Sample Category Title

Summary 12/11 – 12/15

Monday, Dec 11, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Index Q4 | 5.6 | 5.4 |

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | 2.50% | 2.40% |

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | -20.60% | |

| 23:30 | AUD | Westpac Consumer Confidence Dec | -2.60% | |

| 23:50 | JPY | PPI Y/Y Nov | 0.10% | 0.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Index Q4 | |

| Forecast: 5.6 | Previous: 5.4 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | |

| Forecast: 2.50% | Previous: 2.40% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | |

| Forecast: | Previous: -20.60% | ||

| 23:30 | AUD | Westpac Consumer Confidence Dec | |

| Forecast: | Previous: -2.60% | ||

| 23:50 | JPY | PPI Y/Y Nov | |

| Forecast: 0.10% | Previous: 0.80% | ||

Tuesday, Dec 12, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Nov | -2 | |

| 00:30 | AUD | NAB Business Conditions Nov | 13 | |

| 07:00 | GBP | Claimant Count Change Nov | 20.3K | 17.8K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | 4.20% | 4.20% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | 7.70% | 7.90% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | 7.40% | 7.70% |

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | 8.8 | 9.8 |

| 10:00 | EUR | Germany ZEW Current Situation Dec | -75.5 | -79.8 |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | 11.2 | 13.8 |

| 11:00 | USD | NFIB Business Optimism Index Nov | 90.7 | 90.7 |

| 13:30 | USD | CPI M/M Nov | 0.10% | 0.00% |

| 13:30 | USD | CPI Y/Y Nov | 3.10% | 3.20% |

| 13:30 | USD | CPI Core M/M Nov | 0.30% | 0.20% |

| 13:30 | USD | CPI Core Y/Y Nov | 4.00% | 4.00% |

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | 10 | 9 |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | 9 | 10 |

| 23:50 | JPY | Tankan Non - Manufacturing Index Q4 | 27 | 27 |

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q4 | 25 | 21 |

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | 13.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Nov | |

| Forecast: | Previous: -2 | ||

| 00:30 | AUD | NAB Business Conditions Nov | |

| Forecast: | Previous: 13 | ||

| 07:00 | GBP | Claimant Count Change Nov | |

| Forecast: 20.3K | Previous: 17.8K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | |

| Forecast: 7.70% | Previous: 7.90% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | |

| Forecast: 7.40% | Previous: 7.70% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | |

| Forecast: 8.8 | Previous: 9.8 | ||

| 10:00 | EUR | Germany ZEW Current Situation Dec | |

| Forecast: -75.5 | Previous: -79.8 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | |

| Forecast: 11.2 | Previous: 13.8 | ||

| 11:00 | USD | NFIB Business Optimism Index Nov | |

| Forecast: 90.7 | Previous: 90.7 | ||

| 13:30 | USD | CPI M/M Nov | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 13:30 | USD | CPI Y/Y Nov | |

| Forecast: 3.10% | Previous: 3.20% | ||

| 13:30 | USD | CPI Core M/M Nov | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 13:30 | USD | CPI Core Y/Y Nov | |

| Forecast: 4.00% | Previous: 4.00% | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | |

| Forecast: 10 | Previous: 9 | ||

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | |

| Forecast: 9 | Previous: 10 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Index Q4 | |

| Forecast: 27 | Previous: 27 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q4 | |

| Forecast: 25 | Previous: 21 | ||

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | |

| Forecast: | Previous: 13.60% | ||

Wednesday, Dec 13, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | GBP | GDP M/M Oct | -0.10% | 0.20% |

| 07:00 | GBP | Industrial Production M/M Oct | -0.10% | 0.00% |

| 07:00 | GBP | Industrial Production Y/Y Oct | 1.10% | 1.50% |

| 07:00 | GBP | Manufacturing Production M/M Oct | 0.00% | 0.10% |

| 07:00 | GBP | Manufacturing Production Y/Y Oct | 1.90% | 3.00% |

| 07:00 | GBP | Goods Trade Balance (GBP) Oct | -14.1B | -14.3B |

| 08:00 | CHF | SECO Economic Forecasts | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | -0.30% | -1.10% |

| 13:30 | USD | PPI M/M Nov | 0.10% | -0.50% |

| 13:30 | USD | PPI Y/Y Nov | 1.00% | 1.30% |

| 13:30 | USD | PPI Core M/M Nov | 0.20% | 0.00% |

| 13:30 | USD | PPI Core Y/Y Nov | 2.40% | |

| 15:30 | USD | Crude Oil Inventories | -4.6M | |

| 19:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% |

| 19:30 | USD | FOMC Press Conference | ||

| 21:45 | NZD | GDP Q/Q Q3 | 0.20% | 0.90% |

| 23:50 | JPY | Machinery Orders M/M Oct | -0.50% | 1.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | GBP | GDP M/M Oct | |

| Forecast: -0.10% | Previous: 0.20% | ||

| 07:00 | GBP | Industrial Production M/M Oct | |

| Forecast: -0.10% | Previous: 0.00% | ||

| 07:00 | GBP | Industrial Production Y/Y Oct | |

| Forecast: 1.10% | Previous: 1.50% | ||

| 07:00 | GBP | Manufacturing Production M/M Oct | |

| Forecast: 0.00% | Previous: 0.10% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Oct | |

| Forecast: 1.90% | Previous: 3.00% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Oct | |

| Forecast: -14.1B | Previous: -14.3B | ||

| 08:00 | CHF | SECO Economic Forecasts | |

| Forecast: | Previous: | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | |

| Forecast: -0.30% | Previous: -1.10% | ||

| 13:30 | USD | PPI M/M Nov | |

| Forecast: 0.10% | Previous: -0.50% | ||

| 13:30 | USD | PPI Y/Y Nov | |

| Forecast: 1.00% | Previous: 1.30% | ||

| 13:30 | USD | PPI Core M/M Nov | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 13:30 | USD | PPI Core Y/Y Nov | |

| Forecast: | Previous: 2.40% | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -4.6M | ||

| 19:00 | USD | Fed Interest Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 19:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 21:45 | NZD | GDP Q/Q Q3 | |

| Forecast: 0.20% | Previous: 0.90% | ||

| 23:50 | JPY | Machinery Orders M/M Oct | |

| Forecast: -0.50% | Previous: 1.40% | ||

Thursday, Dec 14, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Dec | 4.90% | |

| 00:01 | GBP | RICS Housing Price Balance Nov | -58% | -63% |

| 00:30 | AUD | Employment Change Nov | 10.0K | 55.0K |

| 00:30 | AUD | Unemployment Rate Nov | 3.80% | 3.70% |

| 04:30 | JPY | Industrial Production M/M Oct F | 1.00% | 1.00% |

| 07:30 | CHF | Producer and Import Prices M/M Nov | 0.10% | 0.20% |

| 07:30 | CHF | Producer and Import Prices Y/Y Nov | -0.90% | |

| 08:30 | CHF | SNB Interest Rate Decision | 1.75% | 1.75% |

| 09:00 | CHF | SNB Press Conference | ||

| 09:00 | CHF | SNB's Chairman Jordan speech | ||

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% |

| 12:00 | GBP | MPC Official Bank Rate Votes | 2--0--7 | 3--0--6 |

| 13:15 | EUR | ECB Interest Rate Decision | 4.50% | 4.50% |

| 13:30 | CAD | Manufacturing Sales M/M Oct | 0.30% | 0.40% |

| 13:30 | USD | Initial Jobless Claims (Dec 8) | 221K | 220K |

| 13:30 | USD | Retail Sales M/M Nov | -0.10% | -0.10% |

| 13:30 | USD | Retail Sales ex Autos M/M Nov | -0.10% | 0.10% |

| 13:30 | USD | Import Price Index M/M Nov | -0.80% | -0.80% |

| 13:45 | EUR | ECB Press Conference | ||

| 15:00 | USD | Business Inventories Oct | 0.00% | 0.40% |

| 15:30 | USD | Natural Gas Storage | -117B | |

| 21:30 | NZD | Business NZ PMI Nov | 42.5 | |

| 22:00 | AUD | Manufacturing PMI Dec P | 47.7 | |

| 22:00 | AUD | Services PMI Dec P | 46.0 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Dec | |

| Forecast: | Previous: 4.90% | ||

| 00:01 | GBP | RICS Housing Price Balance Nov | |

| Forecast: -58% | Previous: -63% | ||

| 00:30 | AUD | Employment Change Nov | |

| Forecast: 10.0K | Previous: 55.0K | ||

| 00:30 | AUD | Unemployment Rate Nov | |

| Forecast: 3.80% | Previous: 3.70% | ||

| 04:30 | JPY | Industrial Production M/M Oct F | |

| Forecast: 1.00% | Previous: 1.00% | ||

| 07:30 | CHF | Producer and Import Prices M/M Nov | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Nov | |

| Forecast: | Previous: -0.90% | ||

| 08:30 | CHF | SNB Interest Rate Decision | |

| Forecast: 1.75% | Previous: 1.75% | ||

| 09:00 | CHF | SNB Press Conference | |

| Forecast: | Previous: | ||

| 09:00 | CHF | SNB's Chairman Jordan speech | |

| Forecast: | Previous: | ||

| 12:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 5.25% | Previous: 5.25% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 2--0--7 | Previous: 3--0--6 | ||

| 13:15 | EUR | ECB Interest Rate Decision | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 13:30 | CAD | Manufacturing Sales M/M Oct | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 13:30 | USD | Initial Jobless Claims (Dec 8) | |

| Forecast: 221K | Previous: 220K | ||

| 13:30 | USD | Retail Sales M/M Nov | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Nov | |

| Forecast: -0.10% | Previous: 0.10% | ||

| 13:30 | USD | Import Price Index M/M Nov | |

| Forecast: -0.80% | Previous: -0.80% | ||

| 13:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 15:00 | USD | Business Inventories Oct | |

| Forecast: 0.00% | Previous: 0.40% | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -117B | ||

| 21:30 | NZD | Business NZ PMI Nov | |

| Forecast: | Previous: 42.5 | ||

| 22:00 | AUD | Manufacturing PMI Dec P | |

| Forecast: | Previous: 47.7 | ||

| 22:00 | AUD | Services PMI Dec P | |

| Forecast: | Previous: 46.0 | ||

Friday, Dec 15, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Dec | -23 | -24 |

| 00:30 | JPY | Manufacturing PMI Dec P | 48.2 | 48.3 |

| 00:30 | JPY | Services PMI Dec P | 50.8 | |

| 02:00 | CNY | Industrial Production Y/Y Nov | 5.60% | 4.60% |

| 02:00 | CNY | Retail Sales Y/Y Nov | 12.50% | 7.60% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Nov | 3.00% | 2.90% |

| 04:30 | JPY | Tertiary Industry Index M/M Oct | 0.20% | -1.00% |

| 08:15 | EUR | France Manufacturing PMI Dec P | 43.2 | 42.9 |

| 08:15 | EUR | France Services PMI Dec P | 46.0 | 45.4 |

| 08:30 | EUR | Germany Manufacturing PMI Dec P | 43.3 | 42.6 |

| 08:30 | EUR | Germany Services PMI Dec P | 49.8 | 49.6 |

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | 44.5 | 44.2 |

| 09:00 | EUR | Eurozone Services PMI Dec P | 49.0 | 48.7 |

| 09:30 | GBP | Manufacturing PMI Dec P | 47.5 | 47.2 |

| 09:30 | GBP | Services PMI Dec P | 51.0 | 50.9 |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Oct | 10.3B | 9.2B |

| 13:15 | CAD | Housing Starts Y/Y Nov | 260.0K | 274.7K |

| 13:30 | CAD | Wholesale Sales M/M Oct | 0.50% | 0.40% |

| 13:30 | USD | Empire State Manufacturing Index Dec | 2 | 9.1 |

| 14:15 | USD | Industrial Production M/M Nov | 0.30% | -0.60% |

| 14:15 | USD | Capacity Utilization Nov | 79.20% | 78.90% |

| 14:45 | USD | Manufacturing PMI Dec P | 49.1 | 49.4 |

| 14:45 | USD | Services PMI Dec P | 50.5 | 50.8 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Dec | |

| Forecast: -23 | Previous: -24 | ||

| 00:30 | JPY | Manufacturing PMI Dec P | |

| Forecast: 48.2 | Previous: 48.3 | ||

| 00:30 | JPY | Services PMI Dec P | |

| Forecast: | Previous: 50.8 | ||

| 02:00 | CNY | Industrial Production Y/Y Nov | |

| Forecast: 5.60% | Previous: 4.60% | ||

| 02:00 | CNY | Retail Sales Y/Y Nov | |

| Forecast: 12.50% | Previous: 7.60% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Nov | |

