Sample Category Title

Despite Strong USD Spike after NFP Report, Bitcoin Remains in Uptrend

US jobs data for November comes out 199K vs 184K expected. Unemployment rate changed from 3.9% to 3.7%. It appears that what CPI did a month back, the NFP takes it all back on the euro. Some stops must have been cleared out, so possibly that's a perfect price area for market to stabilize at the "fair" value. But its important to keep in mind that as long as CPI and NFP will show different situation for the economy, the ranges on DXY and EURUSD may not be easy broken.

Away from the EURUSD, despite strong USD reaction bitcoin is doing well at current levels. If can stay unchanged for US session, we think that uptrend is ready to resume next week, if not maybe even earlier. Support on dips is at 41k and 40k.

Sunset Market Commentary

Markets

The diptych of today’s US payrolls and next Tuesday’s US November CPI are the ultimate input for the Fed policy decision next Wednesday. Even as central bankers in their toolbox switched forward guidance for data dependency, the new projections/dots still will be key when investors make up their mind on the Fed’s intentions in 2024. Markets are sure that a final additional hike guided in the September SEP is now without any ground. Key question is when Fed governors see the start of the easing cycle and what amount of easing they see as appropriate for end next year. In the September dots, the Fed saw the unemployment rate on average at 3.8% in Q4 this year. The November unemployment rate today was reported at 3.7% (from 3.9%). US job growth reaccelerated to 199k from 150k the previous month. However payrolls for the previous two months were downwardly revised by 35K. This brings the actual outcome close to consensus (185k). Job growth in the manufacturing sector turned again positive (+28k). Private services added 121k amongst others due to gains in education and health services (+99) and leisure and hospitality (40k). The government hired a net 49k of people. Employment in retail trade contracted (-38k). Average hourly earnings rose a strong 0.4% M/M holding the Y/Y measure at 4.0%. The participation rate rose from 62.7% to 62.8%. The data from the household survey was strong overall with the labour force and employment rising sharply. In all, the report can be considered a slightly better than expected. US yields already traded 2.5-4.5 bps higher in the run-up to the release and this was extended in nervous trade afterwards. US yields currently add between 10 bps (2-y) and 5.5 bps (30-y). Expectations on a first Fed rate hike in March eased from 70% to about 50%,but markets still see about 1.25% points of Fed rate cuts by the end of next year. So, the jury is still out whether today’s report will trigger a sustained correction on recent free-fall in yields. German yields also rose a few bps further after the payrolls gaining 6.5-8 bps in a daily perspective. Equity futures temporarily lost ground, but this was soon reversed. The Eurostoxx 50 (currently +0.9%) even set a new post-corona top. US equities open little changed, but also keep the 2023 top levels within reach. After the some hesitation, the dollar outperforms. DXY trades again north of 104. EUR/USD extends its downtrend (1.0735). USD/JPY also tries to leave recent lows (144.4), but momentum is less obvious as markets ponder the upcoming steps in BoJ policy. EUR/GBP again nears intraday peak levels near 0.8585 touched early today after BoE/TNS inflation expectations (next 12 months) eased from 3.6% to 3.3%.

News & Views

Hungarian November inflation flatlined on a monthly basis, allowing the Y/Y figure to decelerate from 9.9% to 7.9%. (vs at -0.1% m/m and 8% expected). Rising food prices (0.5% m/m) and clothing & footwear (1.2%) were offset by lower prices for motor fuel (3.6%) and electricity, gas & other fuels (1.2%). Ongoing disinflation allows the central bank to continue monetary easing. The base rate stands at 11.5%. Based on guidance offered by vice-governor Virag, the MNB wants to stick to a cutting pace of 75 bps per meeting. This should bring the policy rate to sub 11% end this year (meeting December 19). The Hungarian forint marginally strengthens to EUR/HUF 380.78 today but this had to do EU ministers having approved Hungarian access to $920 million in recovery aid. Its approval was already rumoured end November and doesn’t mean that the remaining € 30 billion European funds are for the taking as well. These remain blocked over graft and rule of law concerns. The resources today were non-conditional and aimed at reshaping the energy complex after Russia’s invasion triggered an energy crunch.

