Sample Category Title

AUD/USD Weekly Report

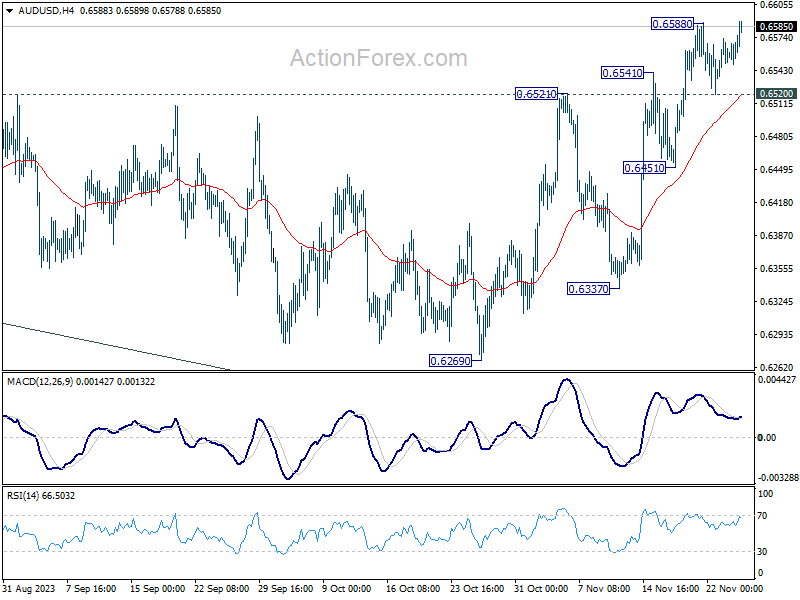

AUD/USD retreated after surging to 0.6588 last week. But late breach of this resistance indicates that recent rally is resuming. Initial bias is back on the upside this week. Current rise from 0.6269 should target falling channel resistance (now at 0.6670) next. For now, outlook will remain bullish as long as 0.6520 support holds, in case of retreat.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of the corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

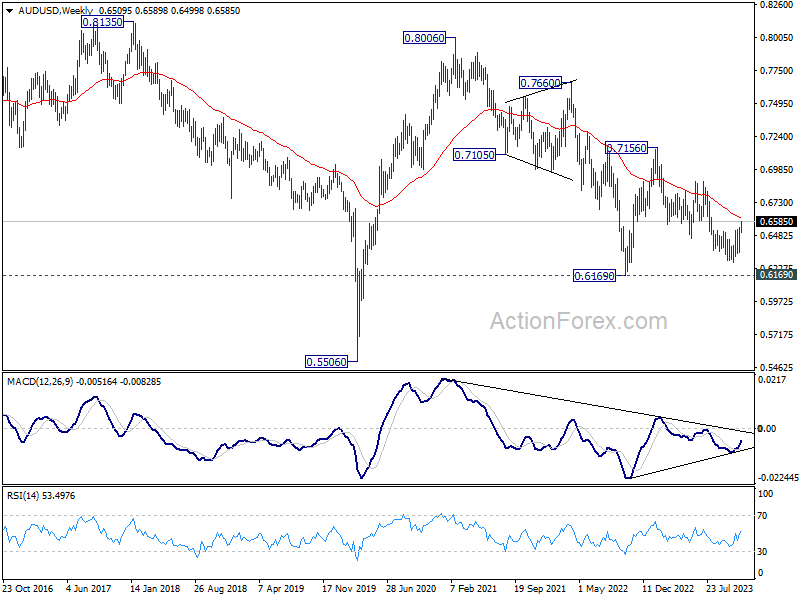

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506(2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen the second leg of the pattern. Hence, in case of deeper decline, downside strong support should emerge above 0.5506 to bring reversal.

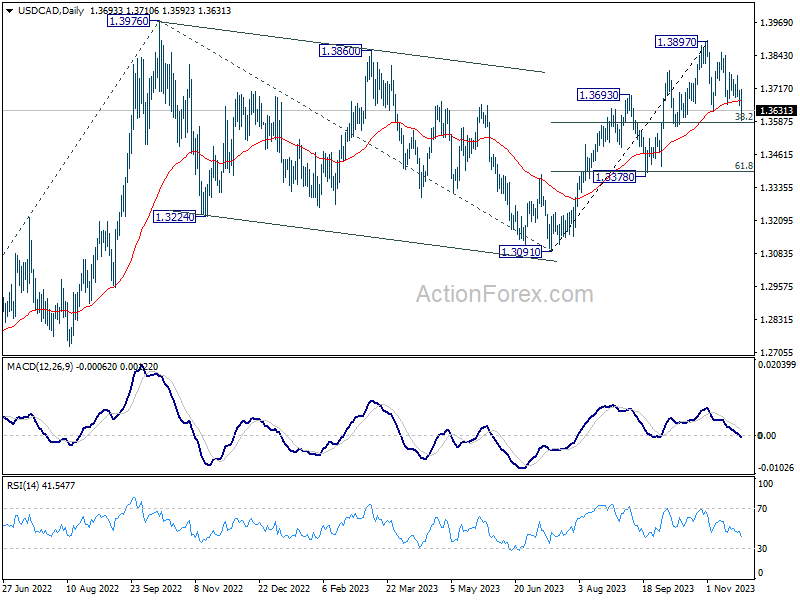

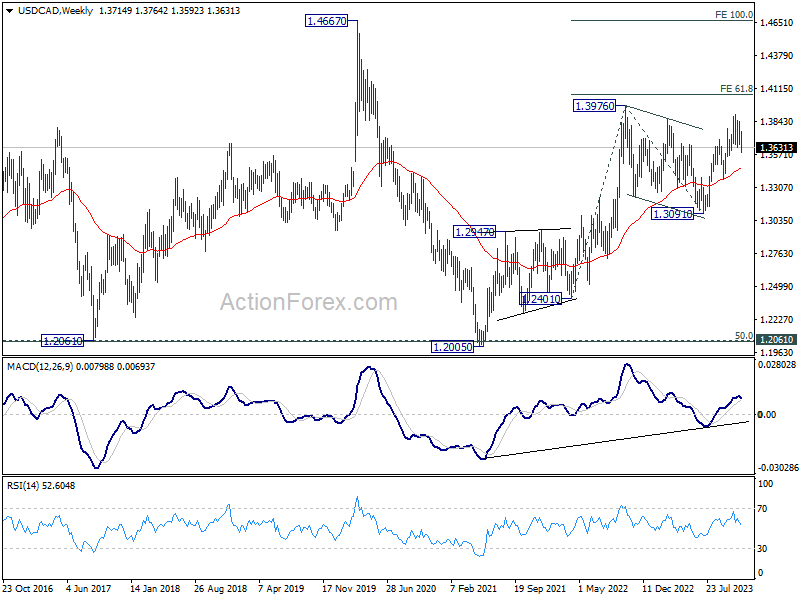

USD/CAD Weekly Outlook

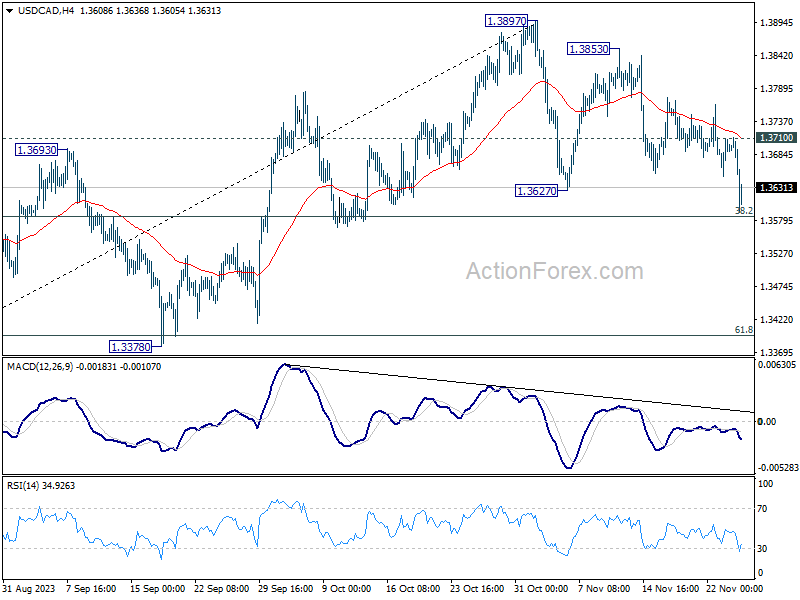

USD/CAD's decline from 1.3897 resumed last week and dipped to as low as 1.3592. For now, strong support is still expected from 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to contain downside and bring rebound. Break of 1.3711 minor resistance will turn bias back to the upside for retesting 1.3897. However, sustained break of 1.3589 will indicate that deeper correction is underway to 61.8% retracement at 1.3399 next.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern only, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as 55 M EMA (now at 1.3126) holds.

