Sample Category Title

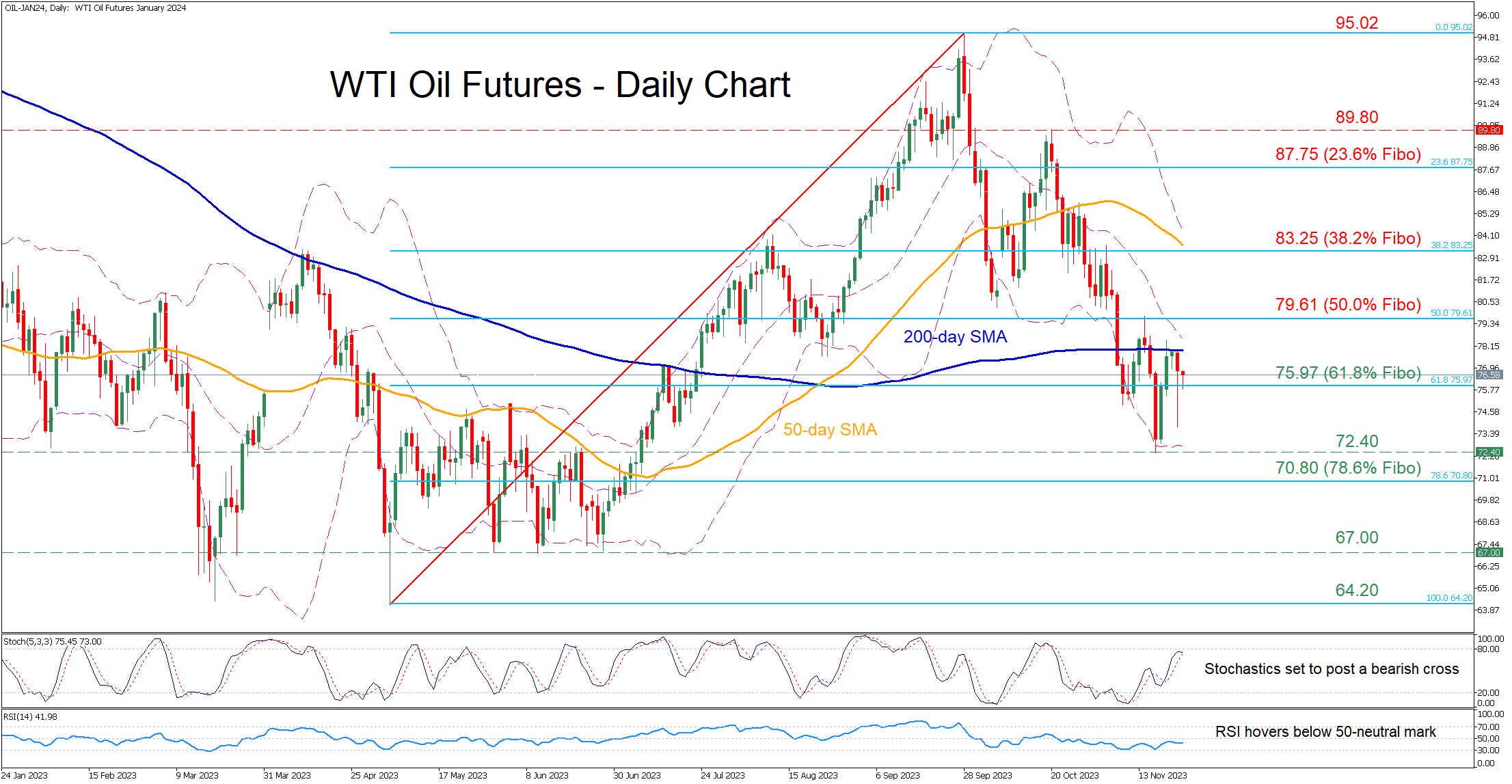

WTI Oil Futures Held Down by 200-day SMA

- WTI futures fall to a 4-month low before attempting a recovery

- But the 200-day SMA repeatedly rejects their rebound

- Momentum indicators suggest that bears are in charge

WTI oil futures (January delivery) have been on the retreat since their October peak of 89.85, breaking aggressively below historical support zones. Last week, the price dropped to its lowest levels since July before recouping some losses, but the 200-day simple moving average (SMA) has been curbing its upside.

