Sample Category Title

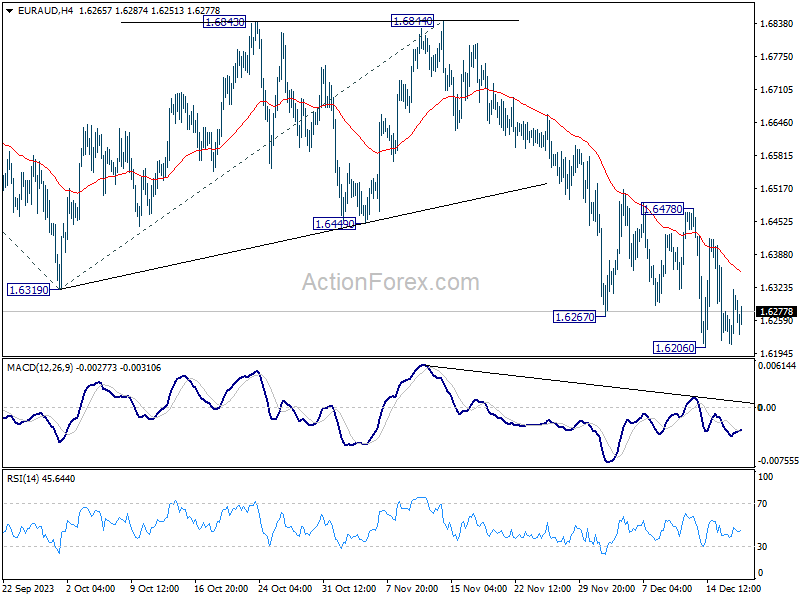

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6177; (P) 1.6303; (R1) 1.6383; More...

Intraday bias in EUR/AUD remains neutral as consolidation from 1.6206 is extending. Outlook remains bearish as long as 1.6478 resistance holds. On the downside, firm break of 1.6206 will resume whole fall from 1.7062. Next target is 100% projection of 1.7062 to 1.6319 from 1.6844 at 1.6106.

In the bigger picture, fall from 1.7062 medium term top is seen as correcting the whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound on first attempt. But risk will stay on the downside as long as 1.6844 resistance holds. Sustained break of 1.6000 would bring further fall to 61.8% retracement at 1.5343.

