Sample Category Title

Sterling and Euro Rise on PMI Data in Consolidating Markets

PMI data are the main drivers in the forex markets today, particularly lifting Sterling and, to some degree, Euro to higher positions. The bounce in Sterling is chiefly attributed to UK services sector bouncing back into expansion territory, a sign of economic resilience. Additionally, the severity of manufacturing recession in UK seems to be diminishing, offering further support to the currency.

Eurozone has also witnessed a slight improvement in its PMI data, with Germany showing relatively more substantial progress. Despite these positive developments, both UK and Eurozone continue to grapple with the looming risks of recession and noticeable increase in inflation pressures.

In other market areas, there is a prevailing sense of consolidation. Canadian Dollar, despite being the weakest performer of the day, is showing resilience by staying above the previous day's low against major currencies. Swiss Franc, ranking as the second weakest, appears to be impacted by the relative strength of Euro and Sterling. Dollar, ranking as the third weakest for the day, exhibits vulnerability to further declines.

On the stronger side of the market, Australian and New Zealand Dollars are performing well, following closely behind Sterling as the second and third strongest currencies. Euro, while experiencing gains, is not leading the pack.

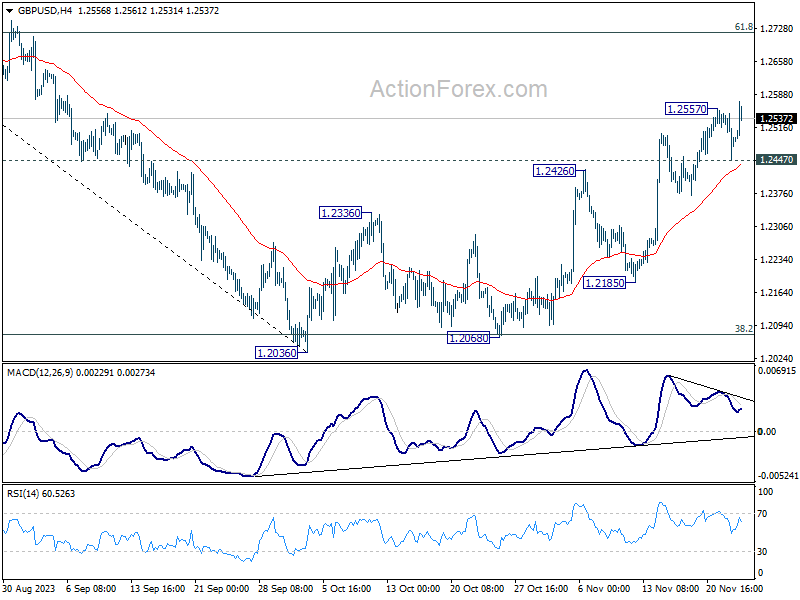

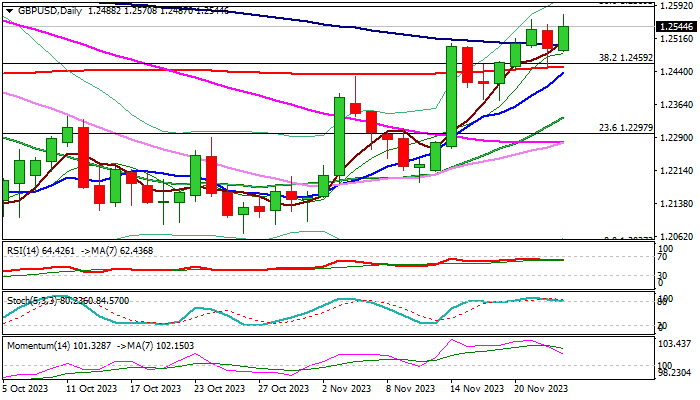

Technically, GBP/USD is taking the lead by breaching 1.2557 temporary top to resume its near term rally. Focuses are now on 1.0964 resistance in EUR/USD, 0.6588 resistance in AUD/USD, and 0.8818 support in USD/CHF. Simultaneous break of these levels should confirm that Dollar selling is back. a

In Europe, at the time of writing, FTSE is down -0.05%. DAX is up 0.19%. CAC is up 0.23%. Germany 10-year yield is up 0.035 at 2.602. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.99%. China Shanghai SSE rose 0.60%. Singapore Strait Times dropped -0.10%.

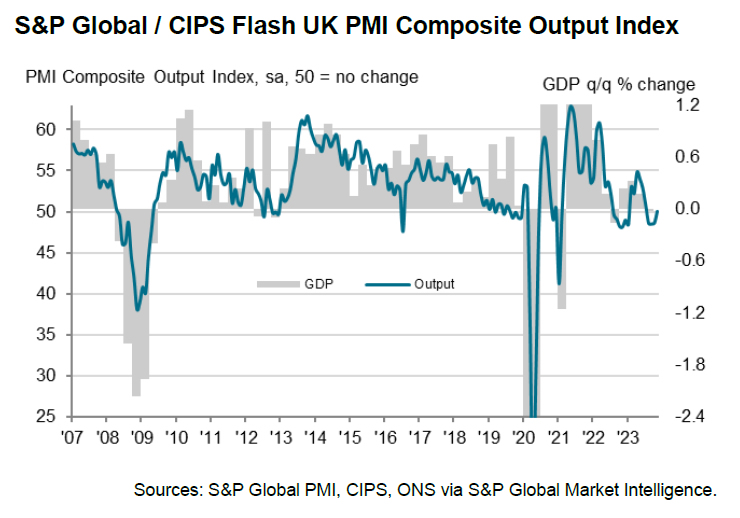

UK PMI composite rose to 50.1, but recession risks and inflation concerns linger

UK PMI data for November reflects a significant improvement in economic activity. Manufacturing PMI rose from 44.8 to a six-month high of 46.7, exceeding the anticipated 45.0. Services PMI increased from 49.5 to a four-month high of 50.5, signaling a return to expansion and surpassing expectations of 49.5. Composite PMI, which amalgamates both sectors, also achieved a four-month high at 50.1, up from 48.7.

Tim Moore, Economics Director at S&P Global Market Intelligence, observed that the UK economy showed signs of stabilization. He noted, "The service sector arrested a three-month sequence of decline and manufacturers began to report less severe cutbacks to production schedules." Moore attributed this recovery in part to a halt in interest rate hikes and a decrease in headline inflation rates. However, he cautioned that the data indicates a likely flat trend for GDP in Q4 2023.

Despite the uptick in PMI figures, Moore highlighted continuing recession risks. He pointed out that new order volumes decreased for the fifth consecutive month, reflecting limited sales opportunities. Additionally, business activity expectations remained low, close to October's recent nadir, and significantly weaker compared to earlier in the year.

Inflation concerns are also evident, especially in the service sector. Moore mentioned that input cost pressures have risen for the first time in four months, with service providers particularly impacted by the need to pass increased staff costs onto customers.

ECB accounts: All agree to hold, yet open to further hike

ECB's October meeting accounts reveal a consensus among "all members" to maintain the three key ECB interest rates unchanged. This decision reflects a shared confidence that current monetary stance was "sufficiently restrictive" for allowing the governing council to assess the "inflation outlook", "dynamics of underlying inflation", and "strength of monetary policy transmission".

The minutes also noted a shift in market expectations, indicating that policy rates are anticipated to remain high for a longer period than previously predicted. Market expectations are transitioning from a "hump-shaped" interest rate path, typically recommended by macroeconomic models, to a "flatter" profile with a delayed first cut in the deposit facility rate.

A key point of discussion was the importance of avoiding an unwarranted loosening of financial conditions. In line with this, some members argued for "keeping the door open for a possible further rate hike", emphasizing the commitment to data-dependence in its decision-making process.

In conclusion, ECB emphasized the need to remain "both persistent and vigilant."

Eurozone PMI composite rose to 47.1, technical recession ongoing

Eurozone's PMI data for November shows marginal improvement but continues to indicate broader recessionary trends. Manufacturing PMI increased slightly from 43.1 to a six-month high of 43.8, exceeding expectations of 43.4. Similarly, Services PMI rose from 47.8 to 48.2, marginally above the predicted 48.0. Consequently, Composite PMI, which combines both sectors, climbed from 46.5 to 47.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, summarized the situation as, "The Eurozone economy is stuck in the mud." Their nowcast model suggests the likelihood of a second consecutive quarter of GDP contraction, meeting the technical criteria for a recession.

Inflation remains a significant issue, particularly in the services sector, where price increases have accelerated due to "astonishingly rapid and even accelerating" rising input costs. De la Rubia attributes these cost increases primarily to higher wages.

The employment situation is also expected to worsen. Initially impacting industrial sector jobs, the economic downturn is poised to affect employment in services sector as well. This could lead to an uptick in Eurozone's unemployment rate, which has so far been relatively stable.

Region-specific dynamics show contrasting trends within Eurozone. Germany's composite index has improved, signaling some positive movement, whereas France continues to show a weakening trend. De la Rubia also points out the challenges faced by Germany, particularly in public investments due to restrictions imposed by the constitutional court's debt brake, which relegate Germany's economy "to the back seat in 2024".