The UN’s FAO food price index averaged 120.4 points in November 2023, unchanged from its revised October level. Increases in the indices for vegetable oils, dairy products and sugar counterbalanced decreases in those of cereals and meat. Diving into the subindices, cereals fell on a sharp drop in maize and international wheat prices amid increased supply a.o. in Argentina. Meat was influenced by minor decreases in poultry, pig and bovine meats. Vegetable oils snapped a three month decline on higher palm and sunflower prices with imports purchases of both rising and seasonally lower output in the former reinforcing upward price pressures. High demand particularly lifted butter prices and skim milk powder in the dairy price index, offsetting the ongoing drop in cheese prices. Sugar, finally, rose amid heightened concerns over global export availabilities with two leading exporters, Thailand and India, seeing worsening production due to severe dry weather conditions (El Niño) and shipping delays from Brazil.

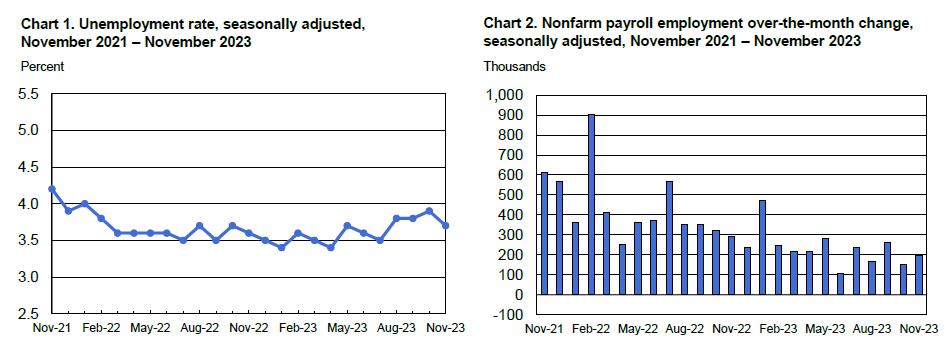

US: Job Growth Rebounds in November, Unemployment Rate Ticks Lower

Non-farm payroll employment rose by 199k in November, slightly ahead of expectations calling for a gain of 185k. Employment figures for September were revised lower by 35k, while October numbers were unchanged.

- Hiring over the last three-months averaged 204k jobs per-month, a slight uptick from the 192k averaged between August-October but well off the 334k averaged over the three-months ending in January.

Private payrolls rose by 150k – a rebound from the 85k reported in October - with service sector (+121k) gains largely concentrated in healthcare & social assistance (+93.2k) and leisure & hospitality (+40k). Meanwhile, retail trade (-38.4k), professional & business services (-9k) and transportation & warehousing (-5k) all shed jobs last month. Goods-producing industries (+29k) were lifted by a strong gain in manufacturing (+28k), although this was entirely due to the resolution of the auto worker strike. The public sector had another solid month of hiring, adding 49k jobs.

In the household survey, employment (+747k) rebounded sharply – more than offsetting last month's pullback – and eclipsed a solid gain in the labor force (+532k). As a result, the unemployment rate ticked down by 0.2 percentage points to 3.7%. The participation rate rose by 0.1 percentage points, returning to its cyclical high of 62.8%.

Average hourly earnings were up 0.4% month-on-month – an acceleration from last month's 0.2% m/m gain and the strongest monthly reading since August. The 12-month change held steady at 4.0%, while the more truncated thee-month annualized rate of change ticked up to 3.4% (from 3.0% in October).

Key Implications

Job growth rebounded in November, in part due to the resolution of the auto worker strike, which helped to add back ~30k workers to last month's payrolls. Looking through the monthly volatility, the trend in hiring has slowed relative to the +300k pace seen at the beginning of the year. However, with the three-month moving average still hovering at just over 200k jobs-per-month, today's job growth is still running at a pace that's more than double trend growth in the labor force.

Term yields have significantly retraced from their mid-October highs as favorable readings on inflation and signs that the labor market is gradually cooling have led market participants to pull-forward the timing of rate cuts. CME futures currently show investors pricing in 125 basis points of rate cuts by the end of 2024, with the first cut coming in March. We view this as premature, particularly given the inflation embers are still glowing and could very easily be reignited by still elevated wage pressures. Policymakers will need to see more compelling evidence that the labor market is on a sustained path towards rebalancing before pushing ahead with any rate cuts. This is unlikely to happen until the second half of next year.

