Sample Category Title

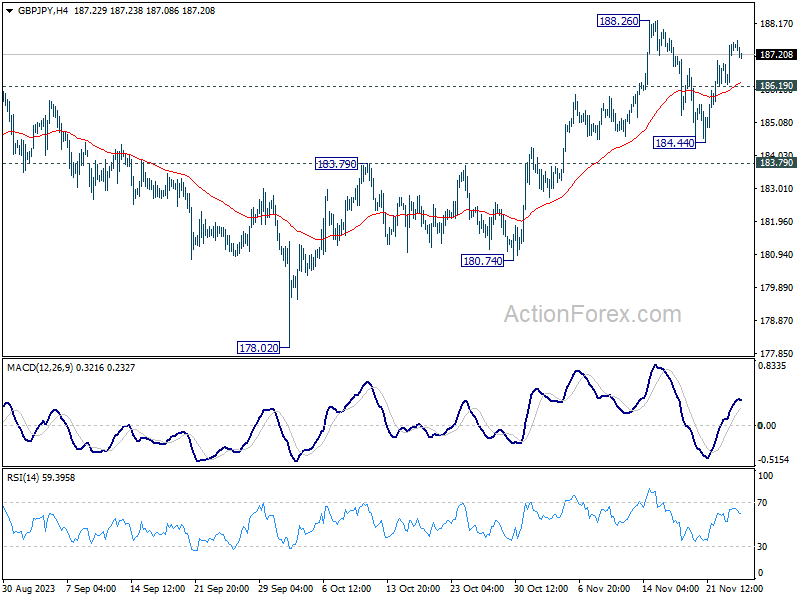

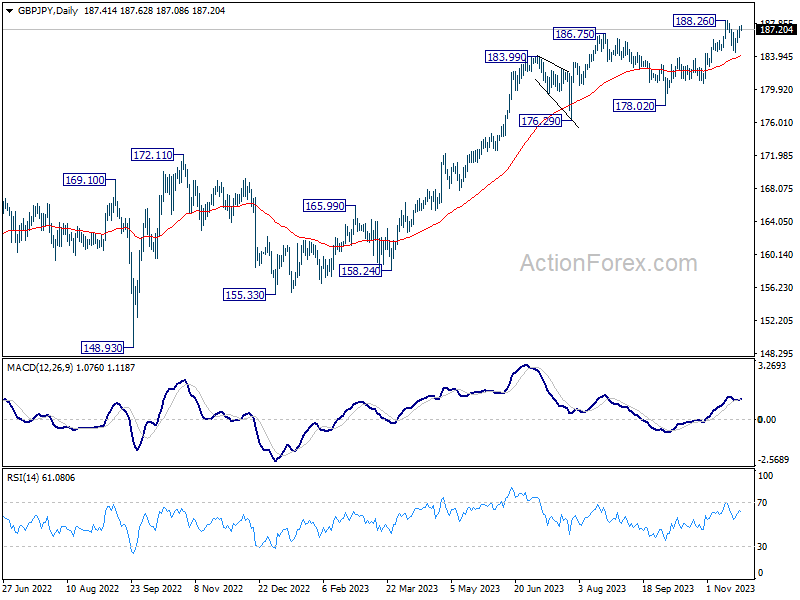

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.64; (P) 187.12; (R1) 187.94; More...

As long as 186.19 minor support holds, GBP/JPY's rebound from 184.44 is still expected to continue to retest 188.26 high. Decisive break there will resume larger up trend. On the downside though, below 186.19 will extend the pattern from 188.26 with another fall to 184.44, and possibly further to 183.79 resistance turned support.

In the bigger picture, as long as 180.74 support holds, larger up trend from 123.94 (202 low) should still be in progress, next target is 195.86 (2015 high). However, firm break of 180.74 will now argue that a medium term top is formed, possibly in bearish divergence condition in D MACD, and bring deeper fall back to 178.02 support.