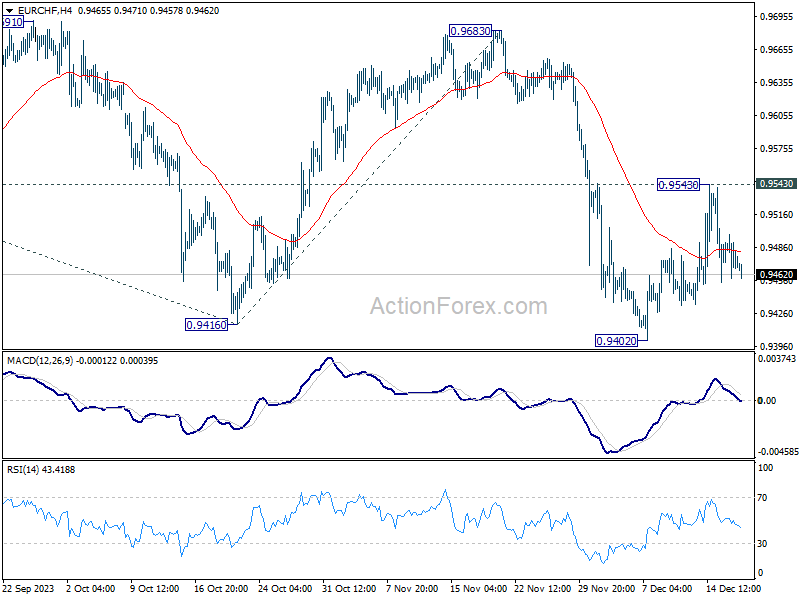

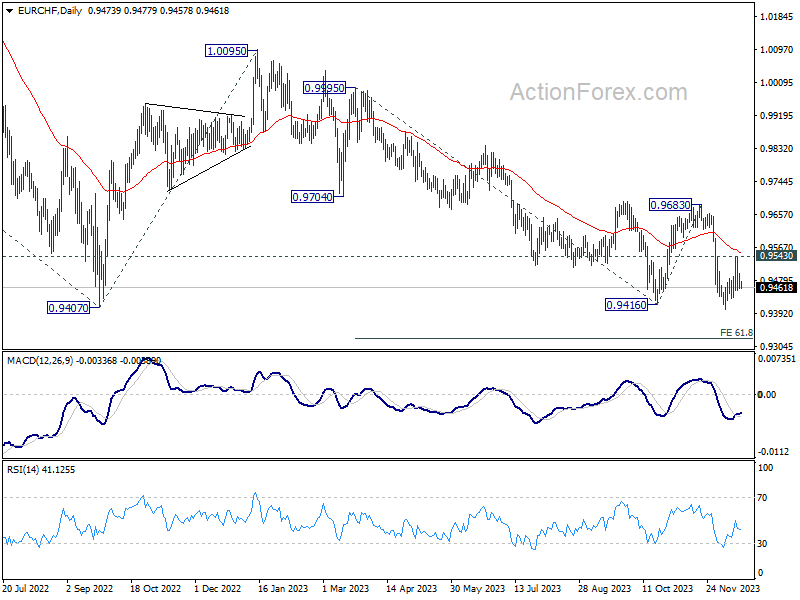

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9454; (P) 0.9477; (R1) 0.9494; More...

EUR/CHF is still extending the consolidation from 0.9402 and intraday bias remains neutral. Deeper decline is expected with 0.9543 resistance intact. On the downside, firm break of 0.9407 will confirm larger down trend resumption. Next target is 61.8% projection of 0.9995 to 0.9416 from 0.9683 at 0.9325. However, sustained break of 0.9543 will bring further rally back to 0.9683 resistance instead.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Firm break of 0.9407 (2022 low) will resume long term down trend. Next target will be 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

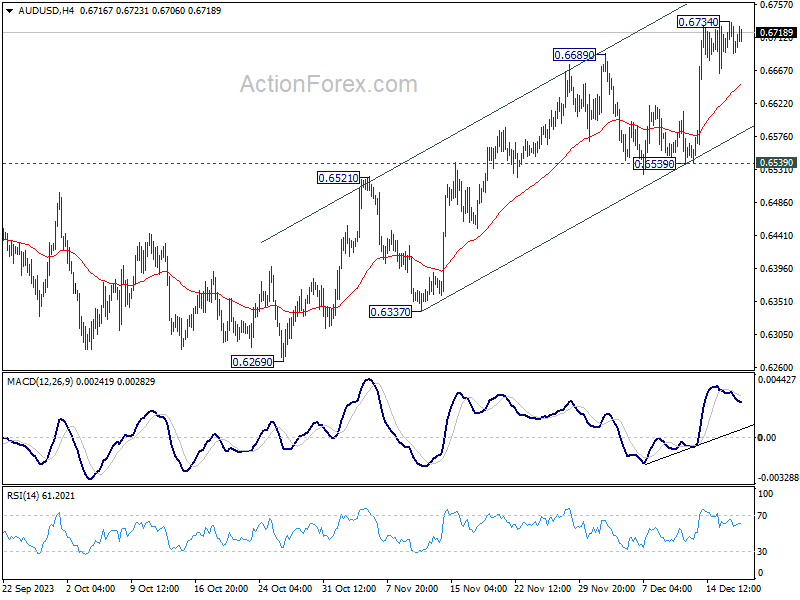

AUD/USD Daily Report

Daily Pivots: (S1) 0.6687; (P) 0.6711; (R1) 0.6731; More...