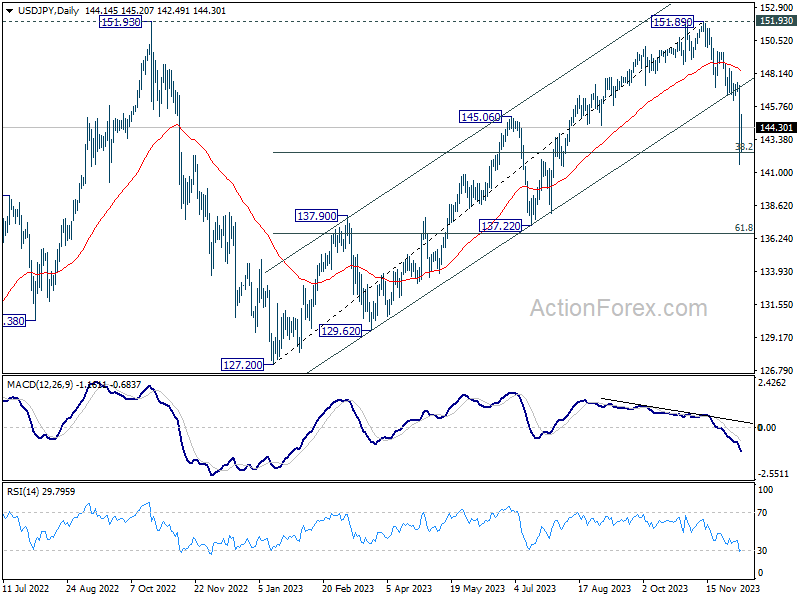

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.43; (P) 144.38; (R1) 147.10; More...

Intraday bias in USD/JPY is turned neutral wit h break of 144.53 minor resistance and some consolidations would be seen. But recovery should be limited below 147.14 support turned resistance to bring another fall. On the downside, break of 141.59 and sustained trading below 142.45 fibonacci level will pave the way to next fibonacci level at 136.63.

In the bigger picture, current fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. This will now remain the favored as long as 147.14 support turned resistance holds.