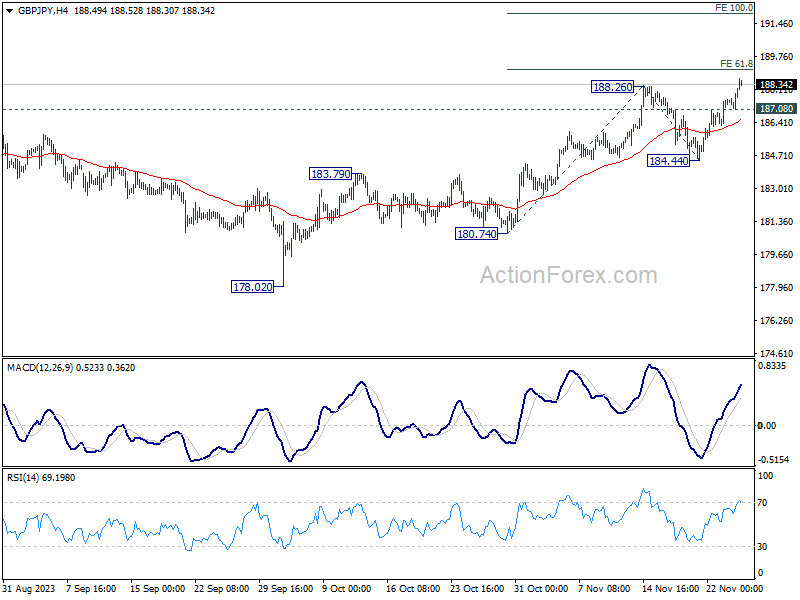

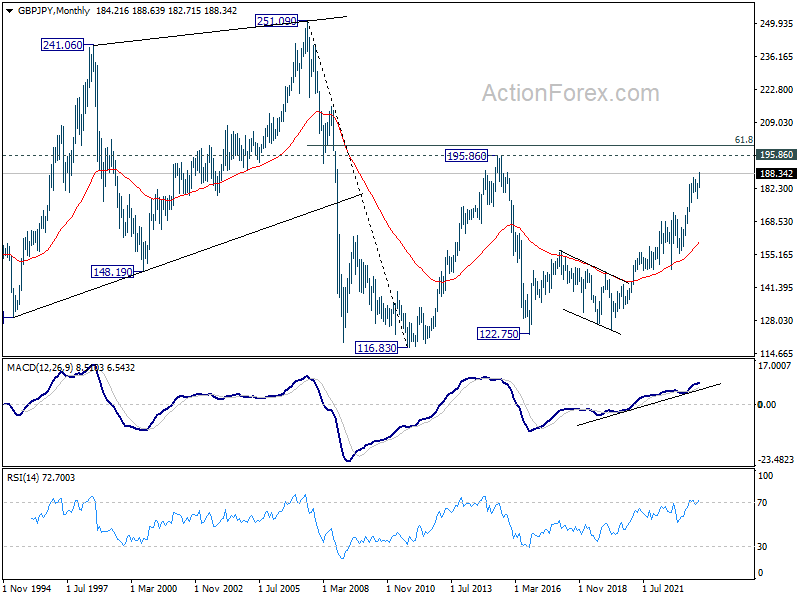

GBP/JPY Weekly Outlook

GBP/JPY's up trend resumed last week by breaking through 188.26. Initial bias stays on the upside this week for 61.8% projection of 180.74 to 188.26 from 184.44 at 189.08 first. Break will target 100% projection at 191.96 next. On the downside, below 187.08 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

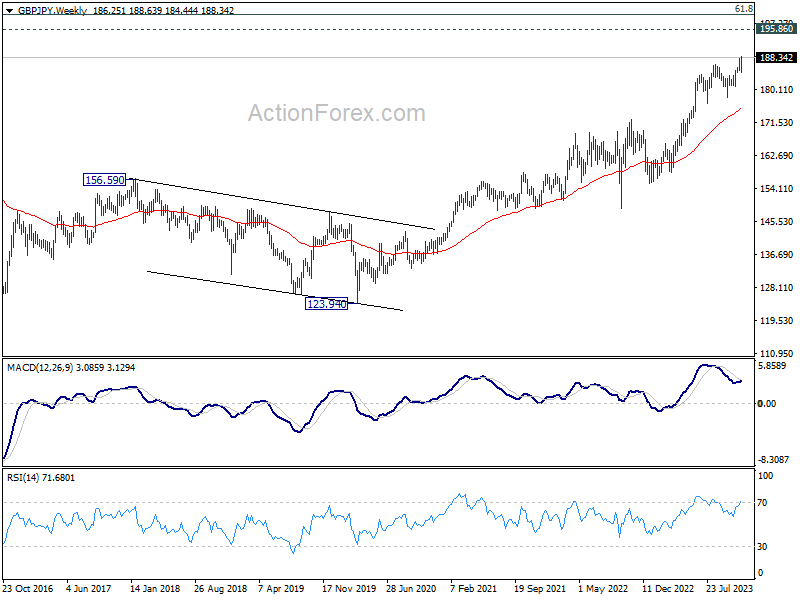

In the bigger picture, as long as 184.44 support holds, larger up trend from 123.94 (202 low) should still be in progress, next target is 195.86 (2015 high). However, firm break of 184.44 will now argue that a medium term top is formed, possibly in bearish divergence condition in D MACD, and bring deeper fall back to 178.02 support.

In the longer term picture, rise from 122.75 (2016 low) in still in progress but started losing upside momentum as seen in W MACD. Further rise will remain in favor, though, as long as 178.02 support holds, to retest 195.86 (2015 high).

