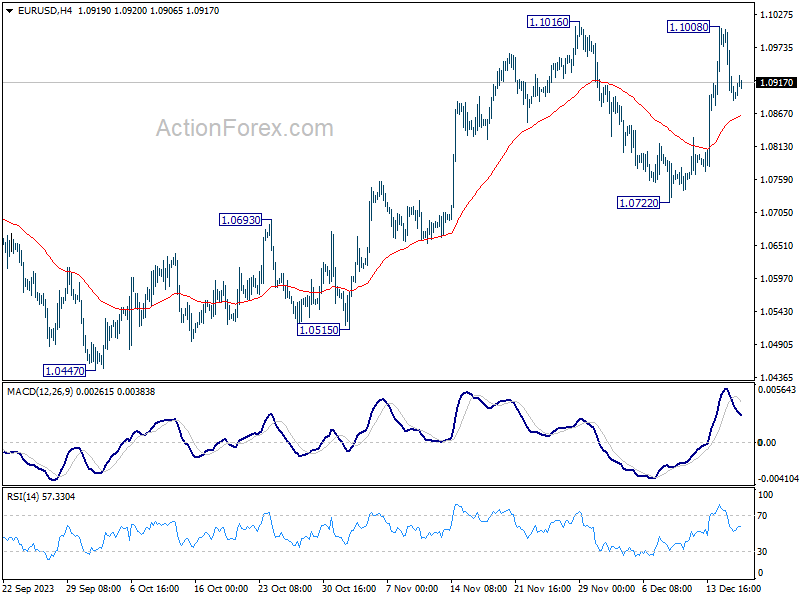

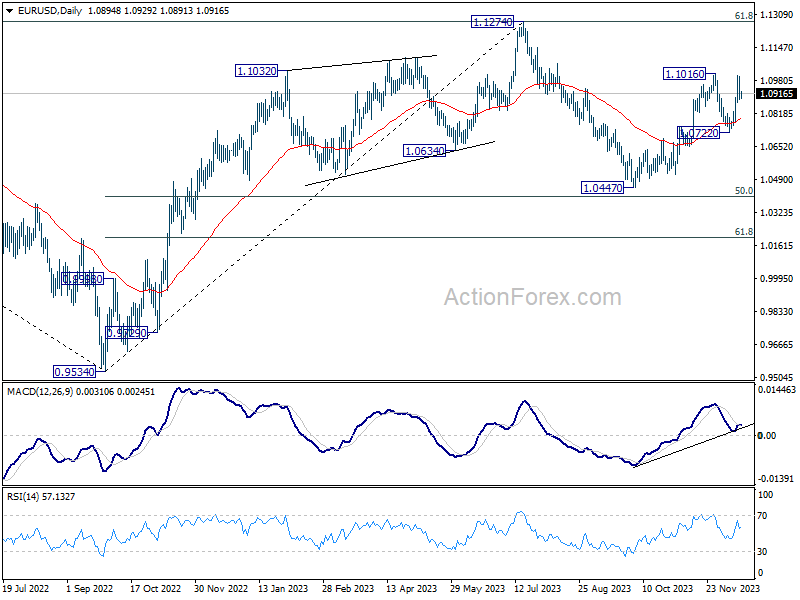

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0855; (P) 1.0929; (R1) 1.0970; More...

Intraday bias in EUR/USD remains neutral at this point. Consolidation from 1.1016 could extend further and deeper retreat cannot be ruled out. But further rally is expected as long as 1.0722 support holds. On the upside, break of 1.1016 will resume the whole rise from 1.0447 to retest 1.1274 high.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