| Forecast: 3.00% | Previous: 2.90% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Oct | |

| Forecast: 0.20% | Previous: -1.00% | ||

| 08:15 | EUR | France Manufacturing PMI Dec P | |

| Forecast: 43.2 | Previous: 42.9 | ||

| 08:15 | EUR | France Services PMI Dec P | |

| Forecast: 46.0 | Previous: 45.4 | ||

| 08:30 | EUR | Germany Manufacturing PMI Dec P | |

| Forecast: 43.3 | Previous: 42.6 | ||

| 08:30 | EUR | Germany Services PMI Dec P | |

| Forecast: 49.8 | Previous: 49.6 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | |

| Forecast: 44.5 | Previous: 44.2 | ||

| 09:00 | EUR | Eurozone Services PMI Dec P | |

| Forecast: 49.0 | Previous: 48.7 | ||

| 09:30 | GBP | Manufacturing PMI Dec P | |

| Forecast: 47.5 | Previous: 47.2 | ||

| 09:30 | GBP | Services PMI Dec P | |

| Forecast: 51.0 | Previous: 50.9 | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Oct | |

| Forecast: 10.3B | Previous: 9.2B | ||

| 13:15 | CAD | Housing Starts Y/Y Nov | |

| Forecast: 260.0K | Previous: 274.7K | ||

| 13:30 | CAD | Wholesale Sales M/M Oct | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 13:30 | USD | Empire State Manufacturing Index Dec | |

| Forecast: 2 | Previous: 9.1 | ||

| 14:15 | USD | Industrial Production M/M Nov | |

| Forecast: 0.30% | Previous: -0.60% | ||

| 14:15 | USD | Capacity Utilization Nov | |

| Forecast: 79.20% | Previous: 78.90% | ||

| 14:45 | USD | Manufacturing PMI Dec P | |

| Forecast: 49.1 | Previous: 49.4 | ||

| 14:45 | USD | Services PMI Dec P | |

| Forecast: 50.5 | Previous: 50.8 | ||

The Weekly Bottom Line: The (Re)balancing Act Continues

U.S. Highlights

- The U.S. economy continued to add jobs in November, while the unemployment rate dipped, and wage growth held steady.

- The JOLTS data also showed a narrowing gap between labor demand and supply, which suggests that activity in the labor market continues to normalize and come into better balance.

- The ISM services index showed that the services sector managed to maintain a modest expansion in November. Nonetheless, the trend continues to show that services sector growth is slowing.

Canadian Highlights

- As expected, the Bank of Canada kept its policy rate at 5%, communicating a wait and see policy stance. Bond markets remained calm, with the 5-year yield moving slightly lower.

- The market has priced in rate cuts for next year, but the Bank looks for signs of broad deceleration across several inflation components before it starts cutting rates. Taming inflation will also help re-anchor consumers’ perception about inflation.

- This week’s trade data pointed to moderating domestic demand as imports fell. Meanwhile. exports edged higher, resulting in a trade surplus in October.

U.S. – The (Re)balancing Act Continues

The major focus on the U.S. economic data calendar this week was the labor market, with the two main reports showing labor demand and supply are gradually coming back into better balance. The service sector also continued to expand while U.S Treasury yields continued to push further below their mid-October highs.

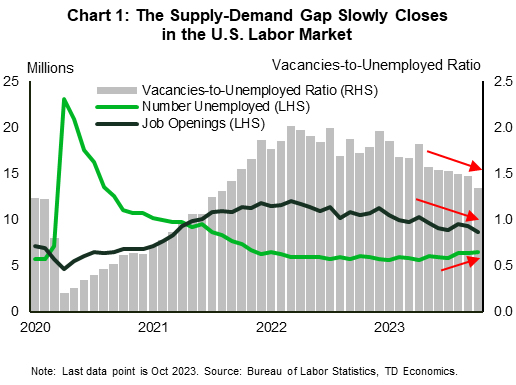

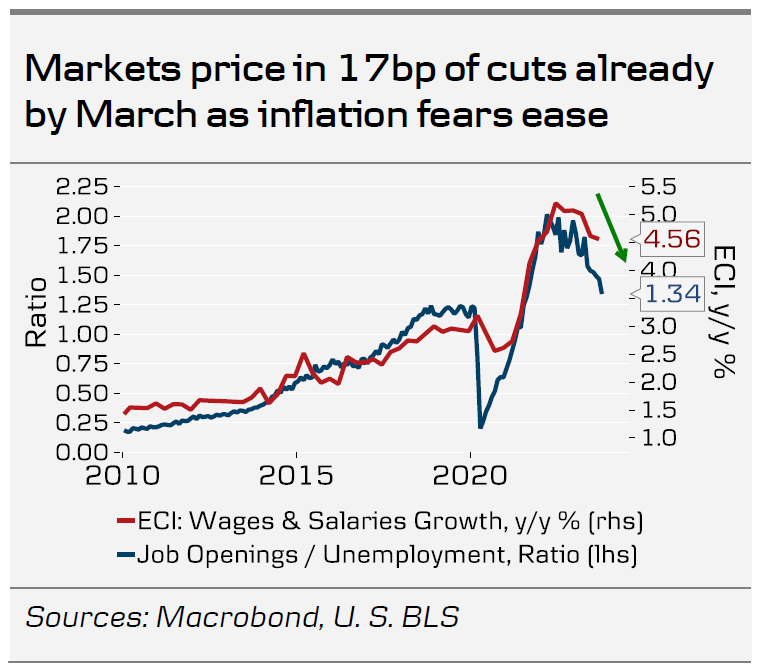

First up, the more backward-looking JOLTS data showed that the number of job openings in October fell by more than expected and slipped to the lowest level since March 2021. Although still higher than before the pandemic, at 8.7 million, openings are down notably from a record high of 12 million in March 2022. To be sure, there were still plenty of jobs available relative to the more than 6.5 million unemployed job seekers in October. However, the gap has narrowed with the vacancies-to-unemployed ratio falling to 1.34 from 1.47 in September — its lowest reading since August 2021. Other elements of the report also supported a softening labor market narrative – lay-offs held steady at 1.6 million and the quit rate remained unchanged at 2.3% for the fourth consecutive month (in-line with where it was immediately prior to the pandemic). Further evidence of labor demand cooling has been seen in continuing jobless claims, which have ticked higher over the past month, suggesting workers are finding it a bit harder to find a new job.

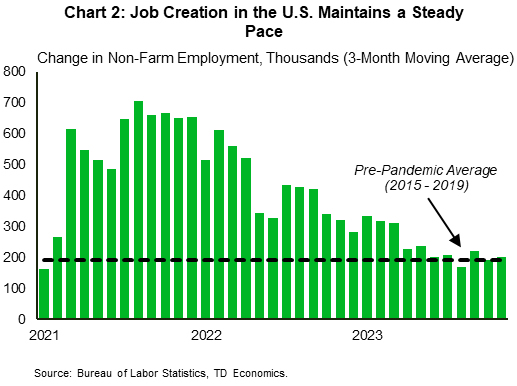

The signal from the more recent November payrolls report was generally in line with the JOLTS data. The economy added 199k jobs in November, largely in line with its pre-pandemic average and up from 150k the previous month (Chart 2). The unemployment rate dipped to 3.7% as the labor force participation rate edged higher. Annual wage growth held constant at 4.0%, down from the highs seen last year, but still above what’s consistent with 2% inflation.

The recent cooling in the labor market alongside easing inflationary pressures has pushed term yields notably lower as market participants have pulled forward the timing of when the Fed could begin cutting rates. Since their recent peak in October, yields have retreated closer to levels seen in September. Given the resilience of the economy thus far however, a further easing in financial conditions could provide a stimulus to demand that could reignite price pressures and prompt further Fed action contrary to market expectations.

On the production side, the services sector of the economy managed to eke out a continued expansion with the ISM services index rising modestly to 52.7 in November. The lackluster growth suggests that activity in the sector is slowing down, which could help to keep a lid on service sector inflation and help wage inflation continue to cool.

The resilient labor market that supported an unexpectedly strong U.S. economy this year is showing signs of cooling. The latest signs that it is coming back into greater balance will be welcomed at the Fed, which will be meeting next week for their final policy decision of the year. When Fed Chair Powell noted that the central bank can “let the data reveal the appropriate path”, this week’s data points to a steady course. All eyes will be on next week’s CPI release to see if it corroborates that plan of action.

Canada – Steady Hand on the Tiller

The Bank of Canada made it easy for the market this week by keeping its policy rate at 5%. On the communication front, the bank's comments that "the slowdown in the economy is reducing inflationary pressures" were balanced by concerns about upside risks to the inflation outlook and that they "remain prepared to raise the policy rate further if needed". There was no major post-announcement reaction in the bond market as the 5-year yield continued easing throughout the week.

Said plainly, the Bank is in wait and see mode. With consumer spending fading and business hiring softening in recent months, policymakers and financial markets are transferring their attention from the direction of the next rate adjustment (rate cuts are priced in next year) to its timing. Before this happens, inflation must come down closer to the target of 2% and so far, the central bank's preferred measures of inflation remain above 3%. While this is much lower than the 5% peak last year, progress since the middle of 2023 has been more limited, and the Bank is concerned that inflation becomes entrenched above 3%.

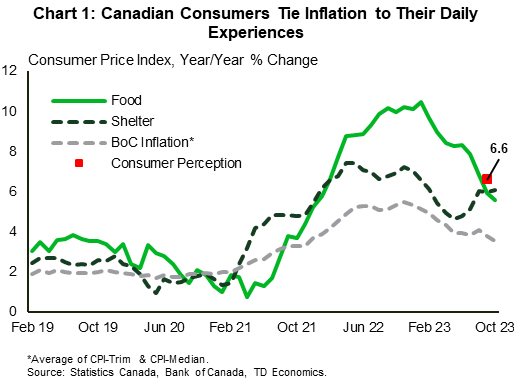

The Bank is also likely a bit concerned about inflation expectations becoming anchored at a higher level, as this would hurt its credibility. The evidence from the most recent Canadian Survey of Consumer Expectations suggest that people overestimate inflation as they tie it to experiences that are part of their everyday lives, such as food and shelter. As a result, consumers perceive inflation to be three percentage points higher than official estimates (Chart 1).

Paradoxically, consumers' responses from the recent survey (conducted when interest rates reached their highest level) suggest that some focus on the fact that monetary policy, contributes to inflation in some ways. This is partly due to the impact of rising interest rates on household mortgage payments. Indeed, our recent report highlights that those who have reset their mortgages in 2023 have reduced their spending the most, while those who haven't seen the impact of higher rates yet also pulled back on spending over the last year in anticipation of higher costs.

This week's trade data also pointed to moderating demand. Canada's merchandise imports fell in October both in nominal and volumes terms. While a portion of the decline is driven by supply constraints (such as strikes of auto workers in the U.S.), most of the slow-down is driven by a pullback in domestic consumer discretionary purchases and slow-down in manufacturing activity. Meanwhile, exports edged up 0.1% driven by large increase in aircraft and other transportation equipment. The resulting surplus sets trade up to boost growth in the final quarter of the year (Chart 2).

All said, the Bank is likely to remain in wait and see mode for some time, as it keeps a close eye on the economic data. Next week we'll take the temperature of the housing market with the latest readings on housing starts and existing home sales. In addition, we'll find out whether households' wealth continued rising through the third quarter of the year.

Weekly Economic & Financial Commentary: Global Central Banks Holding Steady

Summary

United States: The Machine of a Dream

- Nonfarm payrolls increased 199K in November, and the unemployment rate fell 0.2 percentage points to 3.7%. The decline in the already historically low unemployment rate suggests that while the labor market is cooling, it remains exceptionally tight.

- Next week: Consumer Price Index (Tue.), Retail Sales (Thu.), Industrial Production (Fri.)

International: Global Central Banks Holding Steady

- This week saw monetary policy announcements from Australia and Canada that held policy steady, although their accompanying statements were perhaps less hawkish than expected. The Reserve Bank of India also held its repo rate at 6.50% but, given strong growth and upside inflation risks, said it would remain focused on the withdrawal of policy accommodation.

- Next week: Bank of England Policy Rate (Thu.), European Central Bank Deposit Rate (Thu.), China Retail Sales & Industrial Output (Fri.)

Interest Rate Watch: At the Summit, but When to Climb Down?

