Sample Category Title

BoE’s Bailey: Too soon to have discussion on rate cuts

In an interview with ChronicleLive, BoE Governor Andrew Bailey pointed out that the recent decline in inflation is largely attributed to the unwinding of last year's surge in energy prices.

He highlighted two important phases in the inflation reduction process. He anticipates that by the end of the first quarter next year, inflation may fall to just "under 4%", leaving an additional 2% reduction to reach the BoE's target.

This remaining gap, Bailey noted, is the challenging part, emphasizing that "the second half, from there to two, is hard work."

Moreover, Bailey explicitly pushes back against assumptions of imminent interest rate cuts, stating it's "too soon to have that discussion."

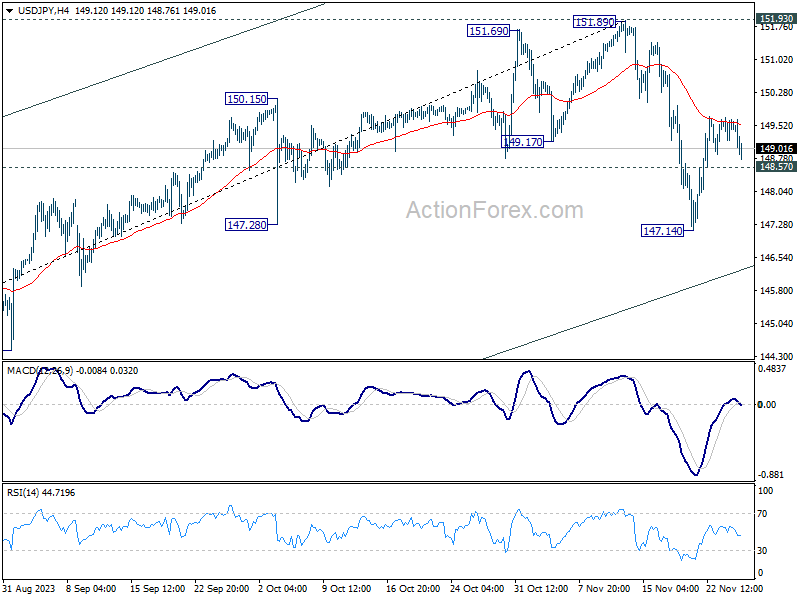

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.19; (P) 149.45; (R1) 149.70; More...

USD/JPY dips notably today but stays above 148.57 minor support. Intraday bias remains neutral at this point. Risk stays on the downside as long as 55 4H EMA (now at 149.55) holds. Break of 148.57 minor support will turn bias to the downside the resume the fall from 151.89 through 147.14 support. However sustained break of 55 4H EMA will revive near term bullishness, and target a retest on 151.89/93 resistance zone.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

Yen Cautious Rebounds While Gold Rallies Above 2k

Yen is having a moderate rebound today, spurred by slightly stronger-than-expected corporate services price inflation data. However, this uptick in is showing only restrained momentum, especially noticeable even against a weaker Dollar. The limited rise can be attributed to low market activity, as there are no significant events scheduled for the day.

Nevertheless, this tranquility in the market is expected to be short-lived, as volatility is likely to escalate with the unfolding of high-profile events later in the week. Key events include inflation data releases from US, Eurozone, and Australia, along with RBNZ rate decision.

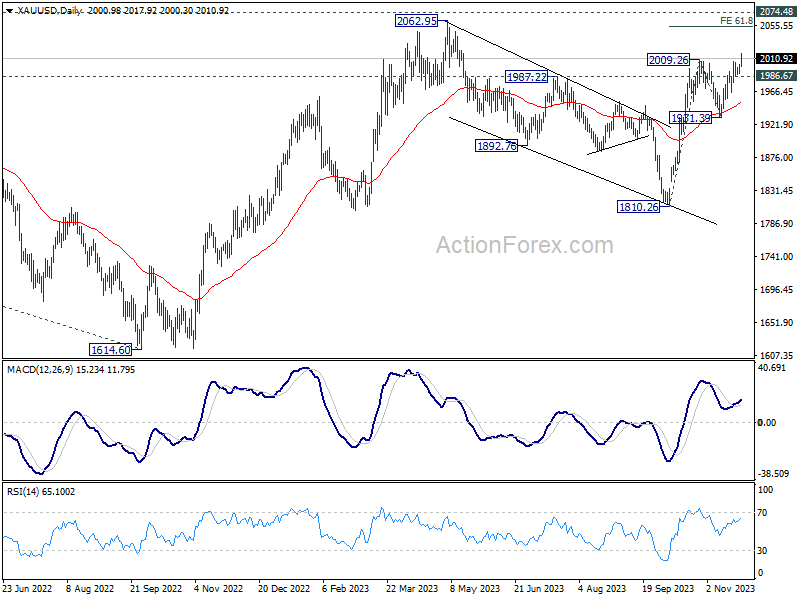

Technically, Gold finally breaks through 2009.26 resistance and resume near term rally to a six-month high in Asian session. Technically, further rally is expected as long as 1986.67 support holds. Next short-term target is 61.8% projection of 1810.26 to 2009.26 from 1931.39 at 2054.37. It remains to be seen if Gold is strong enough to break through 2074.48 long term resistance.