Intraday bias in AUD/USD is turned neutral with current retreat and some consolidations could be seen first. But further rally is expected as long as 0.6539 support holds. As noted before, fall from 0.7156 could have completed with three waves down to 0.6269. Above 0.6734 will target 0.6894 resistance next.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. Price actions from 0.6169 (2022 low) could be just a medium term corrective pattern. Rise from 0.6269 is seen as the third leg of the pattern. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

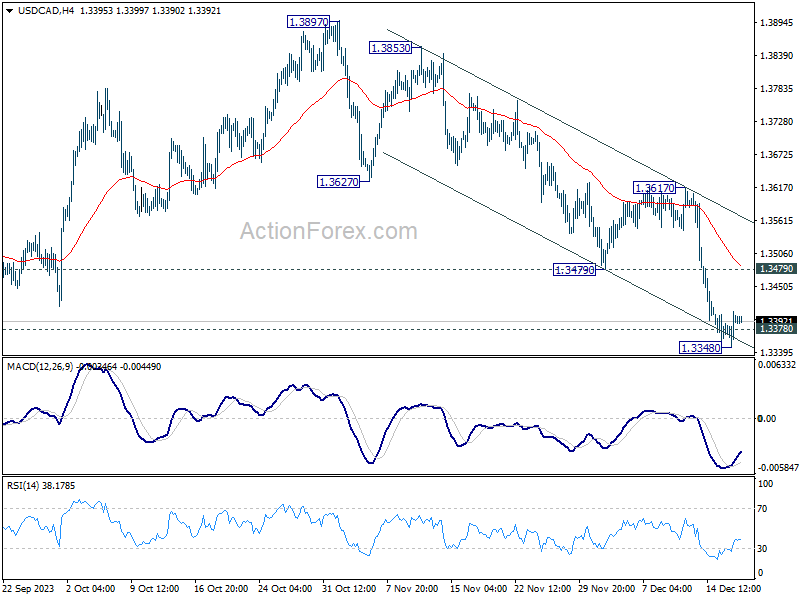

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3363; (P) 1.3386; (R1) 1.3422; More...

Intraday bias in USD/CAD is turned neutral with current recovery, and some consolidations would be seen. Risk will stay on the downside as long as 1.3479 support turned resistance holds. Rise from 1.3091 could have completed at 1.3897 already. Sustained trading below 1.3378 support will bring deeper fall to 1.3091 support next.

In the bigger picture, outlook is mixed up by deeper then expected fall from 1.3897. But after all, price actions from 1.3976 (2022 high) are viewed as a corrective pattern that's in progress. Larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage as long as 1.2947 resistance turned support holds.

