Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.19; (P) 149.45; (R1) 149.70; More...

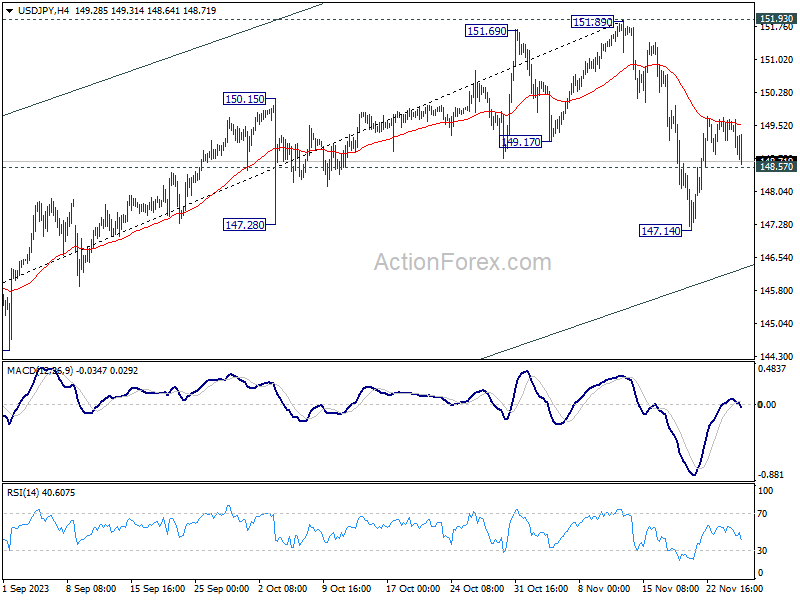

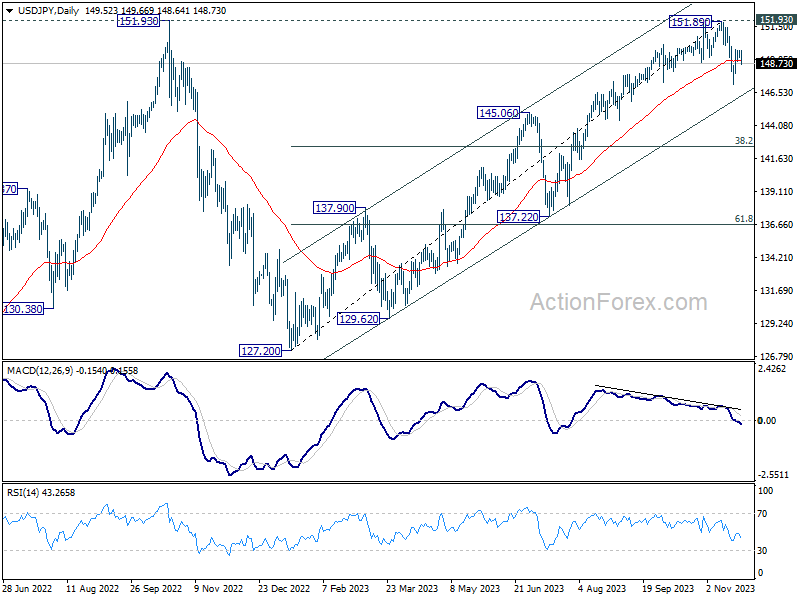

Intraday bias in USD/JPY remains neutral as this point. Risk stays on the downside as long as 55 4H EMA (now at 149.55) holds. Break of 148.57 minor support will turn bias to the downside the resume the fall from 151.89 through 147.14 support. However sustained break of 55 4H EMA will revive near term bullishness, and target a retest on 151.89/93 resistance zone.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