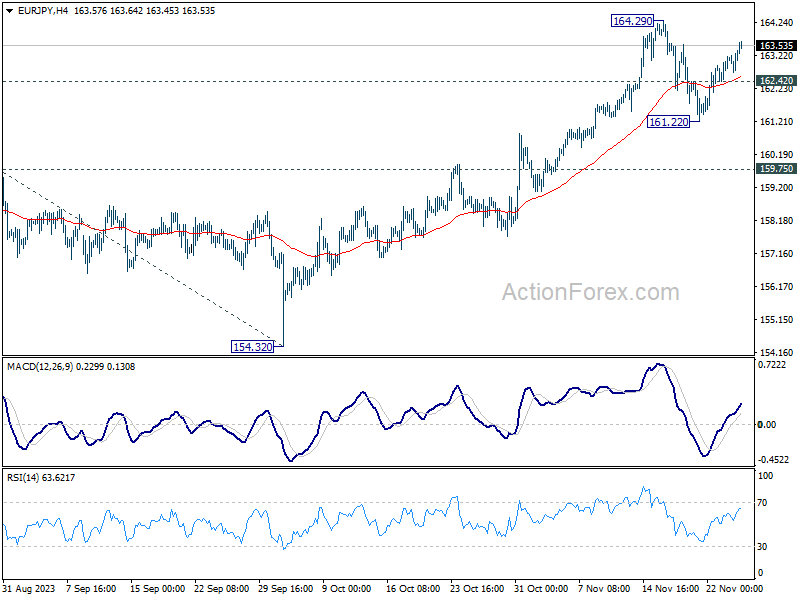

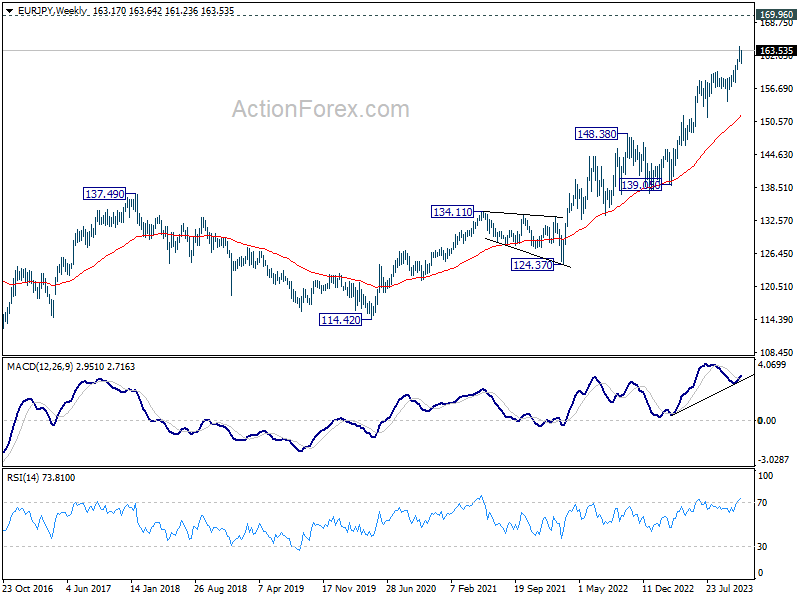

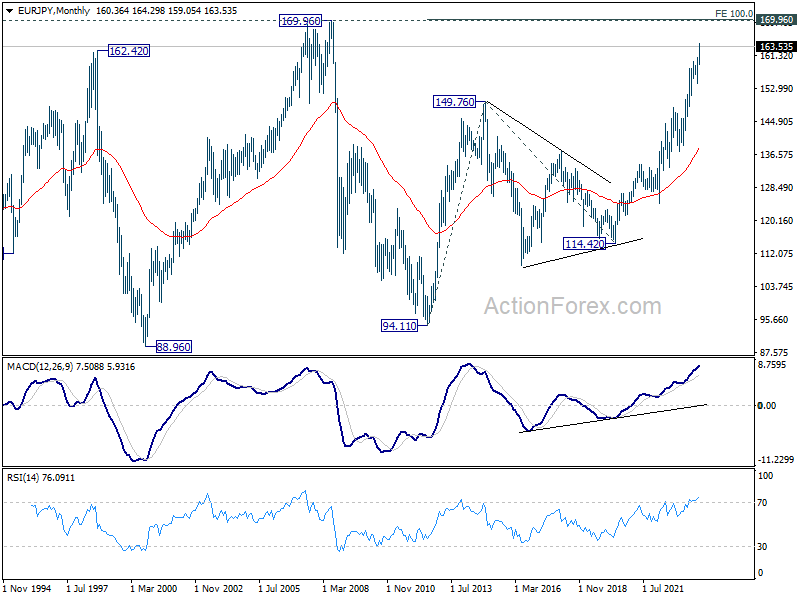

EUR/JPY Weekly Outlook

EUR/JPY's retreat from 164.29 finished at 161.22 and recovered since then. Initial bias stays mildly on the upside this week for retesting 164.29 first. Firm break there will resume larger up trend. On the downside, however, break of 162.42 minor support will turn bias back to the downside, to extend the corrective pattern from 164.29 with another falling leg.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 169.96 (2008 high). On the downside, break of 159.75 resistance turned support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high).

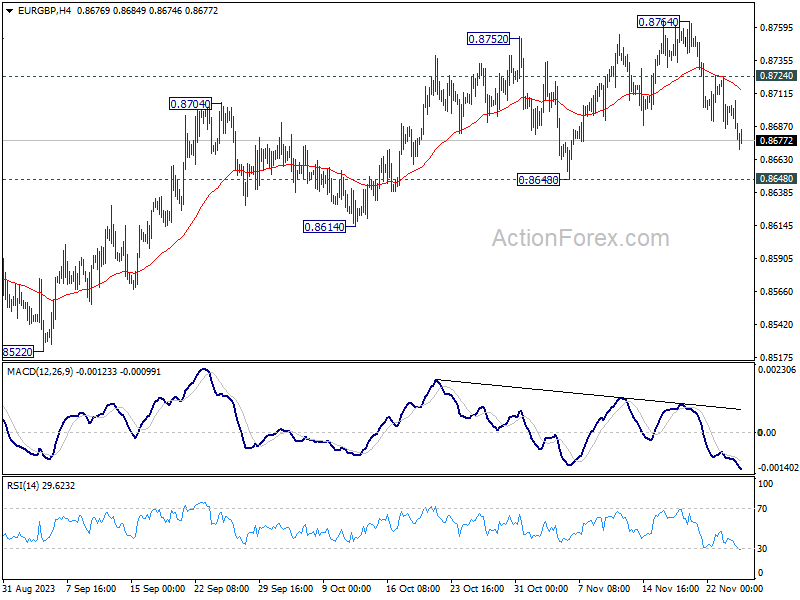

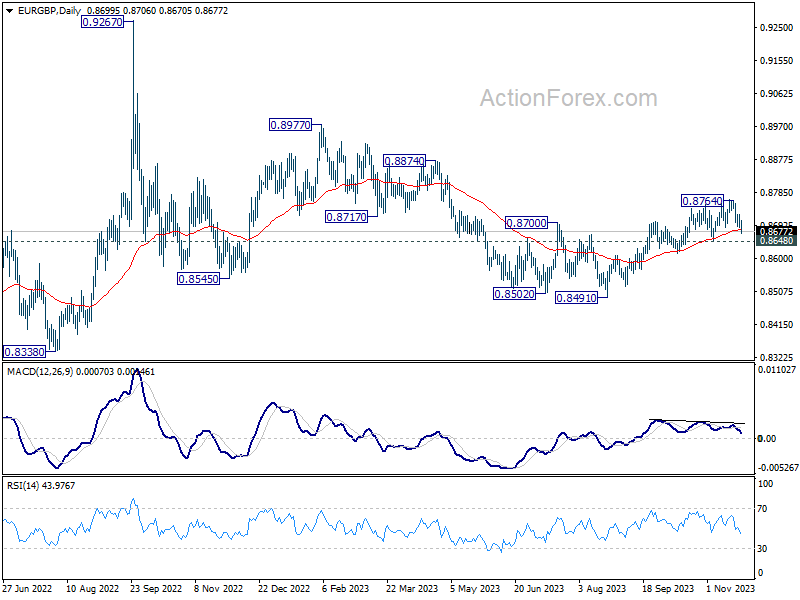

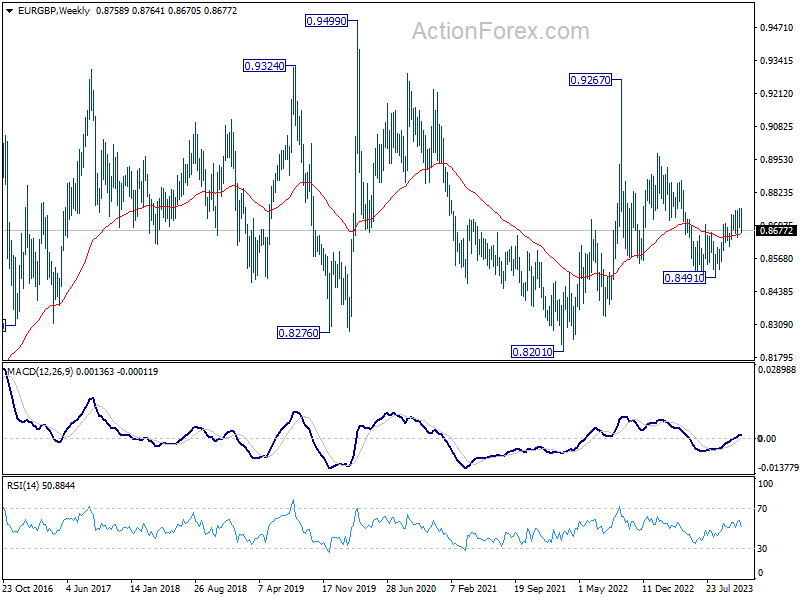

EUR/GBP Weekly Outlook

EUR/GBP's extended fall last week indicates short term topping at 0.8764, on bearish divergence condition in 4H MACD. Initial bias is now on the downside this week for 0.8648 support. Decisive break there will argue that whole rise from 0.8491 has completed and turn near term outlook bearish. Nevertheless, break of 0.8724 minor resistance will retain near term bullishness and bring retest of 0.8764.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. However, firm break of 0.8648 support will dampen this view, and open up the case for another medium term decline through 0.8941.