Should the 200-day SMA hold its ground and the price reverse lower, immediate support could be met at 75.97, which is the 61.8% Fibonacci retracement of the 64.20-95.02 upleg. A break beneath that region could pave the way for the recent four-month bottom of 72.40. Even lower, the 78.6% Fibo of 70.80 could provide downside protection.

Alternatively, if oil extends its short-term bounce, the bulls may attack the 50.0% Fibo of 79.61. Piercing through that area, the price could advance towards the 38.2% Fibo of 83.25. Further upside attempts could then stall around the 23.6% Fibo of 87.75.

In brief, WTI oil futures remain under relentless downside pressure, recording consecutive lower lows. However, a clear jump above the 200-day SMA could shift the short-term picture back to bullish.

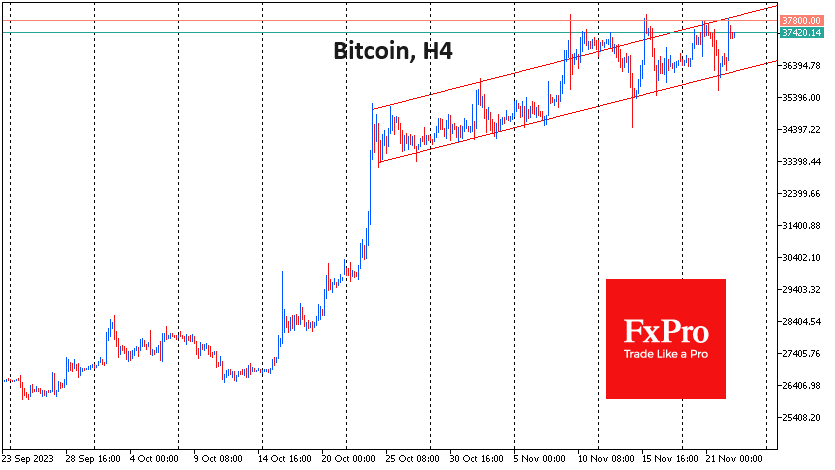

Bitcoin’s Ascending Channel and Ethereum’s Bounce Back

Market picture

Crypto market capitalisation rose 2.4% in 24 hours to $1.42 trillion, with gains across a vast range of altcoins from +0.4% (BNB) to +15.6% (Uniswap). The Crypto Fear and Greed Index added 4 points to 66 (Greed), though it’s still some way off the indicator’s November peak of 74.

Bitcoin bounces around in an ascending channel, hitting its three-week upper resistance of $37.8K on Wednesday evening. An intensifying sell-off thwarts attempts to heat the price, but the pullbacks have become less deep over the past three weeks, suggesting the building up of bullish sentiment. At the same time, this relative stabilisation in the range removes local overbought conditions, allowing to stick to gains of the previous advance. A break of resistance could see a quick rise above $40K.

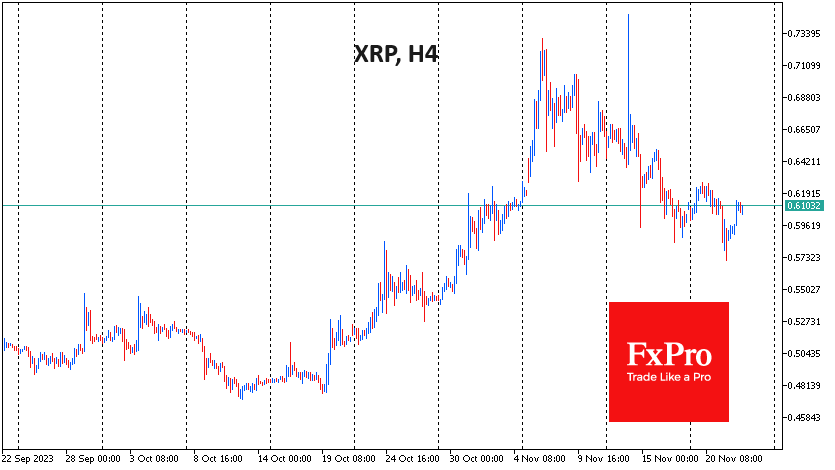

XRP received buyers’ support on Wednesday after touching the 50-day moving average, giving it a chance to stabilise after a pullback of more than 20% from its early November peak.