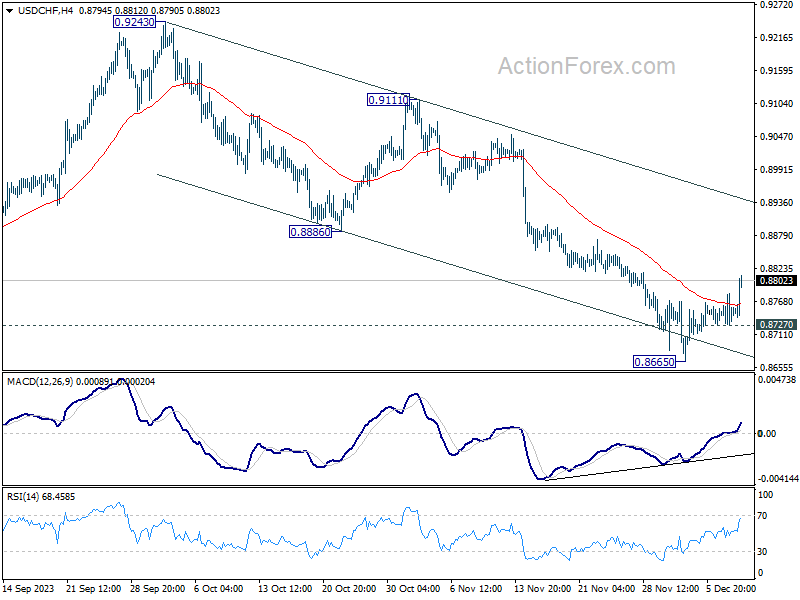

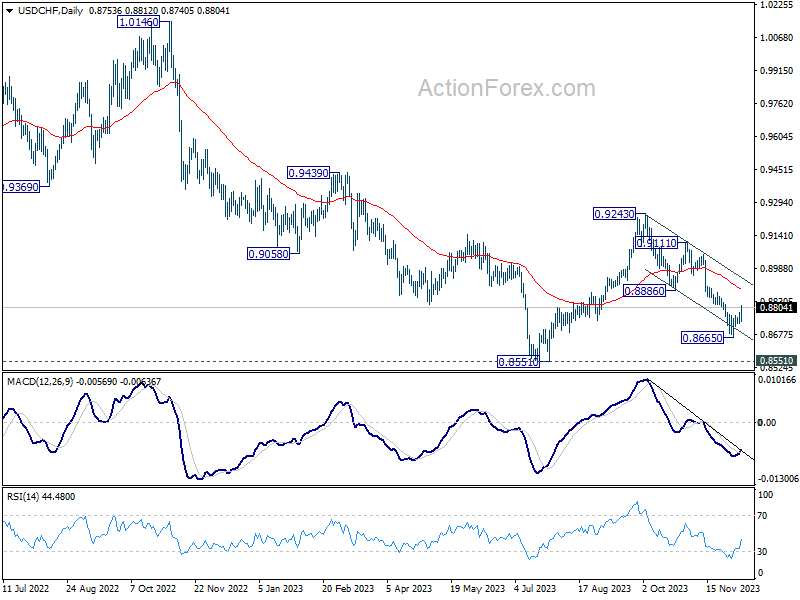

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8727; (P) 0.8754; (R1) 0.8780; More....

USD/CHF's rebound from 0.8655 is in progress and intraday bias stays on the upside for 0.8886 support turned resistance first. Decisive break there will indicate that whole fall from 0.9243 has completed, and bring stronger rally to 0.9111 resistance next. On the downside, below 0.8727 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. For now, this will remain the favored case as long as 0.8886 support turned resistance holds.