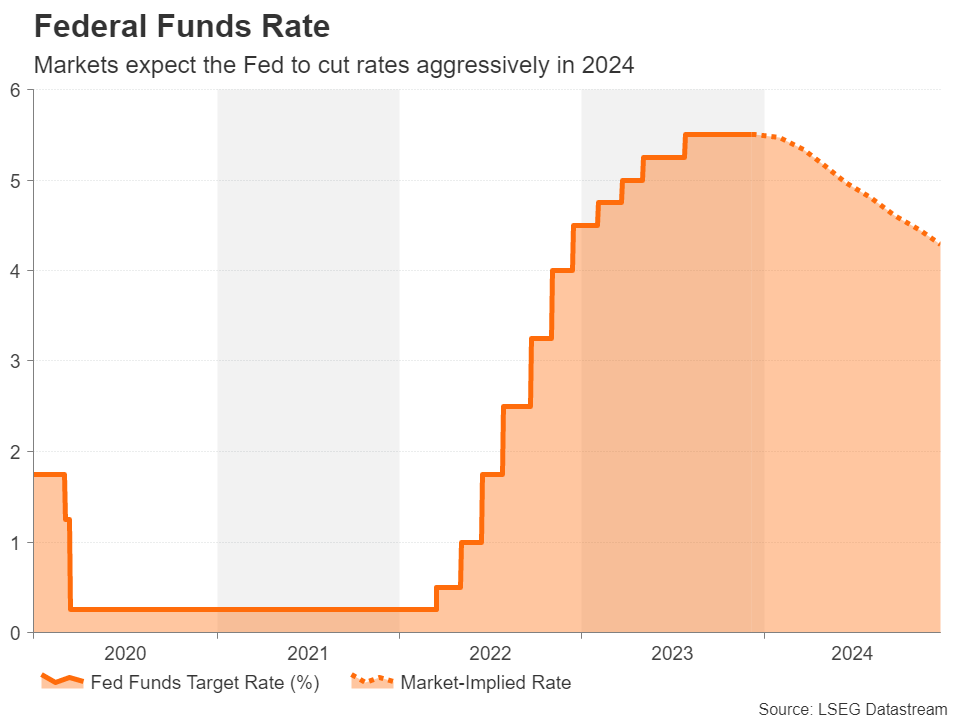

- We see the FOMC leaving the fed funds target range at its current level of 5.25-5.50% at the conclusion of its upcoming meeting on December 13. If realized, the third consecutive hold would suggest that the fed funds rate probably has reached its cycle peak. As such, the conversation will likely shift toward eventual rate cuts.

Credit Market Insights: Balancing Act: Household Balance Sheet Changes in Q3

- Yesterday, the Federal Reserve Board released Q3 data for the financial accounts of the United States. The data showed U.S. household net worth fell over $1.3 trillion on the back of a declining stock market. Net worth of the household sector now sits at roughly $151 trillion.

Topic of the Week: Oil Prices Leg Lower

- Commodity prices have been a topic of conversation for most of the last two years. Geopolitical conflicts have whipped energy and food prices around for most of the last 24 months, and while geopolitical events persist, supply and demand imbalances are creating new volatility, particularly for oil prices.

Canadian Growth Still Softening While U.S. Outperformance Stretches On

Another busy week of data releases should show further signs that the economic growth backdrop in Canada has softened. Preliminary estimates from Statistics Canada a month ago pointed to a 2.7% drop in manufacturing sales in October. Part of that decline was due to a sharp drop in petroleum prices, overall manufacturing output prices were down ~1%, suggesting sale volumes (excluding price impacts) also declined for a third straight month. The early estimate for ‘core’ (excluding petroleum) wholesale sales data, was also lower (-1.1%.) And total hours worked were unchanged in October before pulling back 0.7% in November. Retail sales edged higher after earlier declines, but early data is still pointing on balance to downside risk to Statistics Canada’s advance estimate that GDP increased 0.2% in October, and is consistent with the BoC’s assessment earlier this week (alongside a third straight hold on interest rates) that inflation pressures are easing as the economy softens.

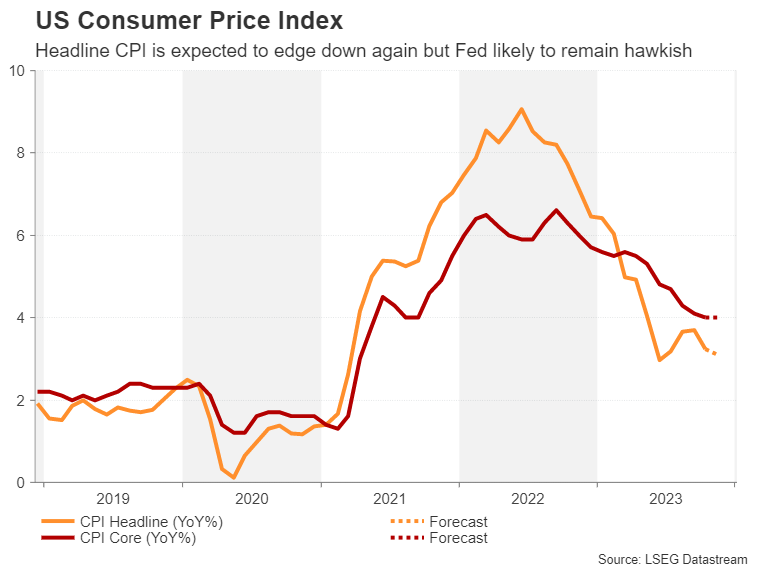

The U.S. Fed is also expected to hold interest rates unchanged for a third straight decision. The U.S. economy has been an island of resilience relative to slower growth in other advanced economies – and a drop in the unemployment rate in November retraced about half of what had been a notable 0.4 percentage point rise over the prior three months. But price growth has moderated with the November inflation data likely to indicate a continued easing of inflationary pressures. We look for the headline inflation to slow from 3.2% year-over-year in October to 3.1%, with a significant reduction in gas prices contributing to a 6% year-over-year decline in the energy CPI. Core inflation is expected to hold steady at 4% year-over-year, but with a 0.3% month-over-month increase that would leave a gradual drift down towards the Fed’s 2% inflation objective largely intact.

Week ahead data watch

U.S retail sales likely ticked down (-0.1%) again in November, the same pace as in October. Gasoline prices went lower by ~7%, lowering sales at pump down sharply. Auto sales also dipped during that month, contributing to part of the slowdown.

The Canadian real estate association (CREA) home resale and price numbers will be watched closely for further signs housing markets are slowing (again). Unit resales in Canada fell 12% from July to October and early market reports suggest activity remained quiet in November.

Bank of England Preview – We Still Favour the Topside in EUR/GBP

- We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 14 December, which is in line with current market pricing.

- Overall, we expect the MPC to stick to its previous guidance emphasising the "higher for longer" approach and pushing back on market pricing of rate cuts.

- We expect a muted reaction in EUR/GBP but see risks for EUR/GBP ending the day higher.

We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 14 December. This is in line with current market pricing. We expect the vote split to be 6-3 with Greene, Haskel and Mann once again to vote for a 25bp hike and the rest of the MPC to vote for an unchanged decision. Note, this meeting will not include updated projections nor a press conference following the release of the statement.

Overall, we expect the MPC to stick to its previous guidance and signals from individual members noting that it is too early to start discussing rate cuts and similarly that interest rates must remain in restrictive territory for sufficiently long to bring inflation sustainably back to target.

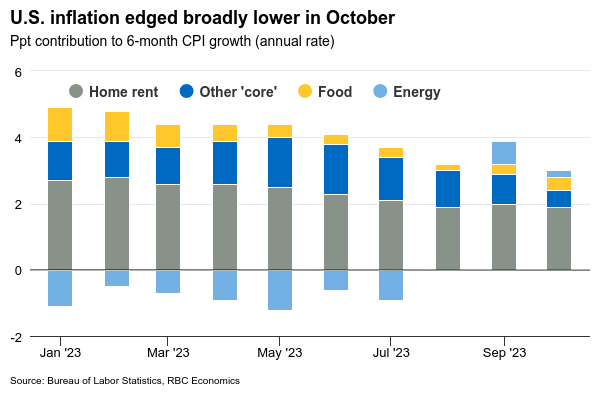

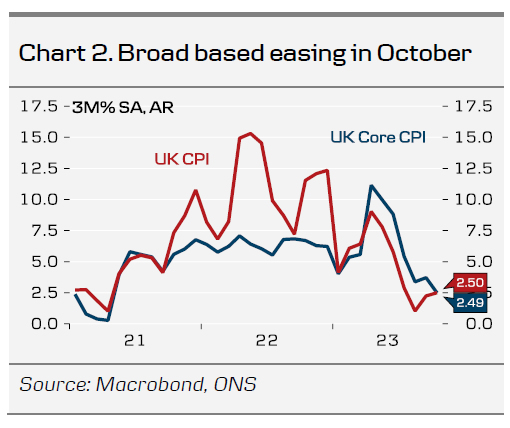

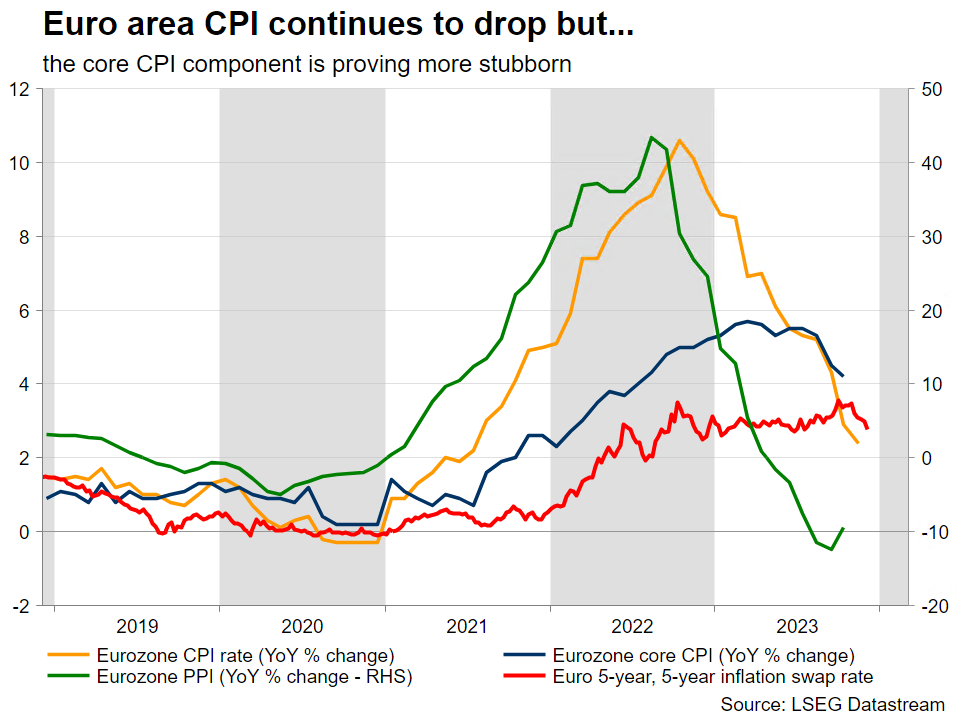

Since the last monetary policy decision in November, data releases have been mixed. As widely expected, large base effects from energy prices led to a markedly drop in headline inflation for October. Similarly, the decline was broad based and larger than expected with core at 0.2% m/m SA and headline at 0.1% m/m SA (chart 2). Service inflation remains elevated but also showed signs of easing. As previously flagged, we do not see inflation developing materially different in the UK compared to elsewhere. PMIs for November came in better than expected edging back above the 50 mark with both service and composite now in expansionary territory. In Q3 the economy flatlined with GDP at 0.0% q/q in line with the BoE's forecast but only narrowly saved by net imports. The KPMG/REC report on UK jobs delivered comforting news for the BoE with pay pressures receding for both permanent and temporary staff and signalled a broad based reduction in hiring activity. The official report by the ONS is released on Tuesday next week before the meeting but we do not expect this to lead to the majority of the MPC deviating from an "unchanged"-decision.