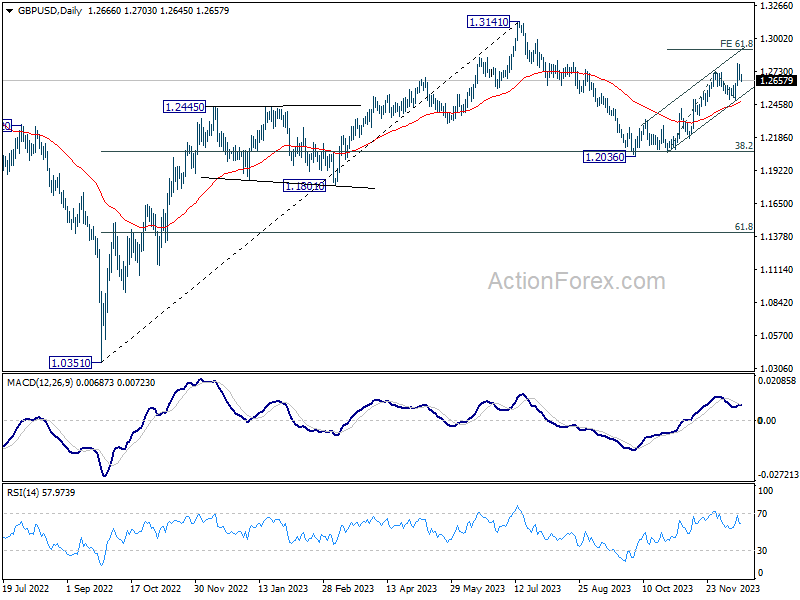

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2638; (P) 1.2715; (R1) 1.2760; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.2793 is extending. While deeper retreat cannot be ruled out, outlook will stay cautiously bullish as long as 1.2499 support holds. On the upside, firm break of 1.2793 will resume the rally from 1.2036. Next target is 61.8% projection of 1.2068 to 1.2731 from 1.2499 at 1.2909.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