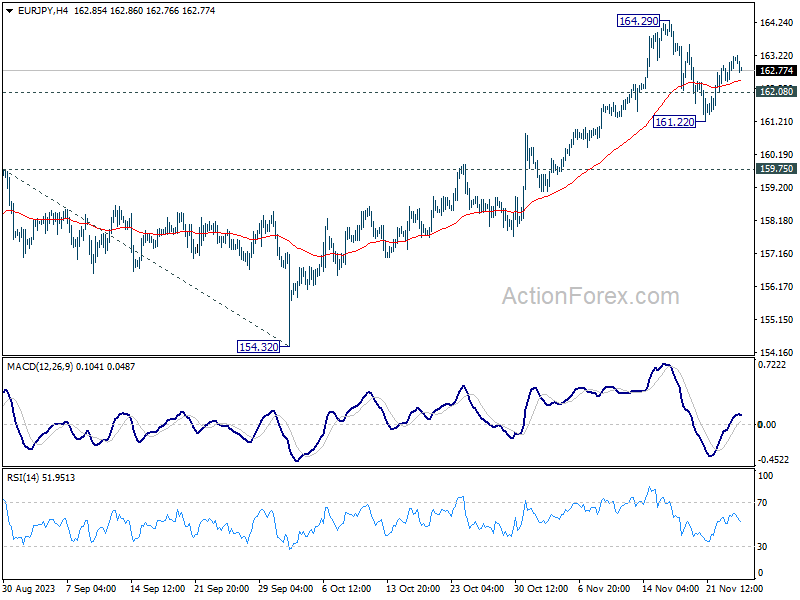

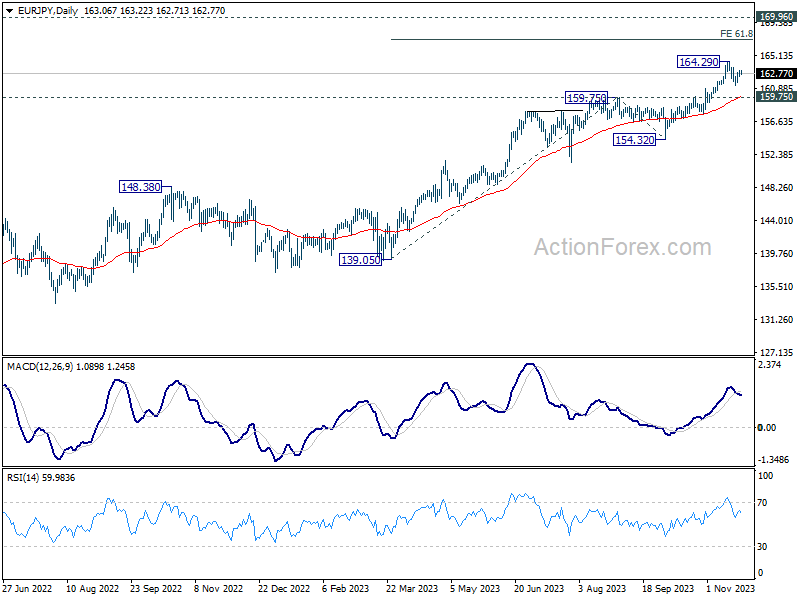

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.63; (P) 162.91; (R1) 163.38; More....

With 162.08 minor support intact, EUR/JPY's rebound from 161.22 could extend further to retest 164.29 high. Firm break there will resume larger up trend. On the downside, however, break of 162.08 will turn bias back to the downside, to resume the fall from 164.29 through 161.22 towards 159.75 resistance turned support.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 169.96 (2008 high). On the downside, break of 159.75 resistance turned support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.

Yen Sees Mild Uptick Following Mixed CPI and PMIs, A Signal for Buyers’ Return?

Trading activity is rather subdued in Asian session today, with most major currency pairs and crosses hovering within yesterday's range.

Yen is showing a slight recovery, albeit in the context of mixed inflation and PMI data. While Japan's core CPI remains persistently above BoJ's target, the latest figures haven't provided a strong impetus for the central bank to shift away from its negative interest rate policy or to alter its yield curve control strategy. BoJ officials have emphasized the importance of a sustainable wage-price spiral, and they are likely to await the results of wage negotiations early next year before making significant policy decisions.

Throughout the week, New Zealand Dollar has emerged as the strongest currency, additionally supported by much better than expected retail sales data released today. Australian Dollar and British Pound Sterling are following as the second and third strongest.

