Sample Category Title

German Ifo business climate rose to 87.3, economy stabilizing

German Ifo Business Climate rose from 86.9 to 87.3 in November, slightly below expectation of 87.5. But that is still the third consecutive increase. Current Assessment index ticked up from 89.2 to 89.4, matched expectations. Expectations index also rose from 84.8 to 85.2, missed expectation of 85.7.

By sector, manufacturing rose from -15.7 to -13.5. Services fell from -1.5 to -2.5. Construction rose from -30.8 to -29.4. Trade rose from -27.3 to -22.2.

Ifo said: "The German economy is stabilizing, albeit at a low level."

NZD/USD Edges Higher as Retail Sales Beat Expectations

- New Zealand retail sales flatline in Q3

- US releases PMIs later today

The New Zealand dollar has posted slight gains on Friday. In the European session, NZD/USD is trading at 0.6059, up 0.17%. The New Zealand dollar is headed to a second-straight winning week and has sparkled in November, with gains of 4% against the US dollar.

New Zealand retail sales unchanged

The New Zealand consumer hasn’t been in the mood to spend and the markets were braced for a decline in third-quarter retail sales. The news was better than expected, however, as retail sales were flat at 0.0% q/q, breaking a streak of three straight losing quarters. The improvement in retail sales points to resilience in the New Zealand economy.

On an annual basis, retail sales came in at -3.4%, little changed from the second-quarter reading of -3.5%. The sharp decline is a result of the central bank’s aggressive tightening and an inflation rate of 5.6%, which is very high and well above the 1%-3% target band.

The Reserve Bank of New Zealand meets on November 29th and is expected to leave the cash rate unchanged at 5.5%. The RBNZ has held rates three straight times and market speculation is rising that the RBNZ will pivot and trim rates in 2024. The RBNZ is unlikely to send any signals about cutting rates, however, especially with inflation well above the target.

I expect the RBNZ to maintain its ‘higher for longer’ policy, which would mean further rate pauses well into 2024. This would provide RBNZ policy makers the flexibility to raise rates if inflation unexpectedly rises or to trim rates once inflation drops closer to 3%, which is the top of the target range, without risking a loss of credibility.

The US wraps up with the release of US manufacturing and services PMIs, with little change expected. Still, the markets will be watching carefully, as the data will provide insights into the strength of the US economy. The consensus estimates for November stand at 49.8 for manufacturing (Oct: 50.0) and 50.4 for services (Oct. 49.8). If either of the PMIs miss expectations, that could translate into volatility from the US dollar in the North American session.

NZD/USD Technical

- NZD/USD continues to put pressure on resistance at 0.6076. The resistance line 0.6161