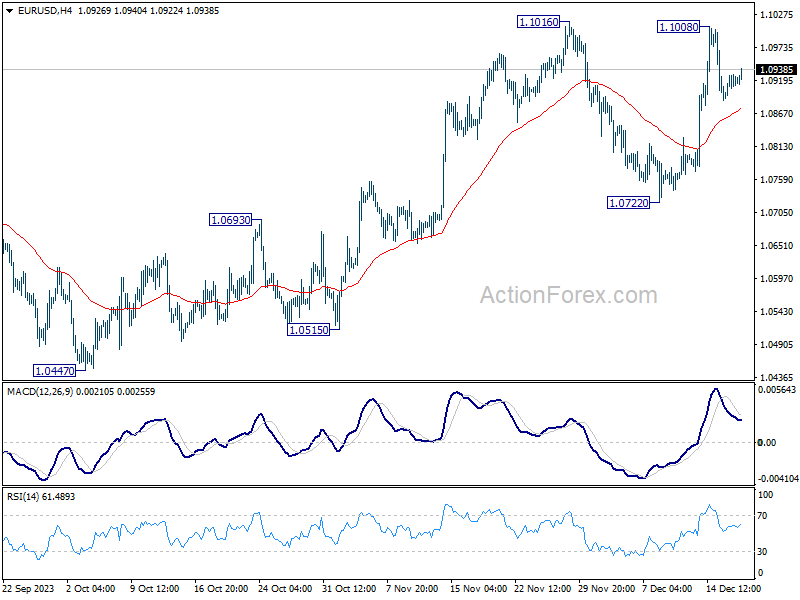

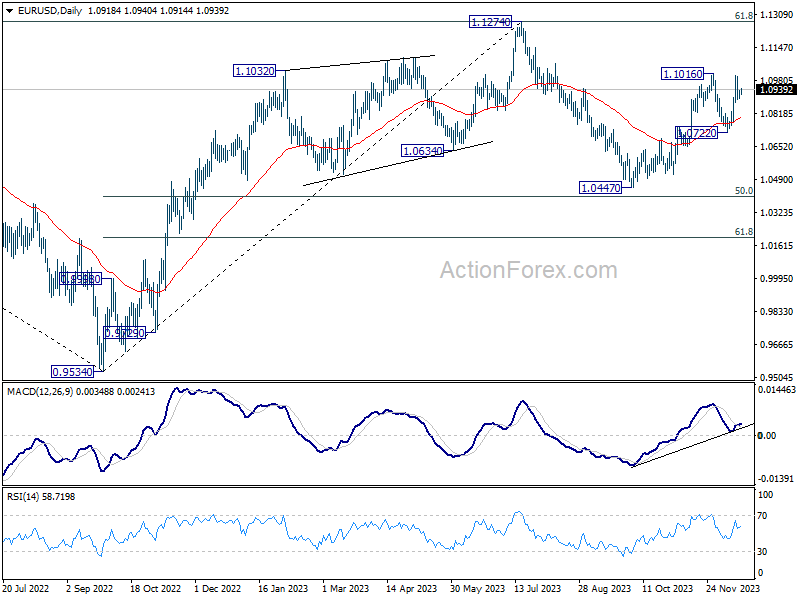

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0900; (P) 1.0916; (R1) 1.0939; More...

No change in EUR/USD's outlook as consolidation from 1.1008 is still extending. Intraday bias stays neutral at this point. Further rally is expected as long as 1.0722 support holds. On the upside, break of 1.1016 will resume the whole rise from 1.0447 to retest 1.1274 high.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

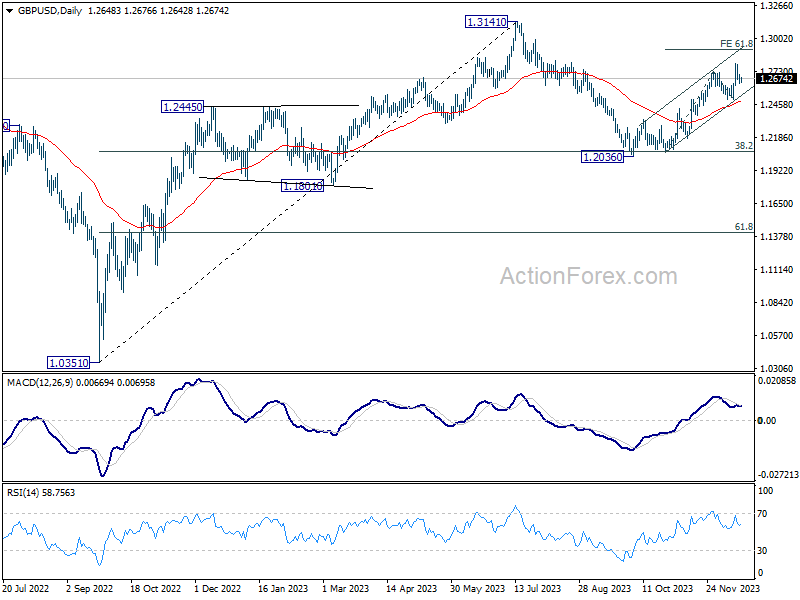

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2616; (P) 1.2660; (R1) 1.2691; More...

