Sample Category Title

USD/JPY Technical: JPY Strength Remains Intact ahead of BoJ

- Consensus is expecting no change to BoJ’s monetary policy, but its policy statement and Governor Ueda’s press conference may signal an imminent shift away from short-term negative interest rates.

- Mounting pressures from public and private sectors with Economy Minister Shindo attending today’s monetary policy decision meeting as a representative from the Cabinet Office.

- Technical analysis suggests further potential weakness in the USD/JPY.

In December, the JPY was the best performer among the major currencies against the US dollar where it soared by +4.85% as of 19 December at this time of the writing.

The recent JPY strength has been attributed to two factors; the US Federal Reserve’s dovish pivot where it guided market participants by projecting three cuts on the Fed funds rate in 2024. In contrast, hawkish guidance from top BoJ officials made two weeks ago where Governor Ueda and Deputy Governor Himino’s remarks have dialled up speculations that the current short-term negative interest rate policy in Japan in place since 2016 is likely to be scrapped sooner than expected and may come as early on the 23 January 2024 monetary policy meeting where BoJ releases its latest economic outlook report on the same day.

Today, the Bank of Japan (BoJ) will conclude its last two-day monetary policy meeting for 2023 while the consensus expectations are expecting no change to the current monetary policy setting, BoJ can still potentially lay the groundwork for its upcoming shift away from short-term negative interest rates via its policy statement and BoJ Governor Ueda’s press conference at 3.30 pm after the close of the Japan’s stock market.

BoJ faced mounting pressures from the public and private sectors

Interestingly, ahead of today’s monetary policy decision outcome, it seems that mounting pressure from the public and private sectors has arisen, prominent Jaan business lobby Keidanren head Tokura said yesterday that BoJ must normalize monetary policy as early as possible. Also, today’s meeting outcome will be attended by Economy Minister Shindo as a representative from the Cabinet Office who cannot vote on monetary policy decisions.

It is rare for a cabinet minister to attend BoJ monetary policy meetings as such “attendee roles” are usually assigned to deputy ministers. In the past meetings that cabinet ministers attended had resulted in major monetary policy changes such as the launch of the mega quantitative asset-buying programme in April 2013.

USD/JPY is hovering around the 200-day moving average

Fig 1: USD/JPY medium-term trend as of 19 Dec 2023 (Source: TradingView, click to enlarge chart

The medium and short-term downtrend phases of the USD/JPY in place since a test on its 151.95 major resistance on 13 November 2023 remain intact as price actions remain below its downward sloping 20 and 50-day moving averages without a bullish divergence condition seen on its daily RSI momentum indicator at its oversold region.

Short-term momentum has turned bearish

Fig 2: USD/JPY short-term minor trend as of 19 Dec 2023 (Source: TradingView, click to enlarge chart

In the shorter term as depicted on the hourly chart, the RSI momentum indicator has staged a bearish breakdown below its parallel ascending support after it hit overbought status yesterday, 18 December.

Watch the 143.30 short-term pivotal resistance and a break below the recent 140.95 low printed last Thursday, 14 December may expose the next intermediate support at 139.20 in the first step (also the close to the 50% Fibonacci retracement of the prior medium-term uptrend phase from 16 January 2023 low to 13 November 2023 high).

On the other hand, a clearance above 143.30 negates the bearish tone for a potential minor countertrend rebound to see the next intermediate resistances coming in at 144.80 and 146.70 if 144.80 is taken out.

Gold Price Could Struggle To Gain Traction – Here’s Why

Key Highlights

- Gold prices dropped toward the $1,970 support before the bulls appeared.

- A key bearish trend line is forming with resistance near $2,036 on the 4-hour chart.

- Crude oil prices started a recovery wave above the $71.20 resistance.

- AUD/USD rallied and cleared the 0.6700 resistance zone.

Gold Price Technical Analysis

Gold failed to continue higher and corrected lower sharply below $2,050 against the US Dollar. It even dived below the $2,000 support before the bulls appeared.

The 4-hour chart of XAU/USD indicates that the price traded as low as $1,972 and recently there was a recovery wave. There was a move above the $2,000 resistance zone. The price cleared the 100 Simple Moving Average (red, 4 hours) and the 200 Simple Moving Average (green, 4 hours).

However, the bears seem to be active near the 38.2% Fib retracement level of the downward move from the $2,145 swing high to the $1,972 low.

There is also a key bearish trend line forming with resistance near $2,036 on the same chart. An upside break above the $2,036 level could send the price soaring toward the $2,0600 resistance. The next major resistance is near the $2,080 level, above which Gold could test $2,120.