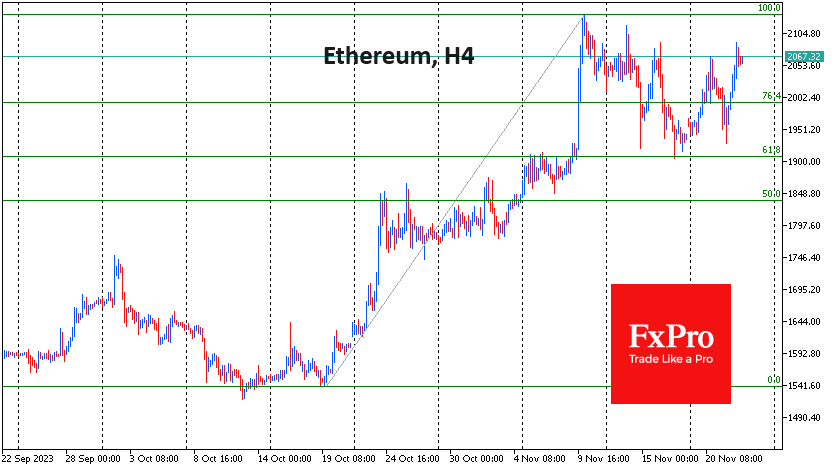

However, the buying of Ethereum on its dip below $2,000 on Wednesday was more notable. Active buying in the world’s second most-capitalised coin took the price back to $2060, near the top of the range since the 10th of November.

News background

Grayscale met with the SEC to discuss converting the GBTC ETF into a spot bitcoin ETF. Grayscale officials announced they signed a fund servicing agreement with Bank of New York Mellon. The institution will act as GBTC’s counterparty, facilitating the issuance and redemption of shares.

In a joint statement with the DOJ, US Treasury Secretary Janet Yellen said Binance had paid for its greed and non-compliance with the law.

Binance will remain one of the largest crypto exchanges for two to three years. The agreements with US authorities are a positive outcome despite the lack of SEC inclusion, Matrixport believes.

Mt. Gox’s creditors will start receiving payments before the end of this year, the bankrupt exchange’s trustee Nobuaki Kobayashi assured. However, given the large number of creditors, the payouts will likely continue until 2024. Mt. Gox’s creditors have been expecting repayment for nearly a decade, and the payment deadline has been repeatedly postponed.

Meanwhile, the crypto exchange HTX (formerly Huobi) and the HECO network were hacked. Unknown persons withdrew assets worth $110 million. The head of HTX has already confirmed the fact of the hack.

Lastly, former Revolut VP of development Hannes Graah, ex-employee of Coinbase and Spotify, backed by Galaxy Digital, will launch the Zeal cryptocurrency wallet in Q1 2024.

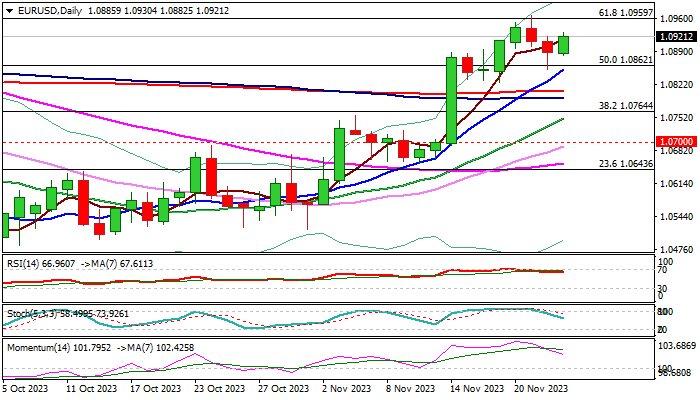

EUR/USD: Bulls Pausing for Consolidation

EURUSD regained traction early Thursday and reduced downside risk, as two-day pullback was strongly rejected on Wednesday.