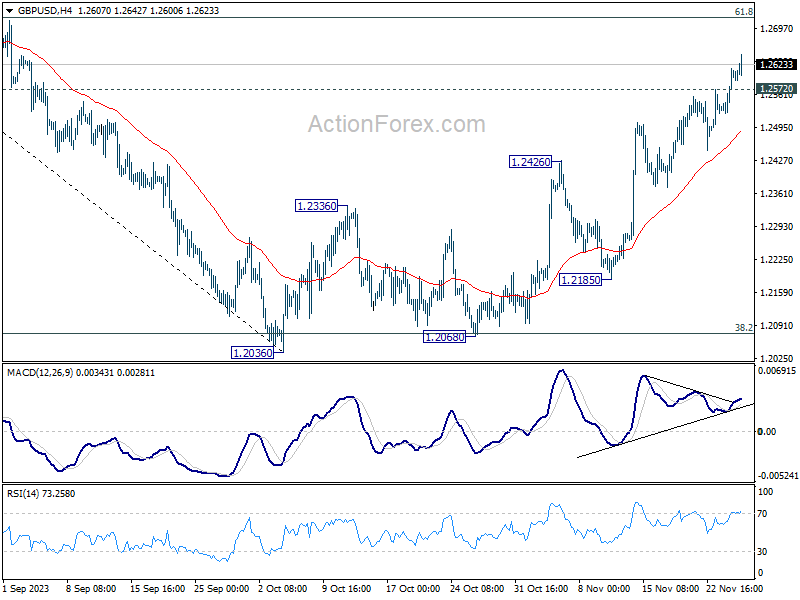

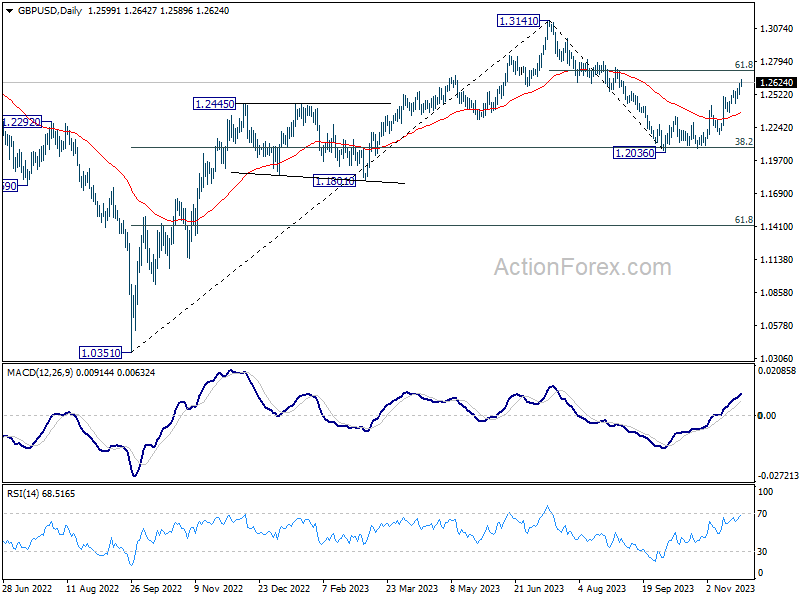

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2548; (P) 1.2581; (R1) 1.2638; More...

GBP/USD hits as high as 1.2642 so far as rise from 1.2036 continues today. Intraday bias stays on the upside at this point. Next target is 61.8% retracement of 1.3141 to 1.2036 at 1.2716. On the downside, below 1.2572 minor support will turn intraday bias neutral first. But further rally will now remain in favor as long as 1.2426 resistance turned support holds.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

Dollar Dips, Euro Struggles in Lackluster Market

As US session commences, Dollar is showing a more notable downturn following a rather uneventful day. In the background risk sentiment is steady, with investors and traders largely holding their positions in anticipation of key economic data releases. The upcoming PCE inflation data on Thursday and ISM manufacturing data on Friday are particularly crucial. These datasets are expected to play a significant role in shaping the current narrative of falling inflation and a stabilizing economy, which is hoped to lead to soft landing.

However, it's also important to note that both Canadian Dollar and Euro are having some struggles too in their respective crosses. Euro, in particular, is looking vulnerable against Sterling and Australian Dollar. Important economic data releases are on the horizon for these currencies as well, including Canadian employment figures and Eurozone PMI flash data later in the week.

Australian Dollar and Japanese Yen are showing strength today. For Aussie, there is some focus on retail sales data due tomorrow, but Wednesday's monthly CPI is likely to be a more significant driver. As for Yen, significant developments to watch include China's PMI data and the Yuan's impact, given the recent parallel trends between the two.

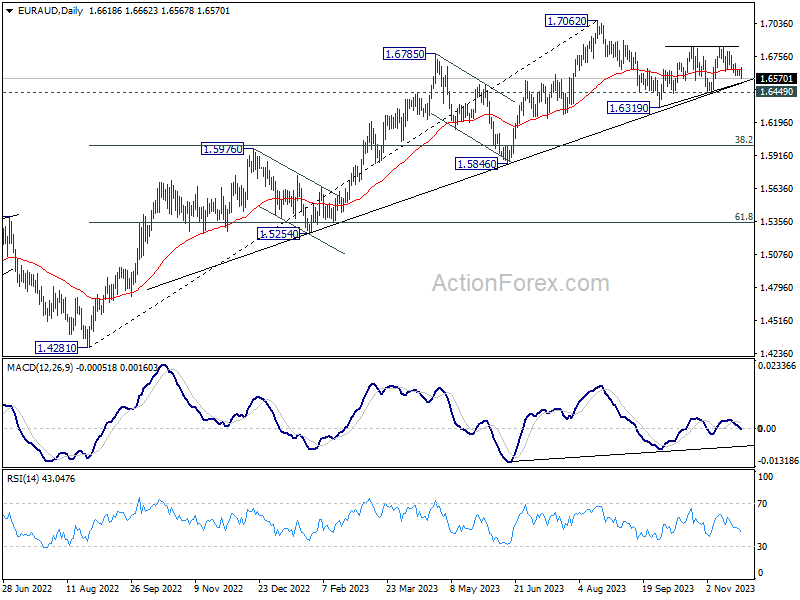

From a technical perspective, the next few days could be critical for EUR/AUD, as it's now heading back to medium term trendline support. Sustained break there, followed by firm break of 1.6449 support will argue that fall from 1.7062 is already corrective whole up trend from 1.4281 (2022 low). In this case, near term outlook will be turned bearish with prospect of falling to 1.5846 support before a sustainable bounce.