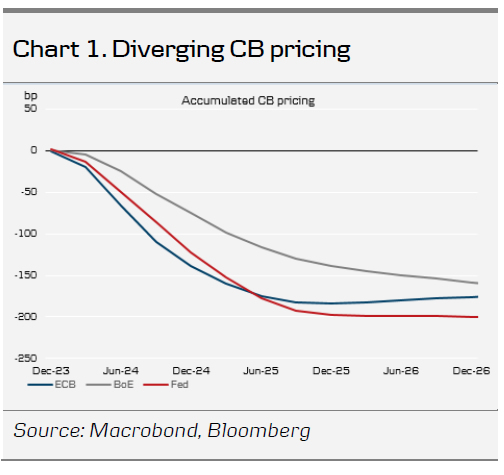

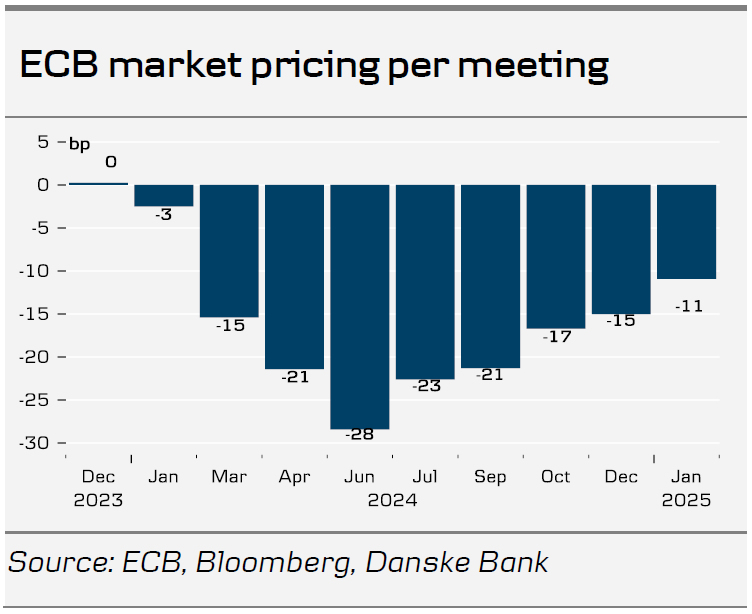

BoE call. We maintain our call that the BoE has delivered its final hike of this hiking cycle, which is in line with current market pricing. We expect the first rate cut of 25bp in June 2024 and subsequently 25bp cuts in the following quarters, totalling of 75bp of cuts for 2024. This is slightly less than current market pricing. We do not see the BoE deviating from the Fed and ECB by the extent currently priced by markets (see chart 1) and expect markets to scale back on expectations from the latter.

FX. In our base case of an unchanged decision, we expect a muted reaction in EUR/GBP. We expect the guidance to provide a hawkish tilt in an attempt to push-back on the pricing of cuts for the next year. However, combined with the expectation of a relatively hawkish ECB later in the afternoon, we expect EUR/GBP to end the day higher. Overall, we see relative rates as a negative for GBP and see the recent rebound as attractive levels to sell GBP. We continue to forecast EUR/GBP to move modestly higher the coming year to 0.89.

ECB Preview: From How High to How Long

At next week's policy meeting we expect the ECB to guide towards a more neutral policy outlook for the near term as we expect the ECB to virtually rule out the possibility of a further rate hike. That would mark the beginning of the end of the 4% policy rate level. This follows on the back of the inflation surprises on the downside in recent months. We expect the ECB to fall short of providing guidance on the timing of the first policy rate cut beyond the near future while repeating its call for a data-dependent approach. This will leave a Q2 24 rate cut as the most likely scenario for the next policy rate change.

During the Q&A part of the press conference, we expect Lagarde to acknowledge that ending the full PEPP reinvestments has been discussed. A formal decision with its technical details published is only expected at the January meeting for an immediate implementation.

While markets are pricing in a very aggressive rate cut cycle through the end of next year of 140bp, and a 70% likelihood of a rate cut in Q1, we continue to expect the ECB to deliver its first cut in June, as we see the ECB respecting the 'sequencing' of first accelerating the liquidity normalisation and subsequently discussing rate cuts. We do not share the markets' view on inflation and a growth outlook that would warrant more than five policy rate cuts next year as a main scenario.

Pushing back on the easing of financial conditions

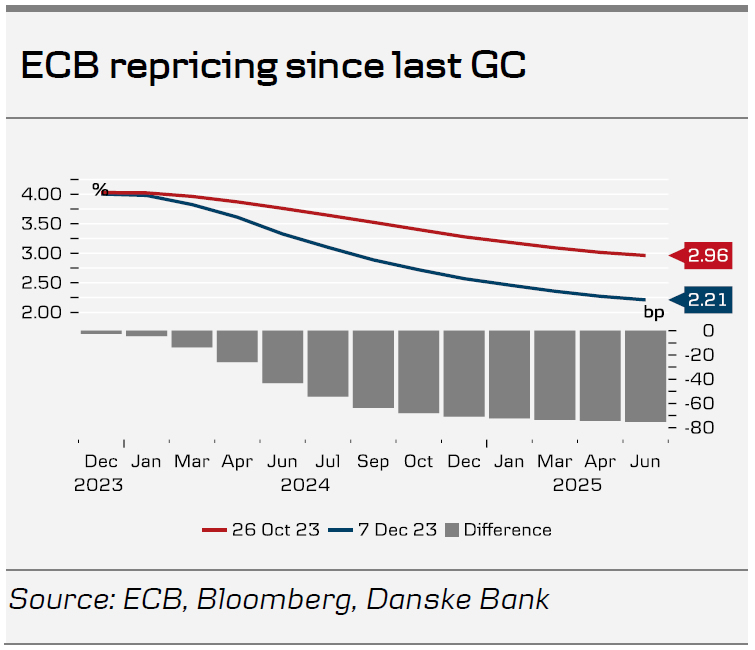

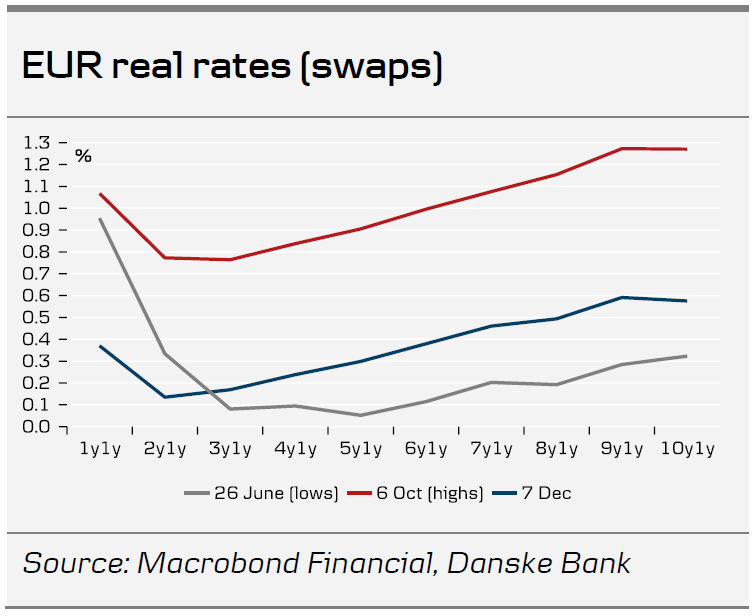

The downside surprise in recent months to inflation releases has provided ECB with an opportunity of shifting the narrative from how high the policy rates should go to how long will they stay at the current 4% level. We expect them to take advantage of this decline and say that in the absence of shocks, the final rate hike has already been delivered. Since the last governing council meeting on 26 October, markets have significantly eased financial conditions to multi-year lows on the back of a decline in rates markets with real rates in Europe approaching the year to date lows. While the inflation decline is an earlier than anticipated win to the ECB, we still view the repricing as unwanted relative to ECB's sought-after calibration of the monetary policy stance.

While several governing council members have pushed back on the rate pricing saying it is 'premature' to discuss rate cuts, it has been with limited success on the market pricing. We expect ECB to push back on the easing of financial conditions that markets have been pricing during the past month. While President Lagarde has seldom commented directly on the policy rate pricing, we expect a moderate push back on the near-term financial conditions, which she has been referring to on previous occasions. We do not think that she will repeat the guidance for no rate cuts in the next 'couple of quarters' as she said two weeks ago – which will bring Q2 next year as the most likely scenario for the first rate cut. Markets are currently pricing 140bp of rate cuts through the end of next year.

The November inflation print gave the ECB an early Christmas present

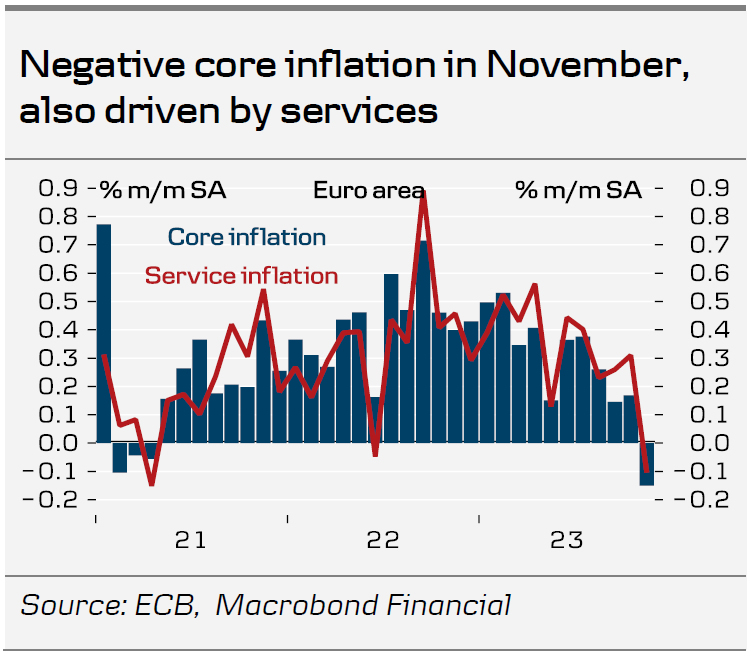

The November inflation print came in somewhat below expectations at 2.4% (compared to consensus of 2.7%) and is the third consecutive inflation surprise on the downside and thus it seems like Christmas came early for the ECB. Most recently, the decline in the inflation November report was broad-based where headline inflation even declined 0.5% m/m. Core inflation ticked down to 3.6% y/y from 4.2% y/y in October. Also remarkably, the monthly change in seasonally adjusted core inflation was negative at -0.2 driven by both negative goods and service price inflation. We expect Lagarde to sound more optimistic on the inflation outlook while at the same time remain cautious about making over hasty decisions.

Economic activity stagnating

Closely approaching year-end, economic activity in the euro area is stagnating after a strong recovery in 2021 and 2022 following the pandemic. Real GDP contracted marginally in Q3 on a quarterly basis, which left the yearly growth rate close to 0%, reflecting how the ECB's restrictive monetary policy is working its way through the economy. That said, private consumption is the key growth sector of the euro area economy. Since the October ECB meeting, we have received the November PMIs that remained in contractionary territory but also sparked some hopes by improving more than expected to 48.7 and 44.2 in the service sector and manufacturing sector, respectively. Given the significant monetary tightening and uncertainty in the economy it is encouraging for the ECB that activity is not declining faster, which supports the 'soft-landing' case. Yet, the downside risk for the growth outlook is still that we suddenly see a more rapid transmission of monetary policy and tightening of financial conditions or a spike in energy prices and geopolitical uncertainty, see A year of transition ahead , 7 December.

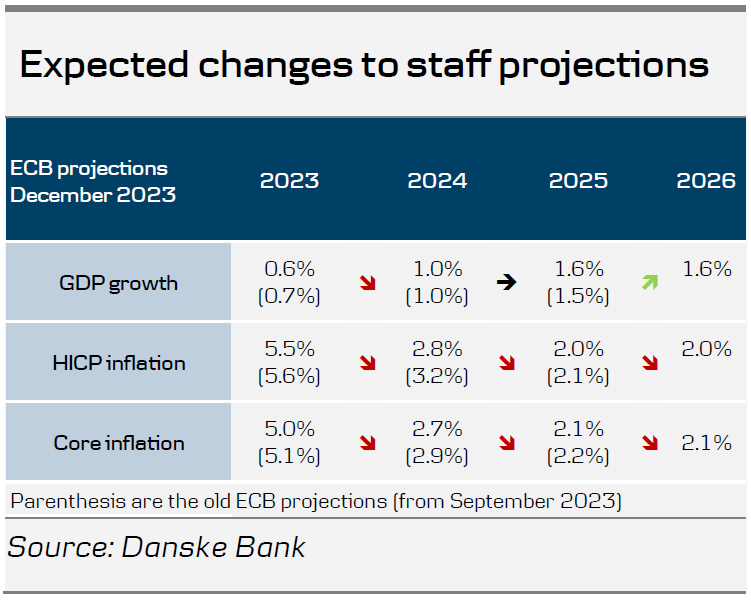

The new staff projection will likely lower the inflation outlook

We will closely watch the ECB staff projections on the back of the recent larger than expected declines in inflation. Both headline and core inflation have printed significantly lower in Q4 23 compared to the September ECB projections. We expect a rebound in HICP in December to 3.0% y/y, which will take the Q4 average to 2.8%. This will be 0.5 percentage points lower than the latest staff projections. This larger under hang as well as lower commodity futures will result in lower inflation projections next year.