Germany PMI Manufacturing rose from 40.8 to 42.3 in November, a 6-month high. PMI Services rose from 48.2 to 48.7. PMI COmposite rose from 45.9 to 47.1, a 4-month high.

France PMI Manufacturing fell from 42.8 to 42.6 in November, a 42-month low. PMI Services ticked up from 45.2 to 45.3. PMI Composite ticked down from 44.6 to 44.5.

Australia PMI composite fell to 27-mth low at 46.4, but no real signs of hard landing

Australia's manufacturing and services sectors showed continued contraction in November, reaching multi-month lows. PMI Manufacturing index fell from 48.2 to a 42-month low of 47.7, while PMI Services index dropped from 47.9 to a 26-month low of 46.3. PMI Composite also decreased from 47.6 to a 27-month low of 46.4.

Warren Hogan, Chief Economic Advisor at Judo Bank, interpreted these figures as evidence of a further slowdown in Australian economic activity. He commented that the data "all but confirms that the economy is experiencing a soft landing," aligning with RBA's expectations. However, Hogan also noted that there are "no real signs of a hard landing" in the survey, indicating a more controlled economic deceleration.

Despite the overall softness in manufacturing, Hogan observed that the sector "does not appear to be slipping into recession" at this stage. Additionally, an improvement in the employment index in the services sector was seen as indicative of "continued strong demand for labour." This sustained high demand for labour, despite lower activity indexes, points to a persistent imbalance between labour demand and supply.

For RBA, the slowdown in business activity is a welcome development. Still, the strong employment index and an increase in price indexes signal ongoing inflation risks into 2024.

Hogan cautions that it is "still too early to think about rate cuts" in Australia.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2445; (P) 1.2498; (R1) 1.2546; More...

Intraday bias in GBP/USD is back on the upside with break of 1.2557 temporary top. Rise from 1.2036 is resuming for 61.8% retracement of 1.3141 to 1.2036 at 1.2716 next. On the downside, though, below 1.2447 minor support will turn intraday bias again first, and probably bring lengthier consolidations.

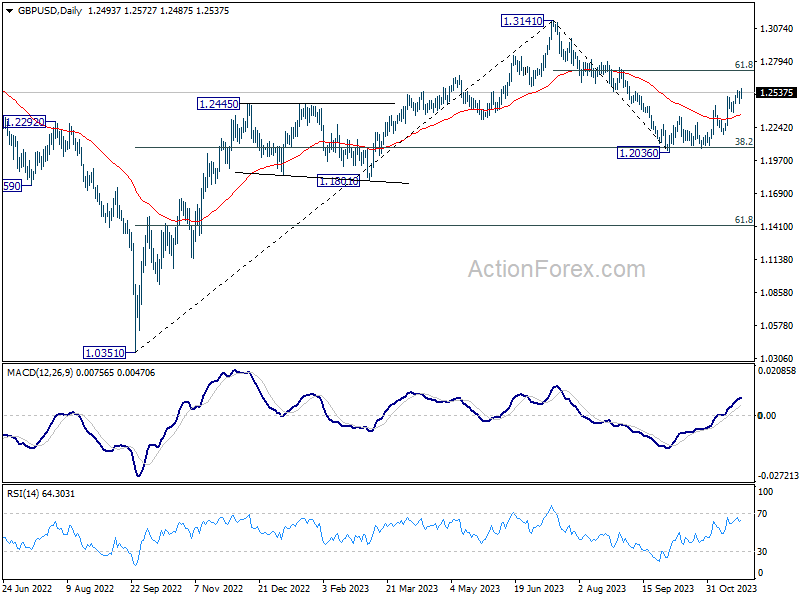

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 argues that current rise from 1.2036 is the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Nov P | 47.7 | 48.2 | ||

| 22:00 | AUD | Services PMI Nov P | 46.3 | 47.9 | ||

| 08:15 | EUR | France Manufacturing PMI Nov P | 42.6 | 43.2 | 42.8 | |

| 08:15 | EUR | France Services PMI Nov P | 45.3 | 45.7 | 45.2 | |

| 08:30 | EUR | Germany Manufacturing PMI Nov P | 42.3 | 41.3 | 40.8 | |

| 08:30 | EUR | Germany Services PMI Nov P | 48.7 | 48.5 | 48.2 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Nov P | 43.8 | 43.4 | 43.1 | |

| 09:00 | EUR | Eurozone Services PMI Nov P | 48.2 | 48 | 47.8 | |

| 09:30 | GBP | Manufacturing PMI Nov P | 46.7 | 45 | 44.8 | |

| 09:30 | GBP | Services PMI Nov P | 50.5 | 49.5 | 49.5 | |

| 12:30 | EUR | ECB Meeting Accounts |

ECB accounts: All agree to hold, yet open to further hike

ECB's October meeting accounts reveal a consensus among "all members" to maintain the three key ECB interest rates unchanged. This decision reflects a shared confidence that current monetary stance was "sufficiently restrictive" for allowing the governing council to assess the "inflation outlook", "dynamics of underlying inflation", and "strength of monetary policy transmission".

The minutes also noted a shift in market expectations, indicating that policy rates are anticipated to remain high for a longer period than previously predicted. Market expectations are transitioning from a "hump-shaped" interest rate path, typically recommended by macroeconomic models, to a "flatter" profile with a delayed first cut in the deposit facility rate.

A key point of discussion was the importance of avoiding an unwarranted loosening of financial conditions. In line with this, some members argued for "keeping the door open for a possible further rate hike", emphasizing the commitment to data-dependence in its decision-making process.

In conclusion, ECB emphasized the need to remain "both persistent and vigilant."

(ECB) Monetary policy accounts

Account of the monetary policy meeting of the Governing Council of the European Central Bank held in Athens on Wednesday and Thursday, 25-26 October 2023

23 November 2023

1. Review of financial, economic and monetary developments and policy options

Financial market developments

Ms Schnabel started her presentation by noting that the market's immediate response to the dramatic geopolitical upheaval in the Middle East, following the terrorist attacks on Israel on 7 October 2023, had so far been contained. Bolstered by continued robust economic growth in the United States, the surge in global long-term bond yields that started over the summer had continued in recent weeks, as investors were increasingly internalising the prospect of interest rates staying high for longer. At the same time, expectations for the future path of short-term interest rates had remained broadly unchanged.

Long-term sovereign bond yields had risen globally. Yields on both sides of the Atlantic were now approaching levels seen from 2005 to 2007 during the last monetary policy tightening cycle. The differential between US and euro area ten-year interest rates had fallen back to the levels observed when the ECB started increasing its key policy rates in July 2022. On aggregate, the recent rise in sovereign bond yields in the euro area had been predominantly driven by an increase in the risk-free rates. However, the rise in yields had not been uniform across euro area countries. Idiosyncratic factors had likely contributed to these developments, and there had been no signs of market fragmentation.

The question arose as to why long-term risk-free rates had risen so sharply at a time when most central banks were nearing the end of the tightening cycle. A decomposition of the increase into real rates and the inflation component showed that the higher ten-year overnight index swap (OIS) rate since the beginning of September 2023 had entirely reflected a rise in the real interest rate. Furthermore, a substantial change could be seen in the term premium, which had increased by around 25 basis points since early September. ECB staff analysis suggested that the repricing of term premia was likely to have largely emanated from the United States as a result of policy and macro spillovers.

Looking at the evolution of the ten-year term premia for the United States and the euro area since the last tightening cycle that started in 2005, the US term premium had remained exceptionally compressed. From a historical perspective, this was exceptional for periods in which interest rates were above the effective lower bound. In the euro area, the term premium had been rising continuously and persistently for over a year. This rise in risk compensation had been broadly expected, as uncertainty about the inflation and policy outlook had increased. However, in the euro area too, the term premium remained visibly below the levels observed during the previous tightening cycle.

The timing of the rise in the global term premium could be explained by the coincidence of three broad factors. The first factor was that many investors had become convinced earlier this year that a global recession was imminent and that central banks worldwide would have to cut interest rates substantially in 2024. Policy expectations had changed substantially since then, however. Investors currently expected cumulative rate cuts of around 60 to 70 basis points in 2024 in the euro area, down from 100 basis points in May. In the latest ECB Survey of Monetary Analysts, median expectations regarding the timing of the first 25 basis point cut had been pushed out to September 2024, from June 2024 previously. At present, investors appeared less certain that the fight against inflation could be rapidly won. This was a global phenomenon extending to many advanced economies. It raised uncertainty about the entire future path of short-term interest rates, resulting in a higher term premium.

The second factor that had likely contributed to the sudden rise in the term premium was related to changes in the supply of, and demand for, US Treasuries. By comparison, net issuance in the euro area was generally expected to be lower in 2024 than in 2023. This was happening as the odds of a policy pivot in Japan were increasing. The market was currently pricing in the Bank of Japan exiting negative rates by April 2024, with the potential for another adjustment in its Yield Curve Control framework as early as October 2023.