No change in GBP/USD's outlook as consolidation from 1.2793 is still extending. Intraday bias remains neutral at this point. Further rally is expected as long as 1.2499 support holds. On the upside, firm break of 1.2793 will resume the rally from 1.2036. Next target is 61.8% projection of 1.2068 to 1.2731 from 1.2499 at 1.2909.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

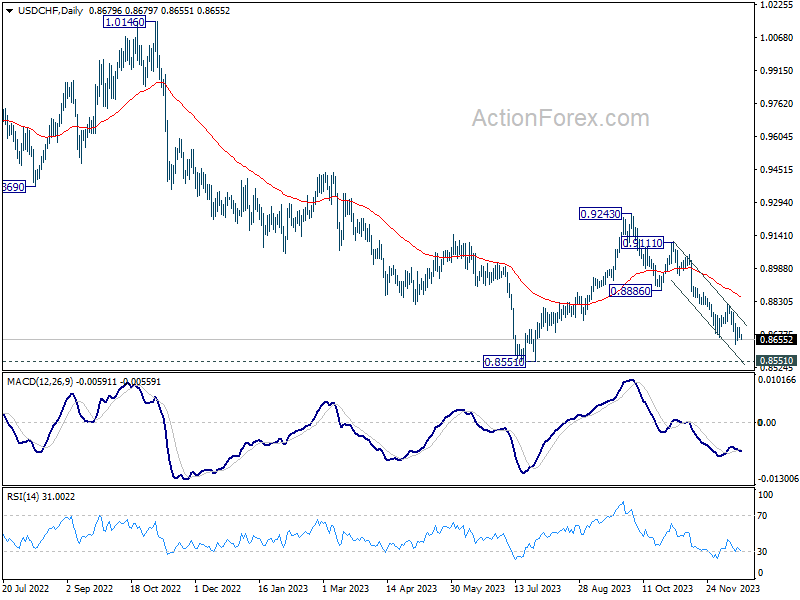

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8655; (P) 0.8683; (R1) 0.8700; More....

Outlook in USD/CHF is unchanged. Intraday bias stays neutral as consolidation from 0.8629 might extend further. But further decline is expected with 0.8819 resistance intact. On the downside, break of 0.8629 will resume larger fall from 0.9243 to retest 0.8551 key support next. On the upside, however, firm break of 0.8819 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 0.8551 are currently seen as a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Strong support should be seen 0.8551 to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243.

New Threat to Inflation

The week started with mixed feelings. Investors broadly ignored the Federal Reserve (Fed) members’ latest warnings that the interest rate cuts won’t come as soon and as fast as priced in by the financial markets. Equity bulls look determined to keep the Xmas magic alive. Big banks like Goldman Sachs also add fuel on fire, citing that the dovish Fed is good for stocks. We all agree. Dovish Fed is good for stock valuations, yet, how long the Fed could remain dovish if the economy heats up?

Anyway, attention was rather on a burst of mergers and acquisitions worth around $40bn that hit the wire on Monday. The S&P500 advanced to a fresh ytd high yesterday, while Nasdaq 100 renewed record for the 2nd straight session. Amazon rallied 2.73% yesterday, as Nvidia tested the $500 offers for the 3rd time since August. Apple was an exception to another euphoric day of trading, as its shares fell after hitting a fresh high last week on news that China is extending its ban of foreign device usage and on news that the company will halt the sale of Apple watches on a patent dispute.

Reality check

Yesterday’s trading was also marked by geopolitical tensions and news. The week started with the news that the world’s leading shipping companies decided to halt transit through the Suez Canal due to attacks by Iran-backed Houthis on commercial ships. The latter increases the risk premium of using the short-cut of Suez Canal and encourages ships to go around Africa instead. Considering that around 12% of global trade goes through the Suez Canal, and the deviation around Africa adds between 6 to 14 days to shipments, the Red Sea disruptions delay the shipment of goods but also increase the price of shipping the goods. This, coupled with the disruption in Panama Canal due to drought-induced delays put the global supply chains under pressure, again.