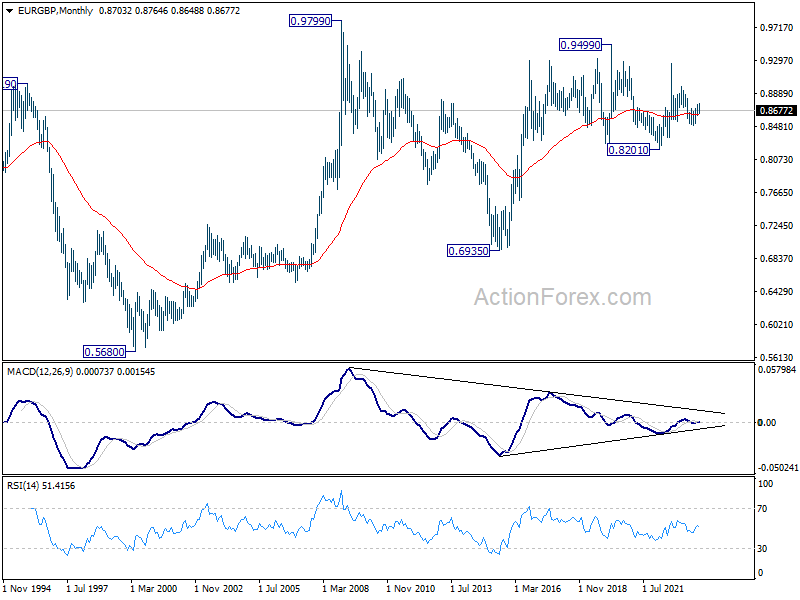

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to resume at a later stage, to 0.9799 (2009 high).

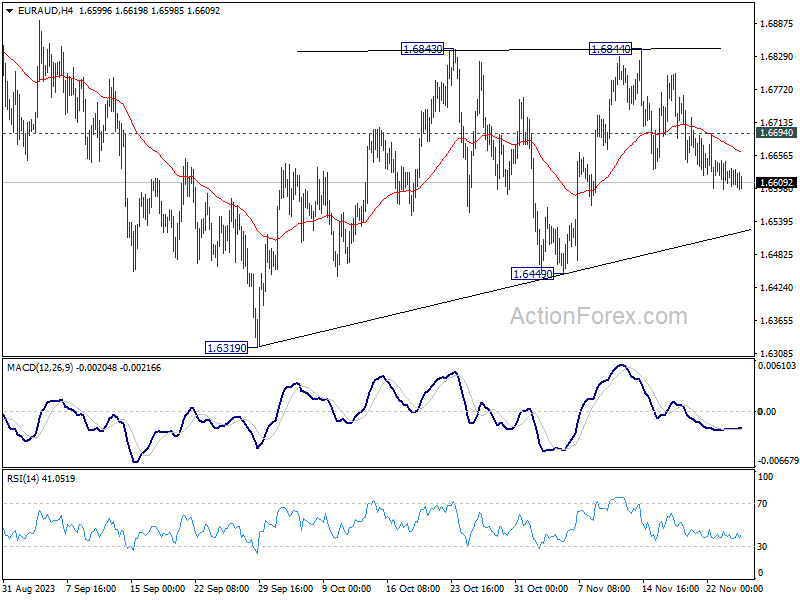

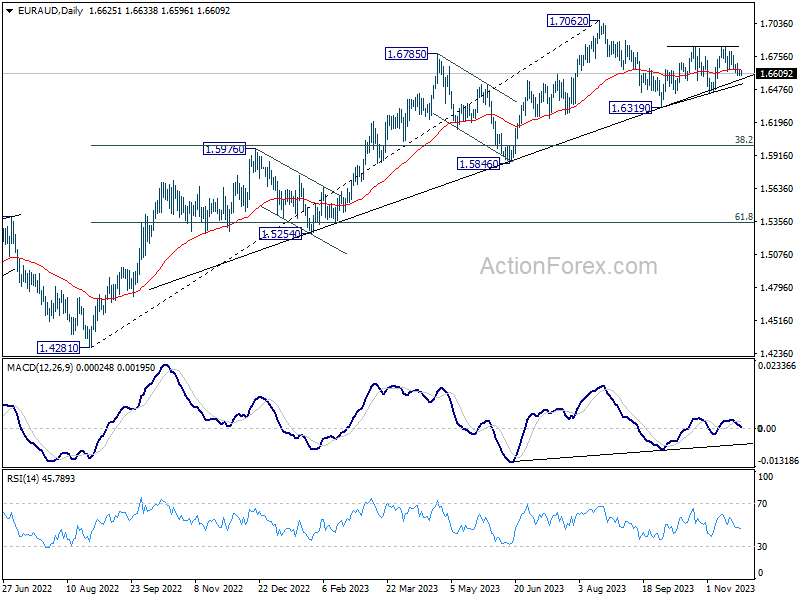

EUR/AUD Weekly Outlook

EUR/AUD's fall from 1.6844 extended lower last week and the development argues that rebound from 1.6449 has completed already. Further decline is now expected this week as long as 1.6694 resistance holds. Firm break of 1.6449 support will argue that the pattern from 1.6319 has completed at 1.6844 as a corrective move, and fall from 1.7062 is ready to resume through 1.6319. On the upside, above 1.6694 minor resistance will turn intraday bias neutral first.

In the bigger picture, while 1.7062 is a medium term top, there is no clear sign of trend reversal as EUR/AUD continues to draw strong support from the medium term trend line. Break of 1.7062 will resume the larger up trend from 1.4281 (2022 low) to 1.7691 fibonacci level. Nevertheless, break of 1.6449 support will argue that deeper correction is underway to 38.2% retracement of 1.4281 to 1.7062 at 1.6000.

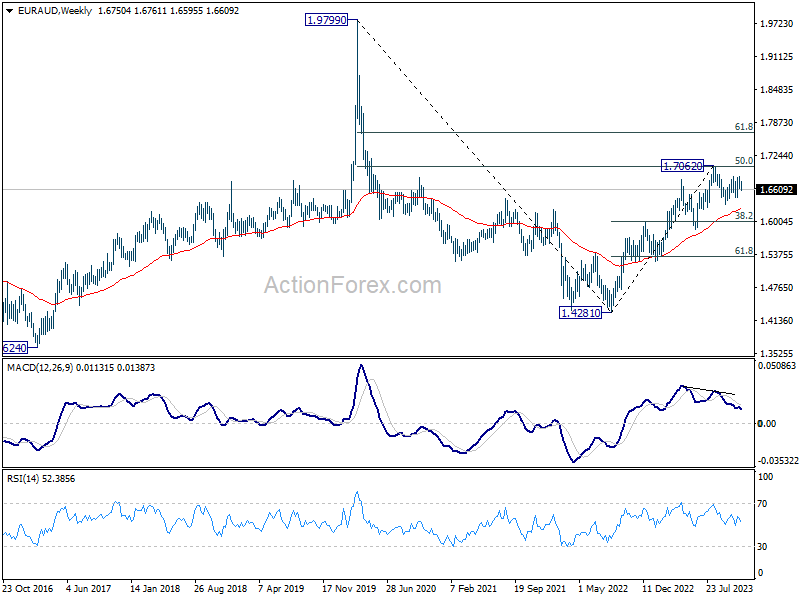

In the longer term picture, loss of upside momentum as seen in 55 W MACD at this stage argues that rise from 1.4281 (2022 low) is more likely a corrective move. Further rise could still be seen as long as 1.5846 support holds. But upside will likely be limited by 61.8% retracement of 1.9799 to 1.4281 at 1.7691. Firm break of 1.5846 support will argue that the rise has completed, and another medium term down leg has started.