Futures point to a downward revision of the technical assumptions on oil and gas prices in 2024 by 5% and 25%, respectively, and 7% and 20%, respectively, in 2025. These revisions will probably also imply that inflation projections get revised down to or below the 2% target in both 2025 and 2026, which will allow the ECB to start thinking about rate cuts.

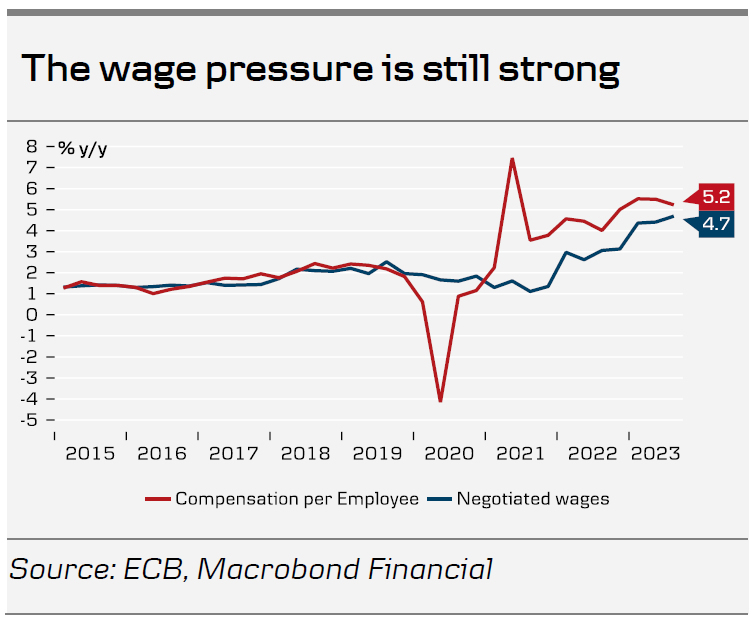

However, we expect the ECB to argue that it is premature to talk about rate cuts as upside risks persist for the inflation outlook, but the communication can be less aggressive than previously. The labour market is historically strong, and companies are reporting labour shortages amid strong wage growth with negotiated wages increases of 4.7% in Q3 and compensation per employee at 5.2%. The strong labour market and increasing real wages will support growth in the coming years. This fact combined with the weaker than projected Q3 GDP print will likely mean that the growth projections do not change significantly.

First step to end the full PEPP reinvestments

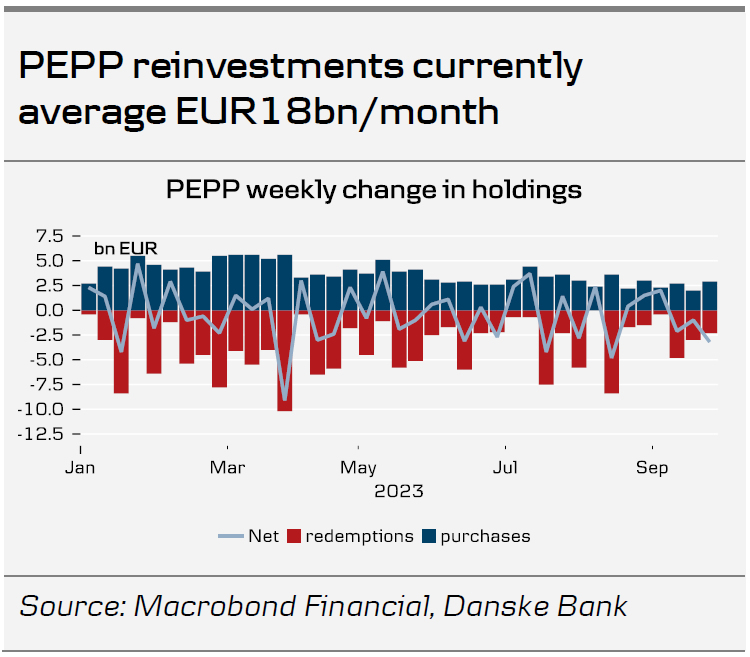

Last week, President Lagarde during a European Parliament hearing said with reference to the ongoing PEPP reinvestments currently guided to run at least until end of 2024, that 'this is a matter which will come probably for discussion and consideration ... in the not too distant future and we will re-examine possibly this proposal'. Given the benign market environment we firmly believe that this will be discussed next week – something that Lagarde will likely acknowledge during the Q&A session. A formal announcement will only follow in January. This will complement the already ongoing balance sheet normalisation from APP. Importantly, we do not expect the ECB to step back from reinvesting PEPP bonds in one take, but take a smoothening approach via a gradual phasing out of PEPP reinvestments. We see the PEPP reinvestments average EUR18bn per month through the past 12 month and we assume a similar redemption pattern is foreseen next year. Once the end to PEPP reinvestments is announced we assume it will be of immediate implementation, and hence no later than 1 April, with our baseline being for 1 March. We expect the first 12m of PEPP holding reduction will be to the tune of EUR150bn altogether. We expect that an announcement in January of the end to full PEPP reinvestments will be a compromise with the doves on the policy outlook.

Pushback on significant ECB repricing could support EUR/USD

We anticipate a relatively muted reaction in the FX markets, as both the ECB meeting and the FOMC meeting the day before are unlikely to bring any major surprises. If anything, there could be a slight pushback on the aggressive repricing of the ECB over the past couple of weeks, i.e., a relatively hawkish ECB underscoring that it is premature to talk about rate cuts. This, in turn, could support our near-term view of a higher EUR/USD. Regarding our strategic case, we maintain our belief that EUR/USD will move lower, based on relative terms of trade, real interest rates, and relative unit labour costs. Our projection for the cross is at 1.06/1.04 over the next 6-12 months. However, in the near-term, we still see potential for a higher EUR/USD. We expect weaker US data, positive risk appetite, and an unwinding of the aggressive ECB cuts that were priced for next year to support the cross in the short term.

Fed Preview: Low-Key Optimism

Fed Preview: Low-Key Optimism

- We do not anticipate the Fed to make changes to its monetary policy in the December meeting, in line with broad consensus and market expectations.

- Focus will be on the updated economic projections, where the 2024 'dot' could be revised slightly lower, yet still above market pricing. Growth forecasts could be lifted slightly, while inflation projections are likely to remain mostly unchanged.

- We stick to our long-standing view that the Fed will initiate quarterly 25bp rate cuts from March. Current pricing signals limited downside potential for longerdated UST yields, but still rhymes with lower EUR/USD in 2024.

The recent FOMC commentators have made one thing clear ahead of the December meeting: now is the time to be patient. Markets have priced out any chance for a further hike and now expect the first cut in either March or May. And we would agree, as we still expect the first cut in March, followed by quarterly 25bp reductions through 2024-2025. First cut 9 months after the final hike would be well in line with historical standards.

In his final speech ahead of the blackout, Powell made little effort to guide the markets for next year. While few FOMC participants have openly discussed the case for rate cuts so far, there has been surprisingly little pushback to the sharp easing in financial conditions.

And for a good reason. Lower inflation expectations have pushed real rates to undoubtedly restrictive levels, while rising labour supply, cooling demand and higher productivity all support the case for easing underlying price pressures. Oil prices continue to fall despite the OPEC+'s supply cuts, suggesting that markets are now pricing in clearly cooling aggregate demand. It is still too early to celebrate victory over inflation, but between the lines the Fed appears to share markets' optimism for now.

To be clear, we continue see some risks of persistent inflation over the long run, stemming from relatively tight labour, energy and housing markets. But as inflation looks to settle closer to 2-3% in 2024-2025, the nominal policy rate will have to be adjusted lower. If our forecasts of quarterly rate cuts and gradually cooling inflation hit the spot, the real policy rate would average 2.6% in 2024, which is still a clearly restrictive level in our view.

This is also what the markets are pricing in, as real short rates are seen stabilizing at 1.0- 1.5% over the next decade. In other words, the current rate cut pricing reflects expectation of cooling inflation and not a looming recession.

As all recent FOMC commentators aside from Michelle Bowman have suggested that they do not anticipate further hikes in their baseline view, the 2024 'dot' could shift lower by 25bp (to 4.75-5.00%). 2023 and 2024 GDP forecasts will likely be adjusted slightly higher on stronger realized data, while inflation forecasts are likely to remain mostly untouched.

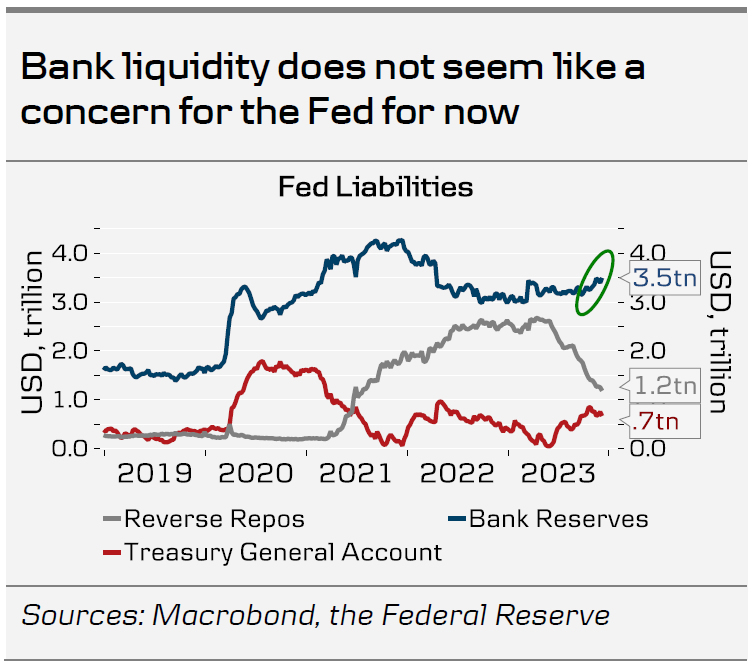

We will also watch out for any questions on the recent spike in SOFR and whether Powell sees it as a concern for the Fed. From liquidity perspective, we still doubt this is the case, as the drawdown of the ON RRP has meant that US bank reserves currently remain at a higher level than at the start of the year despite the ongoing QT.

Markets: December meeting unlikely to rock the boat

We expect a muted reaction in bond markets to the FOMC bringing the dots better in line with recent development. Nevertheless, the rapid repricing of policy expectations the past weeks has left bond yields sensitive to any signs of deviations from the current disinflation narrative for 2024. The bar for the FOMC to markedly affect market pricing seems high, as long as data continues being in favour of an early start to rate cuts.

As such, we do not foresee substantial influence on EUR/USD either. Our projection for the cross remains modestly lower at 1.06/1.04 over the next 6/12M horizon.

Weekly Focus – Central Bank Bonanza

Yield curves flattened further this week as longer dated yields traded lower on the back of softer US labour market data and not least ECB's Schnabel's interview with Reuters where she passed on the opportunity to oppose the recent aggressive market pricing of the ECB. In line with this, the euro has continued to weaken. The big winner on FX markets has been the yen, which benefits on several fronts from a lower global yield environment, a marked decline in oil prices and speculation of imminent normalisation of Bank of Japan policies.

This week, we published our view on the large global economies and the Nordics. It looks like we can get inflation down with only a modest increase in unemployment in the US, the euro area and the Nordic countries. The scene is set for rate cuts during 2024 and 2025, as central banks can gradually release the pressure. However, uncertainty is very high, and there is big risk of both deeper crisis and re-emerging inflation over the coming years.

Data out of the euro area has on balance been uplifting and confirmed that the economy is not falling out of the bed. Retail sales climbed slightly higher in October and final November PMIs adjusted the flash numbers a good bit higher leaving the picture of a modest cooling of the service sector and a weakening manufacturing sector which has at least stopped accelerating further into recession. Manufacturing weakness continues to reflect in German factory orders, though. A few 2020 COVID lockdown months aside, they now stand at the lowest level in over ten years.

US data continues to support our expectation of a soft landing economy. The ratio of job openings to unemployed workers dropped to the lowest level in over two years and as involuntary layoffs tick higher from low levels, the labour market continues to cool off. At the same time, ISM data indicates modest growth in the service sector with the activity index increasing from 51.8 to 52.7.