Big shipping company stocks gain as they can increase their prices, energy companies also started announcing that they will avoid transiting via the Red Sea region. Crude oil and natural gas prices come under a renewed positive pressure.

An extended period of disruption in global trade ways should not only sustain energy prices, but also put a renewed pressure on global supply chains and shipping prices. The latter is a threat to inflation. Remember, the pandemic-related supply chain disruptions were the major reason that sent inflation to almost 10% in the US. Middle East tensions are expected to have a modest impact compared to the pandemic disruption, but the rising shipping costs – if they last – could lead to an uptick in inflation. Therefore, it is well possible that the Fed uncorked the champagne before winning the inflation battle.

As of today, upside risks to inflation persist and build up, and this will inevitably dawn on investors sooner rather than later. A stronger case is being built for a sizeable downside correction in both stock and bond markets into next year.

This being said, the Eurozone’s November inflation numbers are out this morning; headline inflation is expected to have eased to 2.4% and core inflation to 3.6% in November. Inflation in Canada is expected to fall below the 3% mark. Sufficiently soft inflation figures could cheer up investors, but it’s worth keeping an eye on shipping news.

BoJ on Hold

In focus today

Today, euro area final HICP data for November will be released. With all the details out, it will be interesting to see what drove the downtick in inflation in November.

In the US, we will get housing starts and building permits for November.

On the central bank front, we have a few ECB speakers and Fed's Bostic on the wires today.

Following today's BoJ decision, we will get Japanese trade data overnight.

Also, overnight, China will announce 1-year and 5-year loan rates but no changes are expected at this point.

The 60 second overview

BoJ: The Bank of Japan kept its quantitative and qualitative easing with yield curve control policy unchanged this morning as expected. The policy rate stays at -0.1% and the 10-year yield target around 0, with the upper bound of 1.0 percent as a reference rate. The bank offers no clues on plans for tightening in 2024 and even kept the pledge to "not hesitate to take additional easing measures if necessary". USD/JPY took a leg higher on the decision as it traded back above 143, but the yen remains off the very weak levels from November. We continue to look for the April meeting as the most likely timing for the next move from the BoJ but the January meeting could also be interesting. Dismantling YCC and hiking the policy rate out of negative will be on the agenda if wages accelerate in the spring as expected.

Red Sea: The attacks by Houthi rebels on vessels passing through the Red Sea continue to induce shipping companies to pull out of the region. Yesterday, energy prices rose following BP's decision to bypass the waters due to security risks. According to shipping data compiled by Bloomberg, transportation activity through the Red Sea has dropped 35% since the beginning of December. As about 10-15% of global seaborne trade passes through the Suez Canal, the risk of new supply disruptions has risen. This could also pose upward risks to inflation next year. US Defence Secretary Austin will today meet fellow ministers to gather a maritime task force to deal with the attacks.

Equities: Global equities were marginally higher yesterday as US and cyclical growth stocks rose. It was interesting to see financials, industrials, and utilities lower. We argue this does not mark a change of the recent rotations, but markets have made it a long way the last two months and we may be in for a period with smaller moves and less difference between best and worst performers. In the US yesterday, Dow +0.00%, S&P 500 +0.5%, Nasdaq +0.6% and Russell 2000 -0.1%. Asian markets focus on the BoJ meeting which did not bring much news or changes. This resulted in a weaker yen and higher equities. Futures in Europe are marginally higher while US futures are flattish.

FI: Hawkish comments from ECB/Fed members provided some headwinds to bond markets in yesterday's session. Bund yields rose 5-6bp across the curve with markets continuing to price in 150bp worth of cuts next year. The 10Y BTP spread to Bunds tightened a couple of basis points throughout the session. Inflation swap rates rose slightly with energy prices as BP halted their shipping routes through the Red Sea.