If not, the price could start a fresh decline. Initial support is near the $2,000 level. The first major support sits at $1,995 and the 200 Simple Moving Average (green, 4 hours).

The next major support could be $1,970. Any more losses might call for a move toward the $1,960 level in the coming days.

Looking at crude oil, there was a recovery wave above the $71.20 level, but the bears might appear near the $75.00 zone.

Economic Releases to Watch Today

- US Housing Starts for Nov 2023 (MoM) – Forecast 1.360M, versus 1.372M previous.

- US Building Permits for Nov 2023 (MoM) – Forecast 1.470M, versus 1.498M previous.

New Zealand’s trade deficit narrows to NZD -1.2B, led by decreased trade with china

New Zealand's goods trade deficit narrowed from NZD 1.7B to NZD 1.2B in November, aligning largely with market expectations. Exports fell by NZD 337m, representing -5.3% yoy decline, settling at NZD 6.0B. Meanwhile, imports saw a more substantial reduction of NZD 1.3B, -15% yoy decrease, totaling NZD 7.2B.

A key factor in these changes is reduced trade volume with China, which led contraction in both imports and exports. Exports to China decreased by NZD 183m, -9.7% yoy fall. Imports from China also saw a substantial reduction of NZD 347m, marking -17% yoy decrease.

Other key trading partners also showed varied trends. Exports to Australia and EU declined by NZD 35m (-4.5% yoy) and NZD 27m (-9.1% yoy), respectively. Conversely, exports to US increased by NZD 110m, a significant 18% yoy rise. Exports to Japan experienced a sharp decline of NZD 99m, -27% yoy drop.

In the realm of imports, alongside China, EU, Australia, US, and South Korea all registered declines. Imports from the EU decreased by NZD 164m (-14% yoy), from Australia by NZD 219m (-23% yoy), from the US by NZD 68m (-11% yoy), and from South Korea by NZD 231m (-32% yoy).

BoC’s Macklem see rate cuts in 2024, but with focus on core inflation trend

BoC Governor Tiff Macklem, in an interview with Bloomberg overnight, indicated that interest rate cuts are being considered "sometime in 2024," but he emphasized that this decision hinges critically on the sustained easing of core inflation.

Macklem underlined the importance of core inflation as a key focus for BoC. He stated, "We're very focused on core inflation." Specifically, he pointed out the necessity for "a number of months with sustained downward momentum in core inflation" before the central bank can confidently move forward with interest rate cuts.

Nevertheles, Macklem expressed a growing confidence in the effectiveness of the current monetary policy, acknowledging that "increasingly, the conditions are in place to get us back to two-per-cent inflation."

However, he was clear in conveying that this goal has not been fully achieved yet, stating, "but that is not yet assured, we're not there yet."

Fed’s Daly views 2024 as right for rate cuts, timetable uncertain

San Francisco Fed Bank President Mary Daly, in a Wall Street Journal interview yesterday, suggested that it might be appropriate for policymakers to start considering rate cuts in 2024, especially considering the easing of inflation this year. However, she also cautioned that it is premature to speculate on the exact timing of these rate reductions.

Daly emphasized the delicate balancing act Fed faces: the need to achieve price stability while minimizing job losses. Fed's goal is to bring inflation down to its 2% target, but Daly highlighted the importance of doing so gently, "with as few disruptions to the labor market as possible."

Another key point from Daly's interview concerns the real borrowing costs for households and businesses. With inflation showing a downward trend, maintaining the current rate could inadvertently increase these costs. Daly conveyed her wariness that "we could overtighten quite easily, and so that's what I'm mindful of".

Aligning with the broader perspective of Fed policymakers, Daly's views resonate with the median projections released last week. These projections suggest a majority of the 19 Fed policymakers anticipate a 75 basis-point reduction from the current target range of 5.25%-5.50% for the policy rate, aiming to bring inflation down to about 2.4% by the year's end.

NZ First Impressions: ANZ Business Confidence

Business confidence has continued to rise. However, there remains limited momentum in activity, and ongoing inflation pressures.

Key results (December 2023)

- Business confidence: 33.2 (Prev: 30.8)

- Expectations for own trading activity: 29.3 (Prev: 26.3)

- Activity – same month one year ago -4.2 (Prev: -12.5)

- Inflation expectations: 4.61% (Prev: 4.79%)

- Pricing intentions: 50.2 (Prev: 46.8)

The ANZBO measure of business confidence rose to 33.2 in December. That’s the eighth rise in a row, and takes confidence back to levels we last saw in 2015. We also saw a further rise in firms’ expectations for their own trading activity.