Next week will be a busy one. We expect both ECB, SNB and the Fed to be on hold. ECB looks set to guide a more neutral policy outlook for the near term as we expect them to virtually rule out the possibility of a further rate hike. At the FOMC meeting, focus will be on the updated macro and rate projections, and especially if the 'dots' already signal a higher chance of rate cuts for next year. With labour markets cooling and broad-based easing in inflation we also expect the BoE to stay on hold.

On the data front, US CPI data will be key to markets and we forecast another month with modest price pressures and core CPI growth at 0.2% m/m. In the euro area, we look out for December PMIs and expect continued modest contraction in the service sector while the downward trend in manufacturing becomes gradually less steep. We also get the quarterly Tankan survey in Japan, which will hold key information about activity and inflation pressures ahead of the Bank of Japan meeting later this month. In China, another deflation print will likely draw headlines, however retail sales will be more important, as consumers are key to keep the economy afloat.

FX Year Ahead 2024: As the Race to Cut Begins, Which Currency Will Come Out the Winner?

- Will Fed officials be the first to cut rates or will the ECB beat them to it?

- Falling inflation everywhere means a bearish US dollar is not a given

- Yen stands to gain from rate cuts as BoJ may hike

- Is sterling set for another bumpy year?

- Aussie and kiwi pin hopes on China recovery, loonie looks to oil boost

Will the dollar bears finally get their way in 2024?

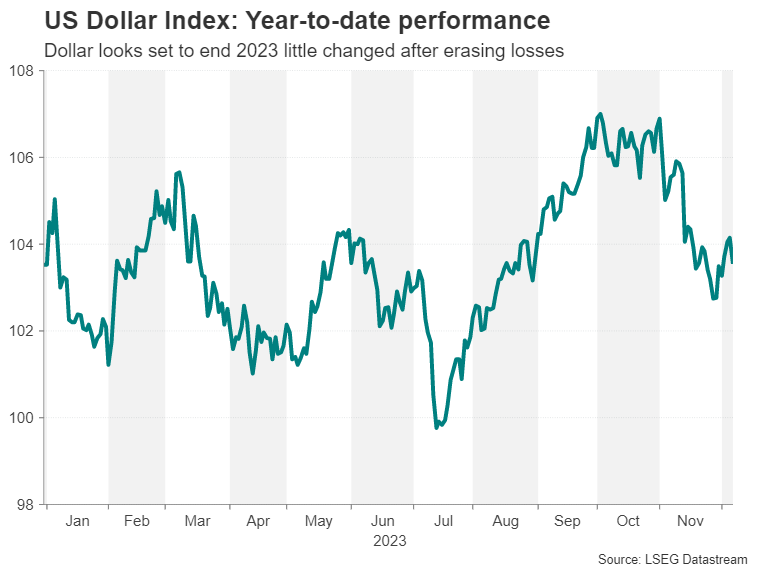

After two consecutive years of gains, a correction in the mighty US dollar was well overdue in 2023. The greenback started the year being taunted by the persistent expectations of a dovish pivot by the Federal Reserve. But those bearish forecasts have not fully materialized as the dollar is on track to finish the year virtually unchanged. Even now, when there is a high probability that a Fed rate cut is just months away, plotting a downwards path may not be very straightforward for the bears.

Looking back on 2023, the big story was of course inflation. The good news is that the high inflation problem will probably start to feel like a thing of the past over the next few months. The bad news is that what replaces it might be a recession.

But first, let’s focus on how much progress the Fed has made as inflation in the United States is likely entering the final leg of its journey to 2%. But we’re not there yet and the Fed isn’t ready to take its finger off the hike button as there are still some upside risks to inflation, mainly from strong consumption and the tight labour market.

The question is, will concerns about a slowing economy spur consumers to make drastic cuts to their expenditure? Aside from high borrowing costs starting to bite for households, there are the added dangers of Congress cutting back on spending in 2024 or businesses downsizing staff. The labour market has cooled notably in recent months, with jobs growth slowing and the unemployment rate edging up slightly.

There is nothing on the near-term horizon to suggest that big job cuts are on the way or that consumer confidence is falling off a cliff, so the base case scenario is that the economy is headed for a soft landing. However, there is some disconnect between the soft landing expectations and the market pricing for hefty rate cuts.

Investors are ending 2023 in jubilant form, betting that the Fed will slash rates by at least 100 basis points by December 2024. But those bets appear to be built on the expectation that inflation will continue to fall sharply rather than the economy stumbling.

But if a recession is avoided and there isn’t a substantial rise in unemployment, how far will the Fed be able to cut interest rates without rekindling inflationary pressures? This might explain why the greenback’s longer-term slide came to a halt during the summer.

That’s not to say, though, that the dollar downtrend has run its course. After all, the Fed has yet to formally signal a dovish pivot. When that happens, possibly in early spring, the dollar will likely come under renewed selling pressure.

The trouble for the bearish view here is that other central banks such as the European Central Bank may also start cutting rates roundabout the same time. The US presidential election in November 2024 is another consideration as the dollar tends to rally post the election and this would especially be true if former President Donald Trump were to get re-elected.

In the more negative scenario, we should not ignore the possibility that the Fed may have already overtightened and a recession cannot be averted.

Summing up, the dollar’s descent may accelerate in the first half of 2024 if the inflation and jobs data keep favouring looser monetary policy. However, the outlook is less certain in the second half, as there’s the risk that either the Fed disappoints those expecting larger rate cuts or the economy takes a turn for the worse, prompting a much bigger dovish tilt.

Another tough year expected for the euro

Despite strong inflationary pressures, weak growth momentum and continuously negative news flow, the euro managed to marginally outperform the US dollar in 2023. This euro outperformance has been the theme in most crosses apart from a few exceptions, most notably euro-pound.

Heading into 2024, European Central Bank policy will remain in the spotlight. The market is expecting almost 140bps of rate cuts with the first 25bps move comfortably fully priced in by April 2024. For this scenario to materialize, there must be a high probability for a recession while the ECB’s own 2024 inflation forecasts should be revised lower as well.

Interestingly, investors are pricing a similar policy outlook for the Fed despite the obviously much stronger US economy. Therefore, a much more aggressive easing strategy by the ECB would most likely weigh on the euro with parity possibly being touted by certain market participants as a viable target. In this context, risk reversals remain somewhat bearish on euro-US dollar for 2024.

The main risk for 2024 lies with a much stronger euro area economy. This looks difficult to foresee at this juncture considering the weak forward-looking growth indicators and the relative tightening of lending standards. However, such an outcome would allow the ECB to keep its policy rates on hold for a longer period than currently envisaged, eventually forcing the market to push out its rate-cut expectations.

To a certain extent, the euro area’s growth outlook depends heavily on China’s efforts to significantly restart its economy. In addition, there are various wildcards for 2024 that could unsettle the global economy and the market. For example, an escalation in the Ukraine and the Middle East conflicts that could affect commodity prices and overall economic sentiment, pushing central banks globally to return to a more accommodative policy stance.

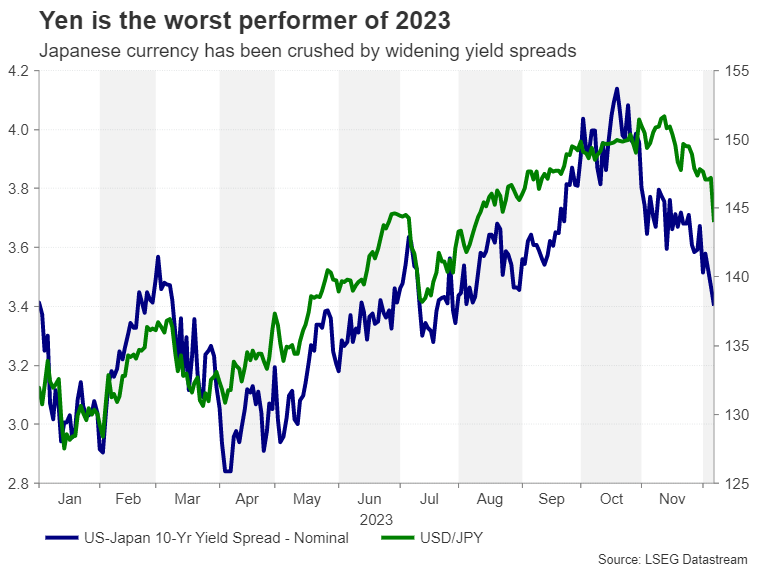

Yen might have a better time in 2024

The Japanese yen looks set to end 2023 as the worst performing major currency. In a year when all the other big central banks kept raising interest rates, the Bank of Japan patiently searched in vain for clues that wage growth is picking up.

But after a short-lived bounce, pay increases sputtered again. There is hope that the next round of the spring wage negotiations will lead to a more sustained acceleration in earnings. The BoJ even upped its inflation forecasts for the next three fiscal years, setting the stage for a possible exit from negative interest rates.

Markets think a BoJ liftoff will come not long after the spring wage negotiations and have priced in a 10-bps increase in the policy rate by April 2024. The inflation data alone has been encouraging, with both headline and core CPI holding above the BoJ’s 2% target.

Yet, the yen has remained extremely pressured, hitting multi-year lows. A couple of tweaks by the BoJ to its yield curve control policy have brought little relief to the Japanese currency. Widening the yield target band would normally be a game-changer for the yen. But when yields have rallied much more in America and Europe, the BoJ’s modest tightening hasn’t had the desired effect.

The question for the yen in 2024 is whether the BoJ will allow the 10-year yield to rise above the current target of 1.0%. If policymakers maintain a tight grip on the yield curve, a surprise early rate hike might provide only a limited boost for the yen.

However, even then, the yen could enjoy a change in its fortunes by the middle of 2024 if not sooner when the Fed, ECB and others begin to cut rates just as the BoJ is unwinding its stimulus policies.

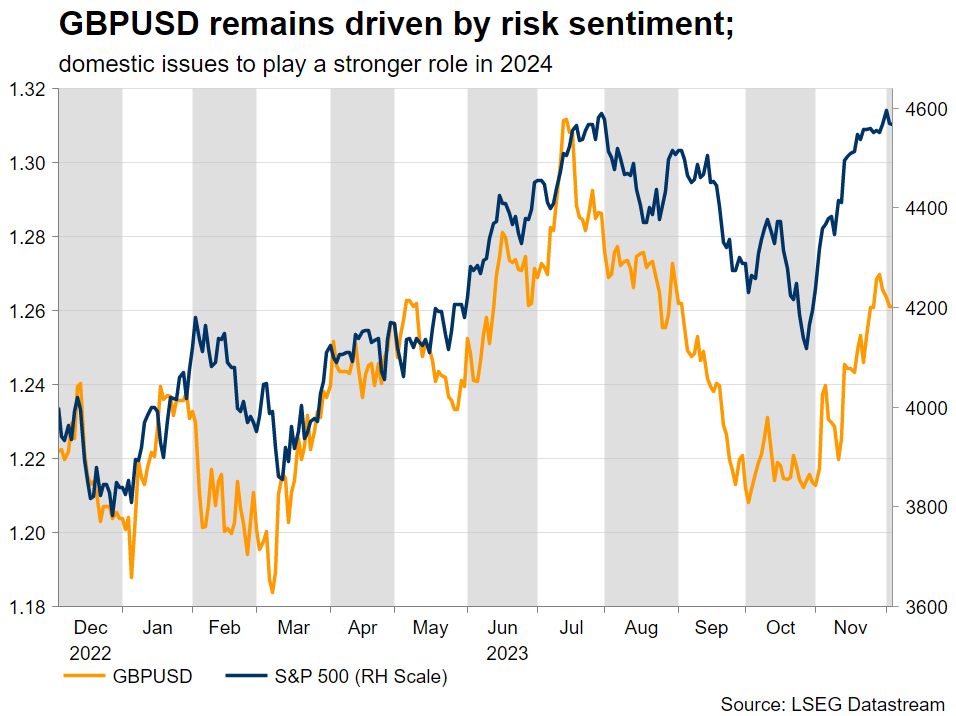

Volatile year on the cards for sterling

Twenty twenty-three has been an odd year for the British pound as, despite the laggard Bank of England and sky-high inflation hampering growth, it managed to outperform its main trading partners.

Next year could be a crucial one for the UK economy as a general election will take place, potentially after the summer break. Elections tend to create nervousness, particularly as the market has developed a love-hate relationship with the opposition Labour party, which is currently ahead in the polls. This increases the possibility for a pound-negative reaction as we get closer to the actual election date.