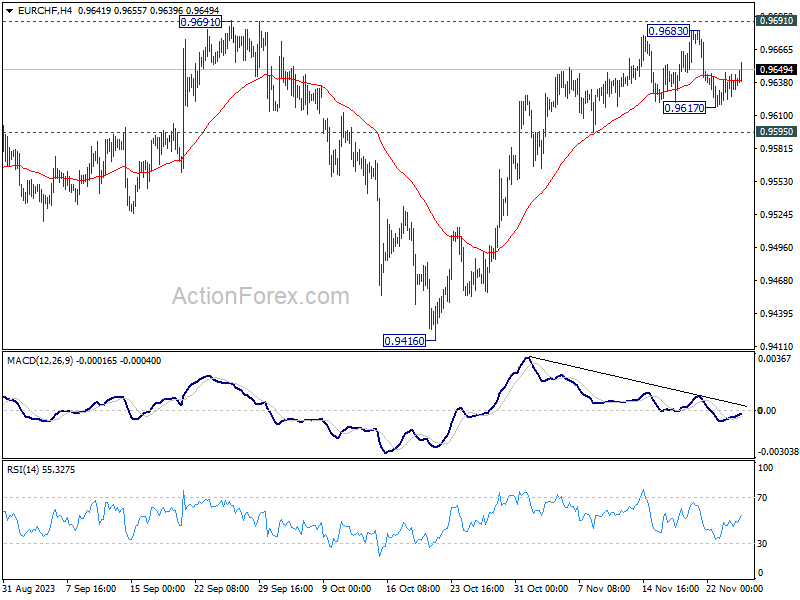

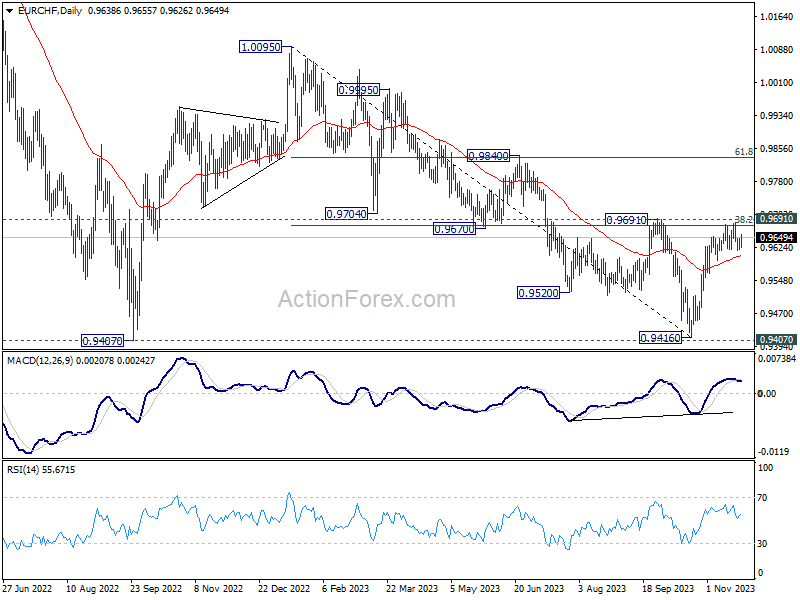

EUR/CHF Weekly Outlook

EUR/CHF failed to break through 0.9691 resistance last week and retreated. But it then recovered after brief dip to 0.9617. Initial bias stays neutral this week for more consolidations. Further rally is still expected and decisive break of 0.9691 resistance will carry larger bullish implication, and target 0.9840 resistance next. However, break of 0.9595 support will indicate short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, fall from 1.0095 (2023 high) might have completed at 0.9416, just ahead of 0.9407 support (2022 low). Sustained break of 0.9691 cluster resistance (38.2% retracement of 1.0095 to 0.9416 at 0.9675) will pave the way to 61.8% retracement at 0.9836 and above. However, rejection by 0.9691 will maintain medium term bearishness for another test on 0.9407 at least.

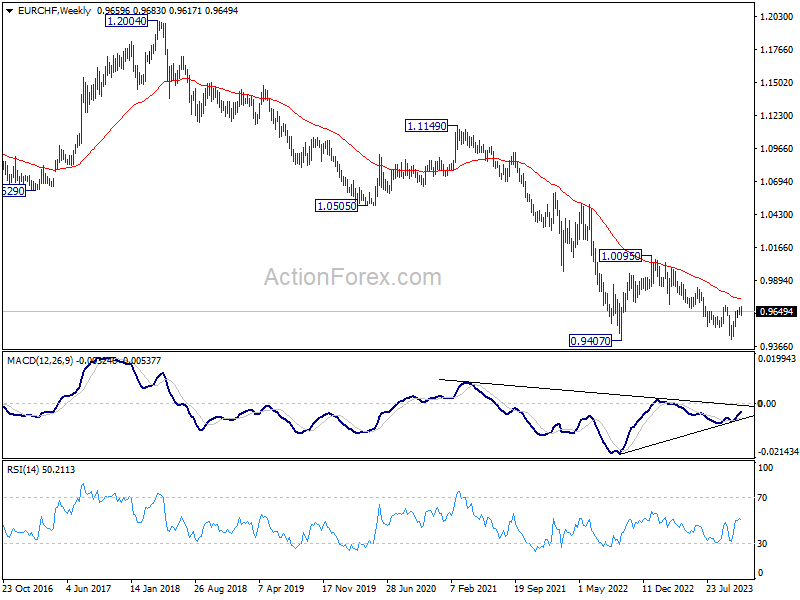

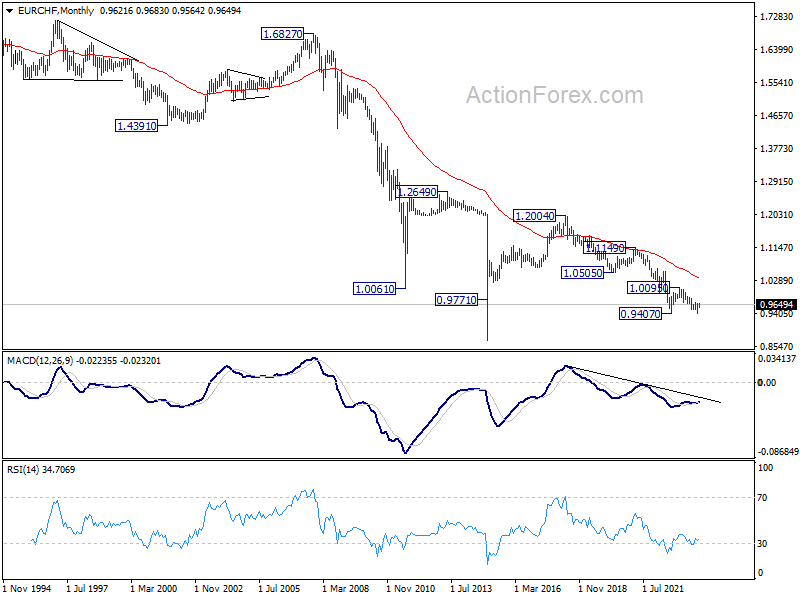

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0341). Price actions from 0.9407 are viewed as a three-wave consolidation pattern first. Larger down trend from 1.2004 (2018 high) might still resume through 0.9407 at a later stage. Break of 1.0095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

The Weekly Bottom Line: Looking for Signs of Slowing

U.S. Highlights

- Minutes from the Federal Open Market Committee (FOMC) meeting reinforced the Fed’s messaging that patience is warranted while the disinflation process is working.

- Existing home sales sag as high prices and financing costs make homes their least affordable since the mid-80s.

- All eyes will be on next week’s personal income and spending report for October, watching for further signs of slowing demand growth.

Canadian Highlights

- Events this week reinforced our view that the Bank of Canada won’t be hiking rates again.

- Inflation decelerated significantly in October, thanks both to energy prices and some welcome softening in core inflation measures.

- The Federal government also released its Fall Economic Statement, which showed that the government won’t be adding any additional inflation stimulus relative to what it was already contributing.

U.S. – Looking for Signs of Slowing

U.S. Treasury yields extended their decline this week, with the 10-year now hovering around 4.5%. As economic data have decelerated, expectations for policy easing next year have helped markets continue to rally – up about 1% this week. This week, minutes from the Federal Open Market Committee (FOMC) meeting reinforced the Fed’s messaging that patience is warranted while the disinflation process is working, while housing starts data showcased that higher interest rates are working to cool the economy. Coming off the Thanksgiving holiday, all eyes are now tuned to next week’s consumer spending report for October for signs of slowing economic momentum and cooling inflation.