The third factor that had likely reinforced the increase in the global term premium had been investors' positioning in the US Treasury market.

In the euro area, market-based measures of longer-term inflation expectations illustrated by the five-year forward index-linked swap rates five years ahead had finally started to come down from their cyclical highs, although they remained volatile and well above 2%. Measures of inflation compensation had declined across the curve, with most of the change at longer tenors reflecting a decline in the inflation risk premium.

The decline in inflation compensation was particularly notable in the current environment, as the conflict in the Middle East implied that risks to energy prices were skewed to the upside. On aggregate, gas futures prices and oil prices were appreciably higher than they had been a few months ago.

The fact that measures of inflation compensation had declined in this environment suggested that the tightening stemming from the ECB's interest rate hike in September 2023, in combination with higher real rates as a result of global spillovers, had fostered the market's confidence in the Governing Council's commitment to bring inflation back to its 2% target in a timely manner.

The speed and magnitude of the rise in real rates, together with the conflict in the Middle East, were also affecting risk assets by weighing on risk sentiment. Stock market volatility had increased visibly, although it remained well below the levels seen after Russia's invasion of Ukraine. Global stock market valuations had declined considerably in recent weeks. That said, valuations in the euro area remained above the levels observed before the start of the monetary policy tightening cycle. One reason was the resilience of the equity risk premium. Although economic sentiment had deteriorated measurably, the risk premium had been constant. A similar phenomenon was observed in the corporate bond market. These marked deviations from past regularities suggested that, when interest rates went up, the risk-taking channel of policy transmission might work differently from when rates went down.

Nevertheless, there were differences across rating categories. Credit spreads for higher-rated issuers had been largely insensitive to the rise in yields. In contrast, the spreads of riskier, high-yield issuers had widened more measurably in recent weeks, although even these were nearer the lows recorded during the current cycle than the highs.

The speed of the bond market rout had also left a significant mark on foreign exchange markets. Since mid-July the euro had fallen by nearly 6% against the US dollar. This constituted a headwind to the Eurosystem's efforts to reduce inflation in a timely manner. The appreciation of the US dollar during this time had been broad-based. So, from a foreign exchange perspective, real yields in the United States were likely seen as a sign of strength by investors, as growth was holding up better than expected.

The global environment and economic and monetary developments in the euro area

Mr Lane then went through the latest economic, monetary and financial developments in the global economy and the euro area. Starting with the global economy, Mr Lane pointed to global growth momentum continuing to slow. The global composite output Purchasing Managers' Index (PMI) had fallen for the fourth consecutive month in September, as the deterioration in the services sector converged towards the contractionary readings for manufacturing. In China, the real estate sector continued to be a drag on growth, but the GDP figure for the third quarter of the year suggested that the economy may be finding its footing again. In contrast, while the US economy had remained robust in the third quarter, it was now showing clearer signs of deceleration. Since the Governing Council's previous monetary policy meeting on 13-14 September, the euro had depreciated both against the US dollar and in nominal effective terms. Its previous appreciation was still adversely affecting euro area trade.

The escalating conflict between Israel and Hamas was increasing uncertainty and posed upside risks to oil and gas prices over the near term. So far, however, the impact on futures prices further ahead had been limited. Oil prices were higher than both at the time of the September meeting and at the cut-off date for the September ECB staff macroeconomic projections for the euro area. However, the negative slope of the current oil futures curve was steeper than in the projections. Mr Lane also recalled that, after a period of elevated levels, crack spreads (the difference between crude oil prices and prices for refined products such as petrol and diesel) had fallen by 36% since the September meeting, while gasoline crack spreads had even fallen by 90%. For the overall energy prices for consumers it was important to monitor the prices of both refined and crude oil. For its part, the gas market still faced a number of supply risks. Gas prices remained lower than at the cut-off date for the September staff projections but were higher than at the time of the previous monetary policy meeting. As regards other commodities, the overall pattern remained one of declining prices for metals and food, which could be linked to the weaker global economy.

The euro area economy had remained weak in the third quarter. The European Commission's composite economic sentiment indicator and the PMI pointed to declining consumer confidence and business activity. Manufacturing output continued to fall in October, according to the flash release, owing to lower inventories, declining orders and tighter financing conditions. Housing and business investment contracted, as demand weakened in response to higher borrowing costs. The decline in housing investment had in fact already started in the second quarter of 2022, with a rebound at the start of 2023 driven by the positive impact of the mild winter. The PMI and the forward-looking indicators of the European Commission pointed to a further decline in housing investment in the fourth quarter of 2023. It was evident that the construction sector accounted for a large part of the weakness in overall activity.

In contrast to housing investment, business investment had held up for a sustained period of time, helped by backlogs being worked through. In the second quarter of 2023, business investment had increased only marginally and new orders were pointing to a contraction in the second half of the year. The outlook for investment would have been significantly worse without the support of the Next Generation EU programme.

Although demand in contact-intensive services sectors still exceeded pre-pandemic levels and activity in tourism remained supportive, the services sector was losing steam. This was due to the fact that weaker industrial activity had started to spill over to business-oriented services, the impetus from reopening effects was fading and the impact of higher interest rates was broadening across sectors. The services PMI had continued its decline in October, according to the flash release, and had been in contractionary territory since August.

Private consumption was expected to have remained weak in the third quarter. Looking ahead, while the European Commission's consumer confidence indicator had been improving until spring 2023, it had started to deteriorate again in the summer months and remained well below its historical average.

Turning to trade, the outlook for exports was weakening. Survey data for September 2023 showed that new export orders for both goods and services remained in contractionary territory, indicating that the global weakness continued to weigh on euro area exports. Furthermore, firms had worked through their backlogs, suggesting that the support coming from this factor was fading. Another key factor dampening the demand for euro area goods was the loss of competitiveness as a result of persistently high energy prices and the past appreciation of the euro.

The labour market was still resilient, with the unemployment rate at a historical low of 6.4% in August. Momentum was starting to soften, however, as the economy remained weak. Employment expectations had declined further in October for both services and manufacturing, according to the PMI flash release, with manufacturing employment expectations falling to their lowest level since August 2020. The labour force had expanded further in the second quarter of the year and was now 2.3% larger than before the pandemic, but fewer new jobs were currently being created.

Turning to fiscal policy, the draft budgetary plans for 2024 indicated a significant decline in support measures, which would imply a restrictive fiscal stance. However, this restrictive stance was not reflecting austerity measures but the winding-down of energy subsidies.

The risks to economic growth remained tilted to the downside. Growth could be lower if the effects of monetary policy turned out stronger than expected. A weaker world economy would also weigh on growth. Russia's unjustified war against Ukraine and the tragic conflict sparked by the terrorist attacks in Israel were key sources of geopolitical risk. This could result in firms and households becoming less confident about the resilience of the world economy and more uncertain about the future, and dampen growth further. Conversely, growth could be higher than expected if the still resilient labour market and rising real incomes meant that people and businesses became more confident and spent more, or the world economy grew more strongly than expected.

Headline inflation had dropped markedly in September to 4.3%, in line with the September staff projections. It was also expected to come down further in the near term, before a temporary mechanical uptick around the turn of the year. The decline in September was visible across all the main components, confirming the general disinflationary process that was under way. Energy prices had fallen by 4.6% on account of negative base effects, and food inflation, while still high, had decreased to 8.8%.

Inflation excluding energy and food, as measured by the Harmonised Index of Consumer Prices (HICPX), had also dropped sharply in September, to 4.5%. This was 0.2 percentage points lower than expected in the September staff projections. The fall had been supported by improving supply conditions, the pass-through of previous declines in energy prices, the impact of tighter monetary policy on demand and corporate pricing power. Non-energy industrial goods inflation had fallen to 4.1% in September, with the monthly dynamics now reverting to historical averages. Services inflation had declined for the second consecutive month in September, to 4.7%. This had been driven in part by the discontinuation of the €9 public transport ticket in Germany last year and the reduction in the impact of changes in HICP weights. However, it might also have reflected some softening of activity in the travel and tourism sectors with the fading out of post-pandemic reopening effects.

Most measures of underlying inflation continued to decline. Measures that adjusted for past energy and supply shocks had largely confirmed their downward trajectory in August. The adjusted Persistent and Common Component of Inflation measure – a good predictor of inflation developments in the past – was now close to 2%. At the same time, domestic inflation remained persistent and had hovered around 5.5% until August, before edging down to 5.2% in September. The still high level of this indicator underscored the significance of continuing wage pressures for underlying inflation.

Moving to the latest wage developments, negotiated wage growth had remained robust in the third quarter. However, the Indeed wage tracker, which captured wage growth for new hires, showed continued evidence of an easing of wage pressures. Contacts in the corporate sector had reported ongoing strong wage growth, although Corporate Telephone Survey respondents expected some moderation next year. Overall, the available indicators continued to suggest that the wage forecast included in the September staff projections was broadly on track. Wage developments would need continuous monitoring in the months ahead, as most wage negotiations would only take place at the start of 2024. The Corporate Telephone Survey also suggested that profit margins had been squeezed during 2023 and would contract further in 2024. This evidence was in line with the expected decline in profit margins over the coming quarters, embedded in the September staff projections.