- There is support at 0.5996 and 0.5885

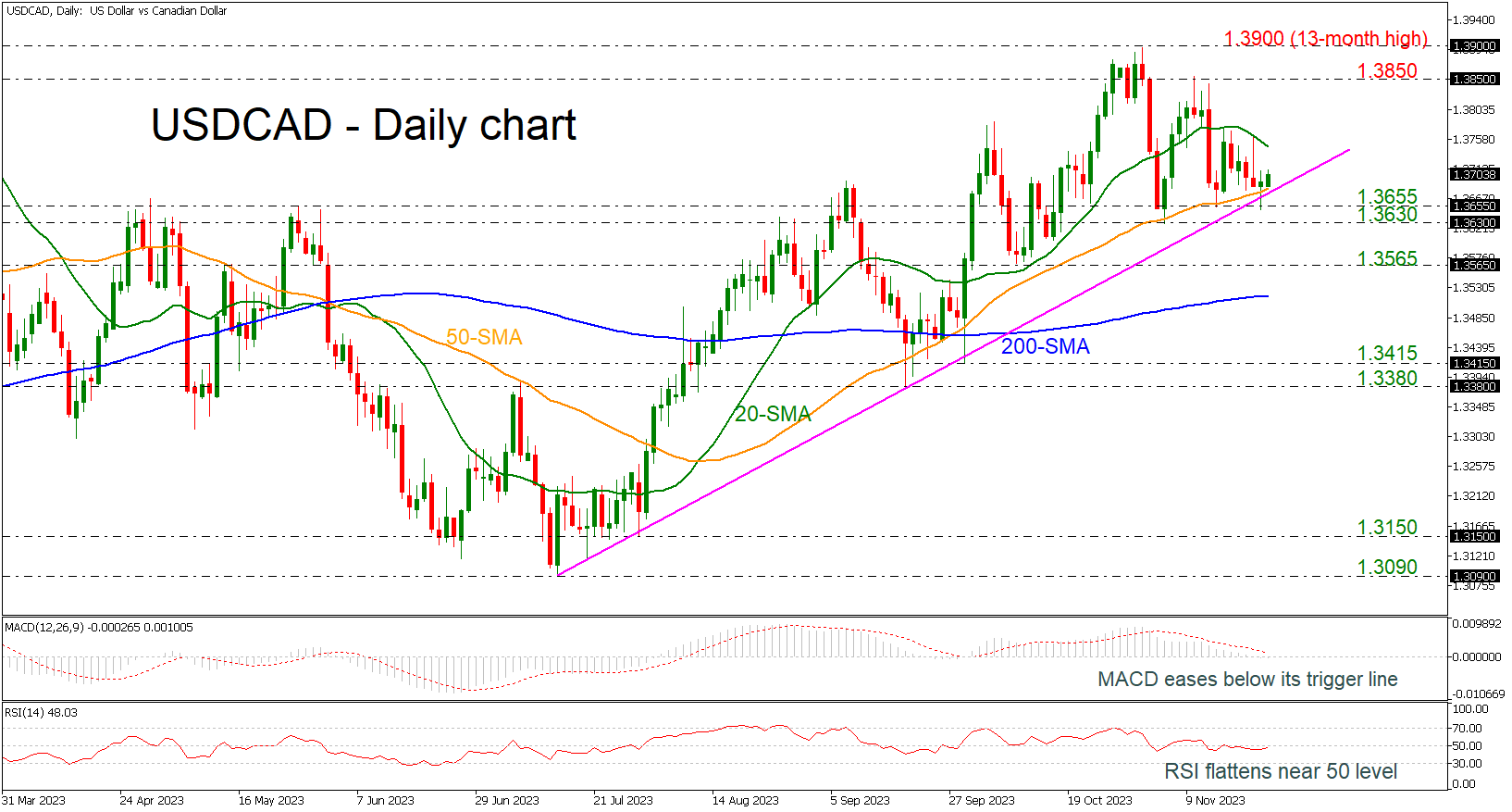

USDCAD Rises After Finding Support on Ascending Line

- USDCAD rebounds off the uptrend line

- Holds within short-term SMAs

- MACD and RSI muted bearish momentum

USDCAD is hovering within the downward sloping 20- and the 50-day simple moving average (SMA) lines but is still standing above the medium-term rising trend line. The pair found support near the 1.3655 support level and the bearish correction may come to an end.

Moving higher, the market may retest the 20-day SMA at 1.3745 before rallying towards the 1.3850 resistance. Above these obstacles the pair would reach the 13-month high of 1.3900.

On the other hand, if the bears take the upper hand and break the uptrend line to the downside would test the 1.3630-1.3655 region. More downside movements could open the way towards the 1.3565 barricade, taken from the low on October 10 before challenging the 200-day SMA at 1.3520.

The technical oscillators muted the bearish action. The MACD is marginally below its trigger and zero lines, while the RSI is moving beneath the 50 level and is ready to cross it to the upside, indicating a bullish movement in the next few sessions.

To sum up, USDCAD is showing some signs for a resumption of the upward movement in the short-term, while in the medium-term it has been posting higher highs and higher lows since July 14.

Gold Price Dips From $2K While Crude Oil Price Recovers

Gold price surged toward the $2,000 zone before the bears appeared. Crude oil price is attempting a recovery wave above the $75.00 zone.

Important Takeaways for Gold and Oil Prices Analysis Today

- Gold price started a steady increase from the $1,965 zone against the US Dollar.

- A key bearish trend line is forming with resistance at $1,995 on the hourly chart of gold at FXOpen.

- Crude oil prices started a decent recovery wave from the $73.80 support.