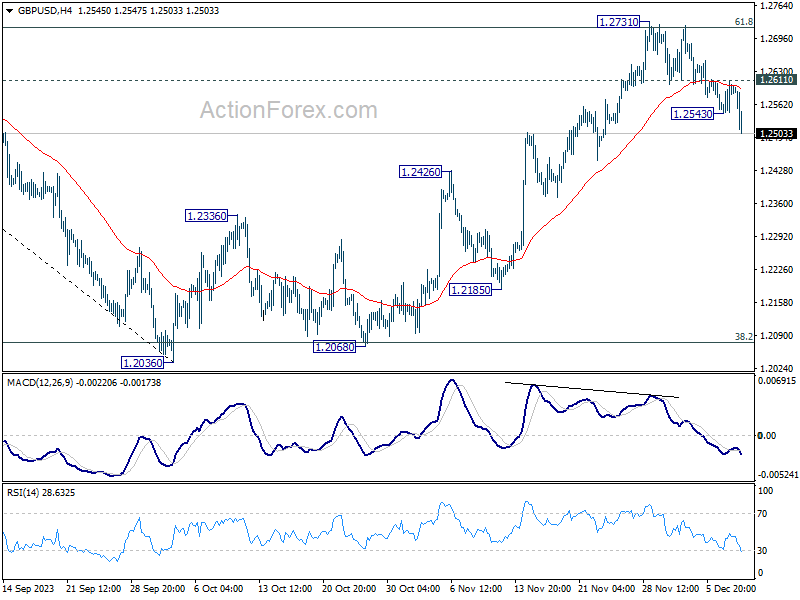

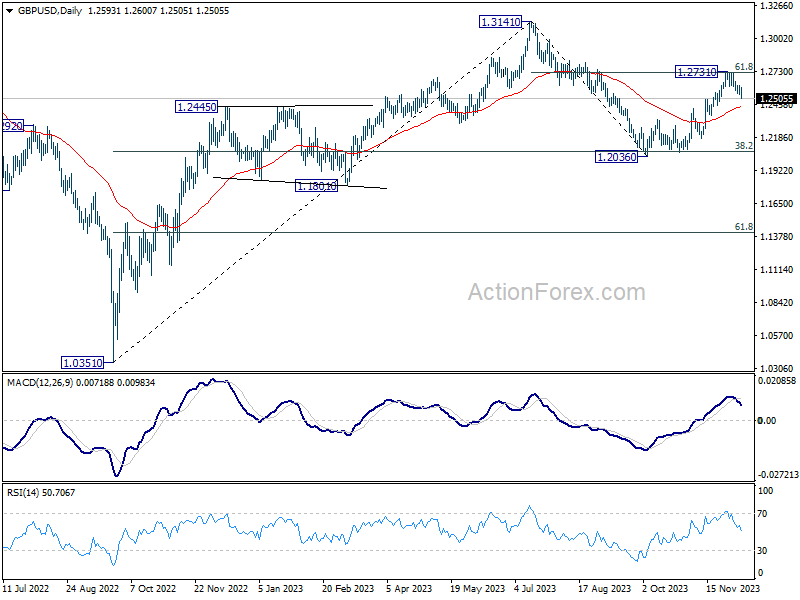

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2554; (P) 1.2584; (R1) 1.2622; More...

GBP/USD's fall from 1.2731 short term top resumed after brief recovery. Intraday bias is back on the downside for 55 D EMA (now at 1.2437). Sustained break there will bring retest of 1.2036 low. On the upside, above 1.2611 minor resistance will turn intraday bias neutral again.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

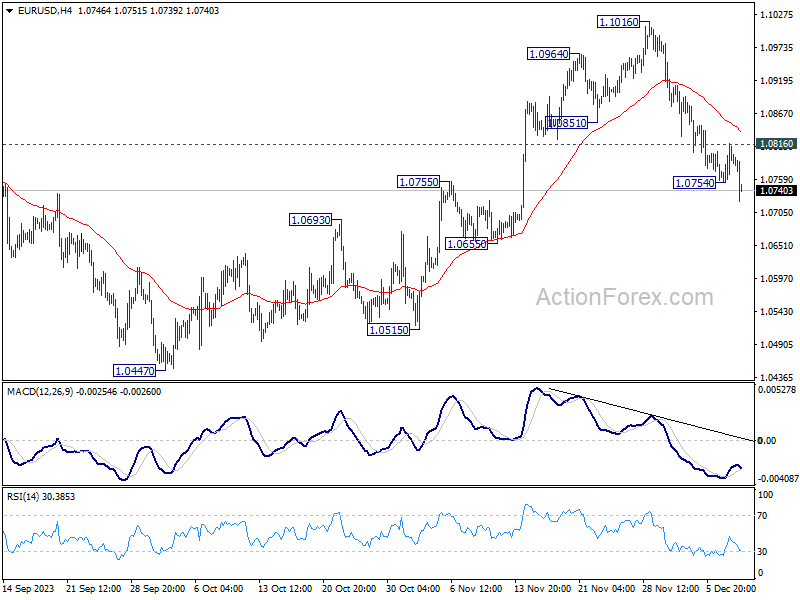

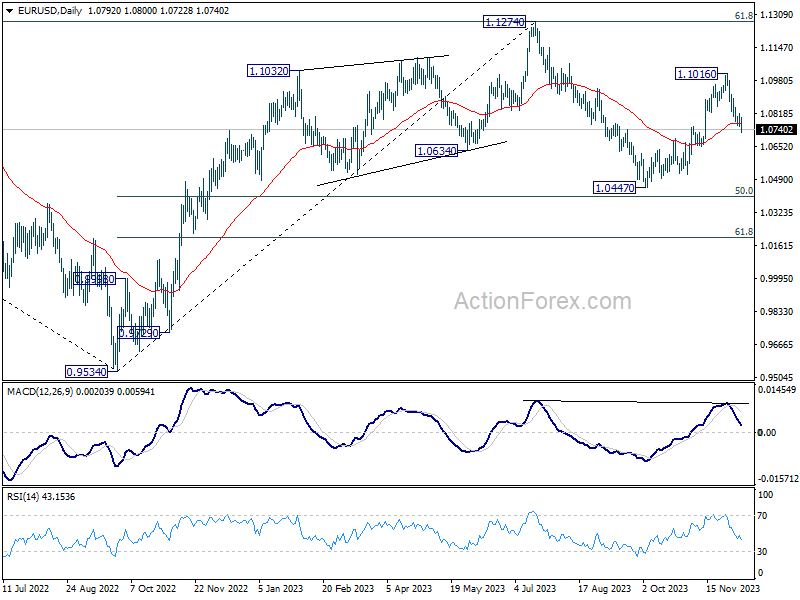

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0760; (P) 1.0788; (R1) 1.0822; More...