Additionally, the situation on the ground remains difficult as inflation remains elevated and other sectors like housing that traditionally support UK household wealth are under strong downside pressure. However, the market is more relaxed about the Bank of England’s actions, expecting only 80bps of rate cuts in 2024, with the first 25-bps rate move seen in August.

Should data releases take a turn for the worse, the market could quickly price in an even more aggressive easing path for the BoE. Under this scenario, and with elections lingering in market participants’ minds, we could see the pound underperforming significantly during the latter part of 2024.

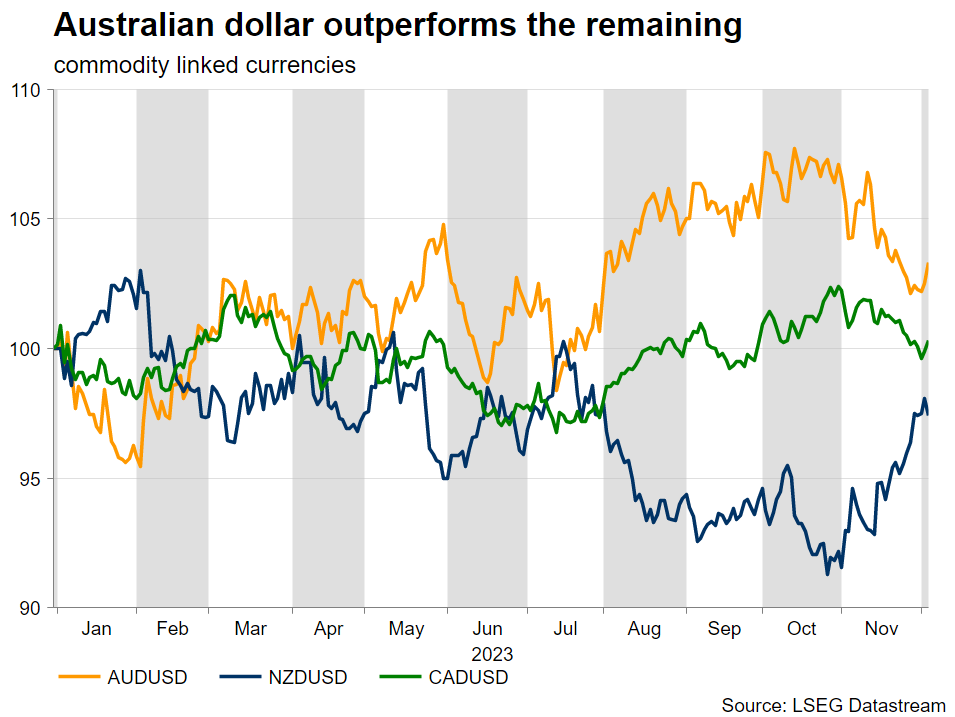

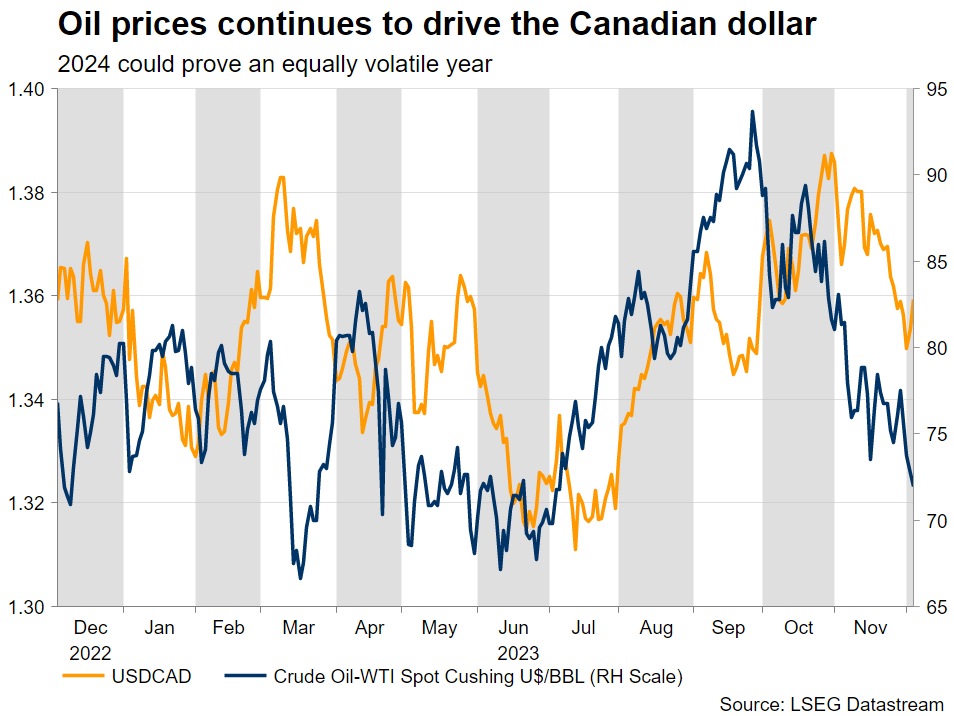

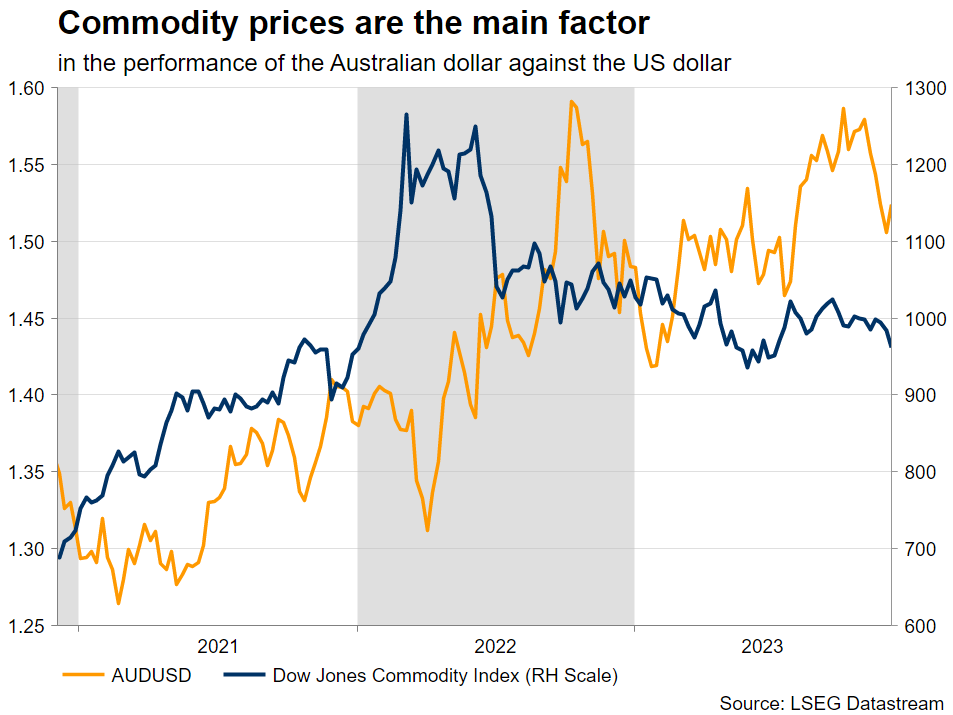

Aussie, kiwi, loonie: China and commodity prices will determine their fate

It has been a difficult year for the commodity-linked dollars due to the lower commodity prices, the constant hawkish drive by their respective central banks and the continued weak growth patch experienced by China. In this environment, the Australian dollar managed to outperform the US dollar, overshadowing the weak performance of the New Zealand dollar.

Twenty twenty-four could prove equally tough for the commodity-linked dollars as they are predominantly pro-risk currencies.

Starting with the Canadian dollar, the Bank of Canada was among the first central banks to pause their tightening cycle. The BoC has remained on the sidelines since July, removing one of the key tailwinds for the loonie, which subsequently has been very volatile.

With the Canadian economy closely linked to both the US economy and oil prices, 2024 is expected to be tough. The BoC has inflation finishing 2024 close to 3%, thus keeping the door open for further rate hikes. But the market is convinced that the first 25bps rate cut will be announced by April with more than 100bps easing pencilled in for 2024.

With OPEC+ trying to keep oil prices from falling further, there is a possibility of another crude oil rally. Such an outcome would cause a new inflation surge globally, boosting the loonie and potentially delaying any rate cuts by the BoC.

Moving down under and the 2024 performance of both the aussie and kiwi mostly depends on China. The various support measures announced by the Chinese administration are welcomed by the market but there is pessimism about their success. If these measures prove effective, then the entire region will enjoy the benefits, starting with commodity-rich Australia.

The Reserve Bank of Australia was the last one to announce a rate hike in November and has maintained its hawkish stance. The market has taken notice of this shift, and it is currently pricing in only 30bps of rate cuts in 2024.

The sluggish domestic economy remains a concern. But should consumer sentiment improve on the back of solid wage increases and China surprises with its growth record, the RBA could stay hawkish, potentially being the last one to cut rates. In this scenario, the aussie stands to benefit, especially against the US dollar.

Similar to the RBA, the Reserve Bank of New Zealand is expected to cut rates by only 40bps during 2024. This is explained by the hawkishness shown by the RBNZ during 2023, due to strong inflationary pressures domestically. Its latest OCR projections point to another rate hike in 2024 with inflation dropping eventually a tad below the 3% threshold.

However, rate hike expectations could intensify further if China’s recovery gathers steam and/or the US achieves a soft landing. In this case, the RBNZ could be the first one to pull the trigger with another rate hike and thus offer strong support to the kiwi.

Week Ahead – Will the Central Bank Bonanza Kill the Festive Joy or Fuel It?

- Fed, ECB, BoE and SNB hold their final policy decisions of the year

- Will they push back on rate cut expectations?

- US CPI and flash PMIs will be crucial too

- UK GDP, Aussie jobs also on the agenda

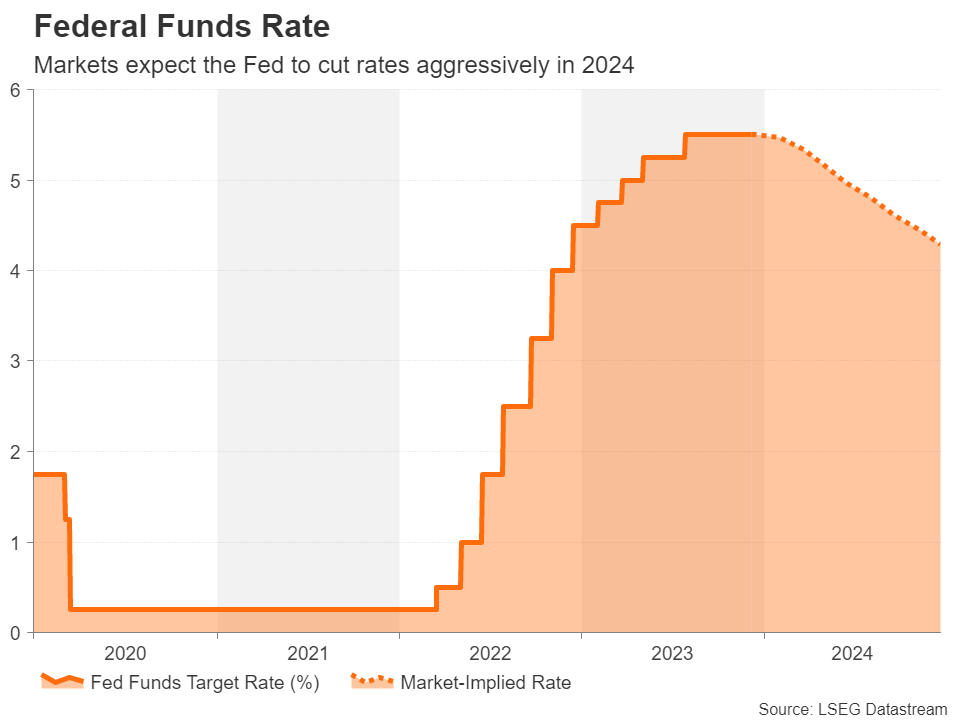

Fed to hold rates but will it signal big cuts?

The Federal Reserve is almost certain to keep its policy rate unchanged on Wednesday as the US economy finally appears to be losing some steam and inflation is coming under control. Chair Powell has set the bar high for raising rates again, while investors have gone a step further and completely priced out any chance of additional tightening.