- There is a connecting bearish trend line forming with resistance near $77.00 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price found support near the $1,965 zone. The price remained in a bullish zone and started a strong increase above $1,985.

There was a decent move above the 50-hour simple moving average. The bulls pushed the price above the $1,985 and $1,995 resistance levels. Finally, the price tested the $2,005 zone before the bears appeared.

There was a minor downside correction below $2,000 and the RSI dipped below 50. There was a move below the 23.6% Fib retracement level of the upward move from the $1,965 swing low to the $2,007 high.

Initial support on the downside is near the 50% Fib retracement level of the upward move from the $1,965 swing low to the $2,007 high at $1,985. The first major support is near the $1,975 zone.

If there is a downside break below the $1,975 support, the price might decline further. In the stated case, the price might drop toward the $1,965 support.

Immediate resistance is near a key bearish trend line at $1,995 and the 50-hour simple moving average. The next major resistance is near the $2,005 level. An upside break above the $2,005 resistance could send Gold price toward $2,020. Any more gains may perhaps set the pace for an increase toward the $2,032 level.

Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price found support near the $73.80 zone against the US Dollar. The price formed a base and started a recovery wave above $74.50.

The bulls were able to push the price above the 50% Fib retracement level of the downward move from the $78.44 swing high to the $73.81 low. The hourly RSI is back above the 50 level, but the price is struggling near the 50-hour simple moving average.

There is also a connecting bearish trend line forming with resistance near $77.00. It is close to the 61.8% Fib retracement level of the downward move from the $78.44 swing high to the $73.81 low.

A clear move above the trend line resistance could send the price toward the $78.40 resistance. Any more gains might send the price toward the $80.00 level.

Conversely, the price might start a fresh decline from the $77.00 resistance. Immediate support sits near the $76.10 level. The next major support on the WTI crude oil chart is $73.80.

If there is a downside break, the price might decline toward $72.35. Any more losses may perhaps open the doors for a move toward the $70.00 support zone.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold Fails to Hold Above 2,000 for the Third Day

The gold price increased slightly in the quiet trading session on Thursday as the U.S. dollar declined during the Thanksgiving holiday.

Possible effects for traders

XAUUSD rose by 0.10% yesterday in a very quiet trading session due to the decline of the U.S. dollar, while the U.S. treasury market remained closed for the holiday. Gold maintained its position above the important 1,990 level. The strength of XAUUSD is largely attributed to the growing anticipation that the Federal Reserve (Fed) may have concluded its cycle of interest rate hikes. Economic reports suggest that the U.S. central bank has effectively eased inflation, reinforcing expectations of a more dovish Fed policy. Lower interest rates decrease the opportunity cost of holding gold. 'Absent any fresh influences, I still don't think that gold has the momentum to maintain prices much above 2,000 for the rest of the year,' said StoneX analyst Rhona O'Connell.

In the Asian and early European trading sessions, gold prices rose due to the weakening of the U.S. dollar. In terms of geopolitical developments, Israel and Hamas initiated a four-day ceasefire this Friday, marking the first break in the conflict that has been ongoing for nearly seven weeks. Easing tensions may put downward pressure on XAUUSD, but some analysts expect the metal to remain strong. 'Spot gold may retest a resistance at $1,999 per ounce, a break above which could lead to a gain into the 2,009–2,016 range,' said Reuters analyst Wang Tao.

EURUSD Rises as Economic Sentiment Improves Slightly

The euro (EUR) gained 0.16% on Thursday as Purchasing Managers Indices (PMIs) came out better-than-expected. However, trading activity remained subdued due to the holidays in the U.S. and Japan.

Possible effects for traders

The results of the latest PMI surveys showed that the downturn in eurozone business activity remains persistent but is easing somewhat. Although the figures indicated that the eurozone's economy may contract again this quarter, the market's reaction was primarily bullish. Furthermore, European Central Bank (ECB) officials have recently suggested that interest rates may have to remain higher for longer. Pierre Wunsch, the Belgian policymaker, told the German newspaper that there is a possibility for another rate hike.