In Asia, Nikkei dropped -0.53%. Hong Kong HSI is down -0.16% China Shanghai SSE is down -0.30%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield closed flat at 0.778.

BoJ's Ueda repeats uncertainty on stably achieving inflation target

In today's address to the parliament, BoJ Governor Kazuo Ueda provided note that the economy is "recovering moderately," which is further evidenced by the narrowing of the output gap to "near zero".

Ueda also highlighted "We're seeing some positive signs in wages and inflation". However, he tempered this optimism by acknowledging the "high uncertainty on whether this cycle will strengthen"

A key point in Ueda's commentary was BoJ's stance on inflation. Despite the positive signs, he stated that the central bank cannot yet assert with confidence that inflation will sustainably and stably achieve its 2% target.

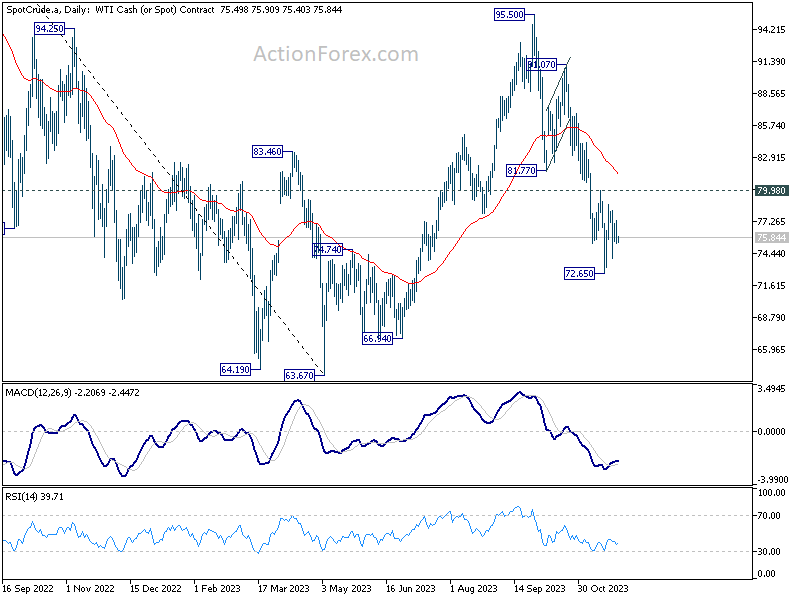

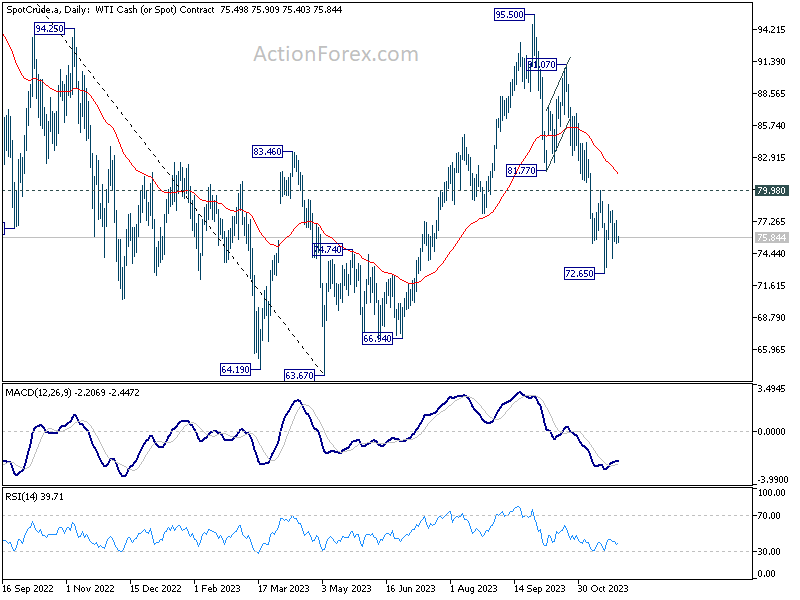

WTI oil staying near-term bearish, anticipating delayed OPEC+ decisions

In the current oil market, stability reigns as prices stay in the near-term range, with all eyes on the impending delayed OPEC+ meeting scheduled for Thursday. There's growing consensus, as per news reports in the past two days, that a compromise on 2024 output levels is within reach. However, it seems the most probable outcome will just be continuation of existing production cuts, rather than any new, drastic changes.