However, while business confidence is on the rise, digging into the details we’re left with a still soft picture of economic activity at the close of 2023. Most businesses (a net 4%) actually reported that trading activity has declined over the past year. While that’s not as low as it was last month, it still points to weakness in economic activity. There’s been particular weakness in the retail and construction sectors, consistent with the feedback we’ve received from businesses around the country.

There was also some notable news on the inflation front. Expectations for inflation over the coming year have continued to ease, dropping from 4.8% previously to 4.6% now. That’s still high, but moving in the right direction.

However, there were more worrying signs when we look at businesses’ expectations for their own finances. The number of businesses who expect their operating costs to rise picked up to 76.2% (from 73.9% previously). There’s also been an increase in the number of businesses who are planning on increasing their prices to 50.2%. That’s the third increase in a row.

Those continued cost and price pressures chime with comments we’ve heard from our own business contacts who have reported that operating cost pressures remain firm. In many cases, they’ve also told us it’s become harder to pass cost increases into output prices. We expect that continued pressure on operating costs will mean that domestic inflation eases only gradually over the year ahead.

Overall, while confidence is up, we’re still left with a picture of limited momentum in economic activity and lingering inflation pressures.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Hybrid – 5 December 2023

Members participating

Michele Bullock (Governor and Chair), Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Elana Rubin AM, Carol Schwartz AO, Alison Watkins AM

Others participating

Christopher Kent (Assistant Governor, Financial Markets), Marion Kohler (Acting Assistant Governor, Economic), Carl Schwartz (Acting Head, Domestic Markets Department)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Penelope Smith (Head, International Department), Tom Rosewall (Acting Head, Economic Analysis Department)

International economic developments

Members commenced their discussion of international economic developments by noting that the information on global inflation had been a little more encouraging over the prior month. Headline inflation rates had declined, driven by a fall in oil prices, while core inflation had continued to ease. Goods prices had declined in some countries in preceding months. However, inflation in the services sector had declined only gradually, reflecting still-tight labour markets, and housing inflation remained strong in a number of countries. Central banks generally expected inflation to return to their targets in late 2024 or 2025.

Members observed that output growth in several advanced economies had slowed noticeably in response to tighter monetary policy and cost-of-living pressures, particularly in Europe. In the United States, output growth had held up better than expected, helped by resilient consumption. Labour markets remained tight, but conditions had clearly eased in response to the slowing in economic activity. Job vacancies had fallen and unemployment rates, while still very low, had increased over preceding months, including in the United States. The pace of wages growth remained above levels considered consistent with central banks' inflation targets for some economies, but they had generally moderated in response to the gradual easing in labour market conditions and inflation. As a result, core inflation was expected to continue to moderate.

Turning to developments in China, members observed that the latest indicators of activity had generally been positive, and growth in retail sales and industrial production in October had remained strong. Activity had been supported by the continued recovery in services consumption after the pandemic, along with a range of supportive fiscal policy measures. There had, however, been little sign of improvement in the property sector. Real estate investment had continued to decline because of weak demand and liquidity constraints facing property developers.

Nonetheless, the continued positive information about the Chinese economy outside the property sector had supported iron ore prices, which had increased a little over the prior month and remained at high levels. Coking coal prices had fallen as supply disruptions in Australia had been resolved. Oil and gas prices had declined further over the prior month, as demand had eased in line with slower global growth and amid signs that the Hamas–Israel conflict seemed not to be spreading more widely across the region. Oil prices were around 15 per cent lower than their recent peak in late September.

Domestic economic conditions

Turning to the domestic economy, members observed that inflation had continued to moderate. The monthly CPI indicator for October showed that annual inflation had eased, with declines in the prices of petrol and holiday travel. Inflation excluding volatile items had also eased, largely reflecting the flow-through of declines in global goods price inflation. Rents had declined in October, but this owed entirely to an increase in Commonwealth Rent Assistance, which offset pressure from very tight rental markets in the capital cities. Tight rental markets were likely to be an ongoing source of inflationary pressure for some time. There had been little new information on inflation in other parts of the services sector. Firms in the Bank's liaison program expected price increases to moderate over the coming year, due to subdued demand and stronger competition among retailers, though many firms had also reported persistent cost pressures. Members noted some measures of inflation expectations had moved a little higher over preceding months but generally remained consistent with the inflation target.