On the other end of the spectrum, Euro is the weakest, closely followed by Dollar. However, it's worth noting that Euro's current position appears to be more about consolidating recent gains against Dollar, and EUR/USD maintains near-term bullish outlook. A reversal in Euro and Dollar's positions could occur once this consolidation phase concludes.

Yen, currently positioned as the third weakest, is in a phase of digesting its gains from the previous week. However, there is potential for Yen to ascend in the rankings before the week concludes. Canadian Dollar and Swiss Franc are displaying mixed performances.

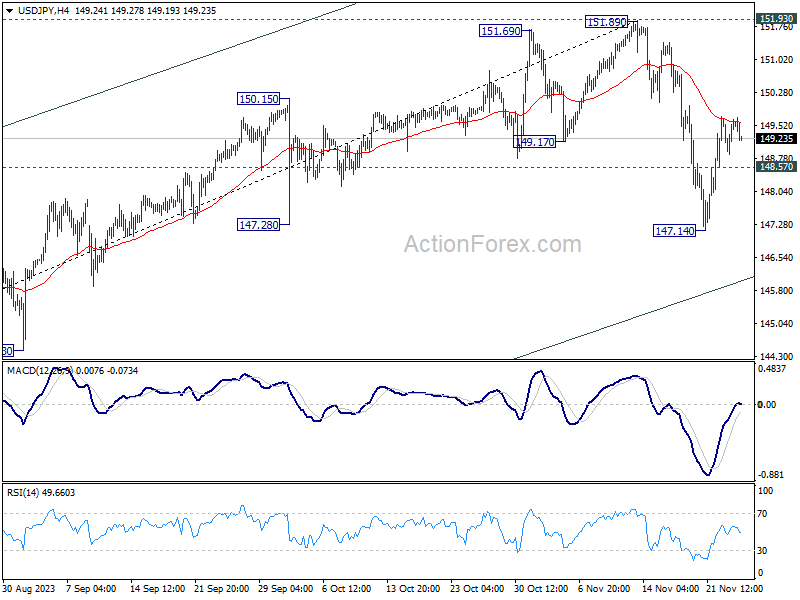

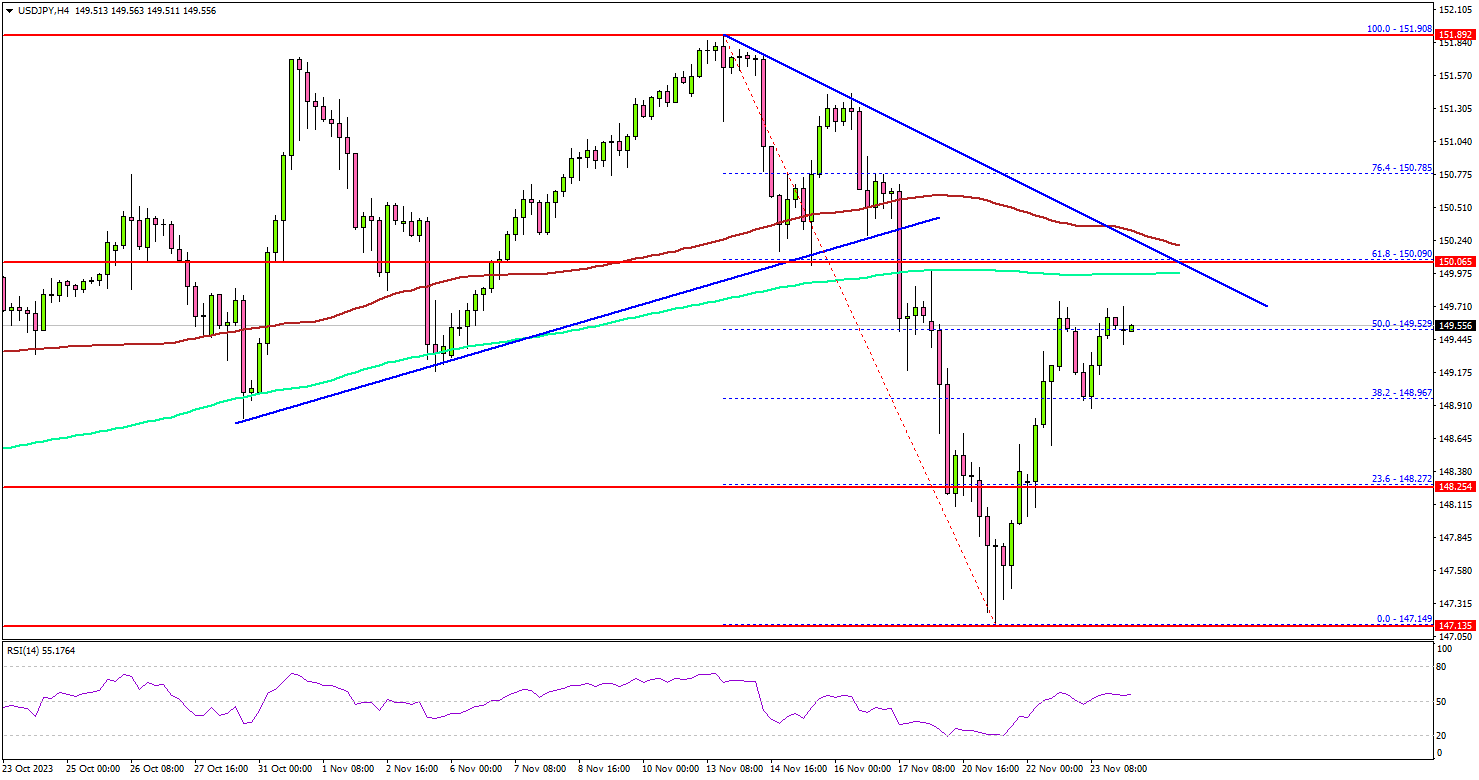

From technical analysis standpoint, USD/JPY's recovery from 147.14 is so far still capped by 55 4H EMA. Fall from 151.89 is still in favor to continue, and break of 148.57 minor support will bring retest of 147.14 support first. However, sustained trading above the EMA will retain near term bullishness, and bring a test on 151.89 high. Market watchers will be looking to see if this scenario plays out this week or in the next.

In Asia, Nikkei closed up 0.55%. Hong Kong HSI is down -1.48%. China Shanghai SSE is down -0.63%. Singapore Strait Times is down -0.52%. Japan 10-year JGB yield is up 0.0431 at 0.774.

BoE's Pill stresses persistence in inflation fight