EURUSD was essentially unchanged during the Asian and early European trading sessions. Today, two important events may affect the currency. Germany will release its Ifo Business Climate report at 9:00 a.m. UTC. Then, the S&P will publish U.S. PMIs at 2:45 p.m. UTC. Both reports will shed more light on how businesses in the two countries consider their current and future economic conditions. S&P PMIs should add extra volatility to the market. EURUSD may rise above 1.09400 if U.S. PMIs come out lower than expected.

Volumes Remain Traditionally Low on Black Friday

Markets

German Bunds sold off yesterday in a move that started on weak November EMU PMI’s and ended with Germany suspending its debt brake for (at least) another year. PMI’s remain at weak levels, suggesting the EMU economy being stuck in the mud. A sixth consecutive sub-50 reading for the composite gauge seals the debate on a technical recession for H2 2023. Falling new orders, lower output and running down of inventories for the first time in three years resulted in falling employment. Small job gains in services failed to cover for big losses in manufacturing. Overall price pressure accelerated again, solely driven by services as a result of above average inflation. For the first time since the October/November rate skips by the ECB, Fed and BoE, markets didn’t grab the opportunity (of weak data) to extend the bond correction higher. It suggests that for now, the frontrunning on Q2 2024 global rate cut bets went far enough. In our view, these expectations don’t align with central bank communication and are still too premature. ECB Villeroy for example said that the ECB in his view won’t raise rates again, but simultaneously stressed that the 4% plateau will likely stay at least for the next several meetings and the next few quarters. Earlier this month, he also suggested to end PEPP-reinvestments sooner than currently planned (“at least until end 2024”). The Bund sell-off accelerated as last week’s constitutional ruling on illegal off-balance sheet spending pushed the German government to suspend the debt brake (0.35% of GDP of new net spending). The decision in theory gives more leeway for additional spending in case of economic downturn and also increases moral hazard behavior on public finances in other EMU countries. German yields added 2.3 bps (2-yr) to 5.8 bps (10-yr). The single currency failed to profit from the interest rate support with EUR/USD spending most part of the trading day just below 1.09. Sterling marginally outperformed with EUR/GBP closing at the 0.87 big figure on diverging PMI’s. UK November surveys outperformed EMU ones with a strong rebound in services pushing the composite UK gauge back above the neutral 50 mark.

Japanese national inflation figures accelerated in October (2.9% Y/Y from 2.8% Y/Y for the BoJ’s preferred ex fresh food gauge), bolstering the case for the BoJ to up its policy normalization efforts. JPY is marginally stronger at 149.40. US investors return from their Thanksgiving holiday, but volumes remain traditionally low on Black Friday. US November PMI’s are the key focus. We hope to a see a similar market reaction as yesterday on EMU PMI to confirm our case that the upward bond correction ran its course.

News headlines

New Zealand is about to have a new government. The National Party, led by incoming prime minister Luxon, sealed an agreement on Friday with ACT and the First party. The cabinet is to be sworn in next Monday and has announced a range of measures including in 2018 cutting personal income taxes but also to remove the central bank’s (RBNZ) dual mandate on inflation and employment introduced by Labour to narrow it down to just price stability. The RBNZ’s annual inflation target ranges between 1-3% with a focus on the 2% midpoint. It is currently required to reach this “over the medium term” but the coalition government is taking advice to replace this by time-specific targets. The previous New Zealand government sought similar advice last year. The central bank then did not support the idea, arguing that monetary policy works with lags that can change over time. It is not unheard of in advanced economies, however. The Bank of Canada seeks to achieve its inflation aim in six to eight quarters.

The European Commission is about to conclude its assessment of Hungary’s amended post-pandemic recovery plan aimed at addressing the energy crunch following the Russian invasion. If approved by the EU finance ministers, Hungary will have access to as much as 20% of the €3.9bn in loans and €700 mln in grants combined, or €920 mln in total. These funds are non-conditional, meaning the bulk of the recovery funds as well as billions of other (cohesion) resources are still blocked over a long-running legal battle between Hungary and the EU over the rule of law and graft concerns. The forint yesterday outperformed regional peers still. EUR/HUF dipped below 380.