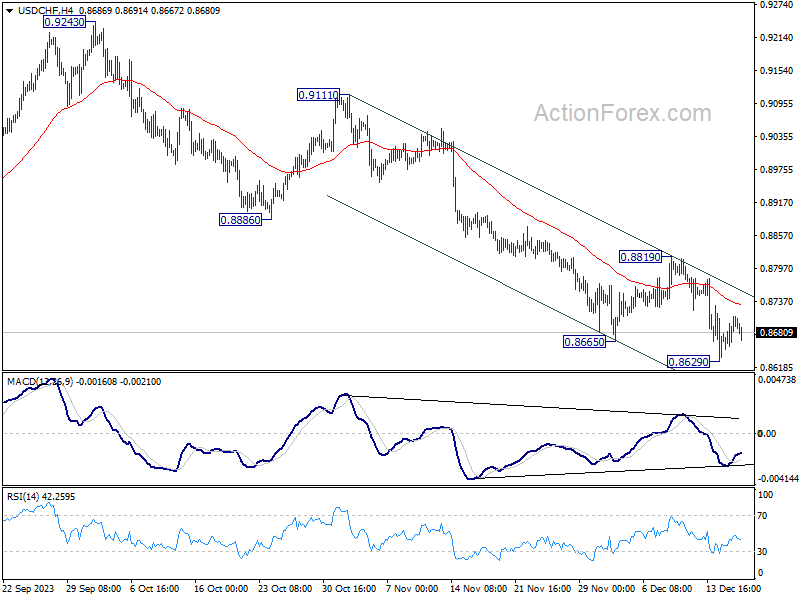

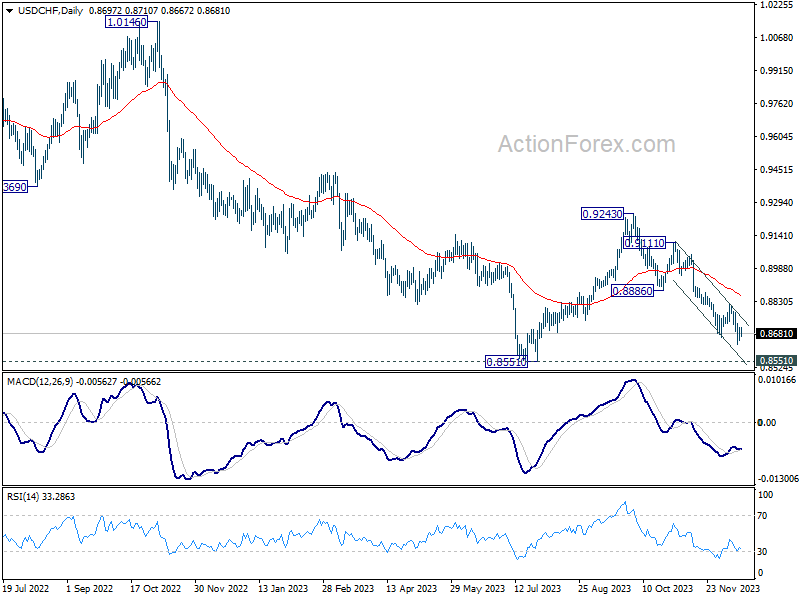

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8665; (P) 0.8689; (R1) 0.8726; More....

Intraday bias in USD/CHF remains neutral as consolidation from 0.8629 is in progress. Outlook remains bearish with 0.8819 resistance intact. On the downside, break of 0.8629 will resume larger fall from 0.9243 to retest 0.8551 key support next. On the upside, however, firm break of 0.8819 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 0.8551 are currently seen as a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Strong support should be seen 0.8551 to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.57; (P) 142.02; (R1) 142.61; More...

USD/JPY is still extending consolidation from 140.95 and intraday bias remains neutral. Stronger recovery cannot be ruled out. But upside should be limited well below 146.58 resistance to bring another decline. On the downside, break of 140.94 will resume the fall from 151.89 to next fibonacci level at 136.63.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

Central Banks Look to Spoil the Party, BoJ Eyed Tonight

Not the most thrilling start to the week but that's to be expected given the number of major events over the last few sessions and the absence of anything significant today.

The second half of last week was quite the ride, with the Fed going further than many expected on rate cuts for next year, the ECB then pushing back stronger than anticipated, and the BoE proving they're not even up for discussion yet as three policymakers voted to hike.

That said, it's almost like the latter two never happened as markets are still pricing 150 basis points of cuts from the Fed and ECB next year and 100 basis points from the BoE.

There's every chance the ECB messaging was designed to prevent a repeat performance of how markets responded to the Fed. And with the former not releasing a dot plot as their US counterparts do, it was easier to take that position. A lot is now priced in and the ECB was likely driven by the desire to stop conditions easing any further.

We've seen more pushback from policymakers on both sides since which suggests no one is particularly pleased with just how carried away investors have got. But as yet, it hasn't had too great an impact and it may take a much bigger effort and some disappointing economic figures to kill the buzz.

We have inflation data from the US and UK this week which could easily do just that, although in the case of the former, the CPI numbers released a couple of weeks earlier tend to be more impactful even if these are the Fed's preferred measure.

The BoJ overnight tonight will also be interesting given the amount of speculation about ending negative interest rates in the new year and further tweaks to yield curve control. This week probably still comes too soon but I would say this is still very much a live meeting that could surprise a few, if not in the form of the decisions then potentially the messaging.

Oil recovers as markets price in more rate cuts

Oil prices are recovering a little but remain broadly under pressure after falling 20% over two months from the middle of October. There's still a lot of uncertainty and debate around the demand outlook for next year and it would appear the prospect of many rate cuts has boosted the odds of a softer landing which could support demand and may have done the same to the price in recent days.

But there are clearly risks to that, not least that markets may have become overly optimistic about cuts next year. Then there's also the risk that past cuts could have an even more dampening impact on the global economy or that OPEC+ compliance is as weak as the deal indicated it could be. There are of course upside risks too, that demand and the economy outperform as they have this year which much lower interest rates could support.