In European session, at the time of writing, FTSE is down -0.26%. DAX is down -0.14%. CAC is down -0.03%. Germany 10-year yield is down -0.058 at 2.588. Earlier in Asia, Nikkei fell -0.53%. Hong Kong HSI fell -0.20%. China Shanghai SSE fell -0.30%. Singapore Strait Times fell -0.27%. Japan 10-year JGB yield fell -0.0026 to 0.776.

BoE's Bailey: Too soon to have discussion on rate cuts

In an interview with ChronicleLive, BoE Governor Andrew Bailey pointed out that the recent decline in inflation is largely attributed to the unwinding of last year's surge in energy prices.

He highlighted two important phases in the inflation reduction process. He anticipates that by the end of the first quarter next year, inflation may fall to just "under 4%", leaving an additional 2% reduction to reach the BoE's target.

This remaining gap, Bailey noted, is the challenging part, emphasizing that "the second half, from there to two, is hard work."

Moreover, Bailey explicitly pushes back against assumptions of imminent interest rate cuts, stating it's "too soon to have that discussion."

BoJ's Ueda repeats uncertainty on stably achieving inflation target

In today's address to the parliament, BoJ Governor Kazuo Ueda provided note that the economy is "recovering moderately," which is further evidenced by the narrowing of the output gap to "near zero".

Ueda also highlighted "We're seeing some positive signs in wages and inflation". However, he tempered this optimism by acknowledging the "high uncertainty on whether this cycle will strengthen"

A key point in Ueda's commentary was BoJ's stance on inflation. Despite the positive signs, he stated that the central bank cannot yet assert with confidence that inflation will sustainably and stably achieve its 2% target.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2548; (P) 1.2581; (R1) 1.2638; More...

GBP/USD hits as high as 1.2642 so far as rise from 1.2036 continues today. Intraday bias stays on the upside at this point. Next target is 61.8% retracement of 1.3141 to 1.2036 at 1.2716. On the downside, below 1.2572 minor support will turn intraday bias neutral first. But further rally will now remain in favor as long as 1.2426 resistance turned support holds.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | 2.30% | 2.10% | 2.10% | |

| 15:00 | USD | New Home Sales M/M Oct | 725K | 759K |

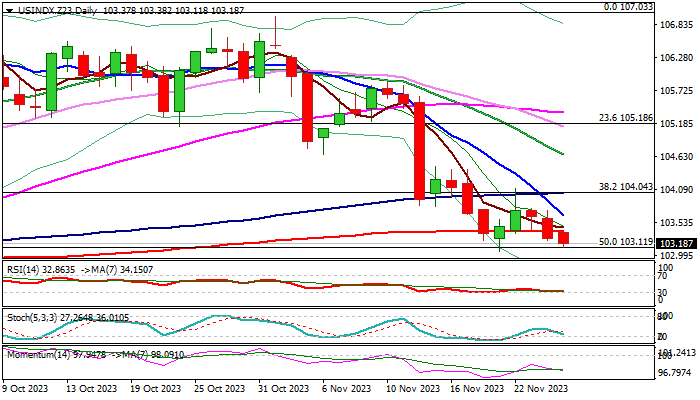

Dollar Index Outlook: Bears Crack Pivotal Support Zone

The dollar index keeps bearish stance at the beginning of the week and cracks the upper boundary of pivotal 103.11/102.84 support zone (50% retracement of 99.20/107.03 rally / Nov 21 three-month low/weekly cloud base).

Last Friday’s close below 200DMA (102.38) generated initial bearish signal which looks for confirmation on firm break of 103/11/102.84 to signal continuation of a downtrend from 107.03/106.96 double top and spark fresh acceleration towards 102.19/00 (Fibo 61.8% / round figure).

Daily studies show strong negative momentum and converging daily Tenkan/Kijun-sen pointing to increasingly bearish configuration.

Growing expectations of an end of Fed’s tightening cycle and speculations of rate cuts in mid-2024, keep the dollar under pressure, as markets await releases of US Q3 GDP and Oct PCE Price Index (Fed’s preferred inflation gauge) for more clues about the next steps of the US central bank.

Broken 200DMA reverted to initial resistance, followed by falling 10DMA (103.66), guarding upper pivot at 104.04 (broken 100DMA / Fibo 38.2%).

Res: 102.38; 103.66; 104.04; 104.66.

Sup: 102.84; 102.19; 102.00; 101.59.

Australian Dollar Extends Gains, Retail Sales Next

- Australian dollar extends gains

- Australian retail sales expected to decelerate to 0.1%

The Australian dollar has extended its gains at the start of the week. In the European session, AUD/USD is trading at 0.6603, up 0.28%. The Aussie has posted an impressive streak, rising 3.8% against the greenback since November 14th.

Australia releases retail sales for October on Tuesday. The consensus estimate stands at a negligible 0.1%, compared to a strong 0.9% gain in September. The sharp gain, which indicated resilience in consumer spending, provided support for the RBA to raise rates at the November meeting. If retail sales misses the estimate, it could sour sentiment towards the Aussie and send the currency lower. RBA Governor Michele Bullock will speak at an event in Hong Kong on Tuesday and investors will be looking for hints about what the RBA is planning at its meeting on December 5th.