The focus therefore on Wednesday will be how soon the Fed will start lowering rates, specifically how many rate cuts do FOMC members foresee in the updated dot plot that’s due the same day. In the last dot plot, policymakers were projecting that rates would end 2024 at 5.1%.

Following the recent soft readings on inflation, markets are betting that the Fed will cut rates five times in 2024, with a 25-bps reduction fully priced in for May. If policymakers push back against such expectations and predict fewer cuts, the US dollar could gain on the back of the hawkish signals.

The most bullish scenario for the dollar is if the Fed doesn’t even adjust its median projection for 2024.

Still, a hawkish rate path will likely not be enough to set the markets straight and Powell will have a tough task on his hands convincing investors that rate cuts are not on the near-term horizon, especially if the inflation data keeps surprising to the downside.

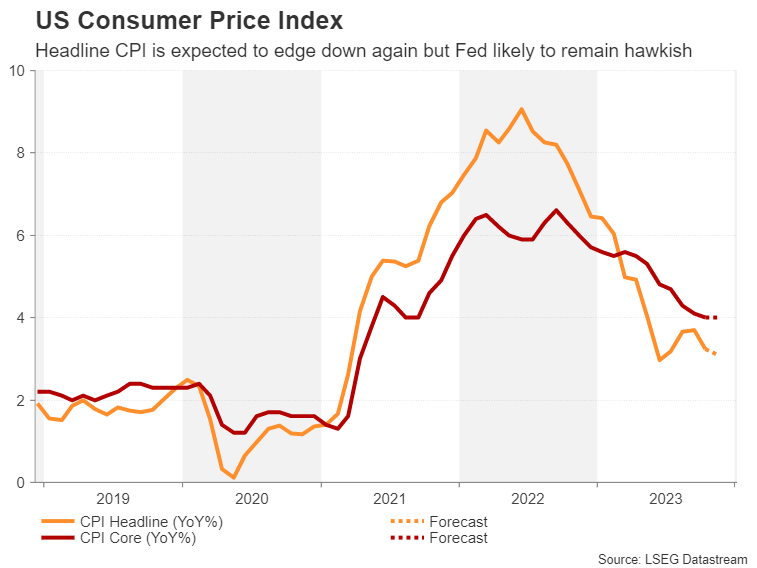

The CPI report for November is due on Tuesday and the forecast is for the annual rate of headline CPI to have inched down to 3.1% from 3.2%.

Investors will also be keeping an eye on the retail sales numbers for the same month on Thursday, while on Friday, there’s a raft of releases, including the Empire State manufacturing index, industrial production, as well as the flash S&P Global PMIs for December.

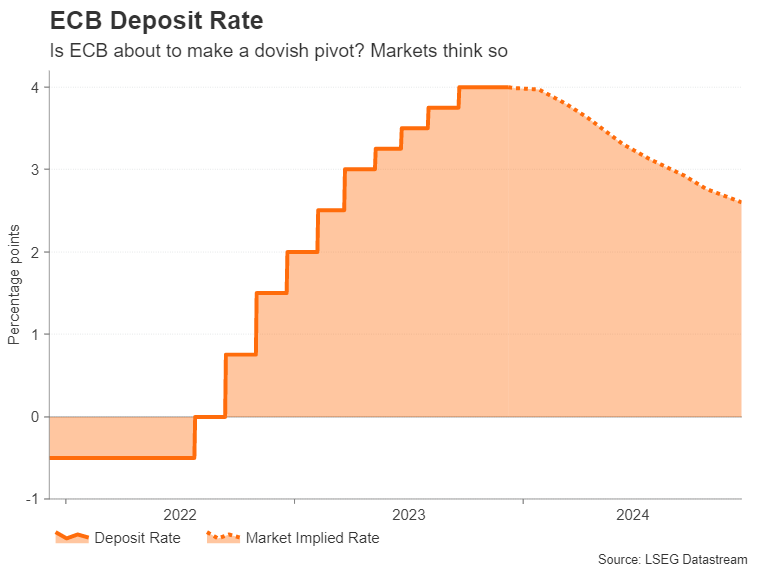

Will ECB decision add to euro’s downside?

The European Central Bank convenes for the final time this year on Thursday and the consensus is that it will keep the deposit rate at 4.0% for the second meeting in a row. Inflation has tumbled quite sharply in the past few months, hitting a more than two-year low of 2.4% y/y in November.

Even ECB policymakers have been taken by surprise by the speed at which inflation has come down lately. Subsequently, the tone has started to shift quite substantially within the Governing Council and a rate hike has now been firmly taken off the table.

Investors don’t see anything upsetting this downward trajectory in inflation and combined with the weakening economic backdrop, speculation is intensifying that the ECB will be the first major central bank to cut, possibly in April.

The euro has come under considerable pressure from the rate cut expectations, slipping below $1.08.

Should President Lagarde endorse the market view in her press conference, there could be further losses for the euro, while there’s not likely to be much relief from the data either.

The flash December PMIs are due on Friday. Only a modest uptick is expected for the services and manufacturing PMIs, though both readings are forecast to remain below 50.

BoE still flying the higher for longer flag

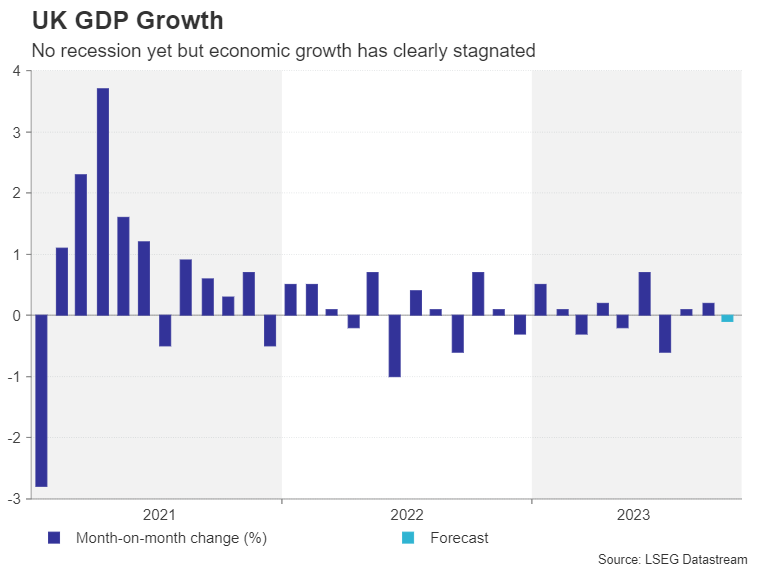

There was finally some good news for the Bank of England last month when inflation nose-dived below 5.0% in October. The pound, however, has perked up against the US dollar as the Fed is seen being less hawkish than the BoE. Another reason why sterling has bounced back lately is that the UK economy so far appears to be steering clear of a recession.

GDP and industrial production figures for October out on Wednesday will provide an updated view on the state of the economy, while there will be further clues from Friday’s flash PMIs. Tuesday’s employment report will be important too as the slowdown in the labour market has yet to translate to a moderation in super-hot wage increases.

The Bank of England is doing its best to strike a balanced tone amid sticky inflation and the ongoing concerns about stagnating growth. But policymakers have had to backtrack on some of their dovish remarks, with Governor Bailey doubling down on the higher for longer stance recently in an attempt to dampen speculation about an early rate cut.

No change in rates is anticipated on Thursday when the BoE meets, but should Bailey try to again brush off rate cut expectations by using stronger language in the statement, the pound is unlikely to gain much unless it is backed by upbeat data or a softer US dollar.

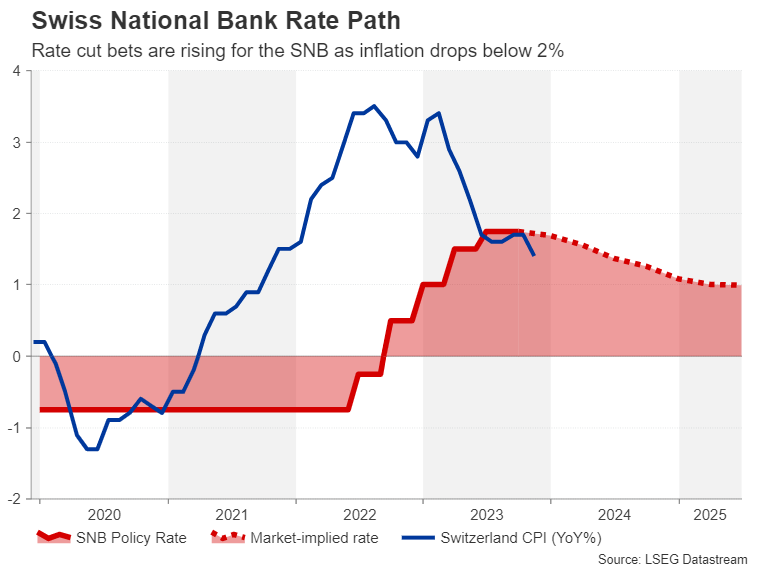

Swiss franc shines ahead of SNB decision

In Switzerland, the central bank will announce its decision early on Thursday. Markets are pricing in a 25% probability for an immediate rate cut. This follows a streak of disappointing data releases, with annual inflation sinking to just 1.4% in November and yearly GDP growth nearly coming to a standstill in the third quarter.

That said, the SNB is highly unlikely to cut rates so soon. The latest commentary from SNB Chairman Jordan in mid-November pointed to the possibility of raising rates further, so it would be a dramatic U-turn to abandon that stance and cut rates immediately.

More likely is that the SNB keeps rates unchanged but abandons its tightening bias and shifts to a neutral position instead. The question is, will that be enough to hurt the Swiss franc, which is the best performing major currency of this year? Markets are already pricing in three rate cuts for 2024, so a neutral shift wouldn’t be any surprise.

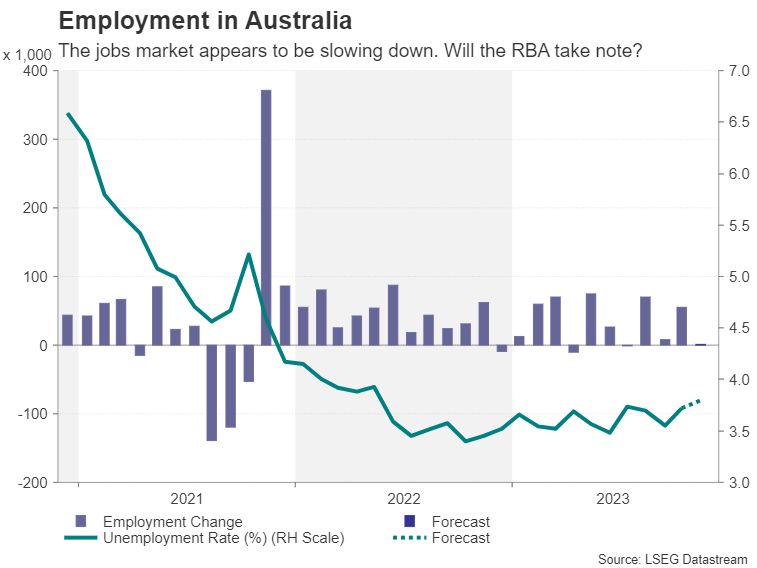

Aussie at risk from weakening economy

Another currency outperforming of late is the Australian dollar. A more hawkish Reserve Bank of Australia has been behind the aussie’s recent rebound but there are doubts about how long Governor Bullock will be able to maintain this rhetoric as the economic data has started to disappoint.

Following the bigger-than-expected drop in CPI in October, traders will be watching Thursday’s employment numbers for November. The flash PMIs on Friday will also be eyed, so will the batch of Chinese releases.

China’s consumer and producer price indices are out on Saturday, and on Friday, attention will turn to the industrial output and retail sales figures for November.

Any improvement in the Chinese data has the potential to offset any downbeat indicators for the domestic economy for the aussie. But the overall market mood will be just as crucial for risk-sensitive currencies and that will likely be determined by the Fed’s message on Wednesday.

Across the Tasman Sea, the third quarter GDP print will be the main item on the agenda for the New Zealand dollar.

Yen rocked by rate hike bets

Speculation is mounting that the Bank of Japan will exit negative rates as early as the December meeting, catapulting the yen sharply higher. Next week’s data are unlikely to significantly alter those expectations but will nevertheless be monitored, particularly the quarterly Tankan survey that’s out on Wednesday. Policymakers would feel more confident about raising interest rates if the data is headed in the right direction so there is scope for the yen to extend its gains in the coming days.

Other Japanese releases will include corporate goods prices on Tuesday, machinery orders on Thursday and the flash PMIs on Friday.