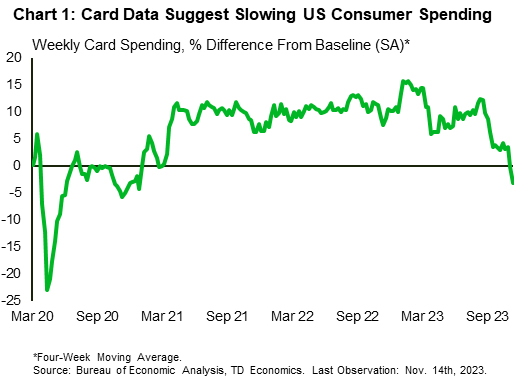

The minutes from the FOMC’s last meeting essentially backed up the hawkish signals the Fed has been putting out while they hold the policy rate fixed. Committee members noted how the economy stayed unexpectedly hot through the third quarter of the year, powered by relentless consumer spending. With the supply shocks from the pandemic and the war in Ukraine still gradually resolving themselves, persistently strong aggregate demand helped keep pressure on prices through much of the year. However, committee members judged that this may be starting to shift (Chart 1). This has left the Fed squarely focused on cooling demand to tame inflation pressures. On this front, the Fed maintains that restrictive policy rates are working, and are at an appropriate level. Moreover, with members agreeing that there needs to be clear evidence that inflation is on a solid trajectory back to 2% before easing, and upside risks ever-present, officials will be keenly looking out for any signs that more needs to be done to restore the supply-demand balance.

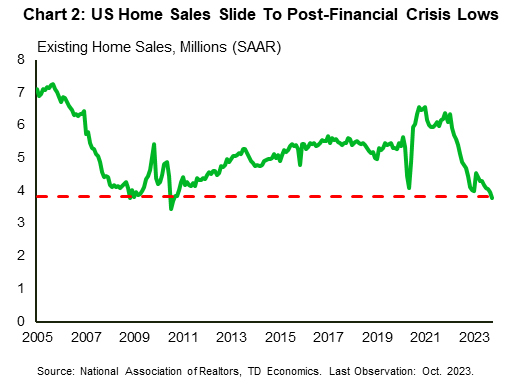

On the demand side, the housing market is clearly responding to the surge in borrowing costs since the summer, with existing home sales in October falling to their lowest level since 2010 (Chart 2). However, conditions today are drastically different than in 2010, when the housing bubble burst leading to an abundance of supply, and a tepid recovery after the Global Financial Crisis saw a drastic improvement in affordability. Today, affordability is weighing on activity as high prices and financing costs make homes their least affordable since the mid-80s. With the Fed poised to keep rates at multi-decade highs, a quick turnaround is unlikely.

However, with healthy economic momentum through the third quarter all eyes will be on next week’s consumer income and spending report for signs of slowing demand growth. With payrolls growth slowing in October, consensus expectations are for real consumer spending growth to slow from 0.4% month-on-month (m/m) in September to 0.1% in October. The Fed’s preferred inflation measure, the core PCE deflator, is expected to follow suit, slowing to 0.2% m/m from 0.4% in September.

Of course, given the experience of the past year, the risks run to the upside, and that the American consumer will once again prove to be more resilient than expected. In that event, the Fed has told us it stands ready to tighten policy further if they assess that data show, “progress toward the Committee’s inflation objective was insufficient.”

Canada – No More Hikes!

Events this week reinforced our view that the Bank of Canada (BoC) won't be hiking rates again. Inflation showed a big deceleration in October, causing BoC Governor Macklem to give one of his more dovish speeches. The Federal government also delivered a slimmed down forecast for deficit spending than expected over the next year. Core retail sales also showed weakness. Overall money markets continue to think the next move for the BoC is going to be a cut in the spring of 2024, leaving the Canada 10-year yield at around 3.8%, much lower than its September peak of 4.3% (Chart 1).

The much-anticipated release of Canadian inflation came in as we expected, with the Consumer Price Index (CPI) posting a 3.1% year-on-year (y/y) increase. This was a marked improvement from the 3.8% y/y rate of price growth in September. Welcome news of course, but nearly all of this was due to the drop in gasoline prices over the last year.

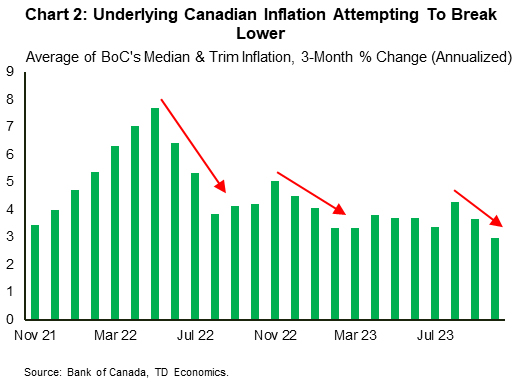

The question is: Will the deceleration in inflation continue? To answer that we must look at the trend in core inflation. This strips out the volatility in food and energy prices. And the good news is that the BoC's core measures broke lower in October on a three-month annualized basis (Chart 2). The average of the BoC's measures had been stuck around the mid-3% level for all of 2023, but as of October this measure now sits at exactly 3.0%. It's not 2% like the BoC would prefer, but it has moved lower. Weaker goods inflation drove the deceleration, as retailers appear to be discounting heavily. Just in time for the holiday shopping season! While we expect this trend to continue, we do not see the same downward trend when it comes to services inflation. Our measure of supercore services inflation that strips out things like housing costs and travel has been running north of 4% for two years now. This is largely driven by wages, which no surprise, are running hot at 5%.

The Federal government's Fall Economic Statement (FES) is also closely monitored by the BoC. Prior to the release, government spending was forecast to grow well above trend economic growth next year. This has drawn some soft criticism from the BoC Governor, who has stated that the Feds are rowing in the opposite direction as the BoC when it comes to wrestling inflation back to target. And while the FES has budgeted for new spending to increase housing supply, the bulk of spending will occur two years from now, containing spending growth in the near term. This means that government spending won't be increasing inflationary pressures in the near-term any more than it already was, but spending will start to ramp up in 2025. Let's hope inflation will be reined in by that point!

Governor Macklem's speech in Saint John following the release of CPI and the FES exuded more confidence regarding the outlook, stating that "interest rates may now be restrictive enough to get us back to price stability". The Governor was clearly encouraged by recent events, and his dovish tone has reinforced bets that the next move by the BoC is going to be a cut to its policy rate.

Q3 to Mark Second Consecutive Pullback in Real GDP as Unemployment Ticks Higher

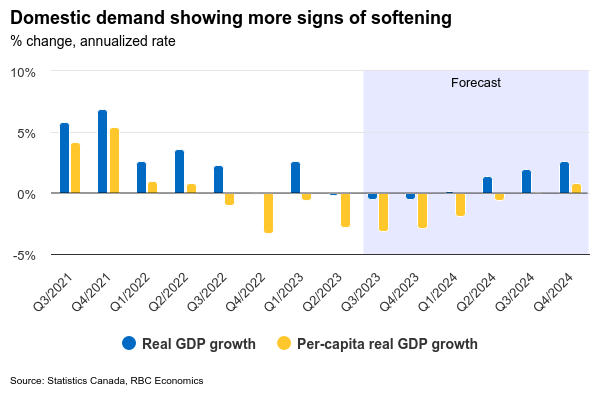

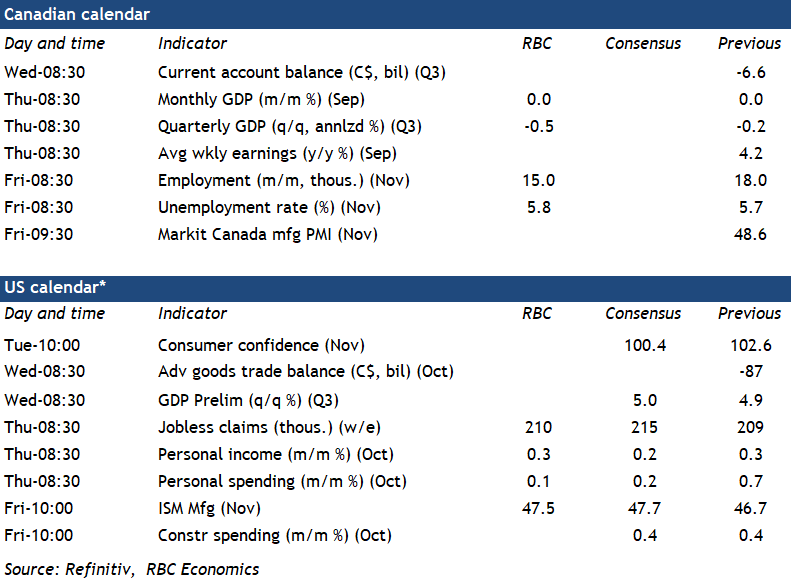

Canadian GDP likely edged lower in Q3 – we expect at a -0.5% (annualized) decline that would be slightly softer than the preliminary -0.1% estimate from Statistics Canada a month ago. Preliminary GDP estimates are highly revision prone, and domestic demand has shown more signs of softening in Q3 with both business and consumer spending slowing. And that small Q3 GDP decline will again look substantially weaker on a per-capita basis given rapid population growth. Canadian real retail sales were down 2.1% (on a quarter-over-quarter annualized basis) in Q3. Restaurant sales declined ~4.5% in Q3 controlling for price changes and our own tracking of service-sector spending softened. Manufacturing output is down 4% from Q2 over July and August, consistent with signs of cooling demand for physical merchandise globally as headwinds from higher interest rates build. Residential investment likely edged higher with higher housing starts offsetting a pullback in home resales. Net international trade will add to GDP growth but largely from lower imports tied to softening in domestic demand.