RBA to undergo major overhaul

Changes, big changes are coming to the Reserve Bank of Australia. The Australian government announced it would introduce legislation to overhaul the central bank. This follows an independent review which called for sweeping changes at the RBA. There has been much criticism of the RBA for its pledge not to raise rates before 2024, only to embark on a tightening campaign which has raised the cash rate to 4.35%. The new Governor, Michele Bullock, has said she is favour of the changes.

Last week, Bullock said on Tuesday that inflation has peaked and that the upside risk to inflation was domestic and demand-driven. Bullock noted that inflation had dropped from 8.0% to 5.5% in less than a year, but it would take much longer for inflation to drop that amount again and fall to 3%. The RBA’s target range is 2%-3%. The RBA remains hawkish and raised rates earlier this month after holding rates for four straight times..

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6618. Above, there is resistance at 0.6650

- 0.6559 and 0.6526 are providing support

Has Inflation Fire Been Extinguished by ECB?

- Key data releases on the menu as the ECB meets in two weeks

- ECB officials have been toning down their hawkish commentary

- The euro would welcome a strong inflation print and the ensuing hawkish rhetoric

- German CPI will be released on Wednesday; EZ aggregate on Thursday 10 GMT

Two weeks left for the last ECB meeting for 2023

With the Thanksgiving holiday break behind us, we are on the homestretch now for 2023. The market is counting down to the last round of central bank meetings starting with the RBNZ this week and concluding with the BoJ meeting on December 19. The ECB gathering is scheduled for December 14 and the market would be very interested in any rhetoric change by President Lagarde.

Ahead of this busy period, ECB members have been flooding the airwaves with their comments. They have been trying hard to convince the market that (1) rate hikes are not completely off the table, (2) rates will probably stay at the current levels for a while and it is too early to talk about rate cuts, (3) the current weak growth patch is expected to continue in 2024 but they do not expect a recession and (4) inflation is expected to edge a bit higher over the coming months.

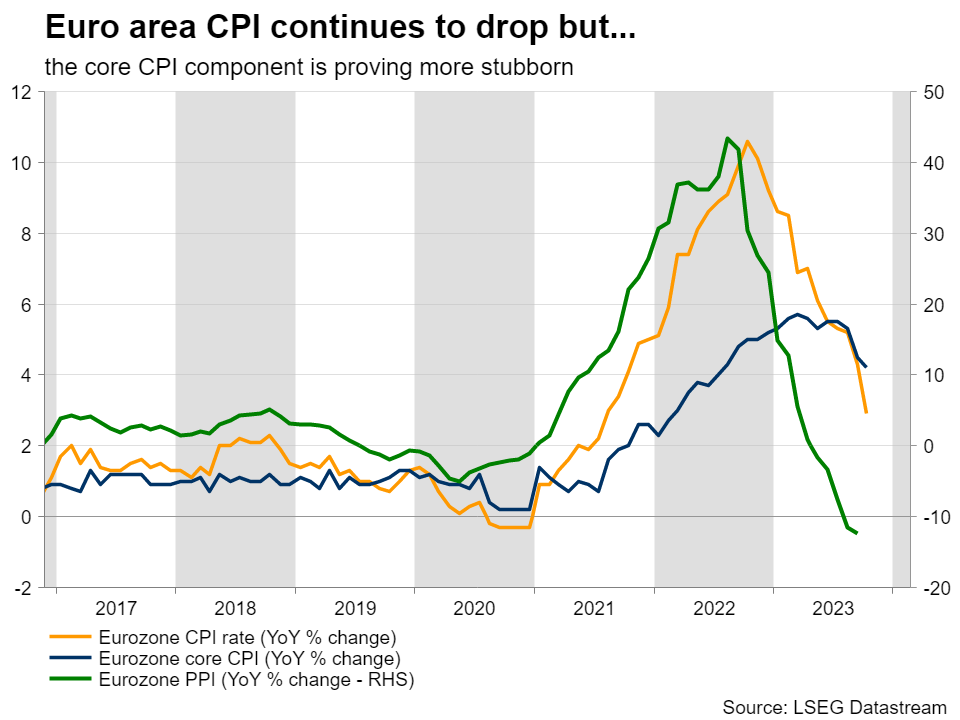

At the end of the day though, their approach is data dependent. Since the October ECB meeting, euro area economic data prints have been mostly mixed. The weak preliminary GDP for the third quarter of 2023 has been followed by subdued retail sales, revealing the impact of a rather long period of continued price increases. Inflationary pressures have been abating but core inflation remains stubbornly high, complicating the outlook. At least, PMI surveys have been picking up pace, although the German PMI manufacturing survey is stuck at an extremely low level.

November inflation report in focus

Τhis week we will get the preliminary inflation report for November. On Wednesday, the various German states will publish their figures with the German national figures expected after 13.00 GMT. The annual German inflation figure has been on an aggressive downward trend since the November 2022 peak of 8.8% with forecasts revolving around another deceleration to 3.5%.

The euro area aggregate print is expected on Thursday. With the headline indicator gravely affected by the weaker energy prices and thus seen recording a 2.8% YoY change, the core indicator is bound to get more attention. The core index, excluding energy, food, alcohol and tobacco, has been falling from the March 2023 peak of 5.7% and it is forecast to fall below the 4% level for the first time since July 2022.