Gold back above $2,000 but can it hold?

December has been a volatile month for gold, with the yellow metal kicking things off with new record highs before immediately giving those gains back to move below $2,000. The last week has seen it bounce back above $2,000, the question now is whether it's a sustainable rebound. While the environment looks favorable for gold, recent moves suggest traders aren't convinced at these levels and I'm not sure how much more optimistic on rates markets can reasonably become. A weaker dollar could help but if recent days are anything to go by, this may well become the season of pushback from central banks desperately trying to manage expectations.

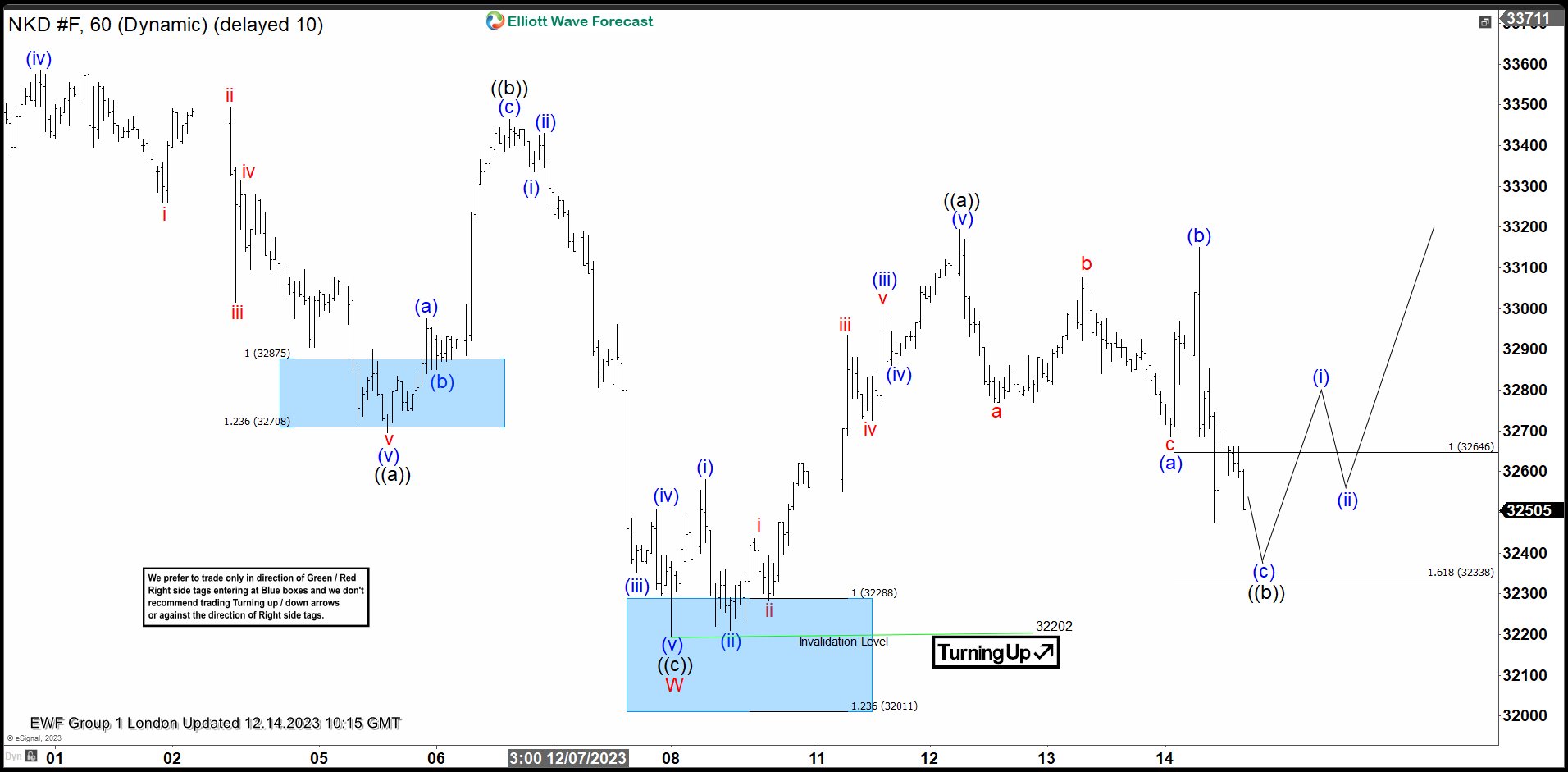

NIKKEI (NKD_F) Forecasting The Rally After 3 Waves Pull Back

Hello fellow traders. In this technical article we’re going to take a look at the Elliott Wave charts charts of NIKKEI Futures published in members area of the website. As our members know NIKKEI Futures has been giving us good trading setups recently. We have been favoring the long side due to impulsive bullish sequences the futures is showing. In further text we’re going to explain the short term Elliott Wave forecast.

NIKKEI Elliott Wave 1 Hour Chart 12.14.2023

NIKKEI ended cycle from the 11.20. peak at the 32202 low. We got 5 waves up in the rally from the short term low. Currently the futures is doing intraday pull back that seems to be unfolding as potential flat pattern , wave ((b)). Pull back already shows 3 waves down from the last peak. The price has reached intraday equal legs area at 32646-32338. At that zone we expect buyers to appear for a 3 waves bounce at least or further rally ideally.

Note: Keep in mind not every chart is trading recommendation. Official trading strategy on How to trade 3, 7, or 11 swing and equal leg is explained in details in Educational Video, available for members viewing inside the membership area.

NIKKEI Elliott Wave 1 Hour Chart 12.16.2023

The futures found buyers at the marked equal legs area as expected and we got good reaction from there. We count pull back completed at 32470 low. Short term rally made 5 waves up from the 32470 low, and now we are getting 3 waves pull back in (ii) blue. We don’t recommend selling in any proposed pull back.