Wages growth had picked up significantly over the preceding year or so. The Wage Price Index had recorded its highest quarterly growth rate since the series commenced in the late 1990s, reflecting the implementation of the Fair Work Commission's decision to significantly increase minimum and award wages. However, on the evidence available, spillovers to non-award wages did not appear to be larger than usual. Year-ended growth in wages was a little stronger than had been expected but the most recent forecasts had wages growth peaking at around 4 per cent by the end of the year. The wages growth outcome for the September quarter was still consistent with these forecasts, but members noted that the balance of risks had shifted a little to the upside. Conversely, there was some evidence of slowing in wages growth in those parts of the labour market where conditions had eased. In liaison, firms had reported that they generally expect wages growth to ease over the year ahead.

Members observed that labour market conditions remained tight, but less so than earlier in the year, as the demand for labour had adjusted to slower economic growth and labour supply had increased. Employment growth had eased to be a little below the rate of growth in the working-age population over the preceding few months, with the unemployment rate drifting up to 3.7 per cent. Members noted that the shifting composition of employment growth towards more part-time jobs and a decline in average hours worked over preceding months were consistent with hours worked being a key margin of adjustment to slower growth in demand. Forward-looking indicators, such as hiring intentions reported in business surveys and information from the Bank's liaison, pointed to a further easing in the demand for labour in coming months.

Output growth in Australia had slowed over the prior year to a rate below trend. The national accounts, which were scheduled to be released the day after the meeting, were expected to show that GDP growth had remained at a below-trend rate in the September quarter. Members discussed the implications for productivity of below-trend growth in economic activity and potential explanations for this outcome. While growth in household consumption had been weak, and was negative in per capita terms, overall demand had been supported by strong business investment and public demand.

Members noted that growth in household consumption was expected to have remained subdued in the September quarter, as higher interest rates and cost-of-living pressures weighed on real household disposable incomes and household spending. Timely indicators suggested that growth in consumer spending had also remained subdued into the December quarter. The increased importance of the November 'Black Friday' sales had distorted usual seasonal spending patterns and would make it difficult to obtain a clear reading of the underlying momentum in retail spending. Housing prices had increased further in November and had more than fully recovered their earlier declines. If sustained, higher household wealth would support consumer spending in the period ahead.

Despite slow growth in consumption, survey measures of business conditions had remained steady over prior months and were generally around average levels. The level of capacity utilisation had trended down over the prior year but remained high. Members noted that shortages of labour and materials remained a challenge in parts of the construction sector. Firms in the liaison program reported that investment intentions remain positive, reflecting solid cashflows and a large pipeline of construction and other projects, which was broadly in line with the results of the most recent ABS Capital Expenditure Survey.

International financial markets

Most advanced economy central banks had left policy rates unchanged since September, with most judging financial conditions to be restrictive. Central banks had continued to emphasise that policy rates may still need to rise further, but most noted that the risks to the outlook had become more balanced as inflation eased and labour market conditions became less tight. Market participants' expectations for policy rates in many advanced economies had been revised lower over the preceding months, with reductions in policy rates priced in by the middle of 2024. However, central banks had emphasised that it was too early to consider the timing of rate reductions.

Government bond yields in advanced economies had declined since the previous meeting, reversing most of the substantial increase over preceding months. The decline in bond yields had resulted from lower real yields, which reflected changing market expectations for policy rates as well as a decline in market-implied inflation expectations. Estimated term premia for sovereign bonds had also declined.

Conditions in private funding markets had loosened a little since the previous meeting. Equity prices had risen strongly as longer term interest rates fell and investors gained confidence that inflation could be returned to central banks' targets without significant declines in corporate profits, economic activity or employment. Corporate bond yields had declined alongside the fall in government bond yields and a narrowing of credit spreads.

In China, government bond yields had increased slightly alongside better-than-expected economic data and the announcement of further government bond issuance to support investment. Equity prices in China were little changed. Prices of securities issued by property developers remained at severely distressed levels, but had been supported in November by reports that authorities had established a list of developers eligible for additional funding.

The Australian dollar had appreciated by around 2 per cent against the US dollar and around 1 per cent on a trade-weighted basis since the previous meeting. Members observed that the trade-weighted Australian dollar was trading near early-2022 levels.

Domestic financial markets

Members noted that financial conditions in Australia were restrictive. Total household debt payments as a share of disposable income had increased significantly during the tightening phase. Although scheduled mortgage payments had increased to an all-time high of 10 per cent in October, estimated payments for personal credit were low relative to history because households' use of personal credit had declined significantly since 2008. As a result, total household debt payments remained below their estimated historical peak. Scheduled mortgage payments will continue to rise as borrowers with expiring fixed-rate loans roll off onto higher mortgage rates and lenders pass on the cash rate increase in November to lending rates.