This outlook, predominantly unaltered barring any unexpected deepening of cuts, steers towards bearish sentiment for oil prices in the near term. A key factor influencing this view is rising inventory levels in US. Concurrently, economic growth in China, a major player in global oil demand, remains tepid. While there have been some positive signs in China, they are not robust enough to shift the demand dynamics significantly.

Another critical element in this equation is Saudi Arabia's decision regarding its additional voluntary cut of 1 million barrels per day, which is nearing its expiry at the end of December.

From a technical standpoint, near term outlook in WTI crude oil stays bearish with 79.98 resistance holds. Current fall from 95.50 if expected to extend through 72.56 to 63.37/66.94 support zone. But strong support would likely be seen to to bring rebound. Overall, range trading should continue for the medium term above 63.67, barring another significant developments.

Focus Shifts to RBNZ, Inflation Reports from US, Eurozone, Australia, and China PMIs

RBNZ is widely expected to hold the Official Cash Rate steady at 5.50% on Wednesday. Accompanying this decision will be the quarterly Monetary Policy Statement, which will include new economic forecasts. Despite some speculation about potential rate cuts in 2024, RBNZ's projections may not strongly reflect this, especially considering the recent resurgence in energy prices. This could imply that the RBNZ may either need to hike rates further or maintain the current levels for an extended period, with the latter seeming more likely. In terms of central bank activities, Fed is also set to release its Beige Book economic report, offering insights into the economic conditions across various regions.

On the data front, key inflation figures are due from several major economies. US will release its PCE and core PCE price indexes, while Eurozone will publish its CPI flash data. Australia's monthly CPI data is also awaited. These inflation reports are crucial for central banks like Fed and ECB, as they could influence the timing and pace of upcoming rate cuts and pace of policy loosening next year. Although Australia's more critical quarterly CPI data will come in January, the upcoming monthly figures will still play a role in shaping market expectations regarding RBA's next moves.

Canada's employment data is another significant release that could impact the forex markets. Particularly, following a strong market response to Canada's recent robust retail sales data, another set of positive employment figures could potentially trigger a notably rally in Loonie.

Lastly, economic indicators from China, including the official and Caixin PMI reports, will be closely watched. These reports are vital in supporting the recent rally in commodity prices, as they provide insights into the Chinese economy's health, a major player in global commodity demand.

Here are some highlights for the week:

- Monday: Japan corporate service price index; US new home sales.

- Tuesday: Australia retail sales; Germany Gfk consumer climate; Eurozone M3 money supply; US house price index, consumer confidence.

- Wednesday: Australia CPI; RBNZ rate decision; Germany CPI flash; UK M4 money supply, mortgage approvals; Canada current account; US GDP revision, goods trade balance, Fed's Beige Book report.

- Thursday: Japan industrial production, retail sales, consumer confidence, housing starts; New Zealand ANZ business confidence; China official PMIs; Germany retail sales; Swiss KOF economic barometer, retail sales; Eurozone unemployment rate, CPI flash; US personal income an spending, PCE price index, Chicago PMI, pending home sales.

- Friday: Japan unemployment rate, capital spending, PMI manufacturing final; China Caixin PMI manufacturing; Swiss GDP, PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final; Canada employment; US ISM manufacturing.

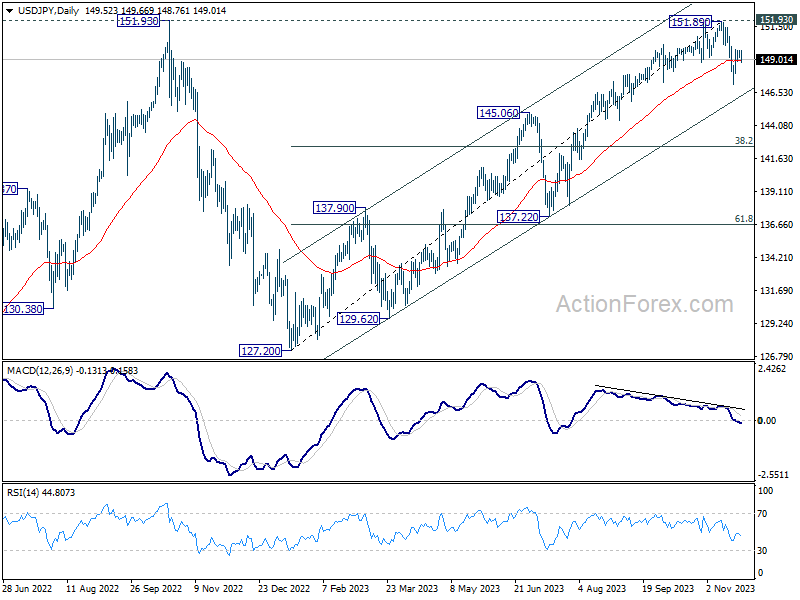

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.19; (P) 149.45; (R1) 149.70; More...