Technical studies are mixed on daily chart as bullish momentum is fading while moving averages remain in bullish configuration, lacking clearer direction signal, although overall picture is bullish.

German Nov PMI’s came above forecasts and lifted the single currency further, offsetting weaker than expected French PMI figures.

Markets await release of EU PMI, which could provide further boost if in line with or above consensus.

Near-term action is held within two Fibo levels, 1.0862 (broken 50% of 1.1275/1.0448, reinforced by rising 10DMA) and 1.0959 (cracked 61.8%) with firm break on either side to generate fresh direction signal.

Loss of 1.0862 pivot to signal deeper correction and expose targets at 1.0808 (200DMA) and 1.0795 (weekly cloud base).

Conversely, bulls may accelerate beyond psychological 1.10 level on sustained break above 1.0959 Fibo barrier.

Caution on expected lower volumes due to US Thanksgiving Day holiday.

Res: 1.0959; 1.1000; 1.1065; 1.1080.

Sup: 1.0882; 1.0862; 1.0808; 1.0813.

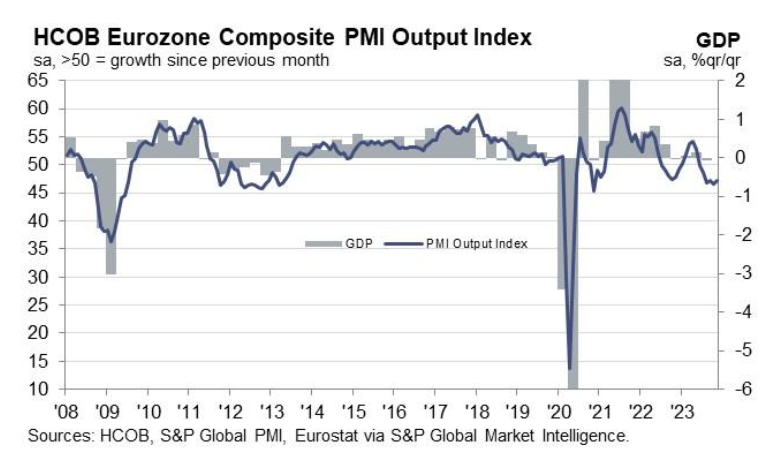

Eurozone PMI composite rose to 47.1, technical recession ongoing

Eurozone's PMI data for November shows marginal improvement but continues to indicate broader recessionary trends. Manufacturing PMI increased slightly from 43.1 to a six-month high of 43.8, exceeding expectations of 43.4. Similarly, Services PMI rose from 47.8 to 48.2, marginally above the predicted 48.0. Consequently, Composite PMI, which combines both sectors, climbed from 46.5 to 47.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, summarized the situation as, "The Eurozone economy is stuck in the mud." Their nowcast model suggests the likelihood of a second consecutive quarter of GDP contraction, meeting the technical criteria for a recession.

Inflation remains a significant issue, particularly in the services sector, where price increases have accelerated due to "astonishingly rapid and even accelerating" rising input costs. De la Rubia attributes these cost increases primarily to higher wages.

The employment situation is also expected to worsen. Initially impacting industrial sector jobs, the economic downturn is poised to affect employment in services sector as well. This could lead to an uptick in Eurozone's unemployment rate, which has so far been relatively stable.

Region-specific dynamics show contrasting trends within Eurozone. Germany's composite index has improved, signaling some positive movement, whereas France continues to show a weakening trend. De la Rubia also points out the challenges faced by Germany, particularly in public investments due to restrictions imposed by the constitutional court's debt brake, which relegate Germany's economy "to the back seat in 2024".