New housing loan commitments had increased further, driven largely by investors and first home buyers. Commitments were 17 per cent above the February 2023 trough, though they were still almost 25 per cent below their peak in January 2022 and at low levels as a share of housing credit. Total extra payments into borrowers' mortgage offset and redraw accounts were still positive but were running lower in 2023 than the pre-pandemic average. This was consistent with pressures on disposable incomes from increases in interest rates and the broader rise in the cost of living.

Market participants' expectations for the path of the cash rate, as implied by market pricing, were a little lower than just prior to the November meeting. Markets were pricing in a 40 per cent chance of a further increase in the cash rate at future meetings. Markets were then pricing in some chance of a reduction in the cash rate by late 2024. This was broadly consistent with the views of market economists, most of whom expected no further rate increases and that the first reductions in the cash rate would be later in 2024.

Members discussed a paper that reviewed the Bank's approach to reducing its holdings of government bonds that had been purchased during the pandemic to support markets and provide economic stimulus. The current approach – endorsed by the Board in May – was to hold these bonds until maturity rather than selling them prior to maturity. This approach recognised, among other considerations, that the Bank's balance sheet was already set to decline rapidly as loans under the Term Funding Facility matured.

Members decided that the approach of holding the bonds to maturity remained appropriate but agreed to keep this under active consideration, including because of the Bank's exposure to interest rate risk and given the relatively gradual decline in the Bank's portfolio of bonds compared with some other advanced economy central banks. The initial tranche of Term Funding Facility maturities in September had passed smoothly, with the larger remaining tranche of maturities to occur through to mid-2024. These flows would continue to provide information on how financial markets respond as the Bank's balance sheet declines. Members discussed the importance of considering the decline in the Bank's balance sheet in the context of the broader operational framework for implementing monetary policy, given that it will affect the size and composition of the balance sheet over the longer term.

Members discussed whether any decision to sell some of the Bank's holdings of Australian Government securities would best be implemented by selling to the market or, in the case of mutual agreement, to the Australian Office of Financial Management (AOFM). While selling directly to the AOFM would have several practical benefits, either approach would involve working closely with the AOFM to avoid market disruption.

Considerations for monetary policy

Turning to the policy decision, members noted that the limited economic data received over the prior month had been broadly in line with expectations. Inflation had continued to decline but remained high. Wages growth had reached 4 per cent a little sooner than had been expected but the staff judged that wages growth was unlikely to rise much further. Output growth had continued below trend and the labour market was tight but easing gradually. Members agreed that financial stability considerations were not a constraint on monetary policy at the current meeting.

Members noted that market expectations for policy rates in other countries had eased significantly over the prior month, while being little changed for Australia. Longer term bond yields had declined notably, perhaps signalling that markets were more confident that central banks would be able to reduce inflation back to their targets in a reasonable timeframe with current policy settings. Members also noted that, in Australia, households' required interest payments as a share of disposable income were much higher than in recent years but still below the level recorded in 2008.

In light of these observations, members considered whether to raise the cash rate target by a further 25 basis points or to hold the cash rate target steady.

The case to raise the cash rate target by a further 25 basis points was centred on the observations that inflation was expected to remain above target for a prolonged period and that there were risks this period could be extended. Members noted that inflation was increasingly being driven by domestic demand. They also observed that underlying inflation was higher in Australia than in several other countries. Furthermore, domestic demand was judged still to be running above the level consistent with the inflation target and growth could be supported in the year ahead by a recovery in real household disposable income as inflation declined. Members noted that the staff's most recent forecasts, which were predicated on a lift in productivity growth, would see inflation return to the top of the target band by the end of 2025, rather than the midpoint of the band.

The case to hold the cash rate target constant reflected the view that the data over the prior month did not warrant a material revision to the outlook and that there is the possibility of a larger rise in the unemployment rate than anticipated. Members observed that monetary policy was working to bring aggregate demand and supply into closer alignment. They noted that the risk that it takes longer than expected to return inflation to target was balanced by the risk that aggregate demand slows more quickly than anticipated. Members acknowledged that consumption growth had been quite weak, as many households are experiencing a painful squeeze on their finances, with inflation and higher interest rates weighing on real disposable incomes. Members also noted that the pace of disinflation in some other countries over recent months had accelerated. If emulated in Australia, this would be helpful in bringing inflation back to target.