USD/JPY dips notably today but stays above 148.57 minor support. Intraday bias remains neutral at this point. Risk stays on the downside as long as 55 4H EMA (now at 149.55) holds. Break of 148.57 minor support will turn bias to the downside the resume the fall from 151.89 through 147.14 support. However sustained break of 55 4H EMA will revive near term bullishness, and target a retest on 151.89/93 resistance zone

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | 2.30% | 2.10% | 2.10% | |

| 15:00 | USD | New Home Sales M/M Oct | 725K | 759K |

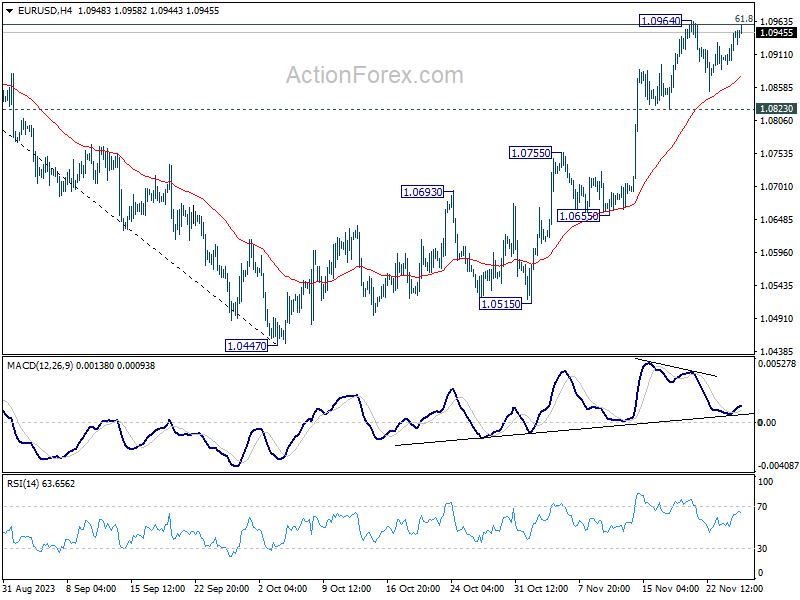

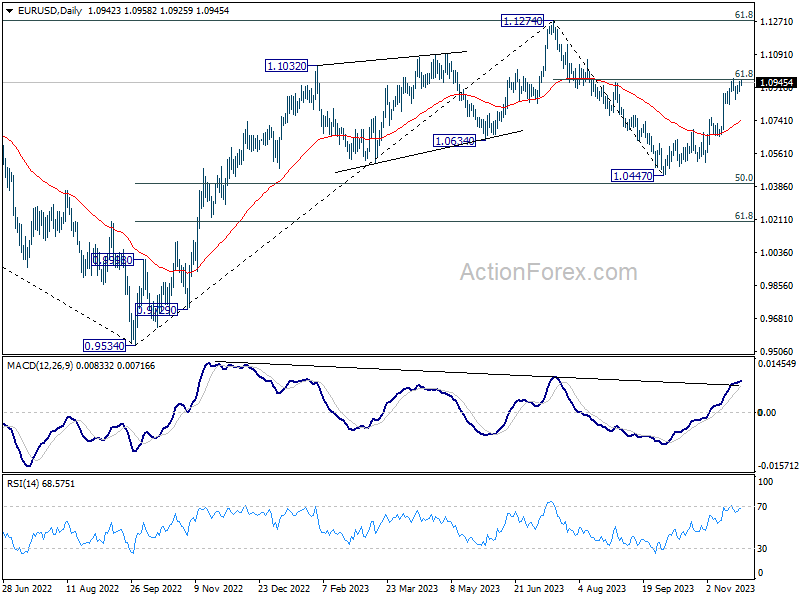

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0907; (P) 1.0928; (R1) 1.0961; More...

Intraday bias in EUR/USD remains neutral for the moment, as it's still capped below 1.0964 resistance. Further rally is in favor as long as 1.0823 support holds. Sustained break of 61.8% retracement of 1.1274 to 1.0447 at 1.0958 will resume the rise from 1.0447 to retest 1.1274 high. However, firm break of 1.0823 will indicate short term topping, and turn bias back to the downside for deeper decline.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

BoJ’s Ueda repeats uncertainty on stably achieving inflation target

In today's address to the parliament, BoJ Governor Kazuo Ueda provided note that the economy is "recovering moderately," which is further evidenced by the narrowing of the output gap to "near zero".