On a Slippery Floor

While the US economy has been surprisingly resilient this year to the Federal Reserve’s (Fed) aggressive monetary tightening, we cannot say that we have a similar soothing picture in Europe. The energy crisis, that followed the pandemic, has been hard on Germany. The country needs money when money becomes rare and expensive. Germany decided to suspend the debt limit for the 4th consecutive year – signaling that borrowing in Europe will continue to increase, and the new debt that the Europeans will take on their shoulders will cost significantly higher than a few years ago.

German bonds fell yesterday on news of yet another suspension of the debt limit. The 10-year German yield advanced to 2.60%, Italy’s 10-year yield jumped to 4.40%, the Italian–German yield spread rebounded this week from the lowest levels since September, and the widening yield spread between core and periphery could become a limiting factor for euro appetite at a time traders should decide whether the EURUSD should appreciate above the 1.10 psychological mark.

As per the European Central Bank (ECB) expectations, European officials do their best to tame the rate cut expectations in the Eurozone. Belgian central bank governor Pierre Wunsch said yesterday that the ECB won’t cut the rates as long as wages growth remains elevated, while the German central bank head Joachim Nagel said that cutting rates too early would be a mistake. A mistake? Maybe. Yet, economic data comes as further evidence that the European economies are not going toward sunny days. Released yesterday, the European PMI figures came in slightly better than expected, but the reading was below 50 for the 6th consecutive month, meaning that activity in the Eurozone contracted for the 6th consecutive month. The Eurozone GDP fell below 0 at the latest reading, while in comparison, the US GDP grew nearly 5%. This is to say that, based on the current data, the Fed has a greater margin for keeping rates steady than their European counterparts. It at least has better credibility. And the Fed’s bigger hawkish margin compared to the ECB should keep the euro appetite limited against the US dollar following the rally since the beginning of October.

In the US, despite warnings that the falling US long-term yields will, at some point, trigger a hawkish reaction from the Fed and eventually reverse, the Fed doves remain in charge of the market. The US dollar index struggles to gain traction above the 200-DMA.

The USDJPY remains offered near the 50-DMA after the Japanese inflation advanced to a 3-month high in October (rose to 3.3% level from 3% printed a month earlier). Normally, it would’ve boosted bets of Bank of Japan (BoJ) normalization, but the BoJ should first awaken from its coma.

In energy, US crude trades near $75/76 region. Downside risks prevail due to speculation that the delayed OPEC meeting could result in Saudi Arabia not doubling its solo production cuts. There is even a slim possibility that they eventually reverse them.

I am wondering if this week’s drama is not staged amid poor buying following the news that Saudi would doble its cuts, to cast shadow in Saudi’s intention to defend oil prices, to bring attention to OPEC and to Saudi which finally would go ahead and double its production cuts hoping that the market reaction would be stronger than if they had announced the same outcome this weekend. In all cases, deteriorating growth prospects will likely limit the upside potential in oil prices in the medium run. The short run will certainly see more volatility.

European Yields Rise on Data and German Debt Break Outlook

Market movers today

Key focus today will be on the German Ifo survey and US PMIs.

The Ifo survey increased in October and is expected to show a further increase in November in line with the signals from the ZEW index and other survey data pointing to a gradual bottoming from a very low level.

US PMIs have shown a bit of a diverging picture with PMI manufacturing moving slightly higher in recent months while service PMI has weakened. We look for a cooling of the economy going into the winter months which should keep service PMI under pressure. In the manufacturing sector a lift in the order-inventory ratio lately suggests we could see a further moderate rise in PMI manufacturing from the current level of 50.

The 60 second overview

Markets: it has been a fairly quiet overnight session following the Thanksgiving holiday in the US. Asian equity benchmarks and DM equity futures are trading slightly higher this morning while oil and USD FX are little changed. US yields are opening a few bp higher following the European sell-off yesterday (more below).

Sweden monetary policy. Yesterday the Riksbank kept the policy rate unchanged at 4.00% and opened up for an announcement of a further QT volume increase already at the next meeting. The policy rate path was kept roughly unchanged but pushed by one quarter, i.e. signalling a continued probability for a further hike (10bp). Read more about the Riksbank decision in our Riksbank flash comment, 23 November.