Early data for the fourth quarter does not look much better. The early estimate of October retail sales was stronger (+0.8%) but manufacturing sales fell 2.7%. Hours worked were unchanged in October alongside a small employment gain and another tick higher in the unemployment rate (to 5.7%).

And we expect November’s Canadian labour market data will underscore broader weakness in the economy. We look for a 15k job gain – not enough to prevent the unemployment rate from ticking higher by one-tenth to 5.8%. Soaring population growth has boosted the available labour supply, but as hiring demand slows, labour is being absorbed more slowly by the job market. Wage growth will be watched closely by the Bank of Canada, but softening labour demand is shifting bargaining power back to employers and we look for wage growth to broadly slow going forward.

Week ahead data watch

SEPH employment data for September will also be watched closely for further signs of softening in the labour market. Job openings (not counted in the more timely Labour Force Survey data) are expected to continue to drift lower as labour demand slows.

We expect U.S. personal income to tick up 0.3% in October, the same pace as in September. Employment growth and wage growth both slowed during that month. Real personal spending likely flattened in October from the 0.4% in September, largely due to weaker retail sales during that month.

Summary 11/27 – 12/1

Monday, Nov 27, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | 2.10% | 2.10% |

| 15:00 | USD | New Home Sales M/M Oct | 725K | 759K |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | |

| Forecast: 2.10% | Previous: 2.10% | ||

| 15:00 | USD | New Home Sales M/M Oct | |

| Forecast: 725K | Previous: 759K | ||

Tuesday, Nov 28, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | BRC Shop Price Index Y/Y Oct | 5.20% | |

| 00:30 | AUD | Retail Sales M/M Oct | 0.10% | 0.90% |

| 07:00 | EUR | Germany Gfk Consumer Confidence Dec | -28.5 | -28.1 |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | -0.90% | -1.20% |

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Sep | 4.20% | 2.20% |

| 14:00 | USD | Housing Price Index M/M Sep | 0.40% | 0.60% |

| 15:00 | USD | Consumer Confidence Nov | 101 | 102.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | BRC Shop Price Index Y/Y Oct | |

| Forecast: | Previous: 5.20% | ||

| 00:30 | AUD | Retail Sales M/M Oct | |

| Forecast: 0.10% | Previous: 0.90% | ||

| 07:00 | EUR | Germany Gfk Consumer Confidence Dec | |

| Forecast: -28.5 | Previous: -28.1 | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | |

| Forecast: -0.90% | Previous: -1.20% | ||

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Sep | |

| Forecast: 4.20% | Previous: 2.20% | ||

| 14:00 | USD | Housing Price Index M/M Sep | |

| Forecast: 0.40% | Previous: 0.60% | ||

| 15:00 | USD | Consumer Confidence Nov | |

| Forecast: 101 | Previous: 102.6 | ||

Wednesday, Nov 29, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Oct | 5.50% | 5.60% |

| 01:00 | NZD | RBNZ Rate Decision | 5.50% | 5.50% |

| 07:00 | EUR | Germany Import Price Index M/M Oct | 0.10% | 1.60% |

| 09:00 | CHF | Credit Suisse Economic Expectations Nov | -37.8 | |

| 09:30 | GBP | M4 Money Supply M/M Oct | -0.20% | -1.10% |

| 09:30 | GBP | Mortgage Approvals Oct | 44K | 43K |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Nov | 93.3 | |

| 10:00 | EUR | Eurozone Industrial Confidence Nov | -9.3 | |

| 10:00 | EUR | Eurozone Services Sentiment Nov | 4.5 | |

| 10:00 | EUR | Consumer Confidence Nov F | -16.9 | -16.9 |

| 13:00 | EUR | Germany CPI M/M Nov P | -0.10% | 0% |

| 13:00 | EUR | Germany CPI Y/Y Nov P | 3.80% | |

| 13:30 | CAD | Current Account (CAD) Q3 | -6.6B | |

| 13:30 | USD | GDP Annualized Q3 P | 5.00% | 4.90% |

| 13:30 | USD | GDP Price Index Q3 P | 3.50% | 3.50% |

| 13:30 | USD | Goods Trade Balance (USD) Oct P | -86.7B | -86.8B |

| 13:30 | USD | Wholesale Inventories Oct P | 0.10% | 0.20% |

| 15:30 | USD | Crude Oil Inventories | 8.7M | |

| 19:00 | USD | Fed's Beige Book | ||

| 23:50 | JPY | Industrial Production M/M Oct P | 0.50% | |

| 23:50 | JPY | Retail Trade Y/Y Oct | 5.90% | 5.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Oct | |

| Forecast: 5.50% | Previous: 5.60% | ||

| 01:00 | NZD | RBNZ Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 07:00 | EUR | Germany Import Price Index M/M Oct | |

| Forecast: 0.10% | Previous: 1.60% | ||

| 09:00 | CHF | Credit Suisse Economic Expectations Nov | |

| Forecast: | Previous: -37.8 | ||

| 09:30 | GBP | M4 Money Supply M/M Oct | |

| Forecast: -0.20% | Previous: -1.10% | ||

| 09:30 | GBP | Mortgage Approvals Oct | |

| Forecast: 44K | Previous: 43K | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Nov | |

| Forecast: | Previous: 93.3 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Nov | |

| Forecast: | Previous: -9.3 | ||

| 10:00 | EUR | Eurozone Services Sentiment Nov | |

| Forecast: | Previous: 4.5 | ||

| 10:00 | EUR | Consumer Confidence Nov F | |

| Forecast: -16.9 | Previous: -16.9 | ||

| 13:00 | EUR | Germany CPI M/M Nov P | |

| Forecast: -0.10% | Previous: 0% | ||

| 13:00 | EUR | Germany CPI Y/Y Nov P | |

| Forecast: | Previous: 3.80% | ||

| 13:30 | CAD | Current Account (CAD) Q3 | |

| Forecast: | Previous: -6.6B | ||

| 13:30 | USD | GDP Annualized Q3 P | |

| Forecast: 5.00% | Previous: 4.90% | ||

| 13:30 | USD | GDP Price Index Q3 P | |

| Forecast: 3.50% | Previous: 3.50% | ||

| 13:30 | USD | Goods Trade Balance (USD) Oct P | |

| Forecast: -86.7B | Previous: -86.8B | ||

| 13:30 | USD | Wholesale Inventories Oct P | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 8.7M | ||

| 19:00 | USD | Fed's Beige Book | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Industrial Production M/M Oct P | |

| Forecast: | Previous: 0.50% | ||

| 23:50 | JPY | Retail Trade Y/Y Oct | |

| Forecast: 5.90% | Previous: 5.80% | ||

Thursday, Nov 30, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Nov | 23.4 | |

| 00:30 | AUD | Private Capital Expenditure Q3 | 1.00% | 2.80% |

| 00:30 | AUD | Private Sector Credit M/M Oct | 0.40% | 0.50% |

| 01:00 | CNY | NBS Manufacturing PMI Nov | 49.6 | 49.5 |

| 01:00 | CNY | NBS Non-Manufacturing PMI Nov | 51.1 | 50.6 |

| 05:00 | JPY | Housing Starts Y/Y Oct | -7.00% | -6.80% |

| 07:00 | EUR | Germany Retail Sales M/M Oct | 0.50% | -0.80% |

| 07:30 | CHF | Real Retail Sales Y/Y Oct | 0.20% | -0.60% |

| 08:00 | CHF | KOF Economic Barometer Nov | 96.2 | 95.8 |

| 08:55 | EUR | Germany Unemployment Change Nov | 25K | 30K |

| 08:55 | EUR | Germany Unemployment Rate Nov | 5.80% | |

| 09:00 | EUR | Italy Unemployment Oct | 7.40% | 7.40% |

| 10:00 | EUR | Eurozone Unemployment Rate Oct | 6.50% | 6.50% |

| 10:00 | EUR | Eurozone CPI Y/Y Nov P | 3.80% | 2.90% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov P | 3.90% | 4.20% |