Ueda also highlighted "We're seeing some positive signs in wages and inflation". However, he tempered this optimism by acknowledging the "high uncertainty on whether this cycle will strengthen"

A key point in Ueda's commentary was BoJ's stance on inflation. Despite the positive signs, he stated that the central bank cannot yet assert with confidence that inflation will sustainably and stably achieve its 2% target.

CHF/JPY Technical: Bearish Elements Sighted Below the All-time High of 170.54

- Bearish readings seen in the daily and hourly RSI momentum indicators have reinforced the weakening medium-term and short-term impulsive up moves of CHF/JPY.

- Watch the key short-term resistance at 169.65 for CHF/JPY.

The major uptrend phase of the CHF/JPY has started to show signs of bullish exhaustion at this juncture which increases the risk of a multi-week corrective decline to retest its 50-day moving and the median line of a major ascending channel in place since 13 January 2023 low, acting at a support zone of 166.55/165.10.

Daily RSI has broken below its former ascending support

Fig 1: CHF/JPY major & medium-term trends as of 27 Nov 2023 (Source: TradingView, click to enlarge chart)

The medium-term bullish momentum of CHF/JPY from the 3 October 2023 low of 160.00 has started to dissipate where the daily RSI momentum indicator has staged a recent bearish breakdown on 20 November and retested its former parallel support at the 60 level.

Watch the key short-term resistance at 169.65

Fig 2: CHF/JPY minor short-term trend as of 27 Nov 2023 (Source: TradingView, click to enlarge chart)

In the shorter time frame as seen on the 1-hour chart, the price actions of CHF/JPY have started to oscillate within an impending minor descending channel from its recent all-time high print of 170.54 on 16 November 2023.

Also, the hourly RSI momentum indicator has flashed out a bearish divergence condition at its overbought region.

All in all, these observations have advocated the start of a potential multi-week corrective decline scenario for CHF/JPY.

If the 169.65 key short-term pivotal resistance is not surpassed to the upside, the CHF/JPY cross pair may see a slide to retest the near-term support of 168.00 (also the 20-day moving average), and below it exposes the next intermediate supports at 166.55 and 165.90 next (also the 50-day moving average and the lower boundary of the minor descending channel).

However, a clearance above 169.65 invalidates the bearish scenario for a retest on the 170.50 major resistance.

Dollar Stays in the Sefensive

Markets

US markets on Friday and after Thanksgiving joined the rebound in yields in Europe on Thursday. Investors apparently found that enough frontloading on (Fed & ECB) rate cuts had been discounted. Eco data didn’t provide much counterarguments. German IFO business confidence rose slightly (87.3 from 86.9), the third consecutive gain. Still, IFO concluded the economy is stabilizing at a low level. US November PMI’s showed a similar picture. The composite index suggests marginal growth (50.7, unchanged). Services improved slightly (50.8 from 50.6), but manufacturing dropped back in contraction territory. Both manufacturing and services cut jobs. On prices, S&P mentions that selling prices ticked up slightly, but price rises remained subdued relative to the average over the last three years and that it was consistent with a rate of increase close to the Fed’s 2% target. Still this assessment didn’t alter the turn north in yields. US yields added between 6.26 bps (10-y) and 4.9 bps (2-y). German yields gained between 2.0 bps (5-y) and 3.1 bps (30-y). For now, the test of the 4.34% area and the 2.50% in respectively the 10-y US (4.49%) and German (2.64%) yields is rejected. Equities didn’t show big directional moves, but mostly held their composure (Eurostoxx50 +0.25%; S&P 500 +0.06%). The dollar couldn’t build on the bottoming out process that tentatively started earlier last week. DXY dropped back from the 103.80 area to close near 103.40. EUR/USD finished the week near 1.0940. USD/JPY lost marginally (149.44), but stays away from recent highs just below 152. Sterling was in good shape. After a better than expected PMI on Thursday, a bigger than expected improvement in GfK consumer sentiment trigger a further GBP rebound. EUR/GBP dropped below 0.87 (close 0.868).

This morning, Asian equities mostly trade with losses of 0.5%-1.0%. Profits at China industrial companies eased substantially to 2.7% Y/Y in October from 11.9% in September, suggesting an underlying deflationary momentum and sluggish growth. US yields still gain marginally. The dollar stays in the defensive (DXY 103.30; USD/JPY 148.95). There are only second tier eco data today. ECB’s Lagarde speaks in the EU Parliament. The US Treasury sells $54 bln 2-y Notes and $55 bln 5-y notes. Later this week, US consumer confidence (Conference Board) is scheduled for release on Tuesday. German, Spanish and Belgian inflation data on Wednesday will give a preview for the EMU release expected one day the later. On Thursday, markets will also keep a close look at the US October PCE deflators. On Friday, the US manufacturing ISM index will be published, but the payrolls will only be released December 8. We look out whether the bottoming out process in core yields is confirmed. The dollar looks fragile with EUR/USD 1.0960 at risk. A drop of USD/JPY below 148.40 might be another sign of the greenback losing some further momentum.