Inflation expectations reported in the ECB Survey of Professional Forecasters had remained broadly unchanged in October. Most of the distribution had remained concentrated around 2%. The ECB Consumer Expectations Survey showed that consumers had not yet adjusted downwards their perception of past inflation. This could suggest that willingness to revise perceived inflation downwards was not as sensitive to actual developments in inflation as willingness to revise it upwards. Consumer inflation expectations had moved up in September, particularly for the one-year ahead horizon. While these developments were in line with those in countries outside the euro area, such as the United States, Sweden and the United Kingdom, and appeared to be linked to the recent increase in energy prices, they needed close monitoring.

The risks to inflation remained twofold. On the one hand, upside risks to inflation could come from higher energy and food costs. The heightened geopolitical tensions could drive up energy prices in the near term while making the medium-term outlook more uncertain. Extreme weather, and the unfolding climate crisis more broadly, could push food prices up by more than expected. Additionally, a lasting rise in inflation expectations above the inflation target, or higher than anticipated increases in wages or profit margins, could also drive inflation higher, including over the medium term. On the other hand, weaker demand – for example owing to a stronger transmission of monetary policy or a worsening of the economic environment in the rest of the world amid greater geopolitical risks – would ease price pressures, especially over the medium term.

Turning to monetary and financial developments, short-term risk-free rates had been stable since the September monetary policy meeting. Long-term rates had risen markedly, however, resulting in some additional tightening of financing conditions. The transmission of the ECB's past monetary policy actions to financing conditions continued to be exceptionally strong and was increasingly affecting the broader economy and dampening demand, thereby helping push down inflation. The rise in bank lending rates for firms and for households for house purchase – to 5.0% and 3.9% respectively in August – had continued to outpace previous hiking cycles, and these costs had reached their highest levels in over a decade.

According to the latest euro area bank lending survey, credit standards for loans to firms and households had tightened further in the third quarter, as banks were becoming more concerned about the risks faced by their customers and were less willing to take on risks themselves. Credit dynamics had weakened further. The annual growth rate of loans to firms had dropped sharply, from 2.2% in July to 0.7% in August and 0.2% in September, when a positive monthly net flow only partially compensated for the large outflow registered in August. Loans to households remained subdued, with the growth rate slowing from 1.3% in July to 1.0% in August and 0.8% in September. The annual growth rate of M3 – the broad monetary aggregate – had remained negative in September, despite a considerable monthly inflow both from the rest of the world and from a partial reversal of the large net redemptions in loans to firms in August. With positive nominal GDP growth in 2023, the currently slightly negative growth in M3 on an annual basis implied that real money growth was strongly negative. Growth in M1 – currency in circulation and overnight deposits – had increased slightly but remained highly negative. Firms and households continued to shift funds from overnight deposits to term deposits – although this had moderated somewhat in recent months – reflecting attractive rates on the latter. This continued to explain the unprecedented rates of contraction in M1.

Overall, the transmission of the policy tightening to lending rates and lending volumes was strong by historical standards, even taking into account the steep path of the ECB's policy rates in the recent past.

Monetary policy considerations and policy options

On the basis of the three elements of the Governing Council's reaction function, Mr Lane proposed maintaining the three key ECB interest rates at their current levels. The incoming information had broadly confirmed the Governing Council's previous assessment of the medium-term inflation outlook. Inflation was still expected to stay too high for too long, and domestic price pressures remained strong. At the same time, inflation had dropped markedly in September and most measures of underlying inflation had continued to ease. The Governing Council's past interest rate increases continued to be transmitted forcefully into financing conditions. This was increasingly dampening demand and thereby helped push down inflation.

Holding the key ECB interest rates at their current levels would confirm the Governing Council's assessment in September that the rates were at levels that, maintained for a sufficiently long duration, would make a substantial contribution to a timely return of inflation to target. This was supported by a range of model-based simulations suggesting that, while the tightening cycle had so far had a substantial downward impact on inflation and GDP growth, the further tightening in the pipeline from the current policy stance would press down further on inflation over time. By its December monetary policy meeting the Governing Council would have new data on GDP growth for the third quarter, the October and November inflation figures, fresh monetary data and a new round of projections.

The Governing Council's future decisions should ensure that the key ECB interest rates would be set at sufficiently restrictive levels for as long as necessary. The Governing Council should continue to follow a data-dependent approach to determining the appropriate level and duration of restriction. In particular, its interest rate decisions should remain based on its assessment of the inflation outlook in light of incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission.

Finally, preserving the option to apply flexibility in pandemic emergency purchase programme (PEPP) reinvestments with a view to countering risks to the monetary policy transmission mechanism related to the pandemic continued to be warranted.

2. Governing Council's discussion and monetary policy decisions

Economic, monetary and financial analyses

As regards the external environment, members took note of the assessment provided by Mr Lane that, while the latest trade data had been better than expected, the near-term outlook for trade had deteriorated compared with the September ECB staff projections. The question was raised as to what extent this was still compatible with expectations that euro area export demand would pick up and be a driver of a strengthening economy in the period ahead. However, it was also stressed that growth in both China and the United States had been better than expected, which pointed to improvements in the international environment.

Turning to commodity markets, it was argued that the 1970s were not a good benchmark for assessing the impact of the latest spikes in oil prices, as energy substitution was easier now than it had been then. Moreover, wholesale gas prices, which had been the main source of recent high levels of energy inflation, had remained well below previous peaks. At the same time, concerns were expressed that the developments in the Middle East could lead to energy-related supply shocks, which, as in the 1970s, would have negative consequences for both growth and inflation worldwide.

With regard to economic activity in the euro area, members generally concurred with Mr Lane that the economy remained weak and the outlook was deteriorating. Subdued foreign demand and tighter financing conditions were increasingly weighing on investment and consumer spending. Recent information suggested that manufacturing output had continued to fall and that the services sector was also weakening. Several factors were at play here: subdued industrial activity was spilling over to other sectors, the impetus from the post-pandemic reopening effects was fading and the impact of higher interest rates was broadening across sectors. The economy was likely to remain weak for the remainder of 2023. However, as inflation fell further, household real incomes recovered and the demand for euro area exports picked up, the economy should strengthen over the coming years.

It was widely underlined that the outlook for the global economy and for the euro area was surrounded by elevated uncertainty. In this context, members noted that the weaker outlook for economic growth since the September monetary policy meeting implied a materialisation of the downside risks that had already been identified at the time of that meeting. Nowcasting tools indicated lower growth in the third and fourth quarters of 2023 than had been expected in the September ECB staff projections, and even implied that there would be a technical recession. It was suggested that continuing weakness in the fourth quarter would increase concern about whether activity would really pick up gradually in that quarter, as had previously been expected, or whether weakness could persist well into 2024. At the same time, it was argued that, while PMI indicators still pointed towards a deeper downturn, they might have lost some predictive power. Furthermore, the latest information pointed to stagnating activity rather than a deep recession.

There were therefore concerns that the weaker short-term outlook, combined with a slight worsening of external demand and a further tightening of financing conditions, could also imply weaker than expected growth in 2024 and 2025. More fundamentally, the question was raised as to where the improvement in economic activity projected by staff in September would come from if growth was currently slowing in all components of demand – namely consumption, investment and exports – and while fiscal and monetary conditions were tightening. At the same time, it was argued that even a somewhat weaker growth outlook was still compatible with a "soft landing" narrative, as entailed in the September ECB staff projections, if inflation continued to decline and real incomes recovered. The observed weaker growth also partly reflected the successful transmission of tighter monetary policy. This transmission was well advanced and its impact now appeared to be close to peaking. The bleaker short-term outlook thus did not stand in the way of the gradual recovery in 2024 and 2025 expected in the staff projections.

A soft landing scenario was seen to be supported by sound household balance sheets. Available data suggested that higher savings in the second quarter of this year reflected, to a large extent, repayments of loans rather than increased cash holdings. While this suggested that households were not imminently about to start consuming more, the improvement in balance sheets was positive for financial stability and made household positions safer in the longer term.

Turning to employment, it was noted that the strength of the labour market had so far been supporting economic activity. Members emphasised different aspects of the latest data. On the one hand, they noted that the labour market was still tight and had once again performed better than expected, with a historically low unemployment rate. Firms holding on to their employees was an essential part of the narrative that growth would resume owing to higher spending. Moreover, even a limited increase in unemployment would still be compatible with a soft landing scenario. On the other hand, the point was made that signs of labour market weakening constituted an important change from earlier assessments. The concern was expressed that the strong performance of the labour market was in part due to labour hoarding and thus was fragile. It was argued that labour markets in Europe today were much more exposed to the vagaries of external shocks and that adjustments, when they occurred, would be stronger than before. If the weakness in foreign demand were to continue, this could be transmitted to the labour market in a more abrupt manner and therefore implied downside risks to growth. In this context, it was also noted that both productivity and average hours worked per person employed had not yet fully recovered from the pandemic, and that it was uncertain whether the economy could find itself in a new normal where these two indicators were simply lower on a structural basis. This also had implications for the inflation outlook in the medium term.