After weighing up these two options, members agreed that the case to leave the cash rate target unchanged at this meeting was the stronger one. Members agreed there was sufficient value in waiting for further data to assess how the balance of risks was evolving and how best to balance these risks when setting policy. They noted that there had been encouraging signs of progress towards the Board's objectives and that this needed to continue. Members also discussed the importance of preventing inflation expectations from drifting away from the inflation target and committed to monitoring this closely. At the time of the meeting, they agreed that inflation expectations remained consistent with the inflation target.

Members agreed that whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend on how the incoming data alter the economic outlook and the evolving assessment of risks. In making its decisions, the Board will continue to pay close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome.

The decision

The Board decided to leave the cash rate target unchanged at 4.35 per cent, and the interest rate on Exchange Settlement balances at 4.25 per cent.

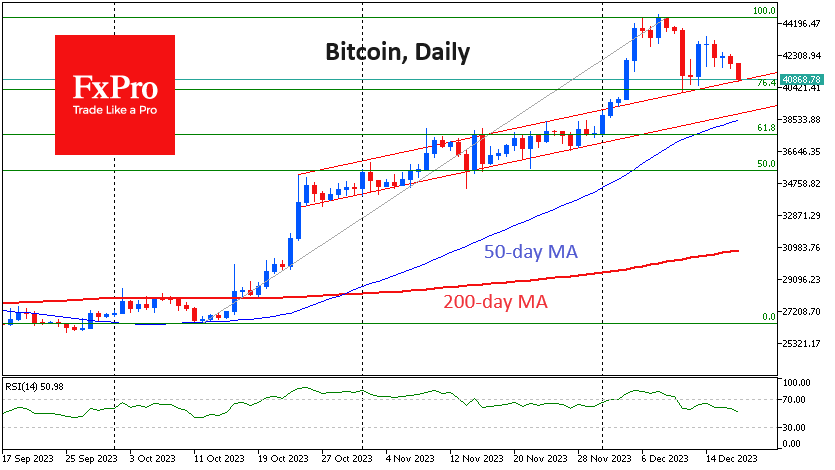

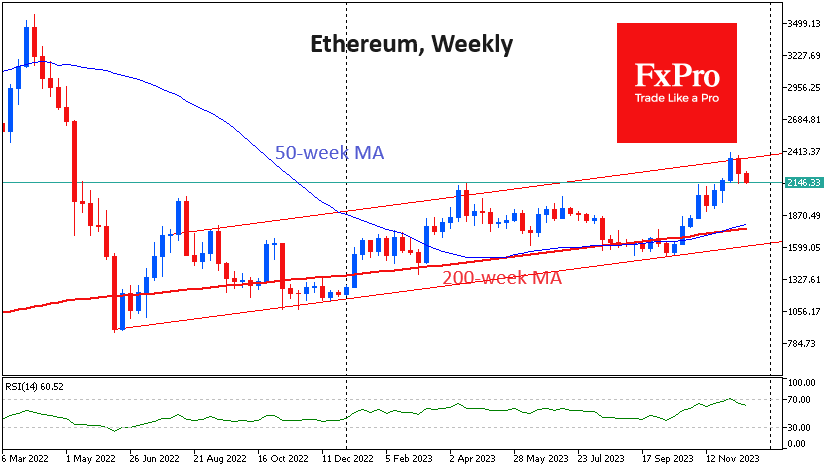

Bitcoin and Ether Set to Deepen Correction

Market Picture

The crypto market has started the new week with a correction sentiment, reducing capitalisation by 3% to $1.54 trillion in the last 24 hours. As is often the case with intense moves, Bitcoin looks more stable than the market, losing only 1.8% to $41.1K. Ethereum is down 2.3% to $2160.

Bitcoin is once again testing the local support it managed to hold last week. But we are attracted by a sequence of lower local highs, indicating an impressive selling proposition. We may be seeing profit taking from all the upside from the October lows. Working off this scenario suggests a pullback to the $38K area if the market falls below $40K. But even this potentially nasty drawdown looks to be just part of a larger bull cycle that Bitcoin is now moving within.

Ethereum is developing a retreat from the upper boundary of the trading channel, currently testing the early April peak area. The scenario of a shallow correction suggests a decline of about $100 more to $2060, but we should be ready for $1700 as well.

News Background

Morgan Creek Digital founder Anthony Pompliano believes that BTC continues to follow four-year market cycles fitting between halvings, and the next growth phase of the first cryptocurrency is now beginning.