However, it remains at an elevated level, and above the headline figure. ECB members are worried that the supply issues and stronger wage increases across the euro area are potentially supporting the stickiness of core inflation.

With the market fixated with rate cuts - the first 25bps rate cut is fully priced in by June 2024 - a possibly strong inflation report is unlikely to affect market expectations. In fact, only a combination of stronger growth indicators such the PMI surveys and repeatedly stronger inflation prints could convince the market that rate cuts are probably not around the corner at this stage.

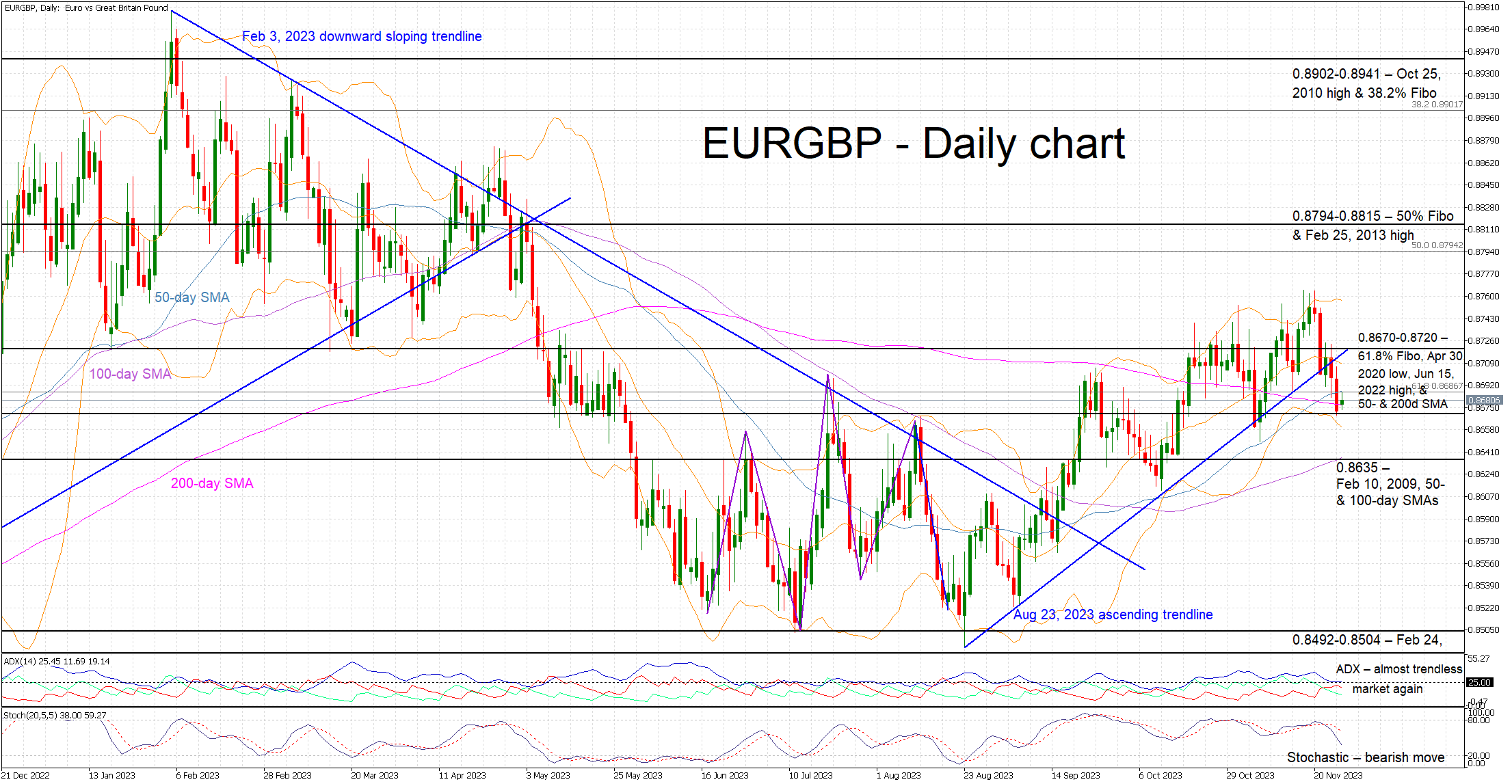

Euro in danger of losing its recent hard-earned gains

The euro has been outperforming the pound since late August, but these hard-earned gains could be under threat now. Last week’s UK Autumn Statement appears to have invigorated the pound bulls but the next leg in the euro-pound pair will probably depend on this week’s data calendar, and predominantly the November inflation report.

A strong set of data this week could help the euro-pound pair climb above the August 23 ascending trendline and potentially open the door for a move towards the 0.8794-0.8815 area. On the flip side, weak data results and dovish rhetoric from ECB officials could mean the current correction might have legs, with 0.8635 being the next credible target.