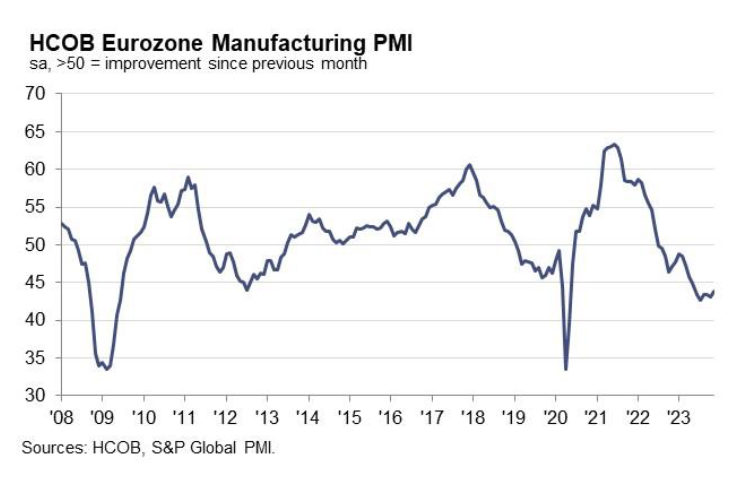

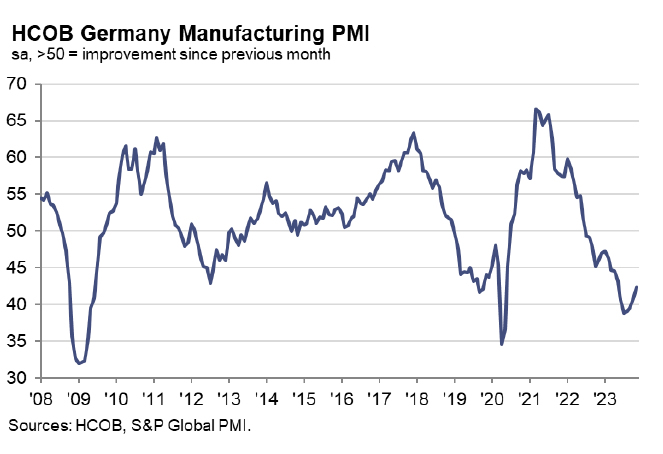

Germany PMI composite rose to 47.1, milder recession but inflation remains high

Germany's November PMI data indicates a modest improvement in its economic situation, albeit still within recessionary bounds. Manufacturing PMI rose from 40.8 to 42.3, marking a six-month high, and Services PMI increased from 48.2 to 48.7. Composite PMI, climbed from 45.9 to a four-month high of 47.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted a cautious optimism about the German economy. He observed, "Despite remaining in recession territory, the rate of slowdown has eased noticeably."

While, the PMI data aligns with the perspective that Germany entered a recession in the third quarter of this year, the recession's depth might be less severe than initially anticipated. According to de la Rubia's nowcasting model, GDP is expected to see -0.7% decline in Q4, an improvement from previous forecasts of -0.9% decline.

Despite these signs of economic easing, inflation remains a significant challenge. De la Rubia pointed out the persistence of inflation, especially in the service sector where input prices surged in November, largely due to increasing wages.

This inflationary pressure is partly transferred to consumers as service sector output prices continue to rise at high rates. The likelihood of sustained inflation is further supported by recent labor market trends, including increased strike activities and significant wage agreements.

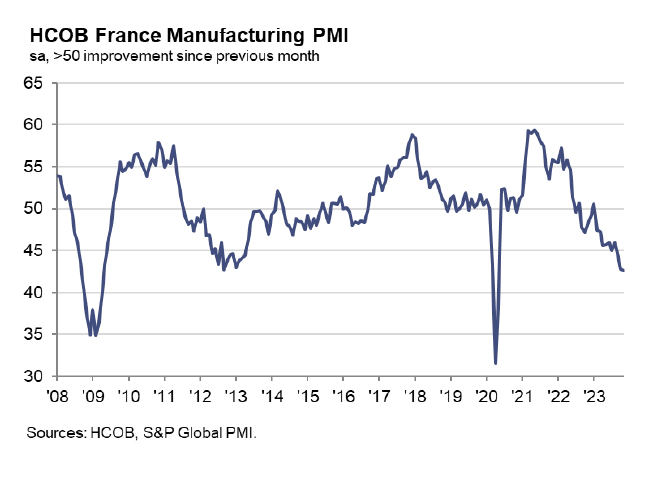

France PMI composite falls to 44.5, continued contraction in a dead-end

Recent PMI data for France underscores a deepening economic downturn. Manufacturing PMI dropped to a 42-month low, down from 42.8 to 42.6 in November, while Services PMI exhibited a negligible rise from 45.2 to 45.3. Composite PMI edged down from 44.6 to 44.5, signaling sustained contraction in the economy.