In a Financial Times interview, BoE Chief Economist Huw Pill emphasized the need for the MPC to avoid prematurely "declaring victory" in the fight against inflation, noting that CPI is still considerably above BoE's 2% target, currently at 4.6%.

Pill acknowledged UK's economic slowdown, noting "slower growth in activity and employment." However, he assessed that the current inflation scenario is "more supply-driven rather than demand-driven." Weakening in economic activity is not necessarily leading to a reduction in inflationary pressures, as might typically be expected.

Analyzing recent economic indicators, Pill observed more evidence of "sort of stubborn, high-level rates of inflation" and and growth that are "stronger" than being compatible with 2% inflation over the medium term.

He also argued that if the slowdown in economic activities and employment growth is linked to a decline in the economy's supply performance, rather than a drop in demand, it wouldn't create the necessary slack to ease domestically generated inflation.

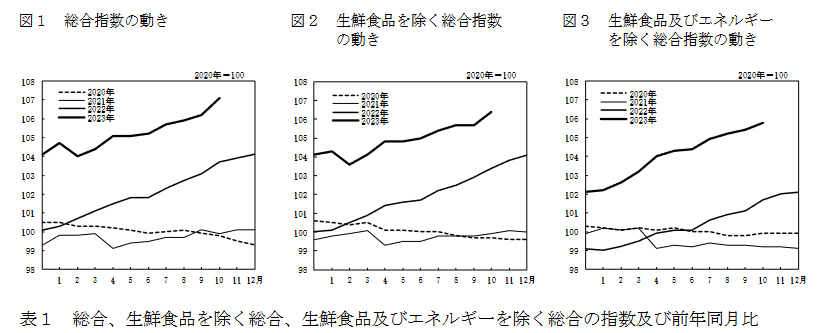

Japan's CPI core rises to 2.9%, above BoJ target for 19th mth, services prices surge

Japan's core CPI, which excludes fresh food prices, rose slightly from 2.8% yoy to 2.9% yoy in October, falling just below expected 3.0% yoy. Notably, this core CPI has stayed above BoJ's target of 2% for the 19th consecutive month, indicating persistent inflationary pressures.