Cryptocurrency Traders Pause after Growth

Market picture

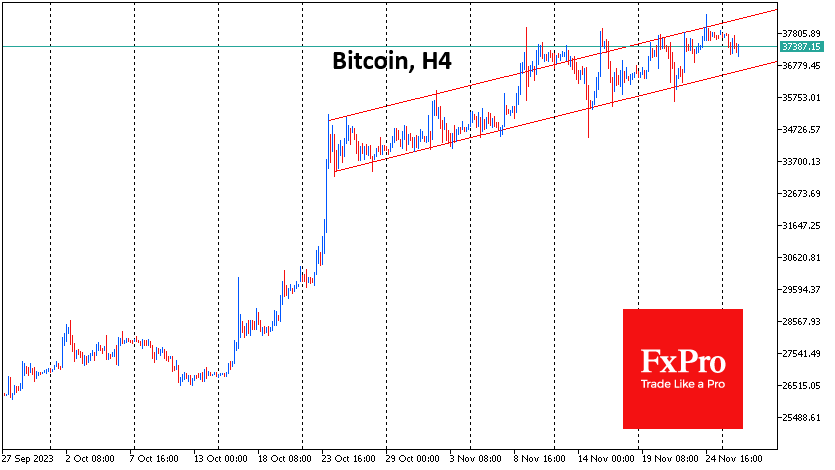

Crypto market capitalisation was near $1.42 trillion on Monday morning, roughly where we saw it a week earlier. Failure to build on the growth at the end of last week caused moderate pressure on prices across a wide range of coins.

For example, the Bitcoin exchange rate was pulling back to $37.0K, having remained within an uptrend for over a month now, with the lower boundary now at $36.6K and the upper boundary at $38.3K. Only a decline below the lower boundary will question the sustainability of the uptrend. Until then, the prevalence of buying on declines in the major cryptocurrencies is very likely.

As a result of another recalculation, Bitcoin mining difficulty increased by 5%. The index reached an all-time high at 67.96 T. The average hash rate for the period since the previous change in the value was 486 EH/s. According to CryptoQuant data, selling pressure from miners is at its lowest level since 2017. Meanwhile, 82% of Bitcoin holders are in profit, and only 15%.

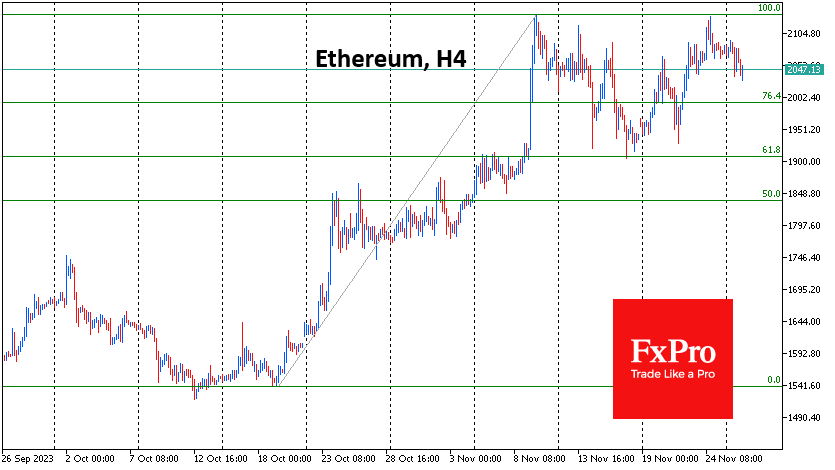

Ethereum failed to hold above $2100 levels for the third time this year. Before that, there were attempts in April and early November. The second most important cryptocurrency rolled back to $2050, which does not look scary yet but sets up for increased pressure in the short term.

News background

The US Commodity Futures Trading Commission (CFTC) has warned crypto exchanges that it will aggressively pursue crypto platforms operating in the US market if they seek to circumvent the CFTC’s customer protection regime.

The surge of interest in spot bitcoin ETFs amid the wait for US regulatory approval could attract up to $70bn of new capital into BTC. The forecast assumes that 10 per cent of the money currently invested in mainstream stock and bond ETFs will move into bitcoin ETFs.

The outflow from the GBTC fund, when converted to a spot ETF, would be $2.7bn, JPMorgan forecasts. GBTC fund shares were previously sold at a discount, and after conversion, their price should be equal to the price of BTC. At the same time, many traders will decide to lock in profits, which will put pressure on the price of the first cryptocurrency.

Crypto analyst Dan Gambardello suggested that during the next bull rally in the crypto market, Cardano (ADA) could rise to $11, thanks to the growth of Bitcoin. ADA’s growth will also be helped by the growing decentralised finance (DeFi) ecosystem, which uses Cardano’s blockchain. According to Gambardello, Cardano has an advantage over Ethereum in terms of reliability, security, and decentralisation.

ECB President Christine Lagarde, who often criticises cryptocurrencies, admitted that her son invested in digital assets but failed to guess the trend and lost almost all his invested money.