EUR/USD's fall from 1.1016 resumed after brief recovery, and intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 1.0770) will pave the way to retest 1.0447 support. On the upside, above 1.0816 minor resistance will turn intraday bias neutral again.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

Dollar Rallies on Strong US Employment Data

Dollar jumps in early US session, buoyed by a robust set of employment data. headline job growth exceeded expectations, narrowly missing 200k mark, while unemployment rate showed a decline. This data suggests a still-tight job market, raising concerns among some market participants that underlying inflation pressures may not be easing as hoped. Notably, strong wage growth stands out as a key indicator of persistent inflationary pressures.

Today's positive employment figures are unlikely to change the prevailing expectation that Fed will keep interest rates unchanged at the upcoming meeting this month. However, the likelihood of an earlier-than-anticipated rate cut seems to have diminished. The market's attention is now shifting towards next week's key economic events, particularly the US CPI data on Tuesday and FOMC economic projections on Wednesday.

In terms of currency market performance for the week, Dollar has solidified its position as the second-best performer, although it remains far from challenging Yen for the top spot. Canadian Dollar ranks as the third strongest currency currently. On the other end of the spectrum, Australian and New Zealand Dollars occupy the weakest positions, followed closely by Sterling. Euro and Swiss Franc are showing mixed performances, positioned in the middle of the currency rankings.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 0.37%. CAC is up 0.90%. Germany 10-year yield is up 0.076 at 2.274. UK 10-year yield is up 0.073 at 4.046. Earlier in Asia, Nikkei fell -1.68%. Hong Kong HSI fell -0.07%. China Shanghai SSE rose 0.11%. Singapore Strait Times rose 1.19%. Japan 10-year JGB yield rose 0.0178 at 0.774.

US NFP grows 199k, unemployment rate down to 3.7%

US Non-Farm Payroll employment grew 199k in November, slightly above expectation of 190k. That was below the average monthly gain of 240k over the prior 12 months.

Unemployment rate fell from 3.9% to 3.7%, below expectation of 3.9%. Participation rate rose 0.1% to 62.8%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings rose 4.0% yoy. Average workweek for all employments edged up by 0.1 hour to 34.4 hours.

BoE survey reveals lower public inflation expectation

The latest Bank of England/Ipsos quarterly Inflation Attitudes Survey show inflation expectations decreased in the near term. There's also a shift in public sentiment towards a more balanced view of the economic situation in the UK, with decreasing number of people expecting further interest rate hikes and an increasing number advocating for stability or reduction in rates.

Median expectation for inflation over the coming year has decreased to 3.3%, down from 3.6% in August 2023. This decline suggests a growing optimism among respondents about the easing of inflationary pressures in the near term. However, when considering the twelve months following that period, expectations remain unchanged at 2.8%, indicating that respondents anticipate a stabilization of inflation rates in the longer term.

Regarding the future path of interest rates, there has been a notable shift in public opinion. Only 44% of respondents now expect rates to rise over the next 12 months, a significant decrease from the 63% who held this view in August. Conversely, 29% expect rates to stay about the same, up from 19%.

When asked about what would be "best for the economy", only 11% of respondents suggested that rates should "go up", down from 13%. Meanwhile, the proportion of respondents who believe that interest rates should "go down" remains steady at 40%, and those who think rates should "stay where they are" have increased to 29% from 26%.

Japan's nominal pay rises 1.5% yoy, but fail to keep pace with inflation, consumer spending drops

Japan's nominal pay growth rose by 1.5% yoy, surpassing the expected 1.0% yoy increase. This marked the fastest rate of increase since June. Regular or base salaries contributed to this increase with a 1.4% yoy rise. However, overtime pay slightly decreased by -0.1% yoy. Special payments, a variable component of wages, saw a significant jump of 7.5% yoy.