Headline CPI, which includes all items, accelerated from 3.0% yoy to 3.3% yoy. However, core-core CPI, which excludes both food and energy, showed a slight deceleration, dropping from 4.2% yoy to 4.0% yoy. Despite this decrease, core-core CPI has remained above 4.0% for seven consecutive months, highlighting sustained inflation in areas beyond just the volatile items.

Breaking down the details, energy prices saw a significant decrease of -8.5% yoy. In contrast, food prices continued to climb, recording a 7.6% yoy increase. Durable goods also experienced a price rise of 3.2% yoy. Notably, services prices surged by 2.1% yoy, marking the fastest gain since 1993. This sharp increase in services prices underscores the broadening of inflationary pressures within the Japanese economy.

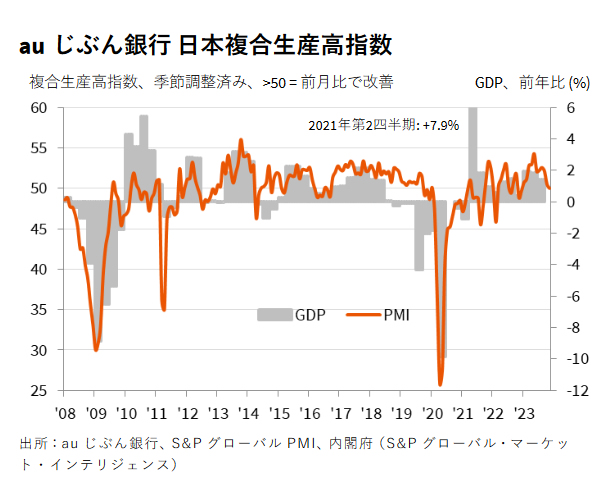

Japan's PMIs: Manufacturing contracts, services slightly improve

Japan's PMI for November shows a continuing contraction in the manufacturing sector and a slight improvement in services.

Manufacturing PMI dropped from 48.7 to 48.1, falling below the expected 48.8 and marking another month below the crucial 50.0 threshold, which separates contraction from expansion. This ongoing contraction has been the trend since June.

Conversely, Services PMI saw a marginal increase, moving up from 51.6 to 51.7, indicating a slight expansion in this sector. However, Composite PMI, which combines both manufacturing and services, edged down from 50.5 to exactly 50.0, highlighting stagnation in overall private sector activity.

Usamah Bhatti, an economist at S&P Global Market Intelligenc said: "Activity at Japanese private sector firms stagnated midway through the fourth quarter of 2023." This stagnation is further reflected in the demand conditions, which Bhatti noted remained "muted in November and were little-changed from October."

New Zealand retail sales volume flat in Q3, value up 1.5% qoq

In New Zealand, Q3 2023 saw retail sales volumes remain unchanged at 0.0% qoq, defying expectations of a -0.8% decline.

However, a contrasting trend emerged in the sales value, which increased by 1.5% qoq, indicating a disparity between the number of goods sold and their monetary value.

On an annual basis, there was a -3.4% yoy decrease in sales volume, whereas sales value saw 1.1% yoy increase.

These divergences should be reflective of inflationary pressures and corresponding shift in consumer purchasing patterns.

Looking ahead

Germany Q3 GDP final and Ifo business climate will be released in European session. Later in the day, Canada retail sales and US PMIs will be featured.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.63; (P) 162.91; (R1) 163.38; More....

With 162.08 minor support intact, EUR/JPY's rebound from 161.22 could extend further to retest 164.29 high. Firm break there will resume larger up trend. On the downside, however, break of 162.08 will turn bias back to the downside, to resume the fall from 164.29 through 161.22 towards 159.75 resistance turned support.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 169.96 (2008 high). On the downside, break of 159.75 resistance turned support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q3 | 0.00% | -0.80% | -1.00% | -0.90% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q3 | 1.00% | -1.50% | -1.80% | -1.60% |

| 23:30 | JPY | National CPI Y/Y Oct | 3.30% | 3.00% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Oct | 2.90% | 3.00% | 2.80% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Oct | 4.00% | 4.20% | ||