Eurozone macro data. European PMI data improved in November with the Eurozone composite measure rising from 46.5 to 47.1. However, this is still recessionary territory. Worryingly for the ECB, price indices showed higher price pressures within the services sector. This is in line with the increasing wage growth, which rose to 4.7% y/y in Q3 vs. 4.6% in Q2 according to the ECB's negotiated wage indicator also released yesterday.

German politics. In Germany, the government has decided to pursue a suspension of the debt brake next year - as it did in 2020 - following the Constitutional Court in Karlsruhe's rejection of the previous plan of spending EUR60bn originally intended for fighting covid-19 on climate and economic transformation. The move will be presented as part of a revised budget next week. This should be doable, as the funds will be aimed at climate expenses, which given the rain and the flooding in Germany in recent years, should be possible to push through parliament (and Karlsruhe). Holding a majority in parliament, the government could decide to keep the suspension until the next election in 2025.

Oil. The oil market took OPEC's decision to postpone its meeting originally scheduled for Sunday by four days with relative ease. Apparently, Angola will not meet demands for reducing its quota next year. In our view, OPEC has more power to push oil prices lower than higher. The cartel's total production led by the big voluntary cut by Saudi Arabia is already low and we doubt it will make substantial further cuts to lift oil prices. Rather there is a risk that disagreement leads to scrapping of quotas and some producers potentially leaving the cartel with everyone free to produce at will, which would be a big blow to oil prices. We think OPEC will muddle through with an extension of current production levels next year and thus do not expect the postponed meeting to be a market mover. Rather the oil market will be at the hands of global risk sentiment and the USD. We look for Brent to average USD80/bbl next year.

Japan. Overnight CPI and PMI data were released. While the PMI data revealed a further decline in the manufacturing index to 48.1 (from 48.7) the service index rose 0.1 index point to 51.7. More importantly for markets, the inflation release showed a pick-up in inflation although slightly below market expectations. That said, prints in core inflation and core-core inflation of 2.9% Y/Y and 4.0% Y/Y, respectively, remain far above Bank of Japan's inflation target and we still expect Bank of Japan to remove its yield curve control at the coming monetary policy meetings and ultimately hike policy rates during 2024.

Equities: Global equities were higher yesterday in a dull session as US was closed for Thanksgiving celebrations. However, European stocks managed to grind led by energy and pharma industries. As mentioned before in our 'Espresso', one should see sessions with stability, not least on the bond side, as positive for the near-term outlook. Asian markets are mixed this morning with Japanese stocks higher on the back of solid data while Chinese markets are lower as developers give up some of their gains form yesterday. US futures a tad higher while European futures are marginally lower.

FI: European yields rose significantly yesterday following the stronger-than-expected PMI data and the German government plan to suspend the debt brake next year. 10Y Bund yields rose 7bp, while the 2s10s curve bear steepened 4bp throughout the day. Long-term inflation metrics (e.g. the 5y5y EUR inflation swap) spiked in reaction to the strong PMI data. Peripherals performed generally in line with the core. In the Netherlands, the surprising election result on Wednesday - putting far-right Geert Wilders in the lead to become PM - did not have any significant impact on spreads. US markets were closed due to the Thanksgiving holiday.

FX: In line with our expectation, the Riksbank yesterday decided to leave the repo rate unchanged at 4.00% and EUR/SEK moved higher on the hawkish "unchanged" decision. EUR/USD had a relatively quiet day due to the Thanksgiving holiday, trading around the 1.09 mark. EUR/GBP jumped lower during yesterday's session as UK preliminary PMIs for November came in significantly higher than expected. Combined with the fiscal measures announced Wednesday in the Autumn Statement this leaves a worrying backdrop with a risk of more persistent inflation for the Bank of England.

Credit: CDS indices were broadly unchanged yesterday with iTraxx Main closing at 68bp (unchanged) and Xover 2bp tighter at 375bp. Following some busy days, the EUR primary market was nearly quiet with only one corporate deal being priced.

USD/JPY: Japan’s Inflation Accelerated, A Struggle for Bulls at 50-day Moving Average

- Resurgence of inflationary pressures in Japan due to higher import costs from energy prices.