EURUSD Regains Traction After Mild Pullback

- EURUSD attempts a strong rebound from 2023 lows

- Posts a fresh 3-month high before paring some gains

- Momentum indicators endorse a resumption of the advance

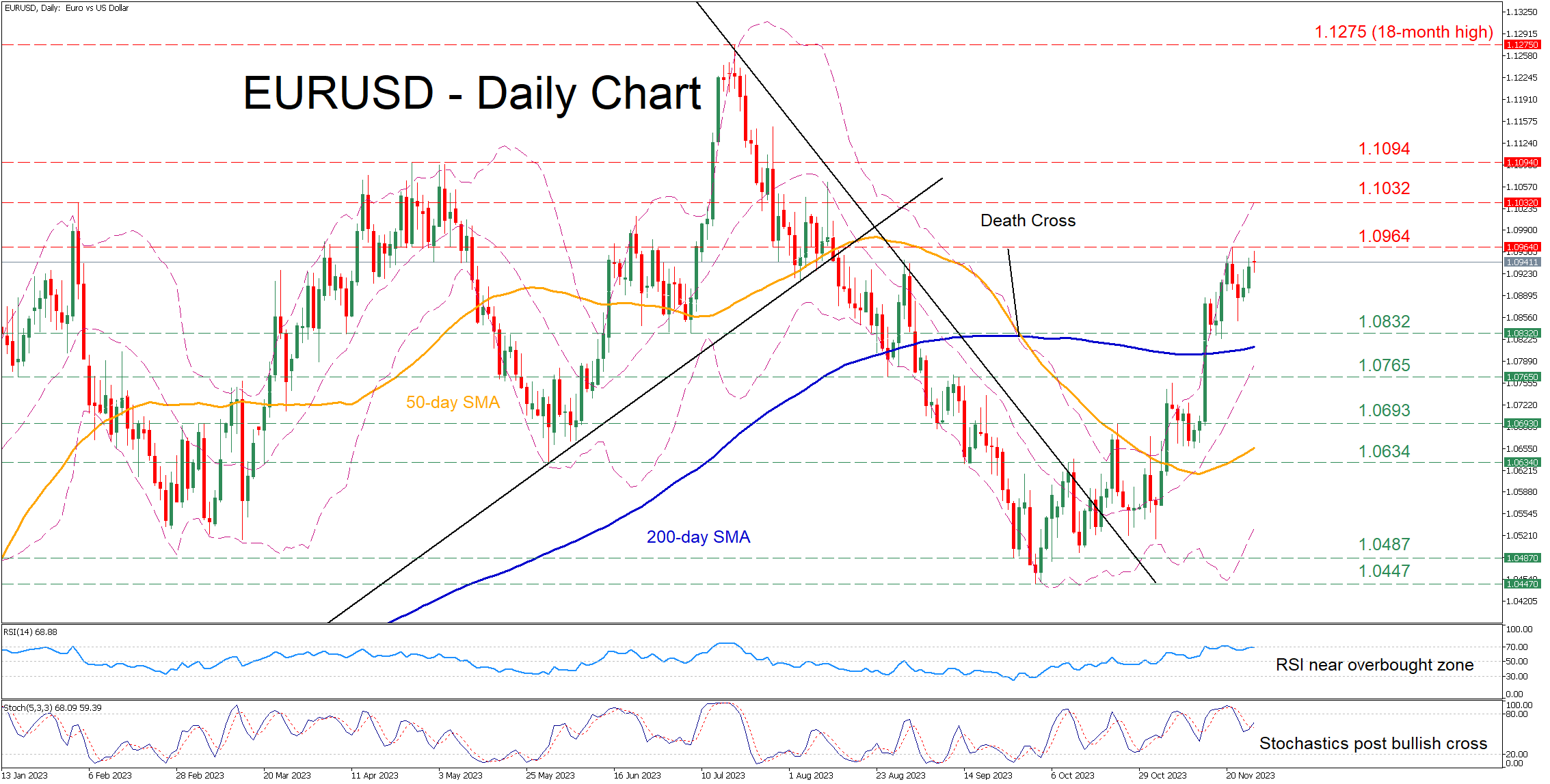

EURUSD has been in a recovery mode following its 2023 bottom of 1.0447 on October 3. Although the pair’s rebound got rejected at a fresh three-month high of 1.0964, the bulls prevented a significant downside correction, with the short-term oscillators remaining heavily skewed to the upside.

Should buying pressures persist, the price could revisit its recent rejection region of 1.0964. Breaking above that zone, the pair might ascend towards the February peak of 1.1032. If that hurdle also fails to provide resistance, the spotlight could turn to 1.1094, which held strong three times in April.

Alternatively, bearish actions could send the price lower to test the June-July support of 1.0832. A violation of that area could set the stage for 1.0765, which served both as support and resistance in September. Failing to halt there, the pair’s decline could resume towards 1.0693 ahead of the May low of 1.0634.

In brief, despite the latest setback, EURUSD remains buoyant and on track to resume its recent recovery. However, a failure to post a fresh higher high might trigger a downside correction.