| 13:30 | CAD | GDP M/M Sep | 0.10% | 0.00% |

| 13:30 | USD | Personal Income M/M Oct | 0.20% | 0.30% |

| 13:30 | USD | Personal Spending Oct | 0.20% | 0.70% |

| 13:30 | USD | PCE Price Index M/M Oct | 0.40% | |

| 13:30 | USD | PCE Price Index Y/Y Oct | 3.40% | |

| 13:30 | USD | Core PCE Price Index M/M Oct | 0.20% | 0.30% |

| 13:30 | USD | Core PCE Price Index Y/Y Oct | 3.70% | |

| 13:30 | USD | Initial Jobless Claims (Nov 24) | 215K | 209K |

| 14:45 | USD | Chicago PMI Nov | 44 | |

| 15:00 | USD | Pending Home Sales M/M Oct | -0.70% | 1.10% |

| 15:30 | USD | Natural Gas Storage | -7B | |

| 23:30 | JPY | Unemployment Rate Oct | 2.60% | 2.60% |

| 23:50 | JPY | Capital Spending Q3 | 3.40% | 4.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Nov | |

| Forecast: | Previous: 23.4 | ||

| 00:30 | AUD | Private Capital Expenditure Q3 | |

| Forecast: 1.00% | Previous: 2.80% | ||

| 00:30 | AUD | Private Sector Credit M/M Oct | |

| Forecast: 0.40% | Previous: 0.50% | ||

| 01:00 | CNY | NBS Manufacturing PMI Nov | |

| Forecast: 49.6 | Previous: 49.5 | ||

| 01:00 | CNY | NBS Non-Manufacturing PMI Nov | |

| Forecast: 51.1 | Previous: 50.6 | ||

| 05:00 | JPY | Housing Starts Y/Y Oct | |

| Forecast: -7.00% | Previous: -6.80% | ||

| 07:00 | EUR | Germany Retail Sales M/M Oct | |

| Forecast: 0.50% | Previous: -0.80% | ||

| 07:30 | CHF | Real Retail Sales Y/Y Oct | |

| Forecast: 0.20% | Previous: -0.60% | ||

| 08:00 | CHF | KOF Economic Barometer Nov | |

| Forecast: 96.2 | Previous: 95.8 | ||

| 08:55 | EUR | Germany Unemployment Change Nov | |

| Forecast: 25K | Previous: 30K | ||

| 08:55 | EUR | Germany Unemployment Rate Nov | |

| Forecast: | Previous: 5.80% | ||

| 09:00 | EUR | Italy Unemployment Oct | |

| Forecast: 7.40% | Previous: 7.40% | ||

| 10:00 | EUR | Eurozone Unemployment Rate Oct | |

| Forecast: 6.50% | Previous: 6.50% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Nov P | |

| Forecast: 3.80% | Previous: 2.90% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov P | |

| Forecast: 3.90% | Previous: 4.20% | ||

| 13:30 | CAD | GDP M/M Sep | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 13:30 | USD | Personal Income M/M Oct | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 13:30 | USD | Personal Spending Oct | |

| Forecast: 0.20% | Previous: 0.70% | ||

| 13:30 | USD | PCE Price Index M/M Oct | |

| Forecast: | Previous: 0.40% | ||

| 13:30 | USD | PCE Price Index Y/Y Oct | |

| Forecast: | Previous: 3.40% | ||

| 13:30 | USD | Core PCE Price Index M/M Oct | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 13:30 | USD | Core PCE Price Index Y/Y Oct | |

| Forecast: | Previous: 3.70% | ||

| 13:30 | USD | Initial Jobless Claims (Nov 24) | |

| Forecast: 215K | Previous: 209K | ||

| 14:45 | USD | Chicago PMI Nov | |

| Forecast: | Previous: 44 | ||

| 15:00 | USD | Pending Home Sales M/M Oct | |

| Forecast: -0.70% | Previous: 1.10% | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -7B | ||

| 23:30 | JPY | Unemployment Rate Oct | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 23:50 | JPY | Capital Spending Q3 | |

| Forecast: 3.40% | Previous: 4.50% | ||

Friday, Dec 1, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Nov F | 48.1 | 48.1 |

| 01:45 | CNY | Caixin Manufacturing PMI Nov | 49.3 | 49.5 |

| 08:00 | CHF | GDP Q/Q Q3 | 0.10% | 0.00% |

| 08:30 | CHF | Manufacturing PMI Nov | 42.0 | 40.6 |

| 08:45 | EUR | Italy Manufacturing PMI Nov | 45.5 | 44.9 |

| 08:50 | EUR | France Manufacturing PMI Nov F | 42.6 | 42.6 |

| 08:55 | EUR | Germany Manufacturing PMI Nov F | 42.3 | 42.3 |

| 09:00 | EUR | Italy GDP Q/Q Q3 | 0% | 0% |

| 09:00 | EUR | Manufacturing PMI Nov F | 43.8 | 43.8 |

| 09:30 | GBP | Manufacturing PMI Nov F | 46.7 | 46.7 |

| 13:30 | CAD | Net Change in Employment Nov | 17.5K | |

| 13:30 | CAD | Unemployment Rate Nov | 5.70% | |

| 14:30 | CAD | Manufacturing PMI Nov | 48.6 | |

| 14:45 | USD | Manufacturing PMI Nov F | 49.4 | |

| 15:00 | USD | ISM Manufacturing PMI Nov | 47.7 | 46.7 |

| 15:00 | USD | ISM Manufacturing Prices Paid Nov | 46.2 | 45.1 |

| 15:00 | USD | ISM Manufacturing Employment Index Nov | 46.8 | |

| 15:00 | USD | Construction Spending M/M Oct | 0.40% | 0.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Nov F | |

| Forecast: 48.1 | Previous: 48.1 | ||

| 01:45 | CNY | Caixin Manufacturing PMI Nov | |

| Forecast: 49.3 | Previous: 49.5 | ||

| 08:00 | CHF | GDP Q/Q Q3 | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 08:30 | CHF | Manufacturing PMI Nov | |

| Forecast: 42.0 | Previous: 40.6 | ||

| 08:45 | EUR | Italy Manufacturing PMI Nov | |

| Forecast: 45.5 | Previous: 44.9 | ||

| 08:50 | EUR | France Manufacturing PMI Nov F | |

| Forecast: 42.6 | Previous: 42.6 | ||

| 08:55 | EUR | Germany Manufacturing PMI Nov F | |

| Forecast: 42.3 | Previous: 42.3 | ||

| 09:00 | EUR | Italy GDP Q/Q Q3 | |

| Forecast: 0% | Previous: 0% | ||

| 09:00 | EUR | Manufacturing PMI Nov F | |

| Forecast: 43.8 | Previous: 43.8 | ||

| 09:30 | GBP | Manufacturing PMI Nov F | |

| Forecast: 46.7 | Previous: 46.7 | ||

| 13:30 | CAD | Net Change in Employment Nov | |

| Forecast: | Previous: 17.5K | ||

| 13:30 | CAD | Unemployment Rate Nov | |

| Forecast: | Previous: 5.70% | ||

| 14:30 | CAD | Manufacturing PMI Nov | |

| Forecast: | Previous: 48.6 | ||

| 14:45 | USD | Manufacturing PMI Nov F | |

| Forecast: | Previous: 49.4 | ||

| 15:00 | USD | ISM Manufacturing PMI Nov | |

| Forecast: 47.7 | Previous: 46.7 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Nov | |

| Forecast: 46.2 | Previous: 45.1 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Nov | |

| Forecast: | Previous: 46.8 | ||

| 15:00 | USD | Construction Spending M/M Oct | |

| Forecast: 0.40% | Previous: 0.40% | ||