- The Bank of Japan may face renewed political pressure to normalize its current dovish monetary policy stance to negate significant JPY’s weakness.

- Recent uptick in 10-year JGB yield from an 11-week low may trigger another potential down leg in USD/JPY.

- Watch the 150.20 key short-term resistance on USD/JPY.

The latest nationwide Japan core inflation for October (excluding fresh food) ticked higher for the first time in four months to 2.9% y/y (slightly below the consensus of 3% y/y) from September’s 13-month low of 2.8% y/y. Overall, it has stayed above the Bank of Japan (BoJ)’s 2% inflation target for the consecutive 19th month.

Meanwhile, the core-core inflation rate (excluding fresh food & energy) inched lower to 4% y/y (but still its highest level since 1981) in October from September 4.2% y/y, the second consecutive month of softness which indicates that the recent rallies seen in benchmark oil prices from August to September were likely one of the main drivers that contribute to the resurgence of inflationary pressures in October.

Economic activities in the services sector have started to improve slightly in November where the flash Services PMI rose to 51.7 from 51.6 in October but still below its 12-month average of around 53.5.

In contrast, manufacturing activities have continued to be in the doldrums as the flash Manufacturing PMI for November contracted further to 48.1 from 48.7 in October, its sixth consecutive month of contraction and its steepest decline since February 2023.

Potential mounting political pressure on BoJ due to higher imported inflationary pressures

Overall, it’s a mixed set of economic readings but the recent months of elevated imported inflation via the lagged effects of higher oil prices that drove up import costs have put Bank of Japan Governor Ueda in a tight spot as he has so far “stubbornly” remained dovish on Japan’s monetary policy and adopted a wait & see approach for further evidence on substantial wage increases before embarking on a path of normalization away from negative short-term interest rates.

The current dovish stance from BoJ has led the JPY to plummet to a 33-year low against the US dollar and is the current primary driver of higher import costs, in turn, putting increasing political pressure on BoJ to act fast to negate this knock-on effect on elevated import costs in order to boost consumer and business sentiment as Japanese Prime Minster Kishida’s most recent approval ratings declined to the lowest level in his current two-year premiership.

The USD/JPY has staged a rebound of +260 pips since the start of this week after it plummeted to a 10-week low print of 147.15 on Tuesday, 21 November in line with broad-based US dollar weakness seen last week.

The recent rebound is likely due to technical factors as the prior steep decline from its 151.95 major resistance has hit oversold conditions on several short-term (hourly) momentum indicators.