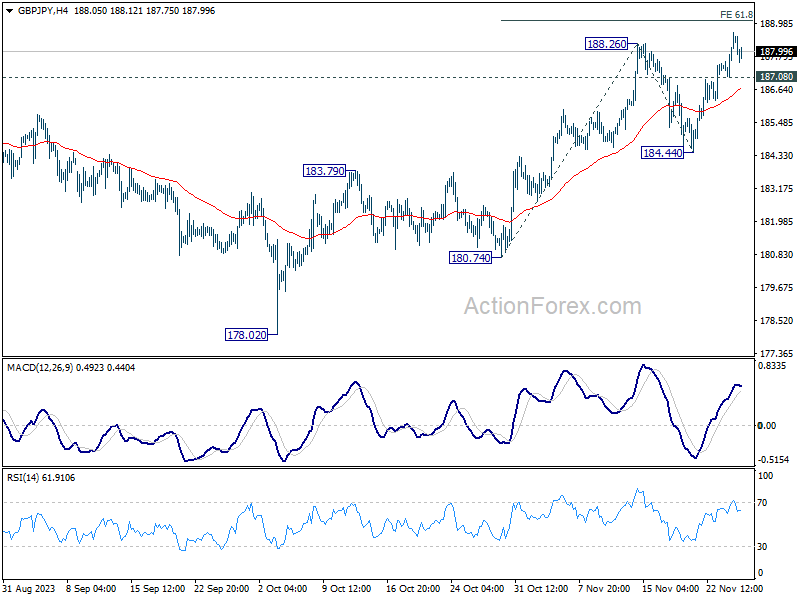

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.43; (P) 188.05; (R1) 188.98; More...

Further rise is expected in GBP/JPY with 187.08 minor support intact. Current rally should target 61.8% projection of 180.74 to 188.26 from 184.44 at 189.08 first. Break will target 100% projection at 191.96 next. On the downside, below 187.08 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, as long as 184.44 support holds, larger up trend from 123.94 (202 low) should still be in progress, next target is 195.86 (2015 high). However, firm break of 184.44 will now argue that a medium term top is formed, possibly in bearish divergence condition in D MACD, and bring deeper fall back to 178.02 support.

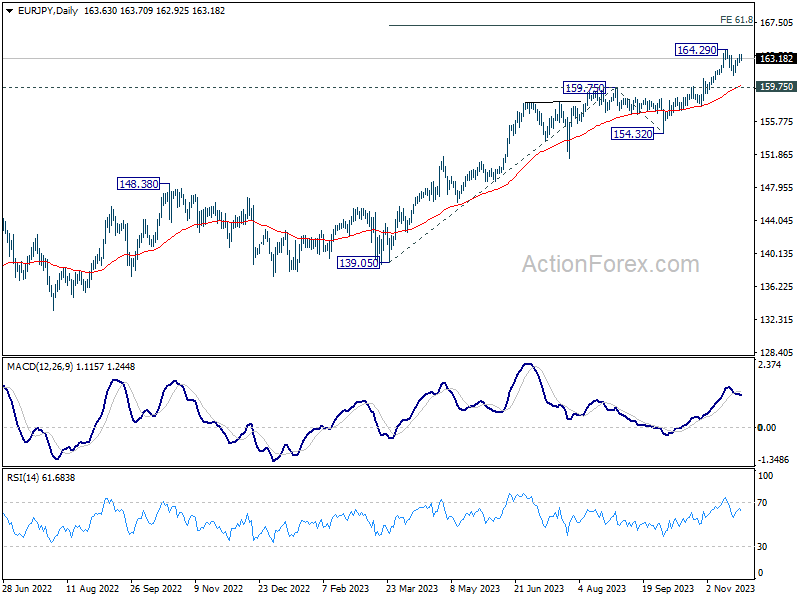

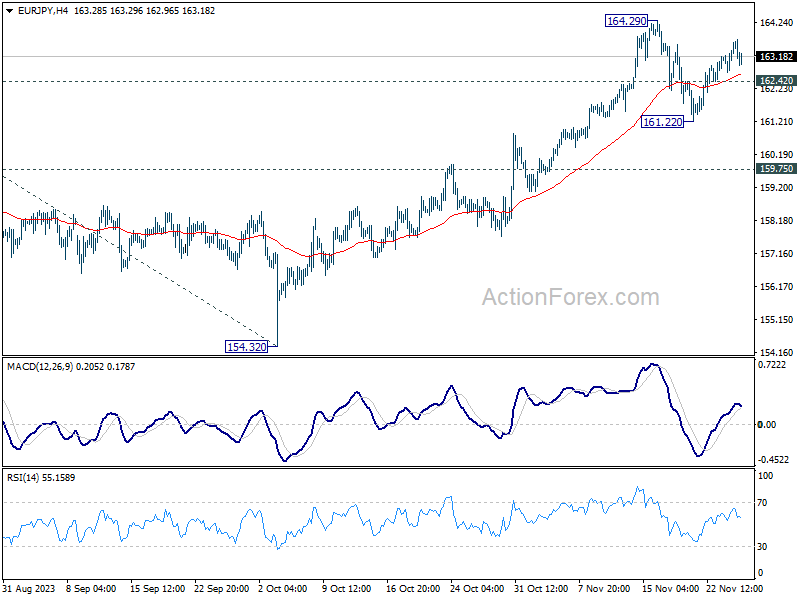

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.91; (P) 163.28; (R1) 163.84; More....

Further rise is still mildly in favor with 162.42 minor support intact. retest of 164.29 should be seen next. Firm break there will resume larger up trend. On the downside, however, break of 162.42 minor support will turn bias back to the downside, to extend the corrective pattern from 164.29 with another falling leg.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 169.96 (2008 high). On the downside, break of 159.75 resistance turned support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.