Fed’s Mester: The next phase is not when to reduce rates

In a Financial Times interview, Cleveland Fed President Loretta Mester put emphasis on the duration of maintaining restrictive monetary policy to ensure that inflation reliably returns to the 2% target. That's contrary to market expectations, which centers on timing and extent of rate cuts.

Mester's key statement, "The next phase is not when to reduce rates... It's about how long do we need monetary policy to remain restrictive in order to be assured that inflation is on that sustainable and timely path back to 2%,"

"The markets are a little bit ahead. They jumped to the end part, which is 'We're going to normalize quickly', and I don't see that," she added.

When the discussion eventually shifts to the timing and pace of rate cuts, Mester highlighted the importance of one-year forward inflation expectations and their alignment towards the 2% target.

"If you don't take action as expected inflation comes down, then you're really firming policy," she warned. "You don't want to inadvertently become more restrictive than you think is appropriate."

EUR/USD: Regains Traction But Recovery Faces Strong Headwinds

EURUSD found a footstep and firmed on Monday after 0.9% drop last Friday, following a double failure at psychological 1.10 barrier.

However, recovery is unlikely to extend much as near-term action is weighed by much weaker-than-expected German Ifo data and rising bearish momentum on daily chart.

Also, long upper shadow on last week’s candlestick and repeated failure to register a weekly close above 1.10 barrier, add to negative signals.

Slight bullish bias can be expected while the price holds above cracked Fibo pivot at 1.0900 (38.2% retracement of 1.0723/1.1009 upleg), but more work at the upside will be required (close above 1.0950) to sideline downside threats.

Caution on break of 1.0900 handle and nearby 20DMA (1.0875) which would risk deeper drop on completion of reversal pattern and a double-top (1.1009/03).

Res: 1.0942; 1.0965; 1.1000; 1.1017.

Sup: 1.0900; 1.0875; 1.0866; 1.0832.