| 00:01 | GBP | GfK Consumer Confidence Nov | -24 | -27 | -30 | |

| 00:30 | JPY | Manufacturing PMI Nov P | 48.1 | 48.8 | 48.7 | |

| 00:30 | JPY | Services PMI Nov P | 51.7 | 51.6 | ||

| 07:00 | EUR | Germany GDP Q/Q Q3 F | -0.10% | -0.10% | ||

| 09:00 | EUR | Germany IFO Business Climate Nov | 87.5 | 86.9 | ||

| 09:00 | EUR | Germany IFO Current Assessment Nov | 89.4 | 89.2 | ||

| 09:00 | EUR | Germany IFO Expectations Nov | 85.7 | 84.7 | ||

| 13:30 | CAD | Retail Sales M/M Sep | 0.00% | -0.10% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Sep | -0.30% | 0.10% | ||

| 14:45 | USD | Manufacturing PMI Nov P | 49.8 | 50 | ||

| 14:45 | USD | Services PMI Nov P | 50.4 | 50.6 |

BoE’s Pill stresses persistence in inflation fight

In a Financial Times interview, BoE Chief Economist Huw Pill emphasized the need for the MPC to avoid prematurely "declaring victory" in the fight against inflation, noting that CPI is still considerably above BoE's 2% target, currently at 4.6%.

Pill acknowledged UK's economic slowdown, noting "slower growth in activity and employment." However, he assessed that the current inflation scenario is "more supply-driven rather than demand-driven." Weakening in economic activity is not necessarily leading to a reduction in inflationary pressures, as might typically be expected.

Analyzing recent economic indicators, Pill observed more evidence of "sort of stubborn, high-level rates of inflation" and and growth that are "stronger" than being compatible with 2% inflation over the medium term.

He also argued that if the slowdown in economic activities and employment growth is linked to a decline in the economy's supply performance, rather than a drop in demand, it wouldn't create the necessary slack to ease domestically generated inflation.

USD/JPY Recovery Could Face Uphill Task – Here’s Why

Key Highlights

- USD/JPY is attempting a fresh increase from the 147.15 zone.

- A connecting bearish trend line is forming with resistance near 150.00 on the 4-hour chart.

- EUR/USD is showing positive signs above the 1.0850 support.

- GBP/USD could extend its rally above the 1.2550 resistance.

USD/JPY Technical Analysis

The US Dollar declined heavily from the 151.90 zone against the Japanese Yen. USD/JPY declined below 150.00 and 149.20 before the bulls took a stand.

Looking at the 4-hour chart, the pair traded as low as 147.14 before it started a decent recovery wave. There was a move above the 148.40 and 148.50 resistance levels. The pair even tested the 50% Fib retracement level of the downward move from the 151.90 swing high to the 147.14 low.

However, the pair is still below the 150.00 barrier, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

There is also a connecting bearish trend line forming with resistance near 150.00 on the same chart. The next key resistance is near the 150.20 level. The main resistance is now near the 150.50 level. A close above the 150.50 zone could open the doors for more upsides. The next stop for the bulls might be 152.00.

If not, the pair might start a fresh decline below the 148.80 support. The first major support is now forming near the 148.50 level. The next key support sits at 148.00, below which the pair could test the 147.50 pivot level in the near term.

Looking at GBP/USD, the pair gained strength above the 1.2500 level and it could even climb toward the 1.2620 resistance.

Economic Releases

- US Manufacturing PMI for Nov 2023 (Preliminary) – Forecast 49.8, versus 50.0 previous.

- US Services PMI for Nov 2023 (Preliminary) – Forecast 50.4, versus 50.6 previous.

Japan’s CPI core rises to 2.9%, above BoJ target for 19th mth, services prices surge

Japan's core CPI, which excludes fresh food prices, rose slightly from 2.8% yoy to 2.9% yoy in October, falling just below expected 3.0% yoy. Notably, this core CPI has stayed above BoJ's target of 2% for the 19th consecutive month, indicating persistent inflationary pressures.