Norman Liebke, Economist at Hamburg Commercial Bank, provided a stark analysis of the situation: "The French economy is kind of in a dead-end." He observed that for six months straight, output has consistently declined, heavily influenced by reduced demand from both domestic and international markets. Liebke attributed these declines to prevailing geopolitical and economic uncertainties. The economist's nowcasting indicates a slight contraction in France's GDP

Furthermore, Liebke forecasts an increase in unemployment in the forthcoming months, marking the first significant employment drop since late 2020. This trend aligns the recent months' downward trend in employment numbers. Prices continue to rise sharply, as Liebke points out, suggesting that official inflation rates might stay elevated for longer than initially expected.

Gold Corrects Slightly But Remains in Uptrend

The gold (XAU) price dropped by 0.43% on Wednesday after higher-than-expected Michigan Consumer Sentiment Index figures.

Possible effects for traders

A technical rise of the U.S. Dollar Index (DXY) and the proximity of a 2,000 resistance level prompted some traders to close their long positions in XAUUSD. However, expectations that the U.S. Federal Reserve (Fed) won't be raising interest rates soon limited XAUUSD drop. Moreover, the market is currently pricing in a 57% chance of a rate cut in May 2024. 'The increase in the market expectations for the Fed cutting cycle to commence earlier in 2024 has been the prime force driving gold prices higher over the last week,' said Daniel Ghali, a commodity strategist at TD Securities.

XAUUSD was rising during the Asian and early European trading sessions. The U.S. market will be closed today and early on Friday due to Thanksgiving. Thus, volatility will be subsided, but the lack of liquidity may result in sharp moves of the instruments in case of unexpected events or data. 'Spot gold may revisit its 21 November high of $2,007.29 per ounce, as it may have completed a correction from this level,' said Reuters analyst Wang Tao.

USDJPY Stabilizes Near 149.00 ahead of Japanese CPI Report

The Japanese yen (JPY) lost 0.76% on Wednesday as the U.S. Dollar Index (DXY) corrected upwards following a better-than-expected Consumer Sentiment report and a smaller-than-expected increase in Jobless Claims numbers.

Possible effects for traders

USDJPY has been rising since 21 November after the FOMC minutes revealed the Federal Reserve (Fed) monetary policy would remain 'cautiously restrictive.' Conversely, the Bank of Japan's (BOJ) monetary policy is extremely loose, which is the main reason USDJPY has been in a major uptrend for the past three years. Still, the market speculates that BOJ may be preparing for a tightening campaign. 'If next year's annual wage negotiations heighten prospects of inflation sustainably hitting its 2% target, the bank may end its negative interest rate policy in April,' the central bank's former Executive Director Kazuo Momma said. Increasing interest rate expectations will support the Japanese yen, which has been under pressure lately after a truce between Israel and Hamas capped gains potential due to USDJPY's status as a safe-haven asset.

USDJPY fell during the early European trading session. Trading activity will be minimal today across foreign exchange markets due to the Thanksgiving holiday. However, the Japanese inflation data release today at 11:30 p.m. UTC will be vital for short-term directional guidance for currency pairs. The data could also influence current projections for rate hikes, which are anticipated to begin in late 2024. If the inflation data comes out stronger than expected, USDJPY may drop below 147.00. However, lower-than-expected figures may push the pair towards 150.00 again.