With regard to fiscal policies, members reiterated that, as the energy crisis faded, governments should continue to roll back the related support measures. This was essential to avoid driving up medium-term inflationary pressures, which would otherwise call for even tighter monetary policy. Fiscal policies should be designed to make the economy more productive and to gradually bring down high public debt. Structural reforms and investments to enhance the euro area's supply capacity – supported by the full implementation of the Next Generation EU programme – should help reduce price pressures in the medium term, while supporting the green and digital transitions. To that end, the reform of the EU's economic governance framework should be concluded before the end of the year and progress towards a capital markets union and the completion of the banking union should be accelerated.

Members noted that countries' draft budgetary plans remained broadly in line with the assumption of a slightly more restrictive fiscal stance in 2024 than in 2023 for the euro area as a whole, as incorporated in the September ECB staff projections. However, further analysis of the impact of the economic cycle and the current economic slowdown on the overall budget balance and the cyclically adjusted balance was seen as warranted. Another issue was the sustainability of recent and future debt developments. In particular, it was pointed out that recent reductions in debt-to-GDP ratios reflected, to a large extent, the impact of high inflation and should not be interpreted as policy-driven consolidation efforts. With inflation receding, these windfall gains could not be counted on any longer, and the impact of higher interest rates on government funding costs was also yet to have its full effect.

Concerns were expressed that ongoing discussions on the fiscal rules in the context of the deliberations about the EU's economic governance framework could imply a vacuum for 2024, as the Stability and Growth Pact had not yet been replaced by new regulations. Disciplined fiscal policies were considered paramount for achieving price stability. However, it was argued that the current fiscal stance risked pushing in the opposite direction, including via measures that altered borrowing costs and could hence be seen as directly interfering with monetary policy transmission. At the same time, the point was made that fiscal tightening without structural reforms would be of limited help and that the economy needed support from the supply side.

Members assessed that the risks to economic growth remained tilted to the downside. Growth could be lower if the effects of monetary policy turned out stronger than expected. A weaker world economy would also weigh on growth. Russia's unjustified war against Ukraine and the tragic conflict sparked by the terrorist attacks in Israel were key sources of geopolitical risk. This might result in firms and households becoming less confident about the future, and could dampen growth further. Conversely, growth could be higher than expected if the still resilient labour market and rising real incomes meant people and businesses became more confident and spent more, or if the world economy grew more strongly than expected.

It was noted that while downside risks identified earlier had materialised, additional risks and uncertainty had arisen since the Governing Council's September monetary policy meeting. This related mainly to the impact of the conflict in the Middle East, particularly if it were to escalate further. As this had come on top of the war in Ukraine, the resulting uncertainty could make firms more apprehensive, leading to less demand for investment. Given that developments in China also remained a source of fragility, it was suggested that downside risks mainly stemmed from the external environment. These also included the possibility of spillovers from the United States, owing to euro area long-term yields moving higher in tandem with those in the United States. At the same time, recent positive surprises suggested that developments in the United States and China could also turn out better than expected. Overall, while growth continued to be weak, the Eurosystem staff projections in December would provide a more comprehensive picture.

Turning to price developments, members broadly agreed with the assessment presented by Mr Lane in his introduction. The incoming information had largely confirmed the previous assessment of the medium-term inflation outlook. Inflation had dropped to 4.3% in September, which was due partly to strong base effects, with the decline broad-based. In the near term, inflation was likely to come down further, as the sharp increases in energy and food prices recorded in autumn 2022 would drop out of the yearly rates. However, energy prices had risen again recently and had become less predictable in view of the new geopolitical tensions.

Regarding headline inflation, members observed that the latest developments had been broadly in line with the September ECB staff projections. Furthermore, it was remarked that the indicators of underlying inflation had been moving in the right direction over recent months and that most had passed their peak and were continuing to decline. Costs, notably for industrial raw materials, had fallen and, overall, pipeline price pressures continued to decline and were being passed through to consumer prices. At the same time, it was noted that domestic price pressures remained strong, reflecting the persistence of services inflation and the impact of continuing wage pressures on underlying inflation. There had been increases in momentum across most components of headline inflation, with the exception of services inflation.

Members noted that the latest information on wages also appeared to be broadly in line with the expectations entailed in the September ECB staff projections. It was highlighted that the increase in the wage drift component had been stronger than growth in negotiated wages. Wage drift being more sensitive to cyclical developments could, however, also imply a more pronounced weakening of wage growth dynamics if demand were to weaken and employment to stagnate. It was remarked that there had been limited signs of second-round effects and no evidence of wage-price spirals thus far. In cumulative terms, real wages in the euro area remained subdued compared with at the beginning of the inflationary process. Information from the ECB wage trackers on recently signed wage agreements pointed to continued strong wage growth. While this was expected to moderate over time, the decline had yet to materialise and was subject to high uncertainty. Rising energy prices might delay or dampen the expected decline in wage growth, as they might be used to justify higher wage demands.

Measures of longer-term inflation expectations were mostly around 2%, but some indicators remained elevated and needed to be monitored closely. The recent decline in market-based inflation compensation was seen as a welcome development and in line with a reinforced credibility for bringing inflation back to target. However, it was also the case that markets were more forward-looking in their expectations, while the expectations of households and parts of the business sector had strong backward-looking elements. This difference needed to be borne in mind in case there were new surprises in inflation. In this context, inflation expectations were seen as fragile, as was visible in the renewed uptick in consumer expectations, possibly in response to the higher energy prices. Moreover, in the latest ECB Survey of Professional Forecasters, respondents had seen an upshift in the balance of risks for inflation expectations at the two-year horizon and a one-third probability that inflation would be above 2.5% in the longer term.

Members also considered that the increased uncertainty surrounding the outlook for economic growth translated into additional uncertainty for the outlook for inflation, particularly beyond the short term. It was noted that headline inflation would likely continue to decline in the near term, largely owing to base effects. At the turn of the year, a temporary rebound in headline inflation could be expected because of energy-related base effects.

Members underlined that the outlook for wage growth continued to be highly uncertain. The picture for wage developments would only gradually crystallise during the course of next year, in view of the long lags between hard data releases. It was argued that the strong decline observed in headline inflation and the increased confidence in inflation returning to the ECB's target should help contain upward pressure on wages in coming negotiations. The high levels of uncertainty surrounding the outlook for wages, as well as the outlook for productivity and average hours worked per person employed, implied a highly uncertain outlook for unit labour costs and, in turn, for inflation. Moreover, unit profits also played a crucial role in determining the future path of inflation. It was noted that the previous upward shift of profit margins could prove temporary if cyclical conditions weakened. At the same time, an easing in other cost factors might help mitigate any upward pressures on margins.

Against this background, members assessed that there were both upside and downside risks to inflation. Upside risks could come from higher energy and food costs. The heightened geopolitical tensions could drive up energy prices in the near term and make the medium-term outlook more uncertain. Extreme weather, and the unfolding climate crisis more broadly, could push food prices up by more than expected. Higher than anticipated increases in wages or profit margins, or a lasting rise in inflation expectations above target, could also drive inflation higher, including over the medium term. By contrast, weaker demand – for example owing to a stronger transmission of monetary policy or a worsening of the economic environment in the rest of the world amid greater geopolitical risks – would ease price pressures, especially over the medium term. There were differing views on the overall balance of risks for inflation. Some members viewed the overall balance as tilted to the upside, owing to upside risks to wage growth and energy prices. Upside risks could also stem from the impact of the recent depreciation of the euro, primarily against the US dollar. Other members saw inflation risks as balanced, with inflation broadly seen evolving as projected and converging back to the 2% target over the medium term, possibly even with a risk of undershooting. Some downside risks to core inflation were seen, owing to economic activity being weaker than expected and recent data for core inflation being slightly lower than expected.

Regarding the consequences of further negative supply shocks, specifically related to energy, the view was expressed that such a scenario was unlikely to play out in the same way as the large commodity price shocks of 2021-22, which had coincided, amid persistent supply bottlenecks, with the release of pent-up demand and the post-pandemic reopening. The increases in oil prices stemming from the conflict in the Middle East had so far been limited, and the market had seen the recent increase as a spike rather than a very persistent shift. The weaker aggregate demand due to tighter monetary policy should, in principle, induce firms to either resist large increases in unit labour costs or absorb them into profit margins rather than pass them on to consumers. It was argued that the large increases in profit margins in 2022 suggested that in future there would be scope to absorb higher energy costs into margins. Still, the upside risks from higher energy prices – coming after a long period of inflation substantially above target – were not seen as insignificant, even if the current macroeconomic environment was quite different. In this context, any persistence in higher energy prices could trigger further second-round effects, especially with a large number of wage agreements being negotiated at the start of the coming year. This could imply a delay or a reduction in the expected decline in wage growth. Overall, the risks posed by the geopolitical environment, including direct or indirect effects of higher commodity prices or its impact on economic sentiment among firms and households, warranted close monitoring.