Headline CPI, which includes all items, accelerated from 3.0% yoy to 3.3% yoy. However, core-core CPI, which excludes both food and energy, showed a slight deceleration, dropping from 4.2% yoy to 4.0% yoy. Despite this decrease, core-core CPI has remained above 4.0% for seven consecutive months, highlighting sustained inflation in areas beyond just the volatile items.

Breaking down the details, energy prices saw a significant decrease of -8.5% yoy. In contrast, food prices continued to climb, recording a 7.6% yoy increase. Durable goods also experienced a price rise of 3.2% yoy. Notably, services prices surged by 2.1% yoy, marking the fastest gain since 1993. This sharp increase in services prices underscores the broadening of inflationary pressures within the Japanese economy.

Japan’s PMIs: Manufacturing contracts, services slightly improve

Japan's PMI for November shows a continuing contraction in the manufacturing sector and a slight improvement in services.

Manufacturing PMI dropped from 48.7 to 48.1, falling below the expected 48.8 and marking another month below the crucial 50.0 threshold, which separates contraction from expansion. This ongoing contraction has been the trend since June.

Conversely, Services PMI saw a marginal increase, moving up from 51.6 to 51.7, indicating a slight expansion in this sector. However, Composite PMI, which combines both manufacturing and services, edged down from 50.5 to exactly 50.0, highlighting stagnation in overall private sector activity.

Usamah Bhatti, an economist at S&P Global Market Intelligence said: "Activity at Japanese private sector firms stagnated midway through the fourth quarter of 2023." This stagnation is further reflected in the demand conditions, which Bhatti noted remained "muted in November and were little-changed from October."

New Zealand retail sales volume flat in Q3, value up 1.5% qoq

In New Zealand, Q3 2023 saw retail sales volumes remain unchanged at 0.0% qoq, defying expectations of a -0.8% decline.

However, a contrasting trend emerged in the sales value, which increased by 1.5% qoq, indicating a disparity between the number of goods sold and their monetary value.

On an annual basis, there was a -3.4% yoy decrease in sales volume, whereas sales value saw 1.1% yoy increase.

These divergences should be reflective of inflationary pressures and corresponding shift in consumer purchasing patterns.

Cliff Notes: Central Banks Remain Alert to Inflation Risks

Key insights from the week that was.

In Australia, the November RBA meeting minutes presented a detailed account of the Board’s deliberations and their assessment of the risks. The Board recognised recent evidence that pointed to lingering resilience in the labour market and domestic demand, alongside the fact that the moderation in underlying inflation is tracking a slower pace than expected. These developments have renewed concerns over inflation expectations, with the Board noting “growing signs of a mindset among businesses that any cost increases could be passed onto consumers”, a worrisome development given that only a “modest” increase in inflation expectations would make it “significantly” harder to return inflation to target.

Such observations were consistent with the Board’s eventual decision to raise the cash rate in November. However, they do not convincingly speak to a need to raise interest rates further. To justify another hike, further upside surprises for inflation and demand are necessary. We instead anticipate a deceleration in inflation and the labour market in Q4 and beyond, and so continue to expect the cash rate will remain at its current level until Q3 2024, when we forecast the next rate cutting cycle to begin.

In addition to inflation and the immediate policy outlook, in her speech this week, RBA Governor Bullock also outlined a number of key developments underway at the RBA to improve the Board’s engagement with staff and the RBA’s communications. RBA Governor Bullock also appeared on a panel with Productivity Commission Chair Danielle Wood. Productivity was a key theme and is also the topic of Westpac Chief Economist Luci Ellis' weekly essay.

In the US, the FOMC released the minutes of their October/ November meeting. Members noted a “further softening in labour market conditions” is necessary for the Committee to feel comfortable inflation will return to target. After the meeting, evidence of such a turn was provided by the October employment report, while the subsequent downside surprise on both headline and core inflation are additional steps in the right direction. Looking ahead, liaison reports of businesses finding it more difficult to pass on price increases to consumers point to a further softening in demand and inflation which, in time, should justify our and the market’s expectations of around 100bps of US rate cuts through 2024.

While yet to receive equal treatment, let alone priority, downside risks to activity are clearly on the Committee’s radar. The cumulative impact of rate hikes are yet to be felt, and “persistent changes in financial conditions could have implications for the path of monetary policy”.