FX: The JPY weakened immediately after Bank of Japan's decision to leave rates and YCC unchanged. USD/JPY rose from 142.60 to 143.60. After last week's gyrations, EUR/USD has remained flat around 1.09 this week. EUR/GBP moved higher again yesterday with focus on a speech by MPC Breeden later today and CPI tomorrow. EUR/NOK has continued to trade on a heavy note this week with the cross moving firmly below the 11.40-mark and EUR/SEK too is on the defensive.

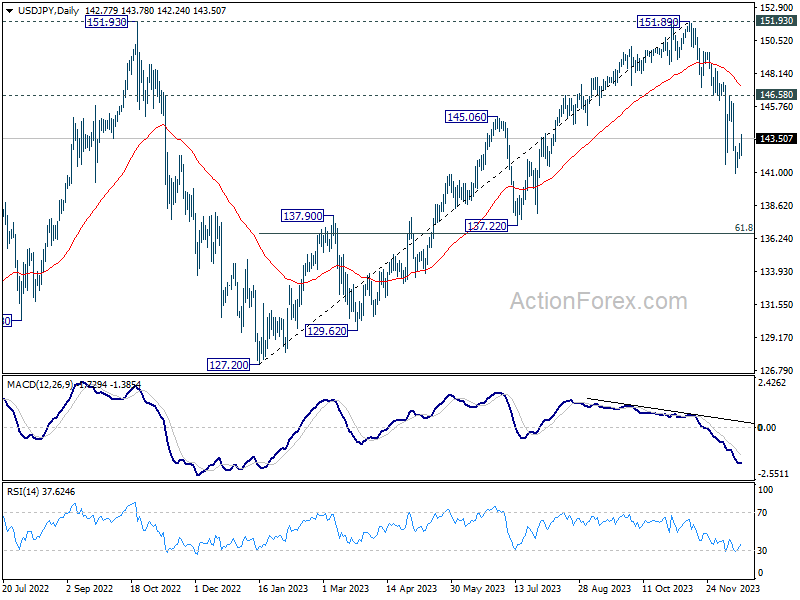

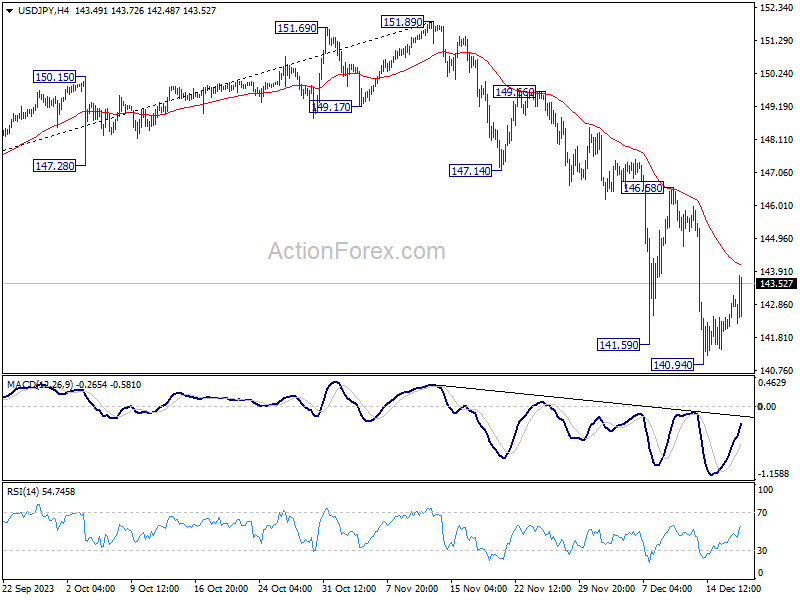

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.15; (P) 142.66; (R1) 143.30; More...

While USD/JPY's recovery from 140.94 extends higher today, outlook is unchanged. Upside of recovery should be limited well below 146.58 resistance to bring another decline. On the downside, break of 140.94 will resume the fall from 151.89 to next fibonacci level at 136.63.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.