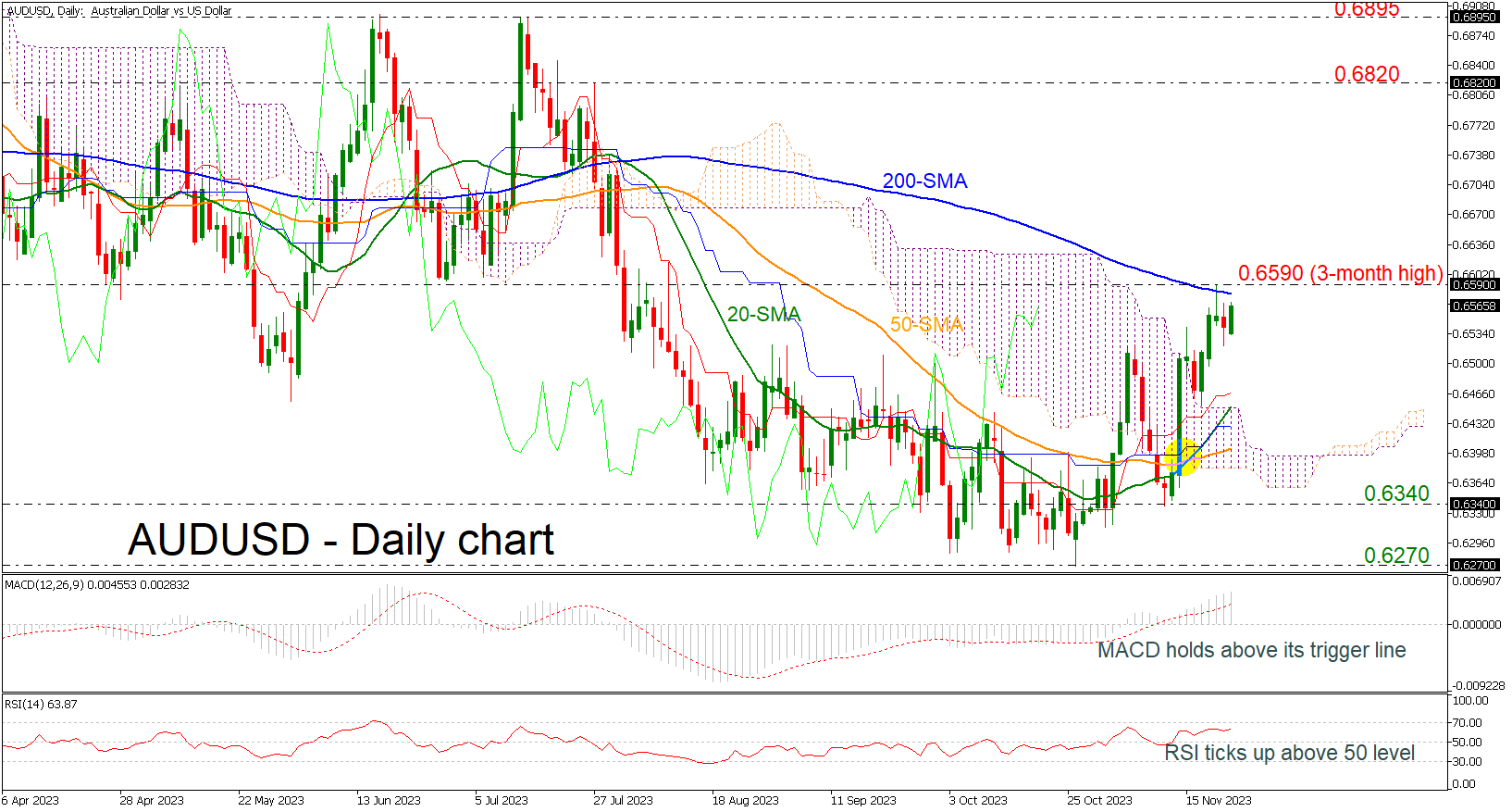

AUDUSD Challenges Recent 3-Month Peak

- AUDUSD faces strong battle near 200-day SMA

- MACD and RSI suggest bullish bias

AUDUSD could not find enough buyers to expand Tuesday’s bull run above the three-month high of 0.6590, closing with some losses on Wednesday.

Technically, the short-term risk is leaning to the upside. The price is developing well above the Ichimoku cloud, while the MACD oscillator is strengthening its positive momentum above its trigger and zero lines. Also, the RSI is pointing north and is moving towards the 70 level.

Given the current positive momentum, the question now is whether the pair will move above the 200-day simple moving average (SMA). A clear step above it and beyond the three-month high of 0.6590 would drive the market towards the next psychological marks, such as 0.6600, 0.6700 and 0.6800 before challenging the 0.6820 resistance level, registered on July 27.