However, the positive trend in nominal pay was offset by the continued decline in inflation-adjusted real wages, which fell for the 19th consecutive month, dropping by -2.3% yoy. A labor ministry official commented, "Price increases have outpaced wage growth." This situation is exacerbated by the consumer inflation rate, which includes fresh food prices but excludes owner's equivalent rent, re-accelerating to 3.9% after a brief two-month slowdown.

Alongside wage trends, household spending in Japan also experienced a downturn, decreasing by -2.5% yoy in October. This decline, while still significant, was less severe than the anticipated 3.0% yoy drop. The continued decrease in household spending, which has now extended to eight consecutive months, reflects ongoing challenges in the domestic consumption sector.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0760; (P) 1.0788; (R1) 1.0822; More...

EUR/USD's fall from 1.1016 resumed after brief recovery, and intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 1.0770) will pave the way to retest 1.0447 support. Nevertheless, break of 1.0894 will turn bias back to the upside for 1.1016 resistance instead. On the upside, above 1.0816 minor resistance will turn intraday bias neutral again.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Sales Q3 | -2.80% | 0.20% | -0.80% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | 1.50% | 1.00% | 1.20% | |

| 23:30 | JPY | Overall Household Spending Y/Y Oct | -2.50% | -3.00% | -2.80% | |

| 23:50 | JPY | Bank Lending Y/Y Nov | 2.80% | 2.80% | 2.80% | 2.70% |

| 23:50 | JPY | GDP Q/Q Q3 F | -0.70% | -0.50% | -0.50% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 | 5.30% | 5.10% | 5.10% | |

| 23:50 | JPY | Current Account (JPY) Oct | 2.62T | 1.85T | 2.01T | |

| 05:00 | JPY | Eco Watchers Survey: Current Nov | 49.5 | 49.2 | 49.5 | |

| 07:00 | EUR | Germany CPI M/M Nov F | -0.40% | -0.40% | -0.40% | |

| 07:00 | EUR | Germany CPI Y/Y Nov F | 3.20% | 3.20% | 3.20% | |

| 09:30 | GBP | Consumer Inflation Expectations | 3.30% | 3.60% | ||

| 13:30 | CAD | Capacity Utilization Q3 | 79.70% | 81.40% | 81.40% | |

| 13:30 | USD | Nonfarm Payrolls Nov | 199K | 190K | 150K | |

| 13:30 | USD | Unemployment Rate Nov | 3.70% | 3.90% | 3.90% | |

| 13:30 | USD | Average Hourly Earnings M/M Nov | 0.40% | 0.30% | 0.20% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Dec P | 61.7 | 61.3 |

US NFP grows 199k, unemployment rate down to 3.7%

US Non-Farm Payroll employment grew 199k in November, slightly above expectation of 190k. That was below the average monthly gain of 240k over the prior 12 months.

Unemployment rate fell from 3.9% to 3.7%, below expectation of 3.9%. Participation rate rose 0.1% to 62.8%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings rose 4.0% yoy. Average workweek for all employments edged up by 0.1 hour to 34.4 hours.