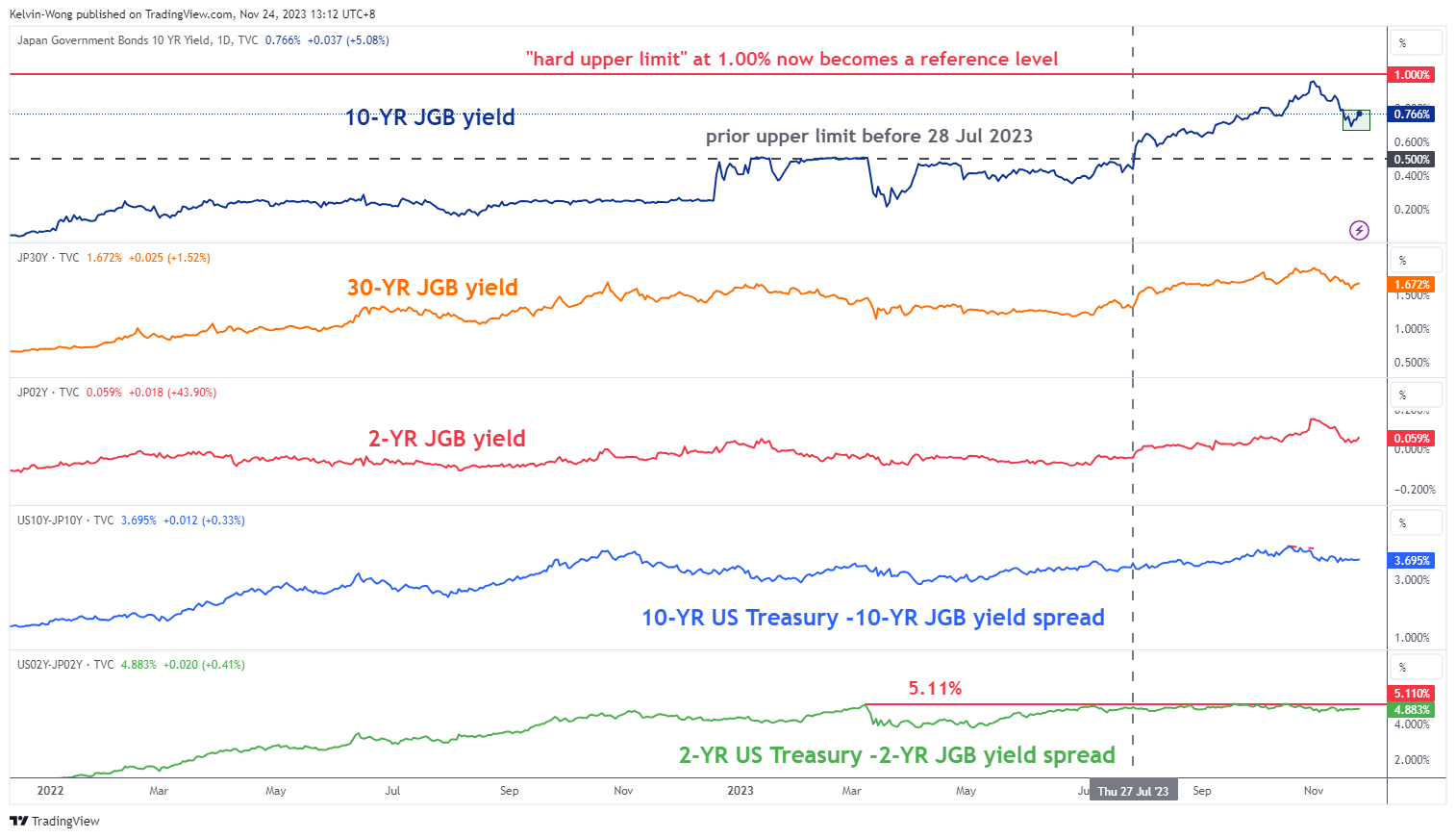

Further shrinkage in the 10-year US Treasury-JGB yield premium may trigger further downside pressure in USD/JPY

Fig 1: JGB yields with US Treasury-JGB yield spreads as of 24 Nov 2023 (Source: TradingView, click to enlarge chart)

The current elevated inflationary pressure in Japan has reinforced a further uptick in the 10-year Japanese government bond (JGB) yield that continued to rise to 0.77% at this time of the writing from an 11-week low of 0.69% printed on Tuesday, 21 November.

Hence, the latest recovery seen in n the 10-year JGB yield is likely to put downside pressure on the declining 10-year US Treasury-JGB yield premium since 19 October 2023 which in turn may undermine the recent 3-day US dollar rebound against the JPY.

Short-term minor corrective rebound in USD/JPY may have reached its terminal point

Fig 2: USD/JPY medium-term trend as of 24 Nov 2023 (Source: TradingView, click to enlarge chart)

Fig 3: USD/JPY minor short-term trend as of 24 Nov 2023 (Source: TradingView, click to enlarge chart)

Technically speaking, the +260 pips rebound seen in the USD/JPY from its 21 November 2023 low of 147.15 has started to show bullish exhaustion signals at its 20 and 50-day moving averages.

The short-term hourly RSI oscillator has continued to exhibit bearish momentum readings after an earlier bearish divergence condition being flashed out at its overbought zone on Wednesday, 22 November.

Watch the 150.20 key short-term pivotal resistance (also the 20-day moving average & close to the 61.8% Fibonacci retracement of the prior minor decline from 13 November 2023 high to 21 November 2023 low) and a break below the near-term support of 148.40 may expose the next intermediate supports of 147.30 and 146.60/20.

However, a clearance above 150.20 invalidates the bearish tone for a squeeze up towards the next intermediate resistance at 151.40 (minor swing high of 16 November 2023).