News & Views

Rating agency Moody’s raised the outlook on the Czech Republic’s Aa3 rating from negative to stable. The decision is primarily driven by the significant reduction in risks related to Russian gas supply which were the key driver of the negative outlook in August 2022. The Czech Republic became independent from Russian gas earlier this year with gas demand from firms and households structurally decreasing as the country achieved a full energy substitution by alternative sources. The stable outlook is also supported by the fiscal consolidation which will stabilize the debt burden and by the local economy’s limited exposure to the risk of economic scarring due to structurally higher energy prices. CZK is untouched by the news this morning with a generally stronger euro lifting EUR/CZK away from the 24.30/40 support area.

The UK House of Lords economic affairs committee released an audit report on the Bank of England. It called for a significant reform of the UK central bank’s internal culture, governance and appointment process after the BoE like most other central banks underestimated inflation risks in 2020 and 2021 resulting in a delayed response. Inadequate forecasting models and all to similar profiles of BoE members are amongst topics raised which need changing. The report recommended that parliament should conduct an “overarching review” of the BoE’s remit, performance and operations every five years. The BoE will respond formally in due course.

USD Slips Below 200-DMA Despite Rebound in Yields

Last week ended on a positive note where the US equities advanced to fresh highs since summer on a holiday shortened trading week. The S&P500 gained for the 4th consecutive week and closed the week near 4560, the rate-sensitive and technology heavy Nasdaq 100 extended gains beyond the summer peak, and hit an almost 2-year high, while the VIX index, which is known as Wall Street’s fear gauge, or the volatility index, slumped to the lowest levels since January 2020. The belief that the Federal Reserve (Fed) is done hiking the interest rates, and the rapidly falling US long-term yields are at the source of this optimism – especially after the latest CPI update in the US printed a softer-than-expected number, suggesting that inflation in the US fell to 3.2% last month. This week, investors will find out if the Fed’s favourite inflation gauge, the PCE index, tells the same story. The PCE index is expected to have fallen from 3.4% to 3.1% in October, and core PCE may have eased from 3.7% to 3.5% during the same month. Anything less than soothing could lead to some more correction in the US long-term yields. The 10-year yield jumped to 4.50% early Monday, though the positive pressure slowed above 4.50%.

News that the Black Friday spending jumped 7.5% this year to hit a record high of $9.8 billion certainly reminds investors that consumer spending in the US remains strong. The latter gives a strong support to the US economy, which in return gives a solid confidence to the Fed that keeping the rates high for long is not necessarily a bad idea. Today, the sales continue with Cyber Monday deals.

Yet the holiday shoppers’ enthusiasm is less visible on the financial markets this Monday. The US futures are down, along with their Asian peers on the back of a rebound in US yields, the nearly 8% slump in Chinese industrial profits in October and news that children in China are suffering from respiratory infections – which spurs speculation that it could be a new strain of Covid. Chinese authorities say that it’s simply a mix of known respiratory diseases. But you know, once bitten, twice shy.

The Dollar Index extends losses below 200-DMA

Friday’s rebound in the US yields couldn’t give a bullish shift to the US dollar. The dollar index slipped below its 200-DMA, closed the week below this level and is under renewed selling pressure this morning despite positive pressure on the yields. The broad-based dollar weakness helps the EURUSD extend gains to 1.0950, with solid resistance seen into the 1.10 level given weaker growth perspectives for the European economies compared to the US in the coming months. Cable trades past the 1.26 level, while the USDJPY remains offered near the 50-DMA, near the 149 level. The yen is benefiting from rumours that a growing number of institutional players are turning long yen on expectation that the Bank of Japan (BoJ) will one day normalize its rate policy. Every day that goes by brings the BoJ closer to normalization and there is a great upside potential for the yen at the current levels – hence a great downside potential for the USDJPY. Yet the right time for getting long yen is anybody’s guess. What we know however is that the upside potential in the USDJPY is certainly limited above the 150 level.

In commodities, gold pulled out offers at the $2000 per ounce and is trading above this level this morning. The softer dollar gives support to the yellow metal, yet the rebound in the US long-term yields, news of a potential extension of cease fire in Gaza beyond today and the fact that the precious metal is worth just shy of its ATH levels hint at a limited upside potential at the current levels.