Turning to the monetary and financial analysis, members largely concurred with the assessment provided by Mr Lane in his introduction. The most significant development since the Governing Council's previous monetary policy meeting was the marked rise in longer-term interest rates, reflecting large increases in other major economies, notably the United States. The decline in the five-year forward inflation-linked swap rate five years ahead was also noted. This had contributed to a more pronounced increase in real interest rates and was seen as a welcome sign of the credibility of the Governing Council's recent monetary policy actions. Overall, the rise in long-term rates and the correction of risk asset prices were judged as further tightening financial conditions, while the depreciation of the euro had the opposite effect.

Members discussed a range of explanations for the rise in US longer-term interest rates, which could also have different implications for expected spillovers to the euro area. These explanations included better than expected US macroeconomic developments supporting narratives of rates remaining high for longer, and a rise in the term premium. An increase in potential output in the United States or rising concerns about the financing requirements associated with persistently high US budget deficits could both have pushed up the natural interest rate. It was noted that technical factors were playing a role. It was also argued that an environment of quantitative tightening – lacking stable demand for bonds from central banks – would naturally increase the term premium, as the market clearing rate for long-term bonds was higher than before, especially in the face of spikes in volatility as seen recently.

There was broad agreement that spillovers from the United States were a major driver of the increase in euro area longer-term interest rates, contributing to a rise in euro area OIS rates of just over 20 basis points since the Governing Council's previous monetary policy meeting. It was noted that the developments were not related to the underlying economic fundamentals and the inflation outlook in the euro area, and that they were driven by the term premium component rather than the expectations component of long-term interest rates. In this regard, it was also argued that euro area fiscal policy may have played a role in driving term premia higher. An additional possibility was that financial markets had started to price in a higher natural interest rate for the euro area.

Members generally agreed that the rise in longer-term interest rates in the euro area had tightened financing conditions by more than anticipated. It was argued that this made it more likely that the Governing Council's monetary policy stance was restrictive enough, although there were still uncertainties around this assessment.

There were different views on the desirability of higher long-term rates for the euro area. On the one hand, they could be seen as undesirable in that they were not linked to euro area developments but contributed to additional tightening. This could unnecessarily weaken economic activity by more than intended and might cause inflation to undershoot. Moreover, higher long-term rates could render fiscal sustainability more challenging for some euro area countries. On the other hand, higher long-term rates could be welcomed after a long period in which term premia had been substantially compressed. They would strengthen monetary policy transmission to activities based on longer-term credit and signal to governments that longer-term borrowing would be more costly in the future. In addition, such tightening would enhance the credibility of inflation returning to target in a timely manner and be consistent with maintaining the policy rates at sufficiently restrictive levels for an extended period. From an economic growth perspective, the impact on the euro area depended on whether the rise in US long-term interest rates was being driven by better growth prospects for the US economy, which would imply positive spillover effects via stronger euro area external demand.

Members agreed that monetary policy continued to be transmitted strongly into broader financing conditions. Funding had become more expensive for banks, and average interest rates for business loans and mortgages had risen again in August, although rates on longer-term loans to non-financial corporations had declined. The latest bank lending survey indicated a further sharp drop in credit demand in the third quarter, driven by higher borrowing rates and cuts in investment plans and house purchases. Credit standards for loans to firms and households had also tightened further. At the same time, it was noted that the resilience of the banking sector was not seen as a concern, that the latest Survey on the Access to Finance of Enterprises suggested financial constraints remained contained in a historical comparison, and that the latest Corporate Telephone Survey suggested banks were still willing to lend to firms in most sectors of the economy.

Against this background, monetary and credit aggregates continued to decline rapidly. Amid weak lending and the reduction in the Eurosystem balance sheet, M3 continued to contract sharply. In August it had fallen, in annual terms, at the fastest rate recorded since the introduction of the euro and in September had remained negative. Credit dynamics had weakened further, with the annual growth rate of loans to firms dropping sharply and that of loans to households remaining subdued. At the same time, it was noted that there were no indications of financial amplification, i.e. weaknesses in the banking sector reinforcing negative macroeconomic developments. Moreover, the earlier large negative flows in credit to non-financial companies were seen as driven mainly by a decline in short-term lending, typically associated with the financing of working capital needs and inventories. Moreover, loan momentum was not falling as quickly as previously, with the large negative net flows recorded in August partly reversed in September.

Still, monetary transmission via the bank lending channel was generally seen to have been stronger than previously anticipated, including by banks themselves, and to have led to a significant tightening of financing conditions. It was also noted that transmission could have been even stronger if it had not been for structural labour shortages and resilient risk sentiment in the financial markets, as reflected in robust equity markets and relatively compressed risk premia. At the same time, it was mentioned that the services sector, which was accounting for most of the persistence of inflation, appeared not to be very sensitive to the tightening of financing conditions according to the Corporate Telephone Survey. Three out of four services firms had not seen an impact from tighter financing conditions on their business activity over the past 12 months and the ratio was even higher looking ahead over the next 12 months. Financial conditions still had indirect effects on the services sector through the slowdown in the growth of aggregate demand. Nevertheless, until recently, this had been compensated for by strong reopening effects.

It was highlighted that for some countries the reduction in mortgage lending was a particular concern. Reference was made to a few countries that had introduced measures to support the mortgage market, which were counteracting the effect of monetary policy measures to bring down inflation. However, it was observed that this was not a general situation across the euro area and, overall, it was widely felt that monetary transmission was working well and was strong yet gradual and orderly.

Looking ahead, it was argued that further transmission was still to come as fixed rate lending was rolled over, especially in countries with a higher ratio of fixed to variable rate loans. This suggested that transmission was unfolding only very gradually owing to long mortgage fixation periods. Moreover, attention was drawn to large cash buffers in parts of the corporate sector that could reduce the need for new borrowing for some time, in conjunction with the inventory cycle coming to an end. The extent of additional transmission remained uncertain but there was a possibility that it could strengthen further, in part because higher long-term interest rates could dampen growth in long-term credit. At the same time, it was noted that the latest bank lending survey suggested banks were expecting to tighten credit standards to a lesser extent in the coming quarter. Such an outcome would mean that, all else being equal, this subset of financing conditions might soon plateau.

Monetary policy stance and policy considerations

Turning to the assessment of the monetary policy stance, members highlighted that the uncertainty surrounding the economic outlook had increased compared with at the time of the September Governing Council meeting, also affecting the assessment of the appropriate monetary policy stance. At the same time, it was noted that financing conditions had tightened on account of the spillovers from the United States, which increased confidence that – barring significant deviations in inflation from the September ECB staff projections – the monetary policy stance was sufficiently restrictive and would bring inflation back to target in a timely manner. Moreover, the view was held that markets had revised their expected interest rate path to higher levels, which – if maintained for some time – would contribute to a sufficiently restrictive monetary policy stance. It was cautioned, however, that in view of the tight labour market the current level of policy rates might not be as restrictive as generally thought. Moreover, the fact that market participants had also moved back the date at which they expected a first rate cut was seen as evidence that they did not perceive a risk of overtightening.

Against this background, members assessed the data that had become available since the September monetary policy meeting in accordance with the three main elements of the "reaction function" that the Governing Council had communicated earlier in the year. These comprised the implications of the incoming economic and financial data for the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission. Overall, the view was held that all three elements of the reaction function were moving in the right direction, providing clear evidence that monetary policy was working as intended.

Starting with the inflation outlook, members broadly concurred with the assessment presented by Mr Lane in his introduction. Overall, the process of disinflation seemed to be proceeding largely as expected, reflecting not only diminishing effects from exogenous factors that had been pushing inflation up, but also the impact of monetary policy. Headline inflation had evolved as projected, although growth had turned out to be weaker than expected, partly owing to a materialisation of downside risks. It was noted that the slowdown in economic activity was also reflecting the dampening effect of past interest rate increases. At the same time, comfort was drawn from the fact that forecast errors for inflation were close to zero and, if anything, the disinflation process was proceeding somewhat faster than expected. Overall, these developments were seen as creating confidence that this process would continue, bringing inflation back to target in a timely manner. It was cautioned, however, that most of the dampening effects from past interest rate increases on inflation had yet to materialise over the coming two years, for which uncertainty – stemming mainly from future wage dynamics, fiscal policy and geopolitical risks – was still high. If upside risks to inflation from these factors materialised, it would likely take some time before their effects on inflation became evident. Moreover, it was recalled that monetary policy faced challenges in addressing the effects of adverse supply shocks on inflation. Overall, it was maintained that, given the current outlook, it could be expected that the Governing Council would be able to bring inflation back to its 2% target by 2025. Although it was generally assumed that the "last mile" in bringing inflation back to target was the most difficult, it was argued that the Governing Council should be careful that its efforts to tame inflation did not eventually lead to an undershooting of the target.

Members agreed that most indicators of underlying inflation appeared to have passed their peak and continued to decline, a signal for which the Governing Council had been waiting for months. At the same time, domestic inflation was stubbornly high and longer-run inflation projections still seemed to be above the Governing Council's target.