Across Europe, the UK and Canada, promising data on inflation and weak activity growth has also seen markets recently price in rate cuts from mid-2024, in effect easing financial conditions. Yet to be convinced the danger has passed, central bank authorities were therefore kept busy this week emphasising that rate cuts are currently not on their horizon.

Of particular note, after Canadian inflation eased to 3.1%yr in October from 3.8%yr in September, Bank of Canada's Governor Macklem noted that the "excess demand in the economy that made it too easy to raise prices is now gone" – a statement that alludes to the removal of upside risks for inflation, but not enough progress to begin considering rate cuts.

In the UK meanwhile, Bank of England Governor Bailey appeared before a Treasury Committee. Though Bailey indicated that rates were at the top of the “table mountain”, the Committee are still wary of upside surprises given services inflation’s momentum and strong wage growth. Communication during the session therefore contradicted market pricing at the time for a rate cut in the first half of 2024.

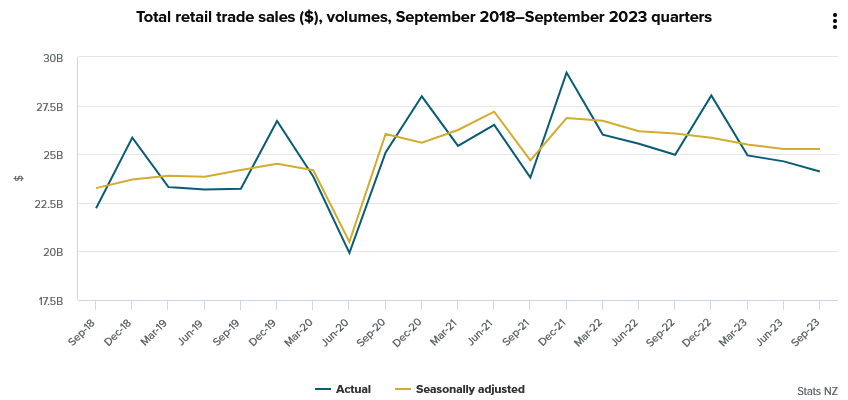

NZ First Impressions: Retail Trade September Quarter 2023

Retail spending was stronger than expected in the September quarter. However, the longer-term trend remains soft.

- September quarter real retail sales (volumes): Flat (Prev: -0.9%)

- Westpac f/c: -2.0%, Market -0.7%

- September quarter nominal sales level: 1.5% (Prev: -0.2%)

- Annual changes (September 2023 vs September 2022)

- Nominal sales: +1.1%

- Volume of goods sold: -3.4%

Retail spending was stronger than we and other analysts expected in the September quarter. However, digging into the details, we’re still seeing signs of softness, and we expect a further slowdown over the coming months.

Looking into the details of the September spending report, nominal spending levels were up 1.5% over the quarter. However, that rise was entirely due to price increases. The volume of goods sold was unchanged. That’s despite strong population growth. In other words, individual households are actually taking home fewer goods even as they splash out more cash.

Looking at the breakdown of spending in the September quarter, we did see increases in spending in the hospitality sector, potentially reflecting the boost to demand from events such as the FIFA Women’s World cup.

Spending in interest sensitive areas was mixed. Sales of items like hardware and recreational equipment did post solid gains. However, that was balanced against reduced spending on motor vehicles and items like electronics and clothing.

What does this tell as about the strength of spending?

The longer-term trend gives us a clearer picture of what’s happening to spending appetites.

Over the past year, nominal spending levels have only risen by 1.1%. Over that same period, prices rose by 4.6%, and the population increased by more than 2%.

Putting that all together leaves us with a soft picture of underlying spending appetites. The volume of goods sold fell by more than 3% over the past year. And on a per capita basis, the fall in spending levels has been closer to 5%.

Looking ahead, we expect spending to continue cooling through the December shopping season and into the New Year. Many borrowers are continuing to roll onto higher mortgage rates, consumer price inflation remains strong, and economic growth and the labour market are softening. That combination points to significant pressure on household balance sheets. However, strong population growth will help to limit the downside for spending in the face of those headwinds.

Implications for GDP growth

Today’s result was stronger than expected. We’re currently forecasting a small 0.1% contraction in September quarter GDP. We’ll review that number over the coming weeks as more data comes to hand.