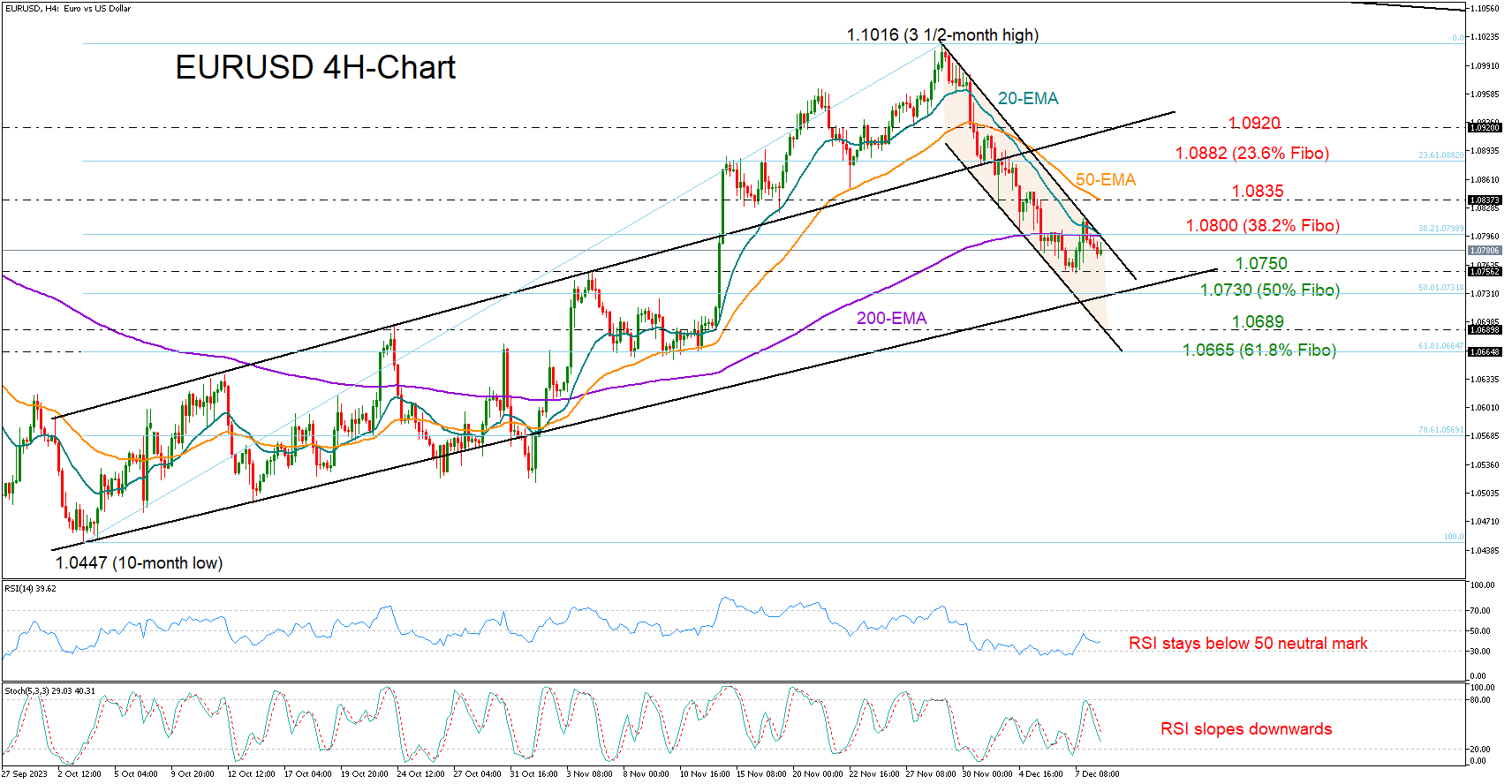

EURUSD Retains Short-Term Negative Trend

- EURUSD trims recent gains ahead of US jobs data

- Short-term downward trajectory stays intact

- Bulls need a clear bounce above 1.0800

EURUSD could not sustain gains above the 1.0800 number and its 20- and 200-period exponential moving averages (EMAs) in the four-hour chart, staying within the tight bearish channel, which followed November’s peak of 1.1016.

The latest pullback dampened hopes for a bullish reversal in the very short-term picture ahead of the all-important US nonfarm payrolls report. Adding to the risks is the falling RSI, which failed to cross above its 50 neutral mark, suggesting the bears could dominate the market in the short term.

If December’s base of 1.0750 collapses, the price might seek shelter around the 50% Fibonacci retracement level of the October-November upleg at 1.0730. The upward-sloping line from October’s lows is adding extra credence to the region. However, if sellers win the battle there too, the decline could continue towards the channel’s lower band at 1.0689. The 61.8% Fibonacci mark of 1.0665 could be the next destination.

On the upside, the bulls will fight for a clear close above the channel and the 38.2% Fibonacci around 1.0800. Such an achievement might boost buying appetite towards the 50-period EMA at 1.0835. Additional increases from there could stabilize near the 23.6% Fibonacci of 1.0882, while an extension above the key ascending line from October at 1.0920 might shift the attention back to November’s highs.

In brief, EURUSD retains a downward trajectory in the short-term picture, with traders waiting for a move above 1.0800 or below 1.0750 to drive the market accordingly.