Turning to the assessment of monetary policy transmission, members generally agreed that transmission was proceeding more strongly than had been anticipated in September. Moreover, a significant part of the interest rate pass-through was still pending and likely to restrain activity and inflation over the projection horizon. It was also pointed out that all successful disinflationary periods had required a prolonged period of rates in restrictive territory and weakening labour markets. At the same time, downside risks were highlighted that could strengthen transmission to economic activity and inflation even further.

In any case, it was stressed that there was no room for complacency, as the difficult part of the disinflation process was only starting. Inflation dynamics over the remainder of the year would likely be characterised by various base effects that could be misinterpreted as a reversal in the inflation trend and lead to market volatility, although the inflation uptick would be short-lived and would not change the overall disinflationary outlook. In this context, it was cautioned against declaring victory over inflation at the current stage, when inflation was still more than twice the ECB's target.

Overall, confidence was expressed in the progress made, although it was seen as important to maintain the restrictive stance for a sufficient time. With rates in restrictive territory, patience and persistence were needed to ensure that inflation converged towards the medium-term target in a timely manner. The Governing Council would assess incoming data as they arrived and act if needed.

Monetary policy decisions and communication

Against this background, all members agreed with the proposal by Mr Lane to maintain the three key ECB interest rates at their current levels. All three elements of the Governing Council's reaction function were considered to support the case for a "hold" in the hiking cycle, after ten consecutive increases in interest rates. Confidence was expressed that the current monetary policy stance was sufficiently restrictive, which gave the Governing Council the opportunity to keep rates at current levels and take time to assess the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission.

It was observed that markets were expecting policy rates to stay high for a longer period than predicted ahead of the Governing Council's September meeting. Expectations were moving from a hump-shaped interest rate path – one that macroeconomic models tended to prescribe as optimal – to a flatter profile with a later first cut in the deposit facility rate. It was deemed important for the Governing Council to avoid an unwarranted loosening of financial conditions. Moreover, members argued in favour of keeping the door open for a possible further rate hike, in keeping with the Governing Council's emphasis on data-dependence.

While the decision at the September meeting had been a close call, the interest rate hike in September had reinforced progress towards the price stability objective. Another important element had been the definition of the 2% inflation target that the Governing Council had introduced following its monetary policy strategy review in 2021. It was noted that throughout this inflation episode, market and survey-based indicators of medium-term inflation expectations had remained anchored at target.

Members agreed that the focus of the current meeting was communication rather than action. It was seen as necessary for the Governing Council to adapt its communication to the considerable uncertainty surrounding the evolving economic and inflation outlook during a phase in which the economy was slowing down. At the same time, it was argued that the Governing Council should strive for continuity and consistency and stick to its previous communication as closely as possible to avoid sending a message of complacency.

Members agreed that the Governing Council should continue to stress its determination to set policy rates, through its future decisions, at sufficiently restrictive levels for as long as necessary to bring inflation back to target in a timely manner. In view of the high uncertainty and the risk that further supply shocks could materialise, the Governing Council's data-dependent approach was also reaffirmed. Even if interest rates were left unchanged at the current meeting, the view was held that the Governing Council should be ready, on the basis of an ongoing assessment, for further interest rate hikes if necessary, even if this was not part of the current baseline scenario.

In conclusion, it was stressed that the Governing Council had to be both persistent and vigilant. Persistence was seen as essential to bring inflation back to 2% in the medium term. This was also meant to convey perseverance and patience in the face of new shocks that could materialise. Vigilance implied that, while the Governing Council had to assert the effectiveness of its measures and to acknowledge the progress that had been made, overconfidence and complacency had to be avoided in view of possible new challenges that could lie ahead until inflation was brought back to target.

Members also agreed with the Executive Board's proposal to continue applying flexibility in reinvesting redemptions falling due in the PEPP portfolio. There was broad agreement that continuity in PEPP reinvestments would be consistent with a decision to keep interest rates unchanged at the October meeting, while a discussion of an early termination of PEPP reinvestments at the current meeting was seen as premature.

Taking into account the foregoing discussion among the members, upon a proposal by the President, the Governing Council took the monetary policy decisions as set out in the monetary policy press release. The members of the Governing Council subsequently finalised the monetary policy statement, which the President and the Vice-President would, as usual, deliver at the press conference following the Governing Council meeting.

Monetary policy statement

Monetary policy statement for the press conference of 26 October 2023

Press release

Meeting of the ECB's Governing Council, 25-26 October 2023

Members

- Ms Lagarde, President

- Mr de Guindos, Vice-President

- Mr Centeno

- Mr Elderson

- Mr Hernández de Cos*

- Mr Herodotou*

- Mr Holzmann

- Mr Kazāks

- Mr Kažimír

- Mr Knot

- Mr Lane

- Mr Makhlouf*

- Mr Müller

- Mr Nagel

- Mr Panetta

- Mr Reinesch

- Ms Schnabel

- Mr Scicluna

- Mr Šimkus

- Mr Stournaras*

- Mr Välimäki, temporarily replacing Mr Rehn

- Mr Vasle

- Mr Villeroy de Galhau

- Mr Visco

- Mr Vujčić*

- Mr Wunsch

* Members not holding a voting right in October 2023 under Article 10.2 of the ESCB Statute.

Other attendees

- Ms Senkovic, Secretary, Director General Secretariat

- Mr Rostagno, Secretary for monetary policy, Director General Monetary Policy

- Mr Winkler, Deputy Secretary for monetary policy, Senior Adviser, DG Economics

Accompanying persons

- Ms Bénassy-Quéré

- Mr Dabušinskas

- Mr Demarco

- Mr Gavilán

- Mr Haber

- Mr Kaasik

- Mr Kroes

- Mr Koukoularides

- Mr Lünnemann

- Mr Madouros

- Mr Martin

- Mr Nicoletti Altimari

- Mr Novo

- Mr Pösö

- Mr Rutkaste

- Mr Šošić

- Mr Tavlas

- Mr Ulbrich

- Mr Vanackere

- Ms Žumer Šujica

Other ECB staff

- Mr Proissl, Director General Communications

- Mr Straub, Counsellor to the President

- Ms Rahmouni-Rousseau, Director General Market Operations

- Mr Arce, Director General Economics

- Mr Sousa, Deputy Director General Economics

Release of the next monetary policy account foreseen on 18 January 2024.

Nikkei 225: Bulls Undeterred by Japanese Government Economic Downgrade

- Recent price actions of the Nikkei 225 are still trading above its 20-day moving average despite the latest official downbeat assessment of Japan’s economy.

- Significant correlation flip between USD/JPY and Nikkei 225 may persist as a weaker JPY may not be a main driver to drive up the price actions of Nikkei 225.

- A strengthening JPY may see the outperformance of consumer-oriented TOPIX equities sectors such as Retail Sales and IT & Services.

- A new medium-term uptrend may have kickstarted in Nikkei 225, watch the 32,090 key medium-term support.

Japan’s government on this Wednesday, 22 November downgraded its assessment for the first time in ten months, citing economic growth in Japan has recovered moderately but appeared to be pausing due to weak domestic demand.

The benchmark Nikkei 225 has continued to trade above its upward-sloping 20-day moving average since the start of this month, November, and rallied by +11% from its key swing low area of 30,530 printed on 4 and 24 October 2024.

The latest official downbeat economic assessment has not derailed the current bullish tone of the Nikkei 225 as it has managed to remain above the “gapped up” support of 32,820 formed on last Wednesday, 15 November; the effect in a global risk-on herding behaviour reinforced by the softer than expected US CPI print for October that was released on last Tuesday, 14 November (current level of Nikkei 225 is at 33,452 as of 22 November).