In energy, appetite in oil is nowhere to be found this morning. The barrel of US crude trades below the $75pb level despite news that OPEC+ is nearing a resolution of the disagreement on output quotas, which led to the group delaying a crucial meeting last weekend. Officials said that discussions with the African nations over the production quotas continue and agreement is within reach – in which case Saudi will likely announce at least 1mbpd extra supply cut to prevent oil bulls from leaving the battlefield. But oil traders need more effort to reverse the selloff in oil prices. The barrel of US crude sees strong resistance around the 200-DMA, near the $78pb level, and the price should rally past the $81pb level for the current bearish trend to reverse.

Israel and Hamas May Extend Truce

Market movers today

A quiet start to an otherwise interesting data week. Norwegian retail sales and US new home sales for October will be released today.

The ECB's Lagarde will give a speech in the afternoon.

Later in the week, the most important release will be the euro area flash HICP on Thursday, we expect further cooling in both headline (2.7%; Oct 2.9%) and core (3.9%; Oct 4.2%) inflation terms. In the US, October Personal Consumption Expenditures (PCE) and November ISM Manufacturing index will be released on Thursday and Friday, respectively. In China, both official NBS and Caixin manufacturing PMIs are due for release (Thursday and Friday, respectively).

The Reserve Bank of New Zealand (RBNZ) will be the only G10 central bank having a monetary policy meeting this week (Wednesday). We expect an unchanged rate decision.

OPEC+ will meet on Thursday and the UN Climate summit COP28 begins on the same day.

The 60 second overview

Market wrap: US bond yields have continued Friday's move higher in Asian trading this morning while equity futures are lower. EUR/USD continues to creep higher.

Israel and Hamas may extend the truce beyond Monday if they can agree on more hostage releases. US President Biden said he hoped the truce could go on as long as hostages were released. Hamas said it would extend the truce if serious efforts were made to increase the number of Palestinians released by Israel. Prime Minister of Israel Benjamin Netanyahu said on Sunday he would welcome extending the truce if it meant that on every day 10 hostages would be released adding that after the truce they would return with full force to achieve the goal of eliminating Hamas.

US released PMIs on Friday for November still pointing to growth below trend but not yet at recession levels. Manufacturing PMI declined from 50.0 to 49.4 (consensus 49.9) while service PMI rose slightly from 50.6 to 50.8 (consensus 50.3). It left the composite PMI unchanged at 50.7 (long term average 54.1).

Chinese government agencies unveiled 25 measures to support financing for the private sector in yet another move to underpin private sector development. It continues the charm offensive towards the private sector that has taken place over the past year in efforts to rebuild confidence and highlight the importance of the private sector.

US Black Friday online sales were up 7.5% compared to last year as consumers were chasing deals.

Equities: Equities were modestly higher on Friday, thereby locking in solid gains for another week. Both US and European markets were about 1% higher for the week. This takes most regions back to late summer-highs and we find this motivated. Gains have been broad-based, with very little distinction between value/growth, cyclicals/defensives or small/large caps. This was also the case on Friday. Unlike the past few weeks, the increase in equities was not been driven by falling yields. In fact, US and European yields have even risen some 10bp for the week. Bond vol coming down is enough to drive equities and will continue to do so, in our view. Asian markets and US futures are lower again this morning.

FI: Last week was eventful given the Dutch election and the surprise victory by the Freedom Party led by Geert Wilders and the closure of the German inflation liked programme by the German Debt Agency (Finanzagentur). Furthermore, the uncertainty surrounding the German fiscal situation continues. Last week the German government suspended the debt brake for 2023 and we expect more news on the budget for 2024 in the coming weeks. Looking at the move in the bond market, yields rose modestly during the week in US and Europe.

FX: EUR/USD rose above the 1.09 mark, while the USD/JPY remains just below 150. EUR/GBP declined below 0.87, primarily due to better-than-expected UK PMIs. EUR/SEK remains slightly above 11.40 after the Riksbank decision, while the EUR/NOK is hovering around 11.70.

Credit: Credit spreads as measured by CDS indices were generally tighter last week as sentiment was buoyed by hopes of a soft landing. iTraxx Main closed at 68bp which was 2bp tighter during the week, while Xover was 12bp tighter at 375bp.

Nordic macro

In Sweden the Financial Market Statistics is released today; household lending growth will the most interesting part of the statistics. Norway releases retail sales for October.