However, if the market fails to climb above the recent peak, traders will turn to the downside again meeting the Ichimoku cloud and the 20- and the 50-day SMAs at 0.6450 and 0.6400 respectively. More losses would put the bearish outlook back into play, resting near 0.6340 and 0.6270.

To sum up, the latest spike in AUDUSD has not excited traders yet. An extension above the 200-day SMA and the 0.6590 barricade is still required to make the upturn look more credible. Note that the bullish cross between the 20- and 50-day SMAs is still intact.

US Stock Markets Extended Their Path Towards 2023 Tops

Markets

The US 2-yr yield tested the post-CPI high (4.94%) yesterday following the release of first weekly jobless claims (209k from 233k vs 227k expected) and next an upward revision to short term (1yr: 4.5% from 4.4%) inflation expectations in University of Michigan’s November consumer survey. Long term inflation expectations (5-10yr) were unchanged at 3.2% while markets expected a downward revision to 3.1%. The former is the highest level since April; the latter the highest in over a decade. These consumer expectations contrast with markets preparing premature central bank rate cuts in Q2 of next year. From a market momentum point of view, it’s nevertheless telling that yesterday’s (second-tier) releases managed to trigger a reaction. It strengthens our believe this month’s correction lower in bond yields most likely went far enough. Daily changes on the US yield curve eventually ranged between +3.1 bps (5-yr) and -1 bp (30-yr). The long end of the curve suffered from more intraday volatility via oil prices. They dropped as much as $3/b intraday (to $78.5/b) after OPEC+ delayed its planned ministerial meeting by a couple of days over diverging views on the level of production cuts. The drop lower in oil prices and (long term) bond yields didn’t last though. Technical elements played as well with 4.34% support in the US 10-yr yield (38% retracement on March-October rise) surviving ahead of the long US weekend (Thanksgiving & Black Friday). German yield changes varied between +3.9 bps (2-yr) and -3.2 bps (30-yr) yesterday. November EMU PMI surveys can today strengthen our scenario that the yield correction lower went far enough. Consensus expects marginal improvements from weak levels (43.5 from 43.1 for manufacturing and 48.1 from 47.8 for services) with likely downside risks. A failure for bonds to rally on such outcome would have a strong signaling function.

US stock markets extended their path towards 2023 tops with gains of 0.5% for major benchmarks. The (trade-weighted) dollar moved away from sell-off lows, but failed to completely hold on to momentum into the close. DXY closed at 103.92 from an open at 103.55, but drifts lower again this morning. EUR/USD closed at 1.0888 (vs intraday low of 1.0852) from 1.0911. EUR/GBP was uninspired by small pre-election tax cuts delivered in Chancellor Hunt’s Autumn statement. Today’s UK PMI’s and how they relate to EMU ones will be key for keeping EUR/GBP in the rising trend channel since September, which is our preferred scenario.

News headlines

Geert Wilders’ PVV is emerging victorious from yesterday’s Dutch (snap) parliamentary elections. With 98% of the votes counted, his far-right party is set to secure 37 seats, up 20 seats from the 2021 election. EU’s former climate chief Frans Timmermans lead a Green Left-Labour alliance and came in second with 25 seats (+8) while the liberal VVD was third with 24 seats (-10). The recently erected centre-right New Social Contract (NSC) party stormed in, gaining 20 seats. Forming a majority in the highly splintered (16 parties!), 150-seat lower house of parliament is expected to take months. While the leader of the biggest party usually becomes prime minister, it could turn out otherwise this time around as both PVV and NSC have already ruled out governing with the PVV. The Green Left-Labour alliance’s natural coalition ally, D66, is set to win only 10 sets (-14), making the formation of a left-wing government equally difficult. PM Rutte (VDD), who’s exiting Dutch politics, will stay in a caretaker capacity in the meantime.

Staying in the European lowland region, Belgian consumer confidence in November extended a gradual recovery that started this summer, the National Bank of Belgium said yesterday. The headline indicator rose from -5 to -4, the highest since the Russian invasion in March 2022. Consumers were more optimistic about the economic outlook and, to a lesser extent, the labour market. On a personal level, households slightly upgraded their expectations for their own financial situation. A downward revision in their saving intentions partially cancelled out the sharp increase recorded in October.