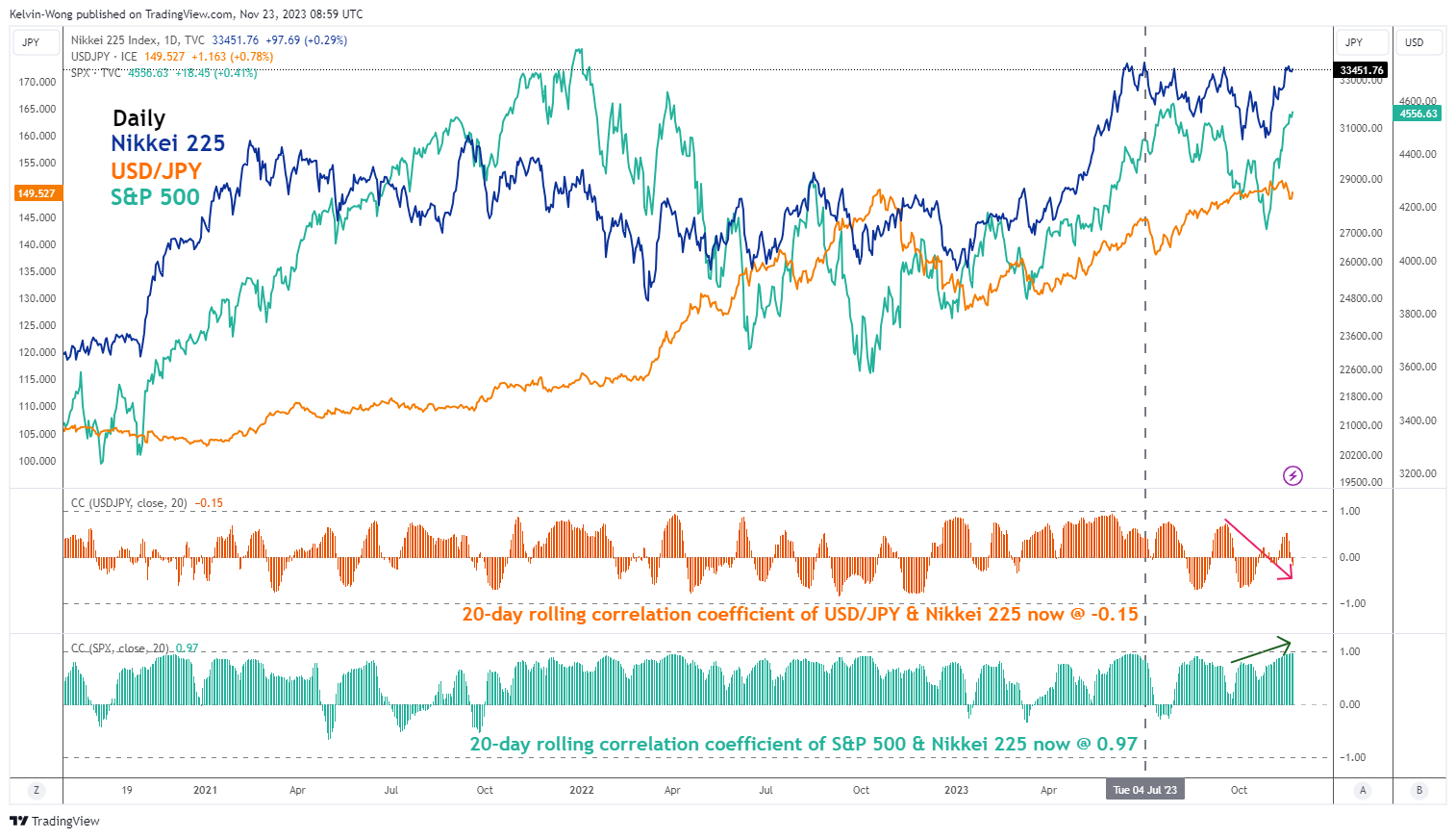

Significant correlation flip between Nikkei 225 & USD/JPY

Fig 1: Correlation trends between Nikkei 225, USD/JPY & S&P 500 as of 22 Nov 2023 (Source: TradingView, click to enlarge chart)

Interestingly, the previous long-term traditional high direct correlation between the movements of the Nikkei and USD/JPY has broken down based on its latest 20-day rolling correlation coefficient reading of -0.15.

From a fundamental standpoint, a persistently weaker JPY (where the JPY has depreciated by as much as 15.9% against the US dollar since the start of 2023) is likely to have a more detrimental effect now on Japan’s economy due to the risk of higher imported inflation which in turn drives up imported energy costs for resources-scare Japan.

Moreover, oil prices are likely to remain sticky on the upside in the medium term as OPEC+ leading member, Saudi Arabia seems to be still in favour of extending current oil supply cuts into 2024.

Therefore, a stronger JPY is much needed for Japan at this juncture to negate the risk of elevated imported inflation that can dent business and consumer confidence which in turn dampens internal domestic spending. Hence, this latest narrative explains the current “correlation flip” between USD/JPY and Nikkei 225.

Consumer-oriented TOPIX equities sectors may benefit from a stronger JPY

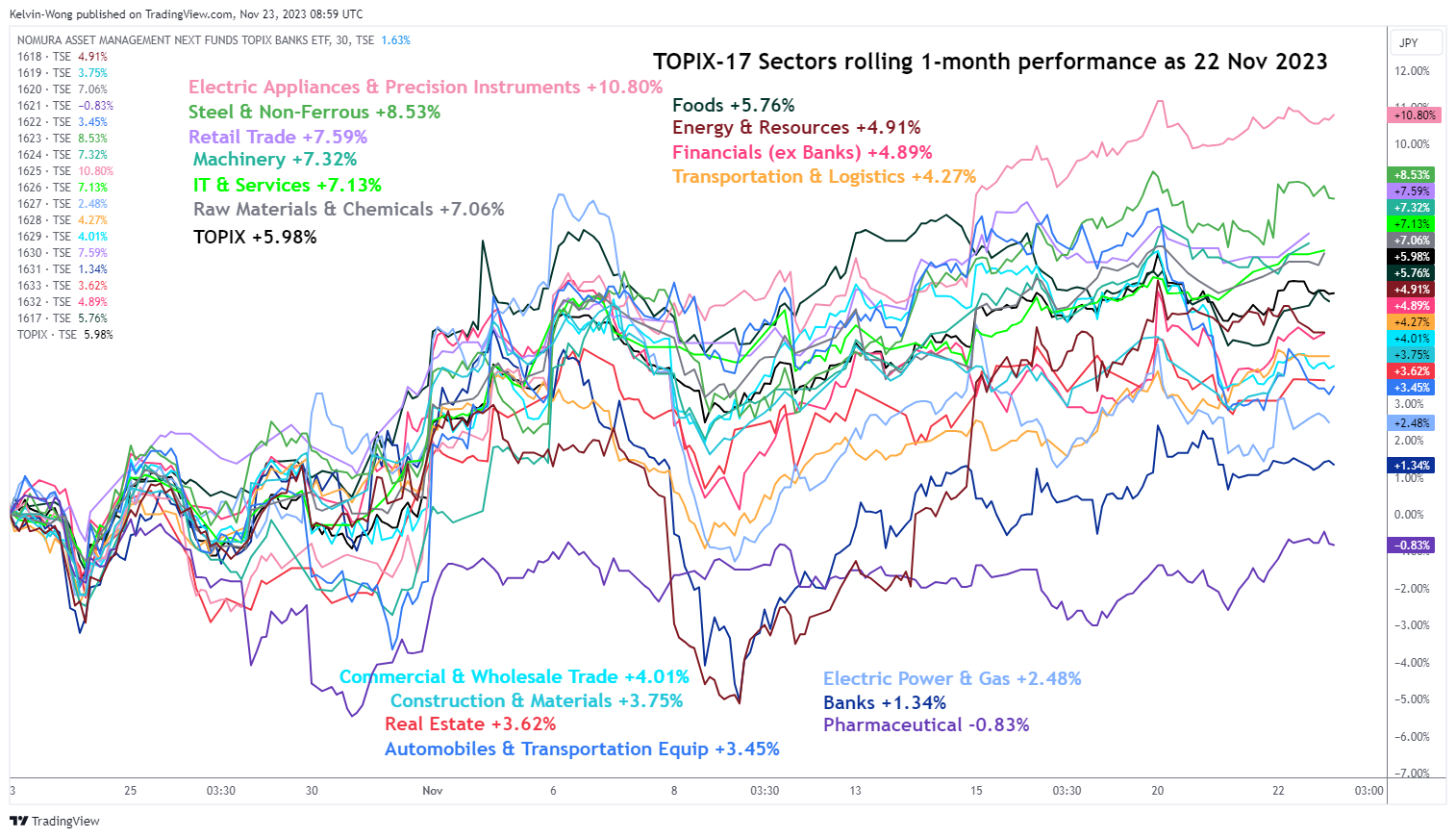

Fig 2: 1-month rolling performance of the 17 TOPIX sectors as of 22 Nov 2023 (Source: TradingView, click to enlarge chart)

In the past week, the JPY has started to strengthen against the US dollar driven by more of an increasing expectation of a dovish tilt from the US Federal Reserve rather than a hawkish Bank of Japan’s modus operandi.

The JPY has been appreciated by as much as around +3% against the US dollar since last Monday, 13 November and it has started to translate to an uptick in bullish sentiment seen in the Japanese equities sectors that are tied to business and consumer confidence and domestic spending.

Based on the one-month rolling performance of the 17 TOPIX sectors as of 22 November 2023, Retail Trade (+7.59%) and IT & Services (+7.13%) have started to show outperformance against the broader TOPIX index (+5.98%).

Potential start of new medium-term uptrend for Nikkei 225

Fig 3: Nikkei 225 medium-term trend as of 22 Nov 2023 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the recent bullish momentum seen in the Japanese stock market is likely to trigger the potential start of a medium-term (multi-week to multi-month) uptrend phase in the Nikkei 225 after the -9.5% corrective decline seen from 16 June to 24 October 2023.

The current price action of the Nikkei 225 as of 22 November is retesting a 33-year swing high of 33,770 after an initial pull-back seen on Monday to Tuesday.

Meanwhile, the daily RSI momentum indicator has continued to exhibit positive momentum readings after its earlier bullish momentum breakout and retest on 7 November 2023.