The bitcoin-based NFT market will grow 100-fold in 2024, researchers at cryptocurrency exchange Bitget predict. The ORDI token, being the leading token of the Bitcoin ecosystem, is already capable of entering the top 30 in terms of market capitalisation during the next bull market. If the BTC ecosystem continues to expand, Bitcoin could reach $100K thanks to a surge in demand for the first cryptocurrency.

The US SEC is reviewing its approach to spot bitcoin ETFs following ‘court decisions’, the regulator’s head, Gary Gensler, commented. The agency is currently reviewing between eight and 12 such proposals, he said.

The SEC rejected a petition by exchange Coinbase to develop rules for the cryptocurrency industry. According to Gary Gensler, existing laws apply to the industry, and there is nothing that would indicate the need for new regulations.

Asset management companies Galaxy Digital and DWS Group, as well as Dutch market maker Flow Traders, are creating a subsidiary firm, AllUnity, which will issue a euro-denominated stablecoin.

One more Solana-based meme token, also featuring a dog, Bonk (BONK), rose 100% overnight after listing on Coinbase. Its capitalisation has already passed the $1.7 billion mark.

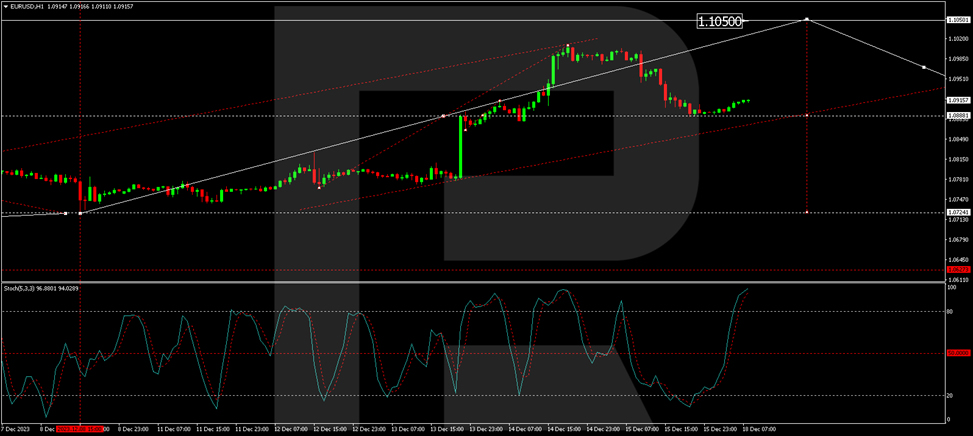

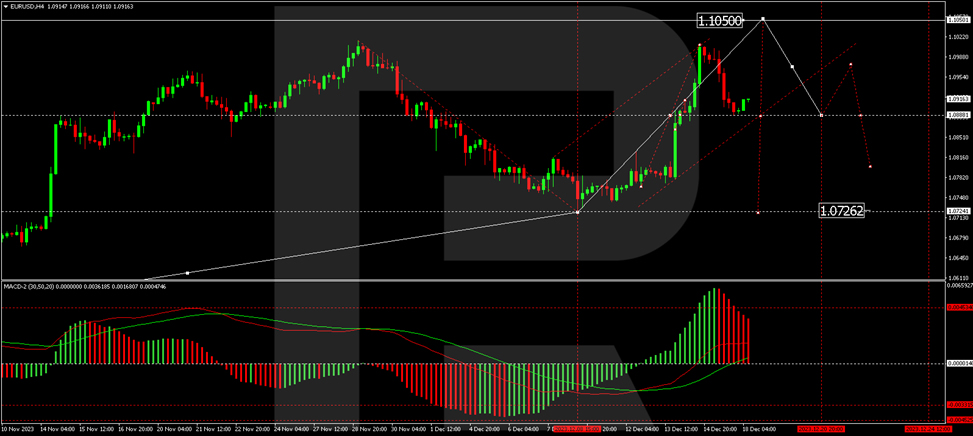

EUR/USD Finds Stability

On Monday, the EUR/USD pair is demonstrating stability, trading around the 1.0910 mark.

Last week was notable for the currency markets, as key financial updates were released. The Federal Reserve and the European Central Bank maintained their interest rates at 5.50% and 4.50% per annum, respectively. In the U.S., retail sales in November saw a modest increase of 0.3% month-on-month, following a decline in the previous month. Industrial production also showed growth, albeit slightly below expectations at 0.2%, compared to the anticipated 0.3%. This was a slight rebound from October's decrease of 0.9%.

A significant development was the decline in the U.S. production PMI for December, which fell to 48.2 points, indicating potential concerns over high inflation levels.

With most critical data released, the currency market is now poised for a period of relative stability as it heads towards the Christmas season.