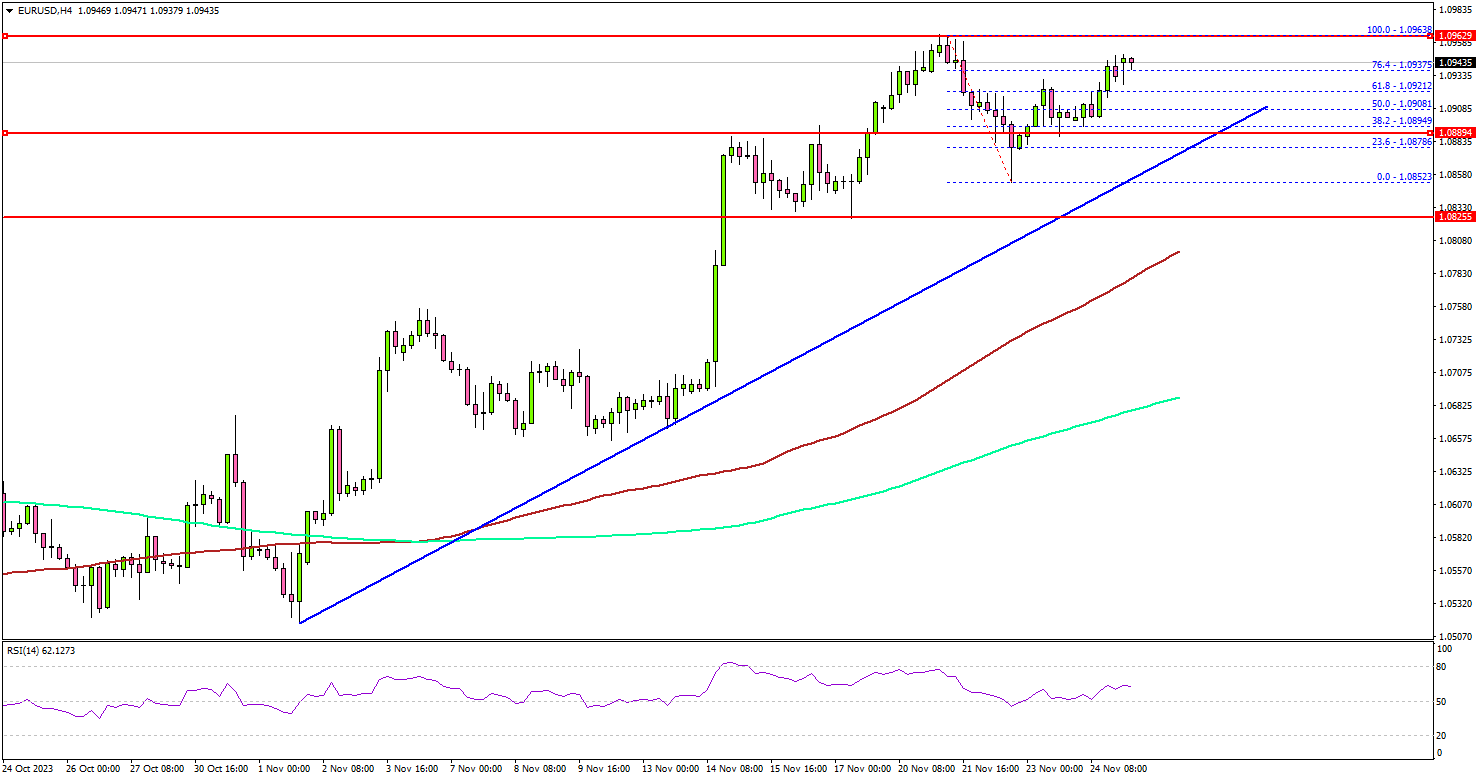

EUR/USD Remains In Uptrend, Gold Rallies Again

Key Highlights

- EUR/USD is still trading in a positive zone above 1.0800.

- A connecting bullish trend line is forming with support at 1.0895 on the 4-hour chart.

- Gold prices rallied again and climbed above the $2,000 resistance.

- Crude oil prices are struggling and might drop below the $73.20 support.

EUR/USD Technical Analysis

The Euro started a steady increase above the 1.0850 level against the US dollar. EUR/USD even climbed toward 1.0960 before there was a downside correction.

Looking at the 4-hour chart, the pair corrected lower and tested the 1.0850 support. The bulls remained active above 1.0850 and the pair started a fresh increase. The pair settled above the 1.0880 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

The pair is now trading above the 1.0920 level with a positive angle. Immediate resistance is near the 1.0960 level. The next key resistance is near the 1.1000 level.

The main resistance is now near the 1.1050 level. A close above the 1.1050 zone could open the doors for more upsides. The next stop for the bulls might be 1.1200.

If not, the pair might start a fresh decline below the 1.0920 support. The first major support is now forming near 1.0900. There is also a connecting bullish trend line forming with support at 1.0895 on the same chart.

The next key support sits at 1.0850, below which the pair could test the 1.0800 pivot level in the near term.

Looking at Gold, there were strong bullish moves above $2,000 and the bulls might now aim for more gains in the near term.

Economic Releases

- US New Home Sales for Oct 2023 (MoM) – Forecast -0.5% versus 12.3% previous.