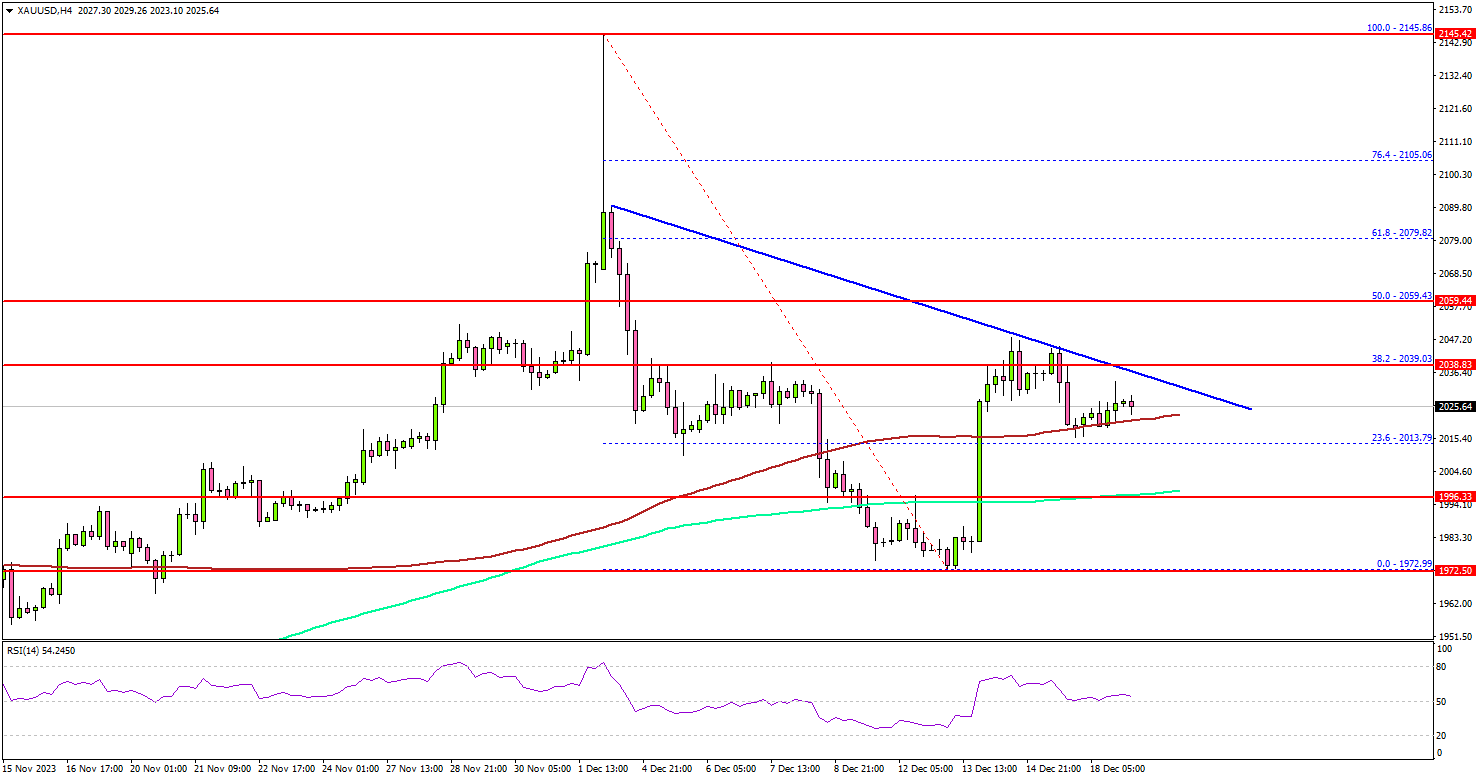

EUR/USD technical analysis

The EUR/USD H4 chart shows that the pair has established a consolidation range around 1.0888. Following an upward breakout, the price hit a local high of 1.1008 before correcting back to 1.0888 (testing from above). A new upward movement towards 1.1050 could initiate today. Upon reaching this level, a downward trend to 1.0727 may begin. The MACD indicator supports this view, with its signal line positioned above zero and pointing upwards.

On the EUR/USD H1 chart, the pair has finished its correction, bouncing off 1.0888. A rising structure is forming towards 1.0970, which could extend to 1.1050. Once this level is reached, a downward movement towards the first target of 1.0725 might ensue. This technical scenario is backed by the Stochastic oscillator, which shows its signal line above 80 and indicates potential further rises to new highs.